Sample Category Title

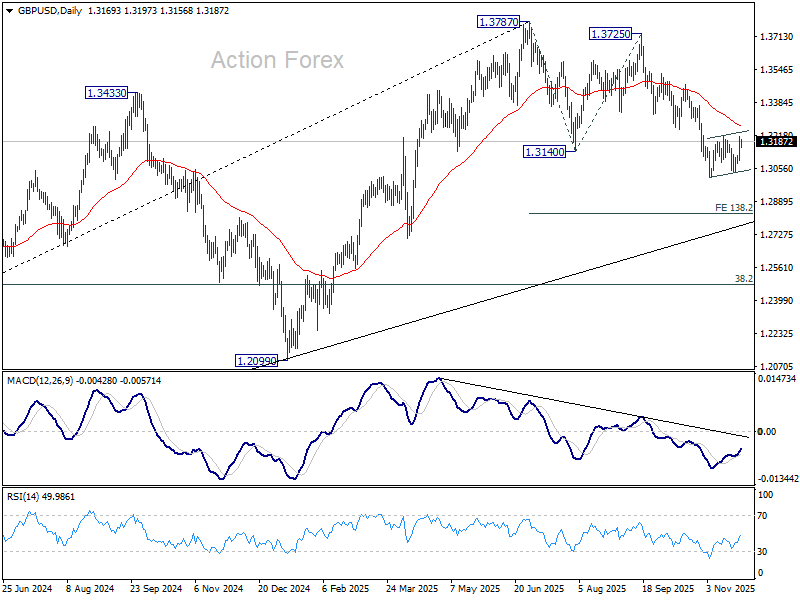

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3103; (P) 1.3158; (R1) 1.3221; More...

Intraday bias in GBP/USD remains neutral as consolidations continue in range of 1.3008/3247. With 1.3247 support turned resistance intact, further decline is expected. On the downside, break of 1.3008 will resume the fall from 1.3725 to 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

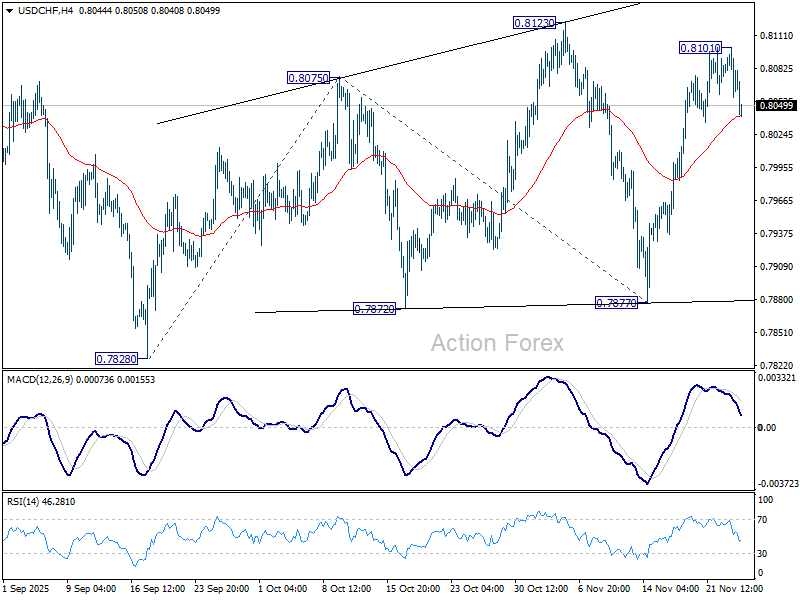

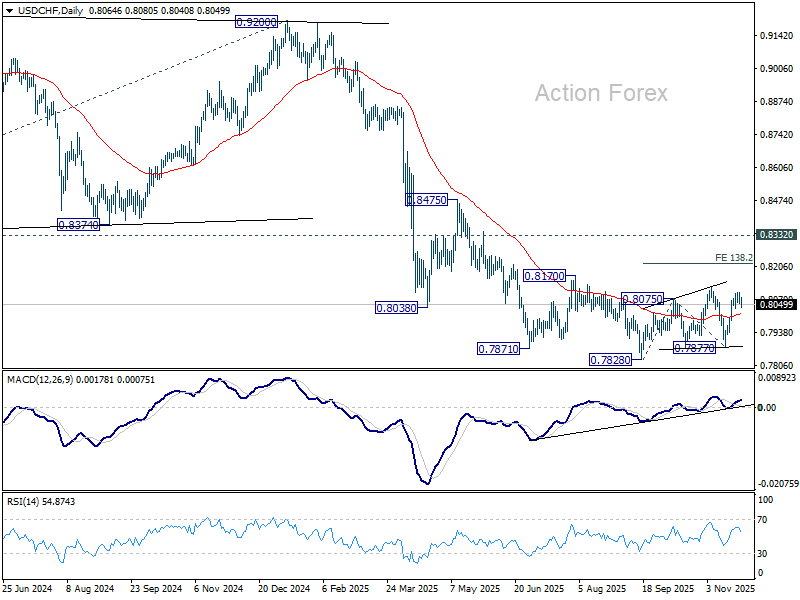

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8057; (P) 0.8079; (R1) 0.8101; More…

Intraday bias in USD/CHF stays neutral and more consolidations could be seen below 0.8101 temporary top. No change in the outlook that current rise from 0.7877 is still seen as the third leg of the corrective pattern from 0.7828 low. Above 0.8101 will target 0.8123 resistance, and then 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. However, sustained break of 55 D EMA (now at 0.8011) will bring deeper fall back to 0.7877 support instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

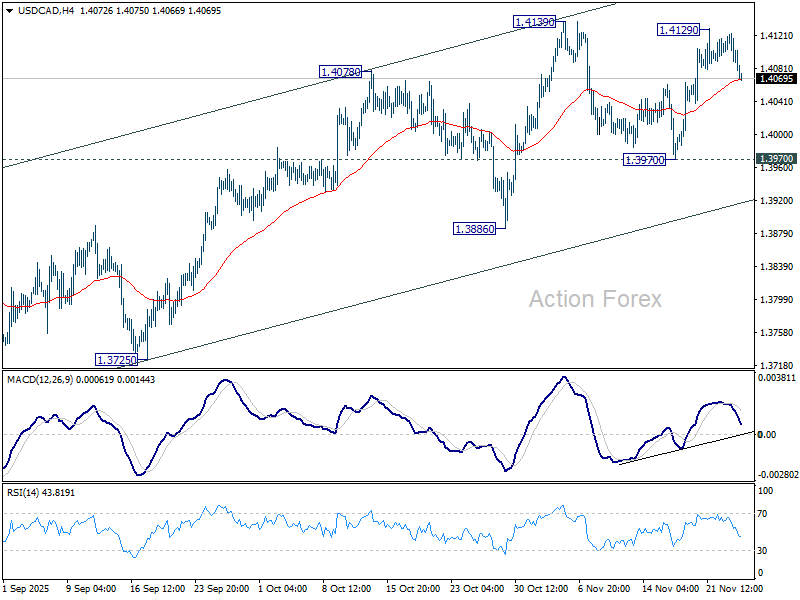

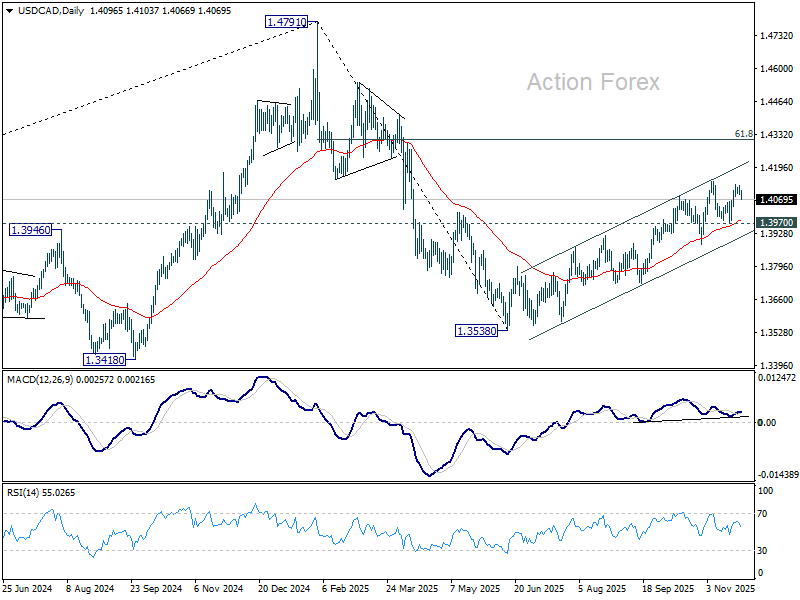

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4084; (P) 1.4105; (R1) 1.4119; More...

USD/CAD failed to break through 1.4139 resistance and retreated. Intraday bias remains neutral and more consolidations could be seen. Further rally is expected with 1.3970 support intact. On the upside, decisive break of 1.4139 resistance will resume whole rally from 1.3538. Next target is 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

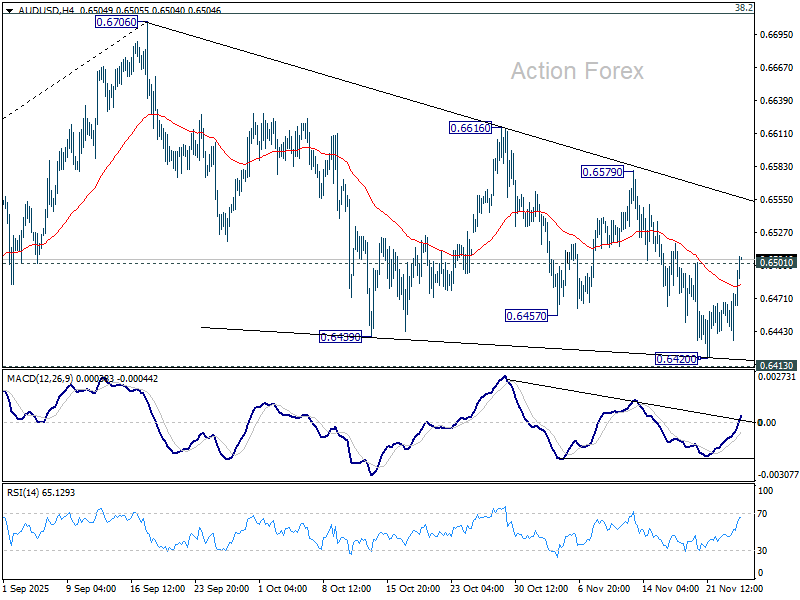

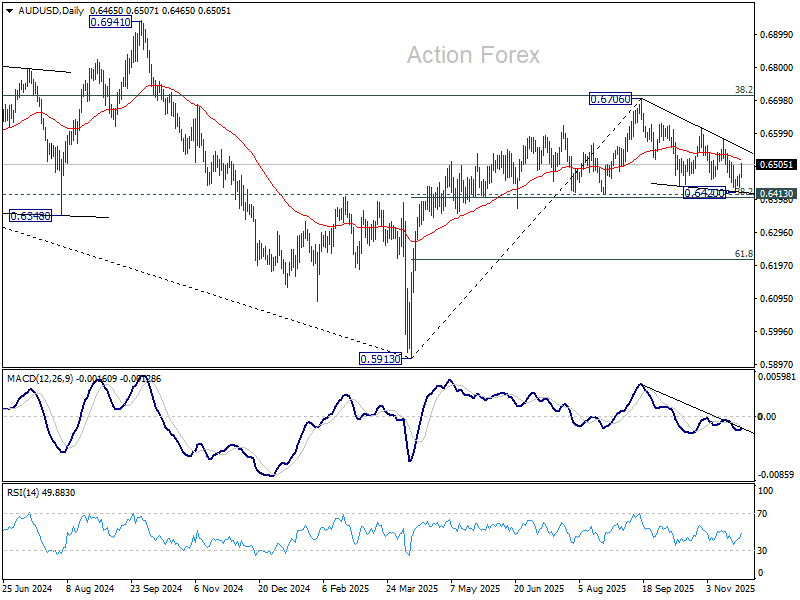

AUD/USD Daily Report

Daily Pivots: (S1) 0.6445; (P) 0.6461; (R1) 0.6485; More...

AUD/USD's extended rebound and break of 0.6501 resistance suggests short term bottoming at 0.6420. Intraday bias is back on the upside for 06579 resistance. Firm break there should confirm that whole fall from 0.6706 has completed as a three wave correction. Stronger rally should then be seen back to retest 0.6706. On the downside, sustained break of 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403) should confirm near term bearish reversal.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

Kiwi, Aussie Dominate; Sterling Awaits for High-Stakes Budget

Risk-on sentiment extended through Asian session, from intensifying bets on December Fed rate cut. The shift in sentiment sent US stocks higher overnight, and pushed 10-year yield briefly below 4% handle. Kiwi and Aussie are the biggest beneficiary of this backdrop, with both additionally supported by domestic developments.

Kiwi is the standout performer as markets digested RBNZ’s hawkishly framed rate cut. By signaling that the OCR is likely already at its trough and projecting only a modest lift through 2027, the central bank effectively pushed back against earlier expectations of a deeper easing cycle. Aussie also attracted buyers after Australia’s inflation data showed sharper acceleration than expected. Any RBA rate cut is pushed further into 2026.

Yen, however, remained soft despite renewed chatter around a December BoJ hike. Reuters reported that the central bank is preparing markets for a possible move as early as next month, following a key meeting between Prime Minister Sanae Takaichi and Governor Kazuo Ueda that appeared to remove political hurdles. Even so, sources suggested a close call between a December hike and a delay to January, with the Fed decision a week earlier likely to influence the decision. But for now, Yen traders appear e unconvinced.

Attention turns next to the UK Autumn Budget, which carries unusually high uncertainty after contradictory messaging from Chancellor Rachel Reeves on tax measures. Markets have little guidance on the scope or direction of fiscal changes, leaving room for large surprises. Gilt reaction will be the clearest test of investor confidence in the government’s fiscal stance. Sterling will trade off Gilt yields, but inversely—this is a confidence story, not a yield-seeking one.

For the week so far, Kiwi leads the performance board, followed by Aussie and Sterling. Dollar sits at the bottom, with Loonie and Yen also heavy, while Euro and Swiss Franc hover around the middle of the pack.

In Asia, at the time of writing, Nikkei is up 1.98%. Hong Kong HSI is up 0.44%. China Shanghai SSE is up 0.14%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is up 0.015 at 1.819. Overnight, DOW rose 1.43%. S&P 500 rose 0.91%. NASDAQ rose 0.67%. 10-year yield fell -0.036 to 4.002.

RBNZ delivers 25bps cut but signals little room for further easing

RBNZ cut the OCR by 25bps to 2.25% as widely expected, but the tone of the announcement was more hawkish than markets had anticipated.

Policymakers revealed they had debated holding rates at 2.50% versus cutting to 2.25%, and the final decision was reached by a 5–1 vote. The lone dissenter in favour of holding highlights pockets of concern about easing too deeply and reflects a more cautious internal balance than many had assumed.

More importantly for markets, RBNZ’s updated forward guidance showed a notably firmer policy path. The Bank now expects the OCR to bottom at just 2.2% through 2026 before gradually rising to 2.7% by the end of 2027. That trajectory implies minimal scope for further cuts next year if the economic outlook holds, effectively signaling that today’s move may mark the end of the easing cycle.

The accompanying statement reinforced that message. RBNZ said economic activity was weak through mid-2025 but is now improving, with lower interest rates supporting household spending and the labor market stabilizing. The fall in the exchange rate is also lifting exporters’ incomes, reducing the need for more aggressive stimulus from here. Risks to the inflation outlook are now viewed as “balanced”.

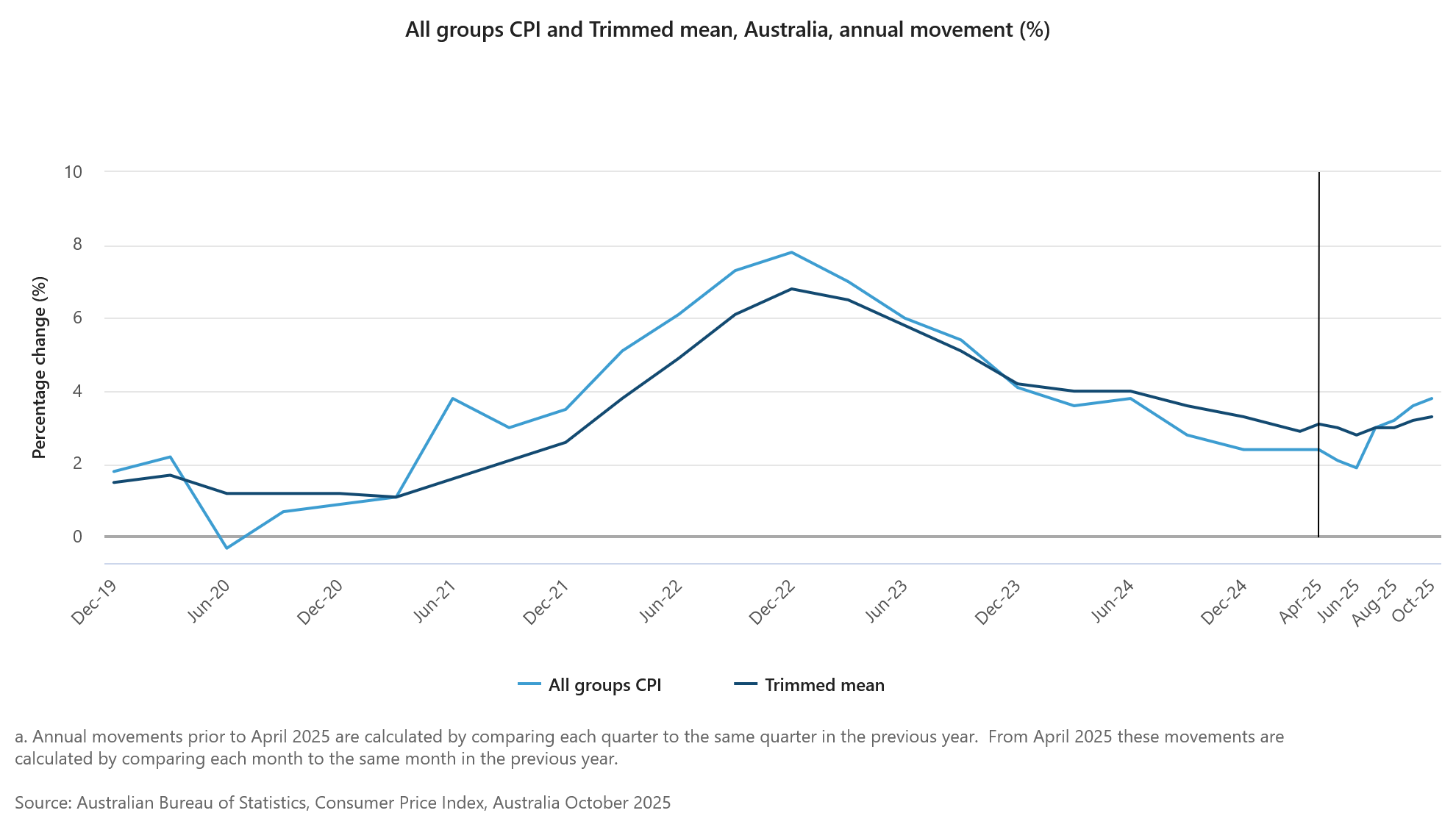

Australia CPI surges to 3.8% in October, goods and services prices accelerate

Australia’s CPI accelerated more than expected in October, rising from 3.5% yoy to 3.8%, beating expectations of 3.6%. Underlying pressure also firmed, with trimmed mean CPI moving up from 3.2% to 3.3%.

Both goods and services inflation picked up, with annual goods inflation at 3.8% (up from 3.7%) and services inflation at 3.9% (up from 3.5), signaling renewed price momentum. The combination will keep the RBA wary of easing again too soon.

The details showed broad-based increases. Housing costs was the largest contributor at 5.9%, followed by food and non-alcoholic beverages at 3.2%, and recreation and culture at 3.2%.

The release is also notable as the first in which Monthly CPI replaces the quarterly gauge as Australia’s primary headline measure.

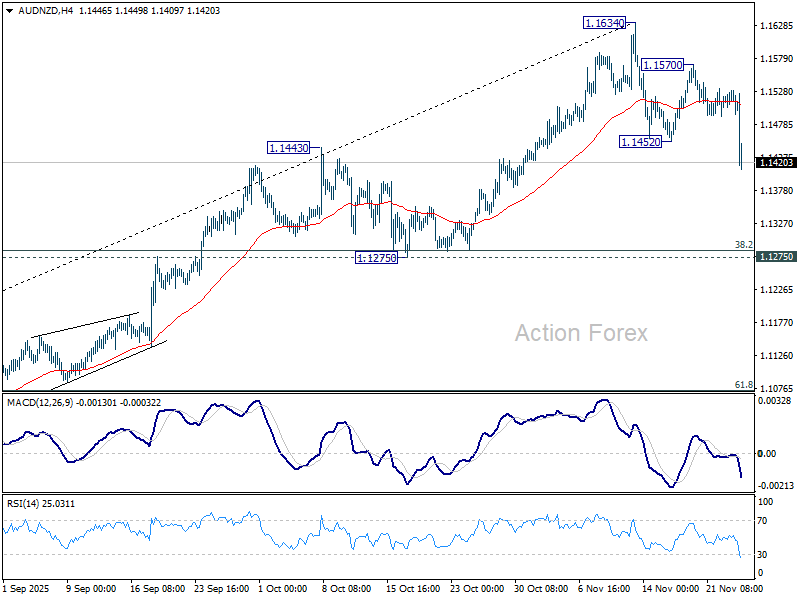

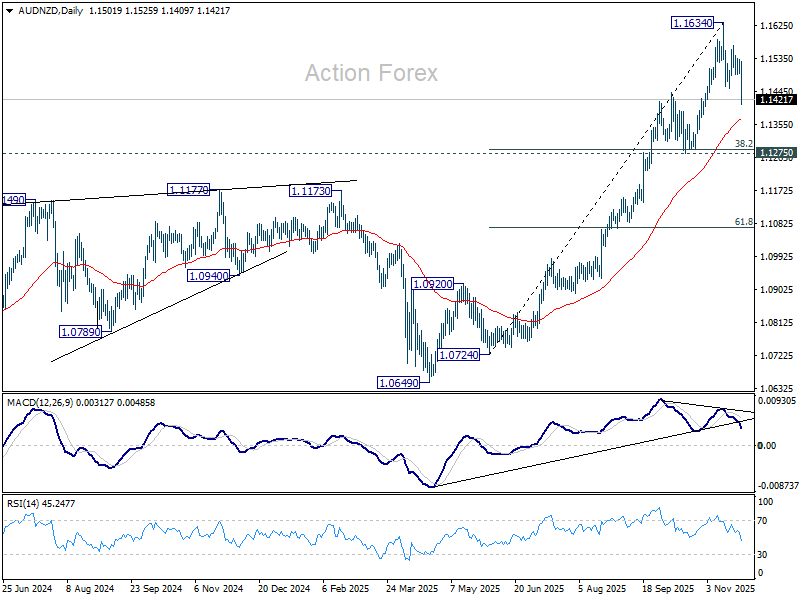

AUD/NZD drops as hawkish RBNZ cut overpowers hot Australia CPI

AUD/NZD tumbled sharply today as markets digested two major releases: RBNZ’s widely expected 25bps cut and Australia’s stronger-than-forecast CPI print. Despite the upside surprise on inflation, AUD buying was no match for the hawkish tone embedded in RBNZ’s announcement, which effectively signaled that the easing cycle is now complete.

That distinction proved decisive. With RBNZ projecting the OCR to bottom near current levels and rise gradually into 2027, the case for deeper easing has evaporated. Although the RBA is also expected to stay on hold through early 2026, the interest-rate differential is now set to remain stable rather than widening. Investors who previously bet on wider divergence, a trend accelerated by New Zealand’s sharp Q2 economic contraction, are now unwinding positions.

Technically, AUD/NZD's break of 1.1452 support confirms resumption of the decline from 1.1634 short term top. Considering bearish divergence condition in D MACD, fall from 1.1634 is likely correcting rise from 1.0724. Deeper fall should be seen to 55 D EMA (now at 1.1367) and possibly below.

But strong support is expected from 1.1275 cluster (38.2% retracement of 1.0724 to 1.1634 at 1.1286) to bring rebound and set the range for sideway trading.

Rise from 1.0649 is still expected to have another rising leg through 1.1634 to complete a five-wave impulsive pattern. But that's unlikely to happen soon. The move may only come when the markets start to bet that RBA would hike interest rate earlier than RBNZ, which won't be in the near future.

That next leg, however, would require a significant shift in rate expectations—specifically, a scenario where markets begin to see the RBA tightening earlier than RBNZ, which is not on the horizon at present.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6445; (P) 0.6461; (R1) 0.6485; More...

AUD/USD's extended rebound and break of 0.6501 resistance suggests short term bottoming at 0.6420. Intraday bias is back on the upside for 06579 resistance. Firm break there should confirm that whole fall from 0.6706 has completed as a three wave correction. Stronger rally should then be seen back to retest 0.6706. On the downside, sustained break of 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403) should confirm near term bearish reversal.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

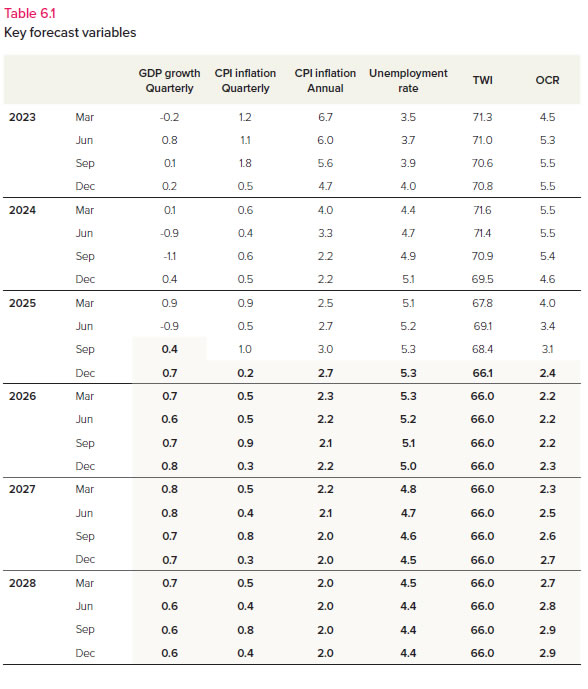

RBNZ Review: Enter the Nightwatchman

- The RBNZ cut the OCR by 25bps to 2.25%. The decision was made following a 5 – 1 vote, with one MPC member voting to hold the OCR at 2.5%.

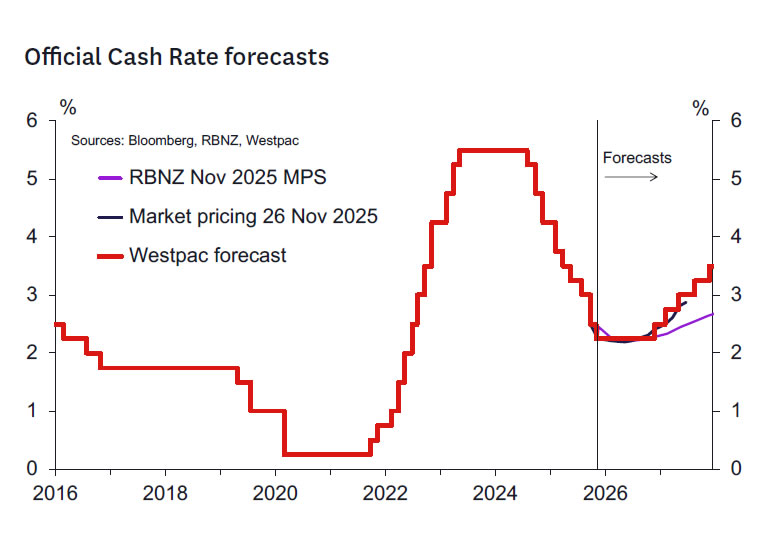

- The RBNZ’s OCR forecast profile was revised down as expected and now shows a terminal OCR of 2.20% (in Q2 2026), down from 2.55% previously.

- The RBNZ’s forecasts imply a first OCR hike around the middle of 2027, with the OCR to gradually move up towards 3% (the RBNZ’s estimated neutral rate) by the end of 2028.

- The RBNZ is presenting a neutral outlook for the OCR looking forward. The MPC retains flexibility to respond to incoming data, and is not drawing a firm line under the easing cycle just yet.

- Westpac expects no further cuts in the OCR. Our baseline forecast is that the OCR will begin a gradual move higher from late next year.

Key take out: OCR cut 25bps, RBNZ signals a neutral bias for February and perhaps beyond.

As widely expected, the RBNZ cut the OCR by 25bps to 2.25%. The decision was reached following a 5 - 1 vote, with one MPC member voting in favour of leaving the OCR at 2.5%.

The general tone of the Monetary Policy Statement seems more neutral than we expected. For example, there was no consideration of a 50bp cut, and one MPC member voted for no change in the OCR. The RBNZ’s assessment that the economy is picking up is perhaps a little more confident that we might have thought. Fixing the March 2026 OCR average at 2.25% sends a neutral bias for the February 2026 meeting. Glenn Turner was definitely opening the batting for the MPC in this innings!

As expected, the RBNZ’s projected track for the OCR was revised lower:

- The terminal OCR is 2.20% (in Q2 2026), down from 2.55% in the August MPS.

- The projected OCR for Q4 2026 was revised to 2.28% from 2.62% previously.

- The projected OCR for Q4 2027 was revised to 2.65% from 2.80% previously.

- The RBNZ assumes the OCR reaches 2.90% in Q4 2028 (the final quarter of the new forecast).

According to the RBNZ, the most important drivers of the reduction in the OCR track were a larger degree of spare capacity in the economy this year than assumed previously (reflecting the weak Q2 GDP outcome) and a lower outlook for export prices (due to recent falls in dairy product prices). The lower exchange rate supports exporter earnings and leans against disinflation in the short term.

The RBNZ is presenting a neutral, but data-dependent outlook. The Governor noted some slight downside risk to the OCR in the short term, but upside risk in the medium term. The Governor noted that the OCR is now at stimulatory levels and should support growth in time. Up to now, the RBNZ has been less clear about whether interest rates are at stimulatory levels.

The overall implication is that the MPC is now ready to send the nightwatchman in to see the innings through for the foreseeable future. The new Governor can reassess the situation next year in light of the data to come.

Notable quotes.

Some notable quotes from the press statement and Statement of Record were:

“Economic indicators are recovering, and economic activity is expected to strengthen through 2026.” “Risks to the inflation outlook are balanced.”

“Committee members discussed an improvement in near-term indicators of economic activity from their lows in the June quarter, suggesting a return to modest GDP growth in the September quarter. Feedback from recent business visits also suggests that, while activity remains weak, demand has stabilised.”

“Some members highlighted the risk that continued caution on the part of households and businesses could further slow the recovery in domestic demand, which could see inflation fall below the target midpoint. Conversely, other members highlighted the possibility of a faster recovery if house prices and household spending increase more quickly than assumed given lower mortgage rates, leading to more persistence in medium-term inflation pressures.”

“Members noted that tariffs have had less impact on the global economy than initially expected, reflecting the imposition of lower tariff rates than originally envisaged, inventory management, and adjustments in global supply chains… The Committee still expects trade barriers to weigh on global economic activity and to have a modest disinflationary effect on New Zealand.”

“The Committee discussed the risk that unsustainable fiscal dynamics and increased politicisation of central banks globally could create the conditions for higher and more persistent inflation.”

“The case for a further reduction in the OCR emphasised significant excess capacity in the economy. This provides confidence that medium term inflation will return to, and remain around, the target mid-point. The economic recovery is at an early stage, and the inflation outlook provides scope to place more emphasis on avoiding unnecessary volatility in output and employment. With this context, retention of the easing in overall monetary conditions delivered to date would support an enduring recovery in economic activity.”

“Future moves in the OCR will depend on how the outlook for medium-term inflation and the economy evolve.”

Westpac’s OCR call.

We continue to expect 2.25% to mark the nadir of the easing cycle. The RBNZ looks like it has a neutral bias looking forward and is certainly not signalling any intention to cut the OCR in February. Of course, much could change between then and now. Hence, we continue to expect the RBNZ to maintain a flexible data-dependent approach. We agree that the current OCR, left long enough, should be sufficient to support the recovery in the economy.

The timing of the return of the OCR to higher, more neutral levels will depend on the pace of the eventual recovery. Hence while we continue to see the first hike as occurring in December 2026 (likely after the 2026 General Election), there are two-sided risks to that call. Should the economy pick up relatively quickly, the normalisation of the OCR could come before the election, closer to the middle of 2026. A disappointing recovery could mean the OCR on hold for longer.

The exchange rate has moved a touch higher as markets likely expected a more dovish outlook than seen today. More generally, we suspect that the New Zealand dollar will remain weak against most currencies until such time as markets turn away from the risks of a lower OCR and consider the timing of the tightening cycle. It will likely be some time before we get to that position.

RBNZ forecast detail.

The RBNZ’s updated forecasts align broadly with our own assessment.

The economy is starting from a weaker position than the RBNZ anticipated back in August. That’s due to the much weaker than expected June quarter GDP result. Like ourselves, the RBNZ thinks that result likely overstated the degree of weakness in activity. Even so, economic conditions were soft through the middle part of the year, and the economy has more spare capacity than the RBNZ anticipated (i.e., a lower output gap). And even with lower interest rates, that spare capacity is expected to dissipate only very gradually.

That lingering spare capacity has reinforced the downward pressure on the RBNZ’s forecasts for domestic inflation. This is an area where we think the RBNZ could be surprised on the upside. The RBNZ has acknowledged the strength in the prices for items like council rates, but expects this to ease. In contrast, we anticipate such pressure will be a bit more enduring.

Nevertheless, we agree with the RBNZ’s more general assessment that spare capacity in the economy will see inflation dropping back over the year ahead.

The RBNZ’s statement noted early signs that the economy is starting to turn. Consistent with such indicators and the large fall in interest rates over the past year, we think that domestic demand will pick up a bit faster than the RBNZ. However, much of that increase in demand will be met by increased imports.

Key things to watch ahead of the RBNZ’s 18 February 2026 Review.

The next RBNZ policy review will take place on 18 February 2026. Given the longer than usual break until the next meeting, there will be a significant number of key domestic economic data releases ahead of that meeting. Indeed, the RBNZ will receive a new round of all the top-tier quarterly indicators, and so there is plenty of scope for outcomes to drive a different outcome to that currently projected by the RBNZ. The most important releases are:

- The Q3 GDP report (18 December): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum. The RBNZ’s forecast of 0.4% growth is in line with our own view. The Q3 release will also include a range of revisions to the historical data, which could have a bearing on the RBNZ’s assessment of the economy’s spare capacity.

- The Q4 QSBO survey (13 January, TBC): The focus will be on indicators of spare capacity and cost/inflation pressures. It will also be interesting to see to what extent hiring and investment indicators are lifting as easy monetary conditions continue to transmit through the economy.

- The Q4 CPI (23 January) and January Selected Price Indexes (17 February): With headline inflation currently at the top of the RBNZ’s target range, the focus will be on whether the CPI is evolving in a manner consistent with the RBNZ’s forecast that it will quickly move back towards the target midpoint over the coming year.

- The Q4 labour market survey (4 February): Developments in both the unemployment rate and labour costs will be compared against the RBNZ’s updated estimates, while measures of labour input will provide some insight into how GDP might have fared during the quarter.

In addition to the above, key monthly activity indicators such as the BusinessNZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest, as will developments in retail spending and housing indicators (albeit the latter tend to be difficult to read given that the housing market typically goes somewhat quiet over the holiday period). The Government’s Half-Year Economic and Fiscal Update and Budget Policy Statement (16 December) might also contain information bearing on expectations regarding the future stance of fiscal policy (of particular interest given the seemingly tight General Election that looms later next year).

Finally, the other factor that will have a bearing on the next policy decision will be the arrival of the new Governor Anna Breman, who takes up her role next week. In addition, the departure of current Governor, Christian Hawkesby, will maintain a vacancy on the MPC. That vacancy may be filled by the time of the February MPS meeting, possibly by a temporary appointment pending the appointment of a new Deputy Governor.

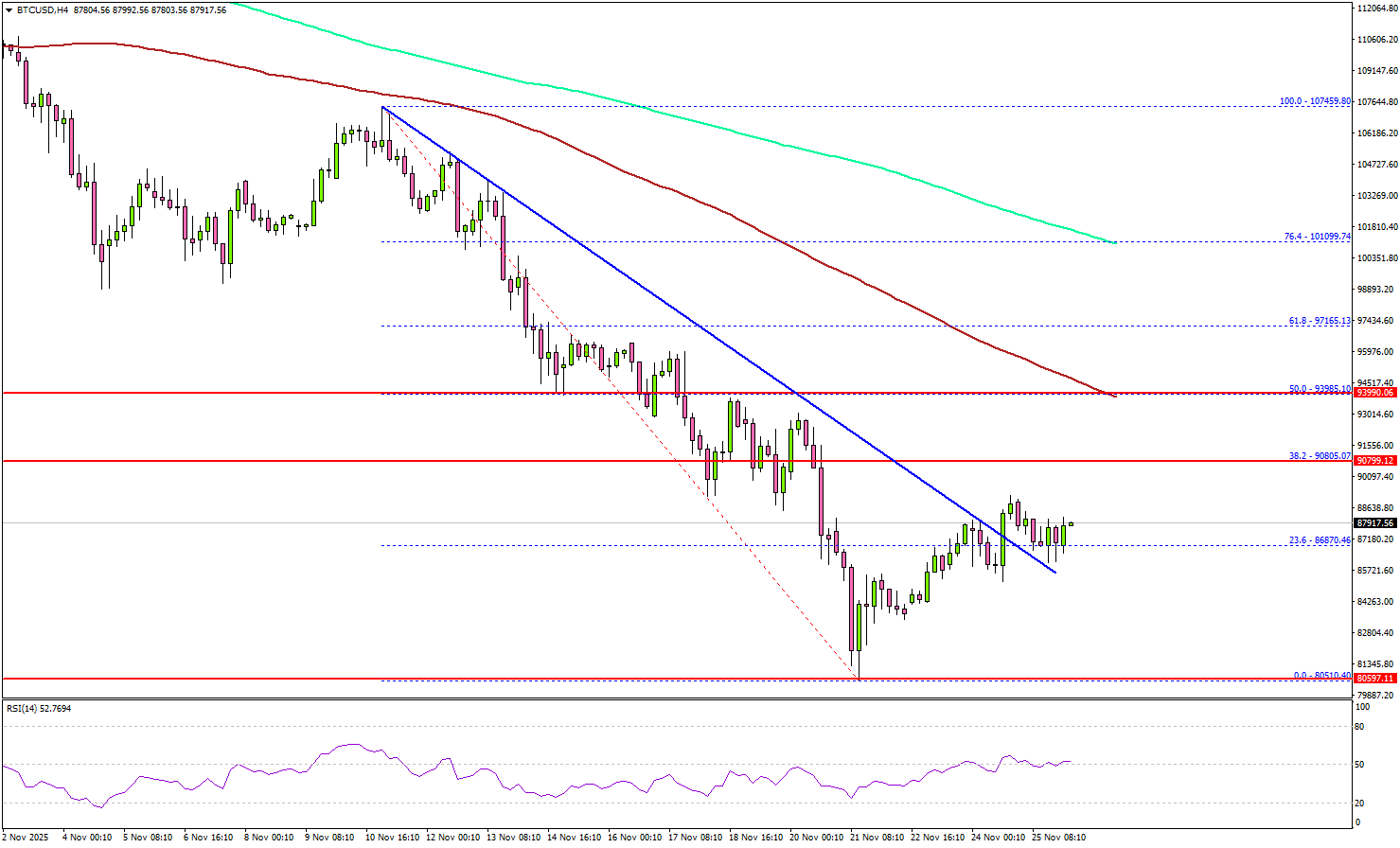

Bitcoin Starts to Rebound, But Momentum Faces a Steep Climb

Key Highlights

- Bitcoin started a recovery wave above $85,000 and $86,500.

- BTC/USD cleared a key bearish trend line with resistance at $86,800 on the 4-hour chart.

- Ethereum also started a decent increase above $2,800.

- XRP price climbed above $2.10 to move into a positive zone.

Bitcoin Price Technical Analysis

Bitcoin price found support near $80,500 and started a recovery wave against the US Dollar. BTC climbed above $85,000 and $86,500 to enter a short-term positive zone.

Looking at the 4-hour chart, the price surpassed the 23.6% Fib retracement level of the downward move from the $107,459 swing high to the $80,510 low. During the increase, the price broke a key bearish trend line with resistance at $86,800.

BTC faces many hurdles and remains below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). If the price extends gains, it could face resistance at $90,800.

The main hurdle is now forming near $94,000 and the 50% Fib retracement level of the downward move from the $107,459 swing high to the $80,510 low. A successful close above $94,0000 might start another steady increase. In the stated case, the price may perhaps rise toward the $95,500 level. Any more gains might call for a test of $97,000.

Immediate support sits at $85,000. A downside break below $85,000 might start another decline. The next major support is $84,200. Any more losses might call for an extended decline toward the $82,800 support zone.

Looking at Ethereum, the price was able to follow Bitcoin and climbed above the $2,850 resistance region.

Today’s Key Economic Releases

- US Initial Jobless Claims - Forecast 227K, versus 220K previous.

- US Durable Goods Orders for Sep 2025 – Forecast +0.2% versus +2.9% previous.

AUD/NZD drops as hawkish RBNZ cut overpowers hot Australia CPI

AUD/NZD tumbled sharply today as markets digested two major releases: RBNZ’s widely expected 25bps cut and Australia’s stronger-than-forecast CPI print. Despite the upside surprise on inflation, AUD buying was no match for the hawkish tone embedded in RBNZ’s announcement, which effectively signaled that the easing cycle is now complete.

That distinction proved decisive. With RBNZ projecting the OCR to bottom near current levels and rise gradually into 2027, the case for deeper easing has evaporated. Although the RBA is also expected to stay on hold through early 2026, the interest-rate differential is now set to remain stable rather than widening. Investors who previously bet on wider divergence, a trend accelerated by New Zealand’s sharp Q2 economic contraction, are now unwinding positions.

Technically, AUD/NZD's break of 1.1452 support confirms resumption of the decline from 1.1634 short term top. Considering bearish divergence condition in D MACD, fall from 1.1634 is likely correcting rise from 1.0724. Deeper fall should be seen to 55 D EMA (now at 1.1367) and possibly below.

But strong support is expected from 1.1275 cluster (38.2% retracement of 1.0724 to 1.1634 at 1.1286) to bring rebound and set the range for sideway trading.

Rise from 1.0649 is still expected to have another rising leg through 1.1634 to complete a five-wave impulsive pattern. But that's unlikely to happen soon. The move may only come when the markets start to bet that RBA would hike interest rate earlier than RBNZ, which won't be in the near future.

That next leg, however, would require a significant shift in rate expectations—specifically, a scenario where markets begin to see the RBA tightening earlier than RBNZ, which is not on the horizon at present.

Australia CPI surges to 3.8% in October, goods and services prices accelerate

Australia’s CPI accelerated more than expected in October, rising from 3.5% yoy to 3.8%, beating expectations of 3.6%. Underlying pressure also firmed, with trimmed mean CPI moving up from 3.2% to 3.3%.

Both goods and services inflation picked up, with annual goods inflation at 3.8% (up from 3.7%) and services inflation at 3.9% (up from 3.5), signaling renewed price momentum. The combination will keep the RBA wary of easing again too soon.

The details showed broad-based increases. Housing costs was the largest contributor at 5.9%, followed by food and non-alcoholic beverages at 3.2%, and recreation and culture at 3.2%.

The release is also notable as the first in which Monthly CPI replaces the quarterly gauge as Australia’s primary headline measure.

RBNZ delivers 25bps cut but signals little room for further easing

RBNZ cut the OCR by 25bps to 2.25% as widely expected, but the tone of the announcement was more hawkish than markets had anticipated.

Policymakers revealed they had debated holding rates at 2.50% versus cutting to 2.25%, and the final decision was reached by a 5–1 vote. The lone dissenter in favour of holding highlights pockets of concern about easing too deeply and reflects a more cautious internal balance than many had assumed.

More importantly for markets, RBNZ’s updated forward guidance showed a notably firmer policy path. The Bank now expects the OCR to bottom at just 2.2% through 2026 before gradually rising to 2.7% by the end of 2027. That trajectory implies minimal scope for further cuts next year if the economic outlook holds, effectively signaling that today’s move may mark the end of the easing cycle.

The accompanying statement reinforced that message. RBNZ said economic activity was weak through mid-2025 but is now improving, with lower interest rates supporting household spending and the labor market stabilizing. The fall in the exchange rate is also lifting exporters’ incomes, reducing the need for more aggressive stimulus from here. Risks to the inflation outlook are now viewed as “balanced”.