Sample Category Title

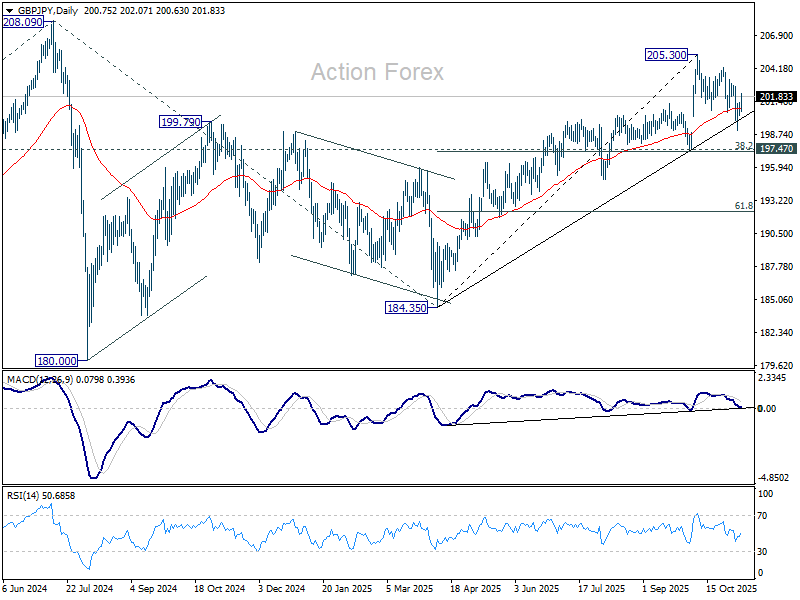

GBP/JPY Weekly Outlook

GBP/JPY edged lower to 199.04 again last week but quickly recovered. Initial bias stays neutral this week first. For now, the structure of the fall from 205.30 suggests that it's only a corrective move. Break of 204.22 resistance will argue that larger rise from 184.53 is ready to resume through 205.30. However, below 199.04 will target 197.47 cluster (38.2% retracement of 184.35 to 205.30 at 197.29).

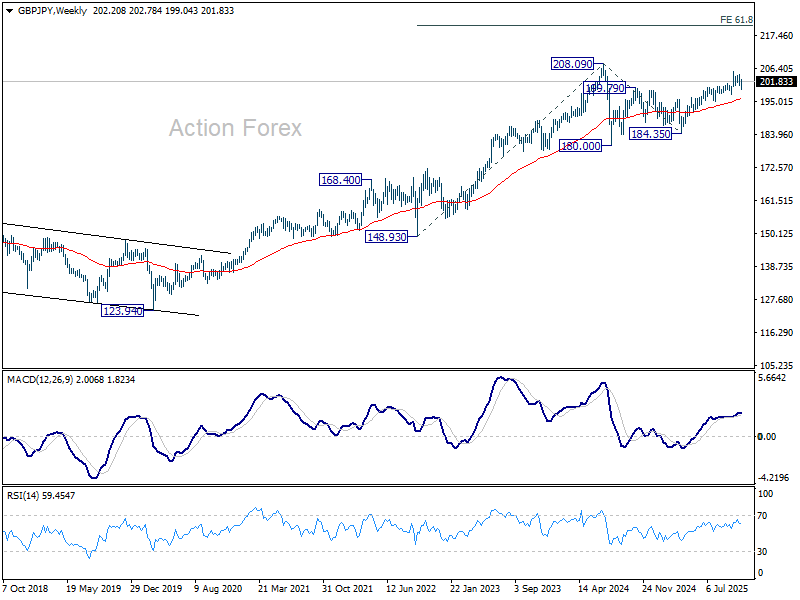

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

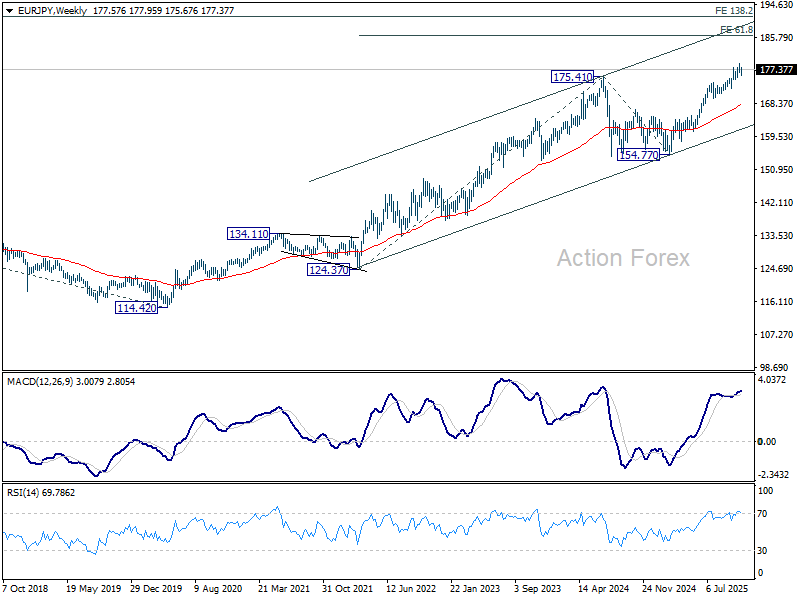

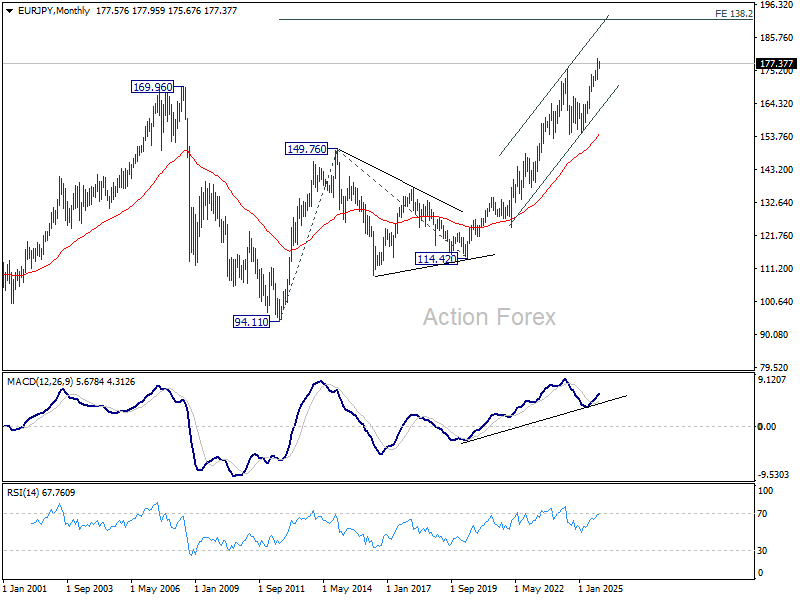

EUR/JPY Weekly Outlook

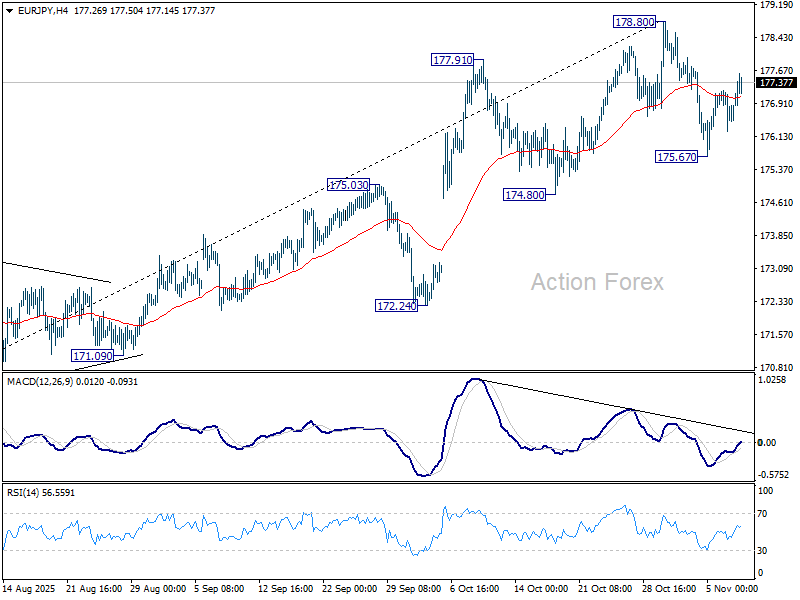

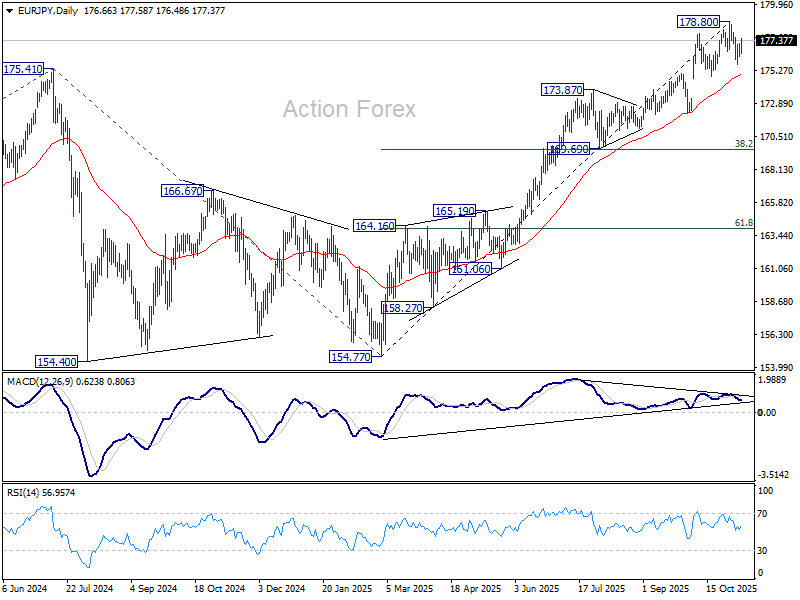

EUR/JPY's retreat from 178.80 extended lower last week but recovered after hitting 175.67. Initial bias stays neutral this week and risk will remain mildly on the downside as long as 178.80 resistance holds. Break of 175.67 will target 55 D EMA (now at 175.00). Considering bearish divergence condition in D MACD, sustained break of 55 D EMA will argue that EUR/JPY is correcting whole rise from 154.87, and target 169.69 cluster (38.2% retracement of 154.77 to 178.80 at 169.69). Nevertheless, firm break of 178.80 will resume the long term up trend.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, firm break of 174.80 support will suggests that it has turned into consolidations first. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 168.20) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

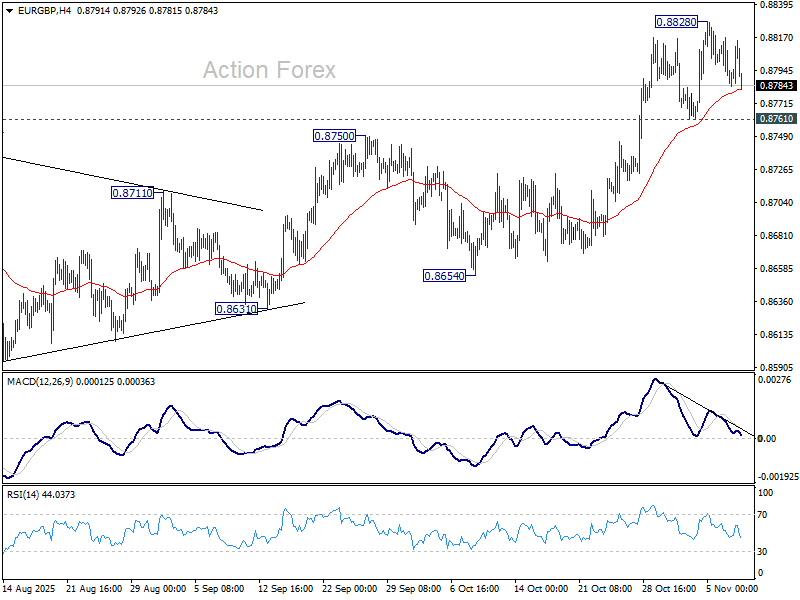

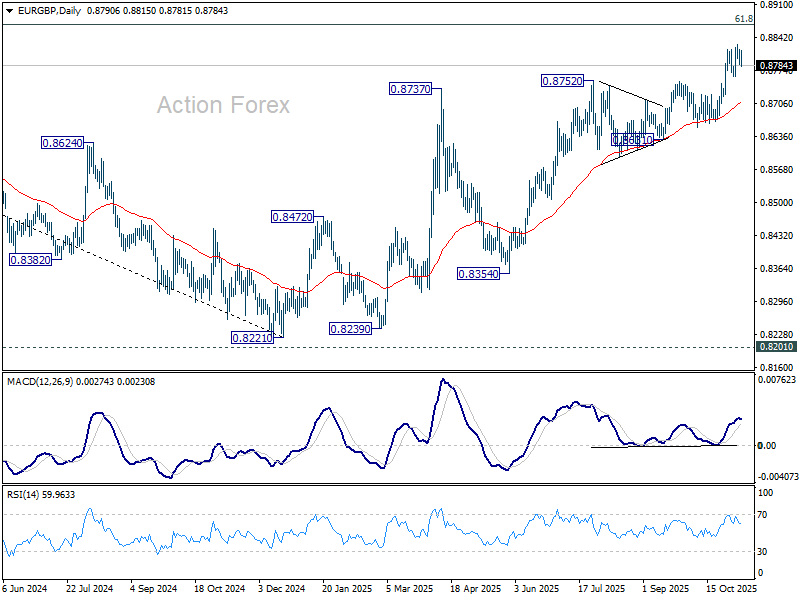

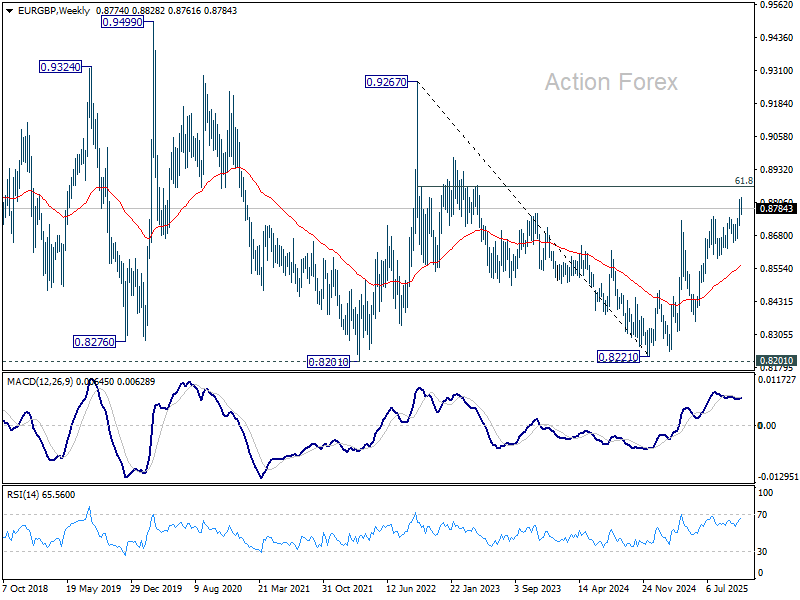

EUR/GBP Weekly Outlook

EUR/GBP edged higher to 0.8828 last week but retreated again. Initial bias stays neutral this week for more consolidations. Further rally is expected as long as 0.8761 support holds. On the upside, break of 0.8828 will resume the whole rally from 0.8221 and target 0.8867 fibonacci level. Firm break there will carry larger bullish implications. However, considering bearish divergence condition in 4H MACD, decisive break of 0.8761 will confirm short term topping, and bring deeper fall to 55 D EMA (now at 0.8708).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

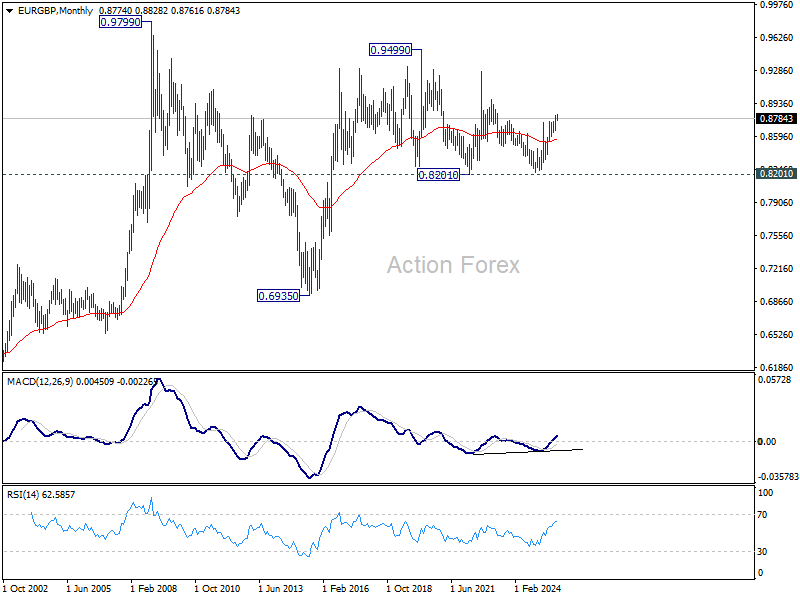

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

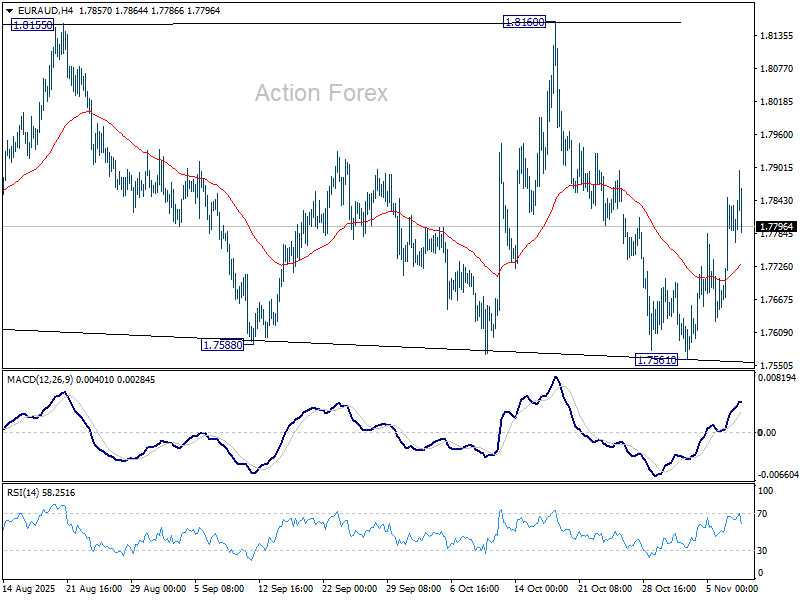

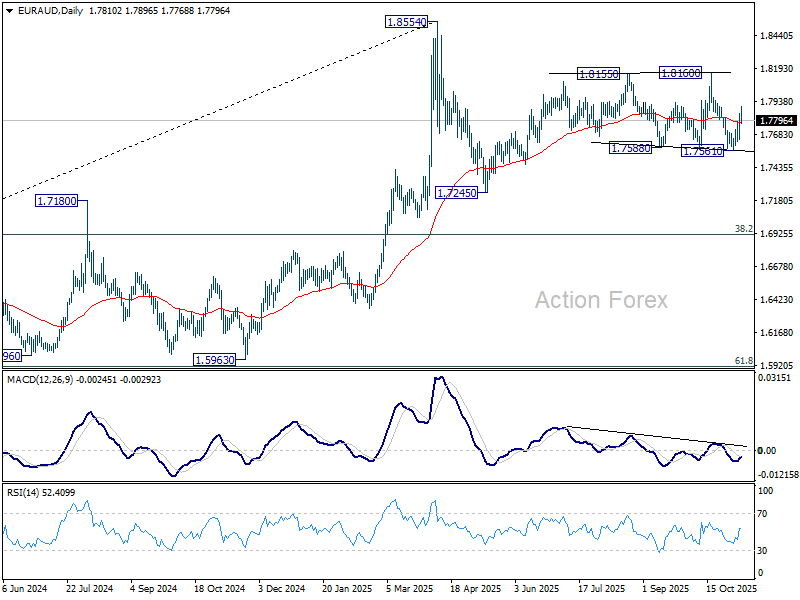

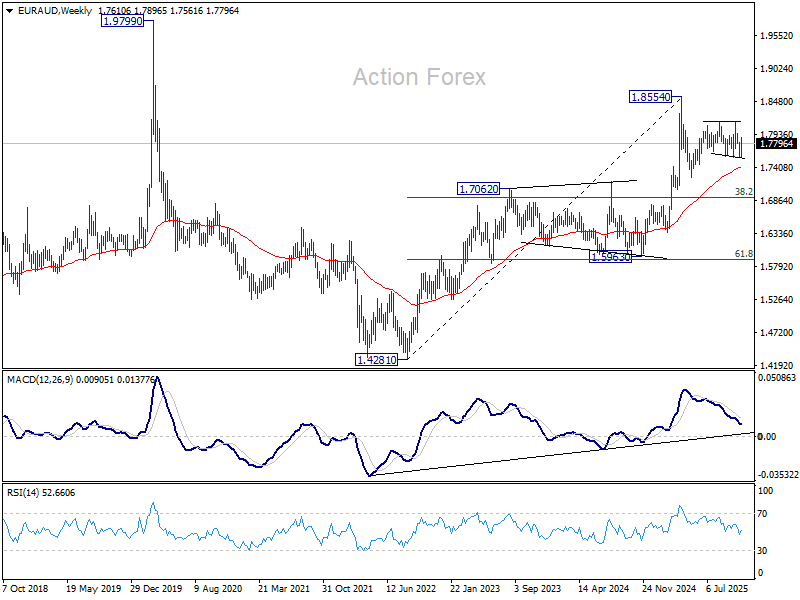

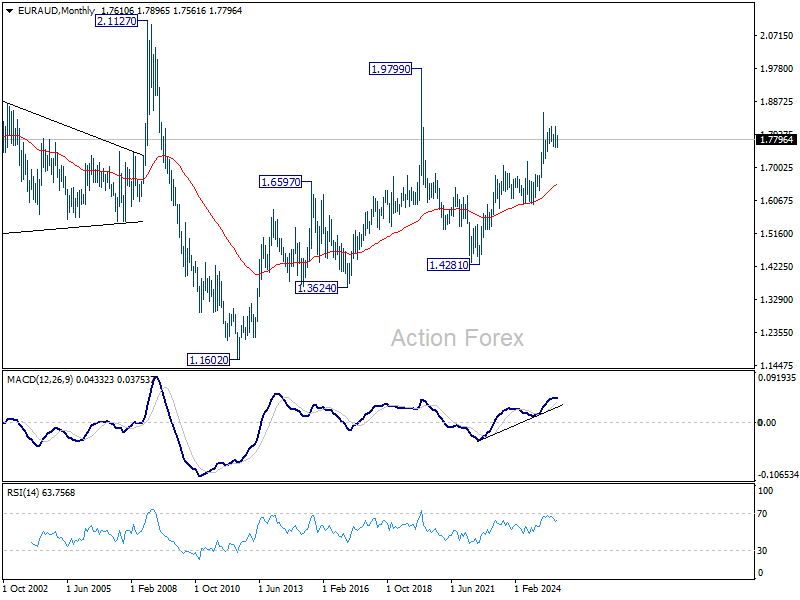

EUR/AUD Weekly Outlook

EUR/AUD's strong rebound from 1.7571 last week dampened the original bearish view. Fall from 1.8160 is likely just part of the sideway pattern from 1.8155. Initial bias is mildly on the upside this week for 1.8160 first. On the downside, however, break of 1.7561 will revive the bearish case that corrective pattern from 1.8554 is in the third leg, and target 1.7245 support.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7406) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound form 55 W EMA will likely bring resumption of the up trend sooner.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6501) holds, this second leg could still extend higher.

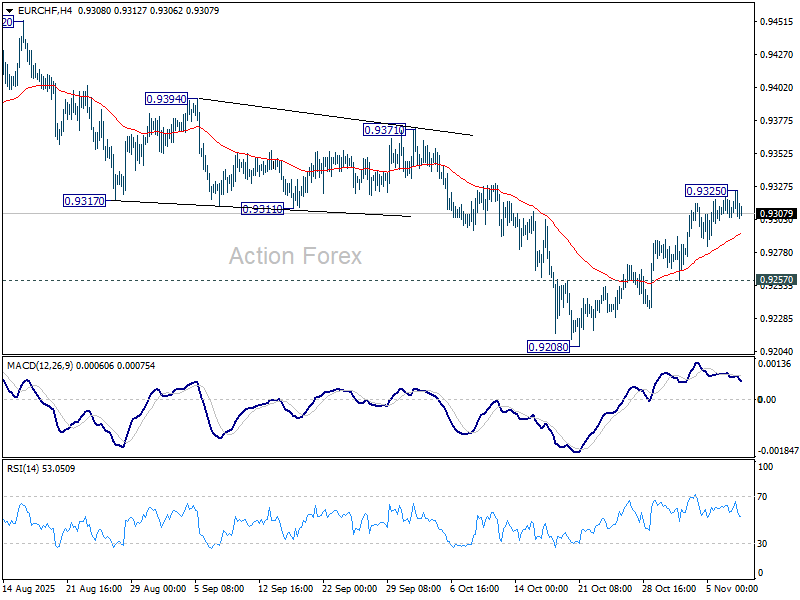

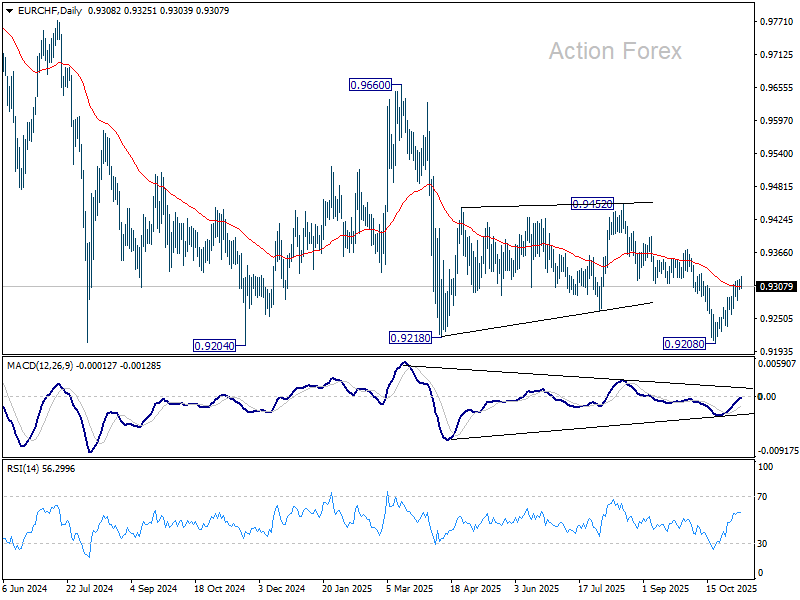

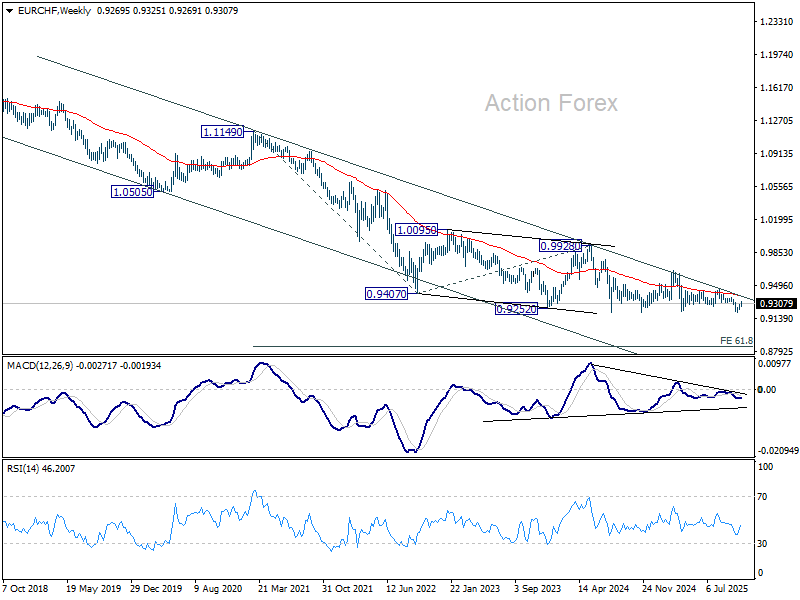

EUR/CHF Weekly Outlook

EUR/CHF's extended rebound last week argues that fall from 0.9452 has completed at 0.9208. But as a temporary top was formed at 0.9325, initial bias is turned neutral this week first. On the upside, break of 0.9325 will target 0.9371 resistance. Break there will pave the way back to 0.9452 resistance next. On the downside, however, break of 0.9257 will revive near term bearishness, and bring retest of 0.9204/8 support zone.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9383). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. However, break of 0.9452 resistance will now be the first sign of medium term bottoming.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9820) holds.

Markets Weekly Outlook – Traders get impatient for the US shutdown to end

Week in review – Markets are starting to get worried from a prolonged shutdown

Navigating through the headlines can be difficult in Markets.

Even when Stock indices break new records week after week, negative headlines can lead readers to adopt a more pessimistic view compared to how things really are – this explains, in part, the “Buy the rumours, Sell the news” adage.

However, when Stock indices start to reverse sharply, headlines begin to have a snowball effect.

November trading began at the beginning of this week and brought with it some winter headwinds:

Almost all global stock indices are lower, and cryptocurrencies have taken a huge hit, leaving investors scratching their heads to know where to put their money.

To accompany these flows, tons of speeches and headlines on high AI stock valuation and spendings start to send vibes of a lack of confidence (and this could also be seen in the latest University of Michigan survey)

As the week comes to an end, a rough beginning of the month for safe-havens, particularly metals, began to materialize in somewhat of a new rebound – Gold is back above $4,000.

US Treasuries are also following suit, closing the week at their highs.

A more hawkish FedSpeak (following Powell's October meeting tone) throughout the week started to cast doubts on a December meeting cut, further hurting Market optimism.

The US Shutdown was not significantly impact markets throughout the past month, but as more governmental services and sectors are affected, with even flight numbers being reduced, this is changing.

US Vice President JD Vance has even sent out warnings on the consequences of the prolonged shutdown.

All of these catalysts begin to have an impact on sentiment in the broader context.

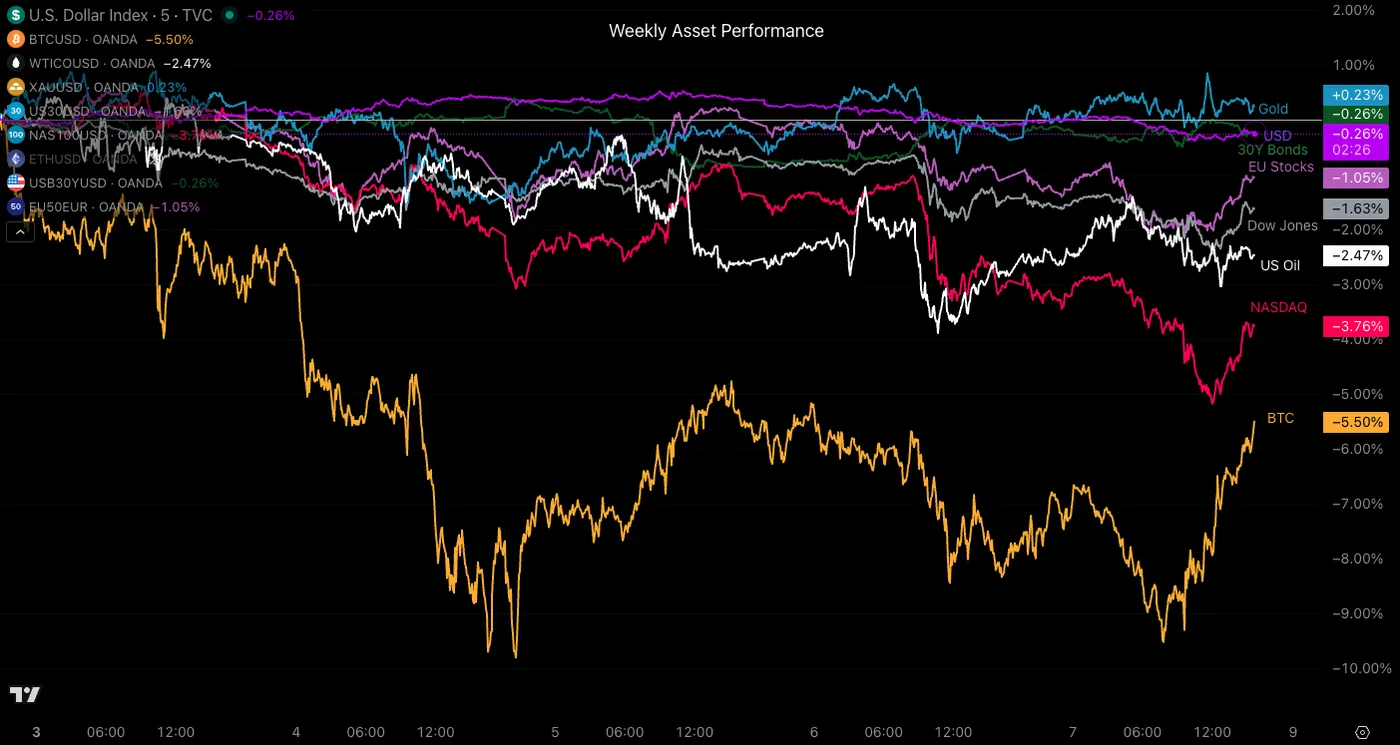

Weekly performance from different asset classes

Weekly Asset Performance, November 7, 2025 – Source: TradingView

Magnitude of movements for cryptocurrencies are usually higher, but this weekly asset performance chart shows well how risk assets took a hit this week.

More defensive stock indices like the Dow Jones finishes down 1.50%, the tech-heavy Nasdaq down 3.56%, dragged down further by pessimistic warnings from the Nvidia CEO or OpenAI's CFO.

At the extreme of the risk and volatility spectrum, cryptocurrencies took a big slap in the face.

Bitcoin, the most stable, lost a bit more than 5% in value – just hanging above the $100,000 mark – while Ethereum, Solana and other altcoins lost a minimum of 10% (and much more).

The Week Ahead – A government reopening?

The week was one of a risk-appetite that reduced drastically.

Nonetheless, some more vodish pricings and hopes for a US government reopening helped equities to catch around the same time that European indices closed.

Market-odds of the timing for a US government reopening – Polymarket – November 7, 2025

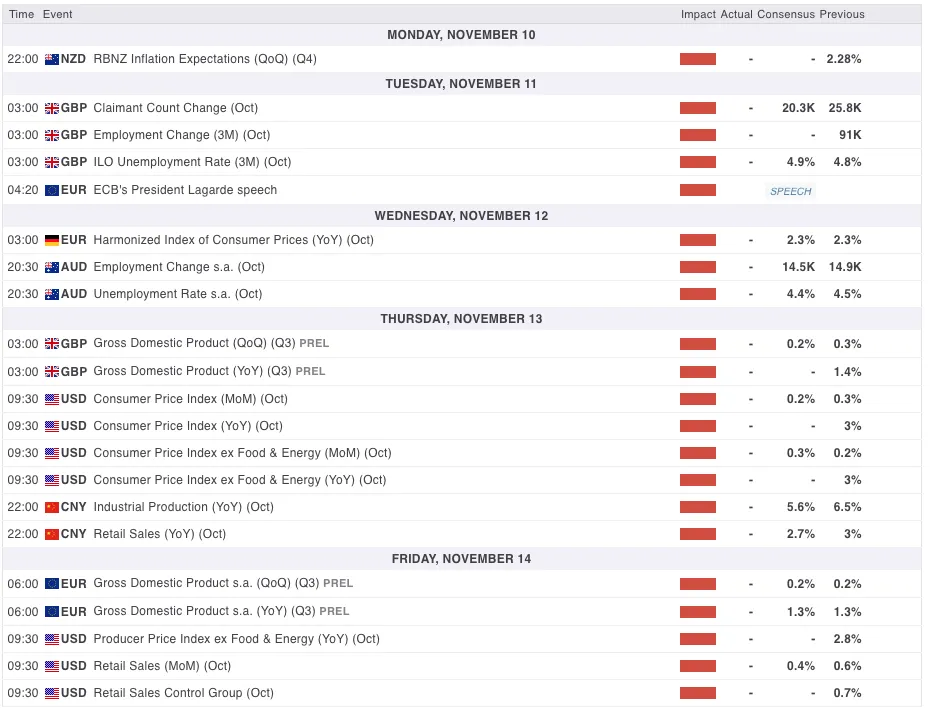

Asia Pacific Markets – Australian Employment, more Chinese production data and NZ inflation expectations

AUD traders will have to stay sharp with Australian data largely taking the front-scene. Monday will begin with Consumer confidence data but the key really is the Australian Employment data, releasing on Wednesday evening (20:30).

The bar is high for the number, with Australia maintaining a strong look throughout the year but has started to show a few signs of slowing.

For those keeping an eye on China (particularly after the disastrous trade numbers released yesterday), APAC traders will want to monitor the Industrial production and retail sales number to see if the PBoC has more room for stimulus (typically a booster for AUD and NZD).

Kiwi data is also not to be forgotten with their very key RBNZ inflation expectations numbers also releasing Monday night at 20:30 (ET).

US, Europe and UK Markets – European & UK Employment with still nothing to see in the US

As the Bureau of Labor Statistics is still closed until further notice and no private data is on the watch next week, traders will have to be a bit more patient to get an idea of the state of the US Economy.

However, there is still work to do, particularly for those interested in European and UK dynamics.

Starting Tuesday, GBP traders will welcome the UK employment (releasing at 3:00 A.M on Tuesday) which will once again have a big influence on the next "live" Bank of England meeting on December 18th (live meaning that the decision should largely depend on upcoming data).

Major UK data continues on Thursday, same time, with the release of the Monthly and Quarterly GDP data.

The EU will also publish their own Employment and GDP figures on Friday at 6:00 A.M. (ET).

Of course, Euro traders will have to log in for the German CPI released in the Wednesday overnight session.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Except for a miracle, don't hope too much for the release of US Data like CPI and PPi this week (they will hopefully get published at some point towards the end of this month or the next).

Safe Trades and enjoy your weekend!

The Weekly Bottom Line: Consumer Sentiment Falls as Shutdown Enters 38th Day

Canadian Highlights

- Surprising forecasters, Canada gained 67k jobs in October and wages accelerated. The healthy jobs print could give a shot in the arm to consumer spending in the fourth quarter.

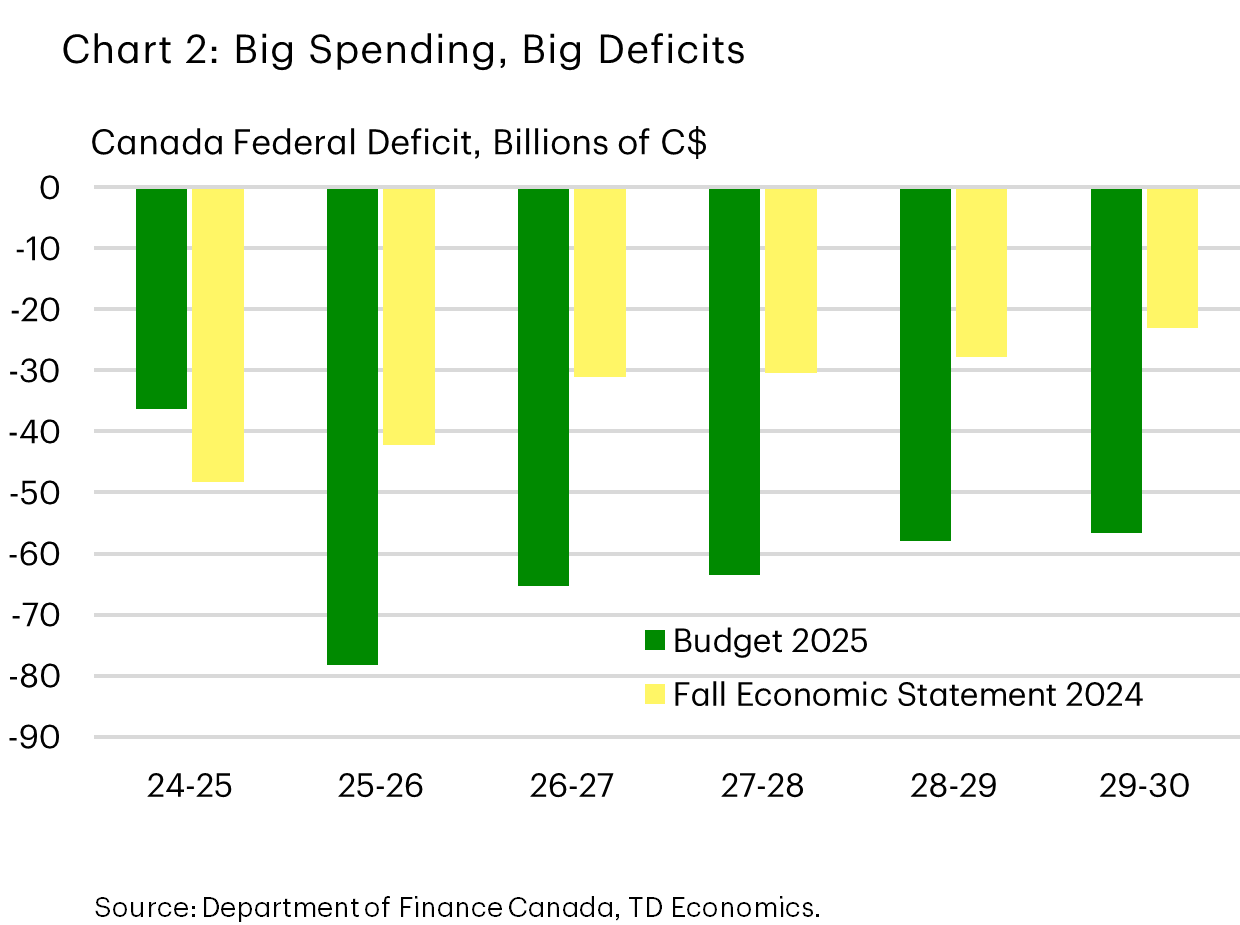

- Canada’s federal budget was heavy on spending commitments and will leave Canada with larger deficits. Still, given ongoing uncertainty, more will need to be done to stimulate investment.

- The solid jobs report and stimulative budget have all but eliminated the chance of a near-term BoC cut.

U.S. Highlights

- The U.S. government shutdown officially became the longest in history, passing the 35-day record set in 2019 on Wednesday.

- The dearth of official data has us looking to alternative indicators which point to some further cooling in the labor market.

- Other data show that consumer confidence has weakened since January and has fallen to near-record lows this month.

Canada – Fortune Favours the Hold

There was plenty for markets to digest this week, with a jobs report and of, course, the federal government’s massively hyped budget (see our analysis of the latter here).

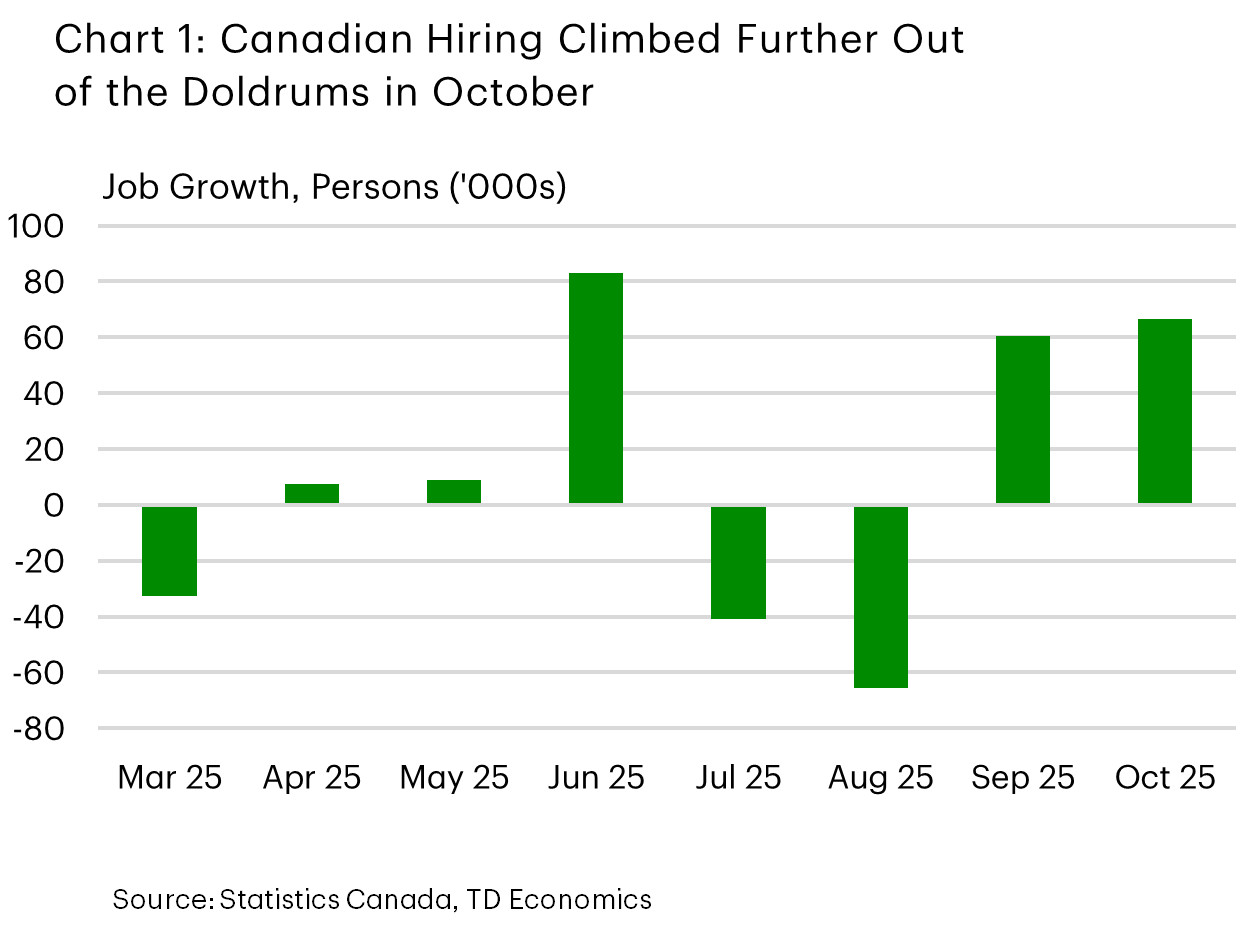

Surprising consensus forecasts yet again, Canada’s job market delivered a solid performance last month, with 67k jobs gained (Chart 1). This marked the second straight sizeable monthly increase, and, together with September’s gain, erased declines observed in July and August. What’s more, the unemployment rate dipped 0.2 percentage points, average hourly wage growth accelerated, and even U.S.-levered industries like manufacturing and transportation/warehousing saw job growth. Of course, it’s rarely the case that we get a jobs report where all aspects point in one direction. This time, the fly in the ointment was that gains were concentrated in part-time positions. Also, hours worked were down 0.2% month-on-month due to labour disputes, which will weigh on output in October. Still, this was a healthy print, which could help support consumption at a time when the economy needs a boost.

At long last, the federal government delivered its budget this week. Billed as a blueprint that would transform the Canadian economy, we have a few key takeaways. Deficits are here to say (Chart 2). This year’s shortfall is pegged at 2.5% of GDP, an unusually large deficit for Canada. However, Canada still stacks up well in relation to other G-7 countries, and it’s the same story for the country’s debt burden, even with net debt-to-GDP forecast to climb above 43% over the projection horizon. Markets didn’t seem overly worried about Canada’s fiscal deterioration, with bond yields effectively unchanged in the wake of the budget and the Canadian dollar down only a smidge. The decision to split the budget balance into capital and operating balances did little except provide a fiscal anchor (i.e. balancing the operating budget by FY 2028/29).

Deficits reflect heavy spending commitments on personal tax relief, defense, housing, corporate tax incentives and infrastructure. Some savings offsets are penciled in on workforce reductions and operational efficiencies. This is a sea change from the prior government, which focused on income support or “affordability” measures for different sectors and populations. In a speech this week, Bank of Canada Governor Macklem agreed with this sentiment.

Infrastructure spending and tax initiatives do change the calculus for firms considering investments, but given uncertainty, this budget alone likely won’t be enough to get companies off the sidelines, especially as Canada’s regulatory burden is left largely unaddressed. Also, much will depend on the execution and uptake of the policies set out in the fiscal blueprint.

For the Bank of Canada, the stimulative aspects of the federal budget, coupled with a solid jobs report, have dealt a serious blow to the odds of follow up rate cuts. Markets have effectively priced-out a move in December. We would agree and see the central bank leaving its policy rate unchanged through next year.

U.S. – Consumer Sentiment Falls as Shutdown Enters 38th Day

The current shutdown of the U.S. government became the longest in history this week, entering its 36th day on Wednesday. The outlook for resolving the shutdown is as murky as ever. While new compromises are being floated, confidence from lawmakers seems low. Pressure will build as constituents have to tolerate travel delays, cuts in food aid, and other more visible signs of the shutdown the longer it goes on. Just as cloudy is the picture of how the economy has been evolving since August, the last month covered by official statistics for most measures.

The dearth of federal government data has us looking to other indicators to assess the state of the economy. The preliminary November reading for the Michigan Survey of Consumer Sentiment showed consumer confidence sliding for a fourth consecutive month – reaching a three-year low. Most of the pullback was due to a further decline in consumers’ perception of current economic conditions, which fell to the lowest level on record (dating back to early 1980’s). The survey also showed that inflation expectations remained elevated at 4.7%. Moreover, only 37% of surveyed households think that “now is a good time to purchase large household goods” – the lowest level since 2022 when the Fed first started to raise its policy rate. And this negative sentiment appears to be spilling over to the hard data, with vehicle sales falling to a 17-month low of 15.3 million in October.

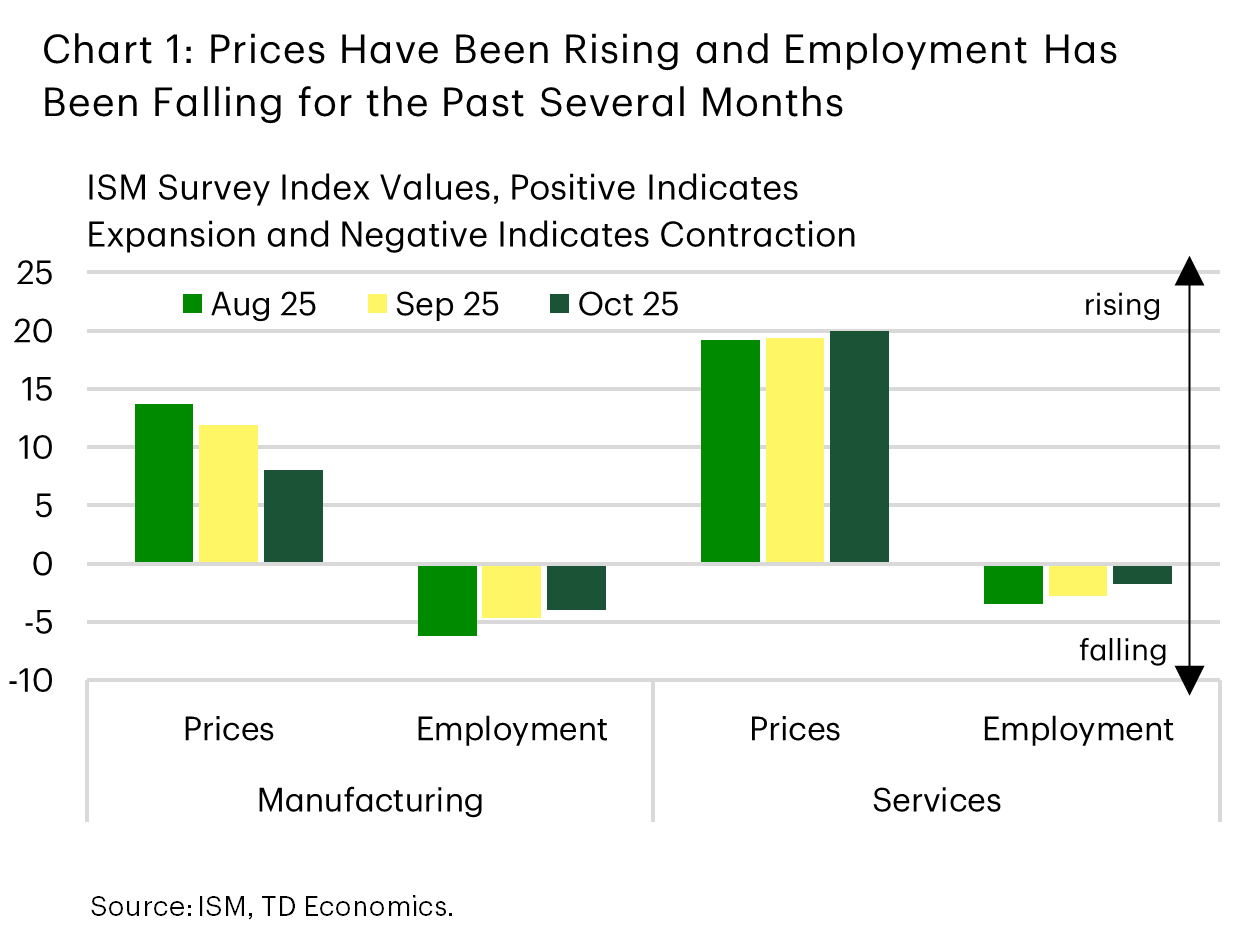

The ISM monthly surveys of firms in the manufacturing and service sector are usually helpful indicators of the direction of the economy. Across both sectors, employment remains in contractionary territory, but encouragingly, has been declining at a slower rate. Meanwhile, price growth remains elevated, particularly in the services sector (Chart 1), which complicates the interest rate outlook, especially given the firming in inflation expectations in the Michigan Survey.

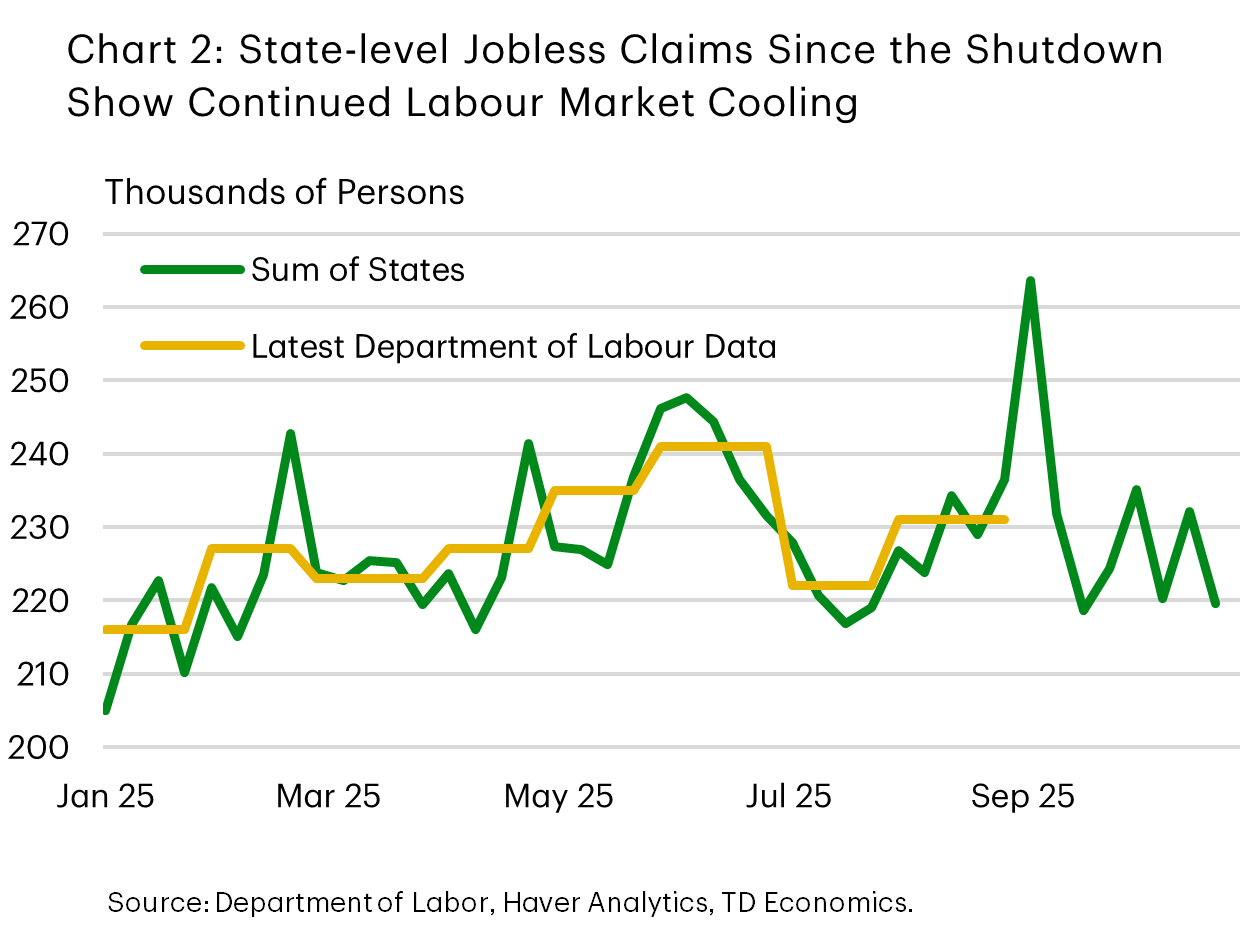

Outside of the ISM’s, we also received several other alternative private sector readings on the labor market. ADP estimates of private payrolls rose 42k in October – a modest pick-up from September where job growth contracted by 29k – bringing the three-month moving average to a meager 3k per-month. Meanwhile, Challenger job cuts surged to 153k last month – a six-month high. The Chicago Fed’s estimate of the unemployment rate ticked a touch higher to 4.4% for October. But encouragingly, state-level jobless claims remain low and relatively stable (Chart 2). Federal Reserve Governor Lisa Cook noted this week that hiring is slowing according to job posting data.

While this slew of indicators is mixed, with some showing more weakness than others, the overall message is that the job market is probably hanging in a state of semi-stasis, what we have been calling “low hire, low fire”. As we turn the page on this week, the big question still in our heads is how long we will be looking at the economy through this clouded, half-closed lens – and for that, we will need to see if there is any hope of the government shutdown resolving soon.

Weekly Economic & Financial Commentary: Supreme Court Hears Tariff Case

Summary

United States: Labor Market Continues to Tread Water

- The longest government shutdown on record continues to drag on. Private sector data show hiring remains weak, but layoffs remain contained. That said, the pressure to trim headcount appears to be broadening, as cost pressures continue to mount and tariff uncertainty persists.

- Next week: NFIB Small Business Optimism Index (Tue.)

International: Global Policy Pause: A Week of Holds with One Exception

- This week, several central banks across both G10 and emerging markets convened to assess monetary policy, with most opting to keep interest rates unchanged. The Bank of England, Riksbank, Norges Bank, Reserve Bank of Australia and Brazil’s Central Bank all held their respective policy rates steady. The only exception was Banxico, which delivered a rate cut, albeit with a hawkish tilt.

- Next week: U.K. GDP (Thu.), China Industrial Production and Retail Sales (Fri.)

Topic of the Week: Supreme Court Hears Tariff Case

- Wednesday’s oral arguments provided the first indication of how the U.S. Supreme Court will strike down President Trump’s tariffs under the International Emergency Economic Powers Act (IEEPA). No matter what the Court decides, the high-tariff environment is set to remain.

Forward Guidance: Canada’s Industry Data to Show Stabilization in Trade Exposed Sectors

We are looking for cautious optimism in Canada’s manufacturing and wholesale reports for September in the coming week.

Manufacturing has borne the brunt of the negative fallout from U.S. tariffs since spring. Production contracted an annualized 9% in Q2. That was the largest one quarter decline outside of the 2020 pandemic since the 2008/09 recession.

But, the sector has shown signs of stabilizing. Average production over July and August is little changed from Q2, and the advance estimate of manufacturing sales in September jumped 2.8%. Part of that increase likely reflects higher prices. Canadian industrial output prices rose1.3%, seasonally adjusted, by our count in September led by higher petroleum prices. That still leaves volume up 1 ½ % from August.

Most Canadian exports have remained duty free under exemptions for CUSMA compliant trade. Details in manufacturing sales next Friday will be closely watched to gauge the impact of U.S. tariffs on targeted subsectors. Early evidence is starting to suggest that tariff impact on these sectors may have been smaller than feared with U.S. buyers appearing to struggle to find alternative cheaper sources.

Unfilled Canadian manufacturing orders were still up 4.6% from a year ago, and 2.7% since March as of August. Exports of steel products have fallen sharply, but aluminum production and prices are both up from a year ago (1.8% in August and 15% in September, respectively). Employment in the aluminum sector (from SEPH data) was up 8% since March as of August.

Concerns remain about the outlook for motor vehicles, but the number of vehicles produced in Canada in September was slightly above year ago levels.

Jobs in manufacturing and wholesale are up

The advance estimate of September wholesale sales (ex-petroleum) from Statistics Canada was little changed after declining 1.2% in August, but rising 1.7% in July. That would leave sales up an annualized 5% in Q3. Seasonally adjusted, September saw the largest monthly increase in both manufacturing and wholesale employment since January.

Overall, stabilizing industry data are in line with steadying trade flows in Q3. It suggests CUSMA exemptions are still working effectively to backstop the bulk of Canada-U.S. trade even as the details after July can’t be directly reported from U.S. Census Bureau’s trade data that’s critically delayed by the ongoing U.S. government shutdown.

U.S. data including October’s consumer price index and retail sales will not be released on schedule in the coming week. Not only is reading the U.S. economy becoming increasingly foggy, the shutdown— now at a record—is having a larger direct economic impact, especially if crucial SNAP benefits are curtailed.

Summary 11/10 – 11/14

Monday, Nov 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 05:00 | JPY | Leading Economic Index Sep P | 107.9 | 107 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -3.9 | -5.4 |

| 23:30 | AUD | Westpac Consumer Confidence Nov | -3.50% | |

| 23:50 | JPY | Bank Lending Y/Y Oct | 3.80% | 3.80% |

| 23:50 | JPY | Current Account (JPY) Sep | 2.26T | 2.46T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 05:00 | JPY | Leading Economic Index Sep P | |

| Forecast: 107.9 | Previous: 107 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | |

| Forecast: -3.9 | Previous: -5.4 | ||

| 23:30 | AUD | Westpac Consumer Confidence Nov | |

| Forecast: | Previous: -3.50% | ||

| 23:50 | JPY | Bank Lending Y/Y Oct | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 23:50 | JPY | Current Account (JPY) Sep | |

| Forecast: 2.26T | Previous: 2.46T | ||

Tuesday, Nov 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Oct | 7 | |

| 00:30 | AUD | NAB Business Conditions Oct | 8 | |

| 02:00 | NZD | RBNZ Inflation ExpectationsQ4 | 2.28% | |

| 05:00 | JPY | Eco Watchers Survey: Current Oct | 47.6 | 47.1 |

| 07:00 | GBP | Claimant Count Change Oct | 20.3K | 25.8K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 4.90% | 4.80% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 4.90% | 5.00% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 4.60% | 4.70% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 42.5 | 39.3 |

| 10:00 | EUR | Germany ZEW Current Situation Nov | -80 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 23.5 | 22.7 |

| 11:00 | USD | NFIB Business Optimism Index Oct | 98.3 | 98.8 |

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Oct | |

| Forecast: | Previous: 7 | ||

| 00:30 | AUD | NAB Business Conditions Oct | |

| Forecast: | Previous: 8 | ||

| 02:00 | NZD | RBNZ Inflation ExpectationsQ4 | |

| Forecast: | Previous: 2.28% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Oct | |

| Forecast: 47.6 | Previous: 47.1 | ||

| 07:00 | GBP | Claimant Count Change Oct | |

| Forecast: 20.3K | Previous: 25.8K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | |

| Forecast: 4.90% | Previous: 4.80% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | |

| Forecast: 4.90% | Previous: 5.00% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | |

| Forecast: 4.60% | Previous: 4.70% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | |

| Forecast: 42.5 | Previous: 39.3 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | |

| Forecast: | Previous: -80 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | |

| Forecast: 23.5 | Previous: 22.7 | ||

| 11:00 | USD | NFIB Business Optimism Index Oct | |

| Forecast: 98.3 | Previous: 98.8 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | |

| Forecast: | Previous: 1.60% | ||

Wednesday, Nov 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | 9.90% | |

| 07:00 | EUR | Germany CPI M/M Oct F | 0.30% | 0.30% |

| 07:00 | EUR | Germany CPI Y/Y Oct F | 2.30% | 2.30% |

| 13:30 | CAD | Building Permits M/M Sep | 0.90% | -1.20% |

| 18:30 | CAD | BoC Summary of Deliberations | ||

| 23:50 | JPY | PPI Y/Y Oct | 2.50% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | |

| Forecast: | Previous: 9.90% | ||

| 07:00 | EUR | Germany CPI M/M Oct F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 07:00 | EUR | Germany CPI Y/Y Oct F | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 13:30 | CAD | Building Permits M/M Sep | |

| Forecast: 0.90% | Previous: -1.20% | ||

| 18:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 23:50 | JPY | PPI Y/Y Oct | |

| Forecast: 2.50% | Previous: 2.70% | ||

Thursday, Nov 13, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | 4.80% | |

| 00:01 | GBP | RICS Housing Price Balance Oct | -14% | -15% |

| 00:30 | AUD | Employment Change Oct | 20.3K | 14.9K |

| 00:30 | AUD | Unemployment RateOct | 4.40% | 4.50% |

| 07:00 | GBP | GDP M/M Sep | 0.00% | 0.10% |

| 07:00 | GBP | GDP Q/Q Q3 P | 0.20% | 0.30% |

| 07:00 | GBP | Industrial Production M/M Sep | -0.10% | 0.40% |

| 07:00 | GBP | Industrial Production Y/Y Sep | -0.70% | |

| 07:00 | GBP | Manufacturing Production M/M Sep | -0.30% | 0.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Sep | -0.80% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -20.8B | -21.2B |

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.10% | -0.20% |

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | -1.80% | |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | 0.80% | -1.20% |

| 17:00 | USD | Crude Oil Inventories (Nov 7) | 5.2M | |

| 21:30 | NZD | Business NZ PMI Oct | 49.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | |

| Forecast: | Previous: 4.80% | ||

| 00:01 | GBP | RICS Housing Price Balance Oct | |

| Forecast: -14% | Previous: -15% | ||

| 00:30 | AUD | Employment Change Oct | |

| Forecast: 20.3K | Previous: 14.9K | ||

| 00:30 | AUD | Unemployment RateOct | |

| Forecast: 4.40% | Previous: 4.50% | ||

| 07:00 | GBP | GDP M/M Sep | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 07:00 | GBP | GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 07:00 | GBP | Industrial Production M/M Sep | |

| Forecast: -0.10% | Previous: 0.40% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | |

| Forecast: | Previous: -0.70% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | |

| Forecast: -0.30% | Previous: 0.70% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | |

| Forecast: | Previous: -0.80% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | |

| Forecast: -20.8B | Previous: -21.2B | ||

| 07:30 | CHF | Producer and Import Prices M/M Oct | |

| Forecast: 0.10% | Previous: -0.20% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | |

| Forecast: | Previous: -1.80% | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | |

| Forecast: 0.80% | Previous: -1.20% | ||

| 17:00 | USD | Crude Oil Inventories (Nov 7) | |

| Forecast: | Previous: 5.2M | ||

| 21:30 | NZD | Business NZ PMI Oct | |

| Forecast: | Previous: 49.9 | ||

Friday, Nov 14, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Oct | 5.60% | 6.50% |

| 02:00 | CNY | Retail Sales Y/Y Oct | 2.70% | 3.00% |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Oct | -0.70% | -0.50% |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | 0.30% | -0.40% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.20% | 0.20% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 9.7B | |

| 13:30 | CAD | Manufacturingles M/M Sep | 2.80% | -1.00% |

| 13:30 | CAD | Wholeleles M/M Sep | 0.00% | -1.20% |

| 15:30 | USD | Natural Gas Storage (Nov 7) | 33B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Oct | |

| Forecast: 5.60% | Previous: 6.50% | ||

| 02:00 | CNY | Retail Sales Y/Y Oct | |

| Forecast: 2.70% | Previous: 3.00% | ||

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Oct | |

| Forecast: -0.70% | Previous: -0.50% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Sep | |

| Forecast: 0.30% | Previous: -0.40% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | |

| Forecast: | Previous: 9.7B | ||

| 13:30 | CAD | Manufacturingles M/M Sep | |

| Forecast: 2.80% | Previous: -1.00% | ||

| 13:30 | CAD | Wholeleles M/M Sep | |

| Forecast: 0.00% | Previous: -1.20% | ||

| 15:30 | USD | Natural Gas Storage (Nov 7) | |

| Forecast: | Previous: 33B | ||