Sample Category Title

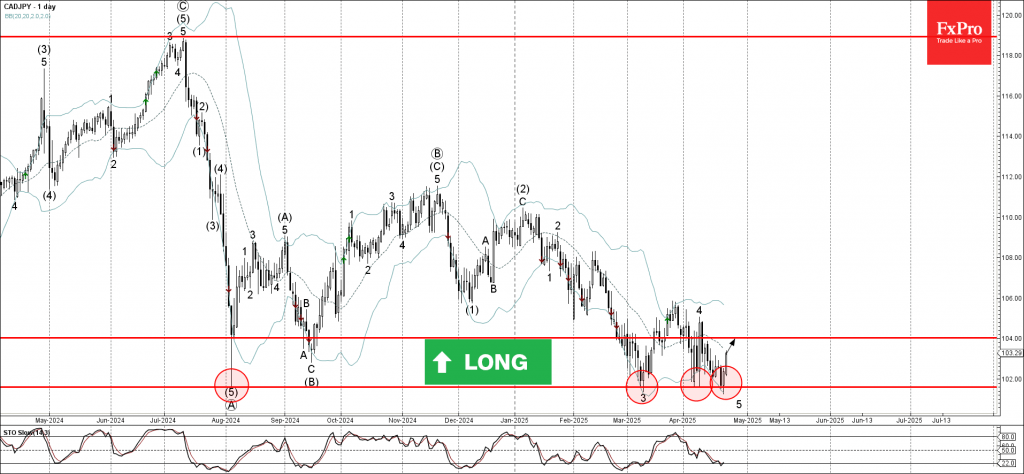

CADJPY Wave Analysis

CADJPY: ⬆️ Buy

- CADJPY reversed from strong support area

- Likely to rise to resistance level 104.00

CADJPY currency pair recently reversed from the strong support area between the long-term support level 101.60 (which stopped the sharp downtrend in August of 2024) and the lower daily Bollinger Band.

The upward reversal from this support area created the daily Japanese candlesticks reversal pattern Piercing Line.

Given the strength of the support level 101.60 and the bullish Canadian dollar sentiment seen today, CADJPY currency pair can be expected to rise toward the next resistance level 104.00.

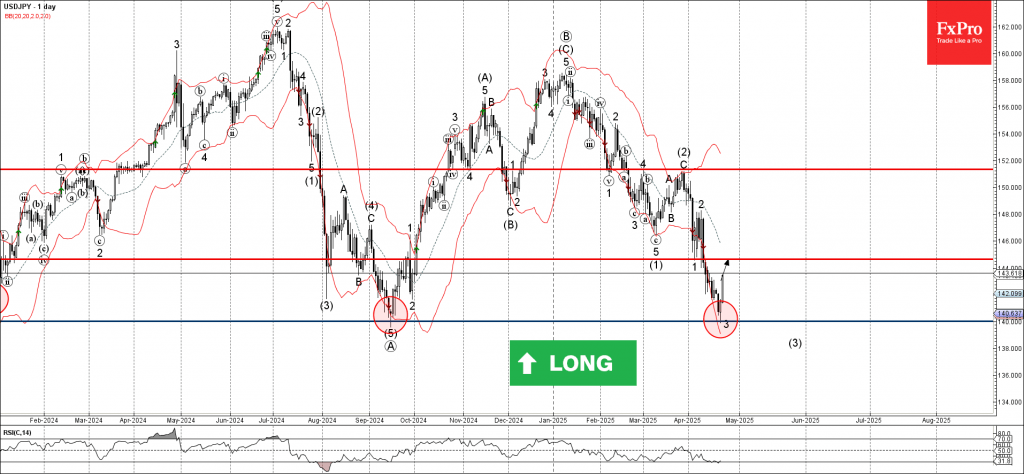

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

- USDJPY reversed from the support area

- Likely to rise to the resistance level 144.65

USDJPY currency pair recently reversed up from the support area between the long-term support level 140.00 (former multi-month low from September) and the lower daily Bollinger Band.

The upward reversal from this support area stopped the previous sharp downward impulse wave 3 of the higher impulse wave (3) from February.

Given the strength of the support level 140.00 and the strongly bearish yen sentiment seen today, USDJPY currency pair can be expected to rise toward the next resistance level 144.65 (former support from the start of April).

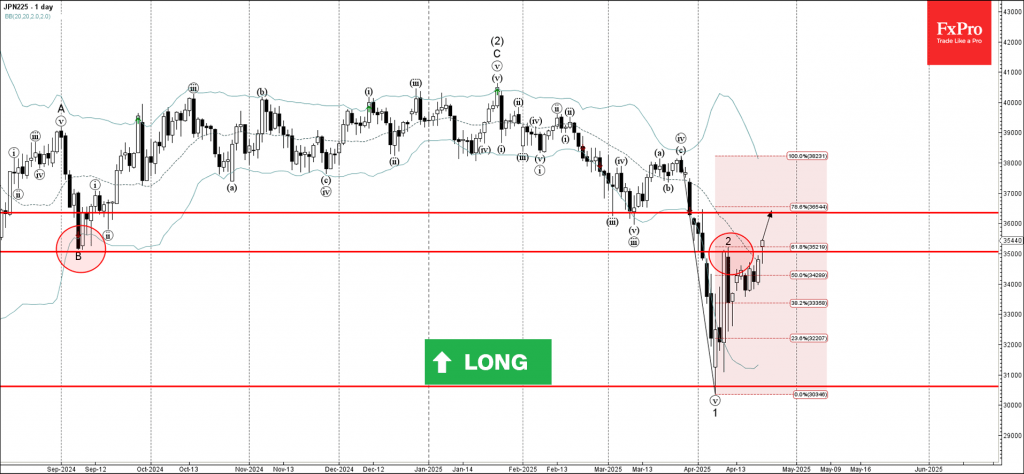

Nikkei 225 Wave Analysis

Nikkei 225: ⬆️ Buy

- Nikkei 225 broke the resistance area

- Likely to rise to resistance level 36355.00

Nikkei 225 index recently broke the resistance area between the pivotal resistance level 35000.00 (which stopped the previous correction 2, former strong support from September) and the 61.8% Fibonacci correction of the downward impulse from March.

The breakout of this resistance area would extend the earlier short-term ABC correction 2 from the start of April.

Nikkei 225 index can be expected to rise toward the next resistance level 36355.00 (former support which stopped the previous corrections iii and v last month).

Sunset Market Commentary

Markets

April EMU PMI surveys showed business activity broadly unchanged. The composite gauge dipped from 50.9 to 50.2 (vs 50.1 expecting), narrowly holding above the boom/bust level (50) for the fourth consecutive month. There were contrasting trends between marginally decreasing business activity in services (49.7 from 51) and the manufacturing sector holding up better than expected (48.8 from 48.7; 27-month high). Moreover, the manufacturing output index rose for a second month straight (51.2 from 50.5), recording a 35-month high. Despite the US introducing general tariffs of 10% and car tariffs of 25%, manufacturers increased production, slowed down job cuts and managed to boost their profit margins thanks to lower input prices and the ability to raise output prices faster. Lower energy prices and the announced increase in defense spending are currently a boon for the EMU’s manufacturing sector. On a national level, German manufacturers even saw a slight uptick in export orders, the first since early 2022. Apart from hopes of reaching some compromises with the US, Germany has a well-diversified export base (90% of exports go to countries other than the US). Overall cost inflation remains centered around services (wages) but input costs increased at the slowest pace since November last year. Selling prices were raised across both sectors. The most pessimistic part of the PMI survey was a sharp drop in business confidence, with sentiment down to the lowest since November 2022. In a separate release, the ECB’s wage tracker predicts wage growth to slow from >=4% in Q1 and Q2 (annualized) to 2.1% Q/Qa in Q3 (from 2.2% last month) and 1.6% Q/Qa in Q4 (up from 1.5%). EMU markets didn’t respond to today’s data releases.

US President Trump succumbed to market pressure a second time by saying it isn’t his intention to sack Fed chair Powell. Earlier this month, he immediately cut reciprocal tariffs to the 10% base rate for at least 90 days. Twice, the U-turn came after US assets went into tailspin. In the same vein, he suggested that high tariffs against China will come down substantially with Treasury Secretary Bessent also indicating that the current implicit trade embargo between the two nations isn’t the longed-for outcome. Markets start seeing a pattern here and responded positively. US stock markets are on track for back-to-back gains of 2.5%. European stock markets equally gain over 2%. US Treasuries rally with the curve bull flattening. US yields lose 2.2 bps (2-yr) to 13.8 bps. Interestingly, the German yield curve bear flattens with yields up 2.2 bps (30-yr) to 6.3 bps (2-yr). It affirms both German Bunds’ safe haven status and markets overly optimistic ECB rate cut bets. EUR/USD held rather steady around 1.14.

News & Views

EUREX, Europe’s largest bond futures (and derivatives in general) exchange, announced the introduction of EU bond futures for September 10. The launch was expected for last year but got postponed due to concerns over the sustainability and the long-term nature of the EU’s joint bond programme. The news will be welcomed by EU officials, who have been pushing for increased liquidity in EU bond trading via several ways, including through the creation of a repo facility. The bloc is also lobbying to have the bonds included in sovereign debt indices but the major index providers (ICE, MSCI) so far keep refusing. The launch reflects EUREX’s “strategic commitment to supporting European ambitions for greater autonomy at a time when the continent is relying on additional debt issuance”, the global head of products and markets said. The EU quickly became the fifth largest borrower in the wake of the pandemic’s Next Generation EU programme. Since then, momentum is building for joint EU borrowing to help finance the upcoming huge defense investments.

UK April private sector activity unexpectedly contracted for the first time in 1,5 years with the composite PMI dropping from 51.5 to 48.2. Optimism for the year ahead outlook slumped to its lowest since October 2022. The decline was led by the services sector, falling to 48.9 from 52.5 on rising global economic & tariff uncertainty and subdued domestic demand. Manufacturing production volumes dropped at the steepest rate since August 2022 due to weakening market conditions, particularly in key export destinations. This resulted in a solid reduction in new work inflows for a fifth month running. Both sectors kept cutting back employment due to decreased workloads and rising payroll costs. The latter is still a consequence of the Labour government’s tax increases and jolted input cost inflation to the fastest pace since February 2023. Output charge inflation picked up to the highest for nearly two years. The stagflationary narrative once again highlights the tough trade-off the Bank of England faces. The pound sterling erased earlier gains against the euro to trade nearly unchanged around EUR/GBP 0.857.

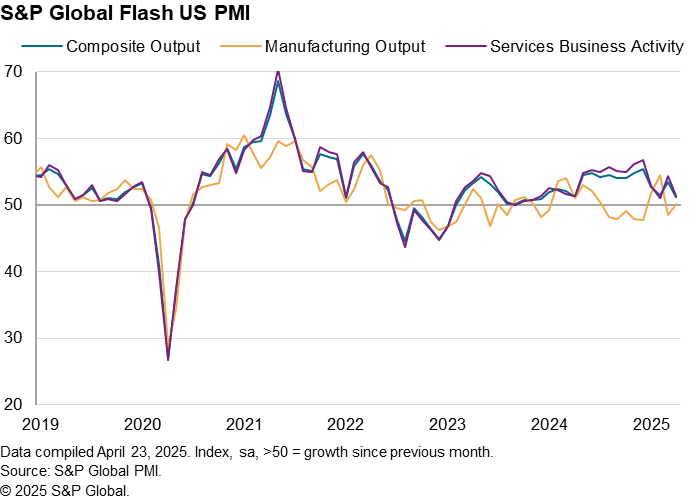

US PMI composite falls to 16-month low, activity cools and price pressures intensify

The US economy showed clear signs of slowing in April, with S&P Global flash composite PMI falling from 53.5 to 51.2, its lowest level in 16 months. While manufacturing activity edged up slightly from 50.2 to 50.7, the services sector lost significant momentum, dropping from 54.4 to 51.4.

According to S&P Global’s Chris Williamson, the early data signals a “marked slowing of business activity growth” at the start of Q2, with output rising at its weakest pace since December 2023. This implies a modest annualized GDP growth rate of around just 1.0%.

At the same time, inflationary pressures are re-emerging. Companies reported a sharp uptick in input costs, led by tariff-related price increases and persistent wage pressures.

In manufacturing, price increases reached their fastest pace in nearly two-and-a-half years. Services firms also raised their selling prices at the highest rate in over a year.

US Stocks React to Trump’s Comments and Earnings, PMI Ahead

Markets have had a rollercoaster 24 hours as President Trump has once again proved to be the market driver.

Wall Street looked ready to extend its best gains in two weeks, with S&P 500 futures rising 2.5%. This came after President Trump reassured markets he wouldn't fire Federal Reserve Chair Jerome Powell. Hopes for easing US-China trade tensions also boosted investor confidence.

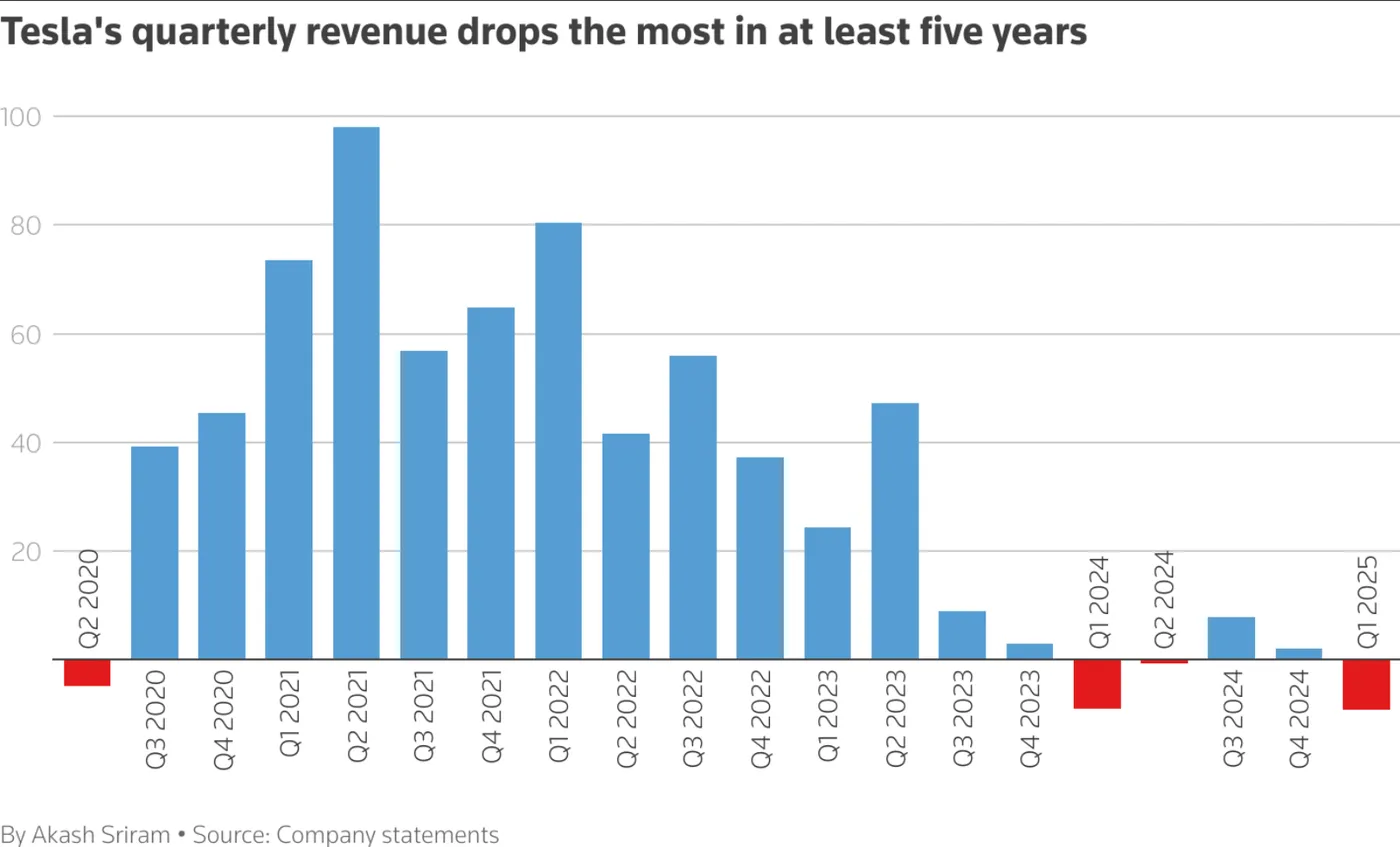

Market sentiment improved thanks to positive earnings reports. Tesla shares rose 7% in premarket trading, even though the company fell short of forecasts. The rise came about when Elon Musk announced he would step back from his government work to focus on the company.

Tesla posted a 16.3% total gross margin, beating analysts'predictions of 15.8%. A big decline from the 17.4% a year earlier.

Still the revenue slumped 20% to $13.97 billion for the quarter.

Source LSEG

Treasuries gained as concerns over Powell’s job eased, with 10-year yields falling to 4.30%. The dollar stabilized after a recent rally. Bitcoin surged past $90,000 for the first time since early March. Gold dropped as safe-haven demand weakened, while oil continued to recover.

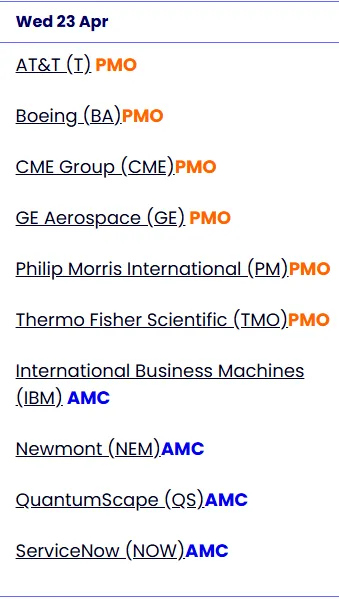

Other earnings releases that have come out include Boeing, who reported a smaller loss for the first quarter, thanks to more production and deliveries after a strike and quality issues halted most aircraft manufacturing in late 2024.

The company plans to increase production of its popular 737 MAX jets to 38 per month by 2025, following last year’s setbacks from worker strikes and other crises.

AT&T shares are up in pre-market trading after gaining more new wireless subscribers than analysts had predicted in the first quarter.

On the earnings front, there are still earnings after market close today which include International Business Machines (IBM), Newmount, QuantumScape and ServiceNow.

Source: Interactiveinvestor

The general improvement in risk sentiment still faces some challenges.Until there are some tariff deals announced officially or official word on US-China relations, the move may eventually run out of steam.

For a full review of Euro PMI data released this morning, please read Euro under pressure as Services PMIs slip

Economic data releases

For now focus will shift to earnings but may still be overshadowed by tariff developments. US PMI may also give us a glimpse if there has been any effects yet from the proposed US tariffs on the data. It might still be too early to tell but comments from manufacturers may shed some light as well.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - Nasdaq 100

From a technical standpoint, the Nasdaq 100 is threatening a change of structure as it looks to print a fresh higher high.

A daily candle close above the 19123 handle should see the requirements being met and should increase the probability of further gains.

Of course in the current climate, sentiment can shift quickly but for now the bias does appear to favor the bulls.

Immediate resistance resistance rests at 19123 and 19436 before the 19781 and 20000 psychological level come into focus.

A change in sentiment could knock the rally back which would bring support at 18361, 17800 and 17304 back into focus.

Nasdaq 100 Daily Chart, April 23, 2025

Source: TradingView.com (click to enlarge)

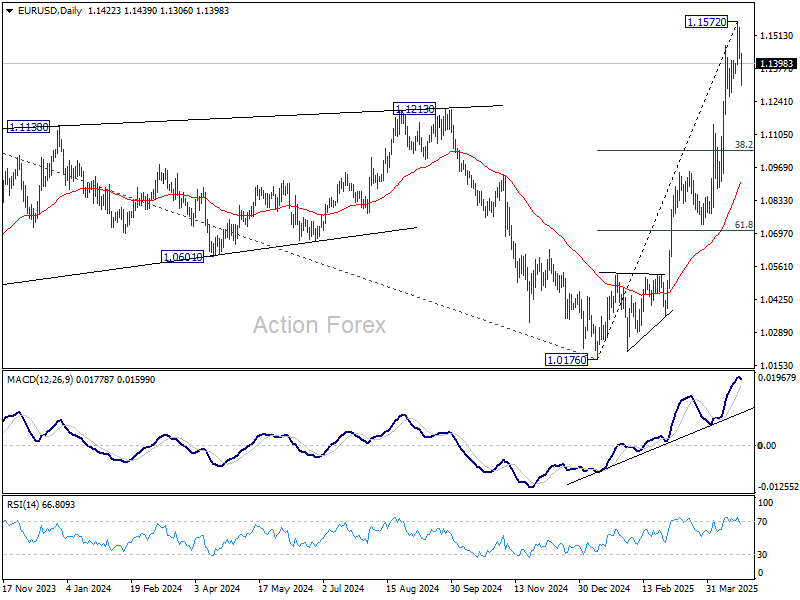

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1377; (P) 1.1462; (R1) 1.1507; More...

Intraday bias in EUR/USD remains mildly on the downside. Pull back from 1.1572 short term topping could extend lower. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

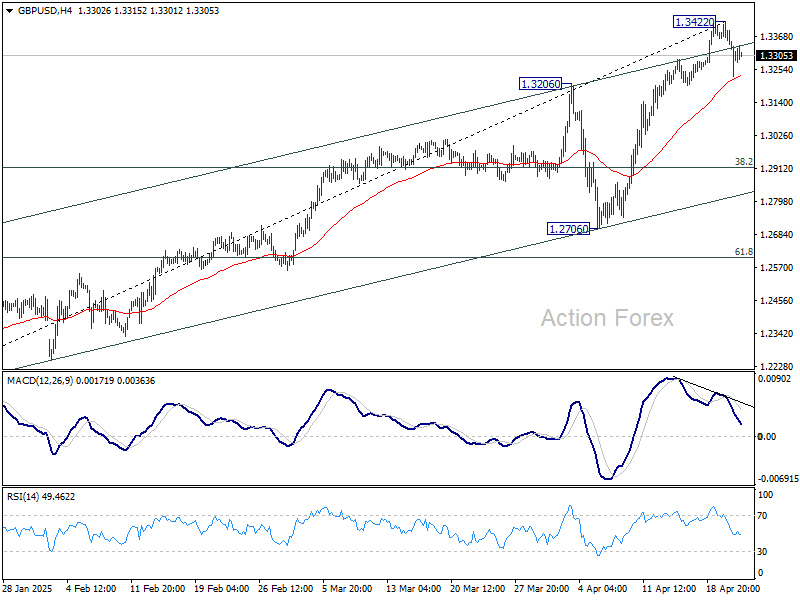

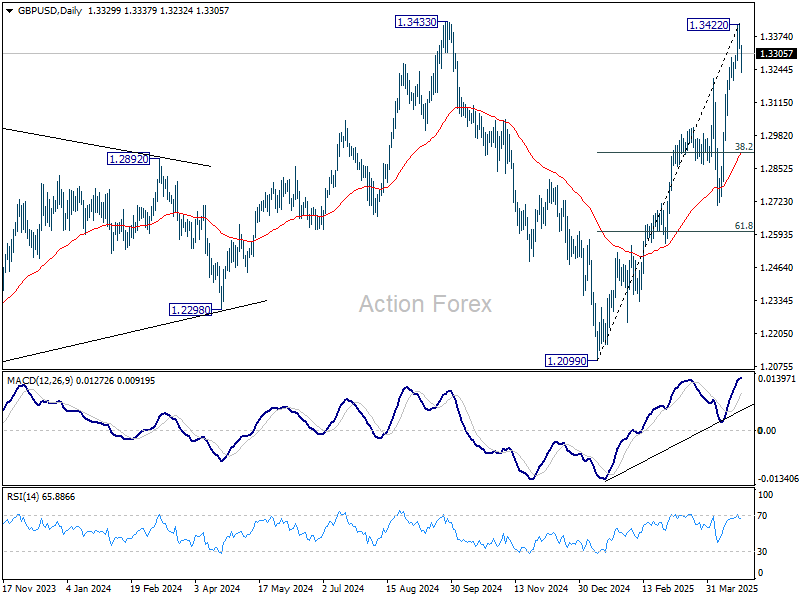

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3298; (P) 1.3360; (R1) 1.3395; More...

Intraday bias in GBP/UD remains mildly on the downside, as pullback from 1.3422 short term top would continue lower. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

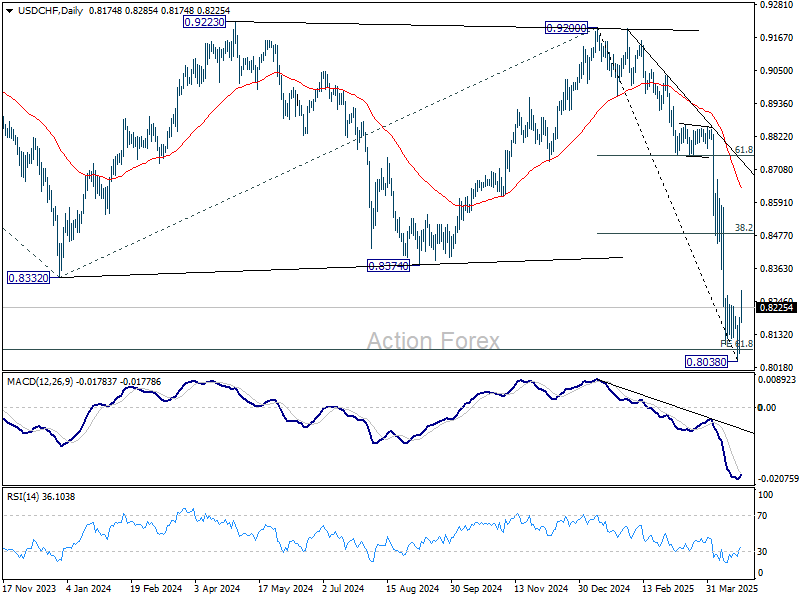

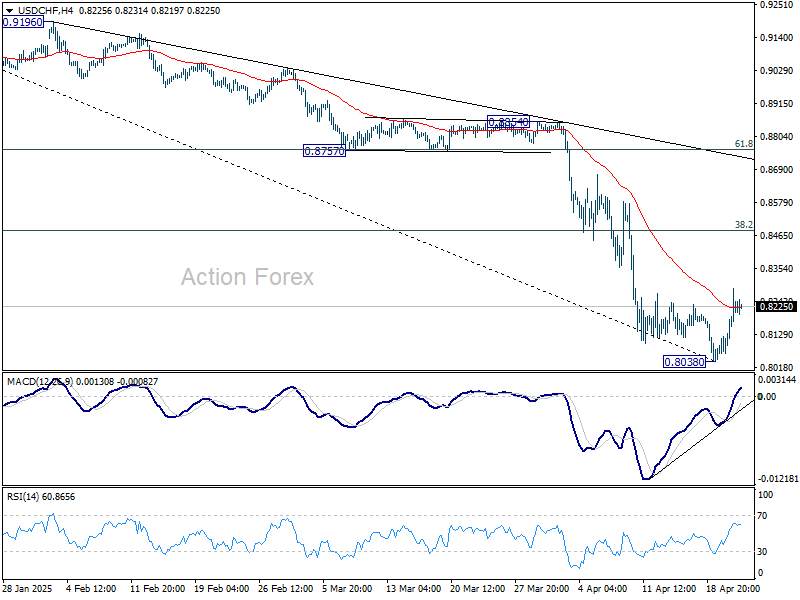

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8106; (P) 0.8149; (R1) 0.8233; More…

Intraday bias in USDCHF is mildly on the upside at this point. Rebound from 0.8038 short term bottom could extend to 38.2% retracement of 0.9200 to 0.8038 at 0.8482. But strong resistance should be seen there to limit upside. On the downside, break of 0.8038 will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.