Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1682; (P) 1.1714; (R1) 1.1766; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7935; (P) 0.7972; (R1) 0.7994; More….

Intraday bias in USD/CHF remains neutral as range trading continues. Risk will stay on the downside as long as 0.8071 resistance holds. Below 0.7914 will bring retest of 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

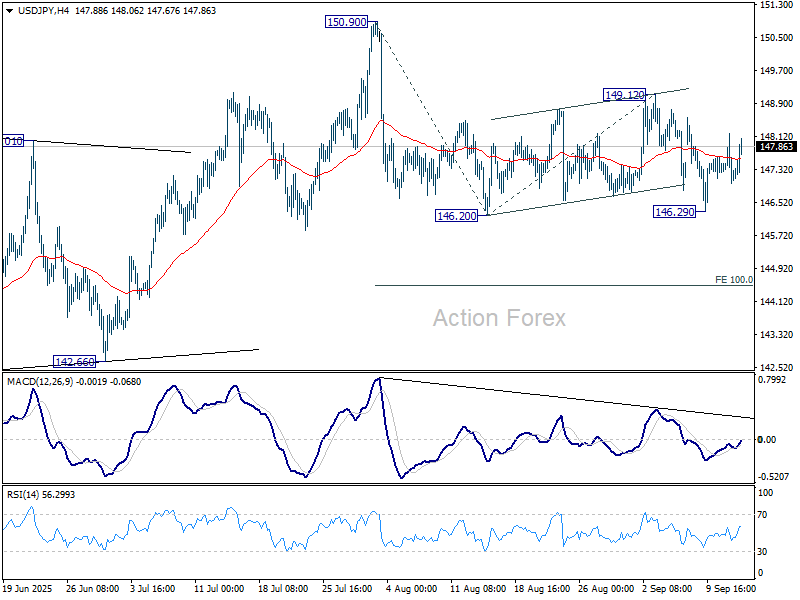

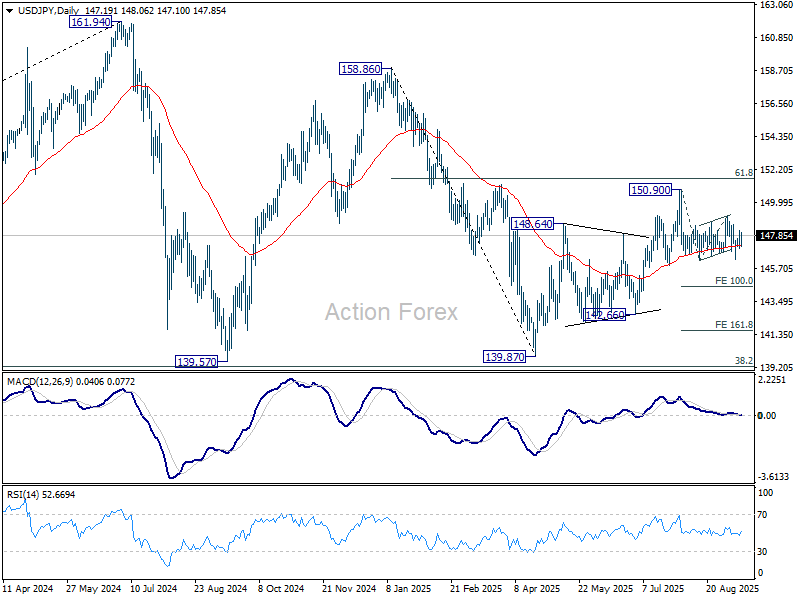

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.75; (P) 147.47; (R1) 147.94; More...

Range trading continues in USD/JPY and intraday bias stays neutral at this point. Risk will stay on the downside as long as 149.12 resistance holds. Firm break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.16) will argue that whole rebound from 139.87 has completed with three waves up to 150.90.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

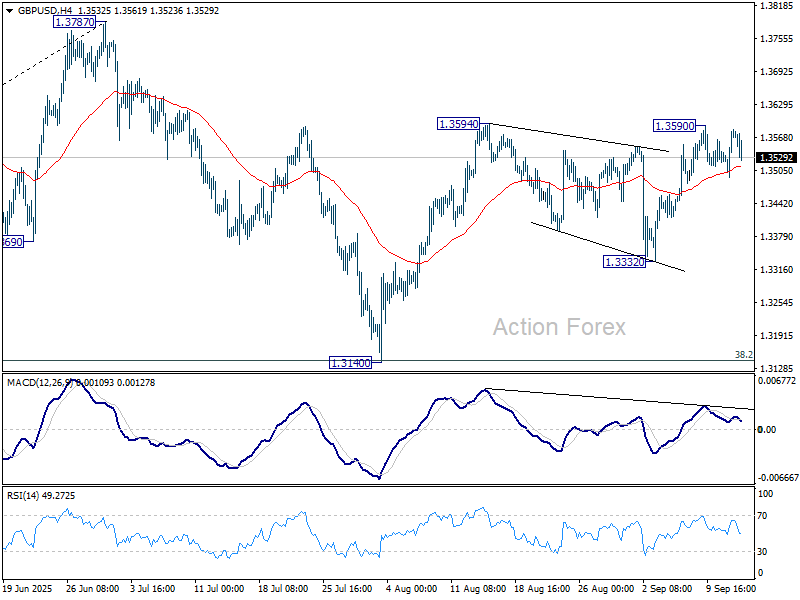

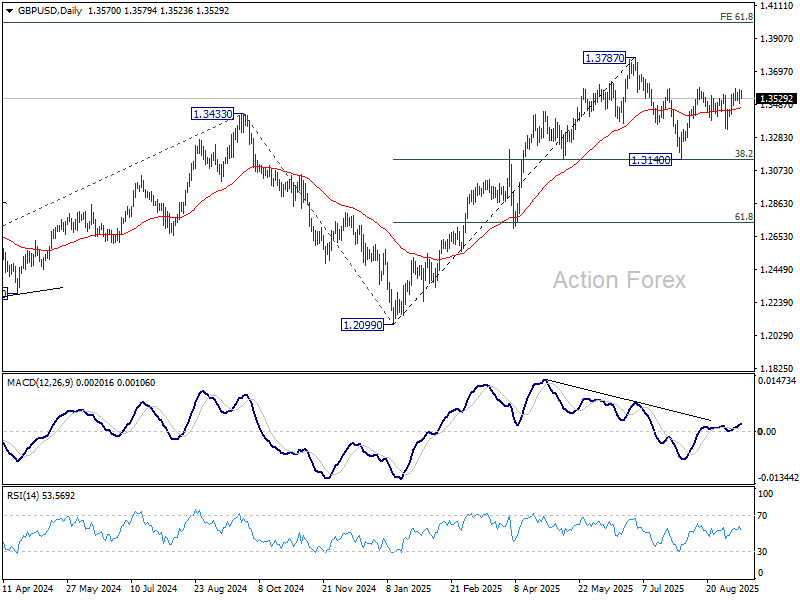

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3517; (P) 1.3550; (R1) 1.3606; More...

GBP/USD retreats mildly as consolidations continues below 1.3590 and intraday bias stays neutral. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

Dollar Recovers Slightly, But Fed Cut Bets Cap Upside

Dollar steadied today, recovering modestly after yesterday's selling, though the move lacked conviction. With investors convinced the Fed will cut rates next week, the greenback remains capped, unable to mount a broader rebound. For now, the greenback is only outperforming Yen and Loonie. Yen remains under pressure from buoyant risk appetite, with the Nikkei setting fresh records just shy of the 45,000 mark. Loonie, meanwhile, is weighed down by expectations that the BoC will resume easing at its upcoming meeting.

Attention later in the session may briefly turn to University of Michigan consumer sentiment and inflation expectations. Still, any reaction is likely to be fleeting, as traders begin winding down ahead of the weekend and with next week’s FOMC meeting looming.

Weekly performance rankings show Aussie comfortably in the lead, followed by Kiwi and then Sterling. The Pound drew some support from a BoE survey showing rising public inflation expectations. At the bottom of the table, Yen is the weakest performer, followed by Loonie and then Euro. Dollar and Swiss Franc are positioned in the middle.

In Europe, at the time of writing, FTSE is up 0.36%. CAC is down -0.06%. CAC is down -0.26%. UK 10-year yield is up 0.047 at 4.657. Germany 10-year yield is up 0.06 at 2.72. Earlier in Asia, Nikkei rose 0.89%. Hong Kong HSI rose 1.16%. China Shanghai SSE fell -0.12%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.024 to 1.602.

UK inflation expectations rise, BoE survey shows

The BoE/Ipsos Inflation Attitudes Survey showed UK households nudging inflation expectations higher. Median expectations for inflation over the next year rose to 3.6% from 3.2% in May, while two-year expectations climbed to 3.4% from 3.2%. Longer-term inflation expectations, five years out, also ticked up to 3.8% from 3.6%.

Concerns over rising prices were tied to broader pessimism about growth. By a margin of 69% to 6%, respondents said the economy would end up weaker rather than stronger if inflation accelerated, compared with 67% to 5% in May.

On the interest rate outlook, 33% of respondents expected rates to rise over the next 12 months, unchanged from May. But more people now expect stability, with 26% seeing no change versus 21% in May. The share expecting cuts fell to 29% from 34%, suggesting households are adjusting to the prospect of “higher for longer” rates.

When asked what would be best for the economy, 33% favored lower rates, down from 37% in May. Meanwhile, 28% preferred no change, up from 26%, and 14% wanted higher rates, up slightly from 12%. The responses suggest growing acceptance that policy will remain restrictive even as concerns about inflation remain elevated.

UK GDP stalls in July, services offset weak production

UK GDP was flat in July, matching expectations, as modest growth in services and construction offset a sharp drop in production. Services output rose 0.1% and construction gained 0.2%, while production fell -0.9%, highlighting ongoing weakness in the industrial sector.

Over the three months to July, GDP rose 0.2% compared with the previous three-month period. Services expanded 0.4% and remained the key driver of growth, while production fell -1.3% and construction rose 0.6%.

ECB officials stress uncertainty, keep options open after rate hold

Several ECB policymakers weighed in after the Governing Council held deposit rate steady at 2.00% yesterday.

Latvian member Martins Kazaks argued the central bank should not provide forward guidance given high geopolitical and economic uncertainty. He said December’s meeting will be crucial, as new staff forecasts will help determine whether inflation is deviating from target in a significant or persistent way.

Kazaks also flagged external factors, including the Euro’s strength— which can suppress import prices— and potentially deflationary Chinese exports as downside risks. “Uncertainty is high,” he said, adding this justifies a cautious, meeting-by-meeting policy stance.

Olli Rehn of Finland struck a similar note, warning about the disinflationary impact of cheaper energy and a stronger currency. He stressed the importance of avoiding inflation moving “too much below or too much above” the 2% objective,.

France’s Francois Villeroy de Galhau left the door open to further easing, saying “another rate cut is entirely possible” in coming meetings.

NZ BNZ manufacturing slips to 49.9, sector weakness persists, optimism patchy

The latest BusinessNZ PMI showed New Zealand’s manufacturing sector stalling in August, with the index slipping to 49.9 from 52.8. BusinessNZ’s Catherine Beard noted the industry “has yet to turn the corner toward sustained growth,” with the reading underscoring patchy conditions and fragile confidence despite being only marginally below the neutral threshold.

The breakdown highlighted a mixed picture. New Orders rose strongly to 55.2, the highest in two years, hinting at improving demand momentum, while raw material deliveries remained in expansion at 50.5. Offsetting this, production fell to 46.6, while employment (49.1) and finished stocks (47.1) also contracted, dragging the overall index lower.

Nearly six in ten respondents offered negative comments, citing flat sales, customer caution, rising costs, and global uncertainty as key drags. Although the proportion of negative feedback has eased from June’s high, sentiment remains weak, and businesses see recovery as tentative at best.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3517; (P) 1.3550; (R1) 1.3606; More...

GBP/USD retreats mildly as consolidations continues below 1.3590 and intraday bias stays neutral. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

WTI Crude Technical: Weakness Prevails Below US$64.36/Barrel as Geopolitical Risk Premium Fizzles Out

The price actions of the West Texas Oil CFD (a proxy for the WTI crude futures) have declined by -7% from the 2 September 2025 high of US$66.52 to last Friday, 5 September 2025 low of US$61.85 on the backdrop of a weaker global demand, primarily on the deteriorating US labour market.

The recent bounce of 4% from its 5 September 2025 low to Wednesday, 10 September 2025 high of US$64.27 has been attributed to OPEC+’s modest production hike of 137,000 barrels per day (bpd) from October, announced on Sunday, 7 September significantly smaller than the previous monthly hikes of about 555,000 bpd in August and September, and 411,000 bpd in June and July as well as an uptick in geopolitical risk premium factor.

Interestingly, the three consecutive days of rallies on the West Texas Oil CFD were halted on Thursday, 11 September, during the Asia session before the release of US CPI inflation and weekly initial jobless claims data.

Let’s now examine the short-term (1 to 3 days) trajectory of the West Texas Oil CFD, the key levels to watch, and key elements ahead of the release of a key demand-related US economic data, the preliminary September reading of the University of Michigan’s consumer sentiment, out later today at 14:00 GMT.

Fig. 1: West Texas Oil CFD minor trend as of 12 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

A continuation of the West Texas Oil CFD’s minor downtrend phase from the 2 September 2025 high of US$66.52.

Bearish bias below US$64.10/64.36 key short-term pivotal resistance to expose the next immediate supports at US$61.30 and US$60.60/60.10 (also close to a Fibonacci extension).

Key elements

- The price actions of West Texas Oil CFD have staged a bearish reaction right at the downward sloping 20-day moving average and broken below the minor ascending support from the 5 September 2025 low.

- The hourly RSI momentum indicator has inched high, and it is now fast approaching its overbought region (above 70), which suggests that the current intraday bounce of 2.3% from today (Friday), 12 September, Asian session low of US$61.93 may fizzle out soon.

Alternative trend bias (1 to 3 days)

A clearance above US$64.36 invalidates the bearish scenario and triggers a mean reversion rebound towards the next intermediate resistances at US$65.00 and US$66.00 (also close to the downward sloping 50-day moving average).

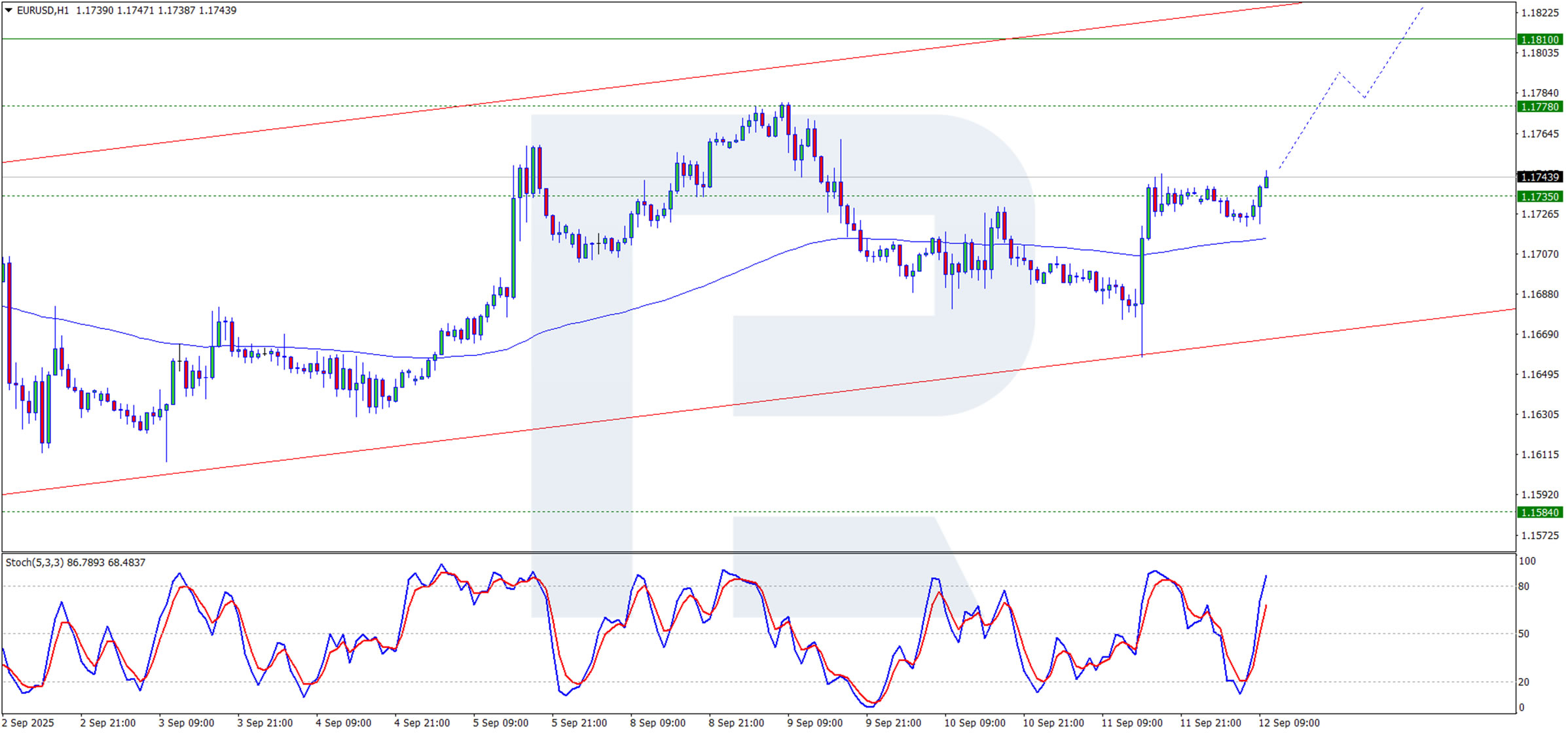

EUR/USD Digests Data Ahead of Fed Decision

The EUR/USD pair held steady around 1.1727 USD on Friday, as the US dollar remained under pressure following the release of inflation data that largely met expectations. The figures reinforce the Federal Reserve’s scope to ease monetary policy amid growing signs of labour market softening.

The US August inflation report showed consumer prices rose 0.4% month-on-month, slightly above the forecast of 0.3%, while the annual rate came in at 2.9%, matching expectations. Meanwhile, initial jobless claims increased by 27,000 to 263,000 – the highest level since 2021 – underscoring emerging weakness in the employment sector.

Interest rate futures now indicate a 93% probability of a 25-basis-point cut at the Fed’s 17 September meeting. Market speculation around a more aggressive 50-basis-point reduction is also gradually building.

Across the Atlantic, the European Central Bank left its key rate unchanged at 2.0% for the second consecutive meeting. In political developments, the US and Japan issued a joint statement emphasising that exchange rates should be market-determined and that excessive volatility is undesirable.

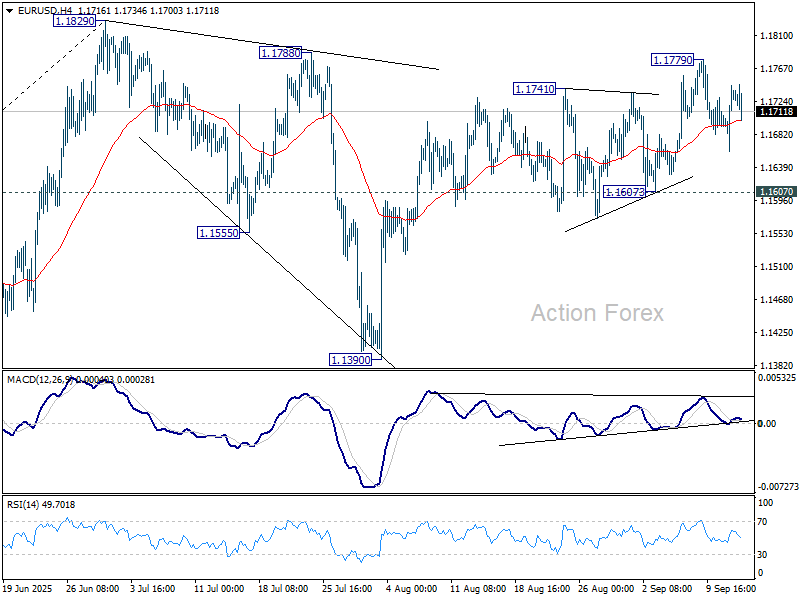

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD has completed an upward move towards 1.1735 USD. A sustained break above this resistance level signals a continuation of the broader uptrend. However, a short-term pullback toward this level – now potentially acting as support – cannot be ruled out.The MACD indicator supports further gains: both the histogram and signal line remain above zero and are rising, confirming bullish momentum. The primary outlook favours an extension towards 1.1810 USD, with a further target at 1.1870 USD, though intermittent corrections may occur.

H1 Chart:

On the H1 chart, the pair is testing resistance and showing signs of consolidation. A clear break above 1.1735 USD may trigger another leg higher. The Stochastic oscillator is testing the 80 level, suggesting strong upward momentum remains intact. The near-term upside target is 1.1810 USD.

Conclusion

EUR/USD remains well-supported as markets price in growing Fed dovishness, driven by softening labour data and stable inflation. With the ECB maintaining a steady stance and risk sentiment cautiously optimistic, the pair looks poised to extend gains, pending next week’s Fed decision. Technically, the path of least resistance appears upward, though a brief retracement may offer entry opportunities ahead of further advances.

UK inflation expectations rise, BoE survey shows

The BoE/Ipsos Inflation Attitudes Survey showed UK households nudging inflation expectations higher. Median expectations for inflation over the next year rose to 3.6% from 3.2% in May, while two-year expectations climbed to 3.4% from 3.2%. Longer-term inflation expectations, five years out, also ticked up to 3.8% from 3.6%.

Concerns over rising prices were tied to broader pessimism about growth. By a margin of 69% to 6%, respondents said the economy would end up weaker rather than stronger if inflation accelerated, compared with 67% to 5% in May.

On the interest rate outlook, 33% of respondents expected rates to rise over the next 12 months, unchanged from May. But more people now expect stability, with 26% seeing no change versus 21% in May. The share expecting cuts fell to 29% from 34%, suggesting households are adjusting to the prospect of “higher for longer” rates.

When asked what would be best for the economy, 33% favored lower rates, down from 37% in May. Meanwhile, 28% preferred no change, up from 26%, and 14% wanted higher rates, up slightly from 12%. The responses suggest growing acceptance that policy will remain restrictive even as concerns about inflation remain elevated.

ECB officials stress uncertainty, keep options open after rate hold

Several ECB policymakers weighed in after the Governing Council held deposit rate steady at 2.00% yesterday.

Latvian member Martins Kazaks argued the central bank should not provide forward guidance given high geopolitical and economic uncertainty. He said December’s meeting will be crucial, as new staff forecasts will help determine whether inflation is deviating from target in a significant or persistent way.

Kazaks also flagged external factors, including the Euro’s strength— which can suppress import prices— and potentially deflationary Chinese exports as downside risks. “Uncertainty is high,” he said, adding this justifies a cautious, meeting-by-meeting policy stance.

Olli Rehn of Finland struck a similar note, warning about the disinflationary impact of cheaper energy and a stronger currency. He stressed the importance of avoiding inflation moving “too much below or too much above” the 2% objective,.

France’s Francois Villeroy de Galhau left the door open to further easing, saying “another rate cut is entirely possible” in coming meetings.

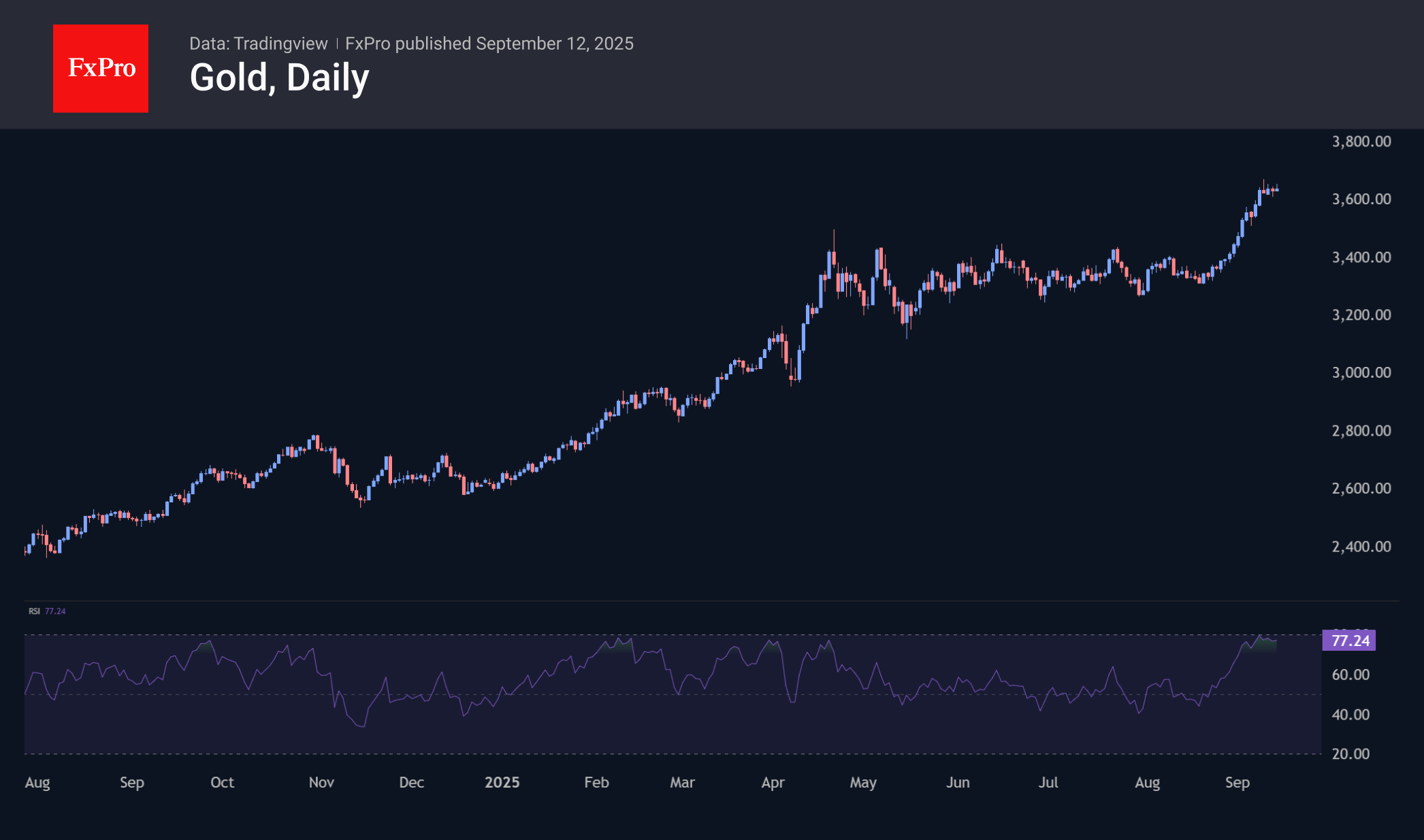

Gold Vulnerable to Sell-the-Fact Pattern Next Week

Gold reacts strongly to geopolitics and has reached another record high, rising for the fourth week in a row. Washington is ready to wage economic war on the Kremlin’s main allies, India and China, if Brussels supports it. As a result, there is an increased risk that central banks will step up their gold purchases as part of their reserve diversification and de-dollarisation processes.

Geopolitics has made the precious metal less sensitive to the Fed’s monetary policy. Even the resurgent US dollar has been unable to put a spoke in gold’s wheel. Neither could the White House’s announcement that it would exclude this asset from the list of potential tariffs.

If Donald Trump manages to drive a wedge between Russia, India, and China, oil prices will rise, and inflation will accelerate. A stagflationary environment and increased central bank purchases of bullion will help gold.

However, in the short term, we note technical overbought conditions after an impressive rise. This was reflected in the stabilisation of prices from Tuesday to Friday, contrary to the continued growth of silver and other precious metals and new highs in stock indices. In daily timeframes, the RSI gradually declines after touching the zone above 80. In 10 out of 11 cases over the past six years, such a signal has been followed by corrective pullbacks, which may well happen again this time.

The expected cut in the key rate on Wednesday risks triggering a “buy the rumours, sell the fact” pattern.