Sample Category Title

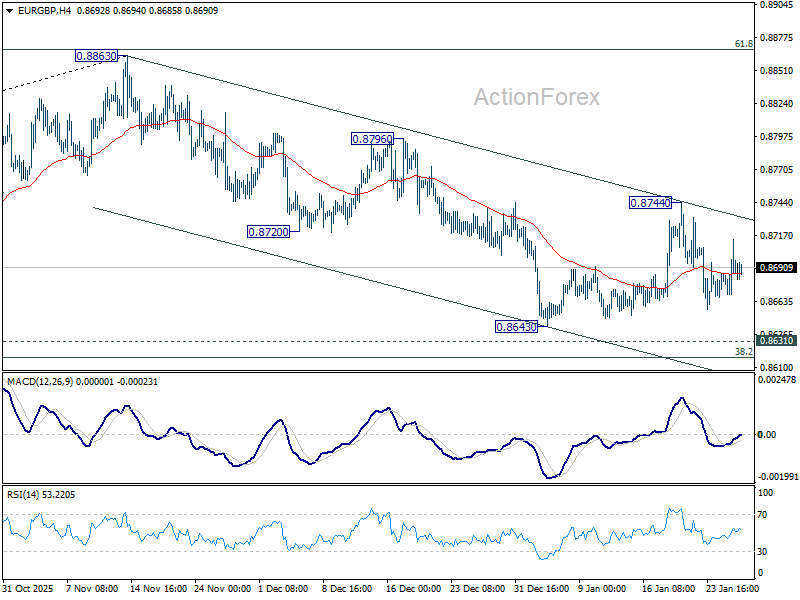

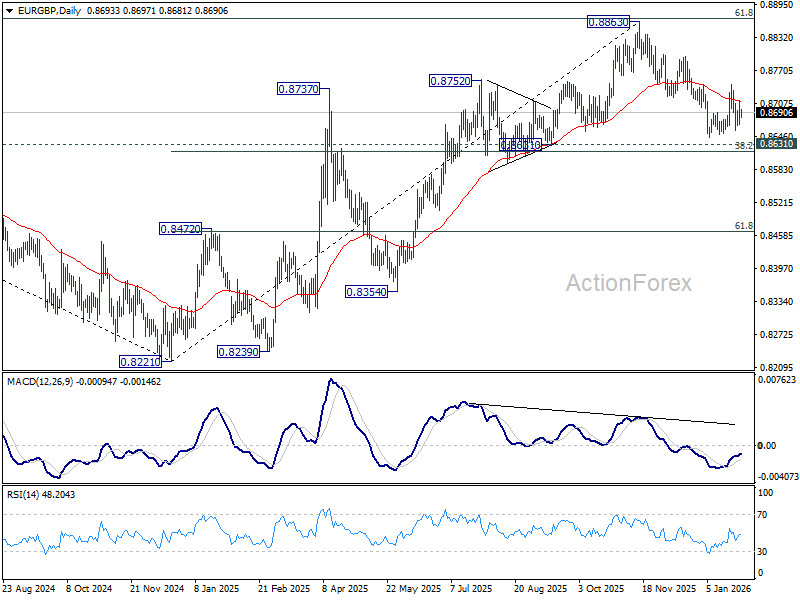

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8671; (P) 0.8693; (R1) 0.8717; More…

Intraday bias in EUR/GBP stays neutral as range trading continues. But risk will remain on the downside as long as 0.8744 resistance holds. Further decline is expected to 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618). Decisive break there will carry larger bearish implications and pave the way to 61.8% retracement at 0.8466.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

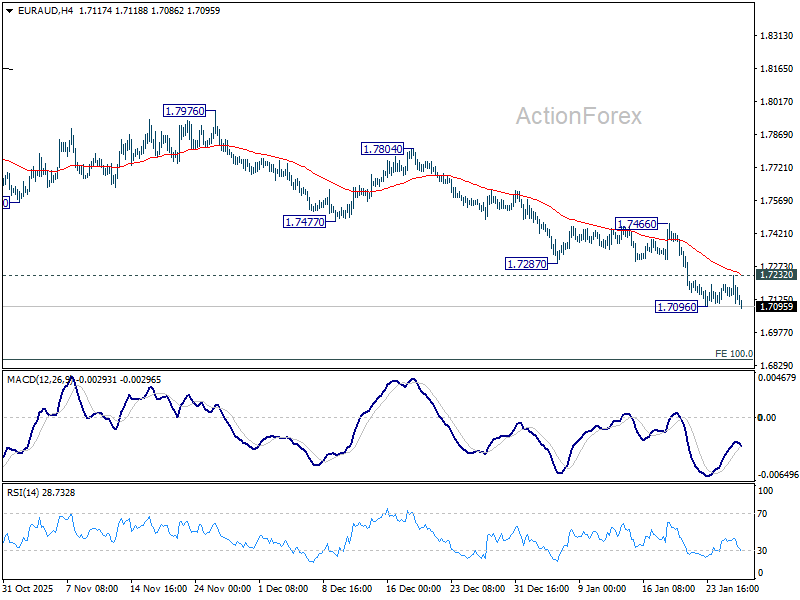

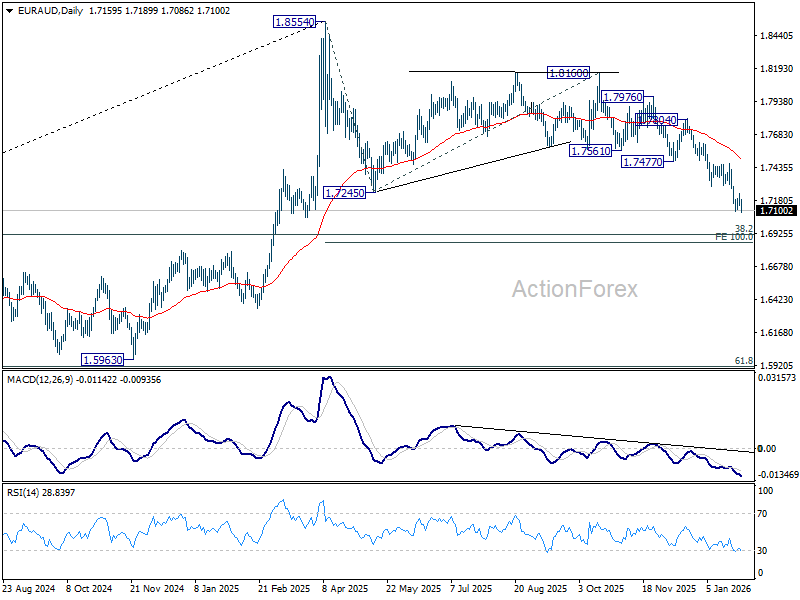

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7131; (P) 1.7183; (R1) 1.7223; More...

Intraday bias in EUR/AUD is back on the downside with breach of 1.7096 temporary low. Current fall from 1.8160 is seen as the third leg of the corrective pattern from 1.8554. Deeper decline should be seen to 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851. Nevertheless, break of 1.7232 resistance will now indicate short term bottoming, and turn bias back to the upside for stronger rebound to 1.7466.

In the bigger picture, the break of 55 W EMA (now at 1.7464) argues that fall from 1.8554 medium term top is correcting whole up trend from 1.4281 (2022 low). Deeper decline is in favor to 38.2% retracement of 1.4281 to 1.8554 at 1.6922, and possibly below. Risk will stay on the downside as long as 55 D EMA (now at 1.7537) holds, in case of strong rebound.

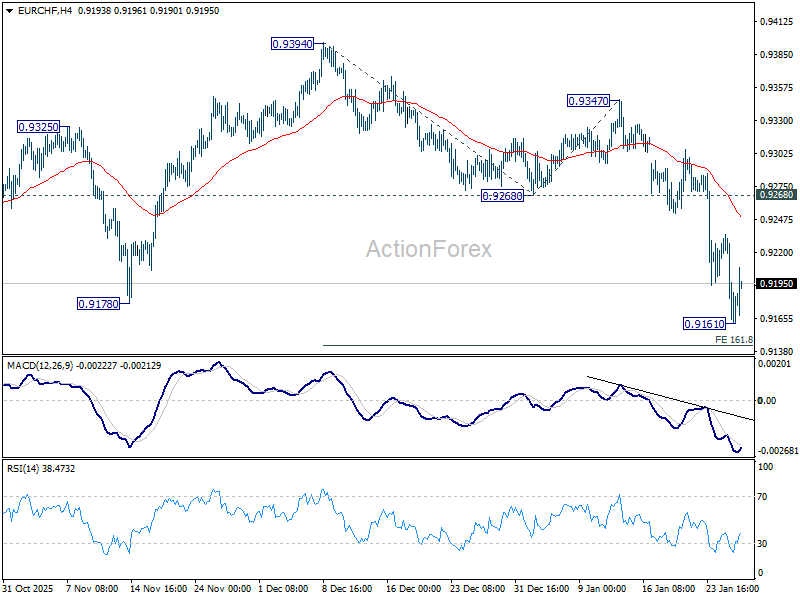

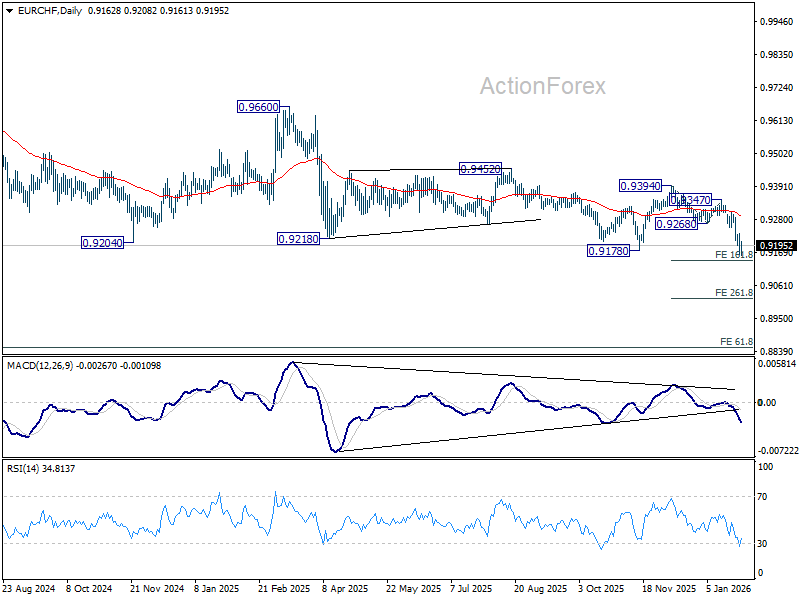

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9141; (P) 0.9189; (R1) 0.9214; More....

Intraday bias in EUR/CHF is turned neutral with current recovery. Some consolidations would be seen first, but upside should be limited below 0.9268 support turned resistance. Firm break of 161.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143 will target 261.8% projection at 0.9017.

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

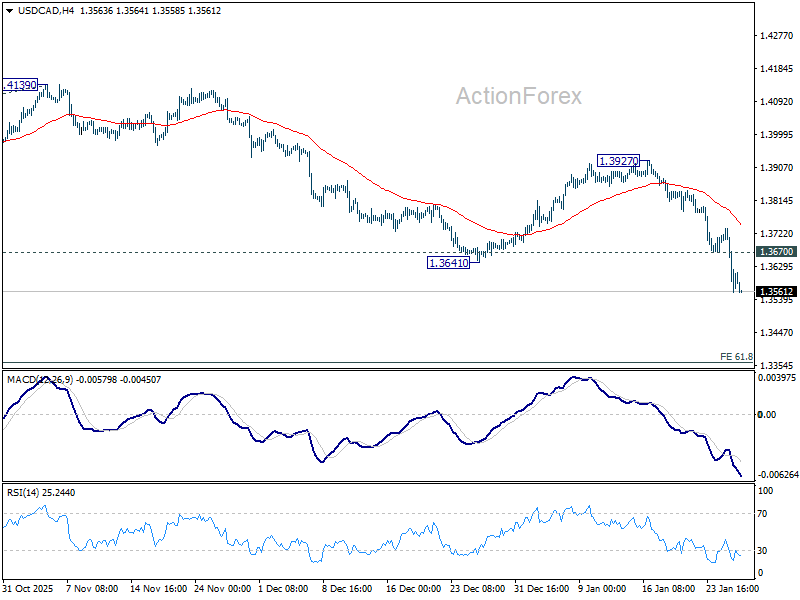

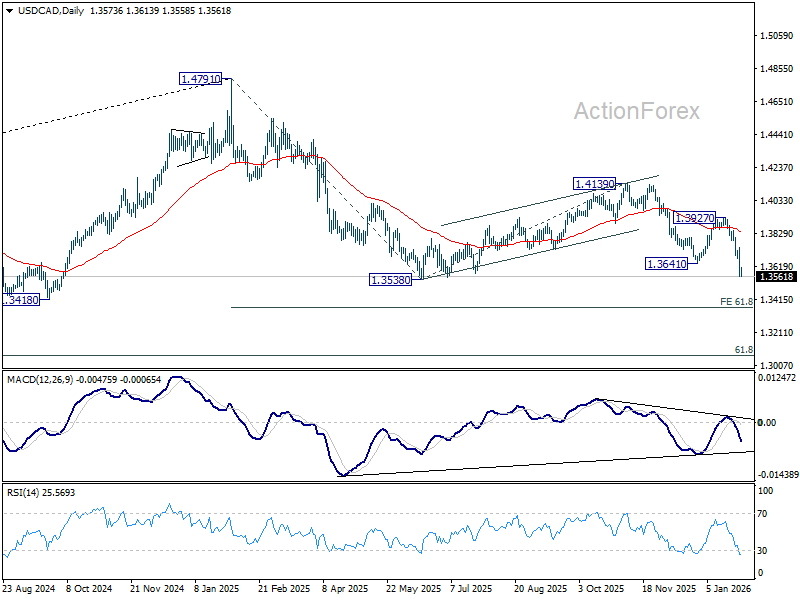

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3512; (P) 1.3626; (R1) 1.3693; More...

Intraday bias in USD/CAD remains on the downside for retesting 1.3538 low. Firm break there resume whole fall from 1.4971. Next target is 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. On the upside, above 1.3670 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

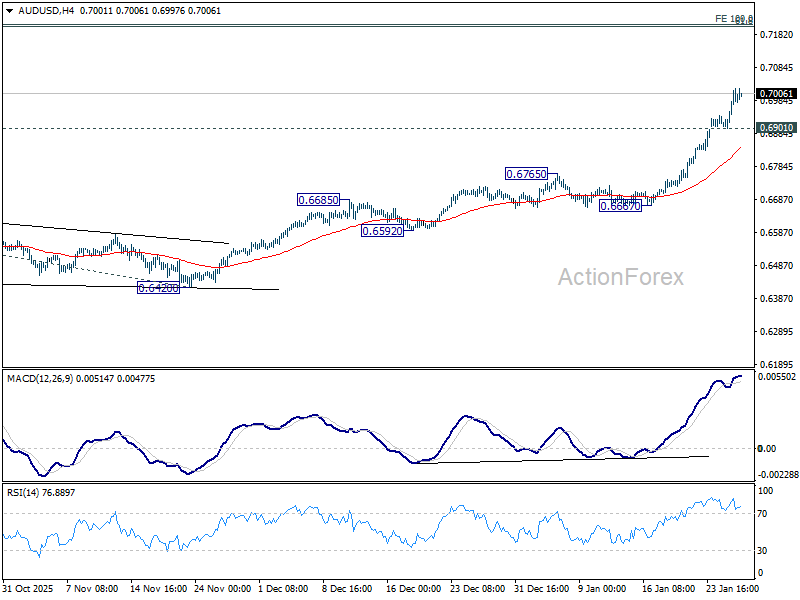

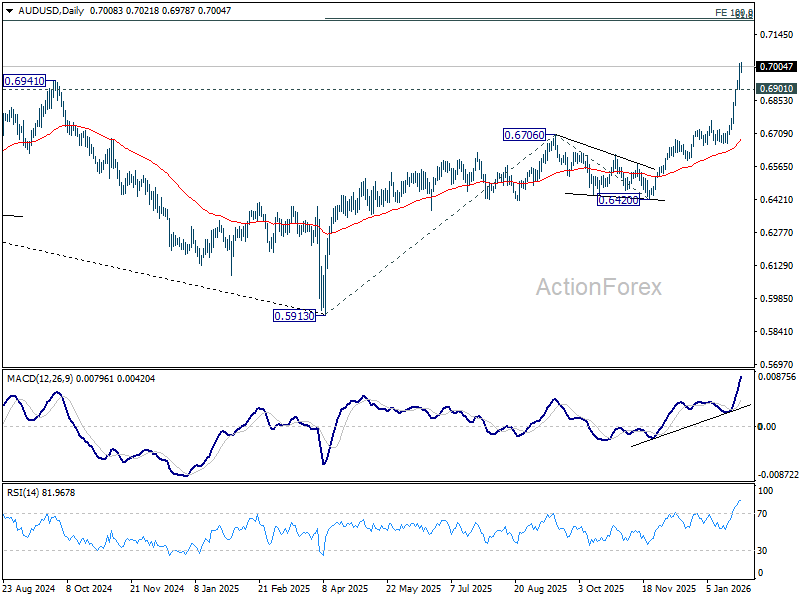

AUD/USD Daily Report

Daily Pivots: (S1) 0.6937; (P) 0.6976; (R1) 0.7051; More...

Intraday bias in AUDUSD stays on the upside for the moment. Current rally is part of the up trend form 0.5913 and should target 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. On the downside, below 0.6901 minor support will turn intraday bias neutral and bring consolidations. Downside of retreat should be contained above 0.6765 resistance turned support to bring another rally.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

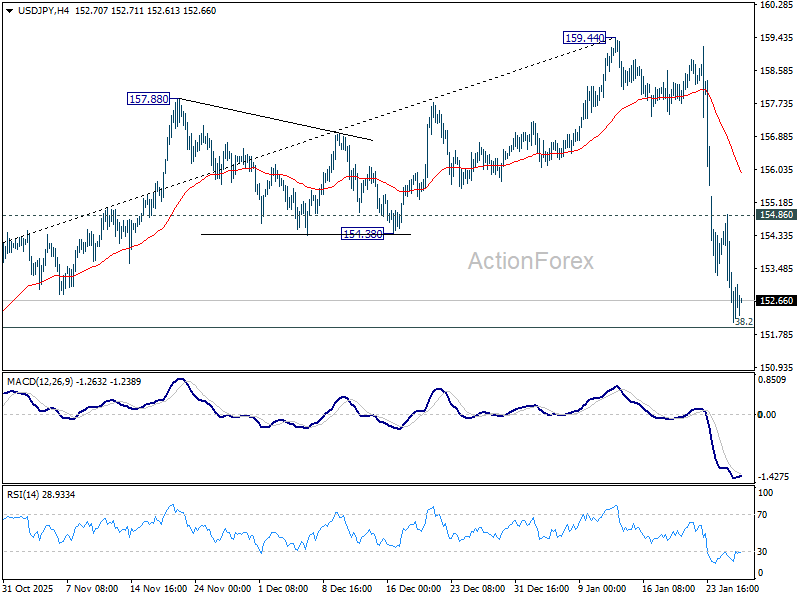

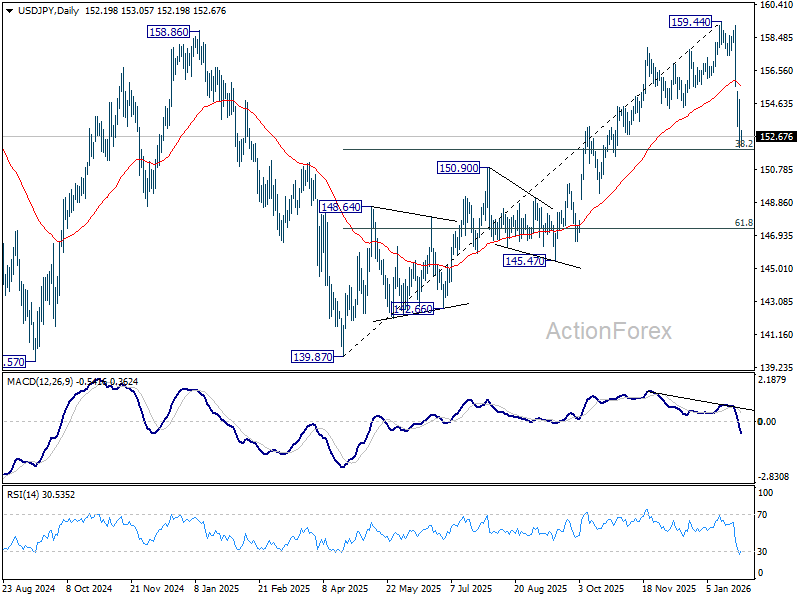

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.25; (P) 153.06; (R1) 154.04; More...

Intraday bias in USD/JPY is turned neutral first with loss of downside momentum. Fall from 159.44 is seen as correcting the rise from 139.87. Strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound, at least on first attempt. On the upside above 154.86 minor resistance will turn intraday bias to the upside for recovery. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

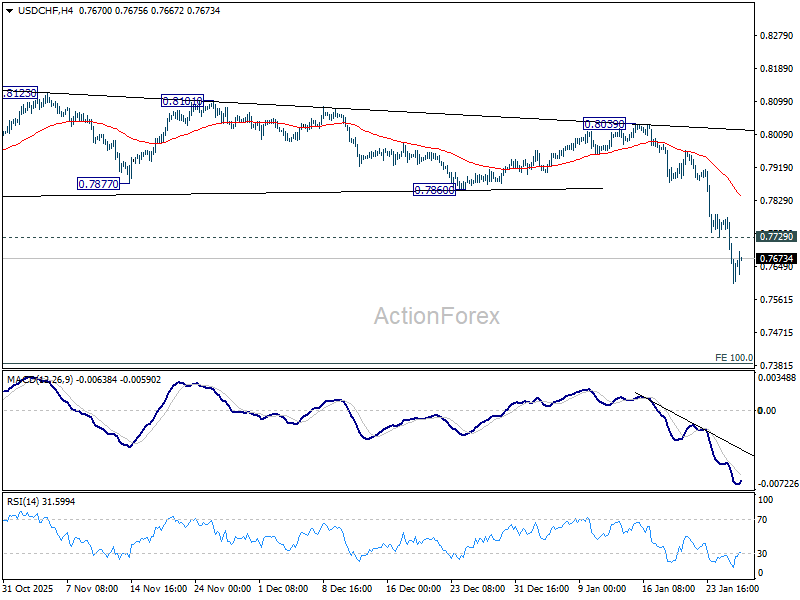

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7550; (P) 0.7667; (R1) 0.7730; More….

Intraday bias in USD/CHF remains on the downside at this point. Current fall is part of the long term down trend and should target 0.7382 projection level next. On the upside, above 0.7729 minor resistance will turn intraday bias neutral again. But recovery should be limited by 0.7860 support turned resistance and bring another fall.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

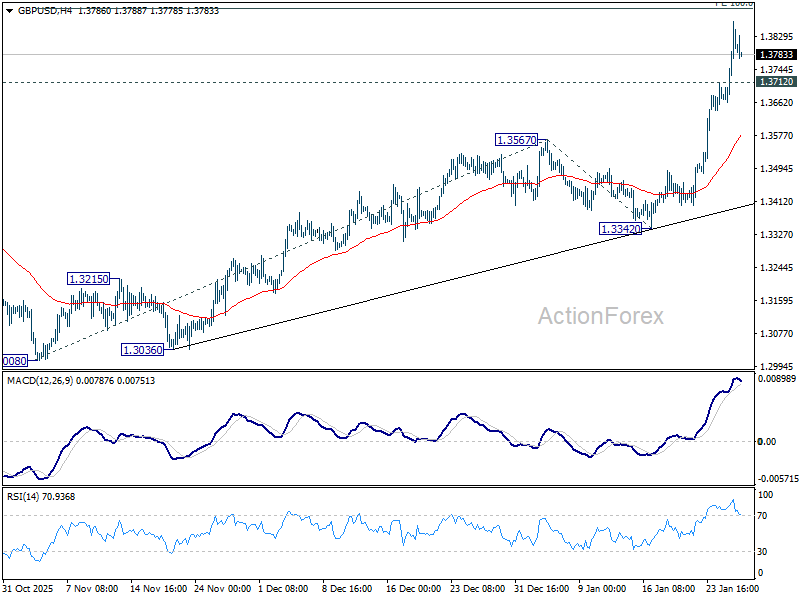

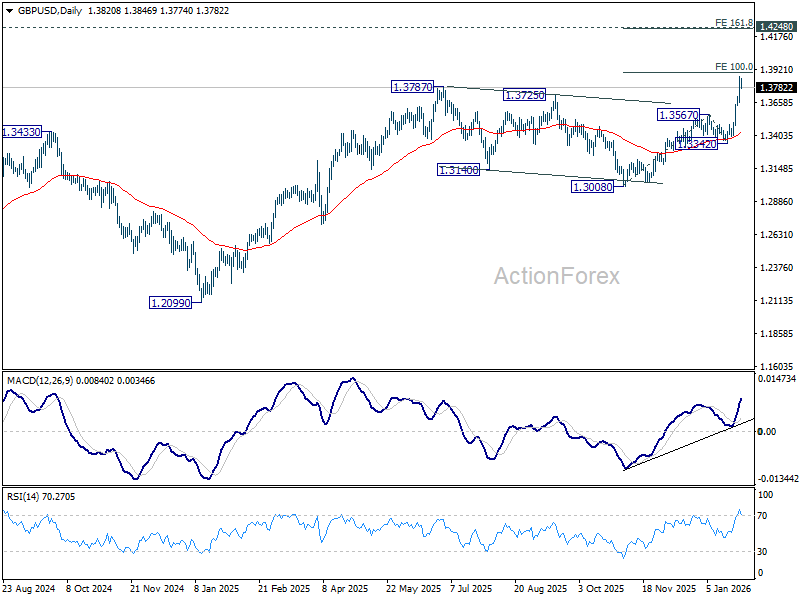

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3719; (P) 1.3794; (R1) 1.3923; More...

Intraday bias in GBP/USD remains on the upside for 100% projection of 1.3008 to 1.3567 from 1.3342 at 1.3901. Firm break there will pave the way to 161.8% projection at 1.4246, which is close to 1.4248 key structural resistance. On the downside, below 1.3712 minor support will turn intraday bias neutral again first. But retreat should be contained by 1.3567 resistance turned support to bring another rally.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

EUR/USD Updates Four-Year High: Everything Works Against the US Dollar

EUR/USD reached 1.2000 on Wednesday after rising to 1.2082 the previous evening, marking a strong four-day rally. The pressure on the US dollar has intensified following comments from US President Donald Trump. He stated that he was not concerned about the weakening of the dollar, viewing its fall as moderate. The market interpreted this as a signal that the administration might be willing to tolerate a weaker dollar to enhance export competitiveness.

An additional blow to the dollar came from rising political uncertainty in Washington, with Trump making fresh statements about Greenland and continuing to criticise the US Federal Reserve’s independence.

Further compounding the dollar’s decline is growing speculation about a potential joint US-Japan currency intervention to support the yen, which has boosted demand for JPY.

Investors’ focus is on the Federal Reserve’s decision, due later tonight. The Fed is widely expected to maintain its current interest rate, but much attention is on potential signals regarding the timing of future rate cuts. Current expectations suggest two 25-basis-point cuts by the end of the year.

Technical Analysis

On the H4 chart, EUR/USD has formed an upward wave towards 1.2080. A breakout above this resistance level would signal a continuation of the bullish trend. For now, the pair is in a corrective phase, with support around 1.1935. The correction is confirmed by the MACD indicator, which shows the histogram and signal line above zero and forming a downward wave. After the correction, the upward trend may resume towards 1.2100 and potentially 1.2200, though corrections could occur during the rise.

On the H1 chart, after testing resistance, EUR/USD is forming a correction. A rebound from support at 1.1935 would signal a continuation of the bullish wave. The Stochastic indicator’s signal lines are approaching the 20 level, suggesting that the correction may continue before resuming the upward trend. The next target for growth could be 1.2100.

Conclusion

The EUR/USD pair continues to show bullish momentum, supported by a weaker US dollar and rising geopolitical tensions. The ongoing correction might offer buying opportunities, with further growth likely towards 1.2100 and 1.2200, depending on the Fed's upcoming decision and global market dynamics.

EUR/USD Climbs Above 1.2000 After Trump’s Remarks

Expectations of lower Federal Reserve interest rates, recession risks, and the negative fallout from the US stance on Greenland have been among the factors acting as bearish drivers for the dollar in recent weeks.

Additional pressure came from signals that the US may be willing to sell dollars to help Japan strengthen the yen. Yesterday’s comments from Donald Trump then gave the market fresh momentum.

“The dollar is doing great,” Trump replied when asked by a reporter whether he thought it had fallen too sharply recently. Does this mean the president is comfortable with the national currency having lost around 9% during the first year of his term?

Trump’s words triggered a sharp weakening of the US dollar against other currencies. In particular, EUR/USD rose above the psychological 1.2000 level for the first time since 2021.

Technical Analysis of the EUR/USD chart

EUR/USD price action towards the end of January formed an ascending channel, within which the upper boundary is acting as resistance.

→ As shown by the first arrow, a long upper wick appeared on the hourly candle, signalling increased selling pressure.

→ The second arrow highlights a similar candle, providing further evidence of seller activity.

The RSI indicator has remained above the 50 level in recent days, confirming the bullish bias, while at the same time creating conditions for a potential pullback.

Should a correction occur, it would allow the channel’s median line to act as support — a level that previously functioned as resistance before being broken.

Given the rapidly shifting news backdrop and frequent comments from officials, further spikes in volatility across currency markets cannot be ruled out.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.