Sample Category Title

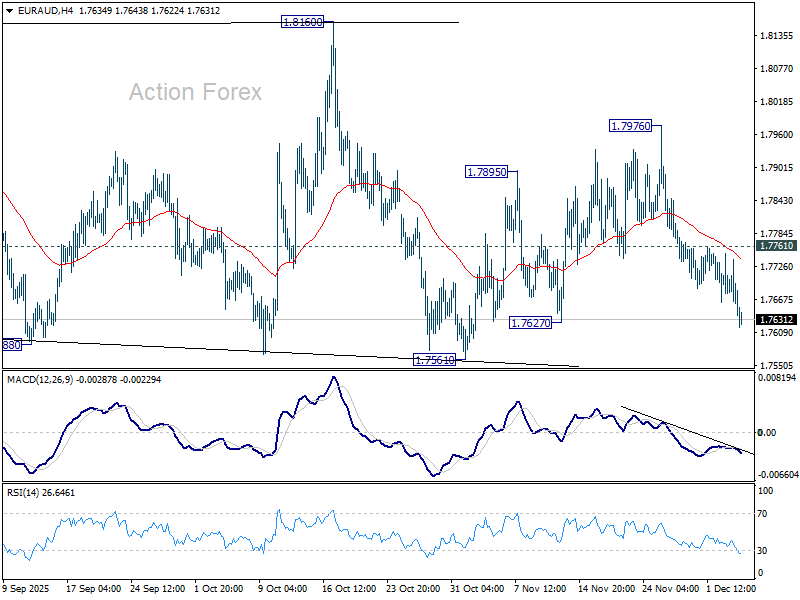

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7647; (P) 1.7699; (R1) 1.7731; More...

EUR/AUD's fall from 1.7976 is in progress today and intraday bias stays on the downside for 1.7561 support. Firm break there should confirm that larger corrective pattern from 1.8554 is already in the third leg. Deeper decline should then be seen to 1.7245 support next. For now, risk will stay on the downside as long as 1.7794 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7426) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

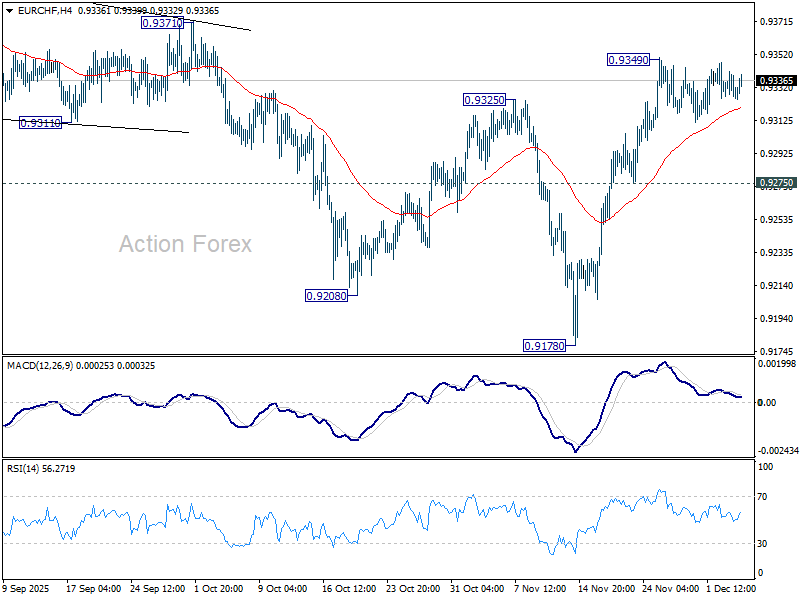

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9325; (P) 0.9335; (R1) 0.9341; More....

EUR/CHF is still bounded in consolidations below 0.9349 and intraday bias stays neutral. As noted before, fall from 0.9660 could have completed at 0.9178, on bullish convergence condition in D MACD. Above 0.9349 will resume the rise from 0.9178, and target 0.9452 resistance next. However, break of 0.9275 will turn bias back to the downside for 0.9178 low instead.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9371). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

Japan’s 30-Year Bond Auction Drew Strongest Demand Since 2019

Markets

US economic data yesterday all but cemented next week’s Fed rate cut expectations. The ADP job report unexpectedly showed a 32k job loss – the second worst reading since June 2020 – and wage growth cooling. But while a further rate reduction to 3.5-3.75% may be a done deal, the bigger question remains what the next move(s) will be. Yesterday’s services ISM in any case argues against going full force. The prices paid gauge fell to a seven-month low but remains historically elevated. Activity rose to a three-month high of 54.5, helping lift the headline index to 52.6. New orders growth fell compared to last month but continued to expand nevertheless (52.9). The employment series remained sub 50 but showed signs of stabilizing. The ISM chair concluded that the November edition had “positive signs of an emerging recovery for the services sector”. It lifted US yields, particularly at the front end, off their intraday lows. Net daily changes varied between -1.5 and -2.6 bps in a bull steepener. European rates hovered sideways in directionless trading. Interest rate differentials along with a modest constructive risk environment gave the euro an edge over the dollar. EUR/USD rose to 1.1671, the highest in over a month. DXY dropped below the 99 barrier. Sterling had a nice bull run, supported amongst others by upwardly revised final PMIs to 51.2. EUR/GBP slid to 0.874. GBP/USD jumped to well north of 1.33.

Japan’s 30-year bond auction stood at the center of attention in Asian dealings this morning. It drew the strongest demand since 2019, profiting from the recent yield uptick to new (record) highs. While the ultralong end of the Japanese curve enjoys some bids as a result, maturities up to 20 year still eke out several basis points. The 10-yr tenor rose to the highest level since 2007. It’s keeping the rest of global peers (Treasuries, Bund futures) under pressure as well. The steepening could be tied to increased rate cut bets by the Fed. That helps explain the solid (Japanese) stock performance. European stock futures also suggest a higher open of around 0.5-0.6%. It’s a small step, though, for markets to redirect the focus to public finances in a context of rising bond yields again. The economic calendar is pretty empty with only jobless claims in the US as worth mentioning. FX markets will be the playground of technically-savvy investors. EUR/USD currently snaps an 8-day winning streak.

News & Views

The National Bank of Poland cut its policy rate by another 25 bps yesterday to 4%, bringing this year’s total effort at 175 bps of policy easing. In a brief statement, the NBP pointed out that inflation annual inflation decline to 2.4% in November, below the 2.5% inflation target. The central bank removed a reference to elevated services inflation and pointed at a slowdown in wage growth. Recent strong growth is on the other side of the balance with domestic demand pushing the annual growth rate to 3.8% in Q3. NBP governor Glapinski holds a press conference this afternoon. Key talking point will be the remaining policy room towards a neutral interest rate level. Polish money markets put the floor currently at 3.5%. Yesterday’s NBP statement indicates that further decisions will depend on incoming data. Fiscal policy, recovery of demand in the economy as well as developments in wage growth, energy prices and inflation abroad remain risk factors for the Polish inflation outlook. EUR/PLN remains stuck in the extremely narrow 4.22-4.30 trading range in place since mid-April.

Hungarian PM Orban announced this morning that the country will lift the minimum wage by 11% after an agreement between the government, employers and trade unions. It’s less than the previously agreed 13% with disappointing economic growth triggering the revision. Guaranteed minimum wages for positions requiring secondary education or vocational training will be raised by 7%.

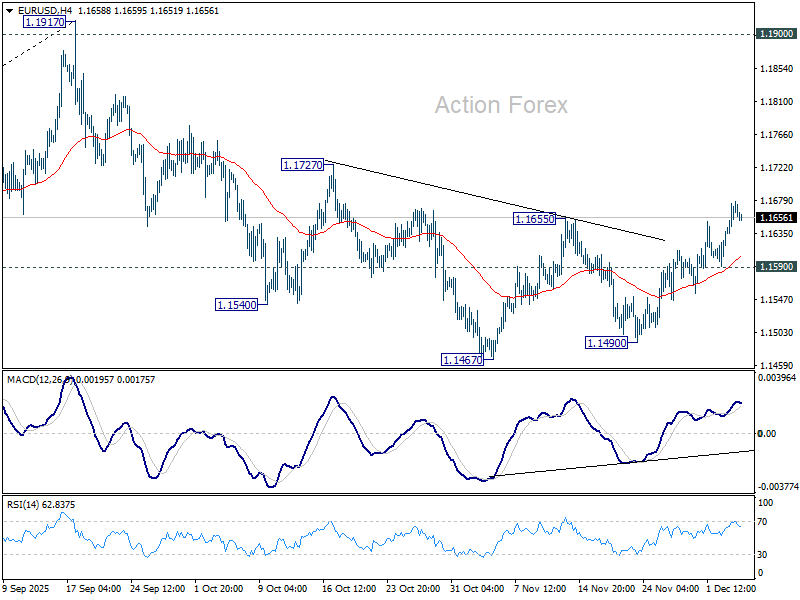

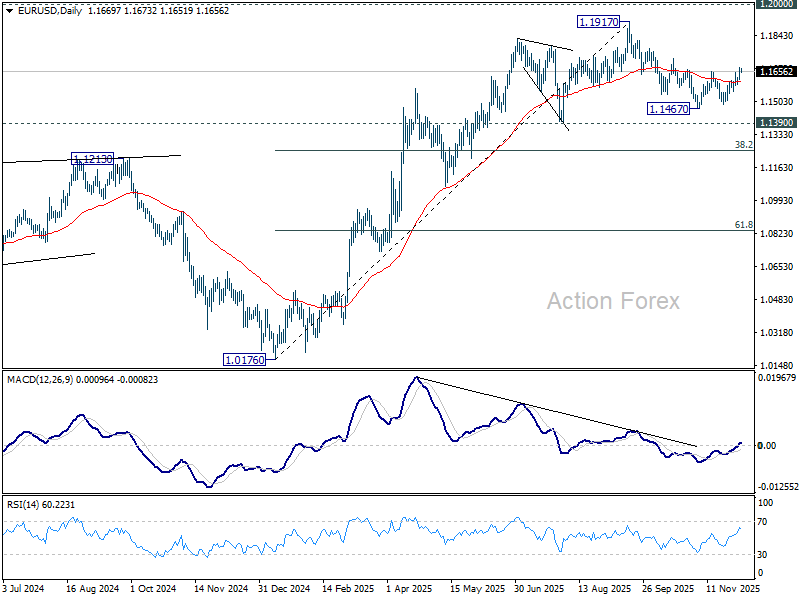

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1635; (P) 1.1657; (R1) 1.1692; More….

Intraday bias in EUR/USD remains on the upside for the moment. Fall from 1.1917 should have completed at 1.1467. Further rise should be seen to 1.1727 resistance first. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

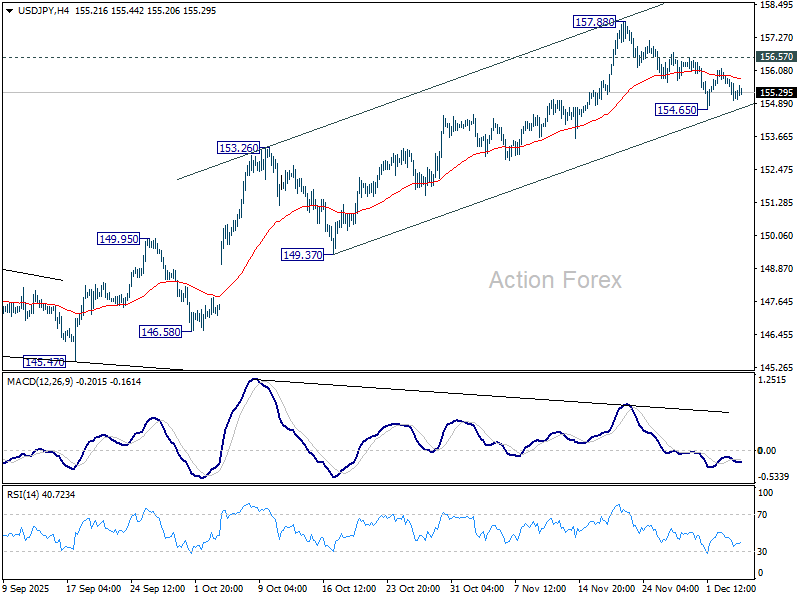

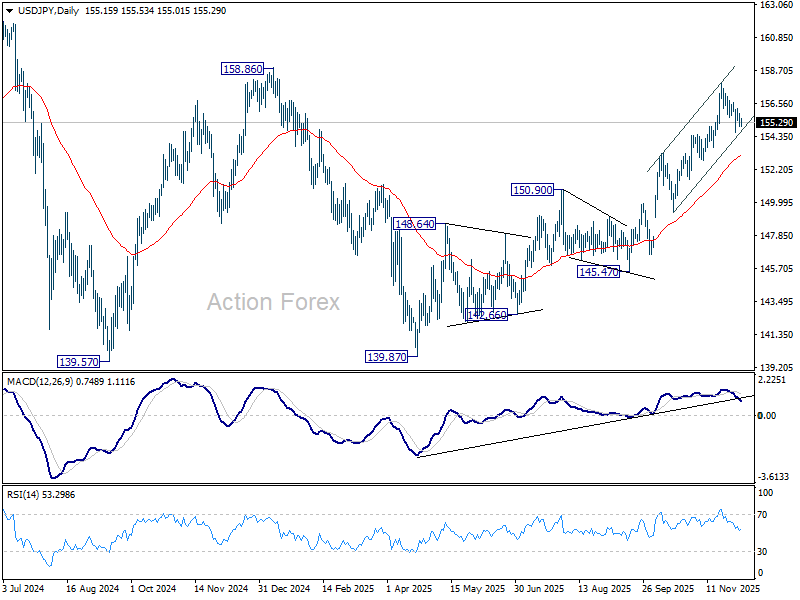

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.85; (P) 155.39; (R1) 155.77; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.13), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

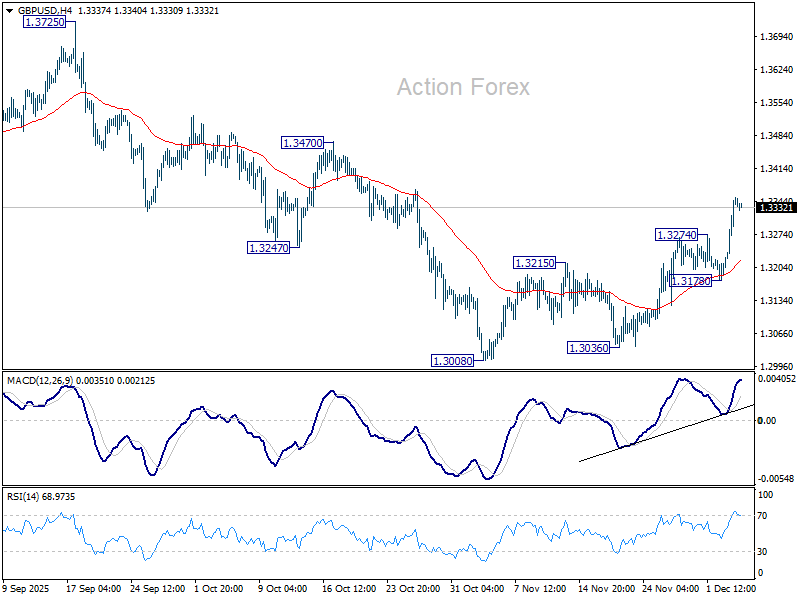

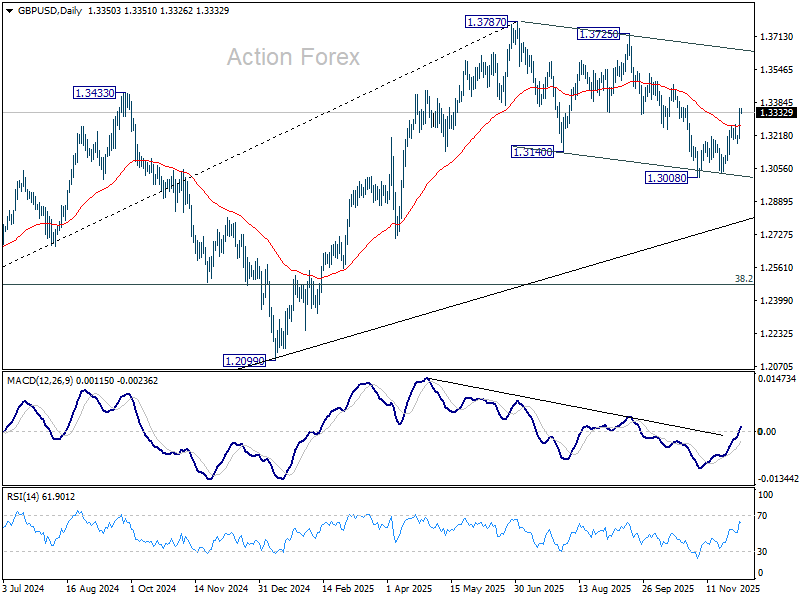

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3250; (P) 1.3303; (R1) 1.3405; More...

Intraday in GBP/USD stays on the upside for 1.3470 resistance. Fall from 1.3787 could have completed as a correction at 1.3008. Firm break of 1.3470 will pave the way to retest 1.3725/3787 resistance zone. For now, risk will stay on the upside as long as 1.3718 support holds, in case of retreat.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

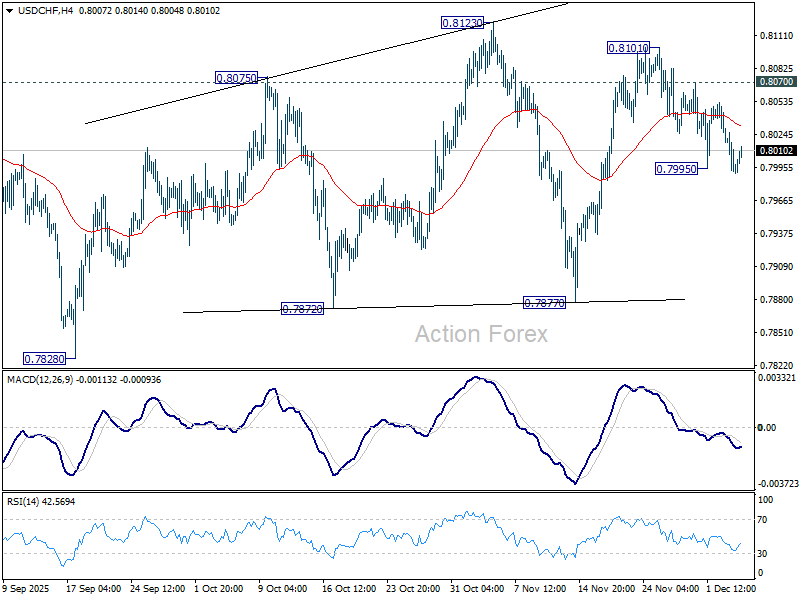

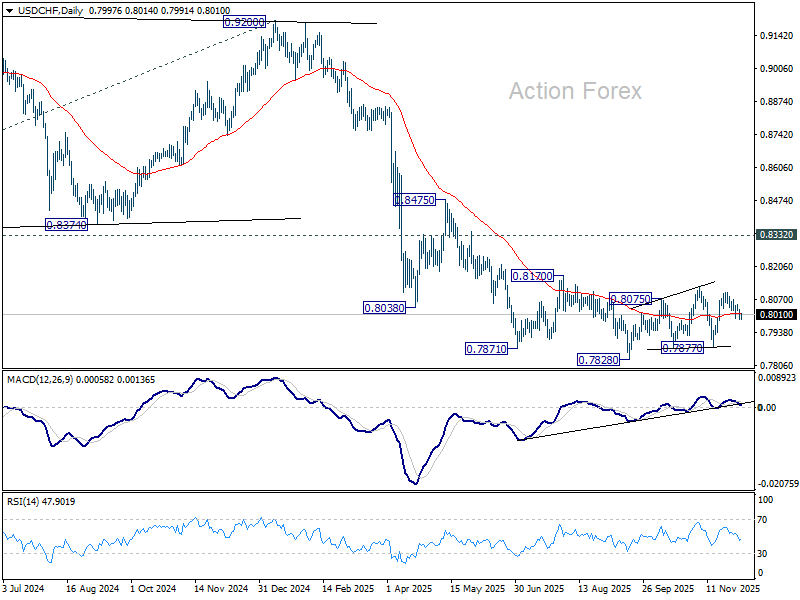

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7978; (P) 0.8010; (R1) 0.8028; More…

Intraday bias in USD/CHF remains neutral at this point. Outlook is unchanged that price actions from 0.7828 low is seen as a corrective pattern. On the upside, above 0.8070 will indicate that pattern is still extending, and turn bias back to the upside for 0.8123 and above. On the downside, below 0.7995 will bring deeper fall back towards 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

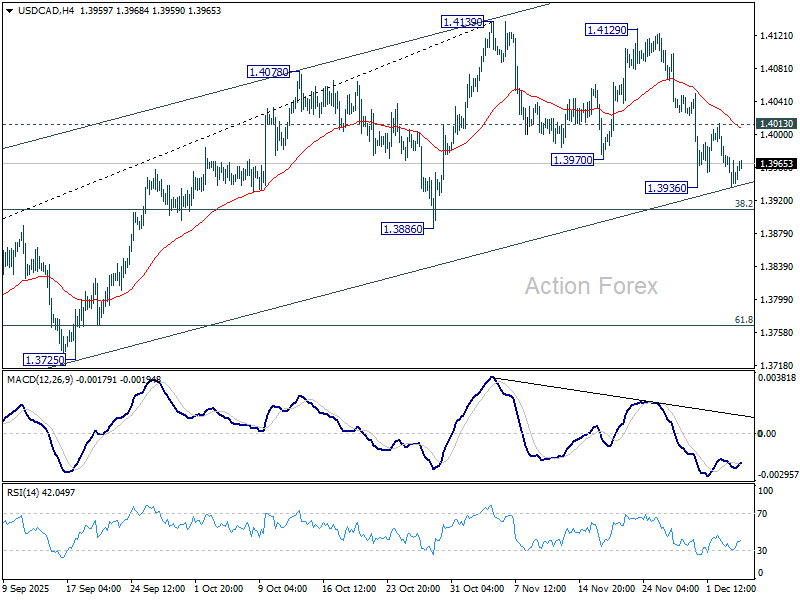

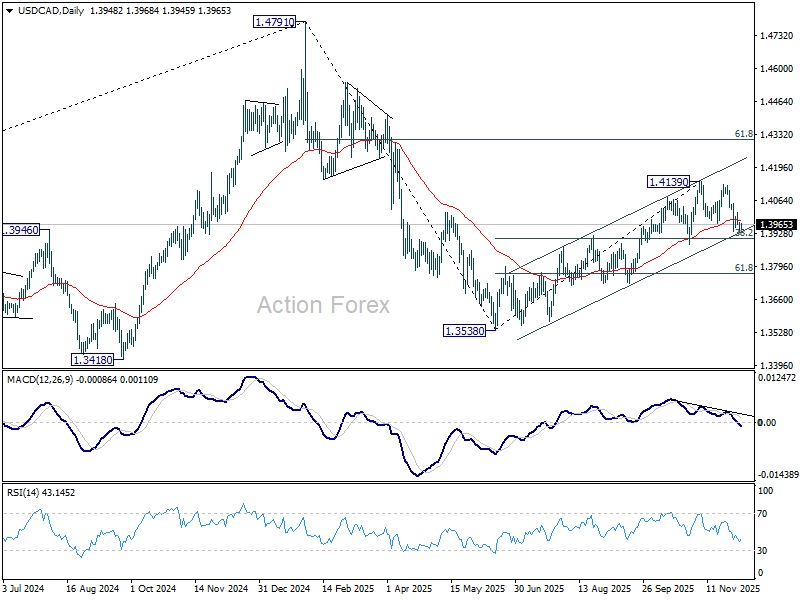

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3934; (P) 1.3955; (R1) 1.3972; More...

Intraday bias in USD/CAD stays neutral for the moment, and further fall remains in favor. Break of 1.3936 will target 38.2% retracement of 1.3538 to 1.4139 at 1.3909. Sustained break there will indicate that whole rise from 1.3538 has completed. Deeper fall should then be seen to 61.8% retracement at 1.3768 next. On the upside, though, break of 1.4013 resistance will retain near term bullishness, and bring retest of 1.4139 high.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

Dollar Stays Weak Despite Small Bounce; Hassett Concerns Add to Pressure

Dollar attempted a mild recovery in Asia today, but the uptick lacked conviction and failed to alter the broader picture of USD underperformance. The greenback remains the weakest major this week, with selling pressure intensifying after Wednesday’s sharp drop in ADP employment that reinforced concerns about labor-market deterioration.

Expectations for a 25bps Fed cut next week are now effectively locked in, with market pricing hovering near certainty. Friday’s PCE inflation release could matter in theory, but it won't meaningfully shift expectations or dissuade the Fed from delivering the December cut. Instead, attention is turning to what comes next, with November’s NFP and CPI—both arriving after the FOMC—likely to guide the early-2026 policy path.

A key emerging theme is political uncertainty around the Fed. Reports indicate that Kevin Hassett, President Trump’s top economic adviser, is being seriously considered as Powell’s successor. Hassett is well known for advocating lower interest rates and has supported Trump’s broader tariff and stimulus policies, raising questions about how independent the Fed’s next leadership might be.

The Financial Times reported that major bond investors have already voiced concerns to the Treasury over Hassett’s potential appointment. Several warned he may push for broad-based rate cuts even if inflation remains above the 2% target—raising fears of a more politically influenced Fed and a return to pro-cyclical policy. With Trump confirming he will announce his nominee early next year, the issue could become a market driver soon. While no decisive reaction has emerged yet, the next few weeks will be key in determining whether these fears become more fully priced into yields and USD positioning.

In the meantime, Dollar remains at the bottom of the weekly performance table, followed at a distance by Loonie and Swiss Franc. At the other end of the spectrum, Aussie thanks to hawkish RBA commentary, with Sterling and Kiwi close behind. Yen and Euro are sitting mid-pack, reflecting a broadly risk-on market tone that is helping higher-beta currencies outperform.

In Asia, Nikkei rose 2.33%. Hong Kong HSI rose 0.21%. China Shanghai SSE fell -0.04%. Singapore Strait Times fell -0.45%. Japan 10-year JGB yield rose 0.034 to 1.928, breaking above 1.9% mark. Overnight, DOW rose 0.86%. S&P 500 rose 0.30%. NASDAQ rose 0.17%. 10-year yield fell -0.029 to 4.057.

BoJ’s Ueda: Neutral rate uncertainty keeps BoJ guessing how far to tighten

BoJ Governor Kazuo Ueda told lawmakers today that Japan’s neutral interest rate remains highly uncertain, describing it as a concept that can only be estimated within a “quite wide range.” He noted that the central bank is attempting to narrow that range and may disclose updated estimates once confidence improves.

Ueda added that the lack of clarity around the neutral rate means the BoJ must operate without a firm sense of how much tightening is ultimately appropriate. This ambiguity, he said, leaves uncertainty around “how far we should raise interest rates,” even as policymakers consider more conventional policy settings after years of ultra-accommodation. Current BoJ estimates place the nominal neutral rate between 1% and 2.5%.

His comments come days after signaling that the BoJ will weigh the “pros and cons” of a rate hike at the upcoming December meeting, a remark markets interpreted as the strongest indication yet that a move to 0.75% is under consideration.

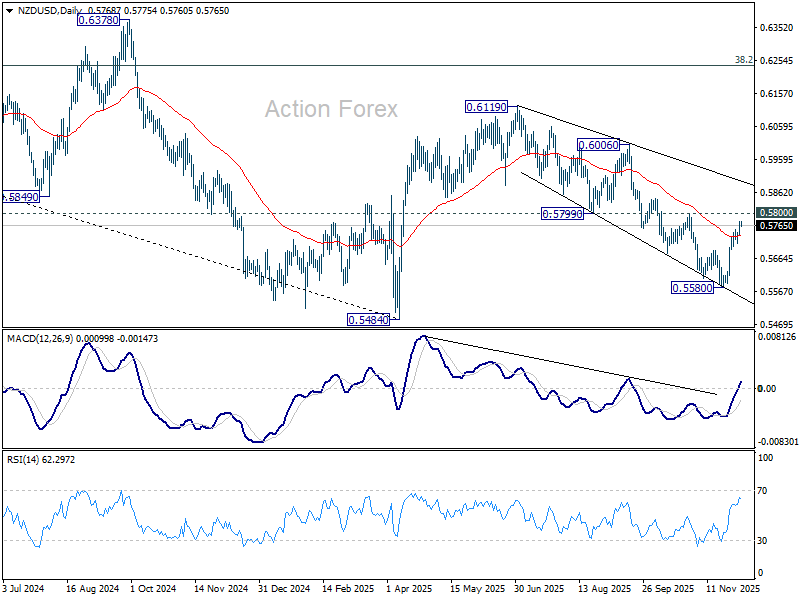

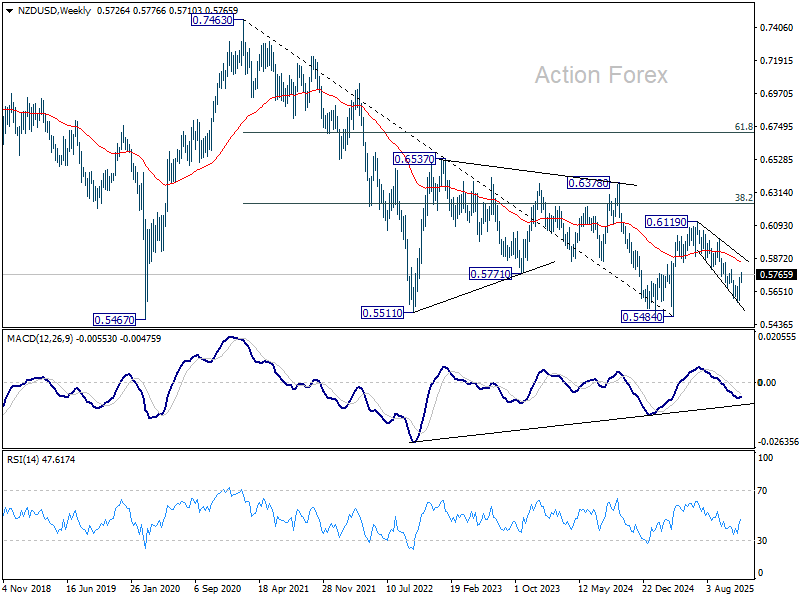

NZD/USD in bullish reversal? 0.5799 resistance holds key

NZD/USD extended its rebound from 0.5580 this week as the pair capitalized on a softer US Dollar, driven by the sharp deterioration in ADP employment data. The weak labor reading reinforced expectations of a December Fed rate cut, prompting another wave of USD selling across major pairs and giving the Kiwi room to advance. Underlying support also stems from the RBNZ’s hawkish cut last week, where policymakers signaled that the easing cycle has likely ended.

Technically, NZD/USD’s break above the 55 D EMA signals that the three-wave corrective decline from 0.6119 has likely completed at 0.5580. Momentum has clearly shifted to the upside, and the structure argues that the pair may now be in the early stages of a broader rally.

The next key hurdle is the 0.5799 support-turned-resistance. Sustained break above this level would further confirm bullish reversal and strengthen the view that the rise from 0.5580 represents the third leg of the larger pattern from 0.5484 low earlier this year.

That would also open the door through 0.6119 resistance, even if the advance from 0.5484 proves to be only a corrective rally within the broader downtrend from the 0.7463 (2021 high).

03

03

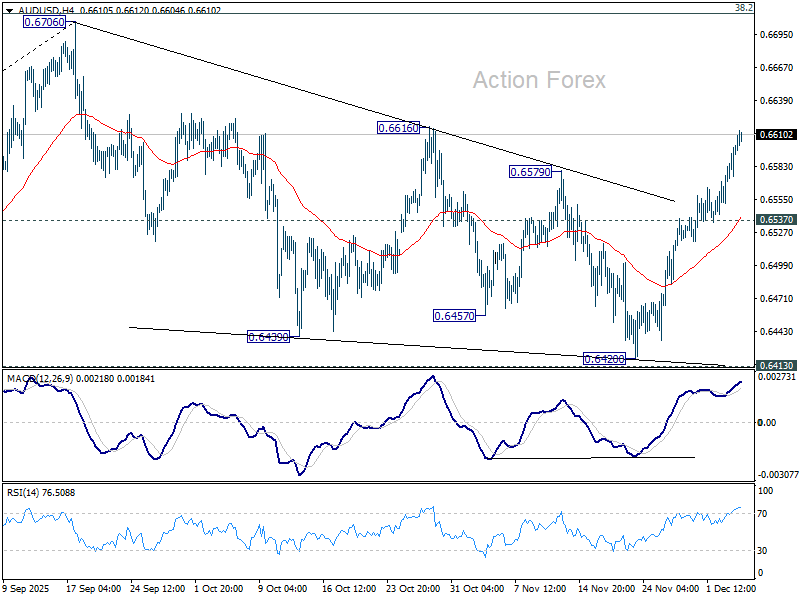

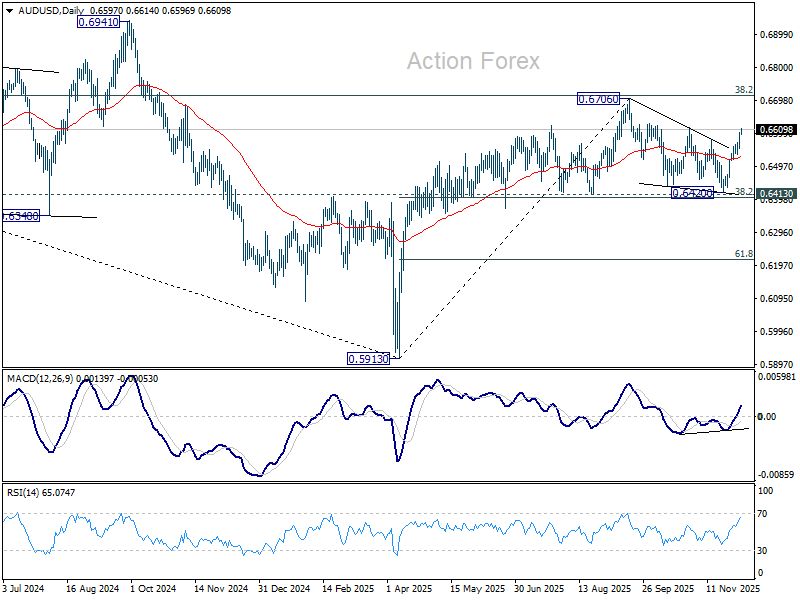

AUD/USD Daily Report

Daily Pivots: (S1) 0.6569; (P) 0.6586; (R1) 0.6619; More...

AUD/USD's rally from 0.6420 accelerates higher today and the solid break of 0.6579 resistance adds to the case that whole correction from 0.6706 has completed at 0.6420. Intraday bias stays on the upside for retesting 0.6709 and then 0.6713 key fibonacci level. For now, risk will stay on the upside as long as 0.6537 support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

US Passed, Japan Scored

The US economy lost 32’000 jobs in November. And no, it’s not AI’s fault. Small companies with fewer than 50 employees shed 120’000 jobs last month, according to the latest ADP report. Those losses outweighed gains in bigger companies. Overall, 32’000 people lost their jobs — the fourth negative print in the last six months. On average, the big and beautiful US economy has added fewer than 20’000 jobs per month over the past six months — a level comfortably pointing at recession.

Add to that the big companies, like Apple and Microsoft, planning headcount reductions — this time citing AI — and you get a pretty… amazing picture for the financial markets.

The job losses will push the Federal Reserve (Fed) toward faster and deeper rate cuts. And if, on top of that, people slow their spending because they’re out of work and inflation eases, that would be the cherry on top.

Odd, but that’s exactly how markets process information.

Yesterday was a typical “bad news is good news” session. You could see the cheery mood across US assets: job losses sent the 2-year Treasury yield below 3.50%, the probability of a 25bp cut in December rose to 90%, and the S&P 500 traded at 6’862 — just 58 points, or less than 1%, below its all-time high.

Interestingly, technology stocks — normally more sensitive to yields because much of their valuation is based on future revenue discounted to today — barely moved. The Magnificent Seven stayed stoic. Microsoft was busy denying a report from The Information claiming it lowered growth targets for AI software sales after many salespeople missed their goals last fiscal year. Investors read it as: “They’re not selling enough AI products, their targets are being lowered, and all these investments could be garbage.” Microsoft shares closed 2.5% lower. Nvidia lost 1% despite news that it could get approval to sell chips to China — if China is still willing to buy, which is no longer guaranteed.

Tesla, on the other hand, gained more than 4% — for reasons I can’t fully explain. Tesla sales are crashing in Europe, the company warned that UK sales are weakening, and Michael Burry called Tesla “ridiculously overvalued.” I agree. Tesla has become a massive meme stock, with a PE ratio near 300: you buy the share for around $446.74 as per yesterday’s close and earn roughly $1.50 per share. Expensive, yes — but some people like it. Plus, there was some non-EV-friendly news: Trump lowered climate goals, which sent Stellantis up almost 8% in Milan. Go figure why Tesla rallied.

Overall, the US session was solid. And the Japanese session was excellent, as a sale of 30-year government bonds drew the strongest demand since 2019 — at the current multi-decade high yield, near 3.40%. Given that pressure in JGBs has been a major risk to global risk appetite — even more so since the Bank of Japan (BoJ) head on Monday hinted at a possible rate hike this month — the rally in JGBs helped lift the Nikkei by 2%.

US futures, however, look mixed despite the rally in Asia. Nasdaq futures are slightly negative at the time of writing. Perhaps Morgan Stanley’s news that it is considering offloading some data-center exposure didn’t help. According to their calculations, the big cloud companies will spend around $3 trillion on data centers through 2028, but their cash flow can fund only half. Oracle’s CDS — now a barometer of AI-related risk — spiked to a 16-year high, hinting that appetite is fading.

Investors are awaiting tomorrow’s PCE numbers, which could further clear the path for rate cuts beyond December. At this pace of economic deterioration, the Fed may have little choice but to cut further. The question is whether softening Fed expectations will revive tech risk appetite, or if the rally will shift to non-tech and smaller companies. The Russell 2000, for example, rallied nearly 2% yesterday on the back of the weak ADP report. Fading AI enthusiasm due to high valuations, combined with lower yields, could push funds toward these companies.

In FX, the US dollar slipped below its 50-DMA and is testing a major Fibonacci support — if broken, it could enter a medium-term bearish zone. The broadly softening USD, on rising dovish Fed expectations, lifted the EURUSD above its 100-DMA. Europeans are unlikely to move rates next year, as inflation is around 2% and risks are two-sided. In Switzerland, zero inflation and strong demand for the franc continue to worry the Swiss National Bank (SNB), which doesn’t want to cut rates below zero. If the Fed cuts enough to lift global risk appetite, it could reduce the rush to Swiss francs.

A Fed cut is also positive for European stocks: lower US yields lift equities, and a stronger euro enhances returns in USD terms.

Elsewhere, copper rallied more than 2% on COMEX, amid concerns that potential US tariffs could squeeze supply. Metals remain investor favorites as appetite for traditional currencies wanes.

As we head toward year-end: it’s time to explore non-tech, non-US pockets of the market. Emerging-market indices benefit when the dollar softens, and European indices have performed very well this year to close the valuation gap. There’s certainly more to take advantage of, though it’s less flashy than the US tech story.