Sample Category Title

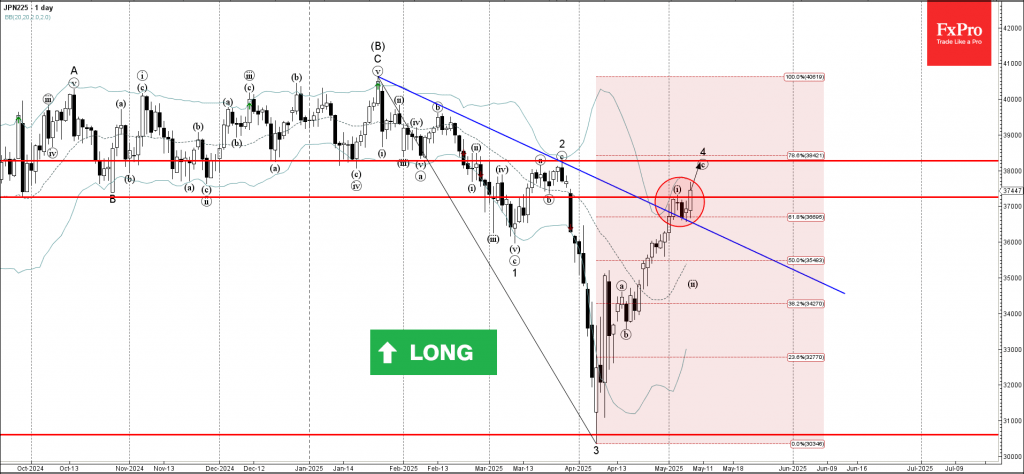

Nikkei 225 index Wave Analysis

Nikkei 225 index: ⬆️ Buy

- Nikkei 225 index broke the resistance zone

- Likely to rise to resistance level 38275,00

Nikkei 225 index recently broke the resistance area between the resistance level 37255.00, resistance trendline from January and the 61,8% Fibonacci correction of the downward impulse from January.

The breakout of this resistance zone accelerated the active impulse wave c of the intermediate ABC correction 4 from the start of April.

Nikkei 225 index can be expected to rise to the next resistance level 38275,00 (former monthly high from March and the target for the completion of the active impulse wave c).

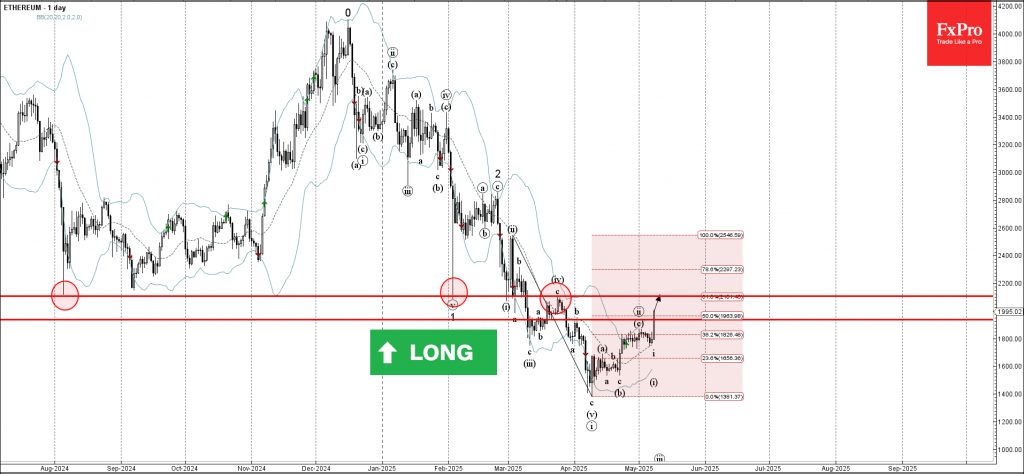

Ethereum Wave Analysis

Ethereum: ⬆️ Buy

- Ethereum broke the resistance zone

- Likely to rise to resistance level 2100,00

Ethereum cryptocurrency recently broke the resistance area between the major resistance level 1935,00 (former monthly top from April) and the 50% Fibonacci correction of the downward impulse from March.

The breakout of this resistance zone accelerated the active short-term ABC correction ii from the start of April.

Given the strongly bullish sentiment seen across the cryptocurrency markets, Ethereum cryptocurrency can be expected to rise to the next resistance level 2100,00 (top of the previous correction iv).

Sunset Market Commentary

Markets

The Bank of England stuck to its quarterly cutting pace in place since August of last year. They lowered the key policy rate by 25 bps to 4.25% in a 3-way vote. Five out of nine members supported the decision with two in favour of a larger, 50 bps, rate cut and two in favour of keeping rates steady. Minutes of the meeting showed that “prior to the latest global developments, most members in this group had judged that this policy decision would be finely balanced between no change in Bank Rate and a further reduction.” Going into the release, some expected the BoE to drop a reference to gradual rate cuts. That is not the case. Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate. Similarly, markets feared significant downgrades to the expected growth path. BoE Bailey at the press conference downplayed those concerns as well. Short term prospects faced an upward revision because of stronger actual data (2025 Q2: 0.8% Y/Y from 0.3%), medium term was slightly downwardly revised (2026 Q2: 1.3% Y/Y from 1.5%), while the long term end point is pretty much the same (2027 Q2: 1.5% Y/Y from 1.4%). This baseline forecast is conditioned on the market path for interest rates. Deputy governor Ramsden added that downward revisions to business investments and the increasing (precautionary) household savings rate could easily unlock upside potential if global uncertainty is reduced, for example by the flagged UK-US trade deal. UK inflation is likely to rise to 3.7% by September, partly because of increases in energy prices and increases in some regulated prices such as water bills. Inflation is expected to fall back to the 2% target after that. But there are risks around this path of inflation. Bank staff prepared two alternative scenarios. In one scenario, there could be weaker supply and more persistence in domestic wages and prices, including from second-round effects related to the near-term increase in CPI inflation. In another scenario, inflationary pressures could ease more quickly owing to greater or longer-lasting weakness in demand relative to supply, in part reflecting uncertainties globally and domestically. Bailey stressed that these are only two examples of a wide range of different paths the economy could take. In the former, inflation ends up 0.4 ppt higher over the forecasting period. In the latter, the path is 0.3 ppt lower over the policy horizon. The baseline projection is 3.4% Y/Y for 2025 Q2, 2.4% for 2026 Q2 and 1.9% for 2027 Q2. The UK Gilt curve bear flattened (UK 2-y yield +6 bps) after the BoE meeting as the central bank wasn’t as doom and gloom as feared (hawkish cut), sticking to its gradual approach. EUR/GBP dipped from 0.8510 to 0.8480. The amount of global uncertainty calls for patience, as witnessed in today’s Riksbank and Norges Bank decisions as well. It should serve as a reminder to the dovish-skewed market positioning going into the June ECB meeting. EMU money markets almost fully discount a June rate cut, with another one priced in by September.

News & Views

The Swedish Riksbank left its policy rate unchanged at 2.25%. The uncreased uncertainty abroad makes the economic outlook slightly weaker. The impact on inflation is more difficult to assess. The executive board still sees monetary policy currently as well balanced providing the room to assess further information. Still it is somewhat more probable that inflation will be lower than that it will be higher compared to the March forecast. The central bank concludes that a slight further easing of monetary policy could occur going forward. Swedish money markets already (more than) fully discounted an additional RB rate cut later this summer (August or September). EUR/SEK holds the 10.90 area after having a good run in February/March. The Norges Bank (NB) also left its policy rate unchanged at 4.50%, the cycle peak in place since December 2023. The MPC also sees uncertainty about future economic developments, but the outlooks still implies that the policy rate will most likely be reduced during the course of 2025. In March, the NB guided the policy rate to be near 4.0% by the end of the year. Inflation has fallen markedly from the peak but is still above the 2% target. For now, a restrictive policy is still needed to bring inflation down to target within a reasonable time horizon. Trade barriers have become more extensive, and there is uncertainty about future trade policies. This may pull the interest rate outlook in different directions. The NB will judge on the basis of new forecasts in June. For now markets still only see a 50/50 chance of a rate cut next month. EUR/NOK is trading little changed near 11.70.

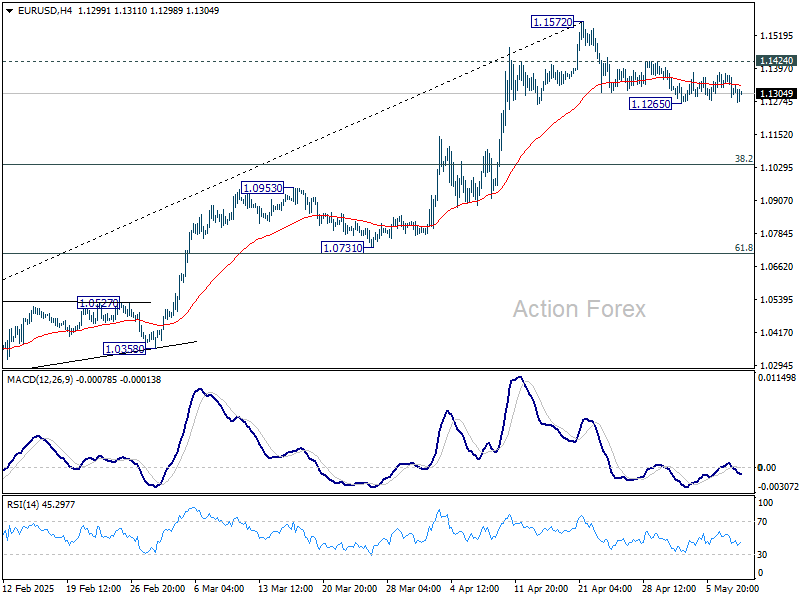

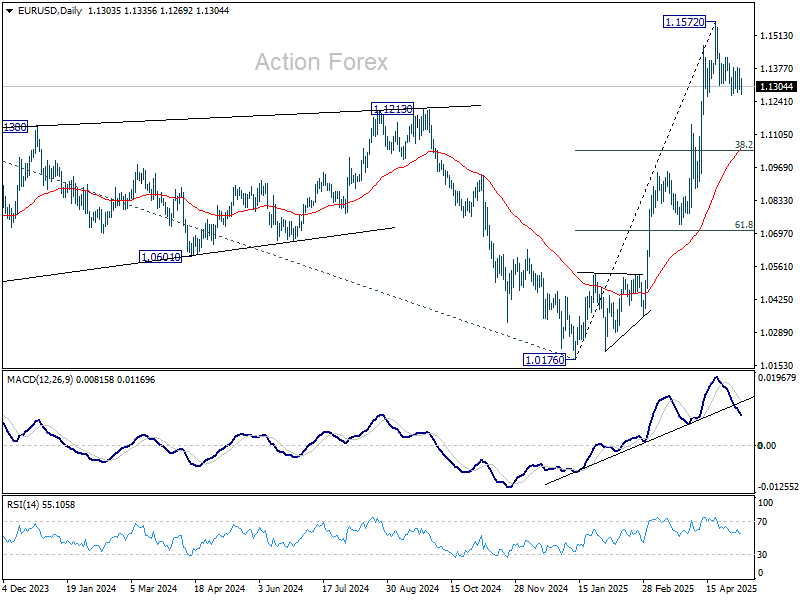

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1270; (P) 1.1324; (R1) 1.1356; More...

EUR/USD is staying in sideway trading and intraday bias remains neutral. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

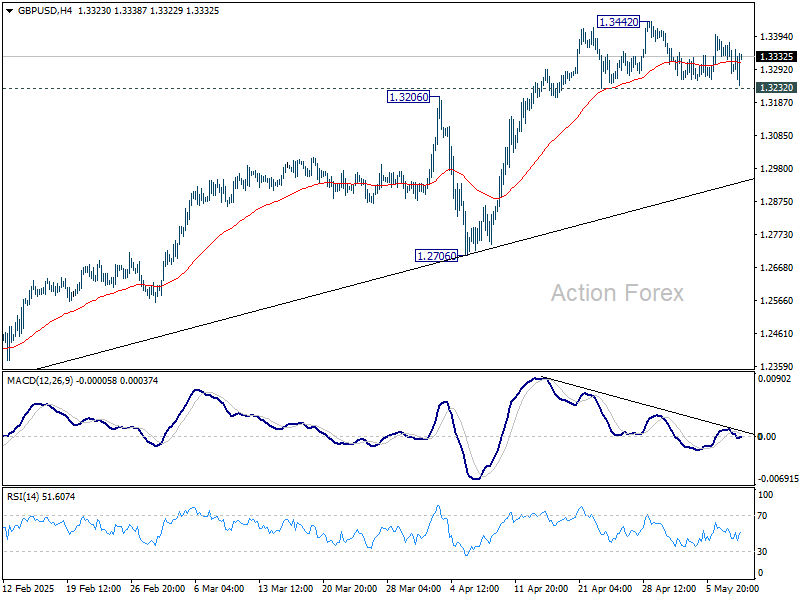

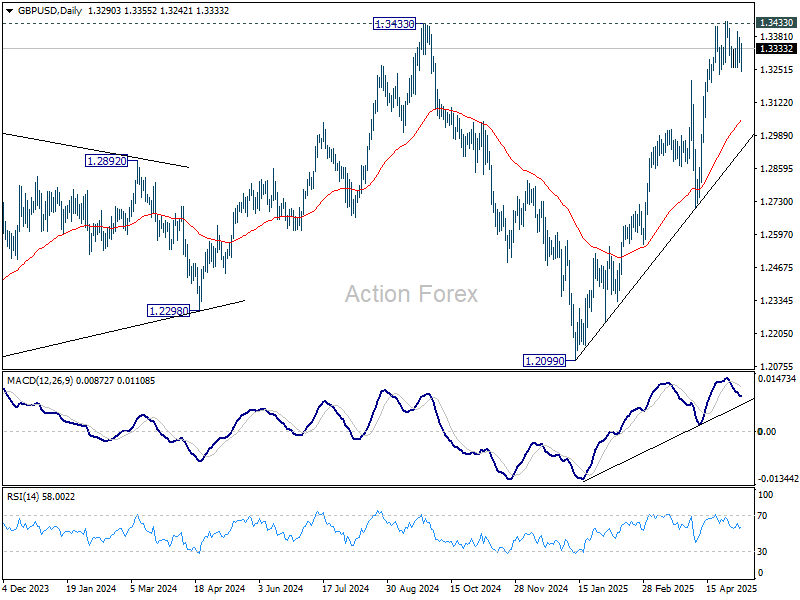

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3254; (P) 1.3318; (R1) 1.3357; More...

Intraday bias in GBP/USD remains neutral as sideway trading continues. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3051) and possibly below. On the upside, decisive break of 1.3433 key resistance will confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

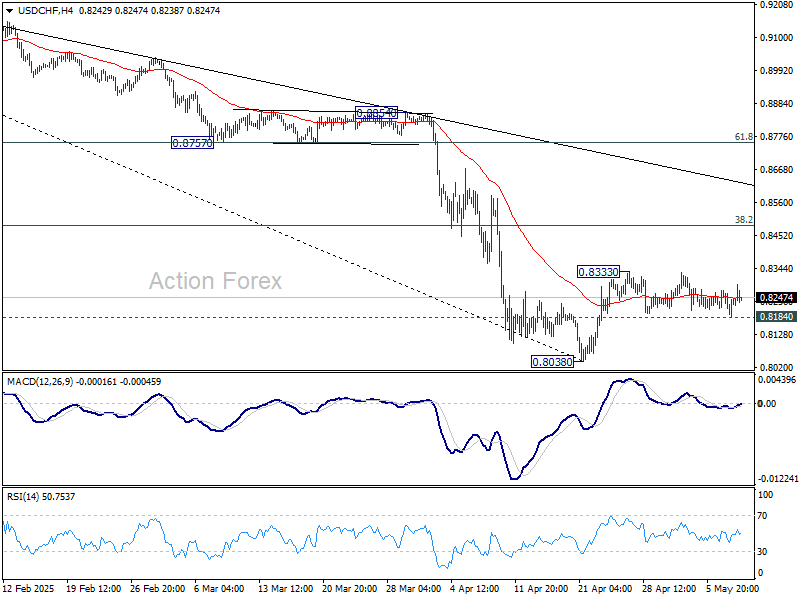

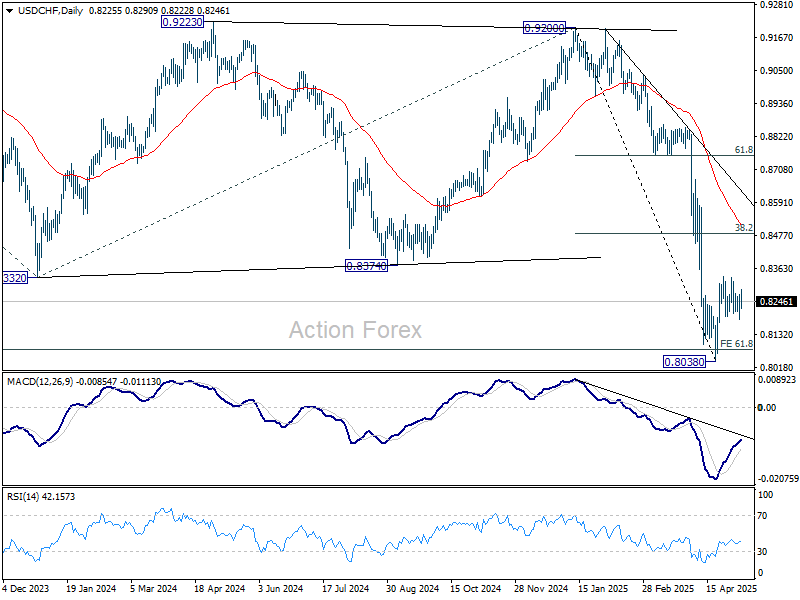

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8192; (P) 0.8232; (R1) 0.8278; More….

Intraday bias in USD/CHF remains neutral for the moment. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, firm break of 0.8184 will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

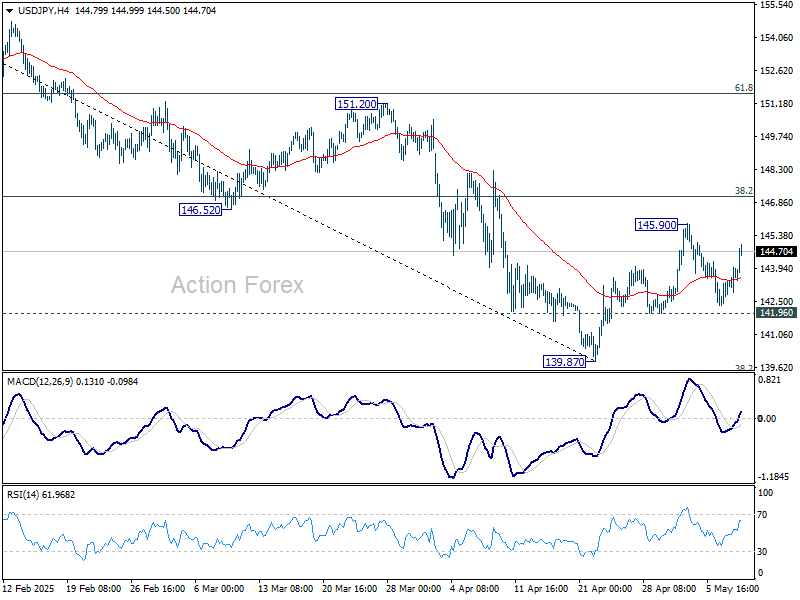

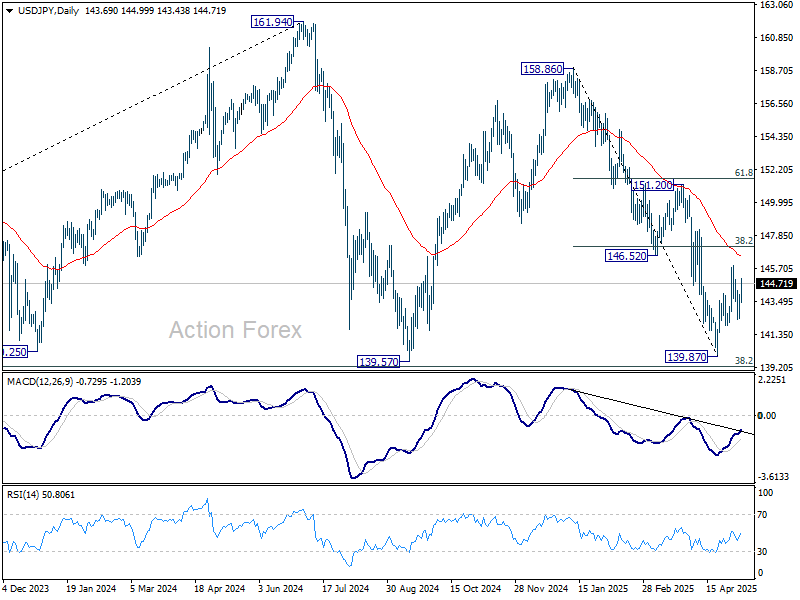

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.81; (P) 143.40; (R1) 144.43; More...

USD/JPY rebounded further today but stays below 145.90 resistance. Overall, rise from 139.87 could extend through 145.90. But near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Pound and Dollar Lead FX on UK-US Trade Deal, BoE Cut Overshadowed

Sterling and the US Dollar are leading gains among major currencies today, lifted by anticipation surrounding the imminent announcement of a comprehensive US-UK trade agreement. The Pound remained resilient after BoE's expected 25bps rate cut. The three-way split within the BoE’s Monetary Policy Committee and the mixed implications of its economic projections have made it difficult for markets to form a decisive reaction.

BoE’s updated economic projections included two alternative scenarios, one based on weaker global demand due to trade disruptions, the other on renewed inflation stickiness from second-round effects. But with global trade dynamics in flux, these projections are highly conditional and arguably academic at this stage. A trade deal with the US may relieve some economic pressure on Britain, but its benefit depends on how the US proceeds with other partners, especially the EU and China.

For now, attention is squarely on the 1400 GMT press conference where US President Donald Trump is expected to formally unveil the UK trade deal. Trump described the agreement as “full and comprehensive,” calling it a first step in a broader realignment of US trade policy. UK Prime Minister Keir Starmer’s office confirmed talks have progressed swiftly and promised an update later today.

Meanwhile, Euro is also holding firm despite signs of growing transatlantic strain. European Commission has announced preparations for countermeasures in response to Washington’s reciprocal tariff regime, launching a WTO dispute and consulting on duties affecting EUR 95B worth of US imports. Still, EC President Ursula von der Leyen emphasized a preference for negotiation, suggesting room remains for diplomacy.

In contrast, Yen is the weakest major currency today, Loonie and Swiss Franc. Aussie and Kiwi are positioning in the middle.

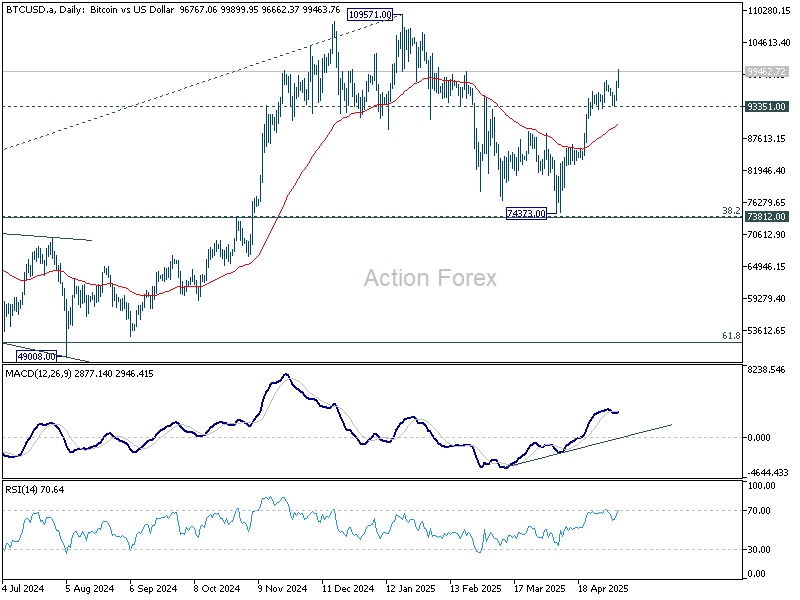

Technically, Bitcoin's rally from 74373 resumed today by breaking through 97944 resistance. Further rally is expected as long as 93351 support holds, to retest 109571 record high. Nevertheless, barring clear sign of upside acceleration, current rise is seen as the second leg a medium term corrective pattern. Hence, strong resistance is expected from 109571 to limit upside to bring near term reversal.

In Europe, at the time of writing, FTSE is up 0.17%. DAX is up 0.80%. CAC is up 0.92%. UK 10-year yield is up 0.025 at 4.489. Germany 10-year yield is up 0.018 at 2.494. Earlier in Asia, Nikkei rose 0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.28%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield rose 0.025 to 1.325.

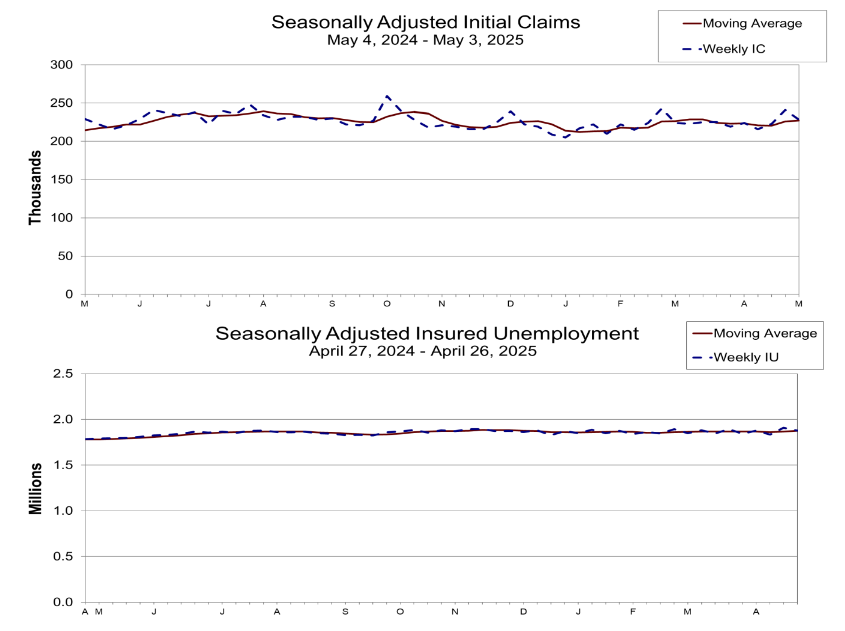

US initial jobless claims fall to 228k vs exp 235k

US initial jobless claims fell -13k to 228k in the week ending May 3, below expectation of 235k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims fell -29k to 1879k in the week ending April 26. Four-week moving average of continuing claims rose 9k to 1875k.

BoE cuts 25bps, three-way vote split reveals growing rift on rate path

BoE lowered its benchmark Bank Rate by 25 basis points to 4.25% , in line with market expectations. However, the decision revealed a rare three-way split among policymakers.

Five members supported the 25bps reduction, while Catherine Mann and Chief Economist Huw Pill voted to keep rates unchanged. On the dovish end, Swati Dhingra and Alan Taylor backed a deeper 50bps cut.

In its accompanying statement, BoE reiterated that a "gradual and careful approach" remains appropriate as it withdraws monetary restraint.

While acknowledging progress on inflation, the central bank emphasized the need for policy to stay “restrictive for sufficiently long” to ensure inflation returns sustainably to the 2% target.

In its latest Monetary Policy Report, the BoE’s baseline forecast sees CPI inflation rising to 3.5% in Q3 2025 before easing back to 2% in the medium term.

But policymakers outlined two risk-laden alternative scenarios. The first, a lower demand scenario, assumes heightened uncertainty depresses domestic spending and inflationary pressures fade more quickly. Under this path, the economy faces a wider output gap and inflation runs -0.3% lower than baseline by the three-year horizon.

Conversely, the second scenario envisions higher inflation persistence, where near-term rise in headline inflation triggers second-round effects in wages and prices, compounded by weak productivity growth. In this case, the impact on growth is modest, but inflation runs 0.4% above baseline throughout the forecast period.

RBNZ flags global growth risks as tariffs echo COVID-era disruptions

RBNZ Governor Christian Hawkesby warned today that rising global tariffs are having a clear and negative impact on global economic activity, prompting the central bank to revise down its projections for global growth.

Speaking to a parliamentary committee, Hawkesby called the effects of the tariff wave “unambiguously” harmful. He added that while New Zealand’s exposure to a 10% US tariff on exports poses challenges, the softer New Zealand Dollar may help cushion some of the blow. Nonetheless, weaker demand from key trading partners is now a growing concern for the country’s outlook.

Hawkesby drew a stark comparison between the supply-side disruptions caused by current tariffs and those seen during the COVID-19 pandemic, stressing that both are capable of delivering long-lasting economic distortions.

“We know from our experience, from the COVID experience, that supply side impacts are significant, and that are long-lasting and can create real challenges,” he said.

He added that the situation remains fluid, with considerable uncertainty about how the structural dynamics of the global economy will adjust to this new trade regime.

BoJ minutes: Caught between global uncertainty and domestic price pressures

Minutes from BoJ’s March meeting revealed growing concern among policymakers over the external risks posed by US tariff policies.

One member warned that downside risks from these policies had “rapidly heightened” and could significantly harm Japan’s real economy, suggesting BoJ should "be particularly cautious when considering the timing for the next rate hike."

However, not all board members advocated for a cautious stance. Another member stressed that even amid heightened uncertainty, BoJ should not automatically default to a cautious stance, stating that BOJ "might face a situation where it should act decisively".

A third voice on the board emphasized the importance of incorporating inflation expectations, upside risks to prices, and progress in wage growth into BoJ’s policy deliberations. Domestic developments could still justify tightening if conditions shift meaningfully.

Separately, BoJ Governor Kazuo Ueda reinforced this message in his remarks to parliament today, acknowledging that while food price volatility, particularly for rice, remains elevated, these pressures would ease over time.

Nonetheless, Ueda emphasized the importance of monitoring price developments closely, given the elevated uncertainty in the global economic environment.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.81; (P) 143.40; (R1) 144.43; More...

USD/JPY rebounded further today but stays below 145.90 resistance. Overall, rise from 139.87 could extend through 145.90. But near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US initial jobless claims fall to 228k vs exp 235k

US initial jobless claims fell -13k to 228k in the week ending May 3, below expectation of 235k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims fell -29k to 1879k in the week ending April 26. Four-week moving average of continuing claims rose 9k to 1875k.