Sample Category Title

Markets Brace for a Fed Rate Cut

In focus this week

Multiple central bank rate decisions are on the agenda, with notably the FOMC meeting and Bank of Canada (BoC) on Wednesday, the Bank of England (BoE) and Norges Bank (NB) on Thursday, and the Bank of Japan (BoJ) on Friday. The FOMC, BoC and NB are expected to deliver a 25bp cut, while we anticipate that both the BoE and BoJ will keep rates unchanged. Regarding the details, the market will be closely watching the Federal Reserve's updated rate projections for clues on the pace of future easing.

Economic and market news

What happened overnight

In China, the monthly data package showed a further weakening of the economy in August across the board. Both consumption and housing moved a notch lower again with retail sales falling from 3.7% y/y to 3.4% y/y (cons 3.8%) and new home prices down 0.3% m/m following -0.31% m/m in July. Industrial production weakened as well, falling from 5.7% y/y to 5.2% y/y (consensus 5.6%). Investment growth also dropped, and unemployment moved higher. The data should ring some alarm bells in Beijing and, as we saw last autumn, pave the way for stronger stimulus signals soon. The weak demand situation contrasts with the strong development in the tech space, which has supported this year's equity rally. The market reaction has been muted with offshore equities actually slightly higher overnight and USD/CNH lower from 7.1275 to around 7.12. Markets are likely betting on stronger stimulus soon.

What happened over the weekend

In the euro area, the credit rating agency Fitch downgraded France to A+ from AA- citing political instability and rising debt. While we initially believed that France would be downgraded, the formation of a new government earlier this week led to speculation that Fitch might postpone the "inevitable". Prime Minister Lecornu is grappling with the challenge of implementing the spending cuts demanded by impatient investors, while simultaneously attempting to secure support from three ideologically diverse parliamentary blocs with conflicting approaches to budget reductions.

In the US, the University of Michigan's preliminary September consumer sentiment survey reported 1-year inflation expectations remaining elevated at 4.8%, while 5-year expectations rose to 3.9% from 3.5% in August. Both figures remain above the Federal Reserve's target. Although the market reaction was rather muted, we think this presents a compelling argument for a more gradual rate-cutting cycle rather than back-to-back cuts.

In the UK, GDP was unchanged in July compared to June, leaving y/y growth at 1.4% and slightly weaker than market expectations. Manufacturing output declined 1.3% m/m while services improved slightly, thus largely confirming the story from PMI data as well.

Equities: Equities were little changed on Friday. In the US, performance was supported by last week's decline in yields, which continued to fuel gains in big tech. The "Magnificent Seven" stocks rose another 1-2% on a light news flow, while Tesla advanced 7%. The S&P 500 and Stoxx 600 finished the day flat, whereas the Nasdaq gained 0.4%, closing at a fresh all-time high. Today's session also looks quiet, with futures little changed this morning. This still wraps up a strong week for equities, with US indices up 1.5% and Europe 1%. Importantly, the recent defensive rebound - led by healthcare - has stalled.

While focus often falls on the US when lower rates spark tech rallies, the impact has been even more pronounced in emerging markets. Korea's Kospi surged an impressive 7% last week, and China's Shenzhen index has climbed nearly 30% over the past three months. This strength comes despite signs that China's credit impulse and macro momentum have rolled over in past months. Like in the US, the link between broad macro fundamentals and equity prices appears to be breaking down due to AI.

FI and FX: A quiet end to a rather busy week as we saw global yields drifting slightly higher on Friday, with modest curve steepening on both sides of the Atlantic. For the week ahead, focus will be on no less than four G10 central bank meetings: the Fed, Bank of England, Bank of Japan and Norges Bank. In FX space, the USD closed the week on a weaker footing, with EUR/USD moving back above 1.1730. Scandies had a strong week, where especially the NOK stood out with EUR/NOK closing the week some 20 figures lower and NOK/SEK edging higher towards the 200dma at 0.9510.

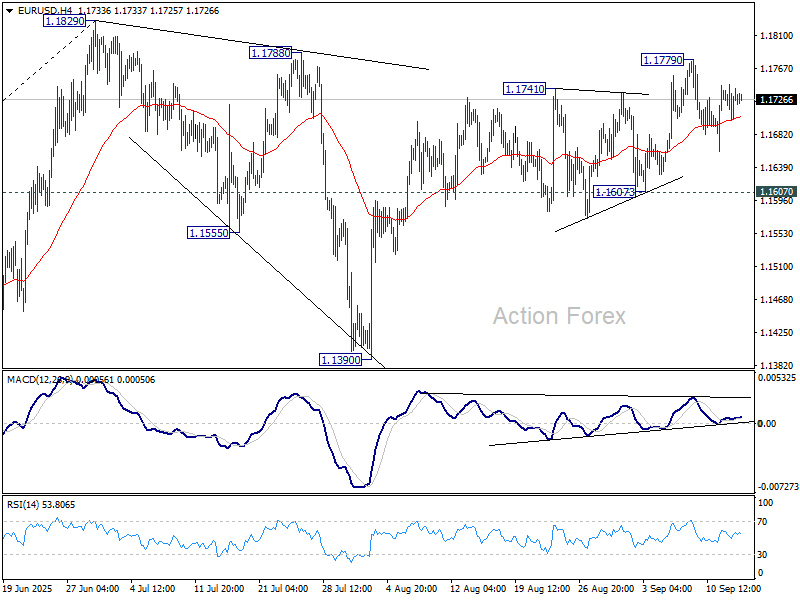

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1709; (P) 1.1728; (R1) 1.1756; More...

Range trading continues in EUR/USD and intraday bias remains neutral. With 1.1607 support intact, further rise is expected. On the upside, above 1.1779 will target a retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 55 W EMA (now at 1.1174) holds.

Traders Look Past Weak China Data, Eye Fed and Madrid Talks

Forex markets were subdued in Asian session today, with major pairs showing little movement while regional equities held steady. The muted tone comes despite a disappointing run of Chinese economic data, which showed broad weakness in activity. Investors appeared reluctant to extrapolate too much pessimism from the Chinese numbers. Instead, the data reinforced expectations that Beijing will be forced to accelerate stimulus measures. For traders, the prospect of stronger state support is cushioning risk sentiment, limiting downside pressure on Asian assets.

The policy outlook in China remains closely tied to the Fed. Once the Fed’s rate-cut path is clearly defined, the PBoC will have greater room to ease without triggering destabilizing capital outflows. That dynamic has kept speculation alive of further PBoC cuts in the months ahead, especially as growth signals soften.

While markets are steady for now, volatility is expected to rise sharply this week with four major central bank meetings on deck. The Fed takes center stage, with a widely expected rate cut that carries unusually high risks due to voting splits and fresh economic projections. The BoC, BoE, and BoJ decisions will also be closely watched, alongside a heavy data calendar that includes UK jobs, CPI, and retail sales, Germany’s ZEW survey, Australian employment, and New Zealand GDP.

While monetary policy dominates, geopolitics is also back in play. High-level U.S.–China trade talks kicked off in Madrid on Sunday, bringing together Treasury Secretary Bessent and USTR Greer with Vice Premier He Lifeng and chief negotiator Li Chenggang. The meeting follows July’s Stockholm discussions that extended a 90-day tariff truce and reopened rare-earth exports to the U.S. That extension keeps the pressure on Beijing while limiting near-term escalation.

Still, expectations for a breakthrough remain muted. There is little chance of a major agreement, with another temporary extension the most likely outcome. Markets are particularly focused on whether Washington delays the Sept. 17 deadline for ByteDance to divest TikTok’s U.S. operations, a decision that could otherwise trigger a ban.

In Asia, at the time of writing, Nikkei is up 0.89%. Hong Kong HSI is up 0.19%. China Shanghai SSE is down -0.17%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is flat at 1.602.

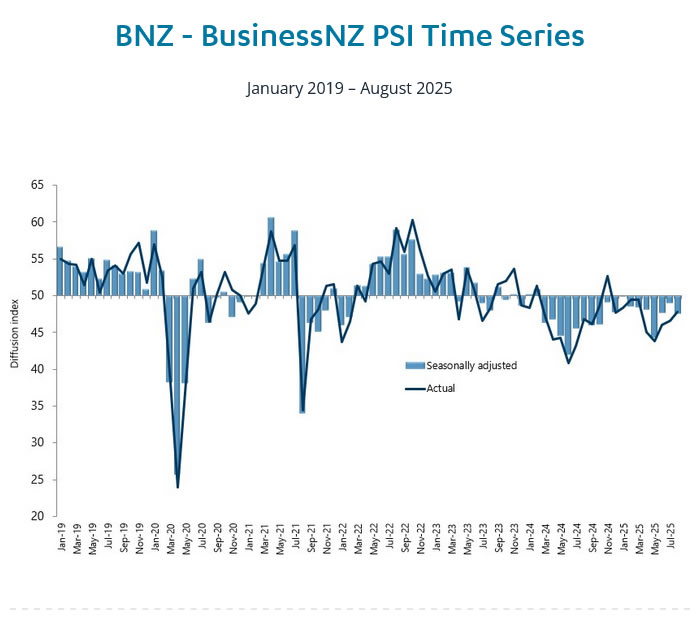

NZ services PMI slumps to 47.5, 18th month contraction

New Zealand’s services sector deteriorated further in August, with BusinessNZ Performance of Services Index slipping from 48.9 to 47.5, well below the long-run average of 52.9. The reading also marks the 18th consecutive month of contraction. Both

Activity/Sales (46.2) and New Orders/Business (47.8) weakened, suggesting demand remains fragile. Employment improved slightly to 48.3 but remains in contraction territory, reflecting businesses’ reluctance to expand payrolls in the face of subdued activity.

The survey showed 59.6% of respondents made negative comments in August, an increase from July but still less pessimistic than June’s tally. Firms cited multiple pressures, including high interest rates, sticky inflation, and the cost-of-living squeeze eroding household spending. Rising operating costs, seasonal slowdowns, supply chain disruptions, and uncertainty over government policy also weighed on sentiment.

China industrial output, retail sales miss forecasts, fixed asset investment slumps

China’s economy slowed in August, with key indicators falling short of expectations. Industrial output grew 5.2% yoy, down from 5.7% yoy in July and short of forecasts for 5.8% yoy, marking its weakest pace since August 2024. Retail sales also slowed, rising just 3.4% yoy versus 3.7% yoy previously and expectations of 3.8% yoy, signaling soft household demand despite ongoing government measures to support spending.

Investment activity showed the sharpest loss of momentum. Year-to-date fixed asset investment rose only 0.5%, far weaker than consensus 1.4% and July’s 1.6%. The drag came primarily from the property sector, where real estate investment plunged -12.9% in the first eight months. Excluding real estate, investment rose 4.2%.

The National Bureau of Statistics highlighted “many unstable and uncertain factors” in the global environment and warned that the economy still faces “multiple risks and challenges.” It urged stronger policy implementation to stabilize employment, businesses, and expectations, but the latest figures suggest momentum remains fragile, with property weakness continuing to weigh heavily on growth prospects.

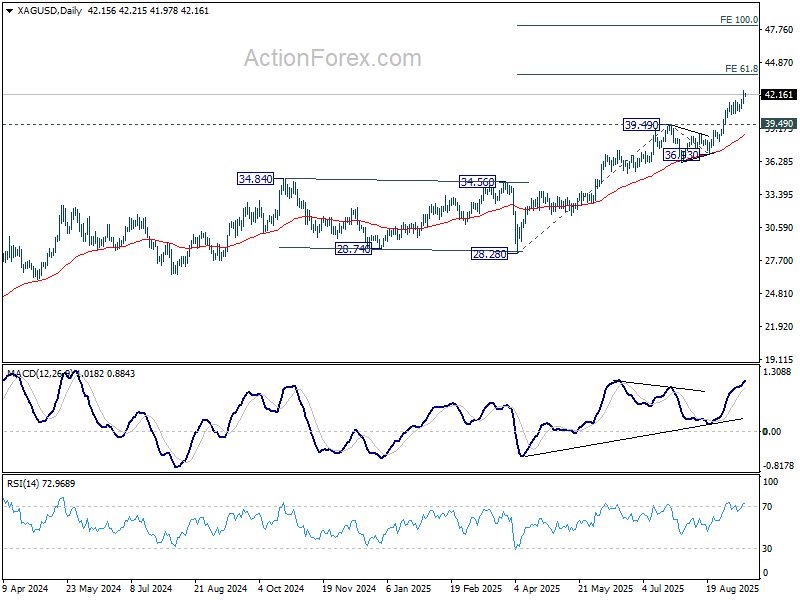

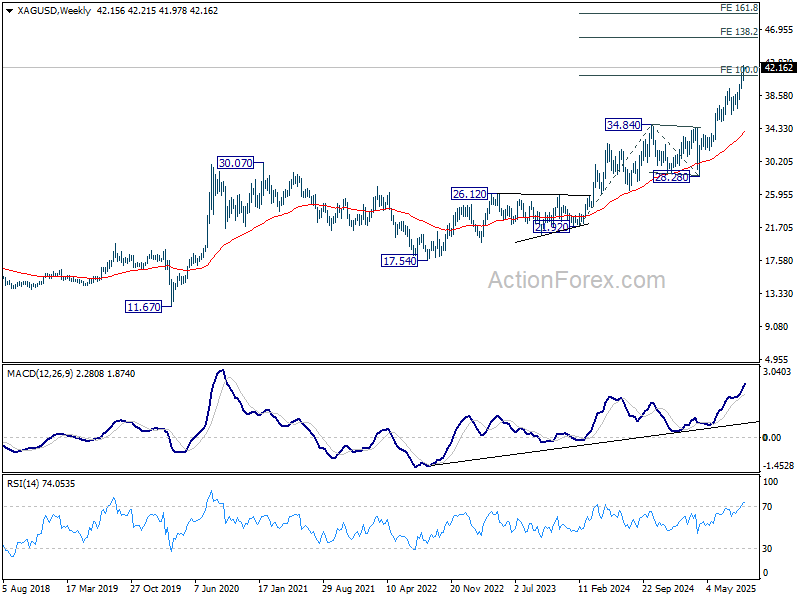

Silver steals spotlight, charging toward 50 while Gold pauses

Precious metals remain firmly bid, but leadership has shifted. Gold’s rally stalled just ahead of a key Fibonacci projection, while Silver broke out to a new 14-year high. Both metals remain supported by a mix of geopolitical risk, policy divergences, and strategic investor demand for hard assets.

Silver’s case is probably more compelling. The market faces a prolonged supply deficit and tightening physical availability, giving its rally deeper structural foundations. This dynamic, coupled with strong investor interest, has pushed prices higher and opened room for further gains on both near-term and medium-term horizons.

Near-term, Silver will remain bullish above former resistance at 39.49, now turned support. Next target is 61.8% projection of 28.28 to 39.49 from 36.93 at 43.85. Decisive break there could prompt upside acceleration to 100% projection at 48.14.

On the broader time frame, Silver has already cleared 100% projection of 21.92 to 34.84 from 28.28 at 41.20, setting up to 138.2% projection at 46.13. There is potential of further rally to 161.8% projection at 49.18 before topping, as the fifth wave of the five-wave rally from 17.54.

So in short, for Silver, holding 40 keeps the bullish structure intact, with acceleration toward 50 possible once 44 is cleared.

Gold, meanwhile, looks set to consolidate further in the short term, below 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63. But pullback should be contained above 3511.49 support to bring rebound. Firm break of 3678.63 will target 323.6% projection at 3765.34 next.

Fed, BoC set to ease as BoE, BoJ hold fire

Global markets face one of the busiest weeks of the year, with four major central bank meetings alongside a heavy slate of data releases. The Fed and BoC are widely expected to resume their rate-cutting cycles, while the BoE and BoJ are set to hold steady but with close attention on forward guidance.

The Fed meeting is the marquee event. Consensus expects policymakers to cut rates by 25bps, bringing the target range to 4.00–4.25%. That would mark the first move since November 2024 with possible signal of re-acceleration of the easing cycle following recent weak labor market data. However, the outcome may not be as straightforward, with the vote split and economic projections likely to carry as much weight as the headline cut.

Several uncertainties cloud the decision. Governors Christopher Waller and Michelle Bowman, both leaning dovish, could press for a 50bps move given the labor market softening. The status of Stephen Miran, nominated as temporary Governor, also looms large—if confirmed in time, his vote could tilt the balance toward a deeper cut. On the other side, Lisa Cook may favor holding steady, introducing the risk of multiple dissents in either direction. This raises the possibility of a fractured committee outcome.

Fresh economic projections will also matter. With job growth stalling and unemployment edging up, the new dot plot may shift from penciling in two cuts this year to three. A Reuters poll showed 60% of economists expect 50bps of easing by year-end, while 37% forecast 75bps. That diverges from market pricing, where traders see over an 80% chance of 25bps moves in both October and December. The outcome will shape expectations not only for 2025 but for how long rates stay restrictive into 2026. Retail sales data later in the week adds another variable for Fed watchers.

The BoC is also set to move. Markets and economists overwhelmingly expect a 25bps cut, lowering the policy rate to 2.50%. A Reuters survey showed 25 of 32 economists anticipate easing this week, aligning with market pricing. Among Canada’s top five banks, RBC stands out in expecting a hold, contingent on the latest inflation release due just before the decision.

Forward guidance will be critical. Over 70% of economists predict the BoC will deliver at least 50bps of cuts by year-end, taking the policy rate to 2.25% or lower, with a minority even expecting 75bps. How Governor Tiff Macklem frames the balance between still-firm wage growth and a weakening consumer sector will guide expectations. Given recent soft Canadian data and rising global risks, markets will be quick to price in more cuts if the BoC leaves the door wide open.

In the UK, the BoE is set to keep Bank Rate unchanged at 4.00% this week. But the outlook is contested. A Reuters poll found 42 of 67 economists expect one final cut in November, while 22 see no further moves this year. Upcoming jobs, CPI, and retail sales data will heavily influence the November call. With inflation expectations edging higher, the BoE is cautious about easing too far, too fast.

The BoJ is also expected to stand pat at 0.50%, preferring more time to assess how new U.S. tariffs and trade deals affect the economy. Policymakers are also monitoring whether food price inflation recedes in coming months, as well as the impact of stronger wage settlements. A Reuters poll showed 55% of economists expect the BoJ to hike to 0.75% by next quarter, leaving risks tilted toward further tightening. Japan’s national CPI release later this week will be a key test of whether inflation pressures are indeed moderating.

Beyond central banks, data releases from Germany’s ZEW survey, Australian employment, and New Zealand GDP will round out a packed week.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; China industrial production, retail sales, fixed asset investment; Swiss PPI; Eurozone trade balance; Canada manufacturing sales, wholesale sales; US Empire state manufacturing.

- Tuesday: Japan tertiary industry index; UK employment; Canada CPI; US retail sales, import prices, industrial production, business inventories, NAHB housing index.

- Wednesday: Japan trade balance; UK CPI; Eurozone CPI final; US housing starts and building permits, FOMC rate decision; BoC rate decision.

- Thursday: New Zealand GDP; Australia employment; Swiss trade balance; ; Eurozone current account; BoE rate decision; US jobless claims, Philly Fed manufacturing.

- Friday: Japan CPI, BoJ rate decision; Germany PPI; UK retail sales, public sector net borrowing; Canada retail sales.

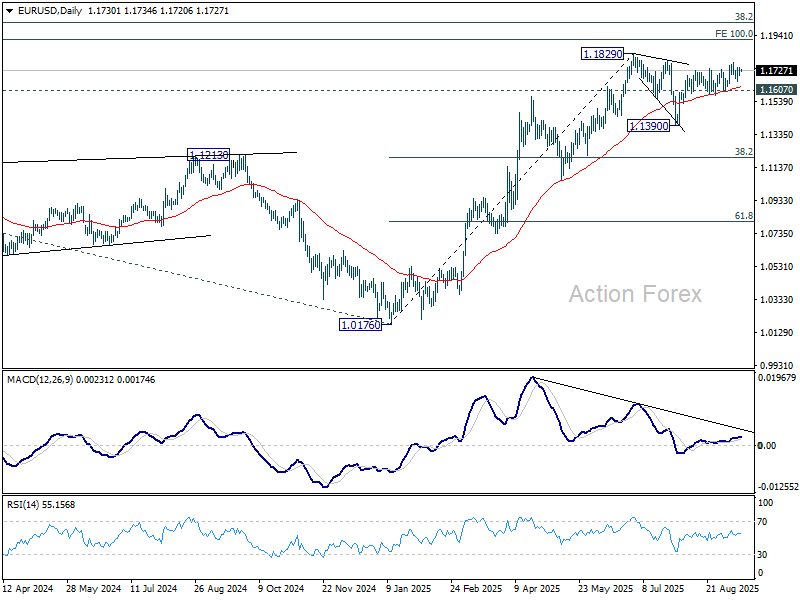

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1709; (P) 1.1728; (R1) 1.1756; More...

Range trading continues in EUR/USD and intraday bias remains neutral. With 1.1607 support intact, further rise is expected. On the upside, above 1.1779 will target a retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 55 W EMA (now at 1.1174) holds.

EUR/USD Technical Outlook – Fresh Upside Attempt in Progress

Key Highlights

- EUR/USD remained in a positive zone and traded above 1.1700.

- A key bullish trend line is forming with support at 1.1705 on the 4-hour chart.

- Bitcoin gained bullish momentum and climbed above $116,000.

- USD/JPY is consolidating below the 148.20 resistance zone.

EUR/USD Technical Analysis

The Euro started a fresh increase above 1.1700 against the US Dollar. EUR/USD cleared 1.1750, tested 1.1780, and recently corrected some gains.

Looking at the 4-hour chart, the pair remained supported and settled above the 1.1700 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It is again rising with a move above the 50% Fib retracement level of the downward move from the 1.1779 swing high to the 1.1658 low.

On the upside, the pair could face resistance near the 1.1750 level or the 76.4% Fib retracement. The first major hurdle for the bulls could be 1.1780. A close above 1.1780 could set the pace for another increase.

In the stated case, the pair could rise toward 1.1850, above which the bulls could aim for a move toward 1.1880. Any more upsides could send the pair toward 1.1920.

On the downside, immediate support is 1.1700. There is also a key bullish trend line forming with support at 1.1705. The next key area of interest might be near 1.1680 and the 100 simple moving average (red, 4-hour).

Looking at Bitcoin, the bulls remained in action and they were able to push the price above the $116,000 resistance zone.

Upcoming Key Economic Events:

- NY Empire State Manufacturing Index for Sep 2025 – Forecast 2, versus 11.9 previous.

- ECB's President Lagarde speech.

Silver steals spotlight, charging toward 50 while Gold pauses

Precious metals remain firmly bid, but leadership has shifted. Gold’s rally stalled just ahead of a key Fibonacci projection, while Silver broke out to a new 14-year high. Both metals remain supported by a mix of geopolitical risk, policy divergences, and strategic investor demand for hard assets.

Silver’s case is probably more compelling. The market faces a prolonged supply deficit and tightening physical availability, giving its rally deeper structural foundations. This dynamic, coupled with strong investor interest, has pushed prices higher and opened room for further gains on both near-term and medium-term horizons.

Near-term, Silver will remain bullish above former resistance at 39.49, now turned support. Next target is 61.8% projection of 28.28 to 39.49 from 36.93 at 43.85. Decisive break there could prompt upside acceleration to 100% projection at 48.14.

On the broader time frame, Silver has already cleared 100% projection of 21.92 to 34.84 from 28.28 at 41.20, setting up to 138.2% projection at 46.13. There is potential of further rally to 161.8% projection at 49.18 before topping, as the fifth wave of the five-wave rally from 17.54.

So in short, for Silver, holding 40 keeps the bullish structure intact, with acceleration toward 50 possible once 44 is cleared.

Gold, meanwhile, looks set to consolidate further in the short term, below 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63. But pullback should be contained above 3511.49 support to bring rebound. Firm break of 3678.63 will target 323.6% projection at 3765.34 next.

Central Bank Meetings and Fed Rate Cut in Focus for the Week Ahead

The market prepared last week for this week’s U.S. Federal Reserve meeting and expectations of a 0.25% cut in interest rates. U.S. PPI inflation came in below expectations and CPI matched forecasts, making it highly likely that the Fed will cut rates. U.S. jobless claims were worse than expected, following weak payroll data earlier in the month, reinforcing the view of a slowing U.S. economy. The European Central Bank kept its policy rate unchanged at 2.15%, while gold extended its rally to fresh record highs on safe-haven demand and lower-rate prospects.

In currency markets, USD/JPY tested lower after the softer U.S. inflation data and on rising expectations that the Bank of Japan will raise rates this year. The pair found support and closed the week near unchanged. Japanese GDP data beat forecasts, and optimism over the appointment of a new prime minister following Ishiba’s resignation further supported sentiment toward Japan.

Equities remained the main focus as U.S. and Japanese stock indexes surged to record highs, driven by expectations of a U.S. rate cut, with the market looking for the next trigger to spark a large move in FX markets.

Markets This Week

U.S. Stocks

U.S. equities hit record highs again last week, supported by expectations that the Federal Reserve will begin cutting interest rates after soft U.S. inflation data. AI-related names remained strong, helping technology stocks outperform the broader market. However, while indexes reached new highs, the short-term uptrend lacks momentum, suggesting range trading is the preferred strategy ahead of the upcoming Federal Reserve meeting. Key resistance is at 45,750, 46,000, and 47,000, with support at 45,700, 45,000, 44,000, and 43,000.

Japanese Stocks

The Nikkei 225 gained 3% last week on optimism over a new Japanese prime minister and positive sentiment from strong U.S. equities. Better-than-expected Japanese industrial production confirmed the economy is performing more strongly than anticipated. Last week’s price action was very positive, so following the uptrend by buying on weakness looks like the best short-term strategy now. Resistance is at 45,000円 and 46,000円, while support is at 44,000円, 43,000円, and 42,000円.

USD/JPY

Stronger-than-expected Japanese GDP data increased expectations that the Bank of Japan will raise interest rates this year, bringing USD/JPY down to test support at 146 early last week. That support held, prompting a rebound toward the middle of the recent 146–149 range by the week’s end. Range trading remains the favored approach in the short term, with a preference for selling, which also suits the medium-term outlook. Key levels remain unchanged, with resistance at 148, 149, and 150, and support at 146 and 145.

Gold

Despite concerns that gold is overbought, prices climbed to fresh record highs last week ahead of the expected U.S. interest rate cut this week. The current buying is largely speculative, following the strong uptrend with no clear resistance on the charts. However, the likelihood of a quick reversal is increasing, making selling on signs of fading momentum the best short-term strategy, while medium-term traders may prefer to stay patient and wait for a retracement to buy. Resistance levels are at $3,600, $3,700, and $3,800, with support at $3,600, $3,500, and $3,450.

Crude Oil

WTI found support at last month’s lows early in the week as fighting intensified between Russia and Ukraine. However, the market met resistance at the downward-sloping 10-day moving average and closed the week near unchanged, staying under pressure close to support as concerns about oversupply and a slowing U.S. economy encouraged selling. With technical indicators pointing lower, selling into strength remains the preferred strategy. Resistance levels are at $65, $70, and $75, while support lies at $60 and $55.

Bitcoin

Bitcoin surged back above the key $112,000 level last week on expectations that the U.S. Federal Reserve will cut interest rates next week. Reports of large buyers returning to the market and increased demand for Bitcoin ETFs, alongside anticipation of positive regulatory actions for crypto ETFs, added to the bullish momentum. Now back above $112,000, the best approach appears to be buying on strength, with technical indicators pointing higher. Resistance levels are at $120,000, $125,000, and $150,000, while support lies at $112,000, $105,000, and $100,000.

This Week’s Focus

- Monday: China Industrial Production, E.U. Trade Balance, U.S. NY Empire State Manufacturing Index

- Tuesday: U.K. Unemployment Rate, E.U. Industrial Production, U.S. Retail Sales and Industrial Production

- Wednesday: Japan Trade Balance, U.K. CPI, E.U. CPI, U.S. Housing Starts and Fed Interest Rate Decision

- Thursday: Australia Unemployment Rate, U.K. BoE Interest Rate Decision, U.S.Initial Jobless Claims

- Friday: Japan National CPI and BoJ Interest Rate Decision, U.K. Retail Sales

This week is set to be busy, with the U.S. expected to cut official interest rates and central bank meetings in the U.K. and Japan where both are expected to keep rates unchanged. How each central bank explains its decision will be closely watched by traders and is likely to create volatility. U.S. retail sales and Japanese inflation are the key economic releases, and it will be interesting to see whether the recent narrow ranges in FX are broken or if equities and gold reverse. Overall, it should be a week full of trading opportunities.

China industrial output, retail sales miss forecasts, fixed asset investment slumps

China’s economy slowed in August, with key indicators falling short of expectations. Industrial output grew 5.2% yoy, down from 5.7% yoy in July and short of forecasts for 5.8% yoy, marking its weakest pace since August 2024. Retail sales also slowed, rising just 3.4% yoy versus 3.7% yoy previously and expectations of 3.8% yoy, signaling soft household demand despite ongoing government measures to support spending.

Investment activity showed the sharpest loss of momentum. Year-to-date fixed asset investment rose only 0.5%, far weaker than consensus 1.4% and July’s 1.6%. The drag came primarily from the property sector, where real estate investment plunged -12.9% in the first eight months. Excluding real estate, investment rose 4.2%.

The National Bureau of Statistics highlighted “many unstable and uncertain factors” in the global environment and warned that the economy still faces “multiple risks and challenges.” It urged stronger policy implementation to stabilize employment, businesses, and expectations, but the latest figures suggest momentum remains fragile, with property weakness continuing to weigh heavily on growth prospects.

NZ services PMI slumps to 47.5, 18th month contraction

New Zealand’s services sector deteriorated further in August, with BusinessNZ Performance of Services Index slipping from 48.9 to 47.5, well below the long-run average of 52.9. The reading also marks the 18th consecutive month of contraction. Both

Activity/Sales (46.2) and New Orders/Business (47.8) weakened, suggesting demand remains fragile. Employment improved slightly to 48.3 but remains in contraction territory, reflecting businesses’ reluctance to expand payrolls in the face of subdued activity.

The survey showed 59.6% of respondents made negative comments in August, an increase from July but still less pessimistic than June’s tally. Firms cited multiple pressures, including high interest rates, sticky inflation, and the cost-of-living squeeze eroding household spending. Rising operating costs, seasonal slowdowns, supply chain disruptions, and uncertainty over government policy also weighed on sentiment.

Platinum (PL) Price Soars in Strong Uptrend

Platinum (PL) shows a bullish sequence from March 2020 low, confirming the right side is higher. In this article, we will explore the latest long-term Elliott Wave technical outlook.

Platinum (PL) Monthly Elliott Wave Chart

The monthly Platinum chart illustrates that the wave ((I)) rally peaked at 2308.8, followed by a wave ((II)) pullback that bottomed at 562. The pullback formed a zigzag Elliott Wave structure. From the wave ((I)) high, wave (A) declined to 752.1, wave (B) rallied to 1918.5, and wave (C) dropped to 562, completing wave ((II)) in a higher degree. The metal has since resumed its ascent in wave ((III)). From the wave ((II)) low, wave (I) reached 1348.2, with a wave (II) pullback concluding at 796.8. In the near term, as long as the 562 pivot low holds, the metal is expected to continue rising.

Platinum (PL) Daily Elliott Wave Chart

The daily Platinum chart shows that the wave ((2)) pullback ended at 843.1. From that low, the metal is nesting higher with wave (1) ended at 1016 and pullback in wave (2) ended at 870. Wave (3) higher is in progress as an impulse in lesser degree. Wave 1 of (3) peaked at 1105, followed by a wave 2 pullback concluding at 875.9. The metal has since resumed its upward trend in wave 3. In the near term, as long as the price stays above 875.9, expect Platinum to continue rising.

Ethereum Wave Analysis

Ethereum: ⬆️ Buy

- Ethereum reversed from support area

- Likely to rise to resistance level 4750.00

Ethereum cryptocurrency recently reversed up from the support area located at the intersection of the support level 4250.00 (which has been reversing the price from the end of August), 38.2% Fibonacci correction of the upward impulse from August and the lower daily Bollinger Band.

The upward reversal from this from the support area (strengthened by the two intersecting up channels) started the active wave B.

Ethereum cryptocurrency can be expected to rise to the next resistance level 4750.00 (target for the completion of the active wave B.).