Sample Category Title

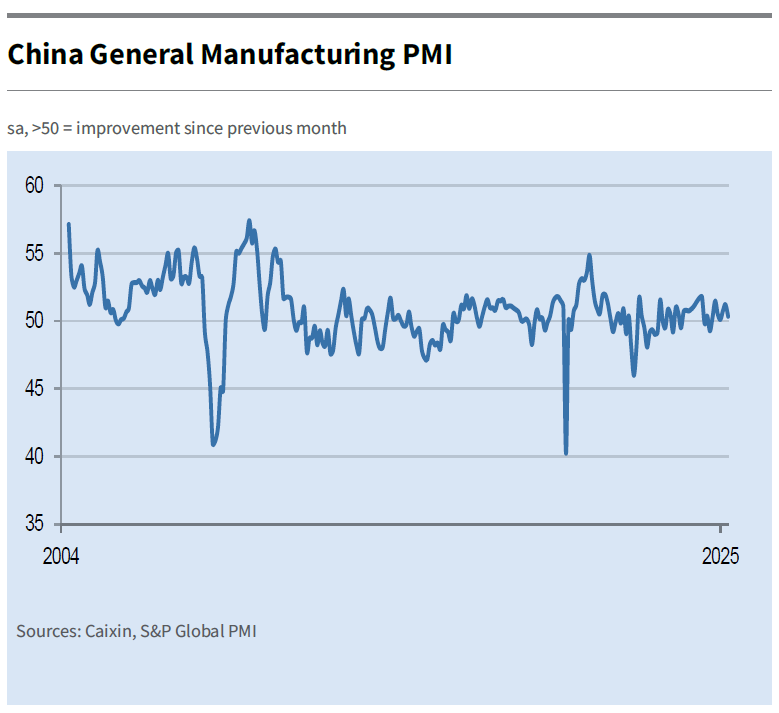

China’s factory activity slumps on trade conflicts, optimism near record lows

China’s factory activity slumped sharply in April as official NBS Manufacturing PMI dropped from 50.5 to 49.0, its lowest level since December 2023 and below expectations of 49.9. Non-manufacturing PMI also weakened from 50.8 to 50.4.

The decline points to early signs of strain from escalating trade tensions, with NBS citing “sharp changes in the external environment” as a key driver.

Private-sector data painted a similarly cautious picture. Caixin Manufacturing PMI dropped to 50.4, its lowest in three months and just narrowly remaining in expansion.

Caixin's Senior Economist Wang Zhe noted that while production and demand grew modestly, the pace has slowed and forward-looking optimism weakened significantly—plunging to the third-lowest level ever recorded. Trade-related uncertainty was a key concern for firms, weighing heavily on sentiment despite hopes for more policy support.

The April PMIs point to early-stage fallout from the China-US tariff standoff. Businesses are already reporting shrinking employment, delayed logistics, and inventory drawdowns. With both consumer and business confidence faltering, the government faces growing pressure to deploy stimulus measures. Unless domestic demand recovers and external risks subside, China’s economy could face more headwinds in Q2 and beyond.

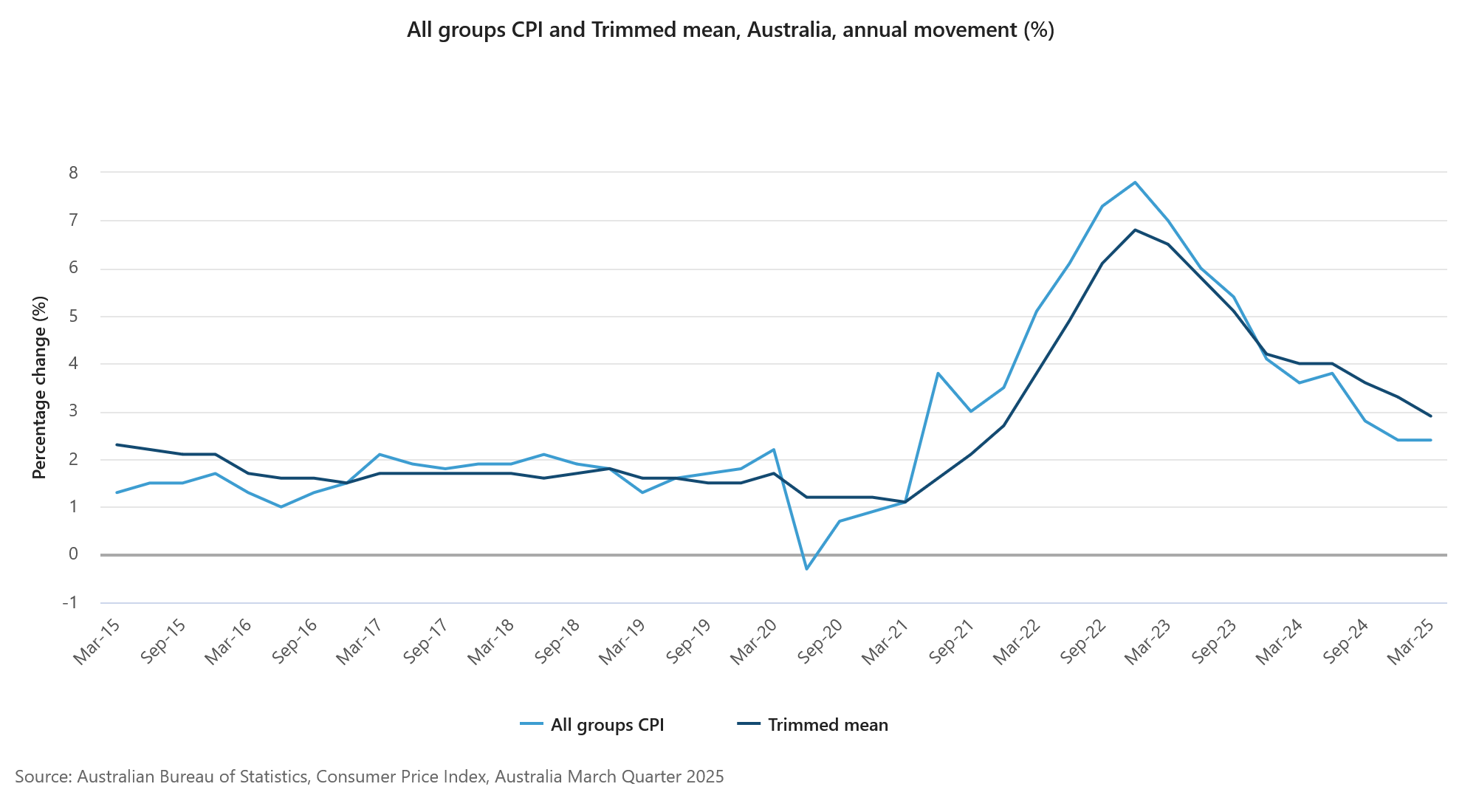

Australia’s trimmed mean CPI returns to RBA’s target band, services inflation eases further

Australia's headline CPI was unchanged at 2.4% yoy in Q1, above expectations of a slight decline to 2.2% yoy. On a quarterly basis, CPI rose 0.9% qoq, also exceeding forecast of 0.8% qoq.

The closely watched trimmed mean CPI, a core inflation gauge, slowed from 3.3% yoy to 2.9% yoy , falling back within RBA’s 2–3% target range for the first time since 2021, in line with market expectations. However, the quarterly increase of 0.7% qoq was a touch higher than the anticipated 0.6% qoq.

Annual goods inflation accelerated from 0.8% yoy to 1.3% yoy, driven by a notable rebound in electricity prices. Services inflation eased from 4.3% yoy to 3.7% yoy, its lowest since mid-2022, amid broad-based moderation in rent and insurance costs.

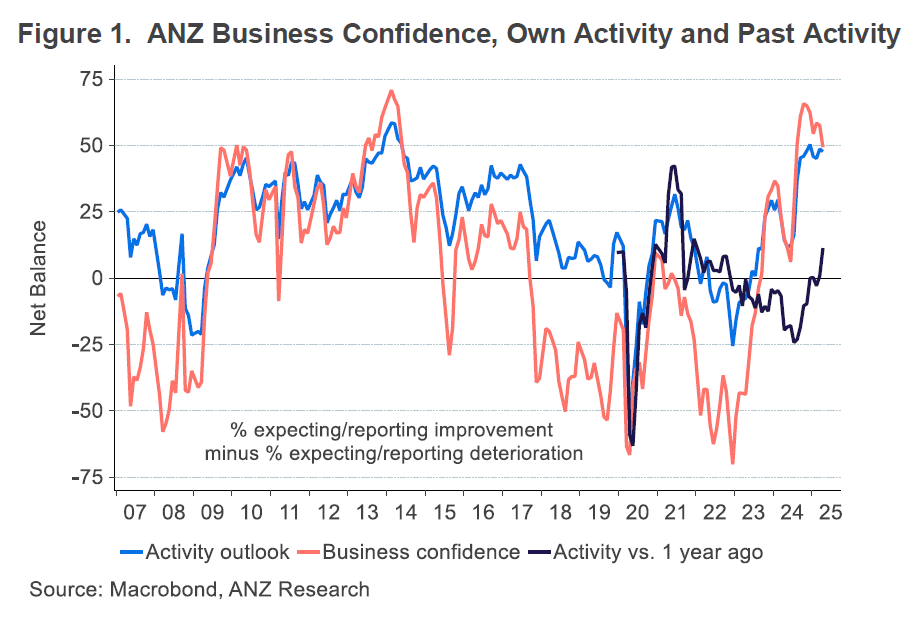

NZ ANZ business confidence falls to 49.3, inflation expectations steady

New Zealand's ANZ Business Confidence fell sharply in April, dropping from 57.5 to 49.3. The own activity outlook also edged lower from 48.6 to 47.7.

ANZ noted the decline may reflect growing apprehension over the global economic outlook, particularly uncertainty stemming from the escalating US-China trade war and broader policy unpredictability from the US administration.

Cost expectations three months ahead surged from 74.1 to 77.9, the highest level since September 2023. This contrasts with a slight dip in pricing intentions, which eased from 51.3 to 49.4. Inflation expectations one year out remained largely steady at 2.65%.

Japan’s industrial output slides -1.1% mom on auto weakness

Japan’s industrial production fell by -1.1% mom in March, significantly worse than the anticipated -0.7% mom decline.

According to the Ministry of Economy, Trade and Industry, the sharp drop was led by a -5.9% mom fall in motor vehicle output. Notably, regular passenger car production slipped -4.1% mom due to weaker export demand, while small vehicle output plunged -23.2% mom, reflecting disruptions in auto parts supply chains.

The slump in production comes against the backdrop of rising trade tensions, with US President Donald Trump imposing a 25% tariff on car and truck imports and a sweeping 24% tariff on all Japanese goods, later temporarily reduced to 10%.

Japanese manufacturers surveyed by METI project a recovery ahead, with output expected to rise 1.3% mom in April and 3.9% mom in May. But ministry officials remain cautious. “The environment surrounding production remains highly uncertain,” a METI representative warned, adding that manufacturers are clearly worried about the impact of US tariffs, though no changes to production plans have been formally announced yet.

Also released, retail sales rose 3.1% yoy in March, below expectations of 3.6%. Still, the result marks the 37th consecutive month of gains, indicating that domestic consumption has yet to show significant signs of stress.

First Impressions: NZ Business Confidence

Business confidence has largely held up since the US tariff announcement.

Key results, April 2025

- Business confidence: 49.3 (Prev: 57.5)

- Expectations for own trading activity: 47.7 (Prev: 48.6)

- Activity vs same month one year ago: 11.3 (Prev: 0.8)

- Inflation expectations: 2.65% (Prev: 2.63%)

- Pricing intentions: 49.3 (Prev: 51.2)

The ANZ April business opinion survey – the first one held since the US “Liberation Day” tariff announcement – was remarkably steady. Sentiment about general conditions was softer compared to March, but firm’s own-activity expectations were little changed, and remain at high levels.

ANZ did note that responses were weaker in the later part of the month, albeit based on a small sample. There was also some divergence in responses by sector, with confidence picking up in the more domestically-focused services sectors, while it fell in the more trade-exposed manufacturing and agricultural sectors.

A net 11% of firms said that conditions were better than a year ago, a strong lift from the March reading. This does at least point to some consistency in the responses, since it was in April last year when this measure fell sharply. Employment was also reported to be slightly higher compared to a year ago.

The pricing gauges of the survey were mixed. A net 78% of firms expect their own costs to increase, compared to 74% in March. This measure has been picking up since late last year, and likely reflects the fall in the New Zealand dollar over that time (though the currency actually rose strongly in the second half of April). However, firms’ own pricing intentions eased back slightly, and expectations of the inflation rate over the year ahead were little changed.

Overall, businesses seem to have taken a measured view so far of the impact of the US tariffs. That may change over time, once we see whether or not the hard data supports some of the more dire predictions about the impact on the global economy. As we noted in our initial assessment, the direct impact of the 10% on NZ exports is unwelcome but is likely to be manageable; the indirect impacts will be more significant but are harder to assess, and will depend in part on how policymakers in other countries respond.

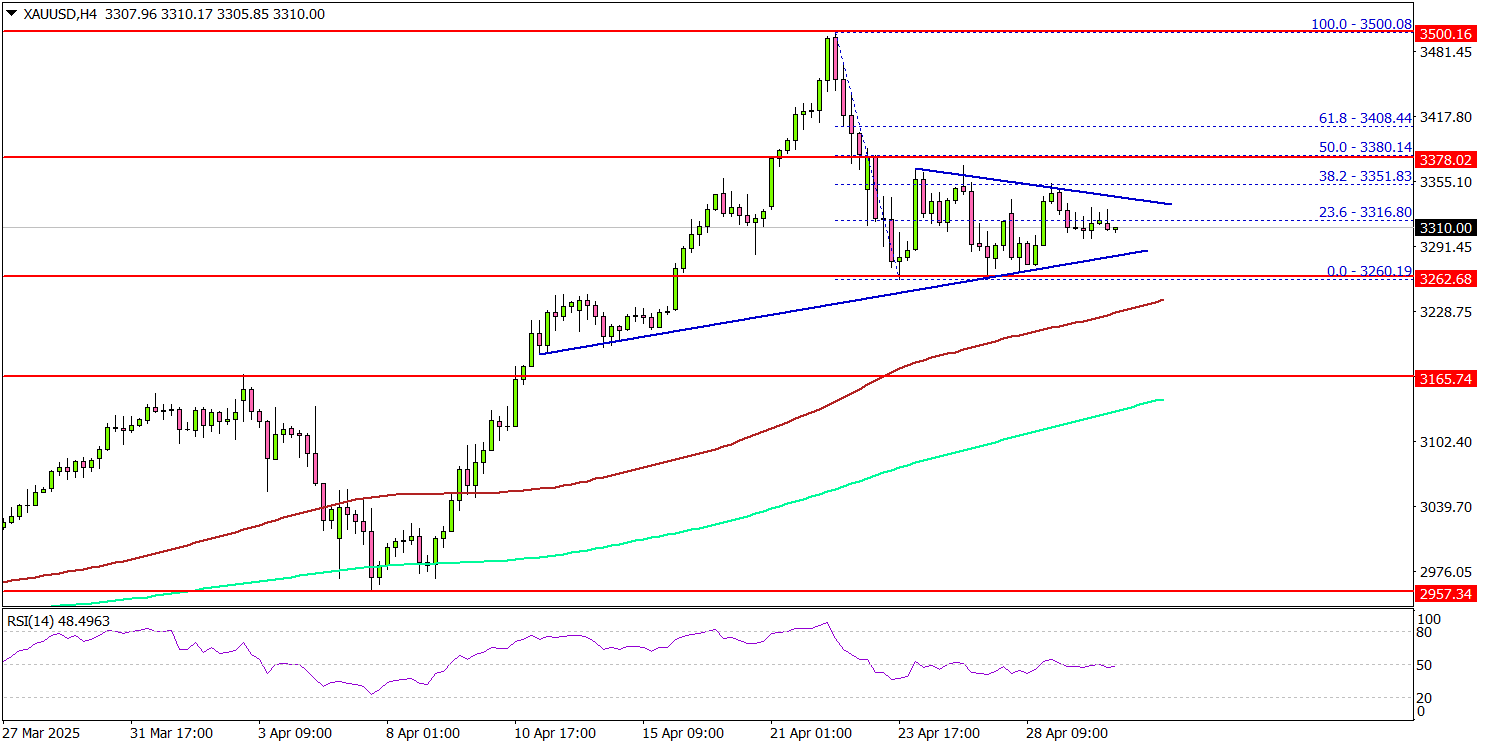

Gold Price Holds Range — But Weakness Could Resurface

Key Highlights

- Gold started a downside correction from the $3,500 resistance zone.

- A key contracting triangle is forming with resistance at $3,335 on the 4-hour chart.

- EUR/USD is consolidating gains below the 1.1420 resistance zone.

- WTI Crude Oil prices are again moving lower below the $62.00 resistance.

Gold Price Technical Analysis

Gold prices started a downside correction from the $3,500 resistance zone. The price declined below the $3,420 and $3,350 support levels.

The 4-hour chart of XAU/USD indicates that the price even declined below $3,300. A low was formed at $3,260 and the price is now consolidating losses. The price is still well above the 200 Simple Moving Average (green, 4 hours) and the 100 Simple Moving Average (red, 4 hours).

There is also a key contracting triangle forming with resistance at $3,335 on the same chart. On the upside, immediate resistance is near the $3,335 level.

The next major resistance sits near the $3,350 level. A clear move above the $3,350 resistance could open the doors for more upsides. The next major resistance could be $3,380, above which the price could rally toward the milestone level of $3,420.

On the downside, initial support is near the $3,285 level. The first key support is near $3,265. The next major support is near the $3,250 level. The main support is now $3,235. A downside break below the $3,235 support might call for more downsides. The next major support is near the $3,200 level.

Looking at EUR/USD, the pair started a short-term downside correction and might soon aim for a fresh increase if it clears the 1.1420 resistance.

Economic Releases to Watch Today

- US Gross Domestic Product for Q1 2025 (Preliminary) – Forecast 0.4% versus previous 2.4%.

- US Personal Income for March 2025 (MoM) - Forecast +0.4%, versus +0.8% previous.

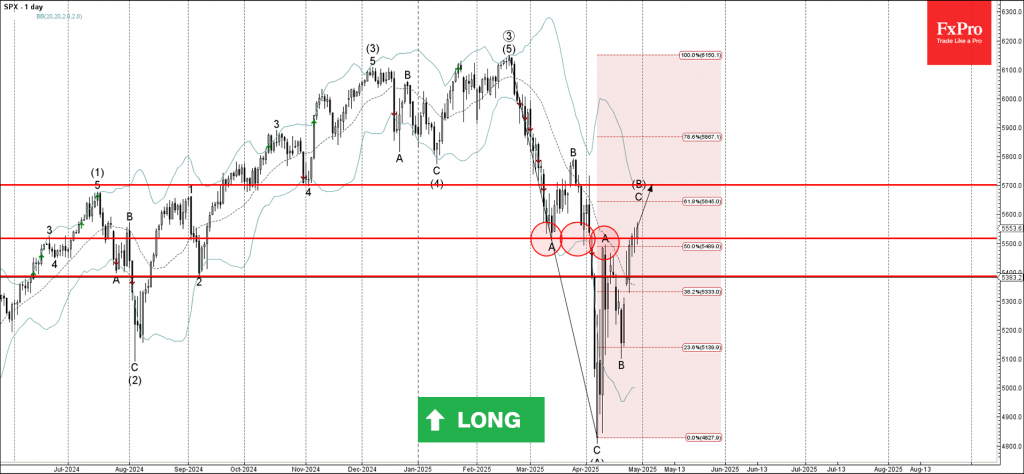

S&P 500 Index Wave Analysis

S&P 500 index: ⬆️ Buy

- S&P 500 index broke key resistance level 5500.00

- Likely to rise to resistance level 5700.00

S&P 500 index recently broke the key resistance level 5500.00 (former support from March, which also stopped A-wave of the active ABC correction B from the start of April).

The breakout of the resistance level 5500.00 coincided with the breakout of the 50% Fibonacci correction of the downward impulse from February.

S&P 500 index can be expected to rise toward the next resistance level 5700.00, target price for the completion of the active impulse wave C.

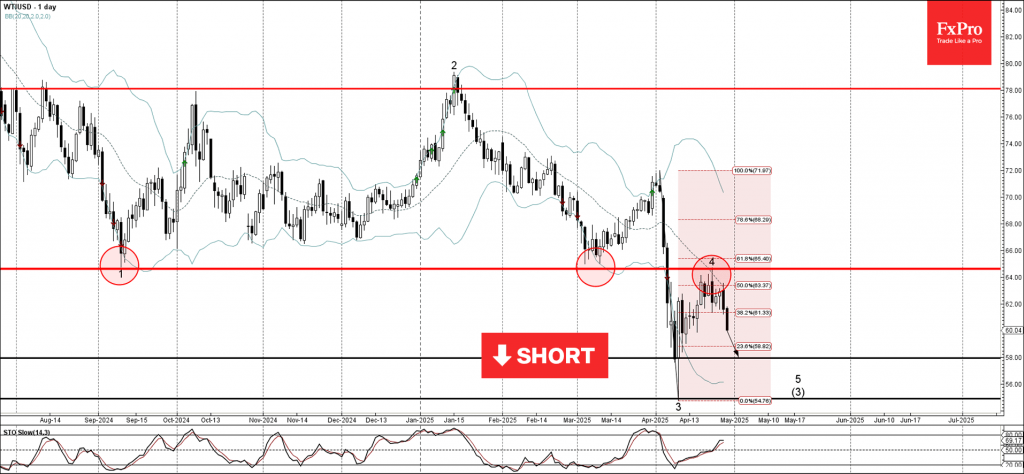

WTI Wave Analysis

WTI: ⬇️ Sell

- WTI reversed from the resistance area

- Likely to fall to support level 58.00

WTI crude oil recently reversed from the resistance area between the resistance level 64.60 (former multi-month low from September 2024), the 20-day moving average and the 61.8% Fibonacci correction of the downward impulse from the start of April.

The downward reversal from this resistance started the active short-term impulse wave 5, which belongs to the intermediate impulse sequence from last year.

Given the clear daily uptrend, WTI crude oil can be expected to fall toward the next support level 58.00.

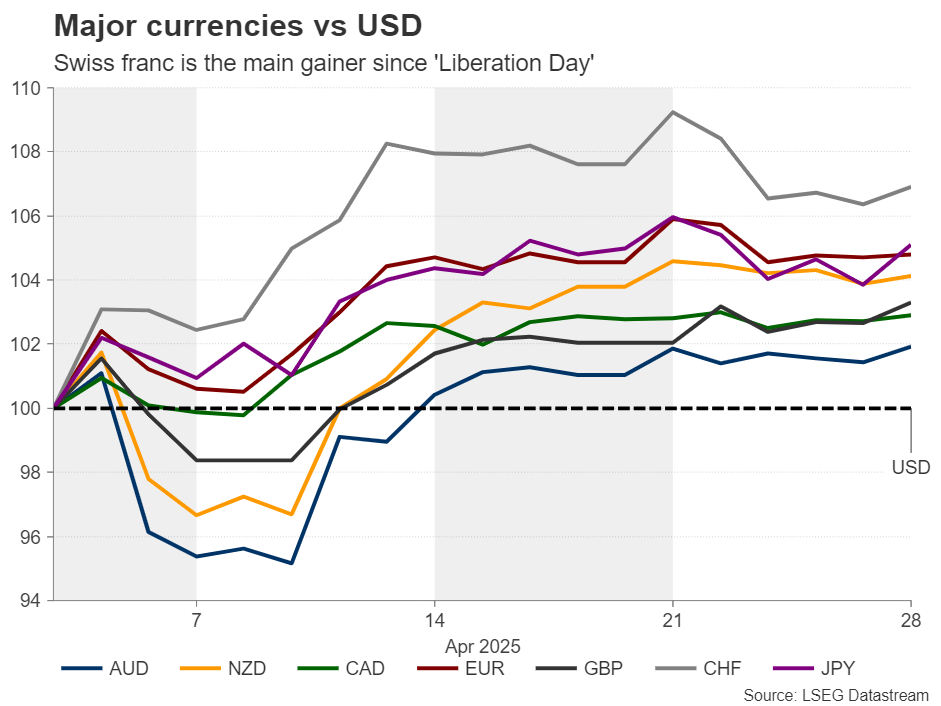

Strong Franc Sparks Bets on SNB Negative Rates

- Franc the main FX winner since “Liberation Day”.

- Could hit Swiss exports, lead the nation into deflation.

- How will the SNB respond: Negative rates or intervention?

- Risk reversals point to strong setback should appetite improve further.

Swiss franc the ultimate FX haven

The Swiss franc seems to be the ultimate safe haven in the FX arena amidst the market turbulence caused by US President Trump’s trade policy and the rhetoric surrounding it. Since the so-called “Liberation Day,” when Trump announced tariffs on all the US’s main trading partner, the franc has been the best performing major currency, with the other safe haven, the Japanese yen, taking second place. In third place, very close to the yen, stands the euro, which benefited from the selling of US assets amid recession fears by the recent fiscal shift in Germany.

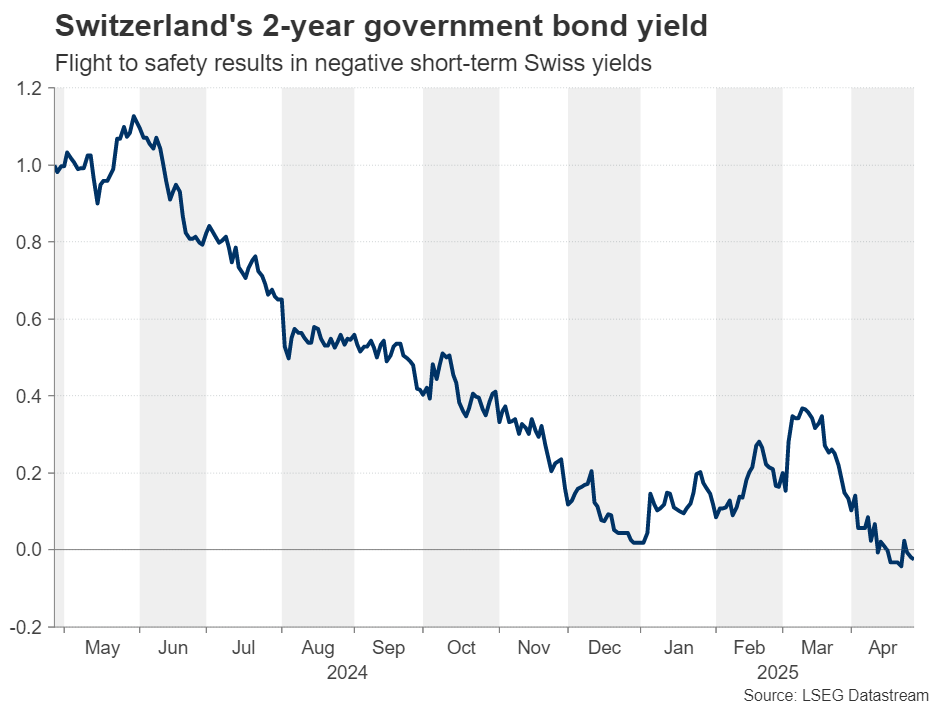

But why did the franc gain the most? Why didn’t the yen follow suit? Switzerland is considered a safe-haven destination for investors due to its strong banking and financial system, its political stability and neutrality, its trade surplus, its favourable tax laws and its strong legal system. Investors were so willing to divert their flows there that they allowed the Swiss 2-year government bond yield to drop into negative territory. This means that investors are willing to lose some money in nominal terms in exchange for the safety of their capital. The yen did not perform in a similar manner, perhaps as traders scaled back their BoJ rate hike bets amid the trade uncertainty.

Surge threatens exporters, increases deflation risk

Having said all that, the appreciation of the franc is a major threat to Swiss exporters as it raises the price of what Switzerland’s trading partners are paying for Swiss goods. Switzerland is a net exporting nation, and the biggest importer of its products is the European Union. Although the euro also appreciated, it did not shine as the franc, leading to a drop in euro/franc and an increase in the price of Swiss products in the rest of Europe.

And the timing couldn’t be worse as US tariffs are also threatening Swiss exporters. On April 2, the US imposed a 31% tariff rate on Swiss goods, before the broader 90-day delay was announced.

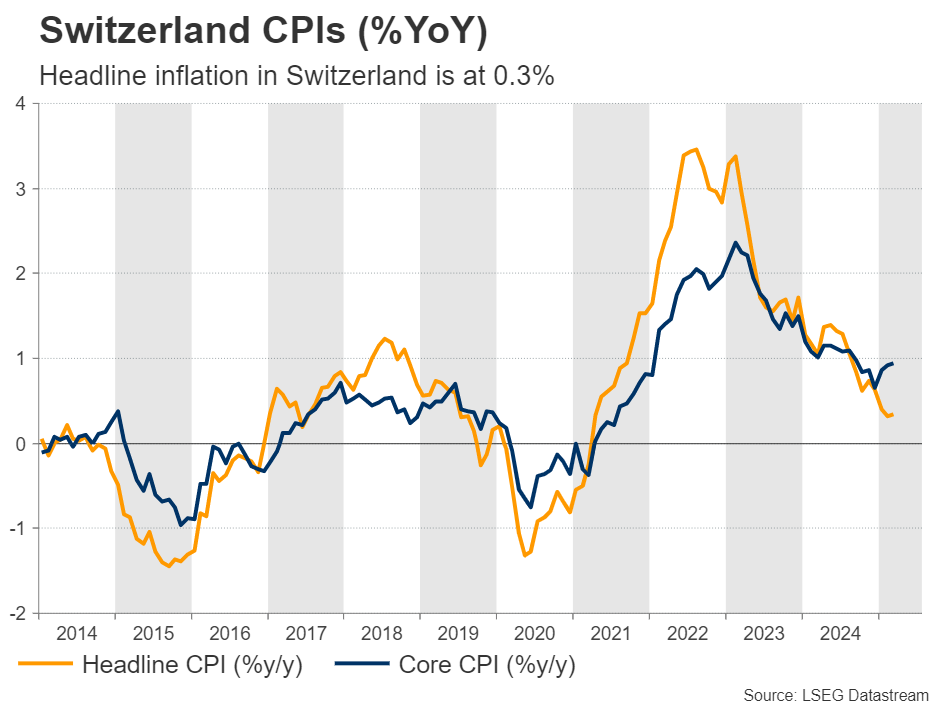

All this could weigh on Swiss inflation and it is very likely to result in deflation. After all, the year-over-year CPI rate in Switzerland is already very low, at 0.3%. And the big question on many market participants’ minds nowadays may be: How will the Swiss National Bank (SNB) respond to that?

Negative interest rates or Intervention

There are two channels through which the SNB had battled the appreciation of the franc. One is through cutting interest rates as most central banks around the globe are doing, and the other is through intervention, by buying its own currency and selling foreign reserves.

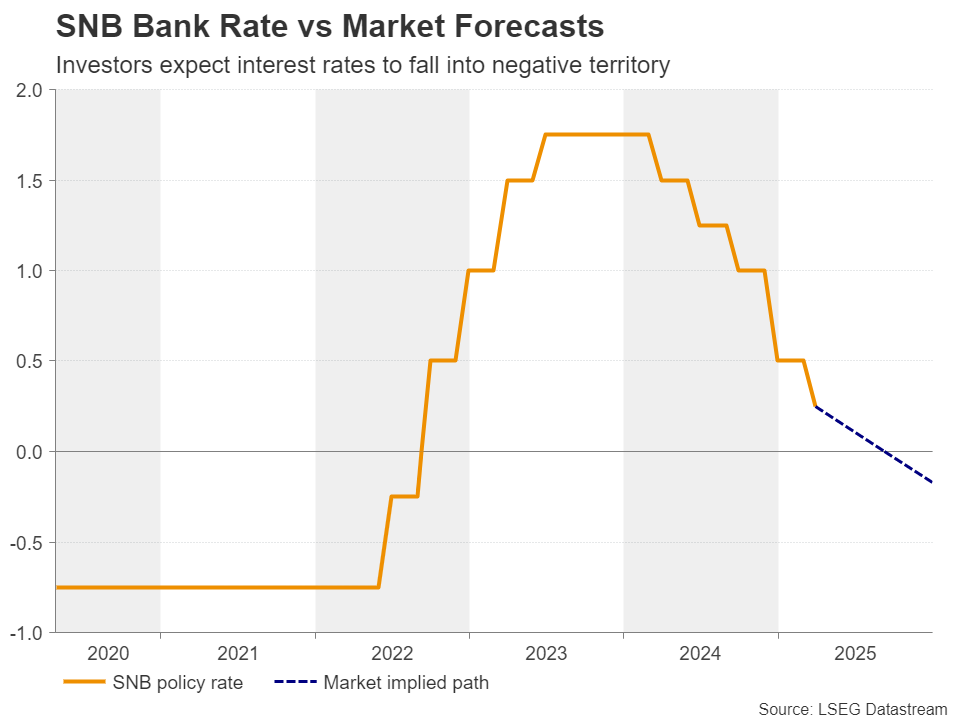

Getting the ball rolling with interest rates, the SNB has the lowest benchmark rate among major central banks, currently at 0.25%, and the franc’s appreciation may have raised speculation that policymakers could push interest rates into negative territory again. Indeed, according to Switzerland’s Overnight Index Swaps (OIS) market, there is an around 80% chance for a quarter-point cut to zero at the Bank’s next decision on June 19, with another 10bps worth of cuts expected by September.

SNB Chairman Martin Sclegel has not ruled out the likelihood of interest rates diving into negative territory but noted several times in the past that such a step would not be taken lightly.

This makes the option of intervention as the more likely one. Or not? According to a Bloomberg analyst-based survey, most participants predict that the Bank will avoid cutting interest rates below zero, with only Goldman Sachs holding such a forecast.

Nonetheless, intervention will not come without consequences. Such a policy risks stirring the US hornets’ nest, with Trump likely branding again Switzerland as currency manipulator as he did back in 2020. Although this could weaken Switzerland’s negotiating hand in potential trade talks, the President of the Swiss Confederation Karin Keller-Sutter said recently that she is not worried about that, which keeps intervention as a more likely option than negative interest rates.

The painless way

The painless way is for the Swiss franc to further weaken on its own. The SNB could still cut interest rates to zero, but officials could refrain from taking them into negative zone and also abstain from intervening. However, for that to happen, risk aversion may need to improve further, driven by new headlines about easing tariff tensions and the potential of trade negotiations.

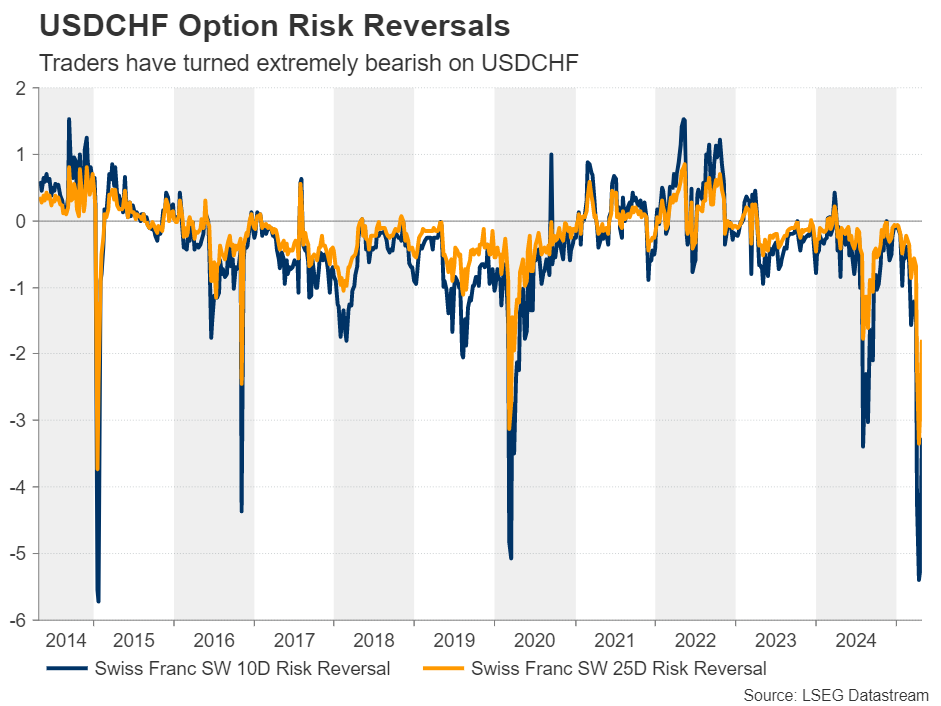

The Swiss franc could fall notably, leading to impressive rebounds in franc pairs. What supports this notion is the fact that, on April 11, the 10-day and 25-day risk reversals of dollar/franc options hit their lowest since January 2015, when the SNB abandoned the 1.20 floor in euro/franc. This points to extremely bearish conditions, which suggests that there may be very little room for the franc to appreciate further and a lot of downside potential in case the broader market environment brightens further.