Sample Category Title

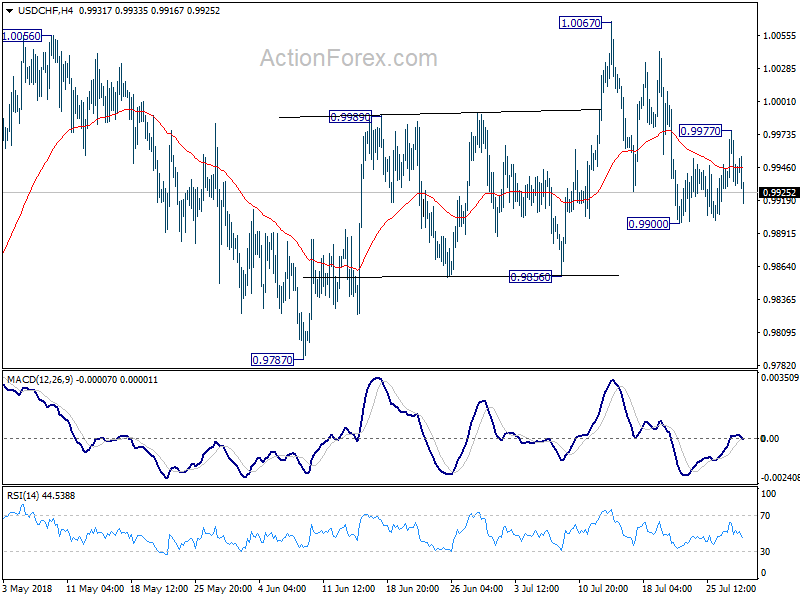

USDCHF: Bearish, Targets Further Weakness

USDCHF - The pair saw a price weakness during early trading on Monday opening the door for more correction. On the downside, support lies at the 0.9900 level. A turn below here will open the door for more weakness towards the 0.9850 level and then the 0.9800 level. On the upside, resistance resides at the 0.9950 level where a break will clear the way for more strength to occur towards the 1.0000 level. Further out, resistance comes in at the 1.0050 level. Above here if seen will turn attention to 1.0100. All in all, USDCHF faces further downside pressure

CAC Subdued Over Lack of Fundamentals

The CAC index has posted considerable gains in the Monday session. Currently, the CAC is at 5502, down 0.17% on the day. On the release front, there are no French or eurozone events on the schedule. On Tuesday, France releases CPI and the eurozone will publish inflation and GDP reports.

European equity markets had a strong week and the CAC joined the bandwagon, posting strong gains of 2.4 percent. Investors responded positively to last week’s meeting between EU Commission President Jean-Claude Juckner and U.S. President Trump. The two leaders agreed to take concrete steps to eliminate tariffs and improve the trade relationship between the U.S and the EU, which has been battered in recent weeks. Most importantly, Trump agreed to hold off on threatened tariffs against European car manufacturers, pushing the shares of French car makers higher and boosting the CAC.

French indicators ended the week on a disappointing note. Flash GDP for the second quarter dipped to 0.2%, shy of the forecast of 0.3%. This marked the smallest gain since Q3 of 2016. There was no relief from consumer spending, which dropped from 0.9% to 0.1% in June, short of the estimate of 0.6%. There could be more bad news on Tuesday when France releases Preliminary CPI. The indicator is expected to decline 0.3%. If this forecast is accurate, it will be yet another indication that the French economy has hit some nasty headwinds in the second quarter.

Canadian Dollar Trading Sideways, GDP ahead

The Canadian dollar is showing little movement in the Monday session. Currently, USD/CAD is trading at 1.3047, down 0.06% on the day. There are no Canadian indicators on the schedule. In the U.S, Pending Home Sales is forecast to rebound with a gain of 0.4%, after two straight declines. Tuesday will be busy on both sides of the border. The U.S will publish consumer spending and inflation indicators, as well as CB Consumer Confidence. Canada will release GDP for the second quarter and the Raw Materials Price Index.

U.S indicators ended the week on a bright note, but the Canadian dollar held its own on Friday against the strong U.S currency. Advance GDP, the first of three GDP reports in the second quarter, posted a strong gain of 4.1%, just shy of the forecast of 4.2%. This was much stronger than the gain of 2.2% in Q1 and marked the strongest quarter of economic growth since 2014. As well, UoM Consumer Sentiment dipped lower to 97.9 but still beat the estimate of 97.1 points. President Trump took credit for the strong GDP report and claimed that “these numbers are very, very sustainable”. However, analysts are being more cautious in their forecasts, calling for growth in the third quarter of around 2.5 percent.

Negotiations over NAFTA have progressed slowly, but policymakers in Canada and Mexico are hopeful that the flexibility that the U.S has shown towards the European Union will extend to NAFTA as well. Last week, President Trump met with EU Commission President Jean-Claude Juckner and announced that the U.S would hold off any further tariffs while the sides were negotiating. Will this goodwill extend to NAFTA as well? The U.S has insisted on far-reaching changes to the pact, including its renegotiation in five years and higher U.S content in automobiles produced in North America. If its demands aren’t met, the Trump administration has said it could pursue separate free trade agreements with Canada and Mexico. However, the latter two countries would like to maintain a trilateral arrangement. If the parties do reach a new agreement, the Canadian dollar would likely move higher.

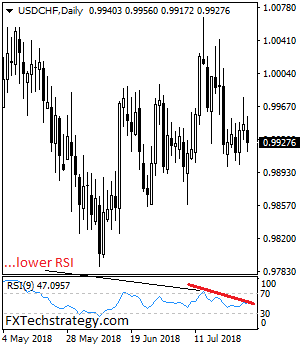

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9923; (P) 0.9951; (R1) 0.9974; More...

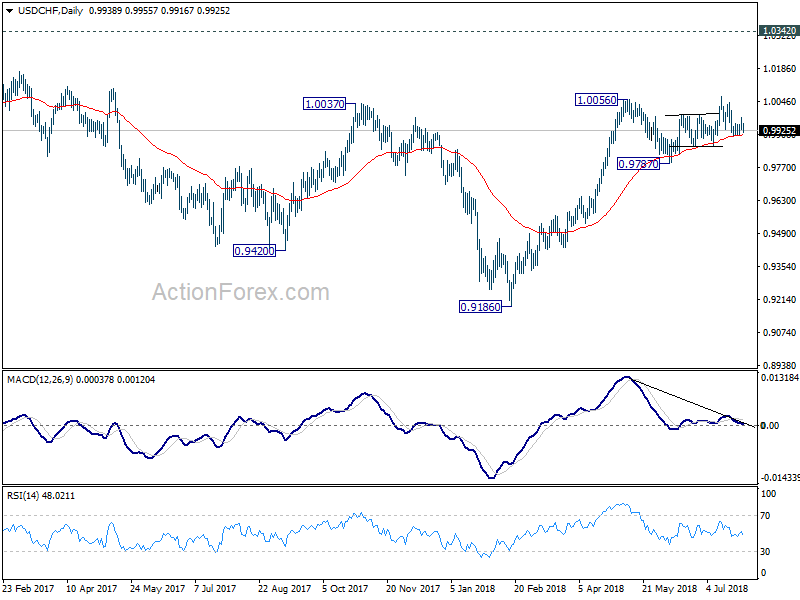

USD/CHF's retreat from 0.9977 extend lower today and focus is back on 0.9900 minor support. Break will resume the fall from 1.0067 and target 0.9856 support first. On the upside, break of 0.9977 will reaffirm the case that pull back from 1.0067 is completed. And, intraday bias will be back on the upside for retesting 1.0067. Firm break there will resume whole rally from 0.9186.

In the bigger picture, as long as 0.9787 support holds, we're favoring the bullish case. That is, rise from 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

Unclear Direction in Forex Markets, Yen Softer ahead of BoJ

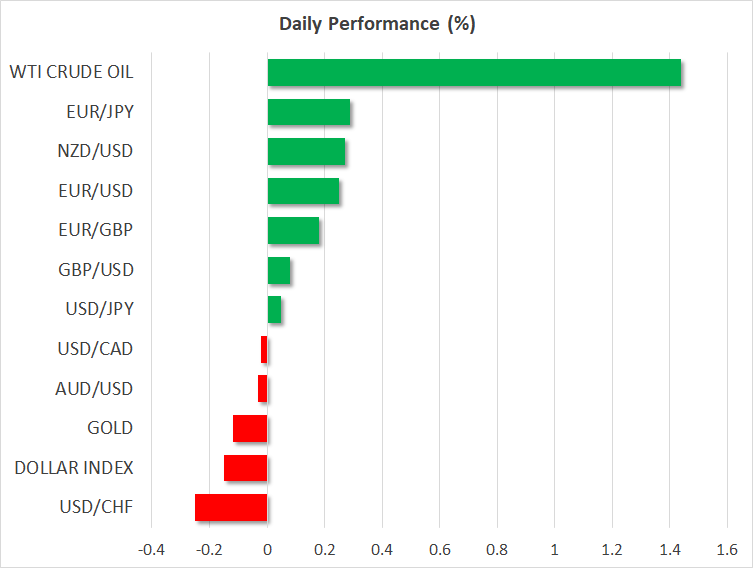

Euro and Swiss Franc are lifted in earlier today but was then out-performed by New Zealand Dollar. On the hand, Yen and Australian Dollar are trading as the weakest ones, followed by Dollar. Direction in the forex markets is relatively unclear as traders turned a bit cautious ahead of the long list of heavy weight events ahead. It starts with BoJ rate decision tomorrow and then we'll have US PCE, ISM and NFP, FOMC, BoE, UK PMIs, Eurozone CPI etc. Yen's softness, despite resilience in JGB yield and mild risk aversion, could be explained by such cautiousness ahead of BoJ. In other markets, WTI crude oil is picking up momentum in recovery and breaches 70 handle. Gold continues to struggle around 1220.

Technically, Dollar's weakness today now put 0.9900 in USD/CHF and 1.3032 in USD/CAD into focus. Recovery in EUR/JPY and GBP/JPY indicates temporary bottoming. But break of 130.25 and 146.51 minor resistance respectively is needed to indicate near term reversal. As Sterling lags behind Euro and Swiss Franc, 1.3070 minor support in GBP/USD will remain a focus for the session.

BoJ policy decision in focus in upcoming Asian session

BoJ rate decision is a major focus in the upcoming Asian session. It's widely expected to keep monetary policy unchanged. Under the Yield Curve Control framework, short term policy rate should be held at -0.10%. Target on 10 year JGB yields will also remain at around 0%. ut recently, there are speculations that BoJ could widened the back for 10-year JGB yield targets, probably up to 0.1%. That's a key factor in driving up JGB yields as well as the Japanese Yen. At this early stage of discussion, we don't think there is enough consensus for BoJ to make a decision. A change in their statement will be a big surprise to the markets.

Today, BoJ offered to buy 10 year JGBs at 0.10% yield again, the third operation of such kind in just over a week. A record JPY 1.64T of JGBs were purchase, surpassing the prior record of JPY 724B in February.

Released in Japan retail sales rose 1.8% yoy in Jun, above expectation of 1.7% yoy.

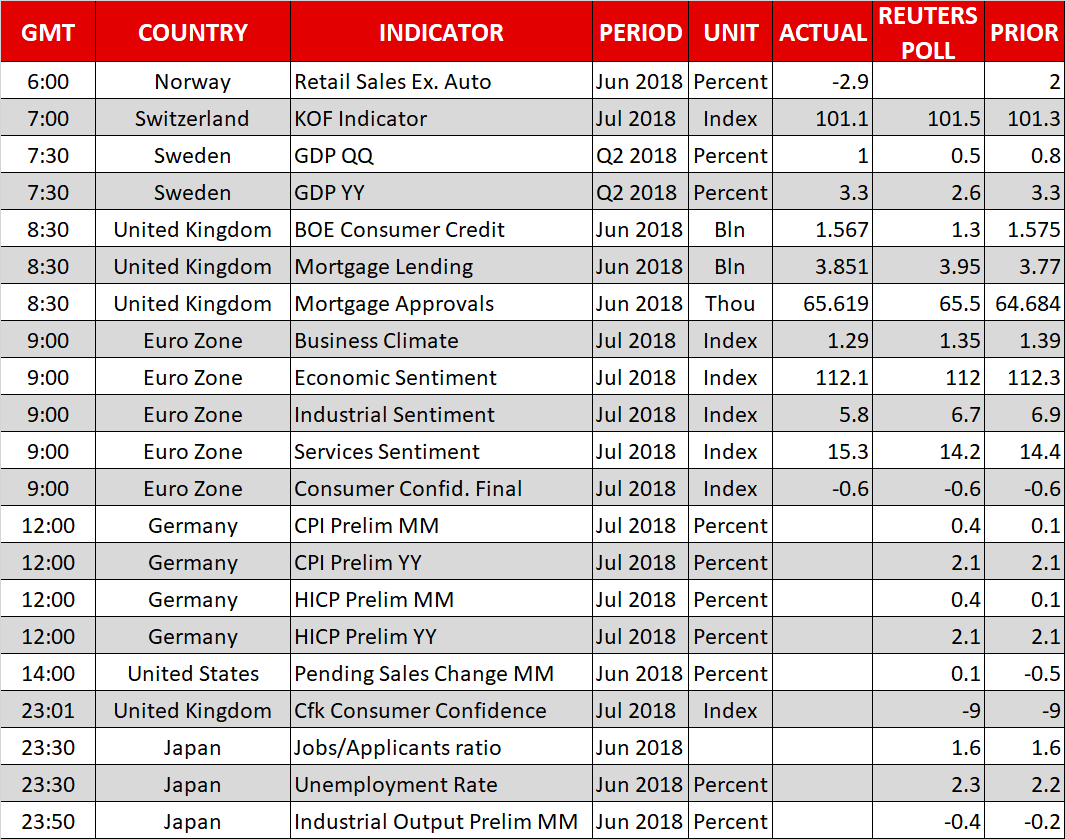

Swiss KOF dropped to 101.1, still slightly above long term average of 100

Swiss KOF Economic Barometer dropped -0.2 to 101.1 in July, below expectation of 101.5. The reading still sit slightly above the long-term average of 100, indicating a slightly above-average economic development in Switzerland in the coming months. KOF noted in the release that "negative indicators for manufacturing, the export industry and the accommodation and food service activities sector were mainly responsible for the slight decrease." On the other hand, "positive signals come from the banking and the construction sectors.".

Also release in European session, UK mortgage approvals rose 1k to 66k in June, M4 money supply dropped -0.3% mom. Eurozone business climate dropped to 1.29 in July, missed expectation of 1.35. Economic confidence dropped -0.2 to 112.1, above expectation of 112.0. Industrial confidence dropped 1.1 to 5.8, below expectation of 6.7. Services confidence rose 0.9 to 15.3, above expectation of 14.2. Consumer confidence was finalized at -0.6. German CPI slowed to 2.0% yoy in July, below expectation of 2.1% yoy.

BoE Carney: We can choose between low road of protectionism or high road of trade liberalization

BoE Governor Mark Carney said in a Bloomberg interview that the world could choose between a "low road of protectionism focused on bilateral goods-trade balances" and a "high road of liberalization of global trade in services." But he warned that the "low road will cost jobs, growth, and stability". Meanwhile, the "high road can support a more inclusive and resilient globalization." Carney said that the trade actions taken by Trump as of June had small impacts. But "a larger increase in tariffs would have a substantial impact".

Domestically, Carney said that it's "more likely than not" that the equilibrium interest rates have risen. But "any given jurisdiction has to take into account its own domestic forces, whether there are headwinds from fiscal policy, headwinds from uncertainty, headwinds from trade discussions or other factors."

He also played down the chance of other EU countries replicating London's success as a global financial center. He said, "in some circles in Europe there is a greater predisposition to ring-fence financial activities," and "that could lead to a very large but effectively local financial center in Europe, as opposed to a global financial center, which I believe London will continue to be."

UK Foreign Minister Hunt said China offered talks on post Brexit FTA

New UK Foreign Minister Jeremy Hunt met with China's Foreign Minister Wang Yi in Beijing today. After the meeting, Hunt said China made an offer to "to open discussions about a possible free trade deal done between Britain and China post Brexit". And he added that "that's something that we welcome and we said that we will explore." Wang didn't mention the free trade talks directly. But he said both countries had "agreed to proactively join up each others' development strategies, and expand the scale of trade and mutual investment".

Wang: China not to blame for trade imbalance with US

Separately, Wang said that "the responsibility for the trade imbalance between China and the United States lies not with China." And he cited the global role of the US Dollar, low saving rates, high level of consumption and US restrictions on high tech exports as some of the reasons for the imbalances. He also reiterated the stance that "China does not want to fight a trade war, but in the face of this aggressive attitude from the United States and violation of rights, we cannot but and must take countermeasures."

CNY depreciation reflect fundamentals, not trade war tactic

Renminbi's depreciation since April this year has accelerated over the past two months. While USDCNY has in aggregate rallied over +6% in June and July, renminbi's weakness was less pronounced against a basket of currencies. The CEFTS index, the official reminbi index, fell -4.4% over the past two months.

As US-China trade conflicts intensify, there has been much speculation that China is weakening its currency as a retaliatory measure in face of Trump's tough tariffs. Many even cited the recent rapid selloff of renminbi as evidence. We agree that there is such a phenomenon that the Chinese government tends to allow its managed-float currency to decline more than rise.

However, we believe the recent renminbi weakness is more driven by slowdown in Chinese economic growth, the shift of Chinese policy (both fiscal and monetary) to the loosening side and the consequential monetary policy divergence between the Fed and PBOC.

For the months ahead, we expect risk remains skewed to the downside for renminbi. However, the Chinese government would carefully calibrate it so that the disastrous selloff back in 2H11 would not repeat.

More in Renminbi Depreciates as a Result of Economic Weakness and Loosening Policies

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9923; (P) 0.9951; (R1) 0.9974; More...

USD/CHF's retreat from 0.9977 extend lower today and focus is back on 0.9900 minor support. Break will resume the fall from 1.0067 and target 0.9856 support first. On the upside, break of 0.9977 will reaffirm the case that pull back from 1.0067 is completed. And, intraday bias will be back on the upside for retesting 1.0067. Firm break there will resume whole rally from 0.9186.

In the bigger picture, as long as 0.9787 support holds, we're favoring the bullish case. That is, rise from 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Jun | 1.80% | 1.70% | 0.60% | |

| 07:00 | CHF | KOF Leading Indicator Jul | 101.1 | 101.5 | 101.7 | 101.3 |

| 08:30 | GBP | Mortgage Approvals Jun | 66K | 66K | 65K | |

| 08:30 | GBP | Money Supply M4 M/M Jun | -0.30% | 0.60% | 0.40% | |

| 09:00 | EUR | Eurozone Business Climate Indicator Jul | 1.29 | 1.35 | 1.39 | 1.38 |

| 09:00 | EUR | Eurozone Economic Confidence Jul | 112.1 | 112 | 112.3 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | 5.8 | 6.7 | 6.9 | |

| 09:00 | EUR | Eurozone Services Confidence Jul | 15.3 | 14.2 | 14.4 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -0.6 | -0.6 | -0.6 | |

| 12:00 | EUR | German CPI M/M Jul P | 0.30% | 0.40% | 0.10% | |

| 12:00 | EUR | German CPI Y/Y Jul P | 2.00% | 2.10% | 2.10% | |

| 14:00 | USD | Pending Home Sales M/M Jun | 0.20% | -0.50% |

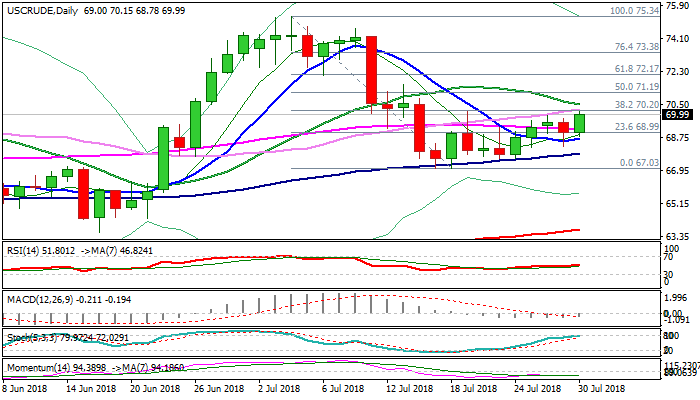

WTI Oil Outlook: Fresh Strength Pressures Key Barrier at $70.20

WTI oil regained traction on Monday and probes above psychological $710 barrier for the first time since 19 July. Worries about global supply continue to underpin oil prices but support is partially offset by lowered tension about global trade war. Today's rally improves daily techs as the price broke above 55SMA and 14-d momentum is attempting to create a bull-cross with its 7-d MA, but slow stochastic is entering overbought zone and may reduce rally's pace. Recovery extension is pressuring pivotal barrier at $70.20 (Fibo 38.2% of $75.34/$67.03, reinforced by 30SMA/19 July strong upside rejection), break of which is needed to further improve near-term outlook on bullish signal that would be generated on clear break higher. Extension above $70.20 and falling 20SMA ($70.51) would open way for stronger recovery and expose barriers at $71.19 (50% of $75.34/$67.03) and $71.64 (13 July lower top). On the other side, overbought conditions may result in stronger hesitation at $70.20 barrier, with subsequent dips expected to find footstep above broken 55SMA ($69.19) and keep bullish near-term bias. Bearish scenario requires confirmation on break and close below north-turning 10SMA ($68.70) to expose rising 100SMA ($67.83) and risk retest of key near-term support at $67.03 (17/18 July lows).

Res: 70.20; 70.51; 71.19; 71.64

Sup: 69.19; 68.78; 68.24; 67.83

Renminbi/Chinese Yuan Depreciates as a Result of Economic Weakness and Loosening Policies

Renminbi’s depreciation since April this year has accelerated over the past two months. While USDCNY has in aggregate rallied over +6% in June and July, renminbi’s weakness was less pronounced against a basket of currencies. The CEFTS index, the official reminbi index, fell -4.4% over the past two months. As US-China trade conflicts intensify, there has been much speculation that China is weakening its currency as a retaliatory measure in face of Trump’s tough tariffs. Many even cited the recent rapid selloff of renminbi as evidence. We agree that there is such a phenomenon that the Chinese government tends to allow its managed-float currency to decline more than rise. However, we believe the recent renminbi weakness is more driven by slowdown in Chinese economic growth, the shift of Chinese policy (both fiscal and monetary) to the loosening side and the consequential monetary policy divergence between the Fed and PBOC. For the months ahead, we expect risk remains skewed to the downside for renminbi. However, the Chinese government would carefully calibrate it so that the disastrous selloff back in 2H11 would not repeat.

Slowdown in Chinese Economic Growth

As we have shown in previous China Watch reports, growth in China’s macroeconomic activities has been moderating and the pace of slowdown has accelerated in the second quarter. Concerning the latest data, industrial production (IP) expanded +6% y/y in June, missing consensus of +6.5% and May’s +6.8%. Retail sales grew +9% y/y, in line with expectations and improving from +8.5% recorded in May. Urban fixed asset investment grew +6% y/y, in line with expectations and continuing with the downtrend resulting from government’s deleveraging efforts. With the exception of IP growth, June’s data met expectations, compared with the downside surprises recorded in April and May. These culminated to the second quarter GDP growth of +6.7%, easing from +6.8% in the first quarter. Headline CPI edged slightly higher to +1.9% y/y in June, from +1.8% in the prior month. Inflation has stayed way below PBOC’s target of +3%. On liquidity conditions, M2 money supply surprised to the downside in June, rising only +8% whereas the market had anticipated a +8.3% growth.

Looser, or Less Tight Policy (Both Fiscal and Monetary) Stance

PBOC has made some unexpected moves in recent months with the latest surprise coming from the injection of RMB 502B through 1-year medium-term lending facility (MLF) last week (July 23). Apart from being the biggest MLF exercise on record, the significance of the move was that this MLF is NOT refinancing maturing facilities, unlike the one implemented on July 13. This happened only a few days after PBOC announced that it would provide MLF funding for new bank purchases of corporate bonds.

Meanwhile, the State Council announced, also on July 23, that it would be “more pro-active in adopting the proactive fiscal policy” (積極財政政策要更加積極). However, it refrains from bringing a “flood of stimuli” (“大水漫灌“式強刺激)to the market. As such, we do not expect to experience the huge government spending adopted in 2011.

The State Council laid down four key areas of stimulus. First, the “proactive” fiscal policy focuses on tax cut. Second, more flexibility on easing or tightening is needed in adopting the prudent monetary policy. The aim is to encourage financial institutions to lend money, through lowering RRR, issuance of small and micro enterprise financial bonds with few or no continuous profit requirements, etc., to local governments in support of completion of infrastructural projects. Third, implementation of the National Guarantee Fund plan should speed up so as to provide RMB 140B in funding for SMEs. Fourth, zombie firms have to be eliminated. While the statement reiterated that the bottom-line remains prevention of systematic risk, it made no mention of “deleverage” anymore.

Monetary Policy Divergence between the Fed and PBOC

Apart from not raising interest rates after the Fed’s rate hike in June, PBOC cut RRR by -50 bps on July 5, injecting about RMB 700B of liquidity to the market. More RRR cut in coming months should be consistent with the Chinese government’s aim to fund local governments. Concerning the Fed, two more rate hikes remain on the pipeline. Economic developments continue to support gradual rate hikes in the coming year. The preliminary estimate of US GDP growth accelerated to an annualized +4.1% in 1Q17, marking the fastest pace since 2014. Donald Trump’s reckless complaint on Fed’s monetary policy should make no influence on the rate hike path.

Reference: http://www.gov.cn/premier/2018-07/23/content_5308588.htm

Busy Week Gets Off to a Slow Start

- Investors encouraged by Trump/Juncker meeting;

- BoE seen raising rates while Fed and BoJ also meet;

- US jobs report bring hectic week to a close.

Equity markets are trading slightly in the red in what has been a slow start to an otherwise very busy week in financial markets.

Stock markets have been gradually rising in recent weeks, making their way back to the record high levels they achieved earlier in the year before the numerous trade conflicts involving the US heated up. The apparent progress made at the White House last week between Donald Trump and Jean-Claude Juncker has eased some concerns for now but the threats generally remain.

Earnings season has delivered a positive distraction for investors, with companies once again reporting stellar quarterly results aided by the obvious benefit of tax cuts. We’ll get results from another 144 S&P 500 companies this week as US corporates look to continue the positive momentum of earnings season so far and potentially propel the index to a new high.

There’s also a number of central bank meetings this week, the most notable of the lot probably being the Bank of England with investors widely expecting a rate hike, taking the benchmark rate above 0.5% for the first time since early 2009. A rate hike is now 86% priced in which could trigger a lot of volatility if policy makers once again hold off, as they did back in May.

The Federal Reserve and Bank of Japan will also hold meetings this week although these events may be less eventful, with neither seen adjusting policy this month. The Fed is also on a very clear tightening path and with the economy performing in line with expectations and the trade conflicts not yet biting, I don’t expect there to be any change in the central bank’s stance.

There has been speculation that the BoJ may look to slightly remove accommodation by increasing the yield it will allow the 10-year to reach, although I’m not sure that will come this week. Investors appear to be testing the BoJ’s resolve, with the yield having hit its highest level since February last year. Should the central bank reject the speculation, I would expect this to quickly reverse course.

This week also sees the release of the US jobs report which is widely regarded to be the most important economic report of the month and is typically a trigger for market volatility.

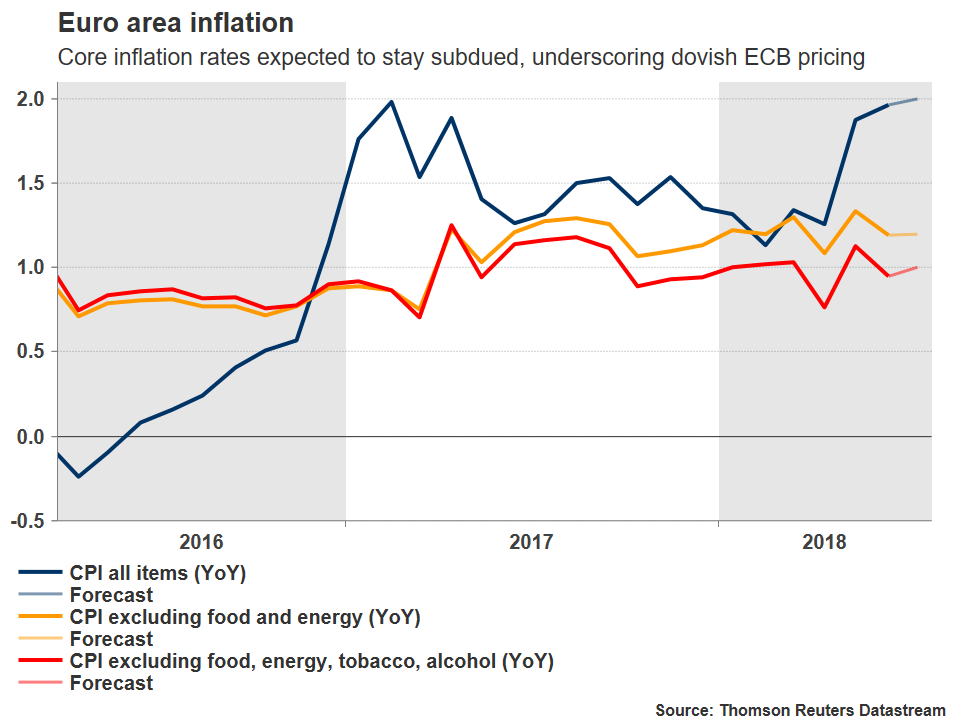

Eurozone’s Inflation and GDP Numbers Set to Guide the Euro

The Eurozone will see the release of its preliminary inflation data for July, as well as the first look at GDP for Q2, both on Tuesday at 0900 GMT. Forecasts are pointing to largely unchanged inflationary pressures and economic growth, something likely to solidify dovish expectations around ECB rate hikes, potentially keeping any advances in the euro limited for now.

The euro is still licking its wounds following the latest European Central Bank (ECB) meeting last week, where President Draghi endorsed the relatively dovish market pricing around a potential rate increase late next year. He was essentially seen as applauding the fact there is some uncertainty involved with current pricing, highlighting that the Bank wants to keep its options open and not pre-commit to anything so early. As a result, bets for a 10bps rate increase in September next year faded a little, with the implied probability for one now resting at 69%, EONIA swaps and Euribor futures suggest. That said, markets are much more confident that such a move will occur by October 2019, something that is fully priced in already.

This week’s data dump out of the Eurozone seems unlikely to alter this pricing in a material manner, at least according to forecasts. In July, preliminary figures are projected to show that the bloc’s headline inflation rate held steady at 2.0% in yearly terms. The core CPI rate which excludes energy and food items is also anticipated to remain at 1.2%, while the measure that also ignores tobacco and alcohol is forecast to tick up to 1.0% on a yearly basis, from 0.9% previously. As for GDP growth, it’s expected to come in at 0.4% in quarterly terms in Q2, unchanged from Q1. This would drag the yearly growth rate down to 2.2%, from 2.5% previously. The bloc’s unemployment rate for June is also due out.

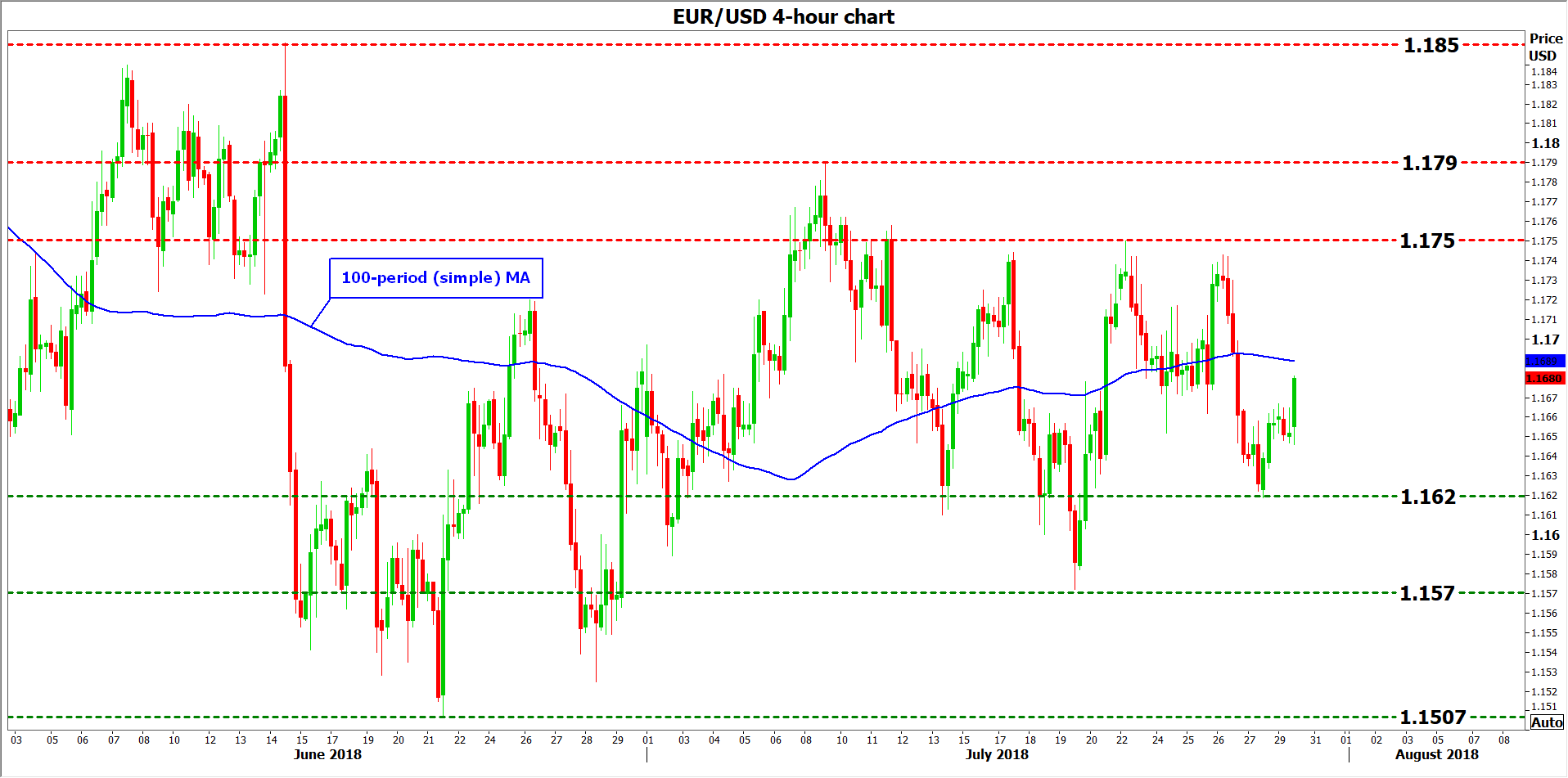

In case these data come in stronger than projected, particularly on the core inflation and GDP fronts, markets could become a little more confident regarding the likelihood of a September 2019 ECB rate hike and hence, push the euro a little higher. Technically, looking at euro/dollar, a first line of resistance in case of advances is likely to be found around 1.1750, the peak of July 23, with the area around it also encapsulating a few tops from the recent past. An upside break could open the way for the 1.1790 zone, marked by the July 9 top, with even greater advances opening the way for the June 14 top of 1.1850.

On the downside, and in case of a data miss that turns investors even more pessimistic around a September 2019 rate hike, immediate support to declines may come from 1.1620, the low of July 27. Even lower, the July 19 trough of 1.1570 would come into view, before the 1.1506 hurdle attracts attention.

Note that the US will also release crucial data just a few hours after the Eurozone. Those can also move the pair.

European Equities and Greenback Lose Ground, German Inflation Coming Up

Here are the latest developments in global markets:

FOREX: The dollar index, which gauges the greenback against a basket of six major currencies, was trading lower by around 0.2%, with euro/dollar being up by roughly the same proportion and trading around 20 pips below the 1.17 handle. The reaction to business and consumer confidence surveys out of the eurozone was minimal, with the focus being on German inflation figures which may act as the preamble to tomorrow’s respective numbers out of the eurozone. Dollar/yen was close to flat and not far above the 111 level, with the immediate focus being on the outcome of the Bank of Japan’s meeting due on Tuesday. Pound/dollar traded marginally higher at 1.3111; the Bank of England meeting on Thursday is eyed, with Brexit uncertainty remaining in the background. Meanwhile, the Swedish krona was elevated on better-than-anticipated Q2 GDP figures out of Sweden; USDSEK was down by 0.9% and EURSEK lower by 0.7% at 1110 GMT.

STOCKS: Major European benchmarks traded lower for the most part, though their losses were limited in magnitude. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.2% and 0.3% respectively. Meanwhile, the UK’s FTSE 100, German DAX and the French CAC 40 were trading lower by 0.1%, 0.2% and 0.25% correspondingly. Some disappointment on the earnings front, in conjunction with negative sentiment on the back of considerable losses from big US tech stocks on Friday, acted as the catalysts for the decline in European equities. In US stocks, futures tracking the Dow were up by 0.1%, those on the S&P 500 were marginally lower, while contracts on the tech-heavy Nasdaq 100 traded down by 0.1%. Caterpillar’s earnings are expected soon; before Wall Street’s opening bell.

COMMODITIES: WTI oil was supported on the back of a draft proposal to scale back on US automobile efficiency requirements that has the potential to boost fuel consumption. The benchmark was last up by 1.4% at $69.70 per barrel. Meanwhile, Brent crude was trading higher by 0.7% at $74.79 a barrel. In precious metals, gold was little changed at $1,222.46 per ounce, trading not far above its lows for the year, at roughly $1,211.

Day ahead: German inflation coming up; US pending home sales also due; Bank of Japan in focus

Important releases as the day unfolds will be the advance estimates of German inflation for July. Meanwhile, pending home sales data out of the US will attract some interest, while Tuesday’s Asian calendar will be a busy one, featuring among others the much-awaited outcome of the Bank of Japan’s latest policy meeting.

July’s preliminary inflation data out of Germany, the eurozone’s largest economy, are due at 1200 GMT. Inflationary pressures as gauged by the consumer price index (CPI) are anticipated to grow by 0.4% m/m, reflecting an acceleration compared to June’s 0.1%. In yearly terms, CPI is forecast to expand by 2.1% y/y, the same pace as in June. The Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, will also be generating interest.

It is of note that the abovementioned figures are coming one day ahead of the eurozone’s corresponding numbers and may thus be seen as giving an indication as far as tomorrow’s release is concerned; in other words, euro pairs may prove sensitive to the German prints. Meanwhile, flash Q2 GDP growth numbers for the eurozone, as well as June’s unemployment rate, will be released alongside euro area inflation readings on Tuesday at 0900 GMT.

Out of the US, pending home sales are slated for release at 1400 GMT; sales are expected to increase by 0.1% m/m in June, after declining by 0.5% in May.

US Secretary of State Mike Pompeo, Commerce Secretary Wilbur Ross and Energy Secretary Rick Perry will be speaking at the Indo-Pacific Business Forum at 1230 GMT. In the meantime, President Trump is scheduled to meet Italian PM Guiseppe Conte at the White House.

Tuesday’s Asian session will be rather packed, including household spending numbers, industrial production figures, as well as data on employment (and unemployment) out of Japan. China will be on the receiving end of readings on manufacturing and services PMI, while business confidence and building approval prints are due out of New Zealand and Australia respectively.

However, the Bank of Japan’s meeting on monetary policy, which is to be concluded tomorrow, is attracting the lion’s share of attention out of Asia. Since around mid-July, the yen has benefitted on the back of growing speculation that the Japanese central bank will adjust its monetary policy framework in a manner that is supportive of a stronger yen. Should this indeed materialize, then the currency is likely to post further gains. It should be kept in mind though, that economic releases that include subdued inflation and weak household spending, are not lending credence to a hawkish tilt by the BoJ. Should the Bank not deliver to the somewhat “hawkish positioning” by markets, then the yen may be in for a sharp sell-off.