Sample Category Title

USD/JPY Drops Below 155.00: Has 2025 Yearly Top Been Reached?

After two months of a relentless rout in the Yen, the Japanese currency is finally finding some stable ground.

The core of the current reversal lies in the clash between the administration’s fiscal policy and the central bank’s monetary response: fiscal recklessness has finally been met with monetary soundness.

Prime Minister Takaichi has been pushing to implement massive stimulus packages, while also pressuring the Bank of Japan to keep rates low to support these projects.

Still, Markets don't get by the "cheap money" concept, which has led to a precipitous 5% to 8% move in the JPY against most majors since the beginning of October.

To balance things out, a round of increasingly hawkish tones from Bank of Japan Governor Kazuo Ueda has reversed the course over the past few weeks, winning his first showdown against Takaichi – as provided by a Reuters Headline.

Ueda confirmed overnight that current policy remains "accommodative" even after recent adjustments, underscoring the necessity of a planned exit from ultra-loose policy – The next BoJ Meeting is on December 19.

The Central Bank is actively working to narrow its estimate of the neutral rate (the level that is neither stimulative nor restrictive).

This rhetoric has created a strong market expectation for a December rate hike, supplemented by strong Japanese Inflation reports.

Complemented by some renewed weakness in the US Dollar, the Yen’s resurgence has led to a top being found in USD/JPY, which has plunged more than 2% off its November highs.

Let's examine the charts to see if technicals suggest a definite top or a temporary resistance.

USD/JPY Multi-Timeframe Analysis

Daily Chart

USD/JPY Daily Chart. December 4, 2025 – Source: TradingView

Since the change in tone from the Bank of Japan, the sky-high prices have been rejected in a daily tight bear channel formation (Where no green candle overlaps the preceding red bar – A sign of seller strength).

Falling 3,000 pips from its highs, the pair has broken below the key 155.00 psychological level but remains above its Daily Pivot Zone, decisive for long-term bull/bear strength.

Looking at the Daily RSI, it's currently crossing the neutral zone which confirms the shift in trend but isn't yet in bearish territory.

Traders will have to consider tomorrow's US Core PCE release, but barring any major crazy beat, the path for USD/JPY is towards some downside.

4H Chart and Technical Levels

USD/JPY 4H Chart. December 4, 2025 – Source: TradingView

USD/JPY technical levels of interest:

Support Levels:

- Session Lows 154.50 and Short-timeframe support

- 153.00 to 154.00 Key Resistance now Pivot

- 50-Day MA 153.00

- 150.00 Psychological Support and 50-Week MA

- 146.00 August Range Main Support

Resistance Levels:

- December 1 highs 156.15 (short-term resistance – 156.00 to 156.30)

- 156.90 to 157.95 recent peak resistance

- 2025 Highs and April 2024 peaks 158.80 to 160.00

- 1990 and July 2024 Peak 161.00 to 162.00

1H Chart

USD/JPY 1H Chart. December 4, 2025 – Source: TradingView

Looking closer to the 1H Timeframe, we spot prices evolving within a downward channel and remaining below the two key 50 and 200-period Moving Averages, the intermediate trend is bearish.

Still, the corrective move may have reached a temporary bottom with the RSI reaching oversold and a rebound attempt is ongoing.

For interesting levels to join the trend, monitor two levels:

Reactions at 155.00 (+/- 100 pips) to spot if the level attract further movement towards the channel lows

On further mean-reversion higher, look at 155.40 which is the 50-H Moving average.

For bulls, look at a break and close above the channel (155.50)

Expect traders to wait for Core PCE for decisive moves.

Safe Trades!

Sunset Market Commentary

Markets

FI, once again, is where most of the market attention went to today. It originated, once again, from Japan where a more than solid demand for a 30-yr JGB auction failed to prevent yields rising in maturities up to 20 year. A Reuters report that the Takaichi government is said to tolerate a BoJ rate hike this month added a little fuel to the fire. Such a move still isn’t fully discounted even though the stars are aligning. The market implied probability did rise from <60% on Friday to 80% in recent days on BoJ governor Ueda’s speech on Monday and further to 89% today. Japan’s 10-year yield hit the highest level since 2007 at 1.94%. The closely watched reference is now 6 bps away from the pre-GFC highs. The Japanese yield situation warrants close monitoring with higher local yields pulling back or keeping capital at home (reversing the long-popular carry trade). Less huge (foreign) buyer of particularly long term bonds – next to central banks and traditional buyers such as pension funds and life insurers – comes at a tricky time when huge supply (government deficits) is already competing for demand. JGBs reaffirmed their importance for global bond markets by dragging Bunds and Treasuries down with them. US yields today add between 2 and 3.5 bps. The front-to-middle segment underperforms marginally following a steep drop in US jobless claims. The 219k reading was the lowest since September 2022. The holiday-shortened week ending Nov 29 came with some Thanksgiving-related distortions that some say help explain the low reading. It won’t alter the Fed’s intentions for next week though. German yields add 0.5-2 bps across the curve. Bunds underperform vs swap with market chatter growing about a potential demise of Merz’ seven months old government. A group of Merz’ own CDU lawmakers rebelled against a pension bill. The 18 that did effectively exceed the CDU/SPD’s majority of 12. Should the group continue to do so in tomorrow’s final vote and the Left party does not abstains (as they said they would), the SPD co-leader Bas said earlier this week it could spell the end of the coalition. New elections according to the polls would favour the extremes, the far right in particular. It wouldn’t come at a worse time after French politics this week also rearing its head again when coalition partner Les Horizons said it wouldn’t support the social security budget bill in December 9’s vote. French OAT/swap spreads have been trending higher all week and trade back above Italy’s. The euro doesn’t want to frontrun any German or French political upheaval for now with EUR/USD holding steady around a 1.5 month high of 1.167 but it’s a tense situation. JPY outperforms, pushing USD/JPY back below 155 for a second time this week. EUR/JPY is also down on the day but remains near the record highs north of 180.

News & Views

Czech inflation unexpectedly fell by 0.3% M/M in November (+0.1% consensus), bringing the annual number down to 2.1% Y/Y instead of the expected stabilization at 2.5%. Gauges for core inflation slowed from 3.2%/3.3% Y/Y to 2.9%/3% Y/Y. Details showed steep drops in goods (-0.6% M/M and +0.6% Y/Y from 1.3%) and food prices (-0.8% M/M & +2.8% Y/Y from 3.9%). Within food subcategories, it were processed food, alcohol & tobacco prices that fell while unprocessed food prices still increased (+0.8% M/M & +1.9% Y/Y from 3.3%). Energy prices were 0.1% lower compared with October and 3.8% lower versus November of last year. Services inflation (+0.1% M/M) held steady at 4.6% Y/Y. The Czech Statistical Office also released Q3 wage data today. Nominal wages increased by 7.1% Y/Y (from +7.6% Y/Y in Q2) with real wage growth coming in at 4.5% Y/Y (from 5.1% Y/Y in Q2), almost matching expectations (+4.6%). The Czech koruna lost ground after inflation numbers with EUR/CZK rising from 24.10 to 24.22. CZK swap yields lose 7 to 9 bps across the curve in a slight bull steepening move.

The Bank of England’s Decision Maker Panel (DMP) survey showed stable price and wage growth metrics at firms in November. Year-ahead and three-year-ahead CPI inflation expectations were unchanged at 3.4% and 3% respectively. Realized annual own-price growth and realized annual wage growth remained steady as well, at 3.8% and 4.5%. Both year-ahead measures increased by 0.1pp compared with October to 3.7% and 3.8%. Employment is contracting with realized and year ahead employment growth falling by 0.7% and 0.2% respectively. The profit margin outlook is mixed, with equal shares expecting improvement or stability (both 38%) next year.

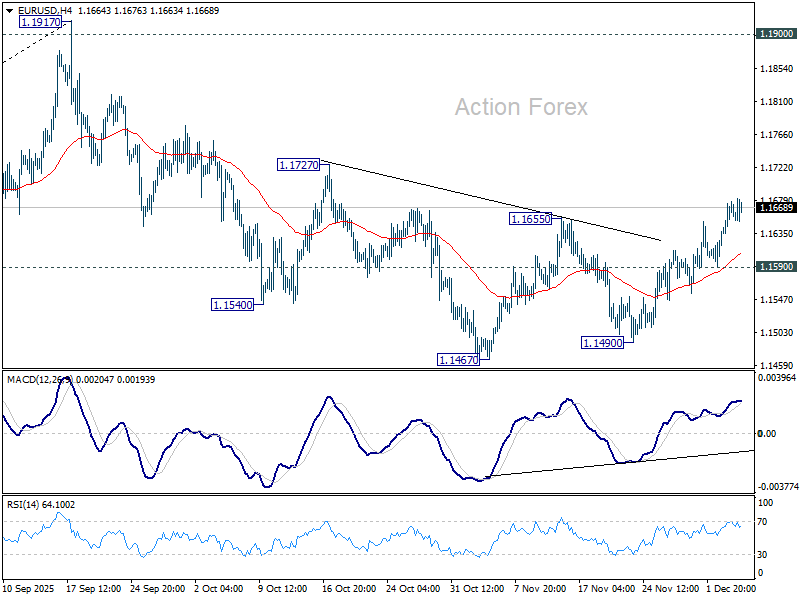

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1635; (P) 1.1657; (R1) 1.1692; More….

Intraday bias in EUR/USD remains on the upside at this point. Fall from 1.1917 should have completed at 1.1467. Further rise should be seen to 1.1727 resistance first. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

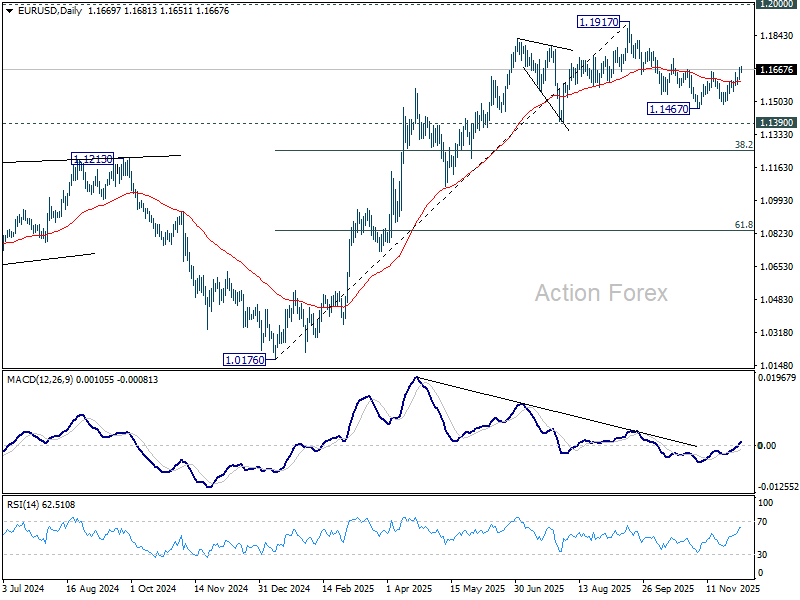

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

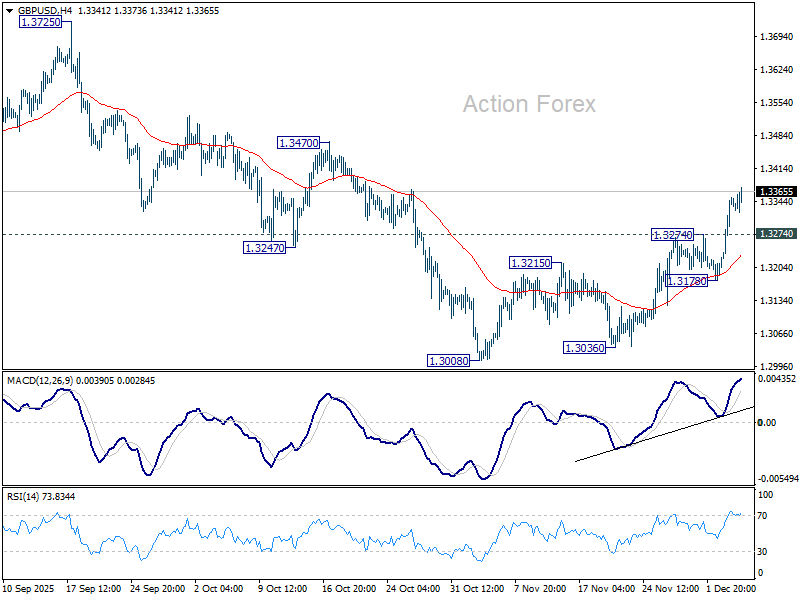

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3250; (P) 1.3303; (R1) 1.3405; More...

Intraday bias in GBP/USD remains on the upside for the moment. Fall from 1.3787 could have completed as a correction at 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3725/3787 resistance zone. On the downside, below 1.3274 resistance turned support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3718 support holds, in case of retreat.

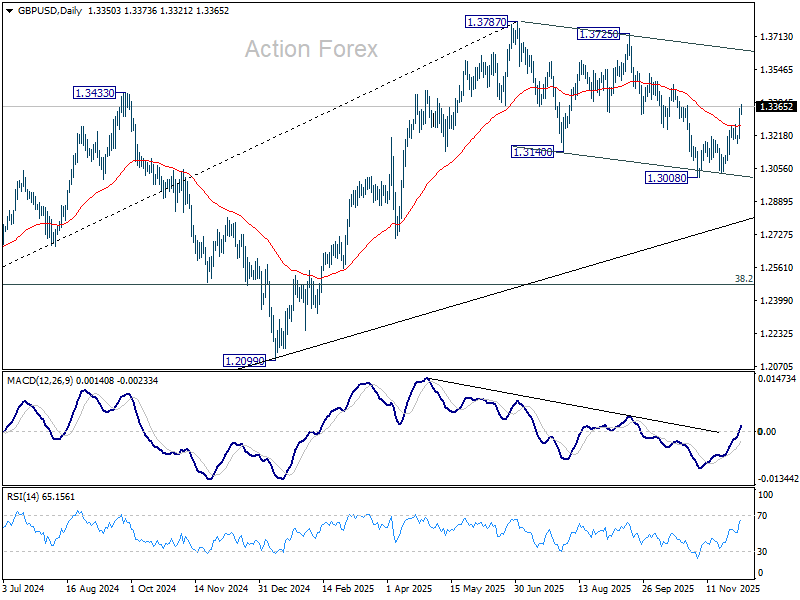

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

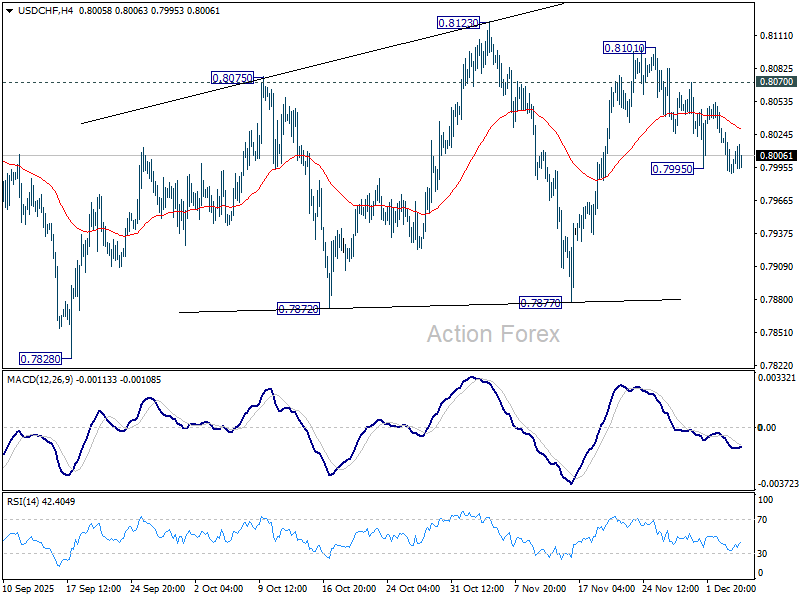

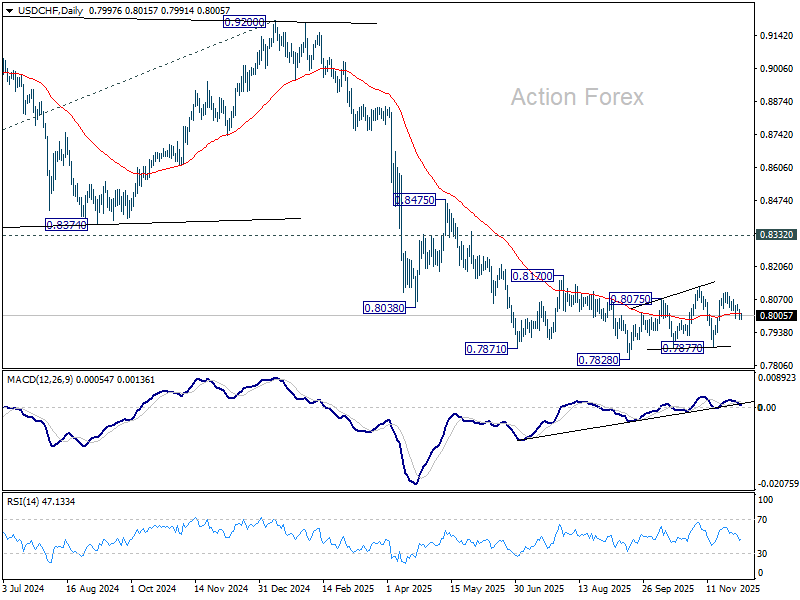

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7978; (P) 0.8010; (R1) 0.8028; More…

No change in USD/CHF's outlook and intraday bias stays neutral. Price actions from 0.7828 low is seen are a corrective pattern. On the upside, above 0.8070 will indicate that pattern is still extending, and turn bias back to the upside for 0.8123 and above. On the downside, below 0.7995 will bring deeper fall back towards 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.85; (P) 155.39; (R1) 155.77; More...

Intraday bias in USD/JPY remains neutral at this point. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.13), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

Muted Reaction to Strong US Claims; Japan’s Bond Markets Flash Caution

Global markets have steadied heading into US session, with equity futures pointing to a flat open after yesterday’s strong rally. Early optimism from Japan and Europe faded through the day, leaving investors cautious but not materially risk-off. The backdrop is one of consolidation rather than clear direction.

US jobless claims delivered a notable surprise, falling to their lowest level in more than three years. Yet market reactions were muted, reflecting scepticism that a single data point signals a genuine improvement in labor market momentum. With Fed funds futures still assigning nearly 90% probability to another 25bp “risk-management” cut next week, the report has not shifted the policy narrative.

Still, the data serve as a reminder that US labor conditions may stabilize as trade uncertainty eases. The extension of the US–China tariff truce in November for another year helps reduce one of the key macro headwinds that has weighed on business sentiment. If conditions continue to firm, both President Donald Trump and his expected Fed Chair pick, Kevin Hassett, may find it harder to justify aggressive, politically driven easing unless the data cooperate.

A separate but increasingly important development sits in Japan, where the 10-year JGB yield surged to 1.941%, its highest close since 2007. Rising yields translate into sharply higher government borrowing costs at a time when Prime Minister Sanae Takaichi is rolling out a massive stimulus package to offset cost-of-living pressures and support growth. Fiscal strains are likely to intensify if yields continue rising.

For the BoJ, the situation complicates an already delicate policy transition. Move too quickly, and the Bank risks pushing yields even higher, deepening fiscal stress. Move too slowly, and inflation pressures may re-accelerate. The policy dilemma is tightening, with global markets increasingly sensitive to how Governor Kazuo Ueda balances these conflicting risks.

Another concern is the narrowing Japan–US yield gap, which reduces the appeal of Yen-funded carry trades. A sudden reversal in Yen weakness could force a broader risk unwind, particularly among leveraged positions that have benefited from ultra-low JPY funding costs. The JGB move is therefore more than a local story—it is a potential global risk event.

Across the currency markets this week, Dollar remains anchored at the bottom of the performance ladder, with no signs of recovery. Loonie and Swiss Franc follow as the next weakest. On the stronger side, Yen leads with help from bond-market repricing, followed by Aussie and Sterling, while Euro and Kiwi sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.90%. CAC is up 0.53%. UK 10-year yield is down -0.011 at 4.440. Germany 10-year yield is up 0.023 at 2.773. Earlier in Asia, Nikkei rose 2.33%. Hong Kong HSI rose 0.68%. China Shanghai SSE fell -0.06%. Singapore Strait Times fell -0.43%. Japan 10-year JGB yield rose 0.046 to 1.941.

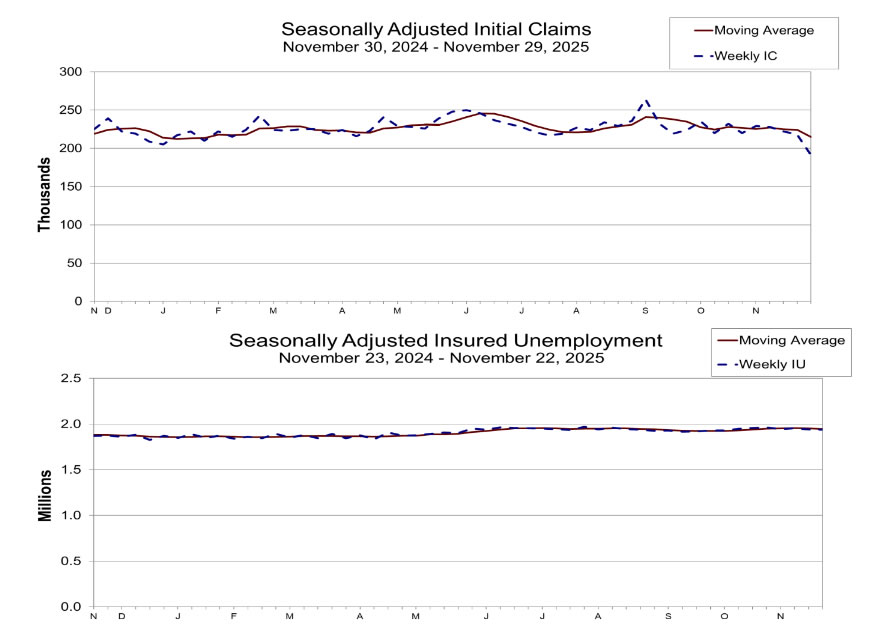

US jobless claims fall sharply to 191k, lowest since 2022

US initial jobless claims fell sharply by -27k to 191k in the week ending November 29, far below expectations of 220k, and marking the lowest level since September 2022. The four-week moving average also by -9k eased to 215k.

Continuing claims slipped modestly by -4k to 1.939 million in the week ending November 22. Their four-week average edging down by -6k to 1.945 million, indicating some stabilization after earlier signs of softening.

The data stand in contrast to the recent deterioration seen in other labor indicators, including the weak ADP report, and highlight ongoing tightness in the job market despite clear signs of cooling elsewhere.

Eurozone retail sales stall in October as non-food demand softens

Eurozone retail sales were unchanged on the month in October, matching expectations and highlighting a subdued consumer environment heading into year-end. Category-level data showed mixed trends: spending on food, drinks and tobacco rose 0.3% mom, while non-food products (excluding fuel) fell -0.2% mom. Automotive fuel sales increased 0.3% mom, helping offset weakness elsewhere but not enough to lift the overall index.

Retail activity across the wider EU was also flat on the month, reinforcing the picture of stagnation in household consumption. The divergence among member states remained notable. Luxembourg posted the strongest monthly gain at 3.6% mom, followed by Estonia (1.7%) and Croatia (1.4). In contrast, Belgium saw a sharp -1.3% drop, with Austria (-0.6%), Ireland (-0.4%) and Sweden (-0.4%) also reporting declines.

BoJ’s Ueda: Neutral rate uncertainty keeps BoJ guessing how far to tighten

BoJ Governor Kazuo Ueda told lawmakers today that Japan’s neutral interest rate remains highly uncertain, describing it as a concept that can only be estimated within a “quite wide range.” He noted that the central bank is attempting to narrow that range and may disclose updated estimates once confidence improves.

Ueda added that the lack of clarity around the neutral rate means the BoJ must operate without a firm sense of how much tightening is ultimately appropriate. This ambiguity, he said, leaves uncertainty around “how far we should raise interest rates,” even as policymakers consider more conventional policy settings after years of ultra-accommodation. Current BoJ estimates place the nominal neutral rate between 1% and 2.5%.

His comments come days after signaling that the BoJ will weigh the “pros and cons” of a rate hike at the upcoming December meeting, a remark markets interpreted as the strongest indication yet that a move to 0.75% is under consideration.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.85; (P) 155.39; (R1) 155.77; More...

Intraday bias in USD/JPY remains neutral at this point. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.13), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

US jobless claims fall sharply to 191k, lowest since 2022

US initial jobless claims fell sharply by -27k to 191k in the week ending November 29, far below expectations of 220k, and marking the lowest level since September 2022. The four-week moving average also by -9k eased to 215k.

Continuing claims slipped modestly by -4k to 1.939 million in the week ending November 22. Their four-week average edging down by -6k to 1.945 million, indicating some stabilization after earlier signs of softening.

The data stand in contrast to the recent deterioration seen in other labor indicators, including the weak ADP report, and highlight ongoing tightness in the job market despite clear signs of cooling elsewhere.

EUR/USD Pair Reaches 1.5-Month High

This morning, the EUR/USD rate moved above 1.1680 during early trading — its highest level since mid-October. The main driver behind the rise is traders’ assessment of the diverging policies of central banks. Based on the fundamental outlook ahead of the December meetings:

→ The market is almost certain that the Federal Reserve will cut rates in December under pressure from the Trump administration, making the dollar appear less profitable and less attractive.

→ The ECB, by contrast, has adopted a wait-and-see stance. Inflation in the Eurozone is close to target, and there seems to be no intention to cut rates aggressively for now.

Technical Analysis of the EUR/USD Chart

In November, the pair formed a broad balance zone:

→ The 1.1500 level acted as support — the price dipped below it twice, but failed to hold beneath this psychological mark.

→ A downward sloping trendline (shown in red) served as resistance.

At the start of December, we see that price growth within the blue ascending channel has led to a bullish breakout above the red resistance line.

However, the chart suggests that the rally may now be losing momentum, because:

→ As the arrow indicates, this morning’s attempt to surpass yesterday’s high may result in a candle with a long upper wick.

→ RSI conditions point to a possible bearish divergence between price highs A and B.

It is possible that the EUR/USD rise to a 1.5-month high could attract sellers — therefore, forex traders should not rule out a pullback towards the lower boundary of the blue channel. A retest from above of the red line is also possible.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Euro Gaining Momentum

- Inflation and the US labour market are slowing down, while the chances of a rate cut are increasing.

- The US dollar is vulnerable, while the euro is being helped by business activity.

The US dollar had its worst series of daily declines since 2020, mainly due to the increased likelihood of an interest rate cut by the Fed and the improved positions of its main competitors. The pound is rising as fears about the budget have been allayed. The yen and the Australian dollar are awaiting interest rate hikes by their respective central banks. The euro is rising due to improved trade conditions, falling energy prices and hopes for peace in Eastern Europe. The USD index is further weakened by demand for hedging in anticipation of the Christmas rally in US stock indices.

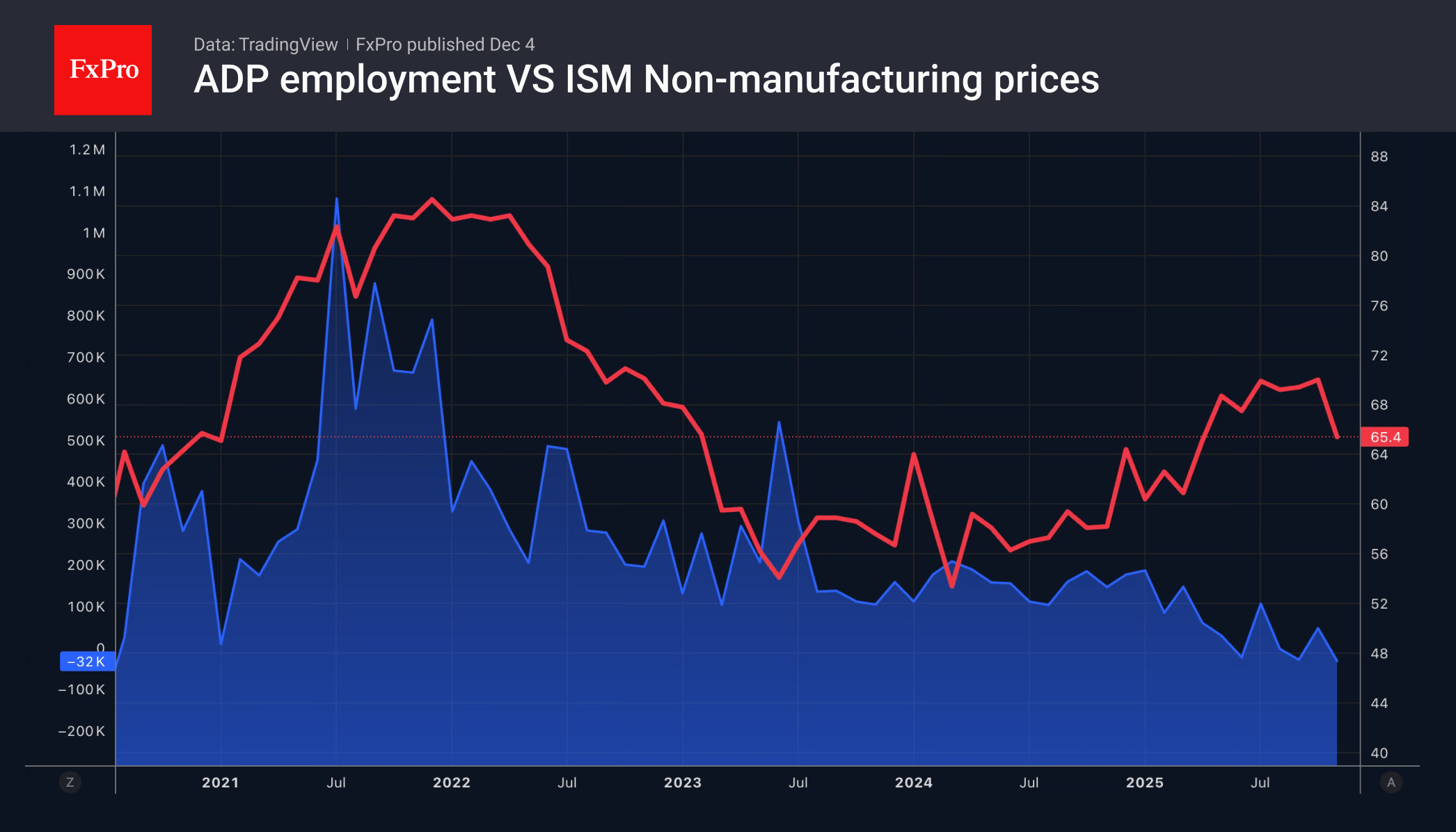

A decline in private sector employment by 32K in November, according to ADP, and a fall in the price component of the PMI in the services sector to a 7-month low have strengthened the position of speculators betting on a decline in December. Doves at the Fed believe it is better to play it safe and ease policy to prevent an uncontrolled surge in unemployment. Hawks complain that lowering rates will accelerate inflation, which is already gaining momentum.

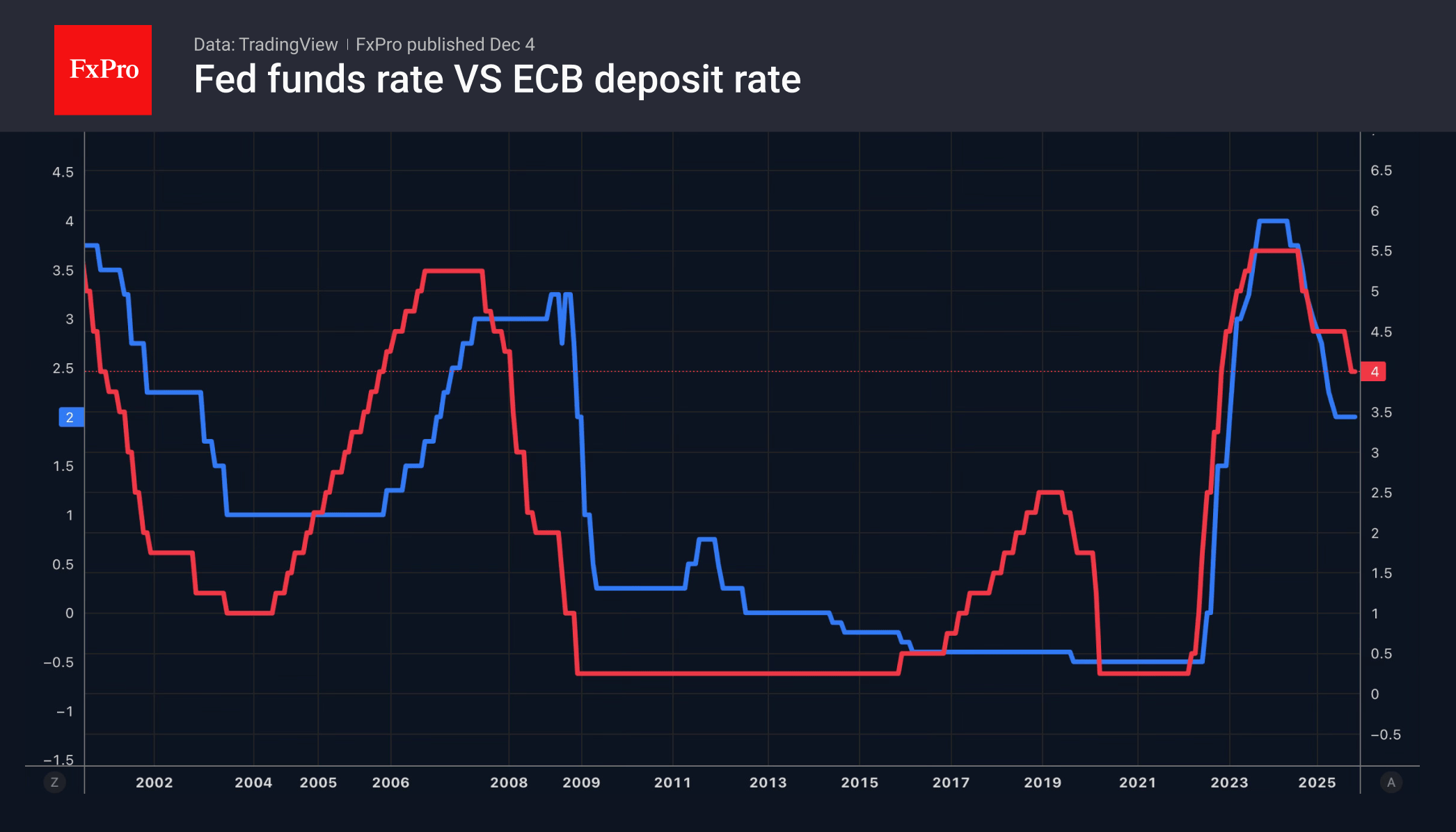

The arguments of the first group of FOMC officials seem more convincing, which is why the futures market assigns a 89% probability of a 25-point cut on December 10th and approximately a 50% chance of a 100-point cut within a year. Since no further reductions are expected from the ECB in the coming year, the market is re-evaluating in favour of EURUSD growth.

Moreover, even without divergence in monetary policy, the US dollar has many vulnerabilities. The potential repeal of tariffs by the Supreme Court, the twin deficits in the budget and trade balance, and faster economic growth outside the US are all factors in favour of a further decline in the USD index.

The euro, on the contrary, draws strength from the remarkable stability of the eurozone. In November, the composite business activity index rose to its highest level in 2.5 years, adding to its sixth consecutive month of growth. Its positive dynamics give hope for a reduction in the economic growth divergence with the US. Along with the divergence in monetary policy between the ECB and the Fed, the economy is driving the upward trend in EURUSD.