Sample Category Title

WTI in Focus with US-Iran Talks Cancelled – US Oil Outlook

- Oil rallies to $65 from the latest new: Iran-US talks cancelled.

- WTI lost some ground after talks were announced but tensions are coming back.

- Exploring an in-depth Technical Analysis of the commodity.

WTI Oil is facing renewed volatility following the latest geopolitical developments:

US–Iran talks scheduled for Friday in Turkey have been cancelled.

Disagreements had emerged between Iranian and US demands. Washington continued to insist on Iran abandoning its ballistic missile program, while Tehran only signaled openness on the nuclear issue.

Markets had initially rallied on the prospect of talks, while oil shed much of its geopolitical premium after the weekend break, gapping lower from $66.00 to $61.50.

But in the current environment, it was unlikely to remain that simple for long.

Iranian officials have reiterated that they remain open to discussions, yet the US now appears to be weighing its options, including preparations for potential intervention.

The core debate centers on whether an intervention could realistically lead to regime change and how escalation might be avoided to prevent a prolonged conflict.

Since the cancellation headline, WTI has jumped back toward $65 and is holding near its relative highs as traders brace for a possible worsening of the conflict.

Odds for a US strike in Iran – Source: Polymarket. February 4, 2026

Polymarket-based odds for a strike before February 28 are just below 30%.

Let's dive into a bottom-up multi-timeframe analysis of WTI (US) Oil to determine whether technicals point to continued upside or if we are reaching a maximum.

We will commence with intraday charts to explore the latest action and see how it develops to Daily charts.

US Oil Bottom-Up Multi-Timeframe Analysis

1H Chart

WTI Oil 1H Chart – February 4, 2026. Source: TradingView

Oil just bounced higher by 3% on the headlines but got rejected right in the middle of its $65 to $66 Key resistance.

Despite the rejection, bears aren't for now able to bring back the commodity to the pre-headline levels so the current pullback just looks like profit-taking.

Some warning signs are arising however with the formation of an inverted Head & Shoulders pattern which could hint to $70 in WTI (see more on the 4H chart just below)

As long as the tensions don't aggravate, expect a $63 to $66 range.

Any close above $66 will be accompanied with some war headlines (particularly if the past week's $66.56 highs break).

WTI 4H Chart and Technical Levels

WTI Oil 4H Chart – February 4, 2026. Source: TradingView

It is difficult to discern momentum in Oil when up and down spikes are so common.

Two things are clear from that timeframe:

- WTI bulls are following closely the 4H 50-period MA to push prices higher

- The action is holding within an upward channel, but any news could lead to an upside breakout

The measured move target from the inverted Head & shoulders is shown in purple.

WTI Technical Levels

Levels to place on your WTI charts:

Resistance Levels

- Past week Spike $66.56

- Minor Resistance $65 to $66 (daily highs $65.55)

- September 2025 Major resistance $67 (could get breached if US attacks)

- Psychological Resistance $70 and Inverted H&S target

- $78.43 12-Day War highs

Support Levels

- $64.00 Key psychological support

- $63.00 4H-50 MA

- May 2025 range Key Pivot $62.30 to $63.43

- May Range lows support $59 to $60.5 Major support

- Iran Premium Support area $58.50 to $59

WTI Daily Chart

WTI Oil Daily Chart – February 4, 2026. Source: TradingView

Now trading well above its 200-Day Moving Average, Oil is turning increasingly bullish.

Fundamental factors over greener energy are still weighing on the long-run trajectory for the commodity, but geopolitical factors say otherwise.

Trader are pushing the commodity towards the 50% retracement of the 12-Day War from June 2025.

Any close above $66.60 would look at high-paced continuation. This would of course be contingent on tensions remaining elevated.

Eco Data 2/5/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Dec | 3.37B | 3.45B | 2.94B | 2.60B |

| 07:00 | EUR | Germany Factory Orders M/M Dec | 7.80% | -1.30% | 5.60% | 5.70% |

| 07:45 | EUR | France Industrial Output M/M Dec | -0.70% | 0.10% | -0.10% | 0.10% |

| 09:30 | GBP | Construction PMI Jan | 46.4 | 42 | 40.1 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -0.50% | -0.20% | 0.20% | |

| 12:00 | GBP | BoE Interest Rate Decision | 3.75% | 3.75% | 3.75% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--4--5 | 0--2--7 | 0--5--4 | |

| 13:15 | EUR | ECB Main Refinancing Rate | 2.15% | 2.15% | 2.15% | |

| 13:15 | EUR | ECB Rate On Deposit Facility | 2.00% | 2.00% | 2.00% | |

| 13:30 | USD | Initial Jobless Claims (Jan 30) | 231K | 210K | 209K | |

| 13:45 | EUR | ECB Press Conference | ||||

| 15:30 | USD | Natural Gas Storage (Jan 30) | -360B | -379B | -242B |

| 00:30 | AUD |

| Trade Balance (AUD) Dec | |

| Actual | 3.37B |

| Consensus | 3.45B |

| Previous | 2.94B |

| Revised | 2.60B |

| 07:00 | EUR |

| Germany Factory Orders M/M Dec | |

| Actual | 7.80% |

| Consensus | -1.30% |

| Previous | 5.60% |

| Revised | 5.70% |

| 07:45 | EUR |

| France Industrial Output M/M Dec | |

| Actual | -0.70% |

| Consensus | 0.10% |

| Previous | -0.10% |

| Revised | 0.10% |

| 09:30 | GBP |

| Construction PMI Jan | |

| Actual | 46.4 |

| Consensus | 42 |

| Previous | 40.1 |

| 10:00 | EUR |

| Eurozone Retail Sales M/M Dec | |

| Actual | -0.50% |

| Consensus | -0.20% |

| Previous | 0.20% |

| 12:00 | GBP |

| BoE Interest Rate Decision | |

| Actual | 3.75% |

| Consensus | 3.75% |

| Previous | 3.75% |

| 12:00 | GBP |

| MPC Official Bank Rate Votes | |

| Actual | 0--4--5 |

| Consensus | 0--2--7 |

| Previous | 0--5--4 |

| 13:15 | EUR |

| ECB Main Refinancing Rate | |

| Actual | 2.15% |

| Consensus | 2.15% |

| Previous | 2.15% |

| 13:15 | EUR |

| ECB Rate On Deposit Facility | |

| Actual | 2.00% |

| Consensus | 2.00% |

| Previous | 2.00% |

| 13:30 | USD |

| Initial Jobless Claims (Jan 30) | |

| Actual | 231K |

| Consensus | 210K |

| Previous | 209K |

| 13:45 | EUR |

| ECB Press Conference | |

| Actual | |

| Consensus | |

| Previous | |

| 15:30 | USD |

| Natural Gas Storage (Jan 30) | |

| Actual | -360B |

| Consensus | -379B |

| Previous | -242B |

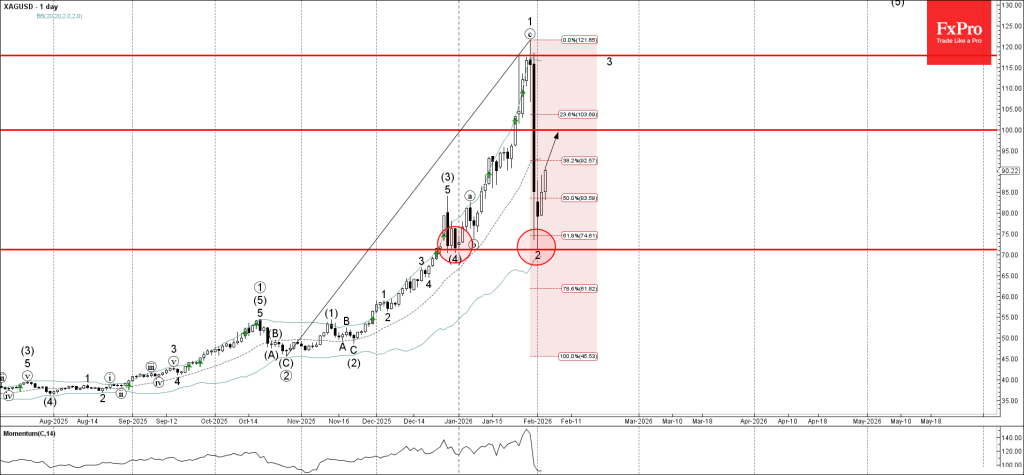

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver rising inside impulse wave 3

- Likely to test resistance level 100.00

Silver recently reversed up from the support zone between the support level 71.25 (which stopped wave (4) at the end of December), lower daily Bollinger Band and the 61.8% Fibonacci correction of the previous upward impulse from October.

The upward reversal from this support area created the daily Japanese candlesticks reversal patterns long-legged Doji, which stopped the previous sharp downward correction 2.

Given the overriding daily uptrend, Silver can be expected to rise toward the next round resistance level 100.00.

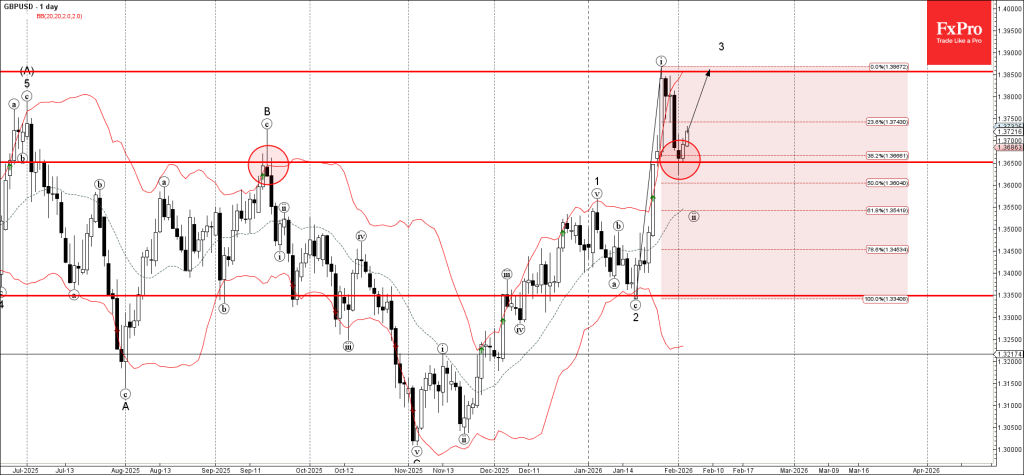

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD reversed from support area

- Likely to rise to resistance level 1.3850

GBPUSD currency pair recently reversed up from the support area located between the key support level 1.3650 (former resistance from September) and the 38.2% Fibonacci correction of the previous sharp upward impulse from January.

The upward reversal from this support area created the daily Japanese candlesticks reversal patterns Bullish Engulfing.

Given the bearish US dollar sentiment seen today, GBPUSD currency pair can be expected to rise toward the next resistance level 1.3850.

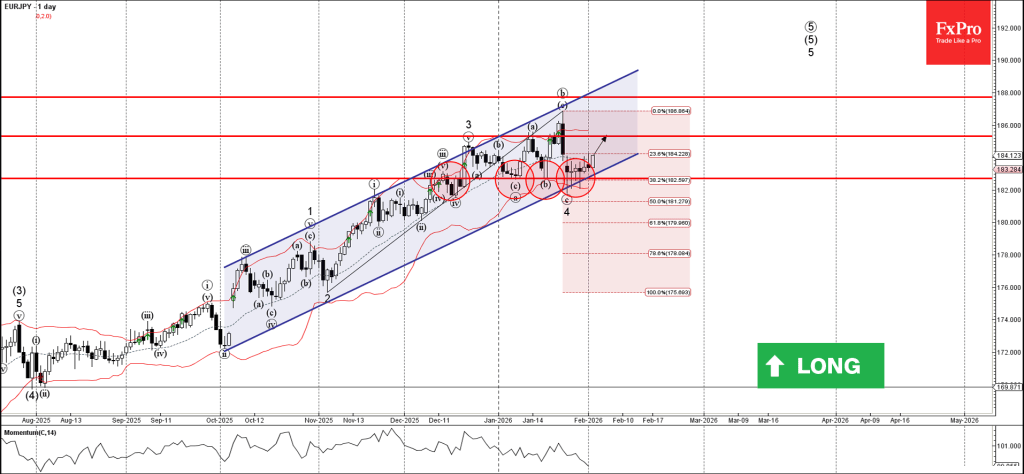

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY reversed from support area

- Likely to rise to resistance level 185.30

EURJPY currency pair recently reversed up from the support area located between the pivotal support level 182.70 (which has been reversing the pair from the start of this year) and the support trendline of the wide daily up channel from October.

The pair made multiple Japanese candlesticks reversal patterns Doji near the support level 182.70 – signalling the strength of this support level.

Given the strong daily uptrend, EURJPY currency pair can be expected to rise in the active impulse wave 5 toward the next resistance level 185.30.

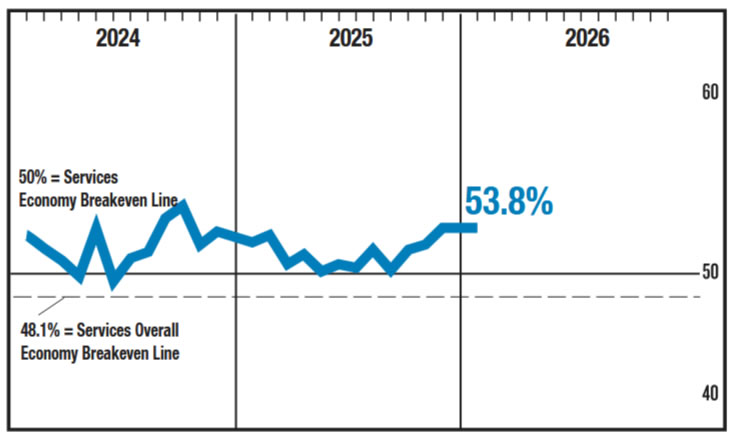

ISM Services Steady in January Despite Large Drop in Export Orders

The ISM Services index held steady in January at 53.8. This is the fourth consecutive month of expansion. Eleven industries out of 18 reported expansion, the same as last month.

The supplies delivery index moved deeper into in expansionary territory in January, marking the 14th consecutive month it has been in expansion. It increased 2.4 points to 54.2, indicating slower deliveries, which is expected when customer demand is increasing.

New Orders gave back some of its gains after a large increase last month, falling 3.4 points but remaining in expansionary territory at 53.1. The business activity posted its highest reading since October 2024, a sign of higher activity.

New export orders showed a large decline, falling to 45.0 from 54.2 in the month prior.

The prices index increased by 1.5 points to 65.1, indicating that price pressures are still prevalent. The employment index managed to remain in expansionary territory, falling to 50.3 from 51.7.

Key Implications

This report affirms that demand in the service sector remains reasonably strong, as we can see in the relatively strong performance of the new orders and business activity sub-indexes. The combination of expanding activity and slower supplier deliveries does raise the specter of price increases. We will get a more direct read on this in next week's CPI release, but the trend of steady employment growth, increasing demand, and increasing price pressures amplify the risk that rates take longer to come down again.

The biggest change in the details of this report is the outsized drop in the new export orders index, which plummeted 9.2 points into contractionary territory and to its lowest reading since March 2023. Respondents indicated that both tariffs and travel restrictions are significantly impacting export orders. Despite the large decrease in the index, only seven industries reported a decrease, meaning that this may not be the bottom for export orders if trade uncertainty continues. There is still the risk that this could spread to the other 11 industries, with the potential to further drag down service activity as a whole.

US ISM services unchanged at 53.8, points to 1.8% annualized GDP growth

US ISM Services PMI was unchanged at 53.8 in January, matching expectations and marking a second consecutive month at the highest level since October 2024. The steady headline reading points to continued resilience in the services sector, which remains a key pillar of overall economic momentum.

Beneath the surface, the details were mixed. Business activity strengthened notably, with the production index rising from 55.2 to 57.4. However, new orders eased back to 53.1 from 56.5. Employment index slipped closer to stagnation at 50.3, down from 51.7. Inflation signals firmed. The prices index climbed sharply from 65.1 to 66.6, highlighting renewed cost pressures in the services sector. Even so, all four major subcomponents remained in expansion territory for a second month.

Based on the historical relationship tracked by the Institute for Supply Management, the January PMI reading is consistent with roughly 1.8 percentage points of annualized real GDP growth.

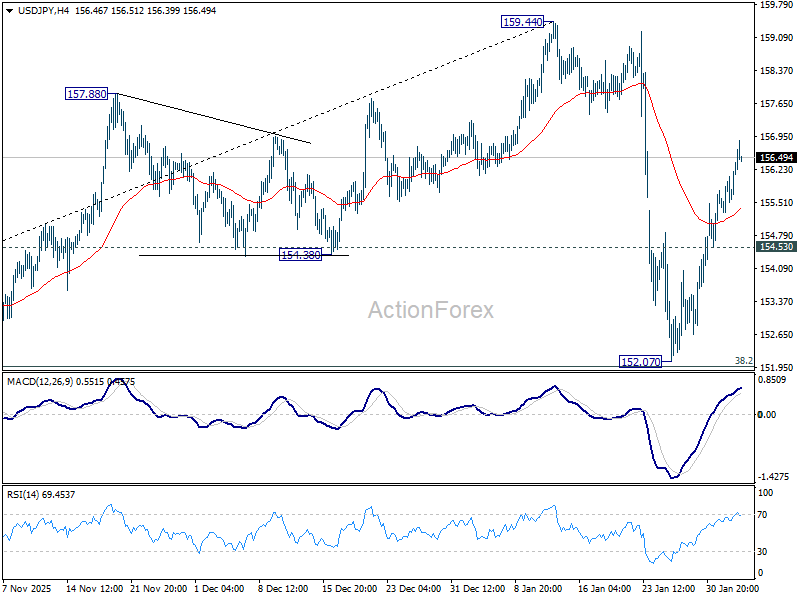

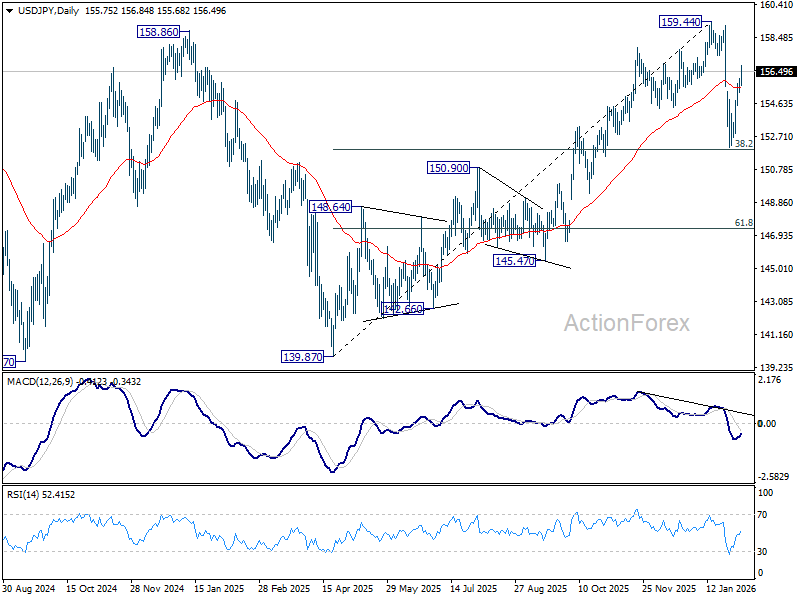

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.35; (P) 155.72; (R1) 156.13; More...

No change in USD/JPY's outlook and intraday bias stays on the upside. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 154.53 minor support will turn intraday bias neutral first. Sustained break of 38.2% retracement of 139.87 to 159.44 at 151.96 will argue that it is reversing whole rise from 139.87.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

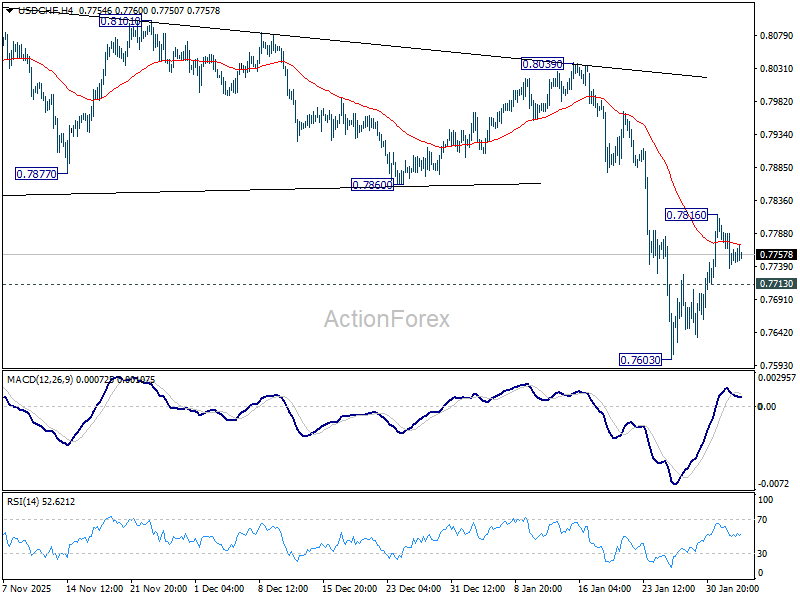

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7726; (P) 0.7765; (R1) 0.7791; More….

Intraday bias in USD/CHF stays neutral at this point. Above 0.7816 will resume the rebound from 0.7603 short term bottom to 55 D EMA (now at 0.7905). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.

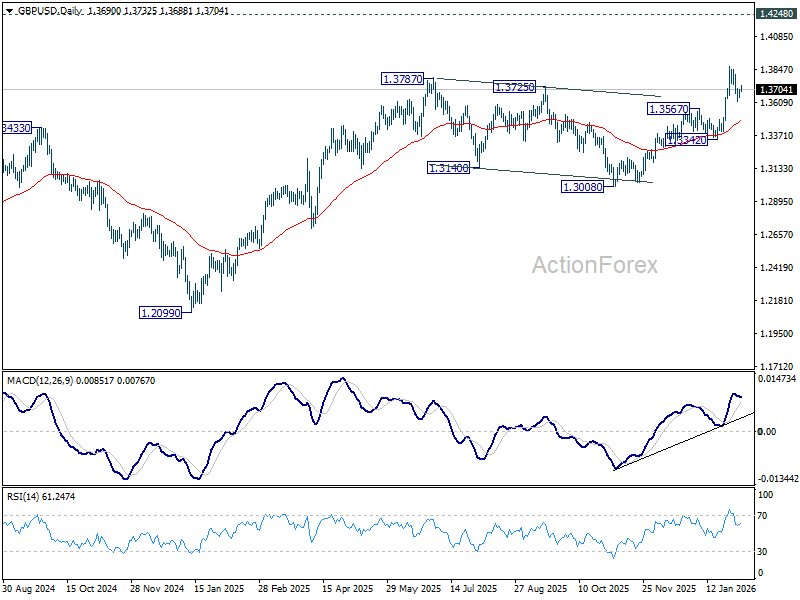

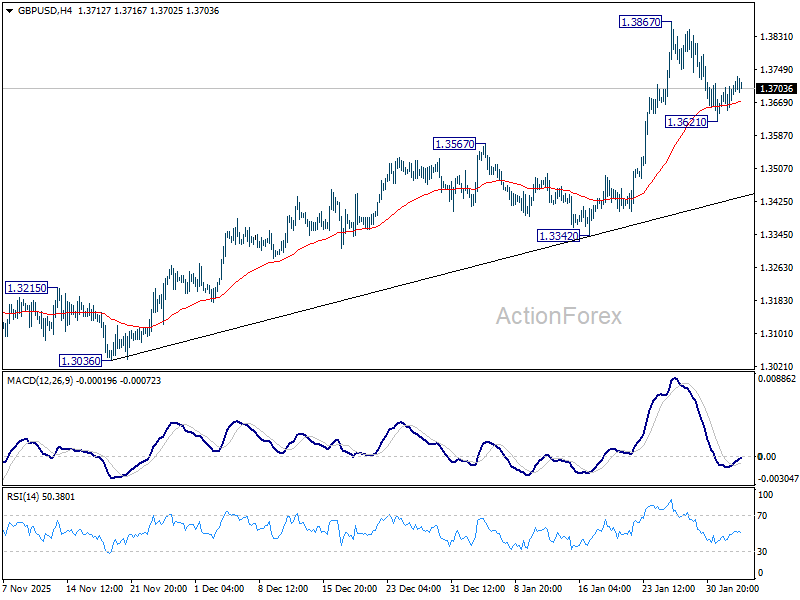

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3664; (P) 1.3686; (R1) 1.3720; More...

Intraday bias in GBP/USD remains neutral for the moment. Below 1.3621 will extend the pullback from 1.3867 short term top to 55 D EMA (now at 1.3471). On the upside, firm break of 1.3867 will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.