Sample Category Title

Risk-On Asia and Hawkish RBA Propel Aussie Higher

Australian Dollar surged broadly in Asia session, drawing fresh strength from a hawkish RBA rate hike that reinforced expectations of further tightening later this year. The move gave the Aussie an extra tailwind on top of an already constructive regional backdrop.

Risk appetite in Asia has been firm, with the latest boost to sentiment coming from a surprise breakthrough on trade. The US and India reached an agreement to immediately lower tariffs on each other’s goods. Under the deal, US tariffs on Indian goods will be cut sharply to 18% from 50%, bringing India broadly in line with Asian peers at 15–19%. In return, India agreed to halt purchases of Russian oil and reduce a range of trade barriers, according to US President Donald Trump.

Indian Prime Minister Narendra Modi also committed to significantly increase purchases of US products. Modi later confirmed the tariff reduction in a post on X, hailing the agreement as a major win for Indian exports. The announcement followed closely on the heels of India’s landmark free trade agreement with the European Union, which Modi described as the “mother of all deals.”

While the trade news supported risk currencies, Yen remained under pressure amid mixed messaging from Tokyo. Japan’s Finance Minister Satsuki Katayama today defended Prime Minister Sanae Takaichi’s recent remarks on the benefits of a weaker yen, saying they reflected standard economic theory. Katayama stressed that Takaichi was speaking in general terms, noting that while a weak Yen has downsides, it can also support corporate revenues, domestic investment, and exports. The comments added to confusion over how tolerant authorities are of further Yen depreciation.

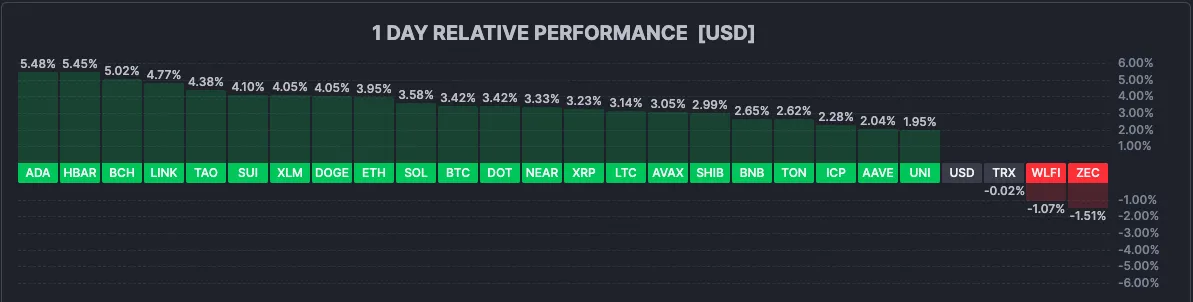

Overall this week so far, the Aussie sits firmly at the top of the FX performance table, followed by Kiwi and Dollar. Swiss Franc trails at the bottom, with Yen and Euro also lagging. Sterling and Loonie are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 3.85%. Hong Kong HSI is down -0.06%. China Shanghai SSE is up 0.44%. Singapore Strait Times is up 0.92%. Japan 10-year JGB yield is up 0.018 at 2.255. Overnight, DOW rose 1.05%. S&P 500 rose 0.54%. NASDAQ rose 0.56%. 10-year yield rose 0.034 to 4.275.

RBA delivers expected hike, forecast path points to another move

The RBA raised the cash rate by 25bps to 3.85% as widely expected, with the decision taken unanimously. While the accompanying statement avoided any explicit commitment to further tightening, the updated forecasts carried a more hawkish undertone.

Notably, the new projections are built on an assumption that the policy rate rises further to around 4.2% by the end of this year. That implicitly points to at least one additional hike being needed in the Bank’s view to contain resurging inflationary pressures.

In its statement, the RBA acknowledged that a broad range of recent data confirms inflationary pressures “picked up materially” in the second half of 2025. While part of the acceleration is judged to be temporary, the Bank highlighted that private demand is growing faster than expected, capacity pressures are higher than previously assessed, and labour market conditions remain slightly tight. Against that backdrop, the Board concluded that inflation is “likely to remain above target for some time,” justifying today’s move.

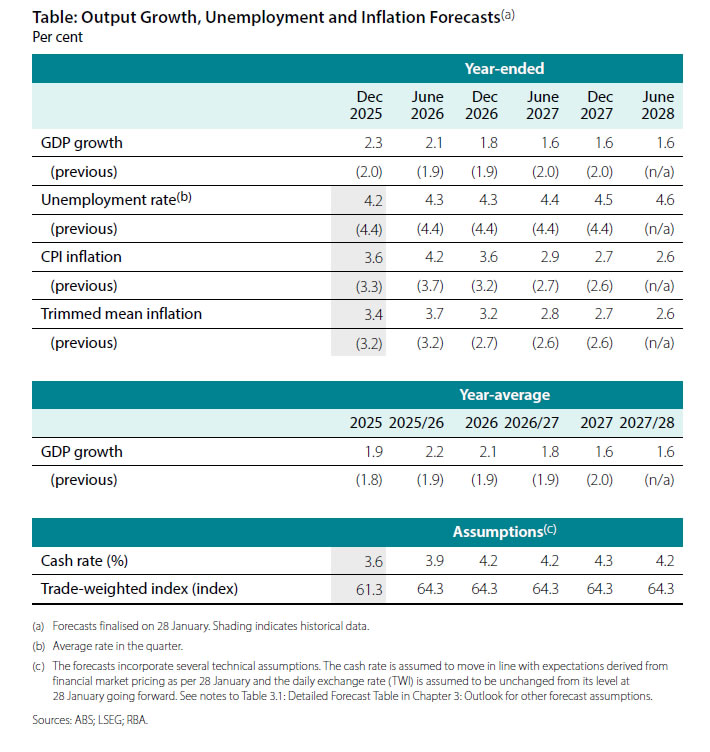

The message suggests policy is shifting from fine-tuning toward a more deliberate effort to re-anchor inflation expectations. The revised forecasts reinforce that view. CPI is now projected to peak at 4.2% in June 2026, up sharply from the previous 3.7% estimate, before easing to 3.6% by December 2026 and only gradually returning to 2.7% by end-2027. Trimmed mean inflation was also revised higher across the horizon, with the peak lifted to 3.7% in mid-2026.

Growth and labour market assumptions remain resilient. Average GDP growth for 2026 was revised up to 2.1% (from 1.9%), while the unemployment rate was nudged lower to 4.3% (down from 4.4%) next year, before edging higher to 4.5% in 2027. That profile suggests the RBA sees room to keep policy restrictive without inflicting material damage on employment, keeping the door open for further tightening if inflation fails to cool as projected.

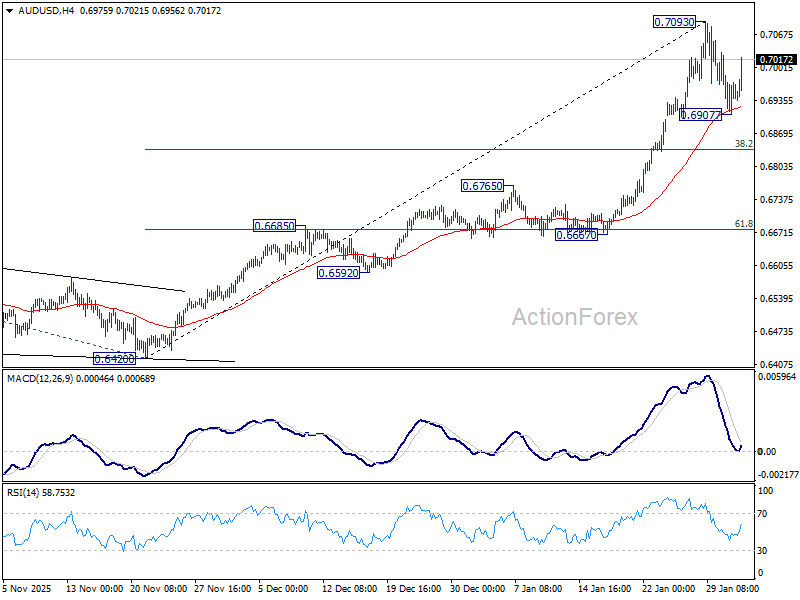

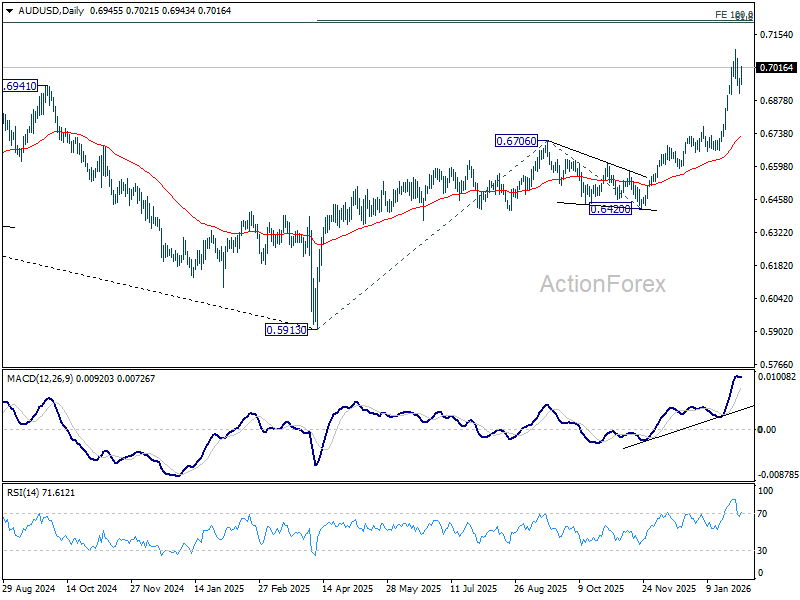

AUD/USD uptrend to resume to 0.72 after hawkish RBA hike

Aussie rallied broadly after the RBA raised the cash rate by 25bps to 3.85%, in line with expectations. While the decision itself was fully priced, the accompanying forecasts carried an implicit signal that another rate hike is likely later this year, providing fresh support to the currency.

AUD/USD quickly pushed back above the 0.7000 mark following the announcement. Technically, strong support has been established at 55 4H EMA, suggesting that the recent consolidation from the 0.7093 should remain shallow and temporary.

Decisive break above 0.7093 would confirm continuation of the broader uptrend from 0.5913 (2025 low). In this scenario, AUD/USD would be on track to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 in the next leg higher.

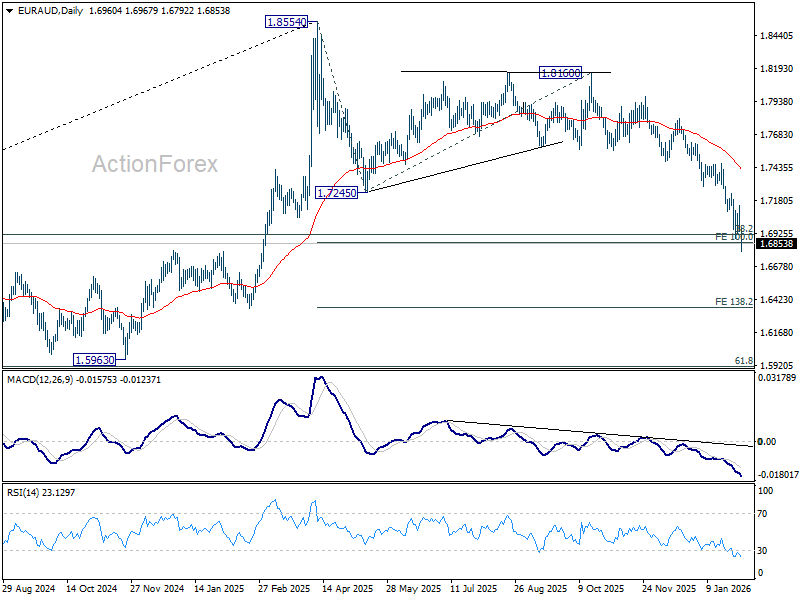

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6947; (P) 1.7016; (R1) 1.7091; More...

EUR/AUD's decline resumed by breaking through 1.6892 temporary low and intraday bias is back on the downside. Sustained trading below 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851 will pave the way to 138.2% projection at 1.6351 next. On the upside, break of 1.7145 resistance is needed to indicate short term bottoming. Otherwise, will remain bearish in case of recovery.

In the bigger picture, fall from 1.8554 medium term top is still in progress. Sustained break of 38.2% retracement of 1.4281 to 1.8554 at 1.6922 will argue that it's already reversing whole up trend from 1.4281 (2022 low). Deeper fall would be seen to 61.8% retracement at 1.5913. For now, risk will stay on the downside as long as 55 D EMA (now at 1.7418) holds even in case of strong rebound.

AUD/USD uptrend to resume to 0.72 after hawkish RBA hike

Aussie rallied broadly after the RBA raised the cash rate by 25bps to 3.85%, in line with expectations. While the decision itself was fully priced, the accompanying forecasts carried an implicit signal that another rate hike is likely later this year, providing fresh support to the currency.

AUD/USD quickly pushed back above the 0.7000 mark following the announcement. Technically, strong support has been established at 55 4H EMA, suggesting that the recent consolidation from the 0.7093 should remain shallow and temporary.

Decisive break above 0.7093 would confirm continuation of the broader uptrend from 0.5913 (2025 low). In this scenario, AUD/USD would be on track to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 in the next leg higher.

RBA delivers expected hike, forecast path points to another move

The RBA raised the cash rate by 25bps to 3.85% as widely expected, with the decision taken unanimously. While the accompanying statement avoided any explicit commitment to further tightening, the updated forecasts carried a more hawkish undertone.

Notably, the new projections are built on an assumption that the policy rate rises further to around 4.2% by the end of this year. That implicitly points to at least one additional hike being needed in the Bank’s view to contain resurging inflationary pressures.

In its statement, the RBA acknowledged that a broad range of recent data confirms inflationary pressures “picked up materially” in the second half of 2025. While part of the acceleration is judged to be temporary, the Bank highlighted that private demand is growing faster than expected, capacity pressures are higher than previously assessed, and labour market conditions remain slightly tight. Against that backdrop, the Board concluded that inflation is “likely to remain above target for some time,” justifying today’s move.

The message suggests policy is shifting from fine-tuning toward a more deliberate effort to re-anchor inflation expectations. The revised forecasts reinforce that view. CPI is now projected to peak at 4.2% in June 2026, up sharply from the previous 3.7% estimate, before easing to 3.6% by December 2026 and only gradually returning to 2.7% by end-2027. Trimmed mean inflation was also revised higher across the horizon, with the peak lifted to 3.7% in mid-2026.

Growth and labour market assumptions remain resilient. Average GDP growth for 2026 was revised up to 2.1% (from 1.9%), while the unemployment rate was nudged lower to 4.3% (down from 4.4%) next year, before edging higher to 4.5% in 2027. That profile suggests the RBA sees room to keep policy restrictive without inflicting material damage on employment, keeping the door open for further tightening if inflation fails to cool as projected.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 3.85 per cent.

While inflation has fallen substantially since its peak in 2022, it picked up materially in the second half of 2025. The Board has been closely monitoring the economy and judges that some of the increase in inflation reflects greater capacity pressures. As a result, the Board considers that inflation is likely to remain above target for some time.

Capacity pressures reflect, in part, the greater momentum in demand seen in recent months. Growth in private demand has strengthened substantially more than expected, driven by both household spending and investment. Activity and prices in the housing market are also continuing to pick up. Financial conditions eased over 2025 and it is uncertain whether they remain restrictive. Credit is readily available to both households and businesses and the effects of earlier interest rate reductions are yet to flow through fully to aggregate demand, prices and wages. More recently, the exchange rate, money market interest rates and government bond yields have risen following a rise in market expectations for the cash rate.

Various indicators suggest that labour market conditions remain a little tight and that they have stabilised in recent months, in line with the pick-up in momentum in economic activity. The unemployment rate has been a little lower than expected and measures of labour underutilisation remain at low rates. Growth in the Wage Price Index has eased from its peak, but broader measures of wages growth continue to be strong and growth in unit labour costs remains high.

There are uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy is restrictive. On the domestic side, if growth in demand is stronger than expected, and growth in the economy’s supply capacity remains limited, it is likely to add further to capacity pressures. Uncertainty in the global economy remains significant but so far there has been little or no depressing effect on the Australian economy; indeed, recent growth and trade in Australia’s major trading partners has surprised on the upside.

Decision

A wide range of data over recent months have confirmed that inflationary pressures picked up materially in the second half of 2025. While part of the pick-up in inflation is assessed to reflect temporary factors, it is evident that private demand is growing more quickly than expected, capacity pressures are greater than previously assessed and labour market conditions are a little tight.

The Board judged that inflation is likely to remain above target for some time and it was appropriate to increase the cash rate target.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

Today’s policy decision was unanimous.

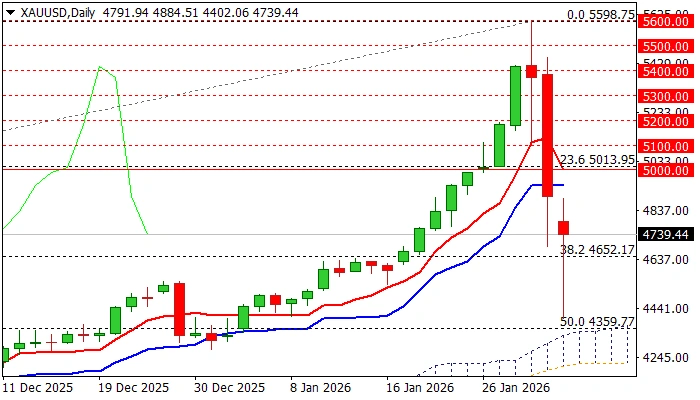

Gold Attempts Recovery As Traders Digest Flash Crash

Key Highlights

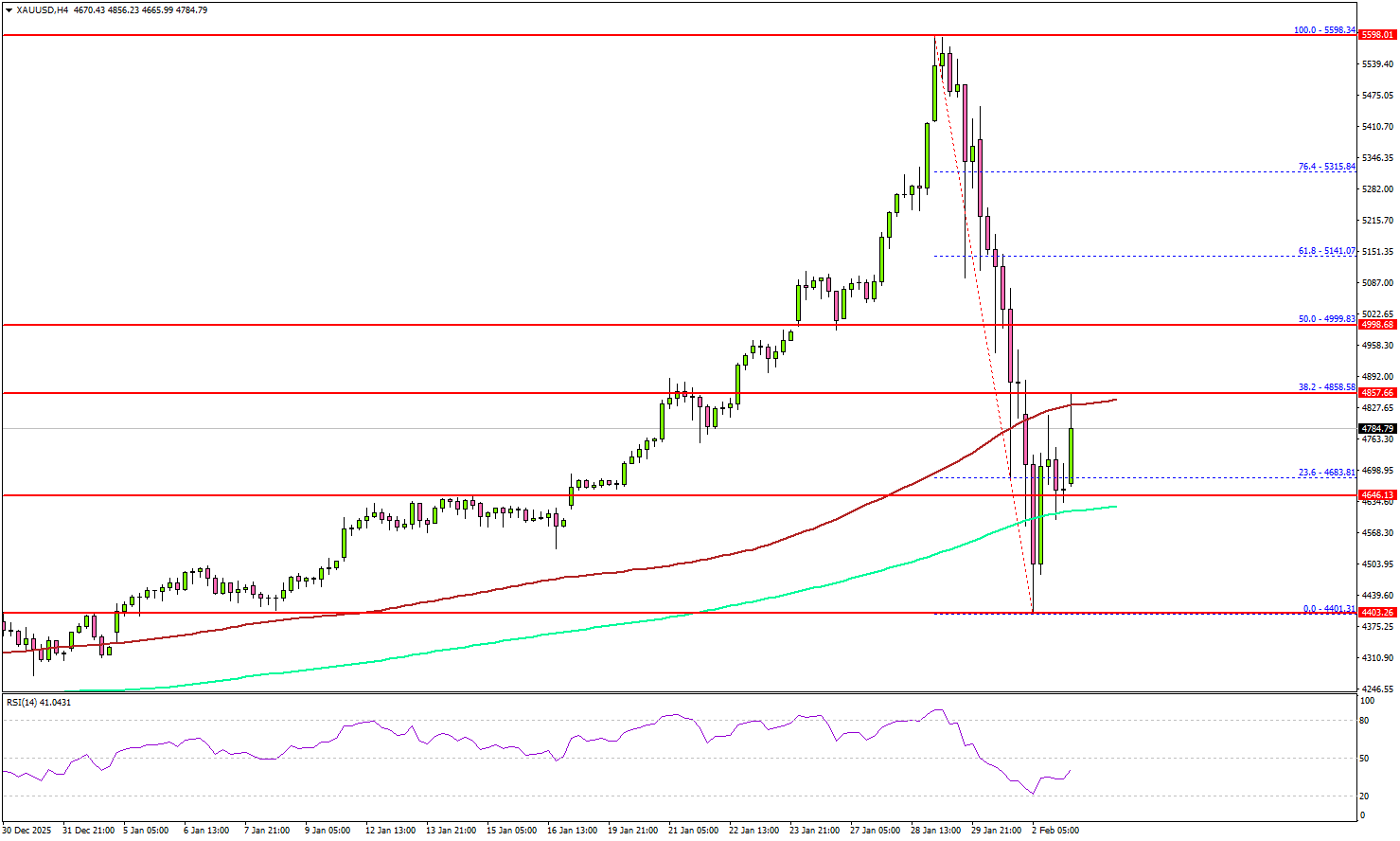

- Gold nosedived below $5,000 before it found support at $4,400.

- It could now face hurdles near $4,850 and $5,000 on the 4-hour chart.

- WTI Crude Oil prices also corrected some gains from $66.50.

- USD/JPY started a recovery wave above 153.75 and 154.50.

Gold Price Technical Analysis

Gold extended its rally to $5,598 against the US Dollar before witnessing a major decline. The price tested the $4,400 zone and recently started a recovery wave.

The 4-hour chart of XAU/USD indicates that the price traded as low as $4,401 and recently started a recovery wave above the 200 Simple Moving Average (green, 4 hours). The price climbed above the 23.6% Fib retracement level of the downward move from the $5,598 swing high to the $4,401 low.

On the upside, immediate resistance is near the $4,850 level and the 100 Simple Moving Average (red, 4 hours). The next major resistance sits near the $5,000 handle since it coincides with the 50% Fib retracement level of the downward move from the $5,598 swing high to the $4,401 low.

A clear move above $5,00 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $5,200. The main target for the bulls could be $5,320.

If there is another decline, Gold might find bids near the $4,620 level. The first major support sits at $4,550, below which the price might slide to $4,500. The main support sits at $4,400. Any more losses might call for a test of at $4,320 or even $4,200 in the coming days.

Looking at WTI Crude Oil, the price recovered above $65.00 before the bears took a stand near $66.50.

Economic Releases to Watch Today

- Fed's Barkin speech.

- Fed's Bowman speech.

Bitcoin breaks $80,000! Altcoins suffer – BTC, ETH and SOL Outlook

- Bitcoin breaks lower and drags pessimistic sentiment in Cryptocurrencies

- With the current volatile environment, investors reduce risk-positioning

- Observing technical analysis for Bitcoin, Ethereum and Solana

Cryptocurrencies are struggling after rejecting early-year rebound attempts.

Risk sentiment remains weak even as equities hover near all-time highs: Investors are reducing exposure to risk-sensitive assets, mirroring the underperformance in semiconductor and tech sectors as high-beta capital rotates back into hardware.

Digital assets faced significant headwinds at the end of 2025, lagging behind most other asset classes – These negative flows still continue to weigh on the sector.

MicroStrategy (MSTR), a key figure in the previous bull run, is now under scrutiny as its Bitcoin holdings near the breakeven point, with an average cost basis of approximately $76,000.

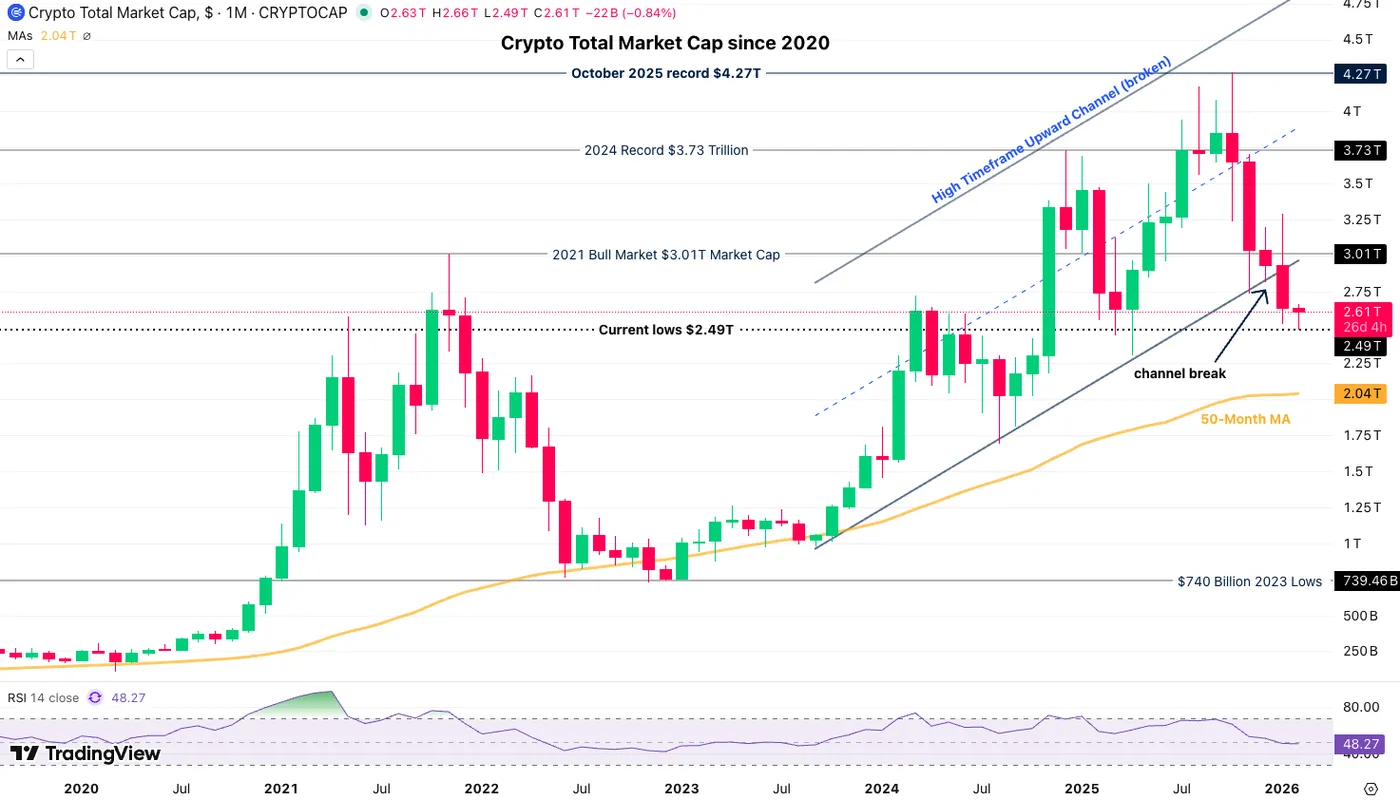

As noted in our year-end analysis, the total Cryptocurrency Market Capitalization is breaking support after previously holding its long-term upward trendline, signaling potential for further downside – Keep an eye on the $2 Trillion mark!

Crypto total Market Cap Monthly Chart – Source: TradingView

Cryptocurrencies are inherently volatile.

Historically, the best investment opportunities arise when interest and mentions are low, while peak popularity often signals a time to take profits.

Currently, the market remains active with traders attempting to buy dips, suggesting sentiment has not yet fully washed out.

Given the bearish short-term outlook, patience is advisable.

Letting prices and hype cool down while waiting for a more favorable macro setup may offer better entry points – Still, the large corrections already favor better entries compared to peak prices from mid-2025.

This is when starting DCA strategies could start to make sense.

Current Session in Cryptos – February 2, 2026 (15:23). Source: FInviz

Following a disastrous weekend session, altcoins are seeing a timid recovery but remain well below last week's levels. Most of the main names are green on the day and the biggest gains stand around 5%.

Let's dive right into the Daily Charts and technical levels for Bitcoin (BTC), Ethereum (ETH) and Solana (SOL).

Bitcoin (BTC) 4H Chart and Technical Levels

Bitcoin (BTC) 4H Chart, February 2, 2026 – Source: TradingView

Bitcoin freshly retested its Liberation Day lows ($74,500) and is rebounding timidly from that level.

With the painful action from the weekend, it is rough to say that dip-buying is looking like a favorable setup – At least for now.

A bullish push above $80,000 and daily close above the level relaunches positive prospects for Bitcoin and the rest of the Crypto Market.

Consolidating below the key psychological level could lead to further downside, with the next Main support at $63,000 (Minor support at $70,000).

Levels of interest for BTC trading:

Support Levels

- $75,000 Key long-term support (Liberation Day lows)

- $68,000 to $70,000 end-2024 Minor Support

- $$60,000 to $63,000 Main 2024 support

Resistance Levels

- $80,000 to $83,000 Major Pivot (November 21 Lows $80,740)

- $88,000 to $93,000 Pivotal Resistance

- $98,000 to $100,000 Resistance

- Resistance at previous ATH $106,000 to $108,000

- Current ATH Resistance $124,000 to $126,000

Ethereum (ETH) 4H Chart and Technical Levels

Ethereum (ETH) 4H Chart, February 2, 2026 – Source: TradingView

Ethereum gave back its early 2026 positive setup, having broken first its $3,000 handle before giving up all of its Mid-2025 explosion throughout last week.

Its overnight wick retested ETH's pre-June War Support zone ($2,100 to $2,300) with the action remaining fragile at that level.

Traders will want to see a high volume and positive candle, preferably after a double bottom for the action to turn more positive – For now, expect consolidation near support.

Levels of interest for ETH trading:

Support Levels:

- $2,100 to $2,300 June War support ($2,150 overnight lows)

- $2,000 psychological support

- $1,385 to $1,750 2025 Major Support

- 2025 Lows $1,384

Resistance Levels:

- $2,500 to $2,700 June 2025 Key Pivot

- $3,000 to $3,200 December resistance

- $3,400 January Highs

- $3,500 (+/- $50) Key Resistance

- $4,000 Dec 2024 Top Main Resistance zone

- $4,950 Current new All-time highs

Solana (SOL) 4H Chart and Technical Levels

Solana (SOL) 4H Chart, February 2, 2026 – Source: TradingView

Solana got subject to quite some heavy selling, representing the rest of the Altcoin market in its struggles.

Now facing a very important test at its $100 Liberation Day support, traders will want to watch if bulls can retake control after the 57% retracement from its 2025 peak.

Repassing above $115 would turn the momentum from bearish to neutral-bullish on short-timeframe.

Levels to keep on your SOL Charts:

Support Levels:

- $97 to $100 Liberation Day lows

- $95.95 Weekend Lows

- $76 to $82 Major 2022 Pivot

Resistance Levels:

- Major Momentum Pivot $115 to $120

- $125 to $130 2026 Base Resistance

- $140 to $150 Major Resistance

- $253 Cycle highs

Safe Trades!

Oil Prices Down 6% as US-Iran De-escalation Hopes Cool Market Heat… End of the Line for Bulls?

Oil prices have slipped 6% today in what is a poor start to the month. This comes after an impressive rally in the month of January.

WTI finished January with gains of around 14% but that turned sour this morning with a 5% plunge in the Asian session. This sharp reversal appears to be driven by a combination of diplomatic shifts in the Middle East and strategic supply decisions by major producers.

The primary drivers behind the drop

The most immediate catalyst for the price drop is the sudden cooling of tensions between the United States and Iran. Just a week ago, markets were pricing in a significant risk of military conflict after US President Donald Trump hinted at potential strikes.

However, remarks made by the President on Sunday expressing hope for a new deal with Iran with a meeting scheduled for Friday this week which has dramatically pivoted investor sentiment.

The prospect of a diplomatic breakthrough suggests a potential easing of sanctions. If an agreement is reached, Iran, a major OPEC member, could legally return significant volumes of crude to the global market.

This "peace premium" being removed from the price of oil has led to a rapid sell-off, as traders re calibrate for a more well-supplied market than previously feared.

OPEC + maintains the status quo

Adding to the downward pressure, OPEC+ concluded its latest meeting with a decision to keep production levels unchanged for March. While the group’s "cautious approach" is intended to maintain market stability, it failed to provide the bullish spark some investors were hoping for. By reaffirming a freeze on planned production increases, OPEC+ signaled that they anticipate seasonally weaker demand in the coming months.

Taking a look at US drilling activity, it appears to be in a slump because low prices are making new investments less attractive for energy companies. Recent data from Baker Hughes shows that the number of active oil rigs held steady at 411 last week, which is significantly lower than this time last year.

While there was a tiny increase in gas drilling, the overall number of active rigs remains 36 below last year's levels. Because experts expect there to be more oil on the market than people actually need this year (a "surplus"), US oil production growth is expected to stay limited throughout 2026.

Forward Outlook - bulls or bears to prevail?

The future of oil prices currently hangs on two major variables: the reality of US-Iran diplomacy and the strength of the US dollar.

- Geopolitical Volatility: While de-escalation is the current theme, financial institutions like DBS and Deutsche Bank warn that the situation remains fragile. Should diplomatic efforts fail or military rhetoric resurface, a renewed rally beyond the $70/barrel mark cannot be ruled out.

- The "Warsh Effect": The US dollar has been gaining strength following the nomination of Kevin Warsh as the next Federal Reserve Chair. Because oil is priced in dollars, a stronger greenback makes the commodity more expensive for international buyers, creating a natural headwind for price growth.

In the short term, markets are looking toward upcoming US inventory data from the API and EIA to gauge domestic demand.

While the current trend is bearish, the structural risks in the Middle East suggest that the "pause" in the oil rally may be temporary rather than a permanent reversal.

For now, investors are moving with caution, balancing the hope of a diplomatic solution against the ever-present threat of supply disruptions. Keep an eye on developments between Iran-US when they meet on Friday in Turkey.

Technical Analysis - WTI

From a technical analysis standpoint, WTI drop is flirting with a close below the 200-day MA.

This would not be the first time that WTI has broken above the 200-day MA and reversed the move in a few days.

The last time WTI traded above the 200-day MA was in July 2025 when the price only managed to hold above the 200-day MA for two days before slipping back below for a prolonged period.

All is not lost for bulls though as the 100-day MA may provide the support that bulls are looking for as it rests on the psychological 60.00 handle, making this area a key confluence zone.

The period-14 RSI is just shy of the neutral 50 level and if it holds above this is a positive signs for bulls as it is seen as a sign of bullish momentum.

WTI Crude Oil Daily Chart, February 2, 2026

Source: TradingView (click to enlarge)

Key levels to keep an eye on

Support:

- 60.00

- 58.50

- 57.00

Resistance:

- 62.32

- 64.73

- 66.15

Eco Data 2/3/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits Dec | -4.60% | 2.80% | 2.70% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | -9.50% | -10.20% | -9.80% | |

| 00:30 | AUD | Building Permits M/M Dec | -14.90% | -6.00% | 15.20% | 13.10% |

| 03:30 | AUD | RBA Interest Rate Decision | 3.85% | 3.85% | 3.60% | |

| 04:30 | AUD | RBA Press Conference |

| 21:45 | NZD |

| Building Permits Dec | |

| Actual | -4.60% |

| Consensus | |

| Previous | 2.80% |

| Revised | 2.70% |

| 23:50 | JPY |

| Monetary Base Y/Y Jan | |

| Actual | -9.50% |

| Consensus | -10.20% |

| Previous | -9.80% |

| 00:30 | AUD |

| Building Permits M/M Dec | |

| Actual | -14.90% |

| Consensus | -6.00% |

| Previous | 15.20% |

| Revised | 13.10% |

| 03:30 | AUD |

| RBA Interest Rate Decision | |

| Actual | 3.85% |

| Consensus | 3.85% |

| Previous | 3.60% |

| 04:30 | AUD |

| RBA Press Conference | |

| Actual | |

| Consensus | |

| Previous | |

Gold: Downside Still Very Vulnerable Despite Today’s Strong Bounce

Gold extended sharp drop and fell to the lowest in one month, after trading on Monday started with about $100 gap lower, signaling that negative sentiment (after Friday’s biggest daily drop in over four decades), persists.

De-escalating tensions over Iran and initial signals that war in Ukraine might be heading towards its end, contributed to fresh selling, with speculations that big names were also in play to significantly lower metal’s price.

The cocktail of key factors pushed the price significantly lower, though on the bigger picture this still looks like a healthy correction of larger rally, as today’s spike low ($4402) found footstep just above 50% retracement of $3120/$5598 (May/ January upleg).

Today’s strong bounce from new low at $4402 (approx. $300) signals growing bids, with close above cracked Fibo 38.2% level ($4652), along with formation of bull-trap, needed to keep in play hopes of an end of potential further recovery.

However, more work at the upside will be still required to validate such scenario (close above Fibo 38.2% of $5598/$4402 pullback) while filling today’s gap and sustained break above $5000 (psychological / 50% retracement) would generate stronger bullish signal.

Negative scenario, on the other hand, may see today’s bounce as positioning for fresh push lower, as near-term action remains weighed by Friday’s massive bearish candle, while overall sentiment is still predominantly negative, due to weaker key fundamental factors, as well as existing fears of more losses after panic selling in past two sessions.

Lower triggers lay at $4359 (50% retracement) and $4348 (top of rising thin daily cloud, spanned between $4348 and $4218), with break here to generate fresh bearish signal and unmask nest targets at $4067 (Fibo 61.8% of $3120/$5598) and $4000 (psychological).

Res: 4859; 4900; 5000; 5100.

Sup: 4402; 4348; 4218; 4170.

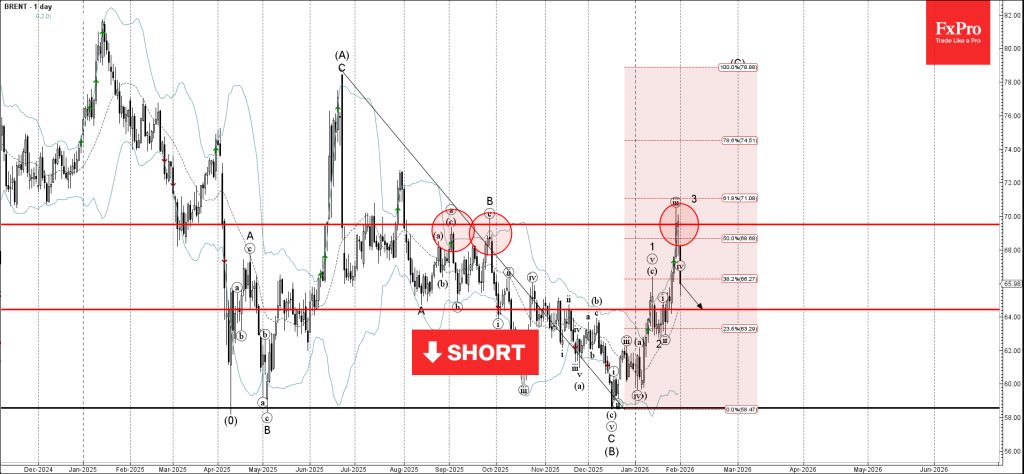

Brent Crude Oil Wave Analysis

Brent Crude Oil: ⬇️ Sell

- Brent Crude Oil reversed from resistance level 69.50

- Likely to fall to support level 64.25

Brent Crude Oil recently reversed from the resistance area located between the pivotal resistance level 69.50 (which has been reversing the price from September), upper daily Bollinger Band and by the 61.8% Fibonacci correction of the downward impulse from June of 2025.

The downward reversal from this resistance area created the daily Japanese candlesticks reversal pattern Long-legged Doji – strong sell signal for Brent Crude Oil.

Brent Crude Oil can be expected to fall to the next support level 64.25 (former resistance from November and January).