Sample Category Title

RBA Raises Cash Rate to 3.85%, Warning Inflation Will Remain Above Target for Some Time

RBA lifts cash rate 0.25ppt to 3.85% as expected, citing higher inflation and stronger growth in private sector demand.

- RBA Monetary Policy Board (MPB) raised the cash rate by 0.25ppts to 3.85% as forecast, citing renewed inflationary pressures coming from a faster recovery in private sector demand than expected. It assesses that the labour market remains a little tight, even though several standard indicators are moving in the easing direction.

- The RBA also published revised forecasts in its Statement on Monetary Policy (SMP). Growth is forecast to be stronger in the near term, and so is inflation. The upgrade to the inflation forecasts were large, and imply quarterly outcomes for trimmed mean inflation of around 0.9%qtr for the next two quarters before reverting to a more moderate 0.7%qtr track. At 3.2%, annual trimmed mean inflation is still forecast to be above target at end-2026.

- Beyond the middle of this year, the temporary elements in inflation are expected to unwind, and restrictive monetary policy to take hold. This will dampen inflation and allow it to return close to the mid-point of the 2–3% target range by the end of the forecast horizon in mid 2028. Also weighing on the inflation forecast would be the significant exchange rate appreciation since the last forecast round, though the RBA downplayed this.

- The Governor expressed some discomfort with the inflation profile still being above the 2.5% at the end of the forecast horizon. The July 2025 Statement on the Conduct of Monetary Policy states that when inflation is expected to be significantly away from the midpoint of the 2–3% target the Board will communicate how long it expects it will be before it again meets its objectives and why.

- The post-meeting statement was non-committal on whether further increases in the cash rate are needed, but the shape of the revised forecasts suggests that staff believe it is likely they will be. Given the feedback loop between inflation surprises and RBA assessments of supply, however, we believe it will pay to be more circumspect and do not expect a follow-up hike in March. But the MPB has set a low bar for further hikes and, should the RBA’s inflation forecast for March quarter be validated (which is highly plausible given our own view is only a little below this), it is likely to hike again in May.

As was widely expected, the RBA MPB raised the cash rate 0.25ppts to 3.85% at its February meeting. The recent run of underlying inflation data had been too strong for the MPB to look past, especially given that growth in private sector demand was stronger than expected, and the prior gradual easing in the labour market seemed to have paused or even ceased coming into year-end.

The RBA’s near-term forecasts for inflation have been upgraded noticeably, reflecting this assessment. While the RBA assesses that the bulk of the recent lift in inflation has reflected temporary factors (including some premature margin rebuilding on the back of stronger consumer spending that might not be sustained), some of it is seen as reflecting capacity pressures being tighter in late 2025 than previously assumed.

Over time, the RBA forecasts imply that the temporary component to the recent lift in inflation will unwind. In addition, tight policy will eventually take hold and bring inflation back down towards the midpoint of the 2–3% target range. The end-point of the forecasts at June 2028 show trimmed mean inflation at 2.6%. This implies that the RBA believes that the path for interest rates assumed in the forecasts delivers tight policy.

Since the previous forecast round in November, the exchange rate has also lifted noticeably. All else equal, this should dampen inflation further out, along with the tighter stance of policy. As an aside, we note that in the post-meeting media conference the Governor attributed most of this to a reaction to the shifting outlook for domestic interest rates. The SMP’s coverage of the sell-off in the USD was brief and did not discuss how this feeds through into the trade-weighted index also through its large weight on the Chinese currency. We think this underweights the disinflationary role the exchange rate could play in coming quarters.

In delivering tight policy, though, the RBA is forecasting a sustained period of soggy growth beyond the near term. GDP growth is expected to be below even the RBA’s pessimistic view of trend growth in supply capacity of around 2%. The unemployment rate is rising at the end-point of the forecast horizon, leading us to wonder if an extension of the forecast period would show inflation falling below the mid-point. This supports our view that, while the cash rate might be rising now, reductions can be expected in late 2027 or early 2028.

The RBA believes that the labour market is still on the tight side of full employment and did not ease further in recent months. While this is similar to our own assessment, we think the RBA is putting a lot of weight on the representativeness of some business surveys. Of the 15 indicators in the RBA’s standard suite for assessing labour market tightness, 11 eased and only 4 tightened, including two from business surveys.

The RBA assesses that supply capacity constraints are contributing to higher inflation, and that supply capacity was probably lower than previously believed. We have previously noted our scepticism about this assessment, given that the RBA’s assessments of trend productivity growth, population growth and (to an extent) trends in the participation rate are all systematically too pessimistic. We note that the discussion in the SMP attempts to show that productivity growth is low (and unit labour cost growth high) by comparing with a long-term trend that includes the late 1990s tech boom, a time when productivity growth ran at more than 2%yr and outstripped the rate in the United States. Excluding the mining sector, productivity growth is running at around 1%yr. The comparison in the SMP of the RBA’s assessment of the output gap with that of the OECD highlights just how consequential the judgement between cyclical and trend productivity growth can be.

The emphasis on supply capacity and the way assessments of it get revised in response to inflation surprises raise a deeper issue: every time the RBA is surprised by high inflation outcomes, it concludes that supply capacity must have been lower in the moment than it previously thought. While the RBA claims that it does not knee-jerk react to past inflation, this approach to analysis of supply capacity induces an indirect feedback loop from recent inflation surprises to its forecasts. By way of example, the recent data surprises have induced the RBA’s models to point to a lift in the NAIRU, the unemployment rate consistent with stable inflation. This then induces more assumed inflationary pressure from any given forecast profile for growth and employment.

In the post-meeting media conference, the Governor again highlighted the role of the Productivity Commission as the centre of excellence in identifying ways to lift productivity. While there are clearly policy levers that can be pulled, this puts all the onus on a policy-oriented view of how productivity growth occurs. Not enough attention is given to the role of capital accumulation or private-sector innovation more generally. The weak outlook for both dwelling and business investment in the RBA’s refreshed SMP forecasts provide no grounds for optimism on this front.

As is usual, Governor Bullock declined to provide any forward guidance on the future path of interest rates from here. Given that the forecasts imply higher inflation than the RBA is comfortable with even after raising rates, further rate hikes are clearly a possibility. However, we think the MPB will wait for another quarter inflation print to assess if things are playing out as expected. The low bar for further hikes means that, absent a downside surprise in the March quarter inflation outcome, the MPB is likely to hike again in May.

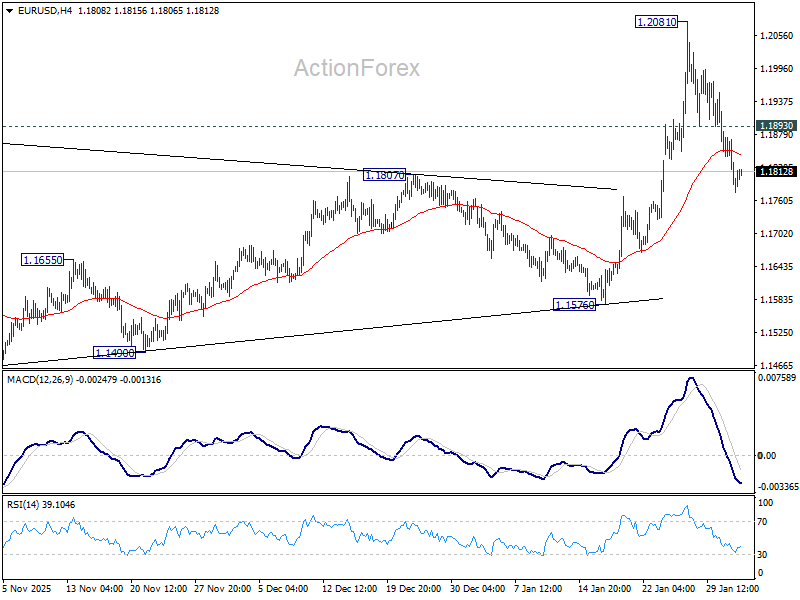

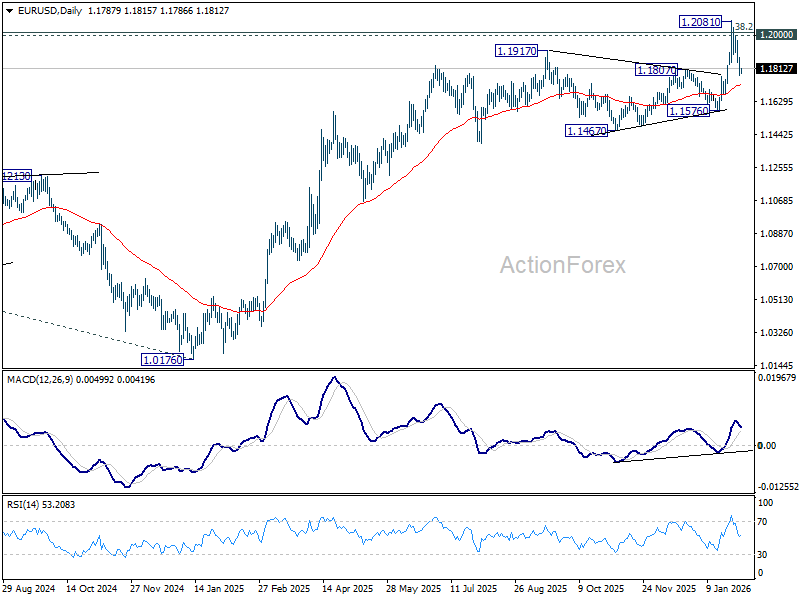

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1752; (P) 1.1814; (R1) 1.1851; More….

Intraday bias in EUR/USD remains mildly on the downside at this point. Fall from 1.2081 short term top would target 55 D EMA (now at 1.1721). Firm break there will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support. On the upside, above 1.1893 minor resistance will turn bias neutral. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1458) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

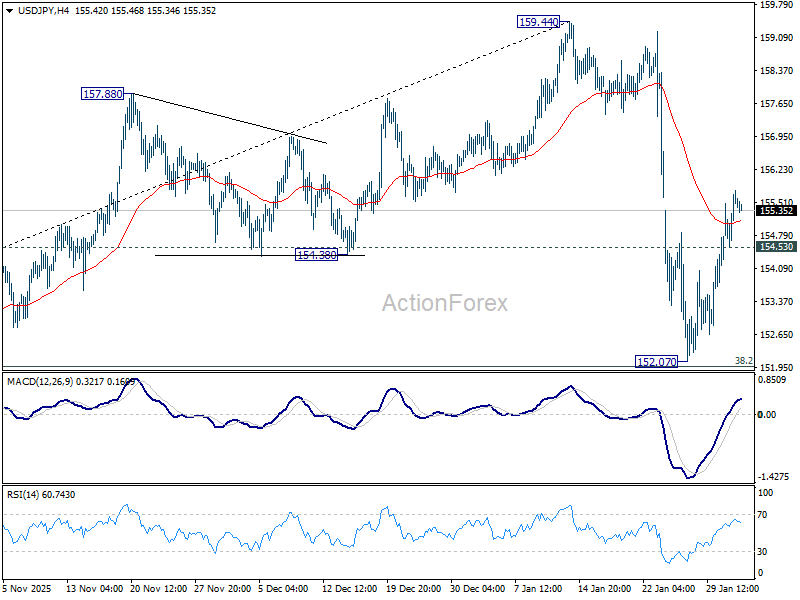

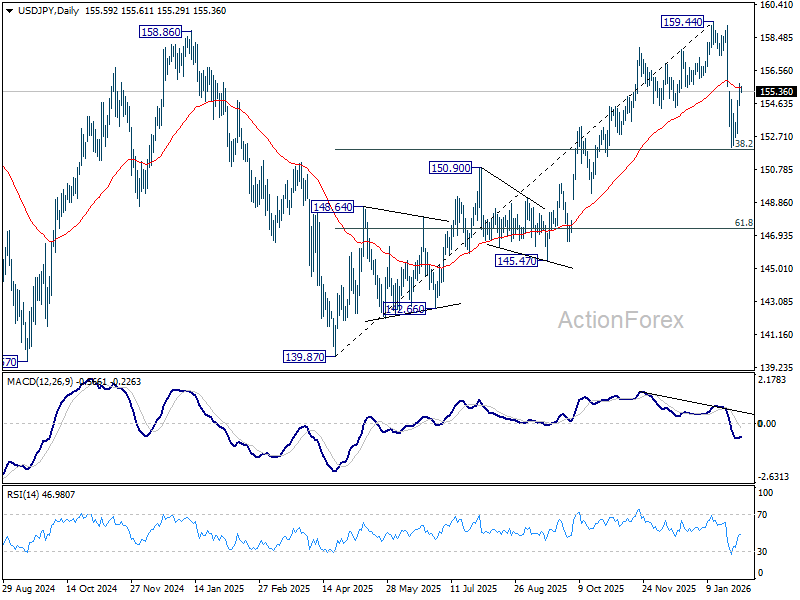

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.84; (P) 155.32; (R1) 156.08; More...

Intraday bias in USD/JPY remains mildly on the upside at this point. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 154.53 minor support will turn intraday bias neutral first. Sustained break of 38.2% retracement of 139.87 to 159.44 at 151.96 will argue that it is reversing whole rise from 139.87.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

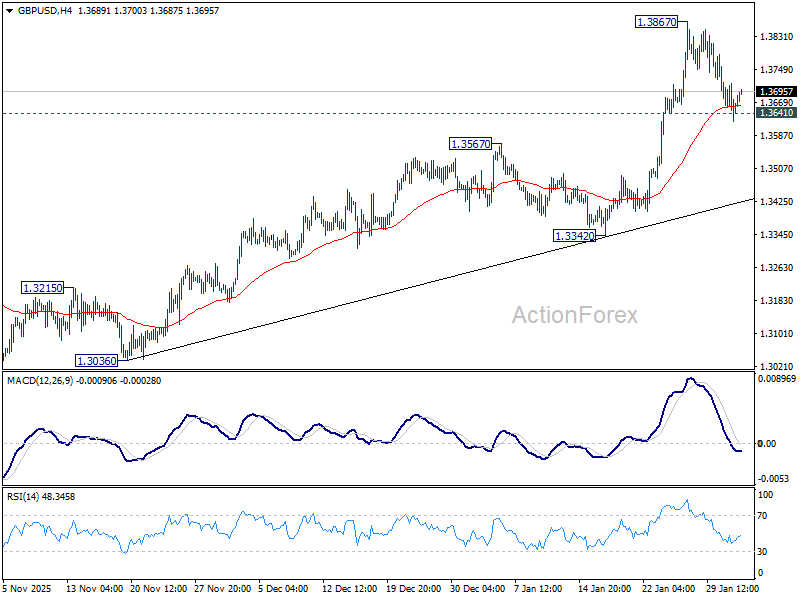

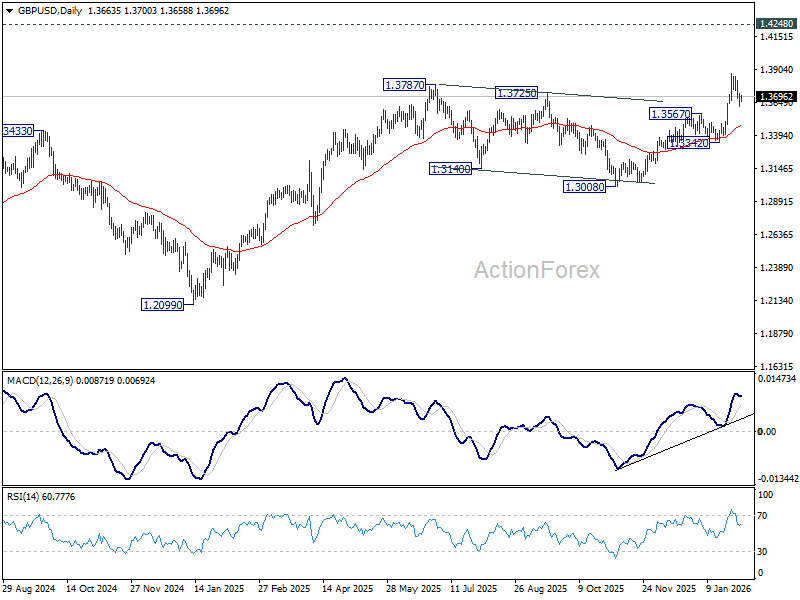

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3622; (P) 1.3668; (R1) 1.3714; More...

Breach of 1.3641 minor support suggests short term topping at 1.3867. Intraday bias is mildly on the downside for deeper pullback to 55 D EMA (now at 1.3471). On the upside, firm break of 1.3867 will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7777; (R1) 0.7839; More….

Breach of 0.7792 resistance suggests short term bottoming at 0.7603 in USD/CHF. Intraday bias is mildly on the upside for stronger rebound to 55 D EMA (now at 0.7912). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.

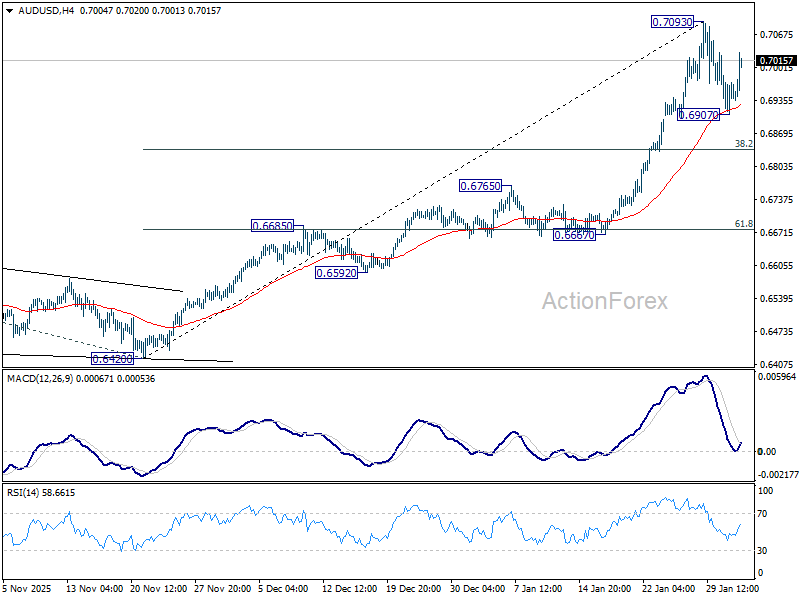

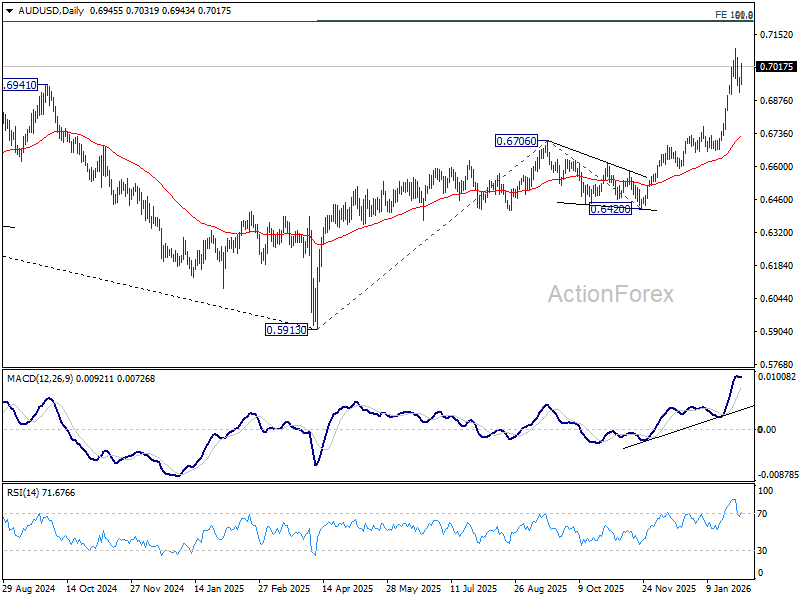

AUD/USD Daily Report

Daily Pivots: (S1) 0.6914; (P) 0.6942; (R1) 0.6976; More...

AUD/USD recovered after drawing support from 55 4H EMA, but stays below 0.7093 temporary top. Intraday bias remains neutral and further rise is expected. Above 0.7093 will extend larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. However, break of 0.6907 will bring lengthier consolidations before rally resumption. Deeper pullback would then be seen to 38.2% retracement of 0.6420 to 0.7093 at 0.6836.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

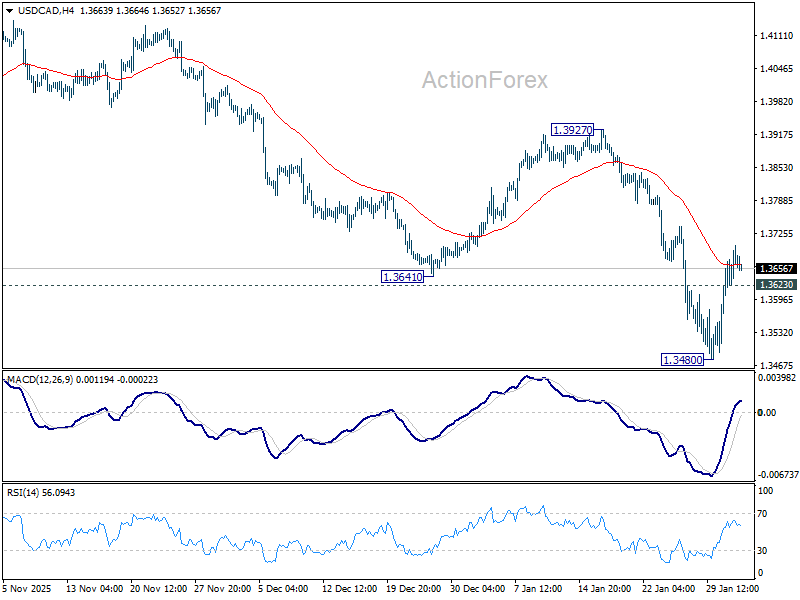

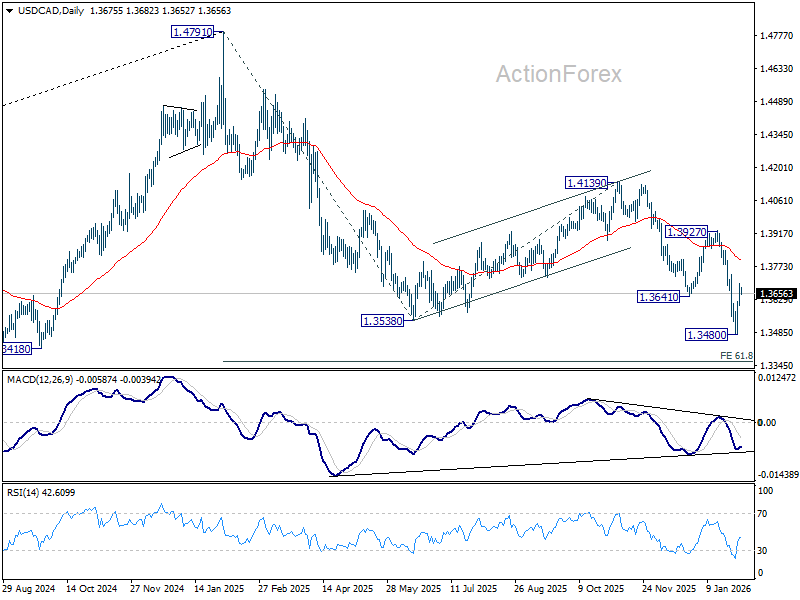

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3623; (P) 1.3663; (R1) 1.3721; More...

Breach of 55 4H EMA (now at 1.3663) suggests short term bottoming at 1.3480. Intraday bias is mildly on the upside for stronger rebound to 55 D EMA (now at 1.3800). On the downside, below 1.3623 minor support will bring retest of 1.3480 low. Firm break there will resume larger fall to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

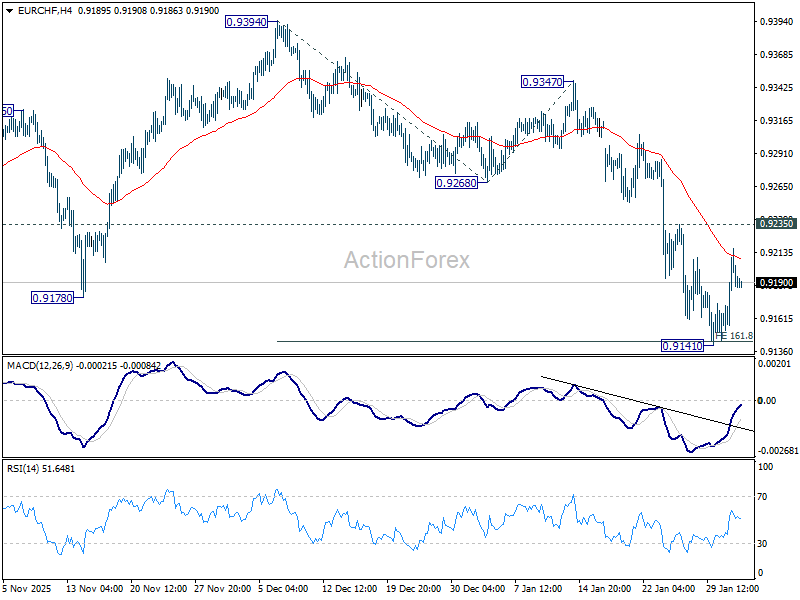

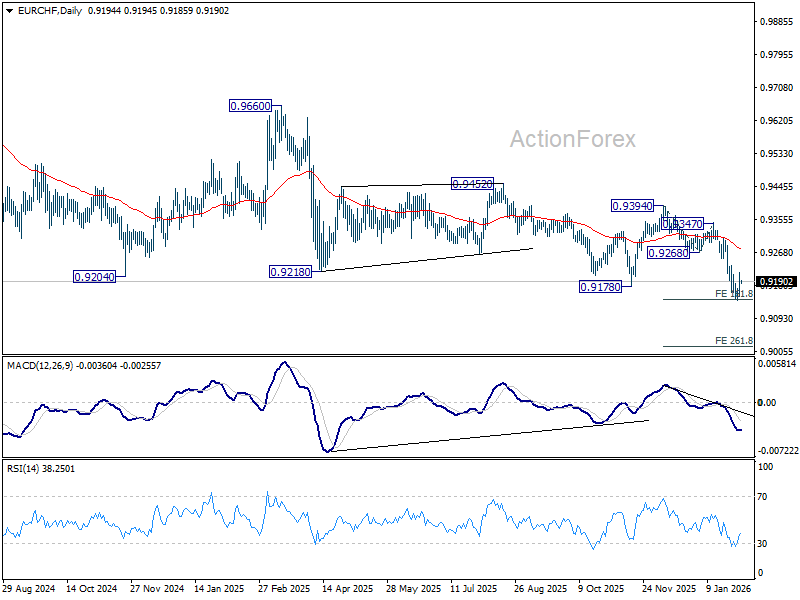

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9159; (P) 0.9188; (R1) 0.9223; More....

Intraday bias in EUR/CHF remains neutral first and more consolidations could be seen above 0.9141. Upside of recovery should be limited by 0.9235 to bring another fall. Decisive break of 0.9141 will extend larger down trend to 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, firm break of 0..9235 resistance will suggest short term bottoming and bring stronger rebound to 55 D EMA (now at 0.9275).

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

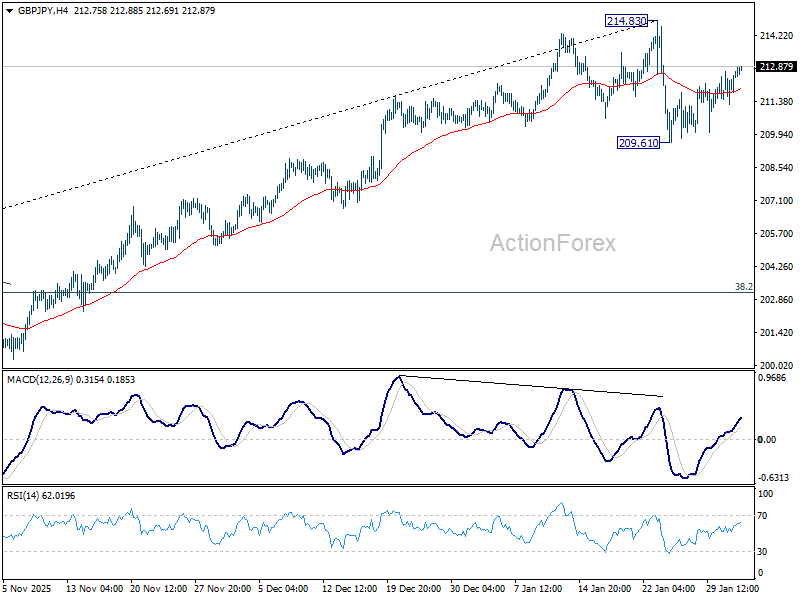

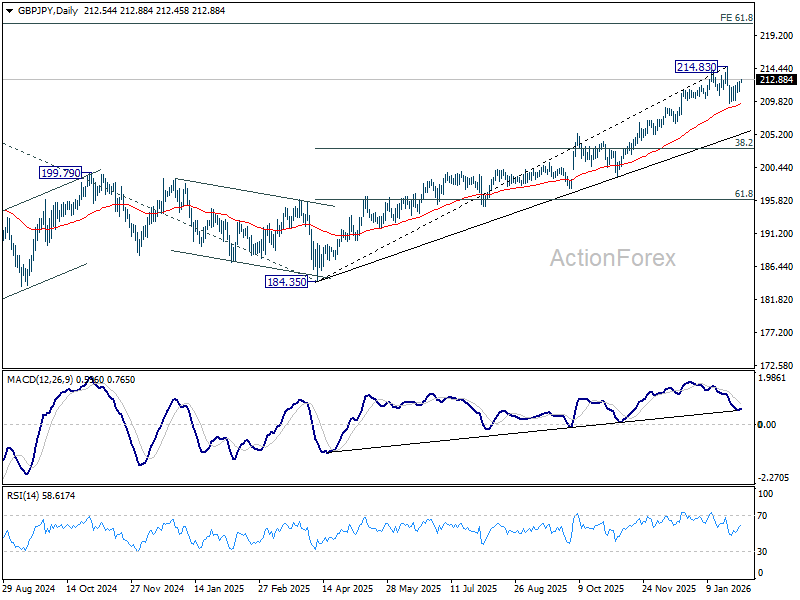

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.69; (P) 212.29; (R1) 213.28; More...

Intraday bias in GBP/JPY remains neutral and more consolidations would be seen first. Risk will stay on the downside as long as 214.83 holds, even in case of stronger recovery. Below 209.61, and sustained break of 55 D EMA (now at 209.51) will argue that it's correcting whole rise from 184.35 and target 38.2% retracement of 184.35 to 214.83 at 203.18.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

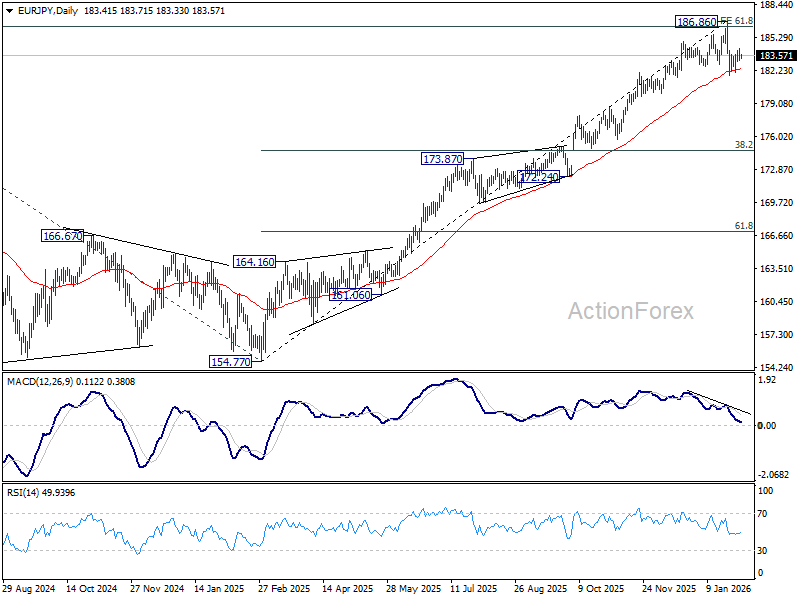

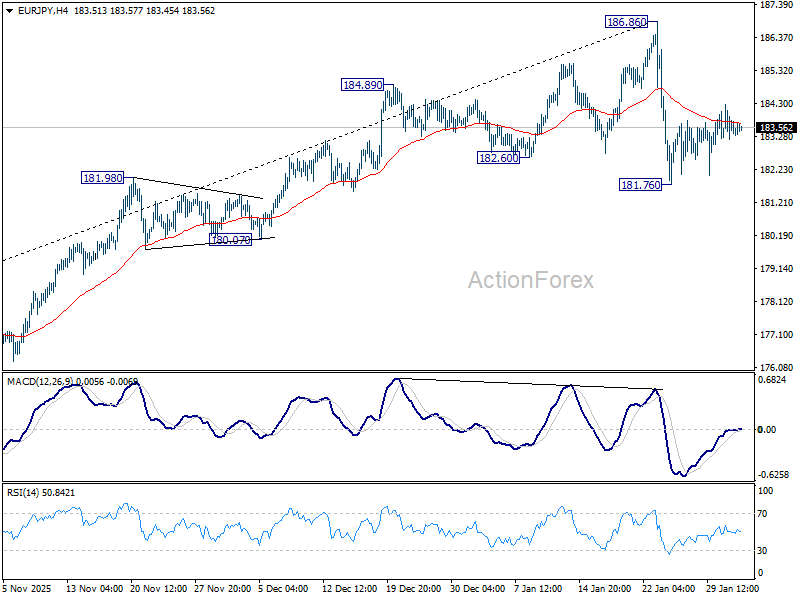

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.01; (P) 183.65; (R1) 184.10; More...

No change in EUR/JPY's outlook and intraday bias stays neutral for consolidations above 181.76. Risk remains on the downside as long as 186.86 holds, in case of strong recovery. Break of 181.76 and sustained trading below 55 D EMA (now at 182.35) should solidify the case that fall from 186.86 medium term top is correcting whole rise from 154.77. Deeper decline should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and and met 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 173.32) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.