Sample Category Title

Australian Inflation Lower Than Forecast, Fed Up Next

The Australian dollar is showing limited movement. In the European session, AUD/USD is trading at 0.6500, down 0.15% on the day.

Australian CPI eases to 2.1%

Australia's inflation rate for the second quarter came in lower than expected. Headline CPI dropped to 2.1% y/y, down from 2.4% in the prior two quarters and falling to its lowest level since Q1 2021. This was just below the market estimate of 2.2%. Quarterly, CPI rose 0.7% in Q2, down from 0.9% in Q1 and below the market estimate of 0.8%.

Services inflation continued to decline and fell to 3.3% from 3.7%. The drop in CPI was driven by a sharp drop in automotive fuel costs. The RBA's key gauge for core CPI, the trimmed mean, slowed to 2.7% from 2.9%, matching the market forecast. This was the lowest level since Q4 2021.

Is an August rate cut a done deal?

The positive inflation report is a reassuring sign that inflation is under control and should cement a rate cut at the Aug. 12 meeting. The Reserve Bank of Australia stunned the markets earlier this month when it held rates, as a quarter-point cut had been all but certain. Bank policymakers said at that meeting that they wanted to wait for more inflation data to make sure that inflation was contained and today's inflation report should reassure even the hawkish members that a rate cut is the right move at the August meeting.

Fed expected to hold rates

The Federal Reserve meets today and is widely expected to maintain the benchmark rate for a fifth straight meeting. Investors will be looking for clues regarding the September meeting, as the markets have priced in a rate cut at 63%, according to CME's FedWatch.

AUD/USD is testing support at 0.6500. Next, there is support at 0.6488 and 0.6474

0.6514 and 0.6526 are the next resistance lines

AUD/USD Technical

- AUD/USD is testing support at 0.6500. Next, there is support at 0.6488 and 0.6474

- 0.6514 and 0.6526 are the next resistance lines

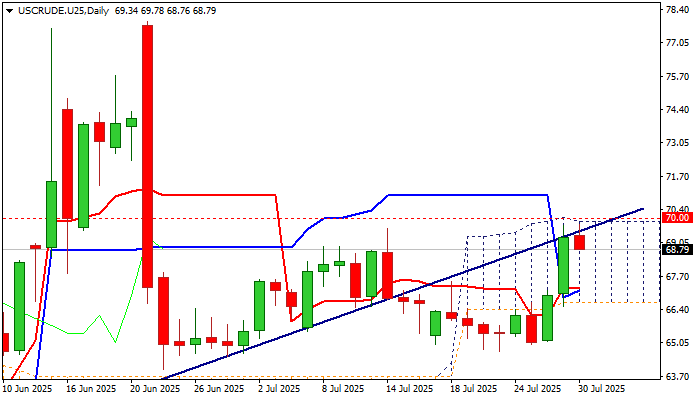

WTI Oil: Bulls Pause Under Cloud Top After Strong Advance in Past Two Days

WTI oil price eases from new five-week high on Wednesday after advancing over 6% in past two days.

Partial profit taking after strong rally was caused by technical signals, as well as on uncertainty over President Trump’s latest threats of imposing a secondary tariffs of 100% to all those importing oil from Russia.

The latest rally was repeatedly capped under the top of thick daily cloud as the price penetrated cloud on Monday and rose near its top on Tuesday, generating strong bullish signal.

Daily studies improved (Tenkan/Kijun-sen bull-cross /14-d momentum broke into positive territory) but overbought stochastic and sideways-moving RSI suggest that bulls are like to take a breather and look for fresh signal.

Dips should find solid supports at $67.96/85 (broken 200DMA / Fibo 38.2% of $64.72/$69.78 upleg) to mark a healthy correction ahead of fresh attack at cloud top and nearby psychological $70 barrier, violation of which to signal bullish continuation.

Otherwise, deeper pullback would keep bulls on hold, but with limited downside risk as long as the price stays above daily Tenkan-sen / 50% retracement of ($67.25).

Return below cloud base ($66.65) will be bearish.

Unexpected rise in US crude stocks (API report showed 1.53M build vs 2.5M draw forecast) contributed to weaker tone today, with release of EIA crude inventories report (-2.3M fc vs -3.16M previous) being in focus today.

Res: 69.62; 70.00; 70.92; 71.33.

Sup: 68.59; 67.96; 67.25; 66.65.

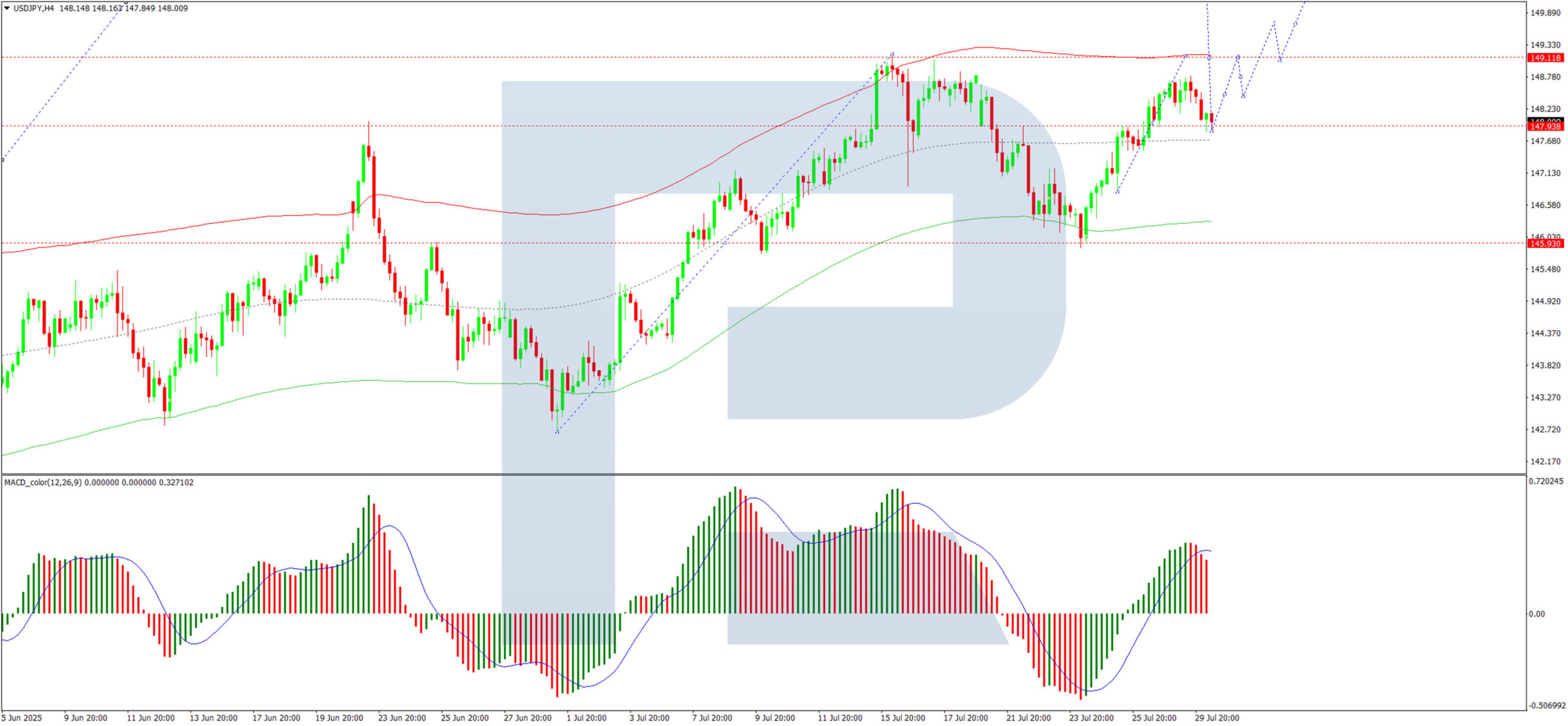

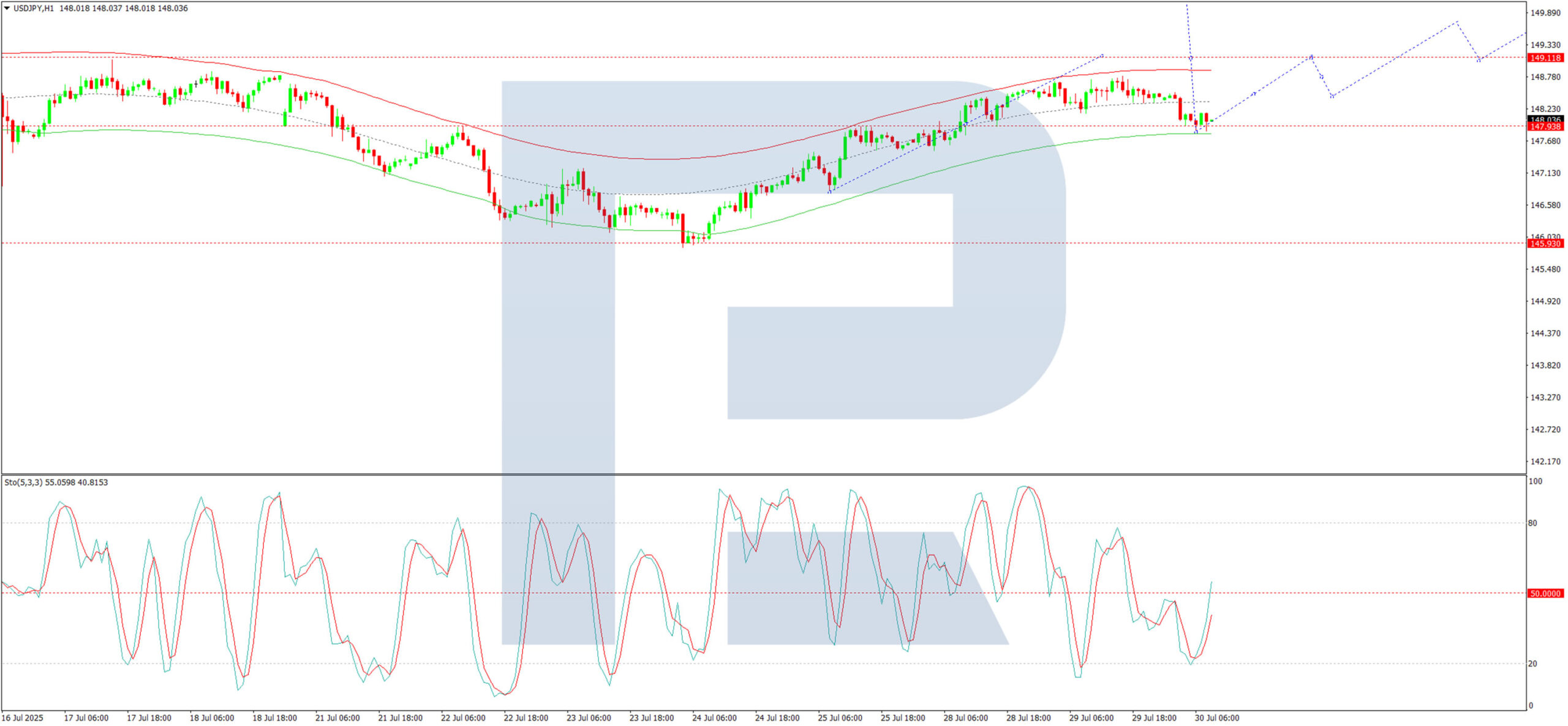

USD/JPY in Correction as Markets Await Signals from Fed and BoJ

The USD/JPY pair fell to 147.92 on Wednesday, with the Japanese yen recovering some of its early-week losses as the US dollar softened ahead of the Federal Reserve’s policy meeting.

While the Fed is widely expected to keep rates on hold, market focus remains squarely on whether policymakers will signal a potential rate cut in September.

Simultaneously, investors are assessing the outcome of this week’s US–China trade talks in Stockholm, which concluded on Tuesday without an extension of the current trade truce.

Domestically, attention turns to the upcoming Bank of Japan (BoJ) policy decision. The central bank is forecast to maintain its current interest rate as it evaluates the economic impact of US tariffs. The BoJ’s quarterly outlook report may also see an upward revision to its inflation forecasts.

Political uncertainty adds another layer of complexity, with growing pressure on Prime Minister Shigeru Ishiba to resign. However, the Prime Minister has firmly denied any intention to step down.

Notably, despite broader US dollar strength across markets, the USD/JPY pair has not fully reflected this trend due to counterbalancing factors.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY continues to consolidate around 147.90, having extended its range upwards to 148.77. Following a retest of 147.90 from above, the next likely move is a push higher towards 149.11, with a potential continuation towards 150.30 if bullish momentum holds. This scenario is supported by the MACD indicator, where the signal line remains above zero and points firmly upwards.

H1 Chart:

Switching to the H1 chart, the pair is forming a consolidation range around 147.90. A breakout to the upside could see a move towards 149.11, followed by a retracement to 148.44. Conversely, a downside break may trigger a decline towards 145.90. The Stochastic oscillator aligns with this outlook, as its signal line sits above 20 and is trending upwards.

Conclusion

The USD/JPY pair remains in a corrective phase, with near-term direction hinging on policy signals from the Fed and BoJ. While technical indicators currently support a bullish bias, traders should remain alert to the possibility of breakout moves as confirmation.

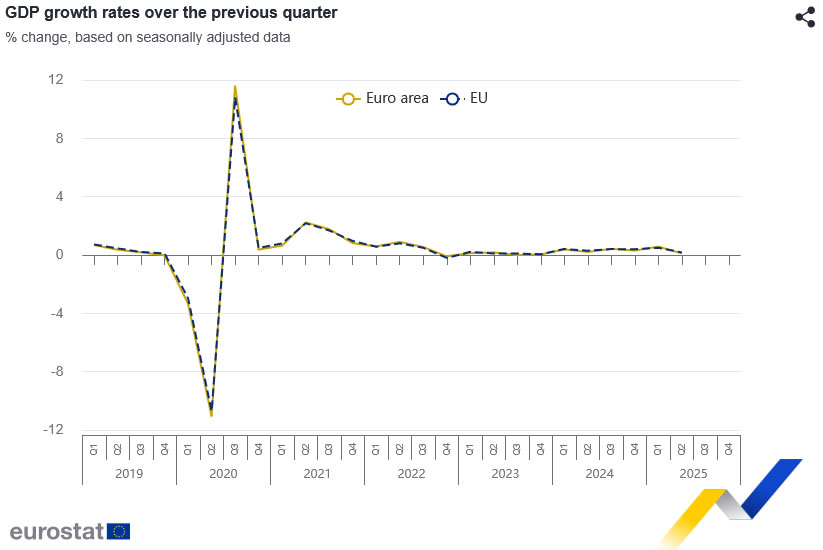

Eurozone GDP beats with 0.1% qoq growth, but Germany and Italy contract

Eurozone GDP grew 0.1% qoq in Q2, slightly above market expectations of flat growth, while the broader EU expanded 0.2% qoq. On a year-over-year basis, GDP rose 1.4% yoy in the Eurozone and 1.5% yoy in the EU—marking a mild deceleration from Q1's annual pace of 1.5% yoy and 1.6% yoy respectively. .

Spain led the quarter with a strong 0.7% qoq gain, followed by Portugal (0.6%) and Estonia (0.5%). However, Germany and Italy both posted marginal contractions of -0.1%, and Ireland saw the largest drop at -1.0%. Despite the mixed quarterly results, all member states reported positive year-on-year growth.

EUR/USD Hits Lowest Level Since Early July

As the EUR/USD chart indicates today, the euro has fallen below the 1.1550 mark against the US dollar, reaching the lows of June 2025. As a result, July may become the first month in 2025 to record a decline in the currency pair.

Why Is EUR/USD Declining?

There are two key factors driving the euro’s weakness relative to the US dollar:

→ Anticipation of the Federal Reserve Meeting. At 21:00 GMT+3 today, the Fed’s interest rate decision will be released. According to Forex Factory, analysts expect the Federal Funds Rate to remain unchanged at 4.25%-4.50%.

→ Market Reaction to the US-EU Trade Agreement. The trade deal signed last weekend between the United States and Europe is being critically assessed by market participants.

As noted in our Monday analysis, signs of a bearish takeover emerged on the chart following the agreement’s signing. Since then, EUR/USD has declined by approximately 1.3%. The question now is whether the downtrend will continue.

Technical Analysis of the EUR/USD Chart

The upward channel that had remained valid since mid-May was decisively broken by bears this week. The nature of the breakout (highlighted by the red arrow) was particularly aggressive, with the price dropping from the 1.1710 level to the D point low without any meaningful interim recoveries.

Key observations include:

→ The drop has resulted in a classic bearish A-B-C-D market structure, characterised by lower highs and lower lows.

→ On the 4-hour timeframe, the RSI indicator has fallen into oversold territory, reaching its lowest point of 2025 so far.

→ Notably (as highlighted by the blue arrow), there was a strong rebound from the 1.1455 support level earlier. Bulls demonstrated significant strength at that time, breaking through the R resistance line.

Given these factors, we could assume that after this week’s sharp decline, EUR/USD may attempt a short-term recovery from the support zone (highlighted in purple). Should this scenario unfold, potential resistance may emerge near the 1.1630 level, as this area aligns with:

→ The 50% Fibonacci retracement of the C→D decline;

→ The breakout point of the lower boundary of the previous ascending channel, indicating a shift in market balance in favour of the bears.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

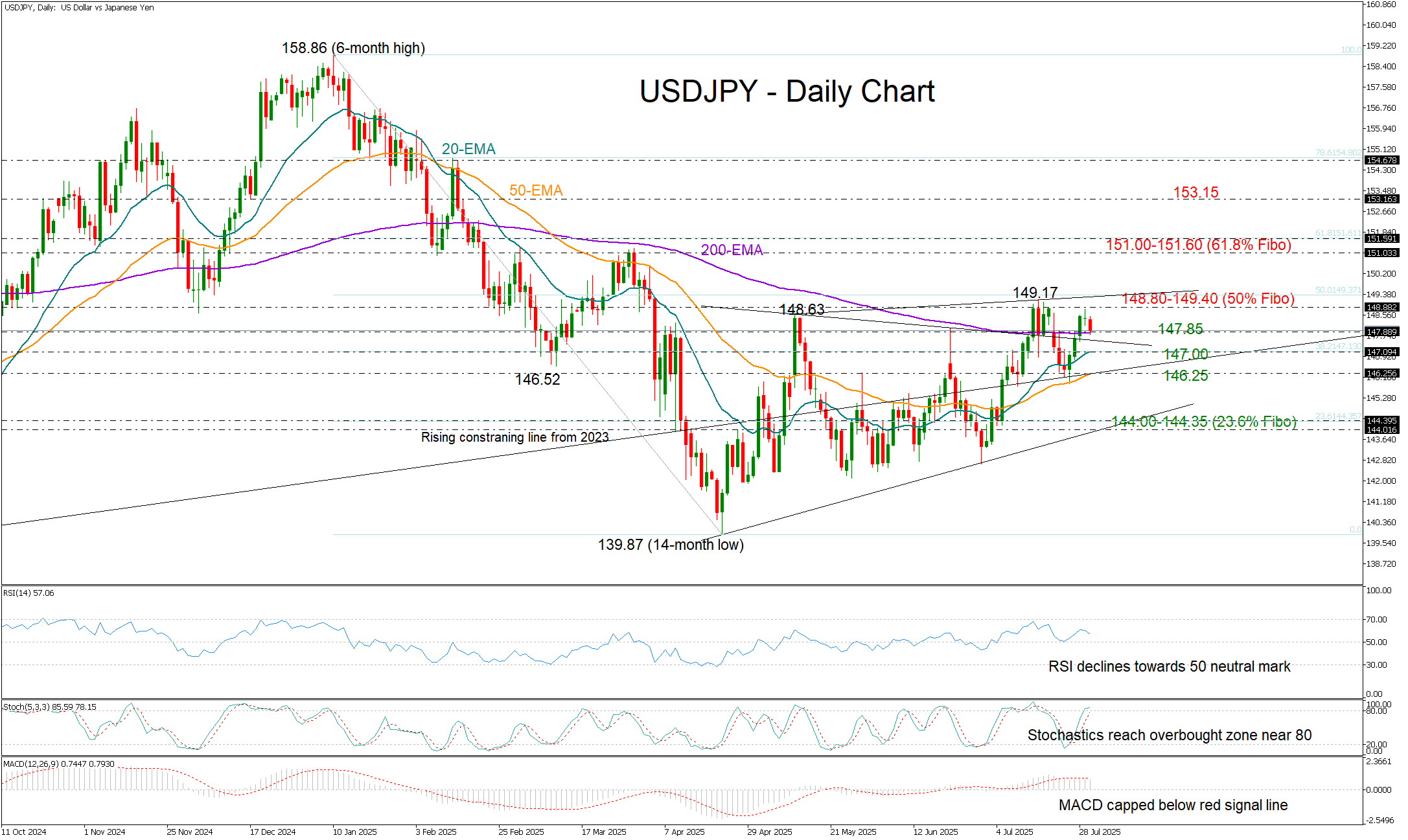

USD/JPY Runs Out of Fuel Near July’s High

- USD/JPY falls after another rejection near 148.80–149.40.

- Technical risk tilts to the downside; focus on 200-day EMA.

USDJ/PY surrendered to the bears early on Wednesday after its three-day bullish streak ran out of steam just below the 148.80–149.40 ceiling, which capped July’s gains.

While market stability is typical ahead of FOMC policy meetings, upcoming US GDP growth figures – and particularly the price component – could inject early volatility before the central bank's rate decision. Investors are anticipating a swift 2.4% rebound following the -0.5% contraction in Q1, the first such decline in over two years.

Technically, Tuesday’s doji candlestick has already raised concerns that the pair could remain trapped within the three-month-old sideways pattern. The momentum indicators are offering little optimism: the stochastic oscillator is about to peak in overbought territory, and the RSI is trending downward toward the neutral 50 mark.

As such, traders may wait for a confirmed negative move below the 200-day exponential moving average (EMA) at 147.80 or even a slide beneath the 20-day EMA at 147.00 to target the 50-day EMA at 146.25. A failure to rebound there could open the door for a deeper decline toward the 144.00–144.35 area, where a tentative support line from April and the 23.6% Fibonacci retracement of the January–April downleg are sitting.

To the upside, a sustained break above the 148.80–149.40 resistance zone is a prerequisite for a rally toward the 151.00 round level and the 61.8% Fibonacci mark at 151.60. Beyond that, the pair could aim for a further advance toward 153.15.

Summing up, USD/JPY remains in a wait-and-see mode, with downside risks increasing after a second rejection at the key resistance zone of 148.80-149.40. A decisive move below the 200-day EMA could signal the start of the next bearish cycle.

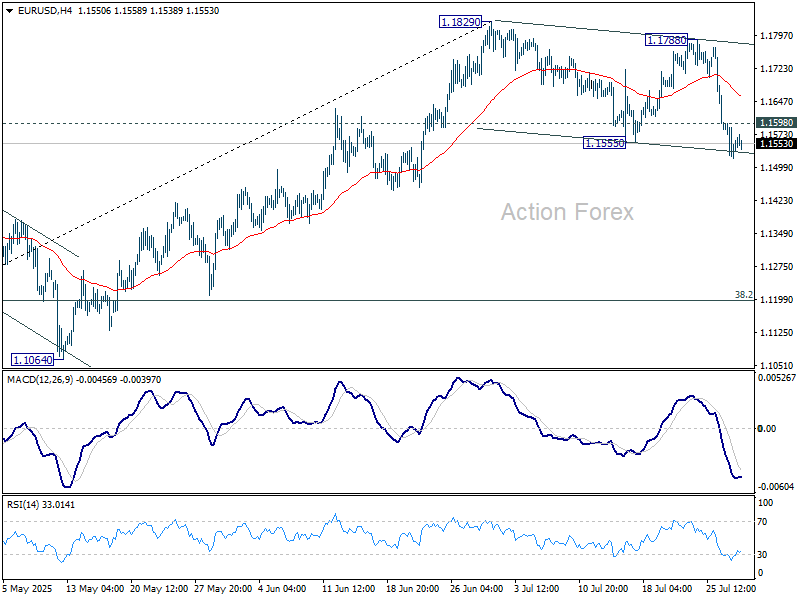

EUR/USD Dips Further While USD/CHF Consolidates Gains

EUR/USD extended losses and traded below the 1.1600 support. USD/CHF is rising and might aim for a move toward the 0.8120 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro struggled to clear the 1.1800 resistance and declined against the US Dollar.

- There is a key downward channel forming with resistance at 1.1575 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF is showing positive signs above the 0.8040 resistance zone.

- There is a connecting bullish trend line forming with support at 0.7990 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair failed to clear the 1.1800 resistance. The Euro started a fresh decline below the 1.1720 support against the US Dollar.

The pair declined below the 1.1660 support and the 50-hour simple moving average. Finally, it tested the 1.1520 level. A low was formed at 1.1519 and the pair is now consolidating losses. The market is showing bearish signs, and the upsides might remain capped.

There was a minor increase toward the 23.6% Fib retracement level of the downward move from the 1.1770 swing high to the 1.1519 low. Immediate resistance on the upside is near the 1.1575 level.

There is also a key downward channel forming with resistance at 1.1575. The next major resistance is near the 1.1665 zone and the 50-hour simple moving average or the 50% Fib retracement level.

The main resistance sits near the 1.1770 level. An upside break above the 1.1770 level might send the pair towards 1.1800. Any more gains might open the doors for a move towards 1.1850.

On the downside, immediate support on the EUR/USD chart is seen near 1.1520. The next major support is near the 1.1465 level. A downside break below 1.1465 could send the pair towards 1.1350.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from the 0.7910 support. The US Dollar climbed above the 0.8000 resistance zone against the Swiss Franc.

The bulls were able to pump the pair above the 50-hour simple moving average and 0.8040. A high was formed at 0.8079 and the pair is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 0.7911 swing low to the 0.8079 high.

There is also a connecting bullish trend line forming with support at 0.7990. On the upside, the pair is now facing resistance near 0.8080. The main resistance is now near 0.8120.

If there is a clear break above the 0.8120 resistance zone and the RSI remains above 50, the pair could start another increase. In the stated case, it could test 0.8200. If there is a downside correction, the pair might test the 0.7990 level.

The first major support on the USD/CHF chart is near the 0.7950 level and the 76.4% Fib retracement level.

The next key support is near 0.7910. A downside break below 0.7910 might spark bearish moves. Any more losses may possibly open the doors for a move towards the 0.7850 level in the near term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBPUSD Elliott Wave Insight: Bounce Should Fail Into Support Zone

The GBPUSD is trading in higher high sequence from 9.22.2022 low in weekly. The bounce is corrective Elliott Wave sequence & expect further upside. It favors pullback in proposed 7 swings from 7.01.2025 high & extend into 1.3162 – 1.2898 area, while below 7.23.2025 high. It should find buyers in to extreme area for next leg higher in daily or at least 3 swings bounce. In 4-hour, it started correcting lower from 7.01.2025 high. It ended W at 1.3362 low of 7.16.2025 & X at 1.3589 high of 7.23.2025 each in 3 swings. Below X high, it favors downside in Y in 3 swings as it broke below 7.16.2025 low, expecting into extreme area. Within W, it ended ((a)) at 1.3523 low, ((b)) at 1.3620 high & ((c)) at 1.3362 low. Above there, it placed ((a)) at 1.3486 high, ((b)) at 1.3371 low & ((c)) as X connector at 1.3589 high. The double correction unfolds in 3-3-3 structure, which will completes, when current bounce fail below 7.23.2025 high to new low into extreme area. It ended ((a)) of Y into 0.618 – 0.764 Fibonacci extension area of W & expect 3 or 7 swings bounce in ((b)).

Below X high, it placed ((a)) of Y at 1.3305 low & favors bounce in ((b)) in 3 or 7 swings against 7.23.2025 high. Within ((a)), it ended (i) at 1.3528 low, (ii) at 1.3563 high, (iii) at 1.3413 low, (iv) at 1.3543 high & (v) at 1.3305 low. Above there, it favors bounce in (a) of ((b)) and expect small upside before it should pullback in (b). The next pullback in (b) should stay above 1.3305 low choppy price action before continue upside in (c). Ideally, ((b)) can bounce between 1.3413 – 1.3481 area as 0.382 – 0.618 Fibonacci retracement of ((a)) before continue lower. Wave ((b)) bounce expect to fail below 1.3591 high before extend lower in ((c)) into 1.3162 – 1.2898 to finish double correction. Because of higher high in daily since September-2022 low, it should find buyers in extreme area to resume higher. It expects sideways to higher until FOMC event followed by selloff, while bounce fail below 7.23.2025 high. We like to buy the pullback into extreme area for next leg higher or at least 3 swings reaction.

GBPUSD – 60-Minute Elliott Wave Technical Chart:

GBPUSD – Elliott Wave Technical Video:

https://www.youtube.com/watch?v=SzqapuFzQpo

Fed Policy Meeting Takes Center Stage

Markets

Yesterday’s first batch of US economic data wasn’t exactly groundbreaking. JOLTS job openings in June came in close to expectations with 7.43mln, easing from the 7.71mln in May while the July Conference Board’s consumer confidence indicator improved a bit more than expected from 95.2 to 97.2. The present situation was seen slightly less favourable than in June but only because of an upward revision to that month’s reading. The expectations component edged higher to 74.4 to nevertheless remain below both the pre- and post-pandemic levels. In any case it didn’t suffice for US yields to stop a decline that was already ongoing earlier in the day. A strong $44bn 7-year auction later only added to the drop. Net daily changes varied between -5.8 (2-yr) to -10.2 bps (30-yr). Such large moves also suggest some Treasury short covering ahead of tonight’s FOMC meeting. Bunds underperformed with yields adding up to 2.6 bps at the front. The sharp narrowing of interest rate differentials helped EUR/USD off the intraday lows but nothing more than that. The couple still lost the 1.1578 neckline to end the day at 1.1547. DXY tested the previous mid-July high at 98.95 but eventually closed below that intermediate resistance. USD/JPY snapped a three-day rise at 148.46. EUR/GBP (0.8648) followed through on technical return action lower after Monday’s failed test of the November 2023 high.

Some trade headlines have been hitting the wires over the last couple of hours again. China’s negotiator told reporters in the wake of a two-day meeting with US counterparts in Stockholm that they agreed on extending the current August 12 tariff deadline. UST Bessent was more cautious and said Trump will make the final call. In the talks with India, the US president said he thinks the country may end up with a 20-25% levy. Moving on to the busy economic calendar today we spot a French Q2 GDP beat this morning. Growing by 0.3% q/q was well above the 0.1% expected and follows a beat in Spain yesterday as well (0.7% q/q). Details were not as bright as the headline figure suggests though. Inventory building offset weak domestic demand and declining capital investments. Germany, Italy and the Euro area publish GDP numbers later today. The same goes for the US, where Q2 growth should have rebounded from an import-lead drag in Q1. The Fed policy meeting takes center stage though. While Powell is bound to leave rates unchanged at 4.25-4.5%, markets are particularly on the lookout for any hint regarding future easing now some (though definitely not all) of the tariff fog is ebbing away. While we don’t expect that to happen given talks with another major trading partner China are still ongoing and the relative resilience of the labour market, such a scenario would pressure the US dollar and rates. Money markets price in a 65% chance for a cut in September.

News & Views

Australian inflation eased to 0.7% q/q from 0.9% in 2025Q2, falling just shy of the 0.8% expected. The yearly print retreated to 2.1% from 2.4%, the lowest annual inflation rate since 2021Q1. Core gauges such as the trimmed mean and weighted median rose by 0.6% to be up 2.7% y/y. Per sector, annual goods inflation was down to 1.1% from 1.3% while services eased from 3.7% to 3.3%. The main contributors to the quarterly rise were housing (+1.2%), food and non-alcoholic beverages (+1%), and health (+1.5%) with transport (-0.7%) partially offsetting the rise due to automotive fuel (-3.4%). The numbers further solidify market expectations for an August rate cut by the Australian central bank (RBA). The RBA unexpectedly kept the policy rate unchanged at 3.85% earlier this month amid risks for a higher-than-expected Q2 CPI outcome. While technically having materialized (for the core gauge, at least), it was only marginal (2.7% vs the 2.6% the RBA expected). Front end Australian swap yields decline up to 4.5 bps. The Aussie dollar holds steady near the lower bound of an upward sloping channel around AUD/USD 0.6514.

Oil prices rebounded over the last days with yesterday’s 3.5% spike particularly catching the eye. Brent crude trades well north of $72/b, the highest since tensions in the Middle East hit a high after Israeli strikes on Iran. The latest uptick followed US president Trump drastically cutting the timeline for Russia to seek a ceasefire with Ukraine from 50 to 10 days. Failing to do so would prompt US sanctions on buyers of Russian oil, mainly China and India. This risks eventually ending up in millions of barrels of reduced Russian oil exports.

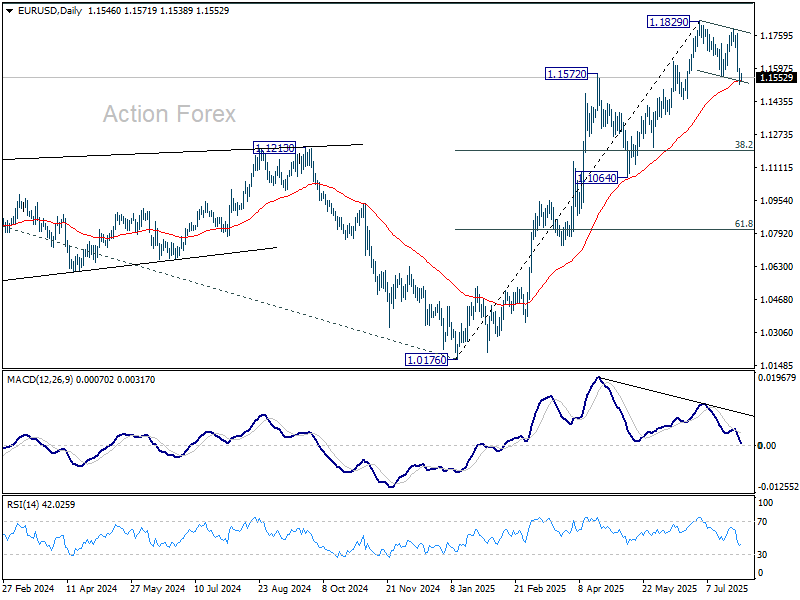

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1510; (P) 1.1554; (R1) 1.1590; More...

Focus stays on 55 D EMA (now at 1.1536). Sustained break there will argue that fall from 1.1829 is already correcting the whole rise from 1.0176. Deeper decline should then be seen to 38.2% retracement of 1.0176 to 1.1829 at 1.1198. Nevertheless, strong rebound from the EMA will maintain near term bullishness. Above 1.1598 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.