Sample Category Title

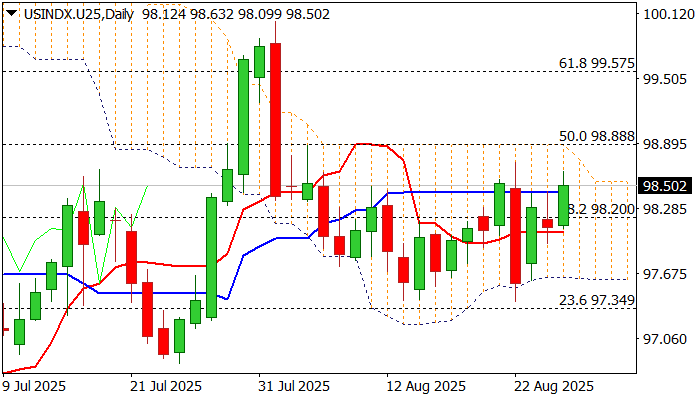

Dollar Index – Bulls Regained Traction and Eye Key Barriers

The dollar index firmed on Wednesday and hit week’s high, showing resilience to the latest political turmoil in the US central bank after President Trump decided to fire Governor Cook.

Fresh gains retested falling 100DMA ($98.60), with firm break here and nearby lower top at $98.71 (Aug 22) needed to confirm positive signal and open way for attack at key barrier at $98.88 (daily cloud top / Fibo 50% retracement of $101.80/$95.97 fall).

Technical picture on daily chart has improved as the price rose above converged 10/20DMA’s, while momentum is strengthening (north-heading RSI rose above neutrality territory and 14-d momentum is rising deeper in the positive territory) that supports bullish outlook.

However, failure to clear 100DMA and cloud top would keep the price within current range ($98.71/ $97.58) and without clear near-term direction.

Investors wait for release of US PCE Index (Fed’s important inflation gauge) due on Friday and US July labor report for August (due next week) to get more details about Fed’s action on monetary policy in September’s policy meeting.

Res: 98.60; 98.88; 99.00; 99.57

Sup: 98.20; 98.05; 97.80; 97.62

CADCHF Wave Analysis

CADCHF: ⬆️ Buy

- CADCHF reversed from strong support level 0.5800

- Likely to rise to resistance level 0.5850

CADCHF currency pair recently reversed up once again from the strong support level 0.5800 (which has been reversing the price from the end of June) standing near the lower daily Bollinger Band.

This is the 3rd consecutive upward reversal from this support level over the last few trading sessions..

Given the strength of the support level 0.5800 and the still oversold daily Stochastic, CADCHF currency pair can be expected to rise to the next resistance level 0.5850 (top of wave ii).

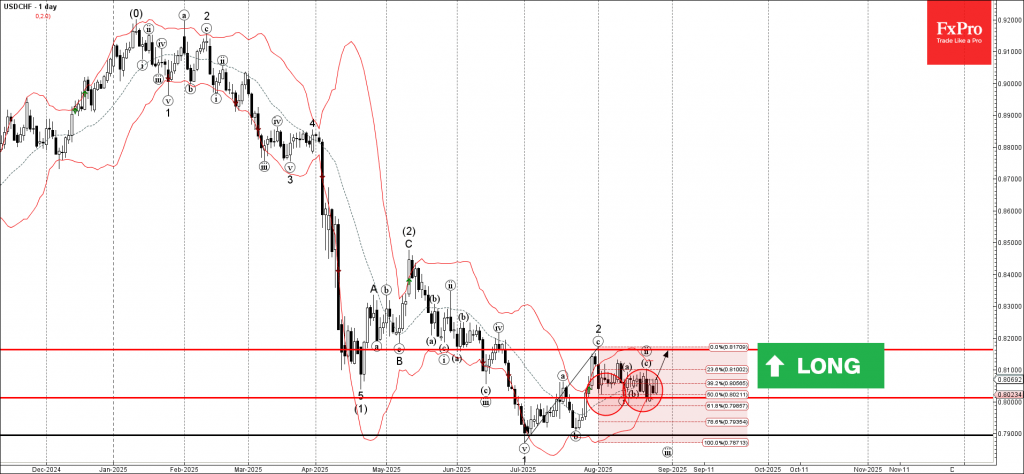

USDCHF Wave Analysis

USDCHF: ⬆️ Buy

- USDCHF reversed from support area

- Likely to rise to resistance level 0.8165

USDCHF currency pair reversed from the support area located between the support level 0.8000, lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from July.

The upward reversal from this support area created the daily Japanese candlesticks reversal pattern Piercing Line.

Given the strength of the support level 0.8000, USDCHF currency pair can be expected to rise to the next resistance level 0.8165 (top of wave 2 from the end of July).

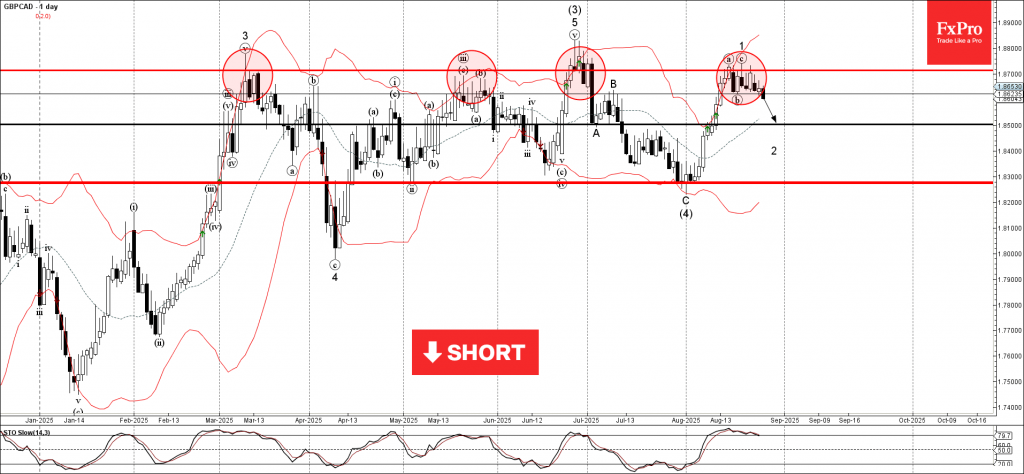

GBPCAD Wave Analysis

GBPCAD: ⬇️ Sell

- GBPCAD reversed from long-term resistance level 1.8700

- Likely to fall to support level 1.8500.

GBPCAD currency pair recently reversed down from the resistance zone between the upper daily Bollinger Band and the strong multi-month resistance level 1.8700 (which has been reversing the price from March).

The downward reversal from this resistance zone started the active short-term ABC correction 2.

Given the strength of the nearby resistance level 1.8700 and the bullish Canadian dollar sentiment seen today, GBPCAD currency pair can be expected to fall to the next support level 1.8500.

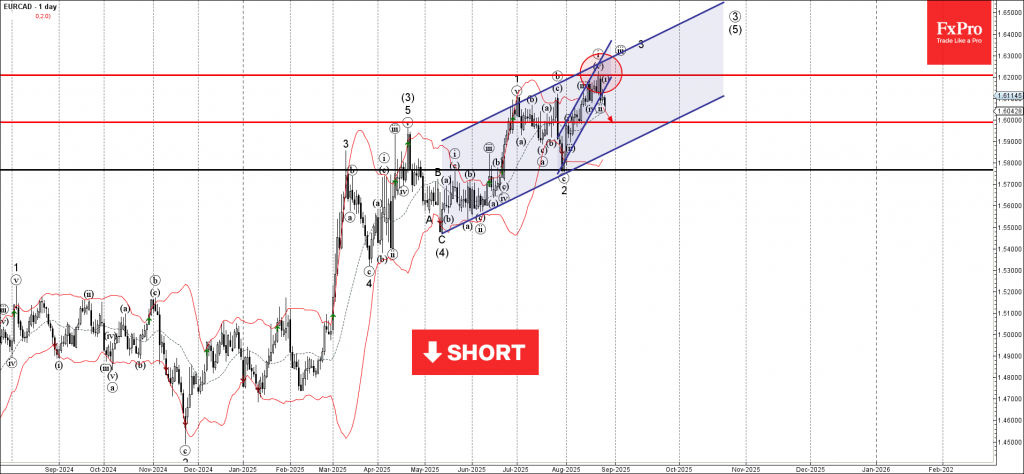

EURCAD Wave Analysis

EURCAD: ⬇️ Sell

- EURCAD reversed from resistance zone

- Likely to fall to support level 1.6000

EURCAD currency pair recently reversed down from the resistance zone lying at the intersection of the upper daily Bollinger Band and the two daily up channels from July and May respectively.

The downward reversal from this resistance zone created the daily Bearish Engulfing – which stopped the previous wave 3.

Given the strength of the aforementioned resistance zone, EURCAD currency pair recently can be expected to fall to the next round support level 1.6000.

Sunset Market Commentary

Markets

French yields remained at the center of attention. Since prime minister Bayrou called a budget-related confidence vote for September 8, OATs have underperformed not only vs. Bund & swap but even vs. Italian BTPs. That continued today, be it at a less alarming pace than on Monday. Some French tenors including the 5-year one already trade higher than their Italian counterparts and the gap between the important 10-year references is narrowing to just 5.5 bps, the narrowest since the early days of the monetary union. The OAT-swapspread surpasses 85 bps, which is the highest since March of this year. French equities were offered some relief after a two-day beating. The CAC40 adds 0.6%, beating its European peers (eg. EuroStoxx50 flat). The political instability theme meanwhile appears contagious and is spreading to the Netherlands as well. A motion of no confidence was filed today. But there is no clear procedure in place on how a minority caretaker government has to handle defeat. The four-party coalition government broke down in June after Wilder’s Freedom Party left and crumbled to just two parties with the exit of the New Social Contract party last week. The current coalition only has 32 seats of the 150. Dutch bonds react stoic though. Spreads vs swap hold steady. The US yield curve steepens further with losses of 3 bps at the front complemented by another 3 bps rise at the ultralong end. The 30-year tenor (4.95%) is marching towards the 5% barrier again. It suggests lingering concerns on the topic of Fed (political) independence. The dollar nevertheless has the upper hand against a weak euro. EUR/USD pushes further south, breaking below the 1.16 big figure. Nothing changed from a technical point of view though. The trade-weighted DXY dollar index inches higher to 98.61. UK gilt yields shot up at their first trading day yesterday amid the same fiscal worries that haunt French bonds and were given some reprieve at first today. But an intraday decline at the long end of more than 5 bps got virtually fully wiped out again as the session evolved. Sterling for the time being manages to capitalize on the poor euro momentum, dragging EUR/GBP marginally lower to 0.8625. Some final market moving events today include a $70bn 5-year bond sale as well as tech-heavyweight Nvidia’s earnings, released after-market.

News & Views

In an interview with the Newspaper L’Agefi, the vice governor of the Swiss National Bank (SNB), Antoine Martin, indicated that the bar for the SNB to cut interest rates into negative territory is rather high. ‘It should be noted that the requirement level for introducing negative rates is higher than it is for cutting interest rates in positive territory’, the SNB vice governor was quoted. Past experience showed that ‘negative rates have worked, but that they create more challenges for banks, investors and also households, which take more risks. This phenomenon can have long-term negative effects’. The SNB at its June policy meeting reduced its policy rate to 0% from 0.25%. Inflation in July rose from 0.1% Y/Y to 0.2I% Y/Y. In its forecasts the Bank even sees a jump in inflation in the coming quarters. The next regular SNB policy meeting is scheduled for September 25. The SNB vice governor saw recent weakness of the Swiss franc against the dollar mainly as USD weakness rather than franc strength will no dramatic effect on inflation. The franc over the previous day’s gained modest traction also against the euro (political risks in France and debate on Fed independence in the US). EUR/CHF moves to the 0.9355 area. Markets will also keep a close eye at the composition of the SNB balance (diversification USD-euro).

The Confederation of British industry (CBI) today published its June distributive traders report. Retail sales volumes fell at a strong pace in the year to August, extending the downturn to an eleventh consecutive month. CBI analyses that weak demand and gloomy sentiment continue to weigh on retailers’ investment and hiring plans. Price pressures remain elevated. The balance of retail sales volumes in the survey declined to -34 from -32. Sales are expected to decline at slower pace in September (-16). Retail sales for the time of year were judged to be “poor” to a somewhat greater extent than in July (-19 from -10). Next month’s sales are set to remain below seasonal norms to a similar degree (-20%). Sentiment among retailers remained poor, with the business situation expected to deteriorate over the coming quarter. Employment continues to decline and is even expected to decline at a slightly faster pace next month. Retail selling price rose in the year to August at the fastest rate since November 2023 (+65 from +35 in May).

Fed’s Williams sees scope for lower rates, praises Cook

New York Fed President John Williams said in a CNBC interview that interest rates are likely to move lower over time, though he offered no timetable for when easing might begin. He described the U.S. economy as generally strong, albeit slowing modestly, and characterized the labor market as “solid,” echoing language used by other Fed officials.

Williams emphasized that any decision will remain data-driven. “If things move in the way that I hope they do in terms of our maximum employment and price stability goals, then I do think it will be appropriate to move interest rates down over time,” he said. Markets continue to expect the next cut to come at the September meeting.

While avoiding direct comment on US President Donald Trump’s attempt to dismiss Fed Governor Lisa Cook, Williams noted her integrity and commitment to the central bank’s mission. He stressed that the Fed’s independence is vital for ensuring long-term economic and financial stability.

He used the moment to reaffirm the principle of central bank independence. “Independent central banks can deliver low inflation, economic and financial stability,” Williams said.

USD/CHF: Dollar-Franc Buoyant Above 0.80000, Although Further Downside Possible

Painting new lows last Friday, gains in today’s session keep the dollar-franc exchange above the key level of 0.8000 - at least for now.

Currently trading around ~$0.80698, recent developments on the Federal Reserve’s autonomy on monetary policy and potential action by the SNB continue to dominate USD/CHF headlines.

USD/CHF: Key takeaways from today’s session

- Boasting reasonable gains in Monday’s session, despite a public holiday in the United Kingdom, USD/CHF trades ~0.46% higher today, as markets adjust expectations for Federal Reserve monetary policy

- Otherwise, questions continue surrounding Federal Reserve independence from the US central government, with President Trump attempting to fire board governor Lisa Cook

- Having reminded markets that intervention remains a real possibility, the SNB remains poised to take action should the franc stage a runaway strengthening versus the dollar

USD/CHF: Dovish fed commentary at Jackson Hole spells trouble for US dollar

Put simply, markets are increasingly certain of a September rate cut, in no small part because of dovish Federal Reserve commentary during last week’s Jackson Hole Symposium.

"With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance"

Jerome Powell speaking at the JHS, August 22nd, federalreserve.gov

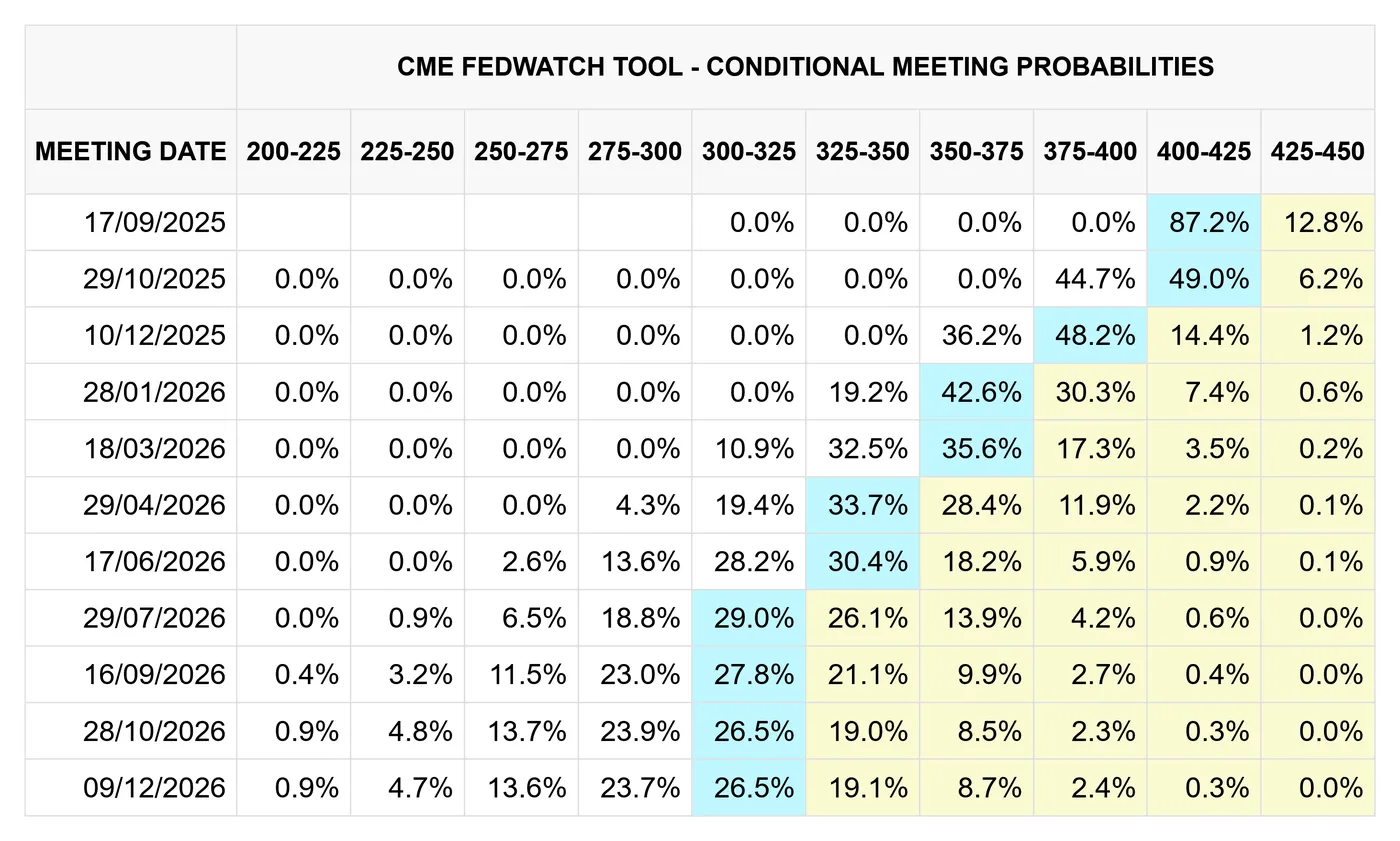

While markets have consistently predicted Fed rate cuts in the remainder of 2025, confirmation from Jerome Powell himself now have markets overwhelmingly predicting a rate cut of 25 BPS in the upcoming decisions September 17th.

CME FedWatch, 26/08/2025

As for USD/CHF pricing, markets would do well to acknowledge how much the dollar has fallen versus the franc this year despite the Federal Reserve's best efforts to tighten monetary policy, especially when compared to the SNB.

As such, any suggestion that the Federal Reserve will lower rates will negatively affect the dollar and introduce selling pressure in USD/CHF markets, a phenomenon seen just last Friday.

USD/CHF: Dollar finds support as Trump firing bid meets a dead-end

While building anonymity between the Republican party and the Federal Reserve is not a hot topic, the latest developments are perhaps the most significant for dollar-franc markets.

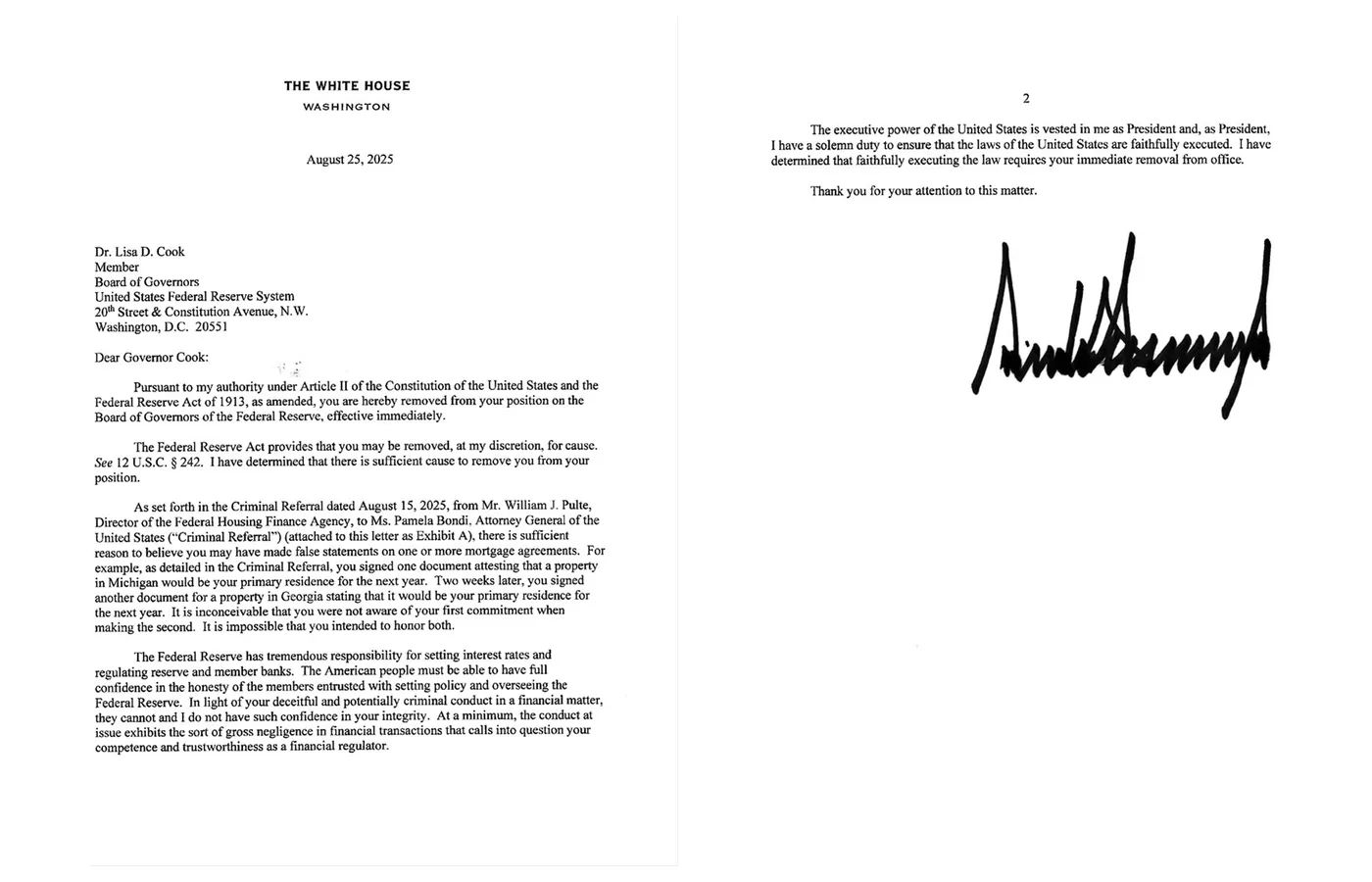

@realDonaldTrump, TruthSocial, 25/08/2025

Sharing the above letter yesterday on his social media platform of choice, TruthSocial, President Trump has made his intentions to fire Governor Cook clear, citing alleged mortgage fraud.

While matters of fraud amongst government officials would not typically be of such interest to financial markets, the move reignites discussion whether any US government should have the power to fire Federal Reserve officials, considering political independence is a core tenet of the institution.

Supposing Trump successfully removes Cook from office and overcomes various legal hurdles, an interesting precedent will be set, especially considering that Trump has been clear in his dislike for Powell and his policy of higher interest rates.

Regarding USD/CHF price action, any developments suggesting that Trump can wrangle more control of the Federal Reserve and its employees and, therefore, appoint governors who favour an aggressive lowering of interest rates will likely introduce some dollar-franc selling pressure.

As such, the next few days remain crucial, especially with USD/CHF hovering around the key level of 0.80000.

USD/CHF: SNB ready to intervene to halt CHF strengthening

Having already strengthened significantly compared to the dollar in the first half of the year, the trusted tool of currency intervention by the SNB remains a real possibility should dollar-franc continue to its decent.

Already trading around multi-year lows and citing the competitiveness of imports, USD/CHF downside may be capped in the near-term, considering the SNB’s clear commitment to intervention where appropriate.

USD/CHF, OANDA, TradingView, 27/08/2025

USDJPY Rallies into its Range Amid US Dollar Rebound – Will the Range Break?

Like other FX pairs, USDJPY has been held in a tight range for the past two full weeks.

There is a lack of clarity regarding the outlook for US cuts due to contradicting data, supplemented by Markets having digested a more balanced/dovish tone from Powell rather than a fully dovish one (from a more balanced/hawkish tone regarding the impact of tariffs).

The question remains: Will there be only 2 cuts this year? This would not change much to the FED's quarterly outlook from previous meetings.

Markets are also awaiting more information regarding who will be the next FED board member. Reactions to the US Dollar have been minimal regarding the firing of Lisa Cook, a board member (hence a continuous voter).

The Bank of Japan has been waiting for the Federal Reserve to cut rates to reduce the huge rate differentials that have hurt the Yen throughout the past 3 years.

Luckily for the BoJ, a basis trade unwind in July 2024, combined with US Dollar weakness, has gradually naturally reduced the Yen's relative weakness. However, it is still at relative lows against its European peers.

Let's examine USDJPY multi-timeframe technicals to see if the daily USD rally is enough for the pair to break out of its range and establish its boundaries.

USDJPY multi-timeframe technical analysis

USDJPY Daily Chart

USDJPY Daily Chart, August 27, 2025 – Source: TradingView

The most volatile FX pair has been held into a 1,000 to 1,900 pip range for the past 18 days, a prolonged consolidation compared to the usual.

Despite all of the headlines throughout the year, nothing really changed compared to the fundamentals of the year-beginning – Markets are still awaiting for a concrete change to the main rates for both the FED and the Bank of Japan, leading to some mostly rangebound action since May.

The range has tightened quite a lot however this month, located between 146.80 (lows) to 148.70 (range extremes), with the price action located between the 50 and 200-Day Moving averages acting as key boundaries.

As a matter of fact, they will be acting as key indicators for a more concrete breakout – expect rangebound action as long as prices remain within these boundaries.

Let's discover where they stand just below.

USDJPY 4H Chart

USDJPY 4H Chart, August 27, 2025 – Source: TradingView

The 4H timeframe allows to spot the current price action heading higher as the current US Dollar buying is bringing the pair above the 200 4H-period MA in a higher-low formation, supported by a short-timeframe upward trendline.

A higher timeframe Head and Shoulders could also be into play but its long-shape may not create enough clarity to make the pattern valid – It is still noteworthy but hold about a 35% chance of materializing further.

Key trading Levels for USDJPY:

Resistance Levels

- 148.78 last Friday highs

- May range extremes from 148.70 to 149.50 (daily MA 200 in confluence)

- 149.00 200-Day MA Key range resistance

Support Levels

- Pivot at the 148.00 zone (acting as immediate support)

- 147.00 50-Day MA Key range support

- 146.50 mid-range and immediate support (Daily MA 50 in confluence)

- 145.00 psychological support

USDJPY 1H Chart

USDJPY 1H Chart, August 27, 2025 – Source: TradingView

Looking even closer, bulls will have to push harder to break the last Friday highs as price action is stalling at the high of 148 pivot Zone, a key short-term pivot.

Particularly as markets lack further data and fundamentals to break out from rangebound price action, the short-term outlook is more rangebound than breakout-prone.

Look at the top in the 1H RSI, if buying goes further, it will add to more chances of testing the range extremes around the last Friday highs.

Safe Trades!