Sample Category Title

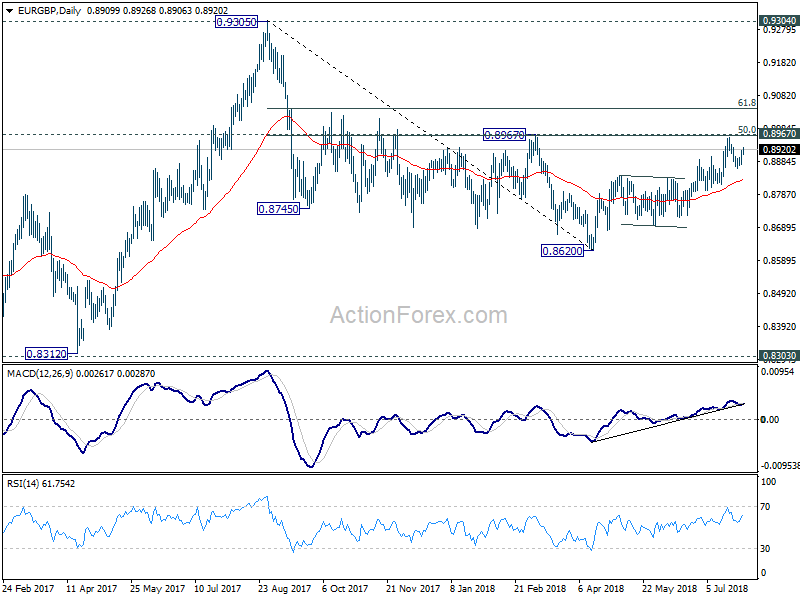

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8889; (P) 0.8905; (R1) 0.8929; More...

EUR/GBP recovers strongly after hitting 0.8864. But upside is limited well below 0.8957 so far. Intraday bias stays neutral first. Overall, while correction from 0.8957 may extend, as long as 0.8815 support holds, larger rally is expected to continue. On the upside, decisive break of 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) should confirm completion of whole decline from 0.9305. EUR/GBP should then target 61.8% retracement at 0.9043 next.

In the bigger picture, EUR/GBP is staying in long term range pattern from 0.9304 (2016 high). The corrective structure of the fall from 0.9305 to 0.8620 is raising the chance that rise from 0.8312 to 0.9305 is an impulsive move. But we're not too confident on it yet. In any case, we'd stay cautious on strong resistance from 0.9304/5 to limit upside in case of further rally. Meanwhile, if there is another medium term decline, strong support will likely be seen from 0.8303 to contain downside.

Gold Spot Bullish Bias Above 1219.00

Pivot (invalidation): 1219.00

Our preference Long positions above 1219.00 with targets at 1225.00 & 1227.50 in extension.

Alternative scenario Below 1219.00 look for further downside with 1217.25 & 1215.50 as targets.

Comment The RSI is above its neutrality area at 50%.

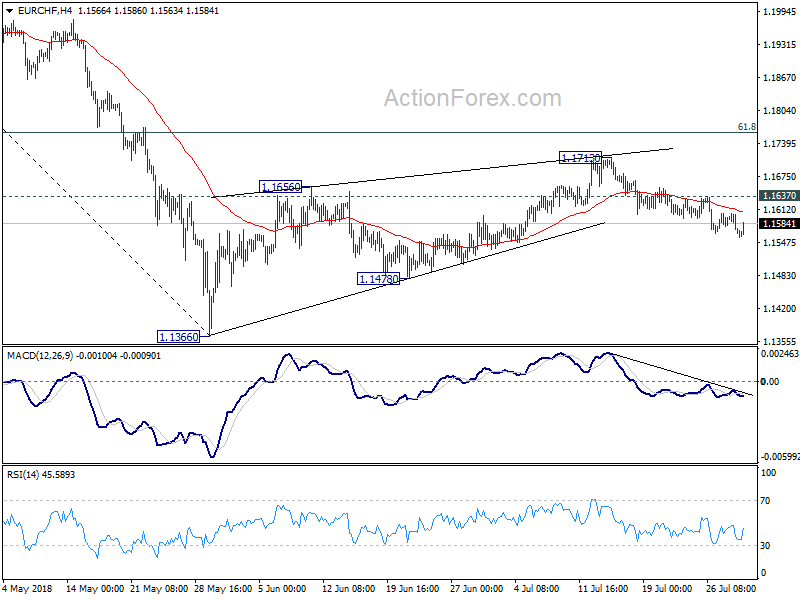

EUR/CHF Under Pressure

Pivot (invalidation): 1.1585

Our preference Short positions below 1.1585 with targets at 1.1550 & 1.1535 in extension.

Alternative scenario Above 1.1585 look for further upside with 1.1605 & 1.1620 as targets.

Comment The break below 1.1585 is a negative signal that has opened a path to 1.1550.

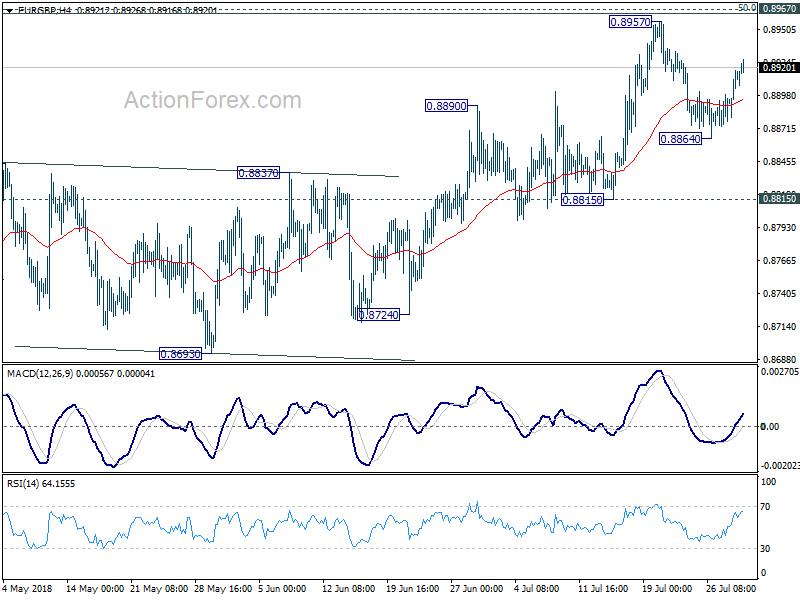

EUR/GBP Further Upside

Pivot (invalidation): 0.8905

Our preference Long positions above 0.8905 with targets at 0.8935 & 0.8945 in extension.

Alternative scenario Below 0.8905 look for further downside with 0.8895 & 0.8880 as targets.

Comment The RSI advocates for further upside.

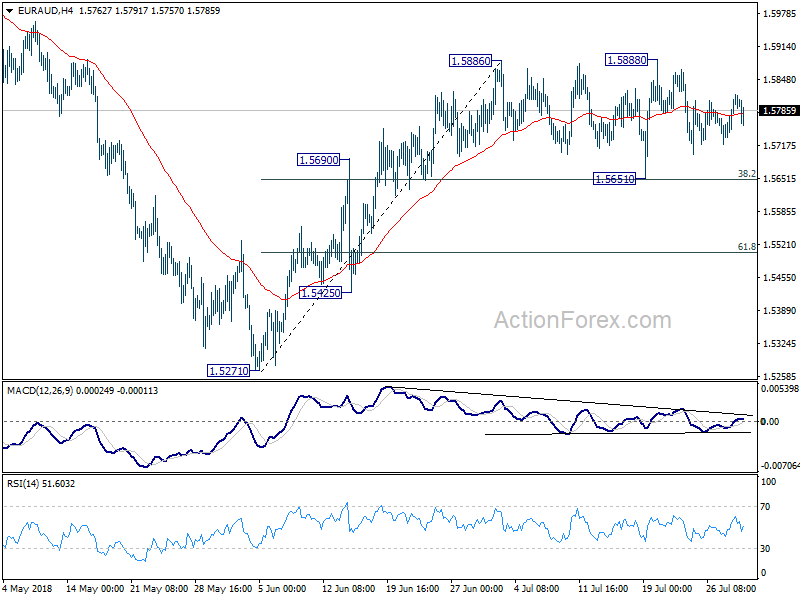

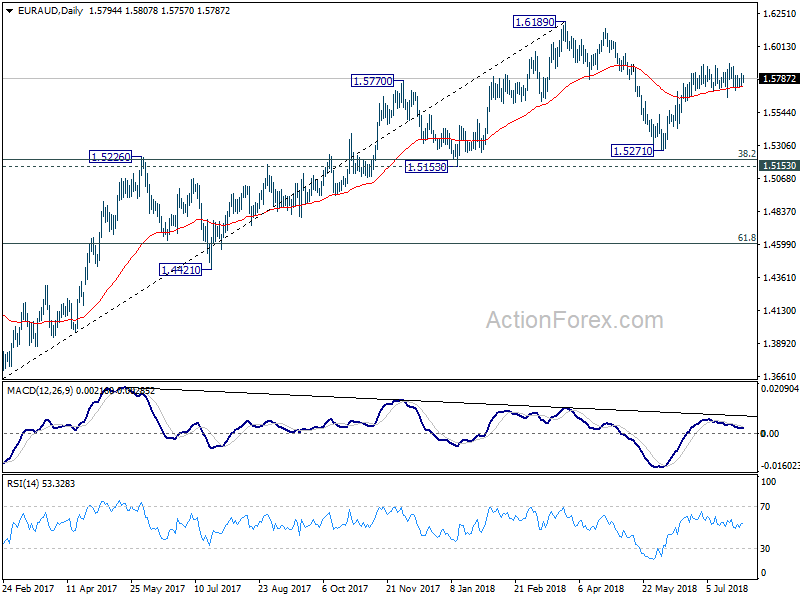

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5752; (P) 1.5787; (R1) 1.5834; More....

EUR/AUD is still bounded in the sideway consolidation pattern from 1.5886 and intraday bias stays neutral. With 1.5651 minor support intact, further rise is expected in the cross. On the upside, break of 1.5888 resistance will extend rise from 1.5271 towards 1.6139/89 resistance zone. However, break of 1.5651 cluster support (38.2% retracement of 1.5271 to 1.5886 at 1.5651) will indicate near term reversal and turn bias back to the downside for 1.5271 low.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5271 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

Bitcoin/Dollar Watch 8035

Pivot (invalidation): 8250

Our preference Short positions below 8250 with targets at 8035 & 7945 in extension.

Alternative scenario Above 8250 look for further upside with 8360 & 8495 as targets.

Comment The RSI lacks upward momentum.

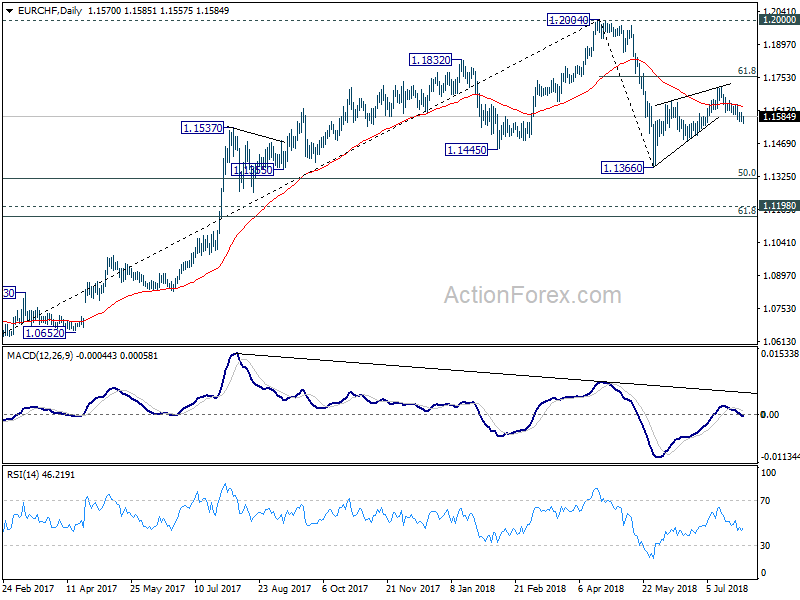

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1552; (P) 1.1581; (R1) 1.1597; More...

Despite diminishing downside momentum, intraday bias in EUR/CHF stays on the downside for further 1.1478 support. As noted before, the corrective rebound from 1.1366 should have completed with three waves up to 1.1713 already. Break of 1.1478 will confirm our bearish view and target 1.1366 low and below. Nonetheless, on the upside, above 1.1637 minor resistance will turn bias back to the upside and could extend the rise from 1.1366. But even in that case, we'd expect strong resistance from 61.8% retracement of 1.2004 to 1.1366 at 1.1760 to bring near term reversal.

In the bigger picture, 1.2004 is seen as a medium term top with bearish divergence condition in daily and weekly MACD. 1.2000 is also an important resistance level. Hence, the corrective pattern from 1.2004 is expected to extend for a while before completion. We're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Bank Of Japan Unwilling To Shift Gears Yet

After weeks of speculation that the Bank of Japan may begin to adjust its stimulus program, the central bank once again decided not to join the global trend towards tighter policies.

The BoJ left its overnight interest rates unchanged at -0.1% and reiterated that it would resume buying Japanese Government Bonds to keep the 10-year yields around 0%. The bank may allow for more flexible movement on the 10-year bonds, howeverthis isn't considered a significant shift in policy. The BoJ also made tweaks toits ETF purchases, as it increased the composition of TOPIX-linked ETFs while shifting slightly away from the Nikkei 225 Indexbut maintained its annual pace of ETF buying.

It seems the Bank of Japan will be the last major central bank to pull the trigger on tightening policy as the Japanese economy continues to struggle with stubbornly low inflation levels. This should allow further widening in spreads between Japan's bonds and other global bonds towards year-end, suggesting that the Yen is likely to remain under pressure for the near future.

The Federal Reserve is next in line to announce policy on Wednesday. That's why today's Core Personal Expenditure figures carry significant importance. If Core PCE came in at 2% or above, it wouldreinforce expectations for two more rates hikes in 2018. Many traders want to know whether President Donald Trump's criticism of the Fed will lead to a change in language; I believe there will be no change in guidance and the Fed will continue sending the message that more rate hikes are on the way.

We also have inflation and Q2 GDP numbers from the Eurozone. Consumer Price Indexfigures are expected to rise 2.0% y-o-y in July, remaining unchanged from June. Meanwhile, GDP growth is expected to see a 0.3% fall from a year ago, towards 2.2%.

In equity markets, the tech sector continued to weigh on sentiment. Shares of Facebook, Twitter and Netflix plunged further on Monday, as investors started to become more worried about their business models after they announced their latest earnings results. Amazon and Alphabet were also dumped.Meanwhile,all eyes will shift to Apple earnings today in the hopes of providing some support for FAANG stocks.

BOJ Adjusts To Allow More Flexible Policy

General Trend:

- Asian equity markets trade mixed as traders digest the BoJ decision

- Samsung Electronics expects H2 results to be driven by memory and flexible OLEDs

- BoJ announced forward guidance, left yield curve control target unchanged; to raise purchases of ETFS which track the TOPIX (as speculated)

- Japan JGB yields move lower in the aftermath of the BoJ rate decision: 40-year yield down over 8bps, near 0.88%

- Japan jobless rate rises for the first time since Feb, job-to-applicant ratio hits highest level since 1974

- Japan prelim June industrial production misses ests

- China July official PMIs decline amid ‘trade war’

- China central bank skipped open market operation for the 8th straight session

- PBOC fixed the yuan slightly weaker

- New Zealand July ANZ business confidence hits the lowest level since 2008

- Rio Tinto expected to report H1 results on Wed

- Apple is due to report Q3 results on Tuesday after the US close

- Japanese companies which may report earnings include Honda, Sony, Nintendo, Panasonic, Renesas, Resona, Yamato Holdings, ANA Holdings, Japan Airlines, Kyocera, Takeda, JFE Holdings and Start Today

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.3%

- (JP) BOJ TWEAKS POLICY TO ENHANCE FLEXIBILITY; adjusts ETF allocation (as speculated); Cuts amount to which negative rate applies, starts forward guidance

- (JP) JAPAN JUN JOBLESS RATE: 2.4% V 2.3%E; Job-To-Applicant Ratio: 1.62 v 1.60e (highest level since January 1974)

- (JP) JAPAN JUN PRELIM INDUSTRIAL PRODUCTION M/M: -2.1% V -0.3%E; Y/Y: -1.2% V 0.6%E

- (JP) Japan 10-year JGB yield trades above 0.105% before BOJ

- (JP) JAPAN JUN ANNUALIZED HOUSING STARTS: 915K V 960KE; Y/Y: -7.1% V -2.5%

Korea

- Kospi opened -0.1%

- (KR) Analysts note that downturn in South Korea economic indicators point to GDP being weaker in H2, which may make it hard to meet 2018 target of 2.9% - Korean press

- (KR) South Korea Aug Business Survey: Manufacturing: 74 v 81 prior (17-month low); Non-manufacturing: 76 v 81 prior

- (KR) South Korea Jun Industrial Production m/m: -0.6% v -0.9%e; y/y: -0.4% v 0.7%e

- (KR) North Korea said to have built new missiles after summit with Trump – press

- (KR) South Korea Jun Construction Output y/y: -7.7% v 0.0% prior

- Samsung Electronics, 005930.KR Reports final Q2 (KRW) Net 11.0T v 11.1Te, Op 14.9T v 14.8T prelim, Rev 58.5T v 58.0T prelim

- 005930.KR Exec: Chip unit still focused on mid and long term profitability; FY19 will see memory chi[ market to remain stable, with strong server demand - conf call comments

China/Hong Kong

- Hang Seng opened -0.2%, Shanghai Composite -0.1%

- (CN) Yuan may fluctuate at low level in short term - China Securities Journal

- (CN) CHINA JUL OFFICIAL GOVT MANUFACTURING PMI: 51.2 V 51.3E; NON-MANUFACTURING PMI: 54.0 V 54.9E (weakest reading since Aug 2017); COMPOSITE PMI 53.6 V 54.4 PRIOR

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 8th consecutive session; Net drains CNY30B v drains CNY130B prior

- (CN) China PBoC sets yuan reference rate at 6.8165 v 6.8131 prior

- (BR) Brazil Pres Temer: talked with China Pres Xi about barriers to sugar and poultry trade

- (CN) China to raise penalties on illegal online finance - Chinese Press

- (CN) China authorities are said to be slowing down rollout of China Depository Receipts (CDR) plan as companies are being slow to apply - financial press

- (CN) Moody's: Trade restrictions will contribute to slowdown in China growth, cutting real GDP growth by around 0.3-0.5 pct points in 2019; US/China trade dispute likely to escalate further in 2018 and impact global growth

Australia/New Zealand

- ASX 200 opened +0.1%

- FCG.NZ Reports Jul collections: New Zealand 13.3M v 11.8M y/y; Australia 9.9M v 8.7M y/y

- (AU) AUSTRALIA JUN BUILDING APPROVALS M/M: 6.4% V 1.0%E; Y/Y: +1.6% V -6.0%E

- (AU) Australia Foreign Min Bishop: Australia, Japan and US form partnership for infrastructure investment

- (NZ) New Zealand Jun Building Permits m/m: -7.6% v +7.1% prior

- (NZ) New Zealand Jul ANZ Activity Outlook: 3.8 v 9.4 prior; Business Confidence: -44.9 v -39.0 prior

- (AU) Australia Jun HIA New Homes Sales m/m: +2.2% v -4.4% prior

Other Asia

- (PH) Philippines Economic Chief Pernia: Risks to GDP include interest rates and disruptive capital flows

North America

- US equity markets ended lower: Dow -0.6%, S&P500 -0.6%, Nasdaq -1.4%, Russell 2000 -0.6%

- S&P500 Technology -1.6%

- TSLA Panasonic confirms to raise production capacity at gigafactory - Japanese Press

- LOGI Reports Q1 $0.34 v $0.24 y/y, Rev $608M v $530M y/y; To acquire California based Blue Microphones for ~$117M in cash

- (US) Trump Attorney Giuliani: Trump interview with Special Investigator Mueller is 'highly unlikely', been driven further from taking questions from Mueller

- (CA) Canada said to be rejected by US from the NAFA talks - National Post; C$ falls 0.25% against USD

Europe

- (UK) Jul GfK Consumer Confidence: -10 v -9e

- (IE) Ireland Central Bank: Trims 2018 GDP growth forecast from 4.8% to 4.7%; affirms 2019 GDP growth forecast at 4.2%

- IGY.DE E.ON said to consider merger with the company - German Press

Levels as of 01:30ET

- Hang Seng -0.6%; Shanghai Composite -0.2%; Kospi -0.1%; Nikkei225 -0.0%; ASX 200 +0.1%

- Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.1%; FTSE100 +0.0%

- EUR 1.1700-1.1719; JPY 110.77-111.43; AUD 0.7404-0.7434;NZD 0.6813-0.6833

- Aug Gold -0.1% at $1,220/oz; Sept Crude Oil -0.5% at $69.81/brl; Sept Copper +0.4% at $2.80/lb

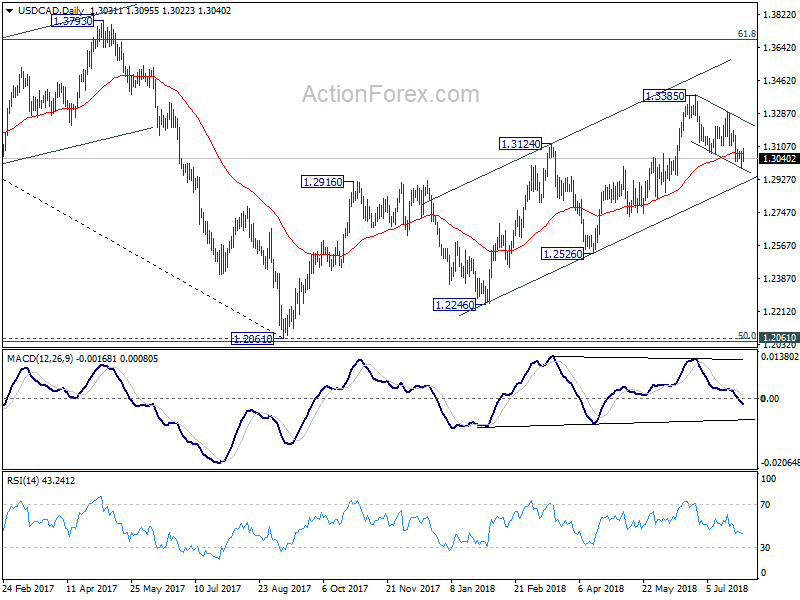

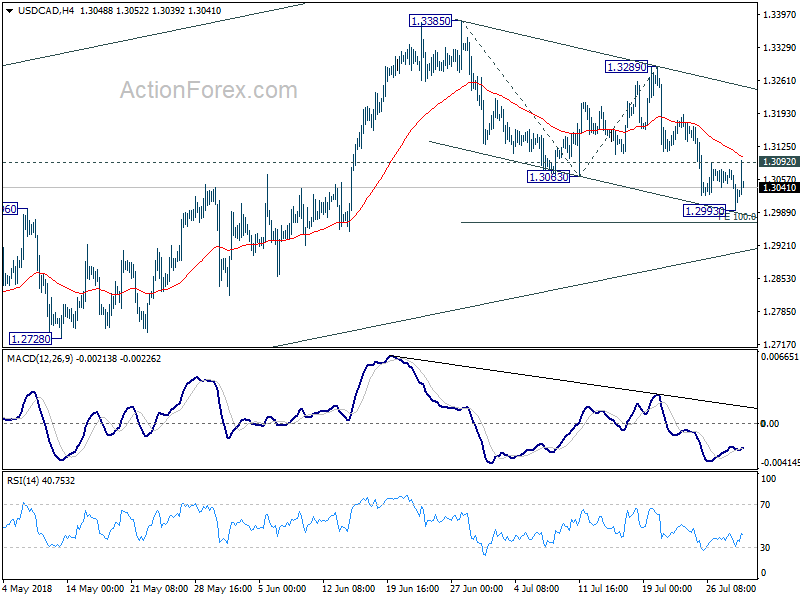

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2993; (P) 1.3037; (R1) 1.3079; More...

USD/CAD recovered after hitting 1.2993 and breached 1.3092 minor resistance. But there is no follow through buying so far. Intraday bias is turned neutral first. On the downside, below 1.2993 will resume the fall from 1.3385 to 100% projection of 1.3385 to 1.3063 from 1.3289 at 1.2967 and possibly below. But we're still seeing the fall from 1.3385 as a correction. Hence, we'd expect strong support from channel line (now at 1.2907) to contain downside and bring rebound. On the upside, firm break of 1.3092 will turn bias to the upside for 1.3289 resistance.

In the bigger picture, as long as channel support (now at 1.2907) holds, we're holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.