Sample Category Title

Ethereum Dynamics Point to an Altseason Approaching

Market Picture

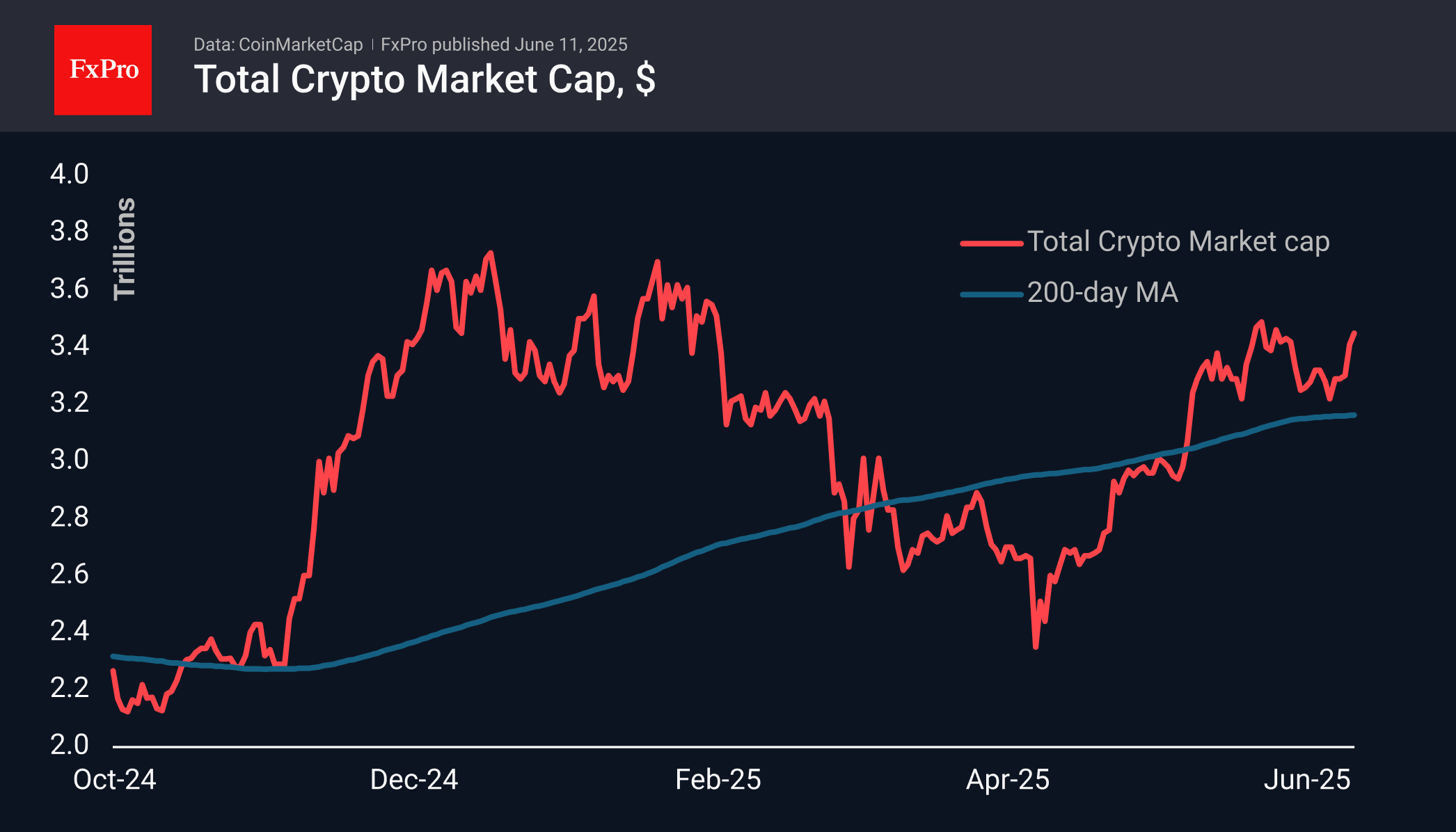

Market capitalisation grew by 0.6% in 24 hours, adding almost 4% in a week to $3.45 trillion. The market consolidated near these values a couple of weeks ago. Such a step-by-step climb is quite familiar. The likely continuation of positive sentiment allows us to consider the area of historical highs around $3.7 trillion as the next stop. The abundance of money from institutional and professional traders has dramatically suppressed FOMO impulses, so the type of market growth now looks more like a climb with frequent breaks than a rocket launch. Although less intense, this type of growth is more suitable for long-term portfolios.

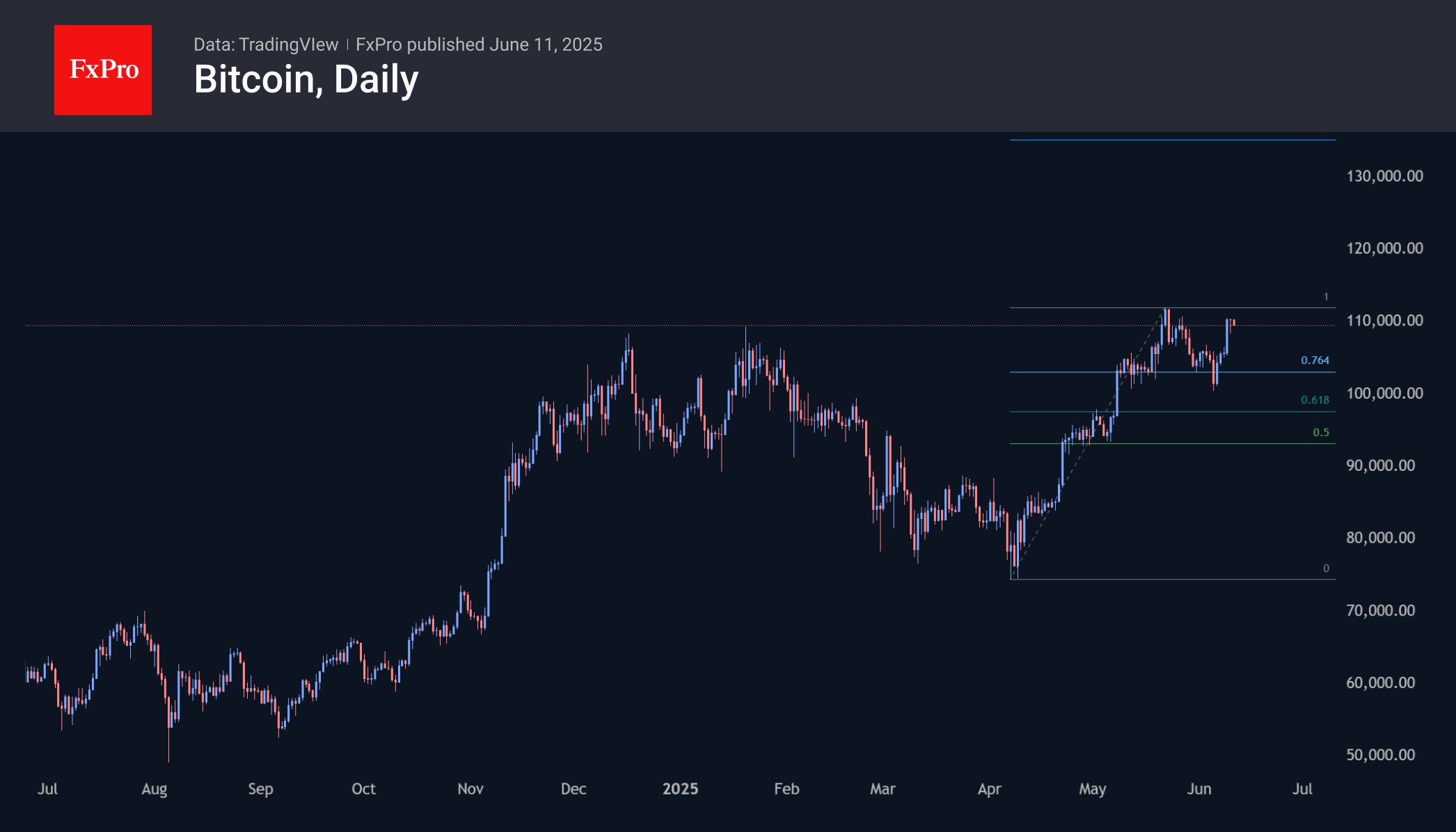

Bitcoin is trading above $109K, experiencing increased selling pressure on growth above $110K. This pressure may become even more intense as it approaches $112K, the area of the historical high set at the end of May. Breaking through this level will make $135K the technical target.

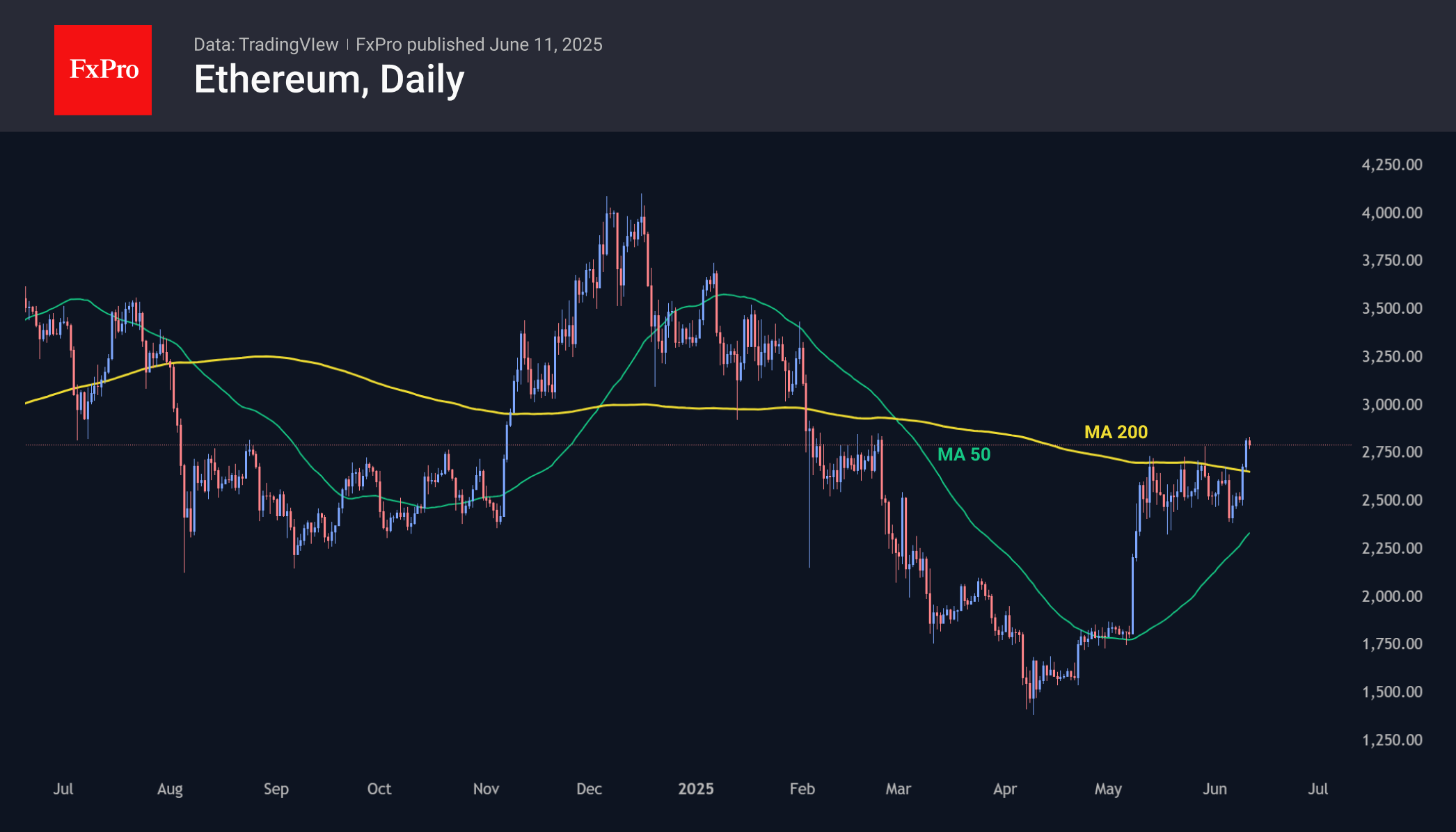

Ethereum has picked up momentum, adding nearly 5% in 24 hours to $2,800. It has recovered losses since the end of February and is consolidating above the 200-day moving average. If Ethereum’s dynamics are an indicator of altcoin sentiment, then we will see increased readiness for the altcoin season.

News Background

BlackRock’s largest Bitcoin ETF (IBIT) has become the fastest-growing exchange-traded fund in history. IBIT’s assets exceeded $70 billion in 341 trading days, while GLD took 1,691 days to do so.

Strategy additionally purchased 1,045 BTC ($110.2 million) last week at an average price of $105,426 per coin. The company now owns 582,000 BTC, purchased at an average price of $70,086. The total investment is estimated at $40.2 billion.

The Coinbase premium (the difference between prices on the largest American crypto exchange and other platforms) has reached a four-month high, indicating support from American buyers, according to CryptoQuant.

According to BaykusCharts, the supply of digital gold on exchanges has decreased by ~35%, from 1.55 million BTC to 1.01 million BTC, since July 2024.

US SEC Chairman Paul Atkins announced the agency’s new approach to non-custodial storage of cryptocurrencies. The agency is also working on measures to exempt De-Fi platforms from regulatory barriers.

USD/CAD Holds Near 2025 Low

When we last analysed the USD/CAD chart on 4 June, we identified a descending channel that remains relevant.

On 5 June, the pair reached a new low for 2025, and it is possible that bears will attempt to extend this move further over the course of the month.

Why is USD/CAD declining?

The Canadian dollar appears to be strengthening amid speculation that a trade agreement between the US and Canada could be finalised soon — possibly on 15 June, when the G7 summit is due to be held in Canada.

Media reports highlight several indicators supporting this view:

→ Prime Minister Mark Carney stated that Canada will meet its NATO spending target of 2% of GDP.

→ Canada refrained from retaliatory tariffs on steel and aluminium.

→ The US ambassador to Canada confirmed that “secret” negotiations are ongoing.

Technical Analysis of the USD/CAD Chart

Note that the R-line, which divides the lower half of the descending channel into two equal parts, acted as resistance — price reversed downward from this line and accelerated lower (as indicated by the arrow). This reinforces the view that bears currently dominate the USD/CAD market.

For now, the 1.3650 level appears to be a support zone for bulls, but its strength may be tested today as markets react to US inflation data. The Consumer Price Index (CPI) report is scheduled for release today at 15:30 GMT+3. Be prepared for potential spikes in volatility.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

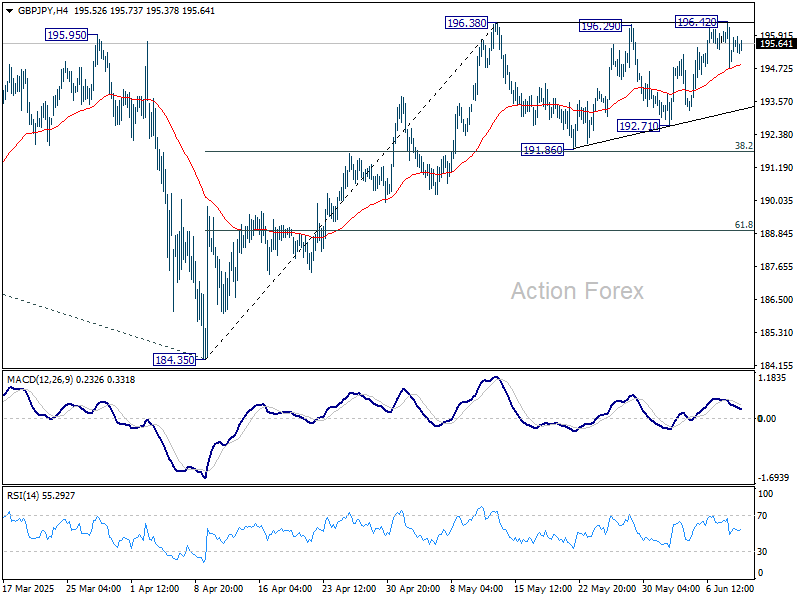

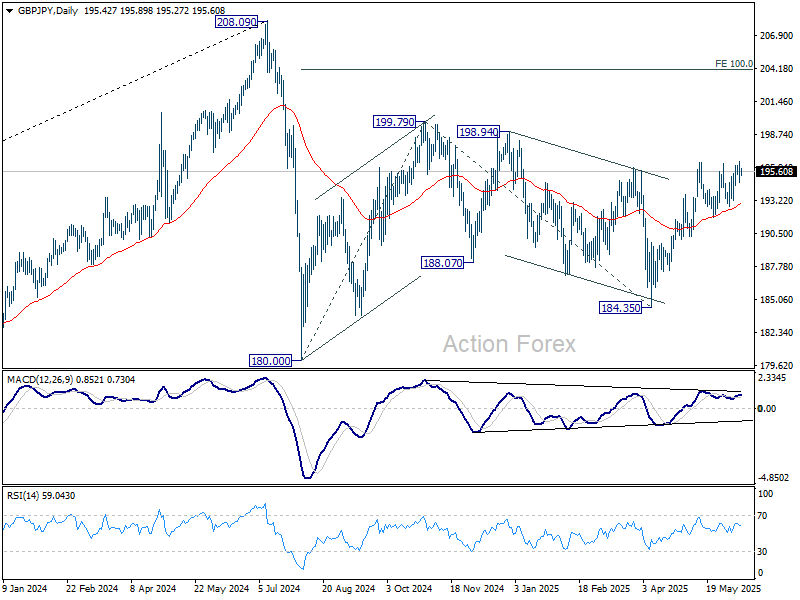

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.75; (P) 195.60; (R1) 196.43; More...

Intraday bias in GBP/JPY remains neutral first, and more consolidations could be seen. But further rise is in favor as long as 191.86 support holds. Firm break of 196.38 will resume whole rally from 184.35 to 199.79 resistance, and possibly further to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

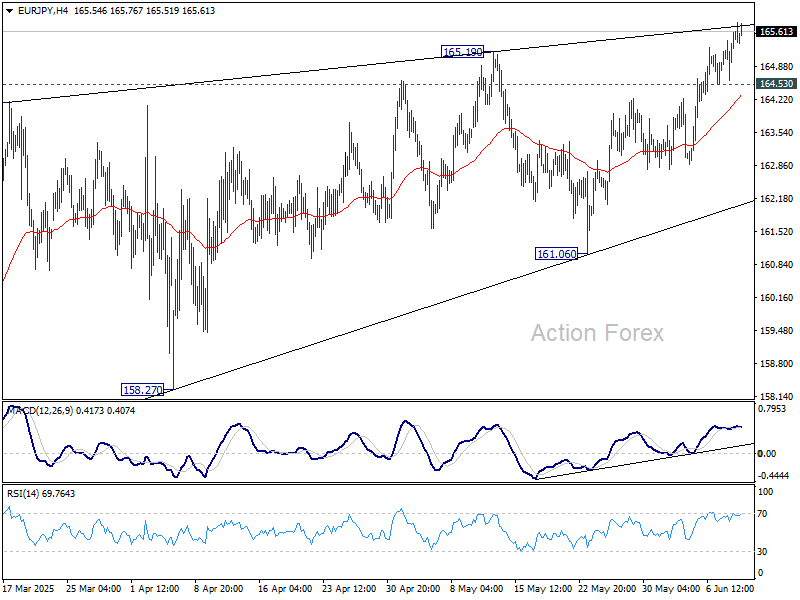

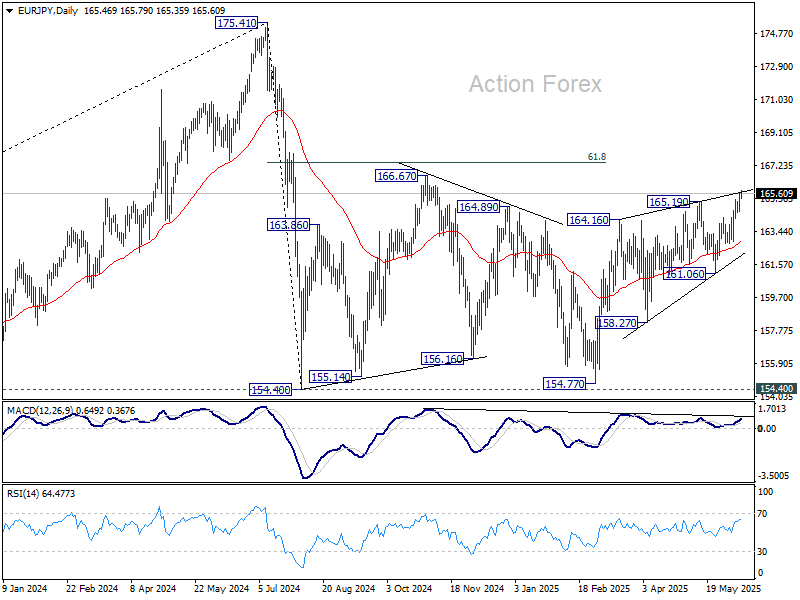

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.92; (P) 165.28; (R1) 165.93; More...

Intraday bias in EUR/JPY remains on the upside at this point. Current rise from 154.77 would target 166.67 resistance, and possibly further to 61.8% retracement of 175.41 to 154.77 at 167.38. On the downside, below 164.53 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 175.41 are seen as correction to up trend from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

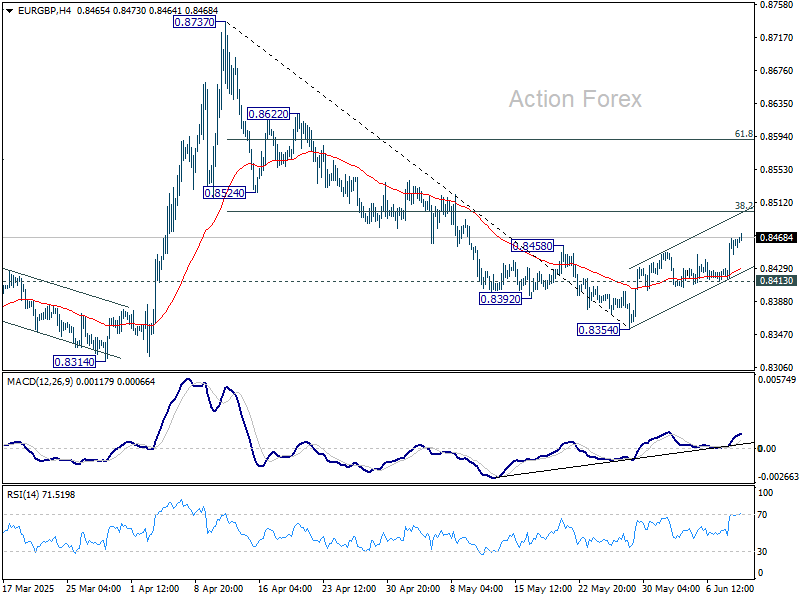

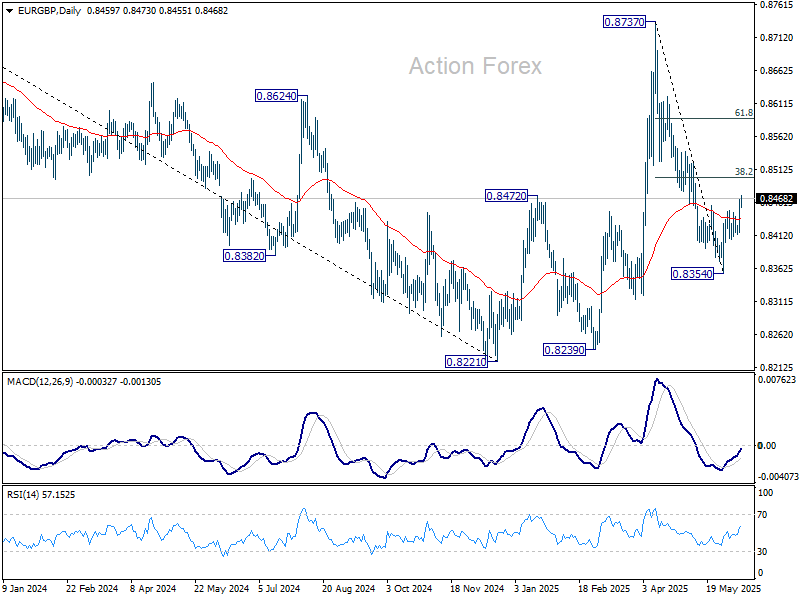

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8432; (P) 0.8450; (R1) 0.8483; More...

Intraday bias in EUR/GBP stays on the upside. Rebound from 0.8354 is in progress for 38.2% retracement of 0.8737 to 0.8354 at 0.8500. Strong resistance could be seen from 0.8500 to complete the corrective bounce. On the downside, break of 0.8413 support will bring retest of 0.8354 low. However, firm break of 0.8500 will pave the way to 61.8% retracement at 0.8591 instead.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. Nevertheless, there is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

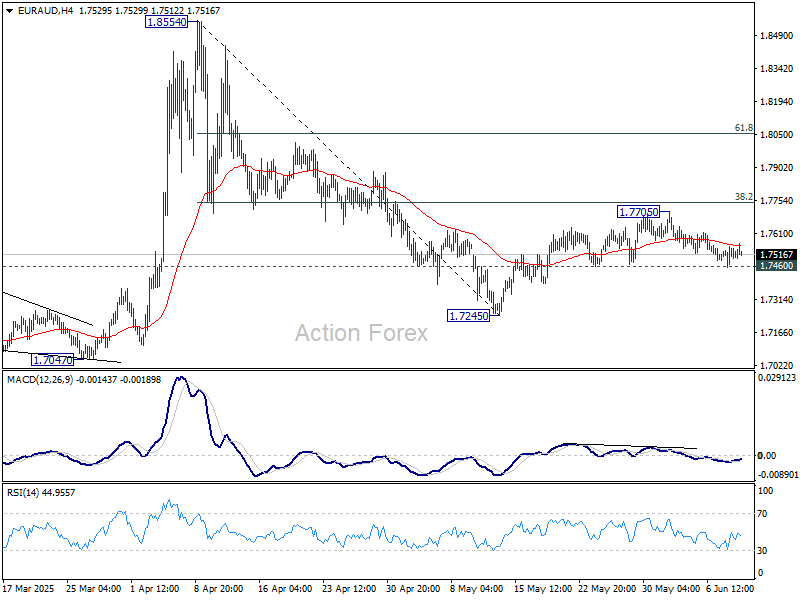

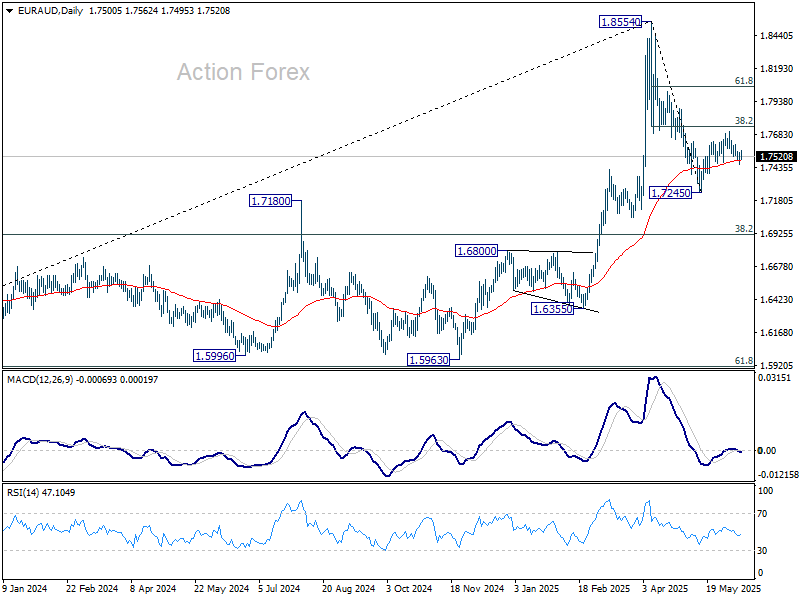

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7469; (P) 1.7511; (R1) 1.7559; More...

Intraday bias in EUR/AUD stays neutral at this point. On the downside, firm break of 1.7460 support will suggest that recovery from 1.7245 has already completed at 1.7705, 38.2% retracement of 1.8554 to 1.7245 at 1.7745. Intraday bias will be back on the downside for 1.7245 first. Firm break there will resume whole decline from 1.8554. On the upside, sustained break of 1.7745 will target 61.8% retracement at 1.8054.

In the bigger picture, with 55 W MACD staying well below signal line, 1.8554 is likely a medium term top already. Price actions from there are seen as a corrective pattern only. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is still expected to resume at a later stage.

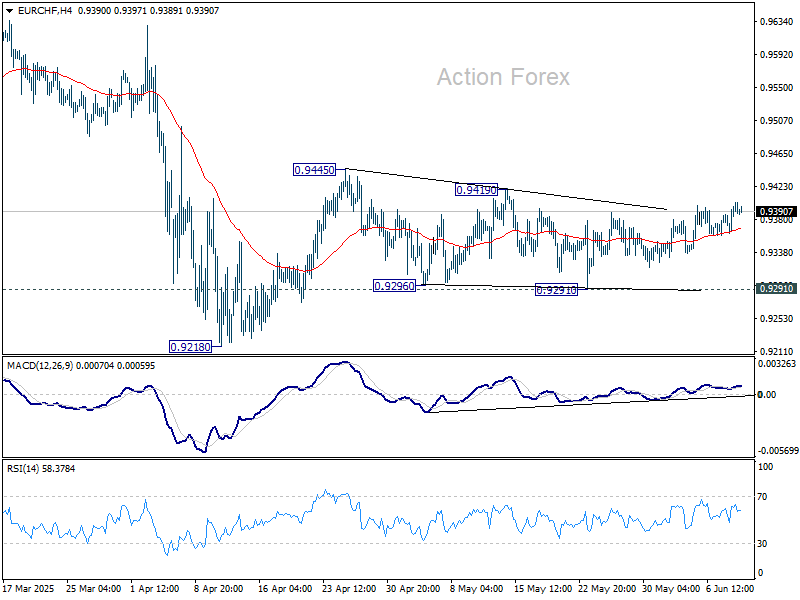

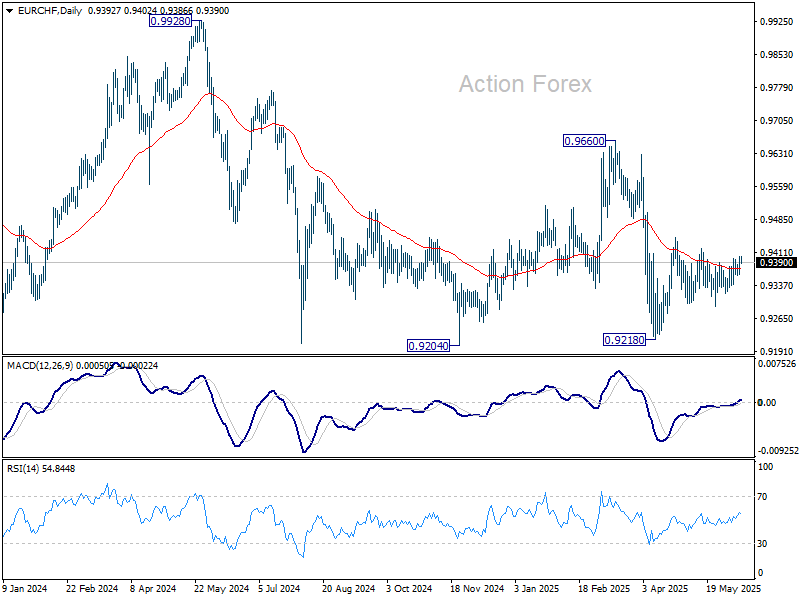

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9375; (P) 0.9390; (R1) 0.9417; More....

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, break of 0.9419 resistance will argue that the rise from 0.9218, either as a correction to fall from 0.9660, or the third leg of the pattern from 0.9204, is ready to resume through 0.9445. Nevertheless, on the downside, firm break of 0.9291 will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9527) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

AUD/USD & NZD/USD Aim Steady Increase

AUD/USD started a decent increase above the 0.6450 and 0.6500 levels. NZD/USD is also rising and might aim for more gains above 0.6080.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar rebounded after forming a base above the 0.6400 level against the US Dollar.

- There is a connecting bullish trend line forming with support at 0.6510 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating gains above the 0.6030 zone.

- There is a key bullish trend line forming with support at 0.6030 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from the 0.6450 support. The Aussie Dollar was able to clear the 0.6500 resistance to move into a positive zone against the US Dollar.

There was a close above the 0.6500 resistance and the 50-hour simple moving average. Finally, the pair tested the 0.6535 zone. A high was formed near 0.6533 and the pair recently started a consolidation phase.

There was a move below the 0.6520 level. The pair dipped below the 23.6% Fib retracement level of the upward move from the 0.6489 swing low to the 0.6533 high.

On the downside, initial support is near the 0.6510 level. There is also a connecting bullish trend line forming with support at 0.6510. It is close to the 50% Fib retracement level of the upward move from the 0.6489 swing low to the 0.6533 high.

The next major support is near the 0.6480 zone. If there is a downside break below the 0.6480 support, the pair could extend its decline toward the 0.6450 level.

Any more losses might signal a move toward 0.6420. On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.6535. The first major resistance might be 0.6550. An upside break above the 0.6580 resistance might send the pair further higher.

The next major resistance is near the 0.6600 level. Any more gains could clear the path for a move toward the 0.6650 resistance zone.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a steady increase from the 0.5990 zone. The New Zealand Dollar broke the 0.6020 resistance to start the recent increase against the US Dollar.

The pair settled above 0.6030 and the 50-hour simple moving average. It tested the 0.6065 zone and is currently consolidating gains. The pair corrected lower below the 0.6050 level and the 23.6% Fib retracement level of the upward move from the 0.6006 swing low to the 0.6064 high.

However, the bulls are active above the 0.6030 level. The NZD/USD chartsuggests that the RSI is stable near 50. On the upside, the pair might struggle near 0.6065. The next major resistance is near the 0.6080 level.

A clear move above the 0.6080 level might even push the pair toward the 0.6120 level. Any more gains might clear the path for a move toward the 0.6200 resistance zone in the coming days.

On the downside, immediate support is near the 0.6030 level. There is also a key bullish trend line forming with support at 0.6030. It is close to the 61.8% Fib retracement level of the upward move from the 0.6006 swing low to the 0.6064 high.

The first key support is near the 0.6005 level. The next major support is near the 0.5990 level. If there is a downside break below the 0.5990 support, the pair might slide toward the 0.5970 support. Any more losses could lead NZD/USD in a bearish zone to 0.5950.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

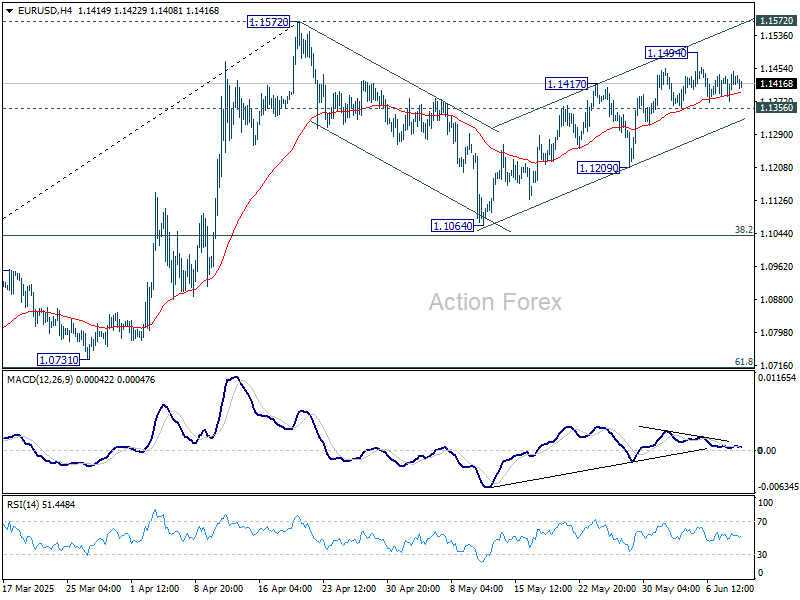

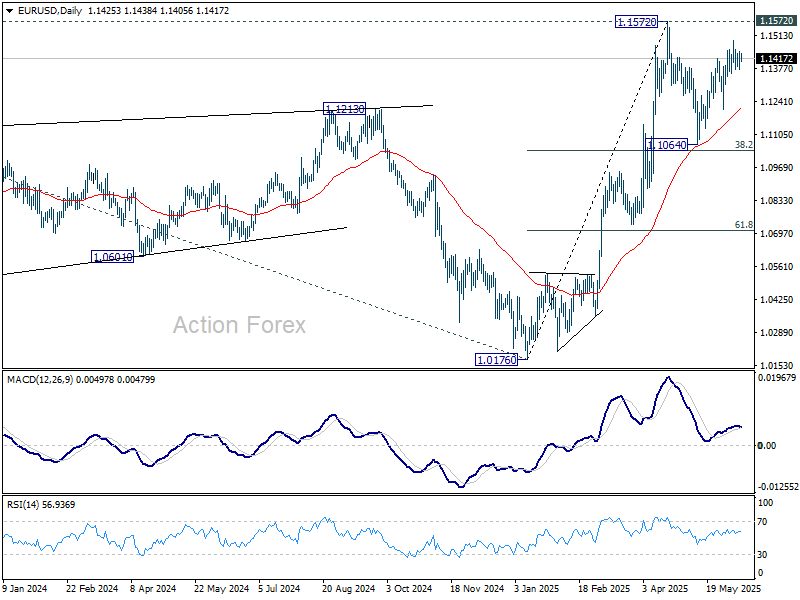

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1383; (P) 1.1415; (R1) 1.1458; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Price actions from 1.1572 are seen as a corrective pattern to rally from 1.0716. While rebound from 1.1064 might extend, strong resistance should emerge from 1.1572 to limit upside. On the downside, break of 1.1356 support will argue that the correction is already in the third leg, and target 1.1209 support for confirmation.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0894) holds.

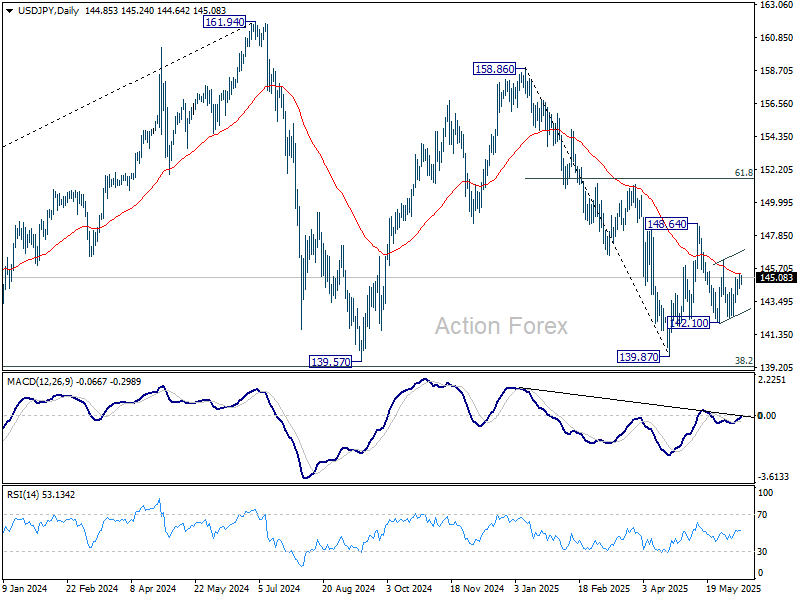

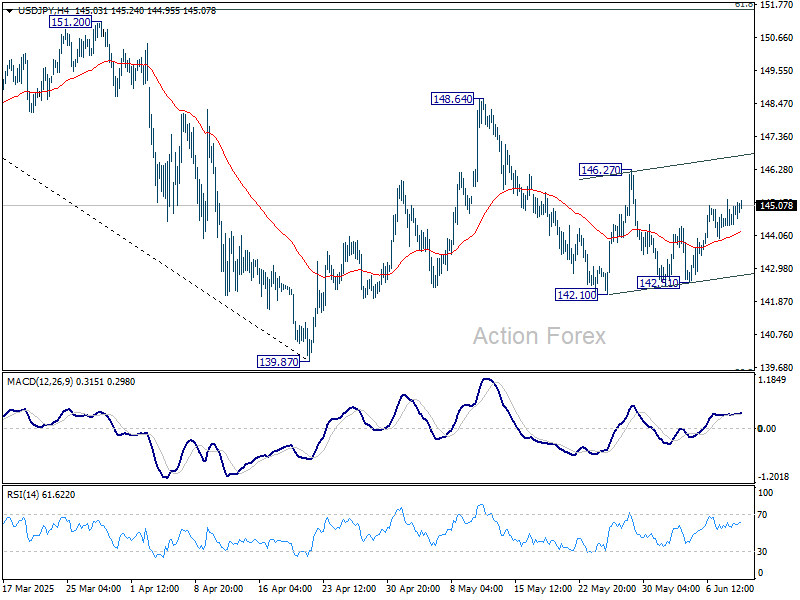

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.44; (P) 144.86; (R1) 145.33; More...

Intraday bias in USD/JPY remains neutral. On the upside, above 146.27 resistance will argue that price actions from 148.64 has completed as a corrective pattern. Intraday bias will be back on the upside for 148.64 resistance and above to resume the rebound from 139.87 low. However, firm break of 142.10 will bring retest of 139.87 instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.