Sample Category Title

British Pound Higher as Consumer Credit Levels Rise

The British pound has posted gains in the Monday session. In North American trade, the pair is trading at 1.3136, up 0.24% on the day. On the release front, British Net Lending to Individuals improved to GBP 5.4 billion, edging above the estimate of GBP 5.3 billion. Later in the day, British GfK Consumer Confidence is expected to post a second straight reading of -9 points. In the U.S, Pending Home Sales posted a strong gain of 0.9%, rebounding after two straight declines. This easily beat the estimate of 0.4%. On Tuesday, the U.S releases consumer spending and inflation indicators, as well as CB Consumer Confidence.

The pound hasn’t made much noise in recent weeks, but that could change later in the week. On Thursday, the Bank of England will set the benchmark rate, and the markets are expecting a 25-point hike, which would raise the rate to 0.75%. BoE policymakers are divided on the timing of hike, the economy is coming off a soft first quarter and wage growth as been weak – both reasons to avoid a hike. Proponents of a rate increase point to the tight labor market and high employment participation rate. Brexit is another factor, as the messy state of negotiations with the EU could lead to a ‘hard Brexit’ (no deal with the EU) which could take a toll on the economy. It could be a busy week for the pound ahead of the rate meeting.

The U.S economy continues to sparkle, and Friday’s Advance GDP for the second quarter reflected this, with an excellent gain of 4.1%. This is much higher than the 2.2% gain recorded in the first quarter. This reading was within market expectations, so the dollar wasn’t able to gain ground. Strong economic numbers have kept the U.S currency at high levels, despite recent remarks by President Trump saying that the dollar is too high and is hampering exports. These comments have weighed on the dollar, but usually for a brief time only, as the performance of the economy has talked louder than Trump’s tweets. On Friday, Trump took credit for the strong GDP reading and claimed that “these numbers are very, very sustainable”. However, analysts are being more cautious in their forecasts, with growth in the third quarter expected to drop to around 2.5 percent.

FOMC Preview: Fed on Holiday

We expect the Fed to maintain the target range at 1.75-2.00% at the upcoming meeting on Wednesday.

It is one of the small meetings without updated projections or any press conference. The only piece of information we will get is the statement, but it does not change much from meeting to meeting.

At the June meeting, the Fed decided to remove several soft sentences from the statement, as it wants more flexibility now the Fed funds rate is close to neutral. We do not believe the Fed wants to change this at this point. Hence, it is unlikely to send any new policy signals. This was also the case during Fed Chair Powell's hearing not long ago.

We still think the Fed is on track to deliver two more hikes this year (September and December), which is in line with the Fed's own projection (although the committee is divided between one and two hikes) and market pricing.

The biggest discrepancy is between the Fed's projections for the number of hikes next year and market pricing, also in light of the flat US yield curve, which is regarded as a reliable recession indicator. The Fed does not expect the yield curve to invert and is likely to continue hiking if it is right. However, the majority of FOMC members have indicated they are ready to pause the hiking cycle if the yield curve (against their expectations) is about to invert. The minutes, due out in a couple of weeks, may shed more light on how the Fed interprets the recent development.

The Fed's 'quantitative tightening' (QT) programme is still open-ended and we do not know how low the Fed wants the balance sheet to go. In our base case, where the economy holds up and does not fall into recession in the next couple of years, the process is likely to continue, and it seems like the bar is high for the Fed to discontinue it even if we see increased financial stress due to tighter liquidity. The Fed is unlikely to stop QT before early 2019 at the earliest but bias among members is to keep it in place for longer. The last increase in the caps is in October. We do not expect any major shifts in the communication on the balance sheet either.

Japanese Yen Stuck at 111 ahead of BoJ Rate Announcement

The Japanese yen is slightly lower in the Monday session. In the North American session, USD/JPY is trading at 110.96, down 0.06% on the day. On the release front, Japanese Retail Sales rebounded in July with a strong gain of 1.8%, edging above the estimate of 1.7%. This marked the strongest gain in 2018. Later in the day, the Bank of Japan winds up its policy meeting and will release a rate statement followed by a press conference. In the U.S, Pending Home Sales posted a strong gain of 0.9%, rebounding after two straight declines. On Tuesday, the U.S releases consumer spending and inflation indicators, as well as CB Consumer Confidence.

The BoJ rate statement could prove to be a non-event, as the Bank is expected to hold rates and no significant changes to the massive stimulus program are expected until inflation levels move higher. Last week’s inflation data was mixed. Tokyo Core CPI improved to 0.8%, its strongest gain in four months. The Bank of Japan has stubbornly held to its inflation of target of just under 2.0%, but this goal remains elusive. Earlier, in the week, Services Producer Price Index improved for a third straight month, jumping to 1.2% in June. This beat the estimate of 1.0% and marked the strongest gain since March 2015. At the same time, BoJ Core Inflation, the BoJ’s preferred inflation indicator, dipped to 0.4%, its smallest gain since in 11 months.

The U.S economy continues to sparkle, and Friday’s Advance GDP for the second quarter reflected this, with an excellent gain of 4.1%. This is much higher than the 2.2% gain recorded in the first quarter. This reading was within market expectations, so the dollar wasn’t able to gain ground. Strong economic numbers have kept the U.S currency at high levels, despite recent remarks by President Trump saying that the dollar is too high and is hampering exports. These comments have weighed on the dollar, but usually for a brief time only, as the performance of the economy has talked louder than Trump’s tweets. On Friday, Trump took credit for the strong GDP report and claimed that “these numbers are very, very sustainable”. However, analysts are being more cautious in their forecasts, with growth in the third quarter expected to drop to around 2.5 percent.

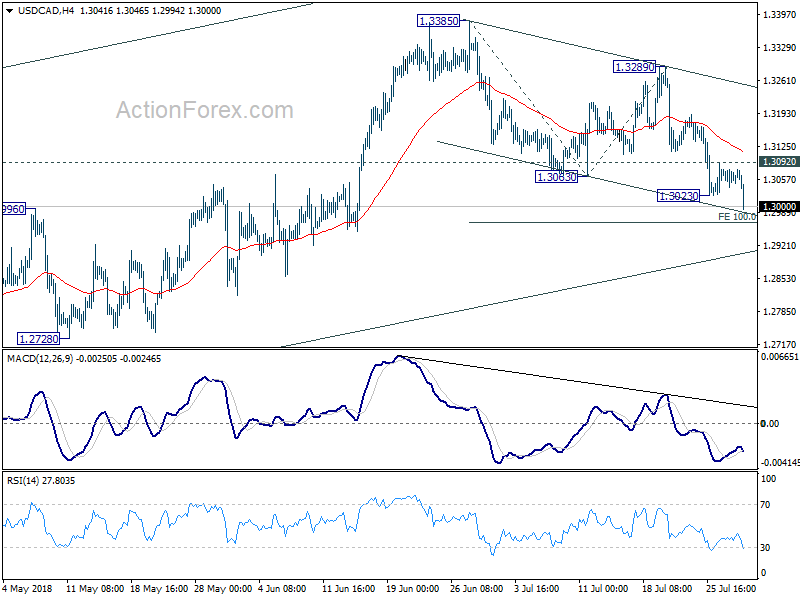

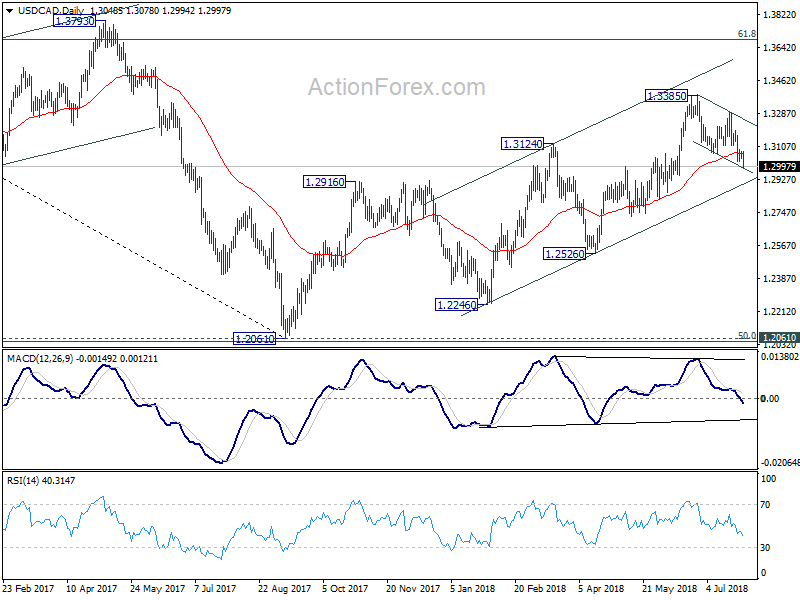

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3041; (P) 1.3061; (R1) 1.3080; More...

USD/CAD's decline resumed by taking out 1.3023 and reaches as low as 1.2994 so far. Intraday bias is back on the downside for 100% projection of 1.3385 to 1.3063 from 1.3289 at 1.2967 and possibly below. For now, we're still seeing the fall from 1.3385 as a correction. Hence, we'd expect strong support from channel line (now at 1.2903) to contain downside and bring rebound. On the upside, break of 1.3092 minor resistance will turn bias to the upside for 1.3289 resistance. However, sustained break of the channel support will carry larger bearish implication and bring deeper fall to 1.2526.

In the bigger picture, as long as channel support (now at 1.2903) holds, we're holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

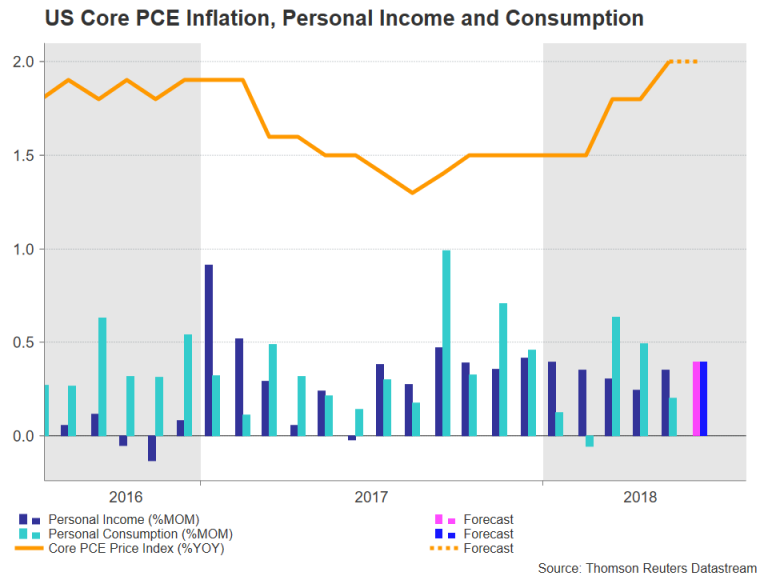

US Consumption Data to Attract Less Attention after GDP Report; Inflation to Remain at 2%

Data on US personal income and spending is not anticipated to attract the usual level of attention on Tuesday (due at 12:30 GMT) as the June figures were already incorporated in last week’s robust GDP stats. The focus will therefore be on core PCE inflation, which the Fed puts the most emphasis on when setting monetary policy. That is not to say that another solid set of numbers tomorrow would not be positive for the US dollar, helping it gain some upside momentum after losing steam earlier this month.

Personal income, which has been growing at a modest but steady pace since the middle of 2017, is forecast to continue this trend in June, rising by 0.4% month-on-month, unchanged from the prior month. Personal consumption is also expected to expand by 0.4% m/m, accelerating from the 0.2% rate seen in May. Strong consumer spending was one of the biggest contributors to the GDP surge in the second quarter and a solid end to the quarter could signal a continuation of this strength going into the third quarter.

Turning to the Fed’s preferred inflation indicator, the core personal consumption expenditures (PCE) price index is projected to remain at 2% year-on-year in June. It hit the Fed’s objective of 2% only in May for the first time in six years. But as the Fed has been stressing its ‘symmetric’ target in recent meetings, the possibility of core PCE inflation moving slightly above 2% in the coming months is unlikely to prompt the Fed to quicken its pace of rate increases.

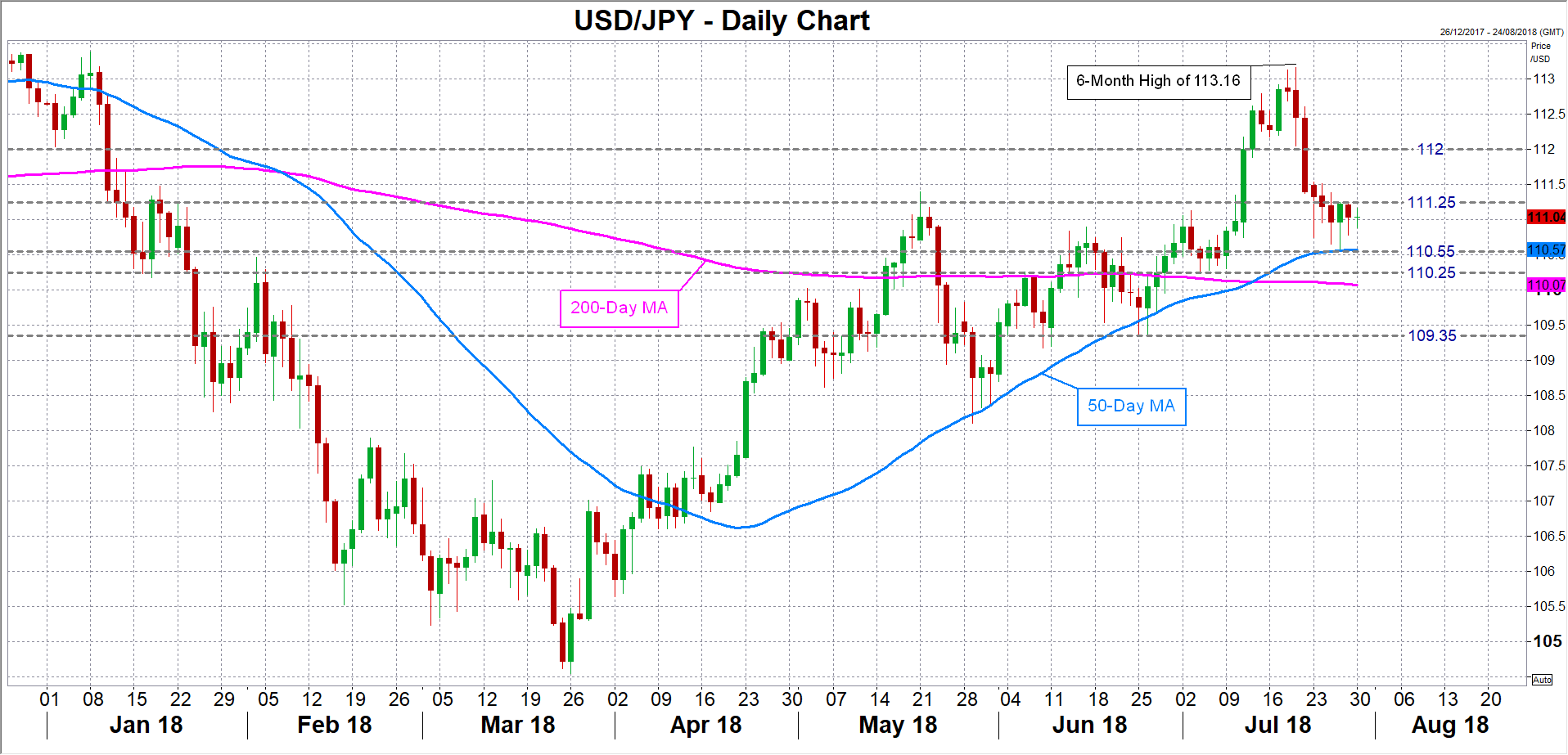

Nevertheless, if there is an upside surprise in the PCE readings, the dollar could receive a much-needed lift, particularly versus the Japanese yen, which the pair has been trading sideways for much of the past week. A push higher could see dollar/yen meeting immediate resistance around 111.25, which it failed to overcome late last week. A break above this level would turn the focus to the 112 handle (a previous support and resistance point), which it needs to overcome if it is to challenge its July top of 113.16.

Should any positive surprises fail to prevent the dollar from resuming its slide, or in the event of some data misses, the 50-day moving average (MA) would likely provide immediate support at around the 110.55 level. A breach of the 50-day MA would increase the risk to the downside, with the next support coming at 110.25, followed by the 109.35 region.

Also to keep in mind prior to Tuesday’s releases are the latest FOMC decision on Wednesday when the Fed concludes its two-day policy meeting, and the July nonfarm payrolls report on Friday. Traders are unlikely to place large bets ahead of those big risk events.

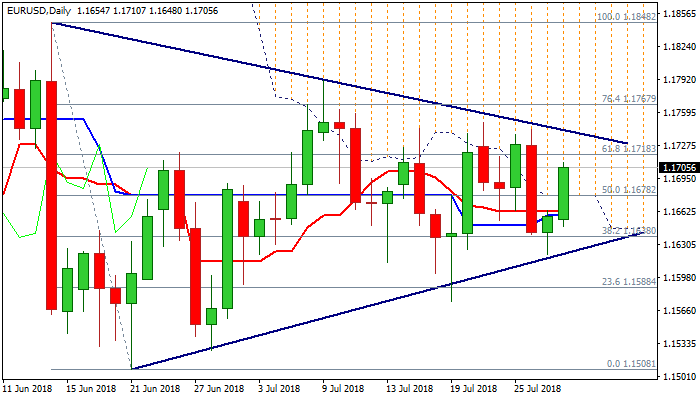

EURUSD Outlook: Bullish Tone in Early US Trading as Fresh Bullish Acceleration Penetrated Daily Cloud

The Euro stands at the front foot in early US trading and probes above 1.17 barrier. Fresh strength was sparked by solid German CPI data and weaker dollar, broke through a cluster of daily MA’s and penetrated thick daily cloud, which shifted immediate focus higher. Close within daily cloud would generate bullish signal for attack at the upper triangle boundary (1.1742) after downside attempts were rejected last Friday on triangle support line (1.1620). Improved daily techs are supportive, but overbought conditions on lower timeframes warn of stall ahead of triangle upper border. The pair would look for a catalyst which could spark stronger acceleration and result in clearer direction signal on break of either side of triangle. Tuesday’s release of German jobs data and EU CPI is in focus, with Fed’s rate decision on Wednesday, seen as key event.

Res: 1.1718; 1.1742; 1.1767; 1.1790

Sup: 1.1678; 1.1648; 1.1628; 1.1574

Sunset Market Commentary

Markets

Core bonds soon came under pressure in Europe this morning. The move was a bit ‘surprising’ given the price action at the end of last week. European bunds at that time enjoyed decent downside protection as Draghi didn’t feel any need to amend its lower for longer strategy on interest rates. On Friday, the US yields curve even bull flattened on a solid US Q2 GDP. This morning bond sentiment turned a bit different. The Japan 10-y yield again tested the 10 bp level and the BOJ stepped in with an unconditional buying promise to prevent a further rise. The Bund future came also soon under pressure. A big selling order in gilts was rumoured to have affected overall sentiment. Whatever the reason, global core bonds suffered even as data and/or global market sentiment at first sight didn’t support this move. The confidence data from the EC were mixed/close to expectations. Spanish (2.3% Y/Y) and German inflation (2.1% Y/Y) were also in line to slightly softer than expected. This afternoon, US bond bonds followed the broader move, but slightly outperformed Bunds. US eco data were second tier and with little impact on trading. The US yield curve bear steepens with yields rising between 1.0 bp (2-y) and 3.2bp (30-y). Bund yields are rising between 1.7 bp (2-y) and 5 bp (10-y). Intra-EMU yield spreads changes were modest despite the correction on core markets. We look whether today’s price action might be the start of a more pronounced repositioning on the bond markets after recent calm. Italy (-1 bp 10y) even slightly outperformed on a decent BTP auction.

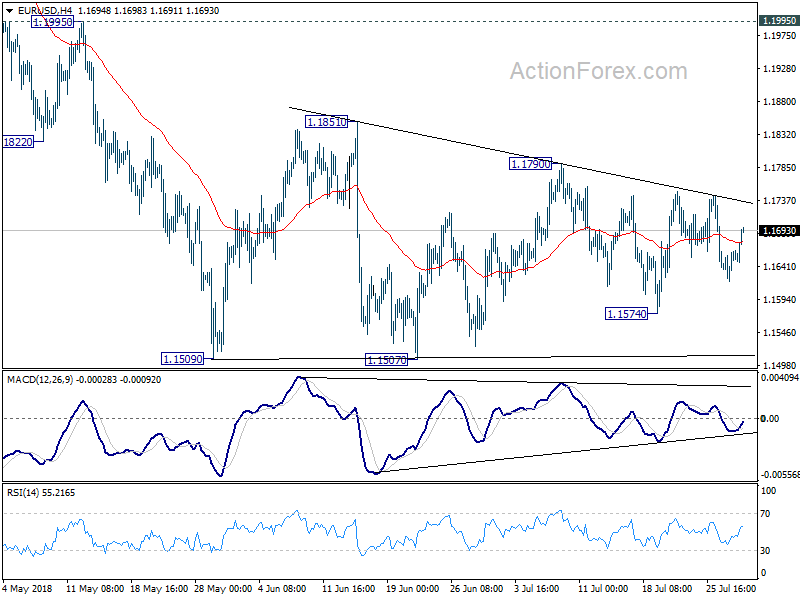

The moves in EUR/USD and USD/JPY were modest given the swings in the bond markets. EMU eco data (EC confidence and German CPI) were close to expectations. A slight narrowing in the US German interest rate differential may have supported the EUR/USD cross rate. The inability of the dollar to gain on Friday’s US GDP release might have signaled short-term players that the downside in this cross rate was rather well protected. Whatever, EUR/USD changed again course, drifting higher in the 1.105/1.1850 range. Whatever, the consolidation pattern is still very well in place. USD/JPY hovers in the 111 area, awaiting the outcome tomorrow’s BOJ meeting.

Today, sterling trading was mostly driven by technical considerations. UK eco data (Money supply & lending data) were mixed. Brexit noise persists by and is currently not giving a clear guidance for sterling trading. EUR/GBP gained a few ticks on the intraday EUR/USD rebound. The pair hovers again near the 0.89 big figure. Cable trades little changed to marginally stronger on USD softness.

News Headlines

The BOJ has intervened in the bond market for the third time in a week today, purchasing $14.76bn in government bonds. The bank announced it after the 10-year yield moved above 0.11%, while the target is about 0%. Today and tomorrow the central bank is having its policy meeting, announcing the outcome tomorrow.

Swedish GDP increased by 1% in the second quarter of this year, while only a 0.5% increase was expected. The 0.7% growth in the first quarter was also upwardly revised to 0.8% Q/Q. These unexpected growth numbers pushed EUR/SEK to the 10.23 area, a decrease of 0.7%.

A Sky News poll has indicated that two-thirds of UK voters think the government will end up with a bad deal when the UK leaves the EU and half wants a new referendum to choose between leaving with a deal, leaving without a deal or staying in the EU. When already asked the question, 48% would prefer to stay in the EU.

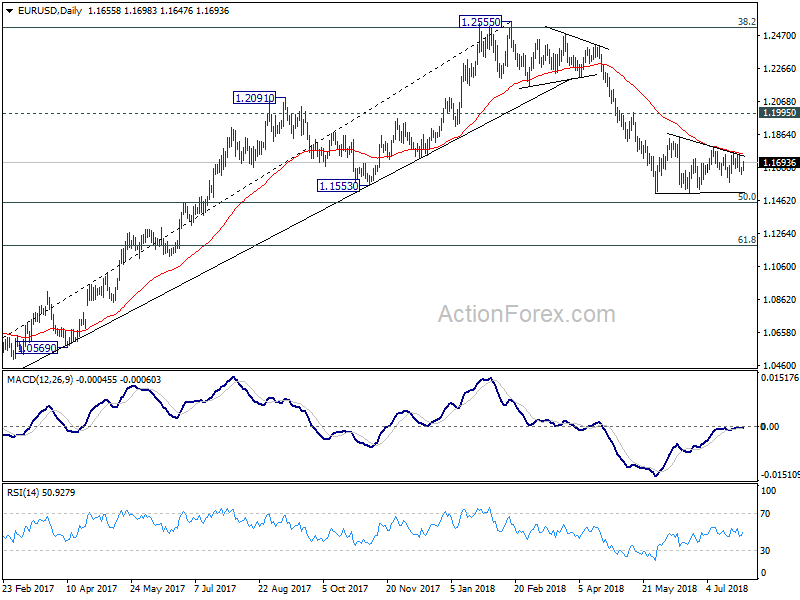

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1631; (P) 1.1648 (R1) 1.1675; More.....

The consolidation from 1.1509 is still extending and intraday bias remains neutral. In case of another recovery, upside should be limited by 1.1851 resistance to bring fall resumption eventually. On the downside, decisive break of 1.1507 low will resume larger down trend from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

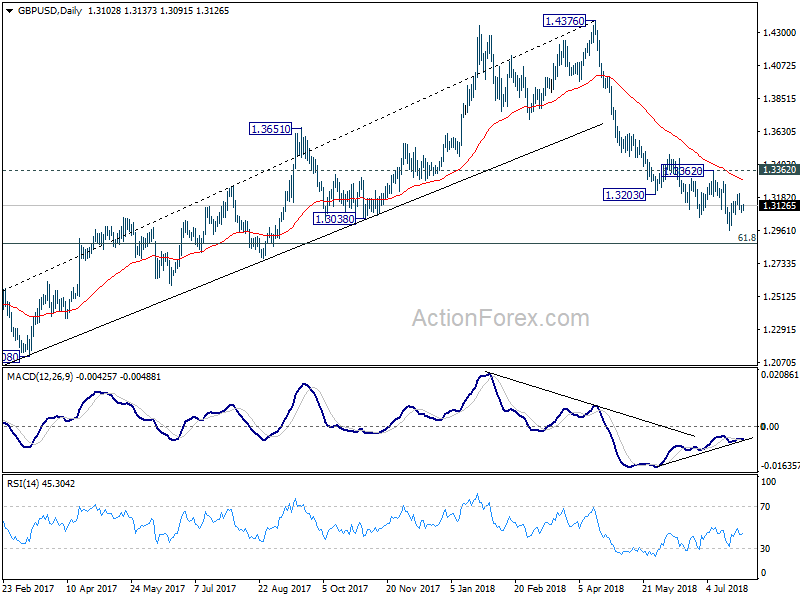

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3076; (P) 1.3110; (R1) 1.3139; More...

Intraday bias in GBP/USD is still neutral for the moment. On the downside, break of 1.3070 minor support will indicate completion of rebound form 1.2956 and turns bias back to the downside for this low. Firm break there will resume larger decline from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3212 will bring further recovery. But still, price action from 1.2956 are a corrective pattern. Upside should be limited by 1.3362 resistance to bring larger decline resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

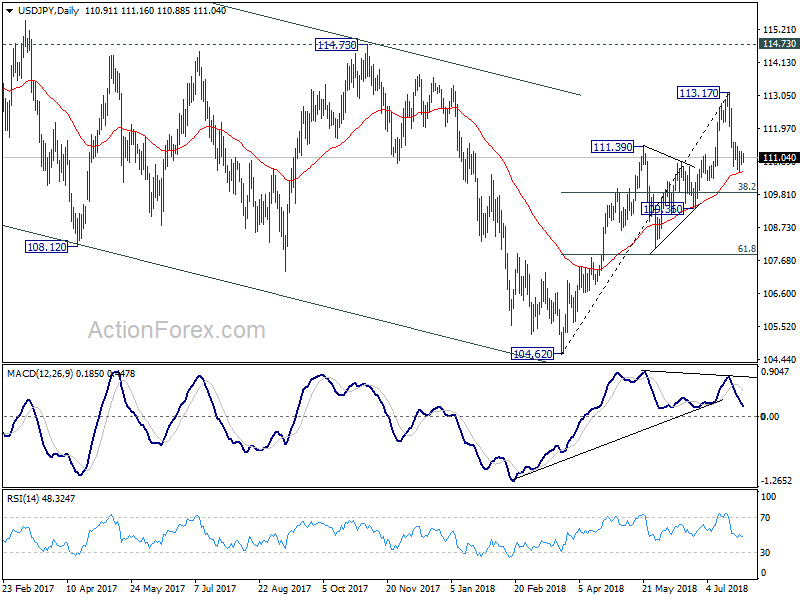

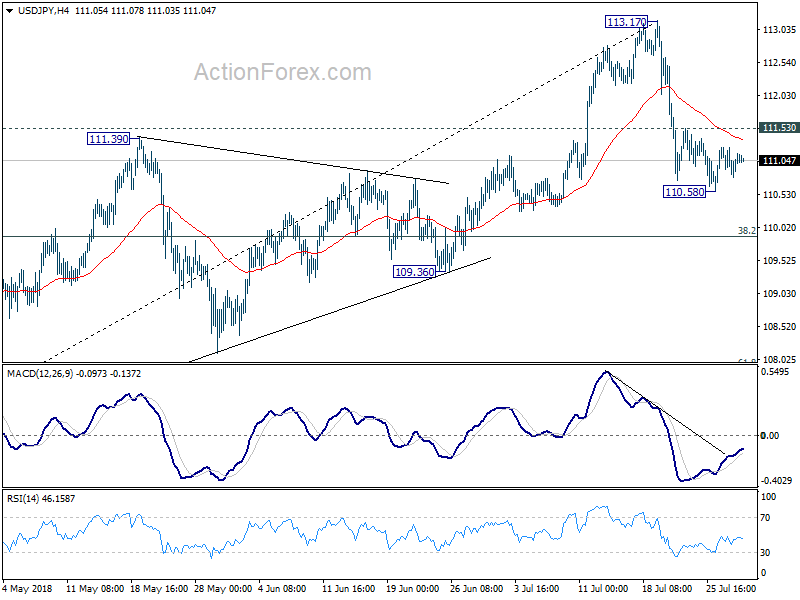

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.79; (P) 111.02; (R1) 111.26; More...

USD/JPY is staying in consolidation from 110.58 temporary low. Intraday bias remains neutral first. Still, as long as 111.53 minor resistance holds, correction from 113.17 could extend lower. Below 110.58 will turn bias to the downside. But we'd expect strong support from 38.2% retracement of 104.62 to 113.17 at 109.90 to bring rebound. On the upside, break of 111.53 will turn bias to the upside for retesting 113.17 high.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.