Sample Category Title

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7391; (P) 0.7403; (R1) 0.7419; More...

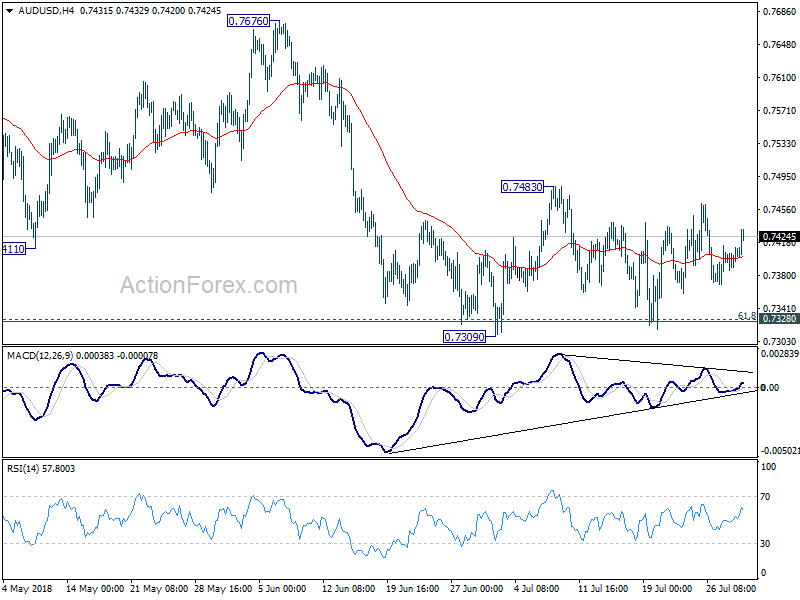

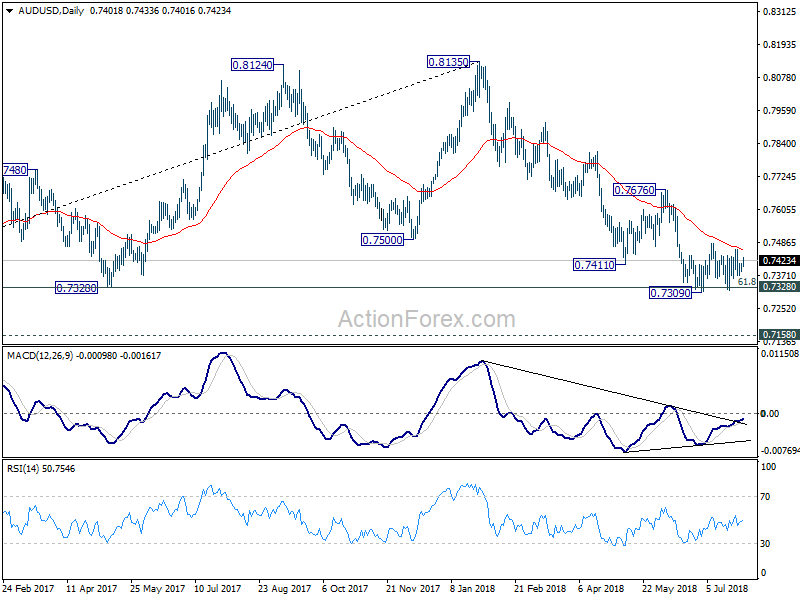

AUD/USD is staying in consolidation from 0.7309 and intraday bias remains neutral. On the upside, above 0.7483 resistance will bring stronger rebound. But upside should be limited below 0.7676 resistance to bring larger fall resumption eventually. On the downside, break of 0.7309 and sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

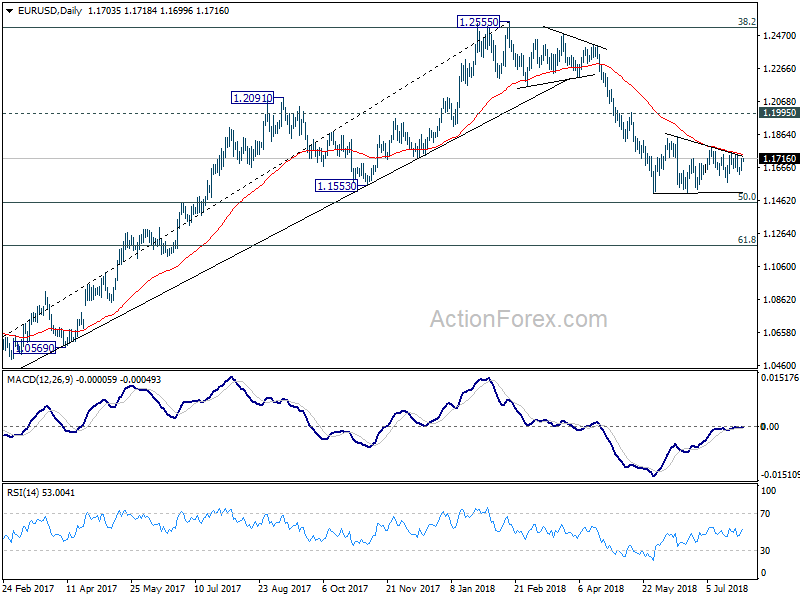

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1631; (P) 1.1648 (R1) 1.1675; More.....

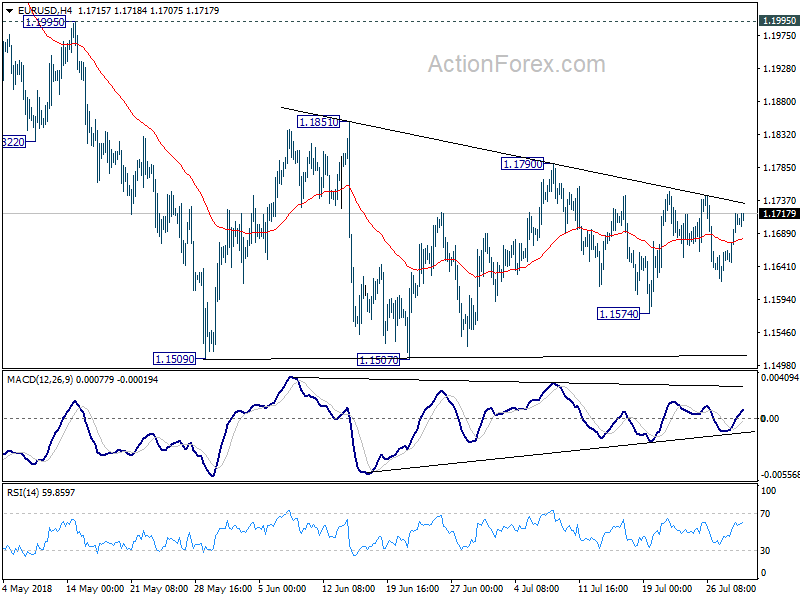

EUR/USD is still bounded in consolidation from 1.1509 and intraday bias stays neutral. In case of stronger recovery, upside should be limited by 1.1851 resistance to bring fall resumption eventually. On the downside, decisive break of 1.1507 low will resume larger down trend from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

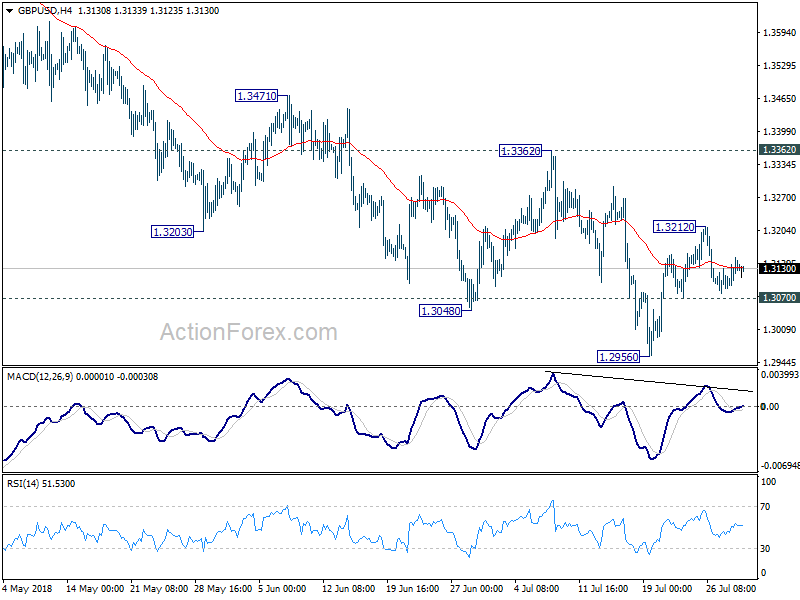

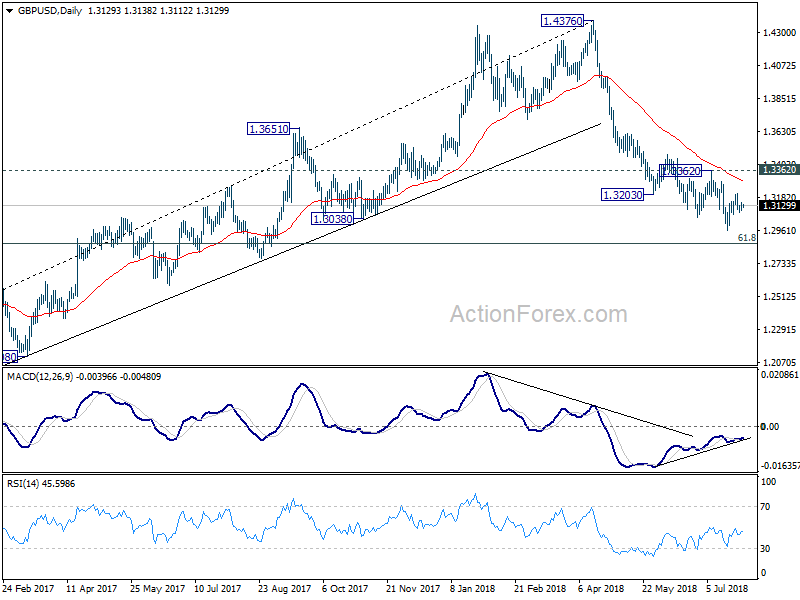

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3102; (P) 1.3128; (R1) 1.3158; More...

GBP/USD is still bounded in tight range of 1.3070/3212 and intraday bias remains neutral. On the downside, break of 1.3070 minor support will suggest completion of rebound form 1.2956 and turns bias back to the downside for this low. Firm break there will resume larger decline from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3212 will bring further recovery. But still, price action from 1.2956 are a corrective pattern. Upside should be limited by 1.3362 resistance to bring larger decline resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

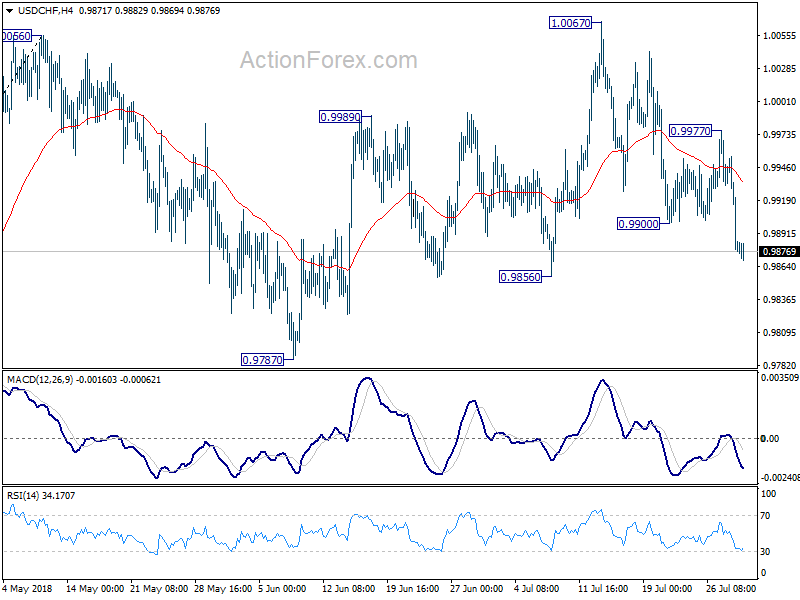

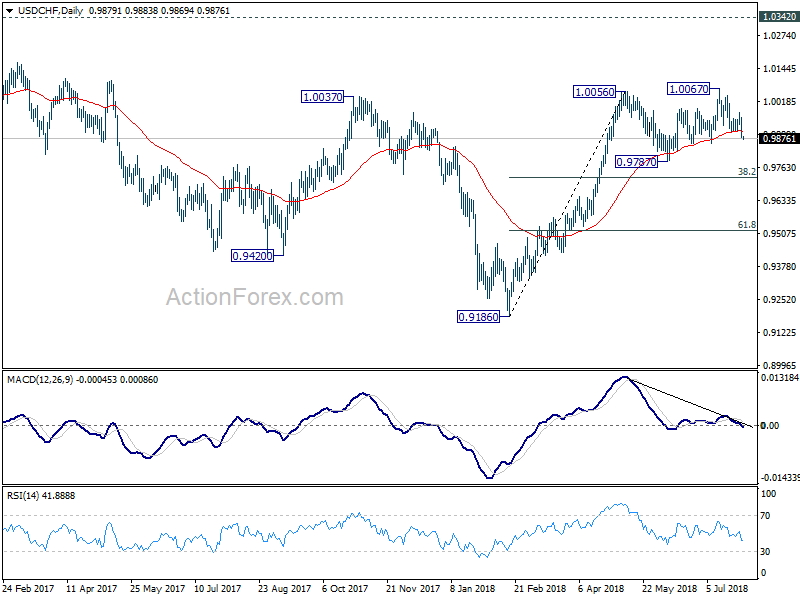

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9854; (P) 0.9906; (R1) 0.9934; More...

The break of 0.9900 support indicates resumption of fall from 1.0067. Intraday bias is turned to the downside for 0.9856 support first. Break will target 0.9787 and below. For now, USD/CHF is seen as in consolidation from 1.0056 with fall from 1.0067 as the third leg. Downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound. On the upside, break of 0.9977 resistance is needed to indicate completion of the decline. Otherwise, near term outlook is mildly bearish in case of recovery.

In the bigger picture, current development suggests that the consolidation pattern from 1.0056 is extending with another leg. As long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds, we'd expect rise from 0.9186 to resume at a later stage to retest 1.0342 key resistance (2016 high). However, sustained break of 0.9724 will bring deeper fall, as another declining leg in the long term range pattern.

Yen Spikes Lower after BoJ, But No Follow Through Selling Yet

Yen spikes lower broadly after BoJ announced to strengthen the framework for continuous powerful easing. But at this point, there is no follow through selling seen yet. Instead, of raising the target on 10 year JGB yields, BoJ simply allow flexibility to move it in move directions of up and down. Also, it added forward guidance that interest rates will stay extremely low for an extended period of time. 10 year JGB yields drops sharply from day high at 0.115 and breaches 0.07. Nikkei, on the other hand, cheers the announcement and reversed earlier loss, up 0.13% at the time of writing.

Staying in the currency markets, while Yen is weak, Canadian Dollar is even worse today on report that Canada is rejected from the US-Mexico NAFTA talk in an unusual move. Australian Dollar is showing some strength. Euro and Swiss Franc follow as the second and third strongest. But the common currency will face the tests of Eurozone GDP and CPI in European session. Dollar is mixed for today as markets await a string of economic data from the US, including consumer confidence and PCE inflation.

Technically, while Yen spikes lower, USD/JPY is held below 111.53 minor resistance, and thus, maintains near term bearishness. GBP/JPY is also held below 146.51 minor resistance. EUR/JPY breaches equivalent resistance at 130.25 but lacks follow through buying so far. USD/CAD breaches 1.3092 but also lacks follow through buying. Overall, there is no "committed" direction in the markets yet.

Yen falls broadly as BoJ strengthens the framework for continuous powerful easing

Yen is sold off sharply after BoJ announced the "Strengthening the Framework for Continuous Powerful Monetary Easing".

On Yield Curve Control framework BoJ voted 7-2 on the following decision. Firstly, short term interest rate target is held unchanged at -0.1%. Secondly, 10 year JGB yield target is maintained at around 0%. But, "yields may move upward and downward to some extent mainly depending on developments in economic activity and prices". The annual pace of monetary expansion is kept at around JPY 80T. BoJ also noted that "in case of a rapid increase in the yields, the Bank will purchase JGBs promptly and appropriately".

Y Harada and G Kataoka dissented the above decision. Harada said allowing long term yields to move upward and downward was to some extent "too ambiguous". Kataoka continued his push to broaden the target to JGB of 10-years and longer.

BoJ also added forward guidance on interest rate. It said "the Bank intends to maintain the current extremely low levels of short- and long-term interest rates for an extended period of time, taking into account uncertainties regarding economic activity and prices including the effects of the consumption tax hike scheduled to take place in October 2019."

BoJ: Growth to slow in 2019/20, inflation expectations lagging behind

In the latest Outlook for Economic Activity and Prices, BoJ said the economy is "likely to continue growing at a pace above its potential in fiscal 2018". For fiscal 2019 through fiscal 2020, the expanding trend is expected to continue, "partly supported by external demand", but pace will "decelerate" due to "cyclical slowdown in business fixed investment" and the impact of planned sales tax hike.

Year-on-year ex-food CPI stayed positive but continued to show "relatively weak developments". And, rise in medium- to long-term inflation expectations has been "lagging behind". BoJ noted that's because "the mindset and behavior based on the assumption that wages and prices will not increase easily have been deeply entrenched". But inflation is still expected to increase gradually towards 2% target, "although it will take more time than expected".

For fiscal 2018, risks are generally balanced. But risks are skewed to the downside for fiscal 2019.

Also release from Japan, unemployment rate rose 0.2% to 2.4% in June. Industrial production dropped -2.1% mom in June. Housing starts dropped -7.1% yoy. Consumer confidence dropped -0.2 to 43.5 in July.

CAD dives as Canada rejected from US-Mexico NAFTA talks

Canadian Dollar drops sharply on a report by the National Post that it's rejected from the senior level NAFTA talks between the US and Mexico, which will be held later this week. Quoting unnamed source, the report noted that the request by Canadian Foreign Affairs Minister Chrystia Freeland to join the meeting was ignore or spurned outright by US Trade Representative Robert Lighthizer. And Lighthizer is planning not to involve Canada unless the latter make some major concessions.

Separately, it's reported that the US and Mexico will hold ministerial-level NAFTA trade talks on Thursday in Washington. According to a Mexican source quoted by Reuters, there will be "technical meetings probably until Wednesday and a ministerial meeting on Thursday."

China PMI manufacturing dropped to 51.2, short term downward pressure emerged

The official China PMI manufacturing dropped -0.3 to 51.2 in July, below expectation of 51.3. Official PMI services dropped -1.0 to 54.0, missed expectation of 55.0. Analyst Zhang Liqun noted in the release that despite the slight decline in the PMI index, "steady growth of the economy remained unchanged". However, "short term downward pressure has emerged".

Looking at the details, eight of the sub-indices declined in the month. They include production, new order, purchase volume, import, purchase price, ex-factory price, suppliers delivery, production and operation expectation, New export orders, was unchanged but in contraction region at 49.8. The data set is seen by some as the first sign of impact from increasing trade tension with the US.

New Zealand ANZ business confidence dropped to 10 year low, economy feels increasingly late in the cycle

New Zealand ANZ business confidence index dropped to -45 in July, down -5 pts. That's the lowest level since May 2008. Own activity index dropped -5 pts to 4, lowest since May 2009. Sub-indicators were weak across the board, and retail is the least

confident sector.

ANZ noted in the release that "this economy feels increasingly late in the cycle". While fiscal stimulus and strong terms of trade will support growth, "sustained low business confidence increases the risk that firms will delay investment and hiring decisions". "The Road ahead is looking less assured, and risks of a stall have increased.

Also from down under, New Zealand building permits dropped -7.6% mom in June. Australia building approvals rose 6.4% mom in June.

Looking ahead

Eurozone Q2 GDP and CPI will be the major focus in European session. Eurozone will also release unemployment rate. Germany will release retail sales and unemployment. Later in the day, Canada will release GDP, IPPI and RMPI. US will release personal income and spending, employment cost index, S&P Case-Shiller house price, Chicago PMI and consumer confidence.

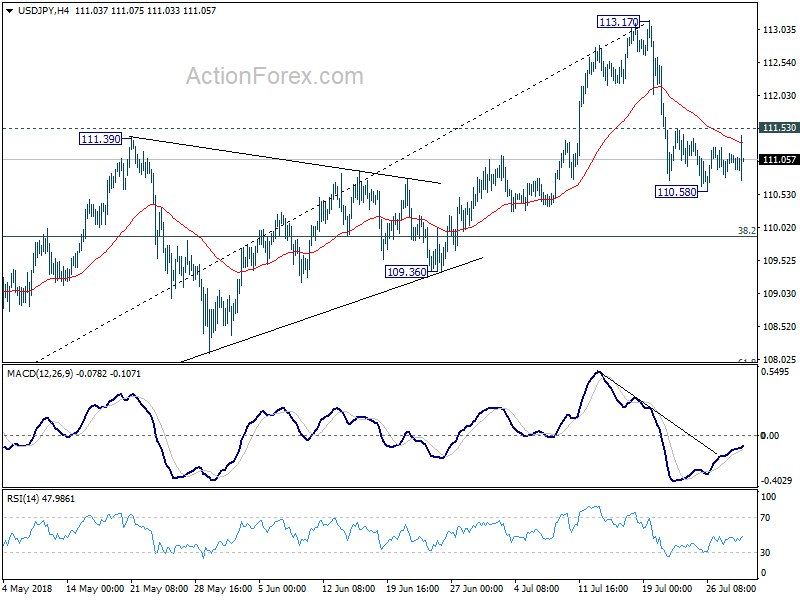

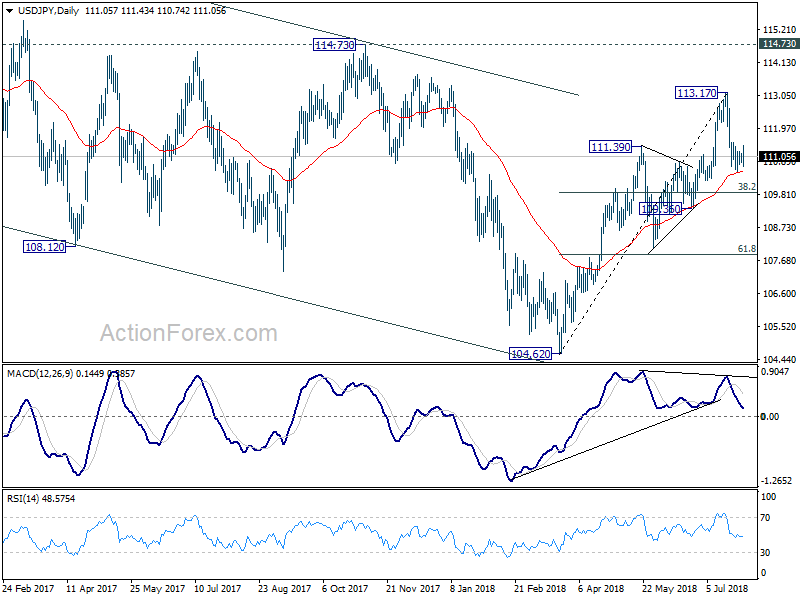

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.92; (P) 111.04; (R1) 111.20; More...

USD/JPY spikes higher to 111.43 earlier today but upside is limited below 111.53 minor resistance. Intraday bias stays neutral for consolidation above 110.58 temporary low. with 111.53 intact, deeper fall is expected. On the downside, below 110.58 will extend the corrective fall from 113.17. But in that case, we'd expect strong support from 38.2% retracement of 104.62 to 113.17 at 109.90 to bring rebound. On the upside, break of 111.53 will turn bias to the upside for retesting 113.17 high.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -7.60% | 7.10% | 6.90% | |

| 23:01 | GBP | GfK Consumer Confidence Jul | -10 | -9 | -9 | |

| 23:30 | JPY | Jobless Rate Jun | 2.40% | 2.30% | 2.20% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -2.10% | -0.30% | -0.20% | |

| 01:00 | NZD | ANZ Business Confidence Jul | -44.9 | -39 | ||

| 01:00 | CNY | Manufacturing PMI Jul | 51.2 | 51.3 | 51.5 | |

| 01:00 | CNY | Non-manufacturing PMI Jul | 54 | 55 | 55 | |

| 01:30 | AUD | Building Approvals M/M Jun | 6.40% | 1.00% | -3.20% | -2.50% |

| 04:03 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -7.10% | -2.50% | 1.30% | |

| 05:00 | JPY | Consumer Confidence Jul | 43.5 | 43.8 | 43.7 | |

| 06:00 | EUR | German Retail Sales M/M Jun | 1.00% | -2.10% | ||

| 07:55 | EUR | German Unemployment Change (000's) Jul | -10K | -15K | ||

| 07:55 | EUR | German Unemployment Claims Rate Jul | 5.20% | 5.20% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 8.30% | 8.40% | ||

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Jul | 2.00% | 2.00% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul A | 1.00% | 0.90% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 A | 0.40% | 0.40% | ||

| 09:00 | EUR | Eurozone GDP Y/Y Q2 A | 2.20% | 2.50% | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.20% | 1.00% | ||

| 12:30 | CAD | Raw Materials Price Index M/M Jun | 2.70% | 3.80% | ||

| 12:30 | CAD | GDP M/M May | 0.30% | 0.10% | ||

| 12:30 | CAD | GDP Y/Y May | 2.30% | 2.50% | ||

| 12:30 | USD | Personal Income Jun | 0.40% | 0.40% | ||

| 12:30 | USD | Personal Spending Jun | 0.40% | 0.20% | ||

| 12:30 | USD | PCE Deflator M/M Jun | 0.10% | 0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y Jun | 2.30% | 2.30% | ||

| 12:30 | USD | PCE Core M/M Jun | 0.10% | 0.20% | ||

| 12:30 | USD | PCE Core Y/Y Jun | 2.00% | 2.00% | ||

| 12:30 | USD | Employment Cost Index Q2 | 0.70% | 0.80% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y May | 6.40% | 6.60% | ||

| 13:45 | USD | Chicago PMI Jul | 61.8 | 64.1 | ||

| 14:00 | USD | Consumer Confidence Index Jul | 126.5 | 126.4 |

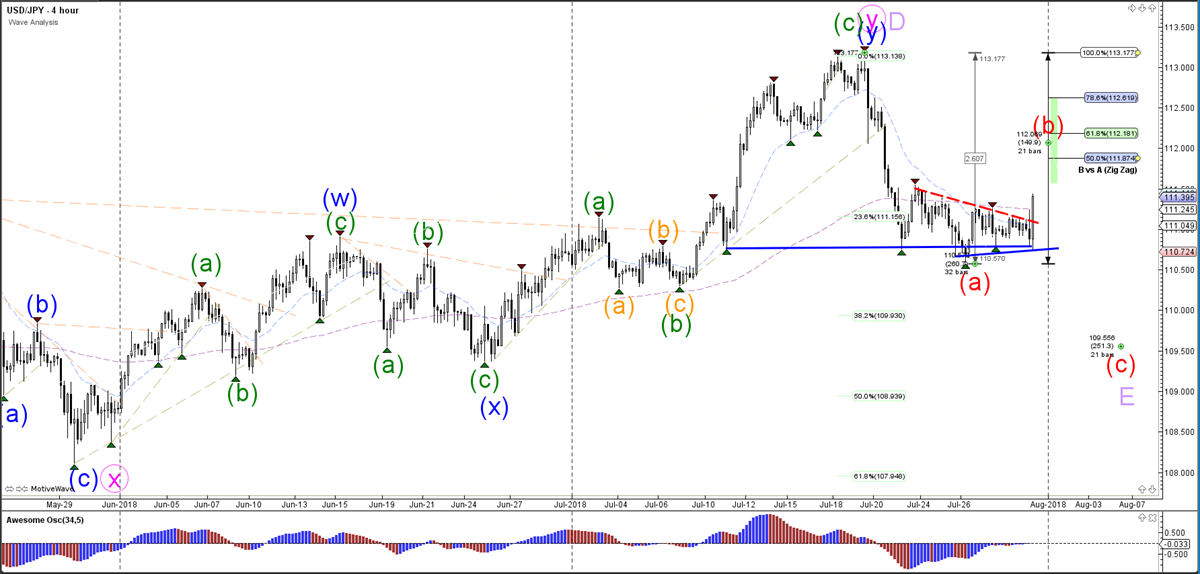

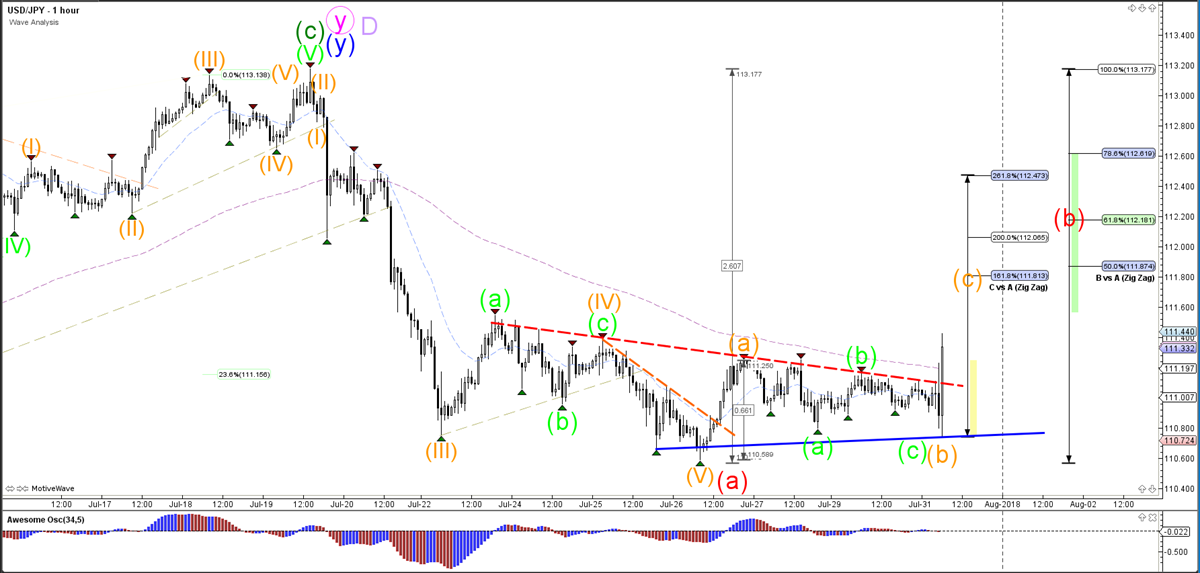

USD/JPY Bullish Breakout Faces Resistance Fib Levels

The USD/JPY is breaking above the resistance trend line (dotted red) of the triangle chart pattern, which is indicating a potential bullish breakout. However, if price is indeed in a wave B (red) of a larger wave E (purple), then price should bounce at the Fibonacci levels of wave B vs A. A break above the 100% Fib level invalidates the ABC (red) patterns and could indicate an uptrend continuation.

The USD/JPY seems to have completed and ABC (green) within wave B (orange). Price could now be ready for an impulsive and bullish wave C (orange) if price manages to break above the resistance trend line (dotted red) with a strong candle.

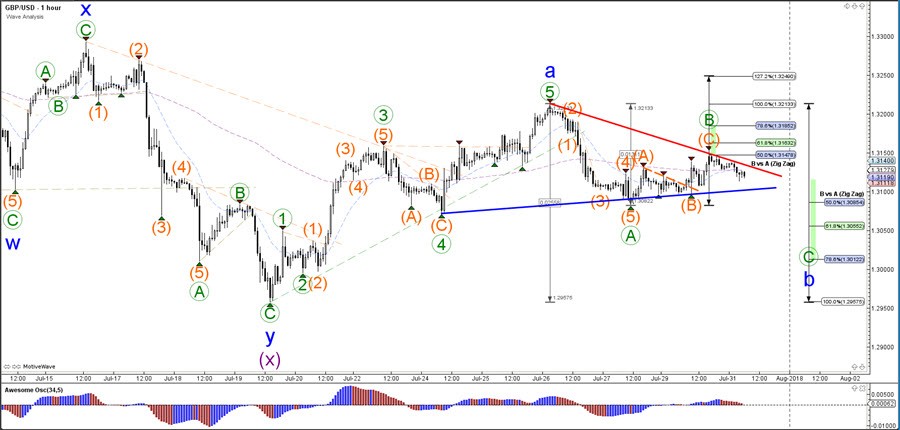

GBP/USD Awaits Critical Breakout Of Triangle Chart Pattern

The GBP/USD made a bullish bounce at the 50% Fibonacci level but price action was slow and choppy. The corrective price pattern seems to be confirming an extended and deeper bearish wave B (blue).

The GBP/USD is expected to eventually finish the wave B (blue) at one of the Fibonacci levels of wave B vs A which could act as a bouncing spot. The Cable will need to break above the resistance lines before a bullish wave C is confirmed whereas a break below the Fibs of wave B vs A makes a wave B (blue) less likely.

The GBP/USD bullish bounce seems to have created an ABC (orange) correction within wave B (green) after stopping and bouncing at the 50% Fibonacci level of wave B vs A. The triangle chart patterns and its support and resistance trend lines remain critical. If price breaks the resistance trend line (orange), then a larger bullish breakout should occur towards a deeper Fib. If price breaks the support trend line (blue), then a larger bearish breakout should take price to deeper Fibonacci levels of wave B vs A (blue).

Fed Prepares for Rate Hike in September

The upcoming FOMC meeting later this week aims at preparing the market for another +25 bps rate hike in September. As no press conference and economic projections would follow the August meeting, the post-meeting statement, and the minutes in three weeks, would be used for communication and setting expectations. We expect the rhetoric of the upcoming statement/minutes would be more or less the same as the June one, at which some members suggested to “modify the language in the post-meeting statement”. Against the backdrop of robust GDP growth, inflation and employment on one hand, and heightening US-China trade conflict on another, the members would likely have rigorous debate over the future path on rate hike. After all, we expect the rate hike path would remain unchanged from the one laid down in June (100 bps increases in both 2018 and 2019). The debate on the change in the “forward guidance” which had been indicating that “the stance of monetary policy remains accommodative” would continue this month with actual change could come later in the year.

The first estimate of US GDP growth soared to an annualized +4.1% q/q in 2Q18, thanks to the strength in private consumption (+4%) and government spending (+3.5%). Business investment grew +5.4%, moderating from +8% in the first quarter, while net exports improved. The strong outcome was a result of fiscal stimulus and strong household spending evidenced the underlying momentum of the domestic economy. However, contribution from net exports could have been driven by temporary factors, including the normalization of auto sales and front-loaded soybean exports to China, which might dissipate in the second half of the year. There will be two revisions to 2Q18 GDP growth data and they could show dramatic change to the preliminary result. Headline inflation improved further to +2.9% y/y in June, from +2.8% a month ago. Core CPI also accelerated to +2.3%, the largest rise since January 2017, from +2.2% in May. PCE, Fed’s preferred inflation estimate, would likely stay around the +2% target in June. The economic backdrop hence warrants the Fed to retain its language that growth has been “solid” and household spending “has picked up”.

Unemployment rate edged higher to 4% in June, from 3.9% in May. The market anticipates it to return to 3.9% in July. Since the FOMC meeting takes place ahead of the release of the June employment report, the member might thus need to adjust the language slightly to illustrate the increase in the unemployment rate in May. The Fed might need to restore the description that unemployment rate has stayed “low” (used in the May statement), after noting that the unemployment rate has “declined” in the June statement.

The June minutes revealed that the members discussed the term structure of interest rates. We expect the discussions would continue in August given the fact the Treasury yield curve has flattened by a greater extent since the June meeting.

Elliott Wave Analysis: SPX Buying Opportunity Soon

SPX Short-term Elliott Wave analysis suggests that the pullback to $2691.80 low on 6.28.2018 ended intermediate wave (2). Above from there, the rally higher to $2848.03 peak ended Minor wave 1. The internals of that rally higher took the form as impulse Elliott wave structure where Minute wave ((i)), ((ii)) & ((iii)) unfolded in 5 waves structure & wave ((ii)) & ((iv)) unfolded in 3 swings corrective sequence.

Up from $2691.8 low, the rally higher to $2743.26 high ended Minute wave ((i)) in 5 waves. The pullback to $2698.95 ended Minute wave ((ii)) and the rally higher to $2804.53 high ended Minute wave ((iii)) as 5 wave structure. From there, Minute wave ((iv)) pullback ended at $2789.24 low and the rally higher to $2848.03 peak ended Minute wave ((v)) which also completed Minor wave 1.

The Index is now correcting cycle from 6.28.2018 low within wave 2 in 3, 7 or 11 swings before further upside is seen. Near-term focus remains towards $2783.14-$2759.10, which is 100%-161.8% Fibonacci extension area of ((w))-((x)) to end the 3 swings pullback in Minor wave 2. Buyers should appear from the above area either for new highs or for 3 waves reaction higher at least. We don’t like selling it.

SPX 1 Hour Elliott Wave Chart

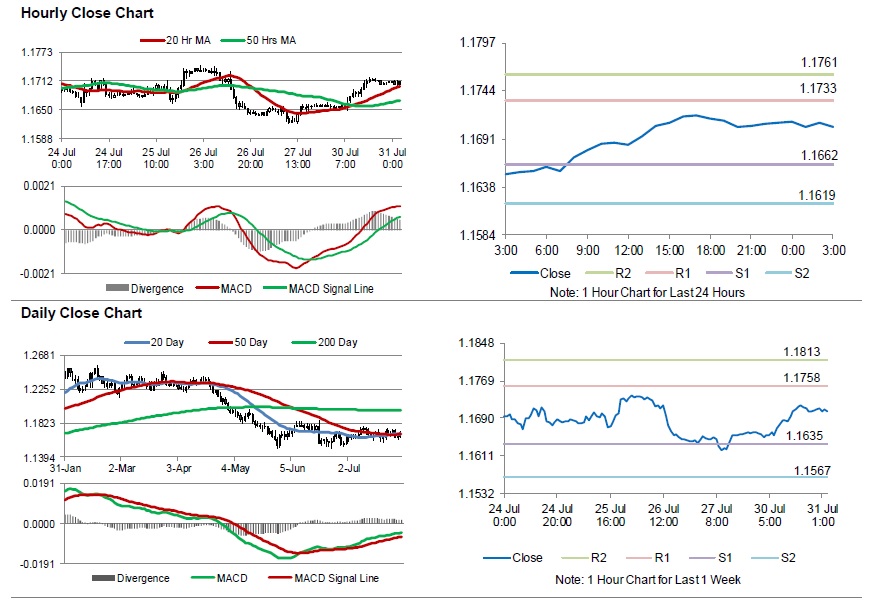

Euro-Zone’s Consumer Confidence Remains Steady, While Economic Confidence Falls To A 1-Year Low In July

For the 24 hours to 23:00 GMT, the EUR rose 0.45% against the USD and closed at 1.1709.

Data showed that the Euro-zone's final consumer confidence index remained unchanged at -0.6 in July, at par with market expectations and confirming the preliminary print. Meanwhile, the nation's economic sentiment indicator dropped to a one-year low level of 112.1 in July, compared to market expectations for a decline to a level of 112.0. In the previous month, the economic sentiment indicator had registered a reading of 112.3. Moreover, the region's business climate indicator eased to 1.29 in July, after recording a revised reading of 1.38 in the prior month. Market participants had expected the index to drop to a level of 1.35.

Separately, in Germany, the preliminary consumer price index (CPI) climbed 2.0% on an annual basis in June, undershooting market expectations for an advance of 2.1%. In the previous month, the CPI had climbed 2.1%.

In the US, data revealed that US pending home sales rebounded 0.9% on a monthly basis in June, higher than market expectations for an advance of 0.1%. Pending home sales had registered a drop of 0.5% in the prior month.

On the contrary, the nation's Dallas Fed manufacturing business index eased to 32.3 in July, less than market expectations for a drop to a level of 31.0. The index had registered a reading of 36.5 in the preceding month.

In the Asian session, at GMT0300, the pair is trading at 1.1704, with the EUR trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.1662, and a fall through could take it to the next support level of 1.1619. The pair is expected to find its first resistance at 1.1733, and a rise through could take it to the next resistance level of 1.1761.

Going ahead, investors will await Euro-zone's Q2 gross domestic figures along with the consumer price index for July and unemployment rate for June, slated to release in a few hours. Moreover, Germany's retail sales for June and unemployment rate for July, will be on investors radar. Later in the day, the US personal income and spending data for June, followed by the consumer confidence index and the Chicago purchasing manager's index, both for July, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.