Sample Category Title

The US Dollar Weakened Despite Data On GDP

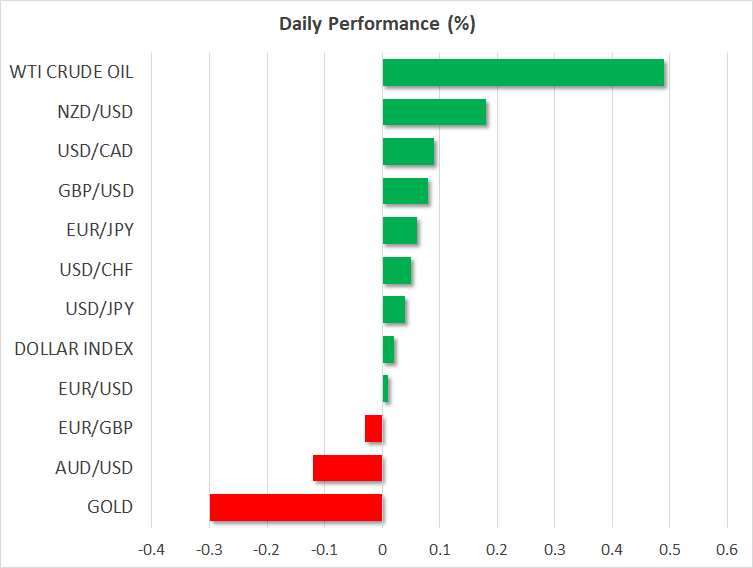

On Friday, the US currency weakened against the basket of major currencies despite a positive report on GDP. The GDP index rose to 4.1% in the second quarter, as experts expected. The growth of the US economy gives grounds for the Fed to adhere to a gradual increase in the interest rate. However, the tension between the US and trading partners remains. The US dollar index (#DX) closed in the negative zone (-0.08%).

This week, economic reports from the US, Japan, the Eurozone and the UK will be in the focus of attention. Also, the conflict between the US and China is still not closed. It is expected that on Wednesday the United States will introduce again additional duties on Chinese goods $16 billion worth. China is likely to respond the same. We recommend following the economic calendar, as well as the trade war.

The "black gold" prices are consolidating. At the moment, futures for the WTI crude oil are testing a mark of $69.00 per barrel.

Market Indicators

On Friday, the bearish sentiment was observed in the US stock market: #SPY (-0.68%), #DIA (-0.34%), #QQQ (-1.35%).

At the moment, the 10-year US government bonds yield is at the level of 2.96-2.97%.

The news feed on 2018.07.30:

- German consumer price index at 15:00 (GMT+3:00);

- Pending home sales index in the US at 17:00 (GMT+3:00).

Markets Await BOJ Announcement Tomorrow

- General Trend: Asian equity markets trade mostly lower, in line with Friday’s US session

- Chinese equities move between gains and losses

- Shares of Tencent hit lowest level since Dec, decline over 2% on session

- Nasdaq Futures extend losses

- BMW raised prices in China on tariff impact

- Cautious trading for the Nikkei ahead of Tuesday’s BoJ decision and forecasts

- BoJ acts again to slow rise in yields

- PBOC skipped OMO for the 7th straight session, says month-end fiscal spending to support liquidity

- PBoC set the yuan weaker: The Chinese currency faces increasing short-term depreciation risk (Chinese press)

- There is renewed speculation that China might cut the RRR in H2 (Chinese Press)

- Japanese companies which may today report earnings include Sumitomo Mitsui Financial, Aozora Bank, Daiwa Securities, Mitsubishi Electric, Japan Exchange, Oriental Land, TDK, TEPCO, Shionogi and Capcom.

- China official July PMI data due on Tuesday

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.4%

- (JP) BOJ AGAIN CONDUCTS FIXED-RATE JGB PURCHASE OPERATION FOR an unlimited amount of 5-10-YR JGBs at 0.10% (3rd operation within the past week)

- TOPIX Retail Trade index -0.7%, Information and Communications -0.6%, Real Estate -0.6%; Marine Transportation +0.8%

- Japanese megabanks outperform ahead of earnings from Sumitomo Mitsui and BoJ policy decision

- (JP) Japan Jun Retail Sales m/m: 1.5% v 1.5%e; Retail Trade y/y: 1.8% v 1.7%e

- Inpex, 1605.JP Notes start of gas production at the Ichthys project, sees start of shipments towards the end of H1 FY18

- JGB (JP) Japan 10-year JGB yield near 0.105%

- Mitsubishi Electric, Reports Q1 Net ¥47.6B v ¥56.9B y/y; Op ¥61.6B v ¥75.5B y/y; Rev ¥1.05T v ¥1.03T y/y; Affirms guidance

Korea

- Kospi opened -0.2%

- E-Mart, 139480.KR New discount store seeing an avg of 10K customers per day; sales have easily exceeded initial target in 1st month of opening - Korean press

- (KR) South Korea Industry Min Paik announces KRW1.5T investment over the next 10-yrs to maintain chip industry competitiveness - Korean press

- (KR) South Korea Jun Department Store Sales y/y: 5.4% v 1.8% prior; Discount Store Sales y/y: +0.2% v -4.5% prior

China/Hong Kong

- Hang Seng opened -0.6%, Shanghai Composite -0.1%

- Hang Seng Info Tech index -2.3%, Consumer Goods -1.6%, Services -0.9%, Energy -0.6%, Financials -0.5%

- (CN) China Securities Journal Commentary: PBoC may lower the reserve ratio requirement (RRR) in Q3

- (CN) China CNY currency (Yuan) faces increasing depreciation risk in the short-term - China Securities Journal

- (CN) China targeted policy does not mean boost for property market - Chinese Press

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 7th consecutive session; Net drains CNY130B v drains CNY0B prior

- (CN) China PBoC sets yuan reference rate at 6.8131 v 6.7942 prior

- USD/CNY trades above 6.84 for the first time since late June 2017

- (CN) China State Councillor Wang Yi: China and US should solve trade frictions in WTO framework; China remains open to dialogue

Australia/New Zealand

- ASX 200 opened -0.0%

- ASX 200 Resources index -0.8%, Financials -0.6%; Telecom +1%

- (AU) Australia held special elections in 4 states to fill seats emptied by dual citizenship issues, results saw no changes and general election in 2018 less likely

- RMS.AU Guides initial FY19 gold production 200-220K ozs at AISC of A$1,150-1,250/oz, Guides Q1 50-54K ozs at AISC A$1,250/oz

- (AU) Moody's: Smaller Australia banks raising home loan rates opening door for major banks to follow

- Pacific Edge, [+23%], PEB.NZ Accepted NZ$2.6M investment offer from Manchester Management Company, to issue ~8.2M shares at NZ$0.32/share

North America

- (US) US Supreme Court Justice Ginsburg has indicated she expects to remain on the court for 5 years or more - CNN

- (US) President Trump said to have told aides he "hates wind power" - US press

- (US) US Fed Researchers said to study metro-area data for clues on inflation during periods of low unemployment - US financial press

- (US) Canada, EU, Japan, Mexico and South Korea to meet in Geneva next week to discuss their response to Trump’s threat to impose tariffs on foreign auto imports - press

- CBS [CBS]: May create special committee of board to oversee investigation of accusations against CEO Les Mooves, board may discuss whether Moonves should 'step aside' pending a probe into the harassment allegations - US financial press

Europe

- (IT) Italy Deputy Prime Minister (PM) Di Maio said a referendum on whether Italy should leave the euro is not in the governing contract and will not be pursued – financial press

- BMW.DE To raise the prices of the X5 by 4% and X6 by 7% made in the US and sold in China in response to tariffs, effective July 30th - FT

- (UK) Foreign Sec Hunt: China and UK agree to explore post-Brexit free trade deal - Comments alongside China Foreign Min Wang Yi

Levels as of 01:30ET

- Hang Seng -0.8%; Shanghai Composite -0.3%; Kospi -0.2%; Nikkei225 -0.7%; ASX 200 -0.4%

- Equity Futures: S&P500 -0.3%; Nasdaq100 -0.5%, Dax -0.2%; FTSE100 -0.1%

- EUR 1.1650-1.1665; JPY 110.90-111.16; AUD 0.7386-0.7406;NZD 0.6792-0.6804

- Aug Gold -0.3% at $1,219/oz; Sept Crude Oil +0.3% at $68.89/brl; Sept Copper -0.7% at $2.78/lb

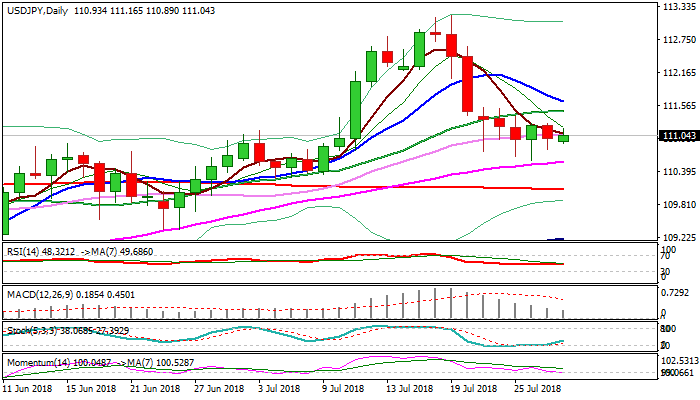

USDJPY Outlook: Congestion Extends Into Fourth Day, BoJ Policy Meeting On Tuesday Is In Focus

Early Monday’s action was so far in green as last week’s multiple downside rejections above key supports at 110.64 (50% of 108.11/113.17) and 110.57 (rising 55SMA), generated initial recovery signal.

However, the downside is still vulnerable as momentum is weak and the pair was so far unable to clearly break above 30SMA (111.08).

Stronger acceleration higher and break above pivots at 111.47 (20SMA) and 111.57 (Fibo 38.2% of 113.17/110.58 bear-leg) are needed to generate stronger recovery signal.

The pair may hold within congestion that extends into fourth straight day, awaiting BoJ policy meeting, due early Tuesday, which may provide further signals.

The central bank is expected to maintain its ultra-low interest rates but speculation about considering changes to its massive asset-purchase program may generate stronger direction signal.

Res: 111.16, 111.47, 111.57, 111.88

Sup: 110.89, 110.58, 110.07, 109.99

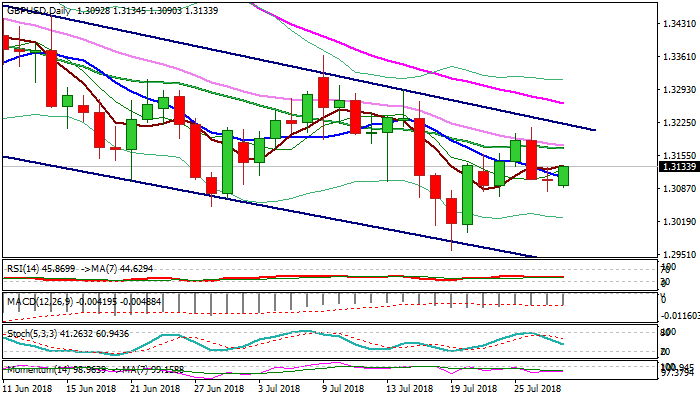

GBPUSD Outlook: Recovery Is Seen As Positioning As Bears Dominate, Central Banks Eyed For Stronger Signals

Cable moved higher in early European trading on Monday, following tight range in Asia.

Friday's action ended in Doji candle after failing to break Fibo 50% support at 1.3085, with subsequent bounce seen as positioning, as primary trend is negative and daily techs are in bearish setup.

Falling and widening hourly cloud (1.3128/51) marks solid resistance, which should ideally limit upticks and guard upper trigger at 1.3176 (converged 20/30SMA's).

Only break above 1.3219 (upper boundary of bear-channel) would sideline bears.

Central banks are in focus this week, with Fed coming on Wednesday and expected to signal the third rate hike this year in September's FOMC meeting, while the BoE's MPC is meeting on Thursday, with wide expectations for quarter point rate hike.

Res: 1.3151, 1.3176, 1.3219, 1.3263

Sup: 1.3085, 1.3071, 1.3055, 1.3000

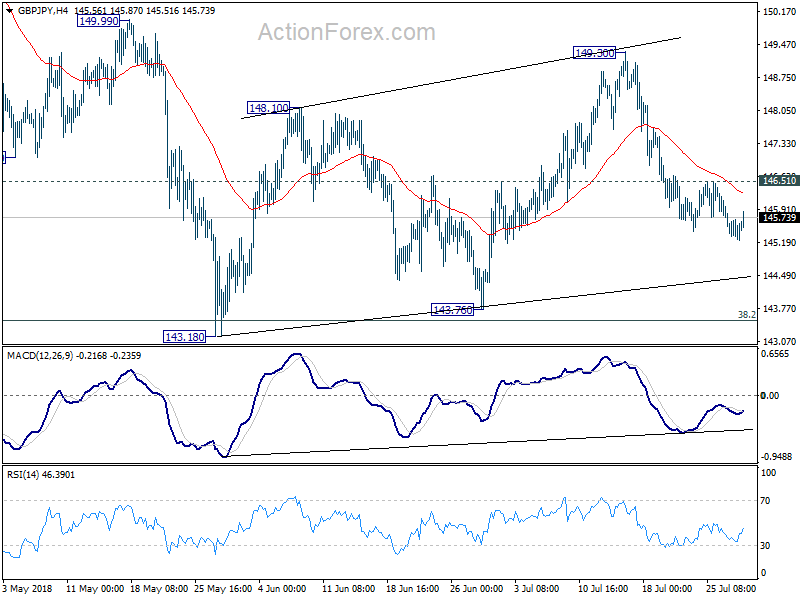

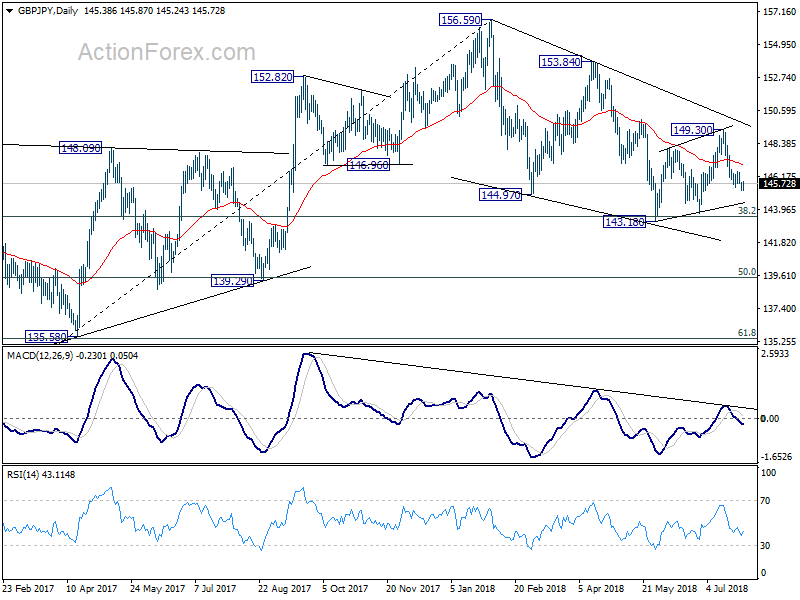

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.22; (P) 145.53; (R1) 145.79; More...

No change in GBP/JPY's outlook. With 14651 minor resistance intact, deeper fall is expected to 143.18/76 support zone. Break will resume larger decline from 156.59. On the upside, though, above 146.51 minor resistance will turn bias back to the upside for 149.30/99 resistance zone instead.

In the bigger picture, decline from 156.59 is seen as a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

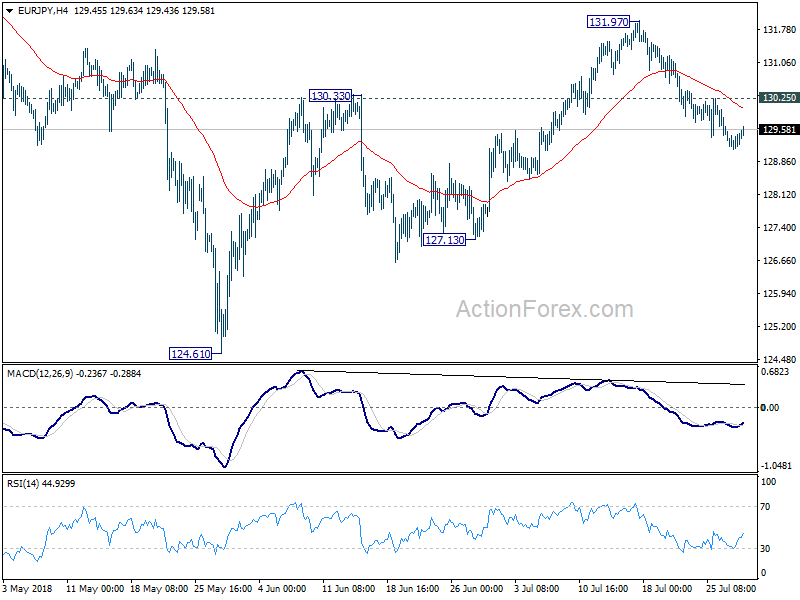

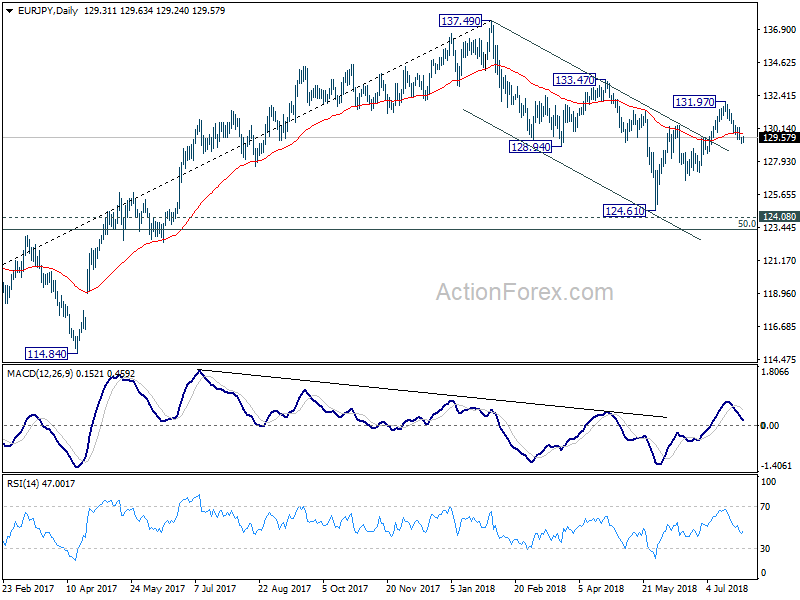

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.17; (P) 129.37; (R1) 129.62; More....

No change in EUR/JPY's outlook. With 130.25 minor resistance intact, deeper decline is expected to 127.13 support. The rebound from 124.61 should have completed with three waves up to 131.97 already. Break of 127.13 will confirm this bearish case and target a test on 124.61 low. On the upside, though, above 130.25 will bring retest of 131.97 instead.

In the bigger picture, for now, medium outlook remains cautiously bullish. the three wave structure of the fall from 137.49 to 124.61 argues that it's a correction. Also, 124.08 key resistance turned support was defended. Break of 133.47 resistance will affirm the bullish case that rise from 109.03 (2016 low) is still in progress for another high above 137.49. And this will remain the favored case as long as 127.13 support holds.

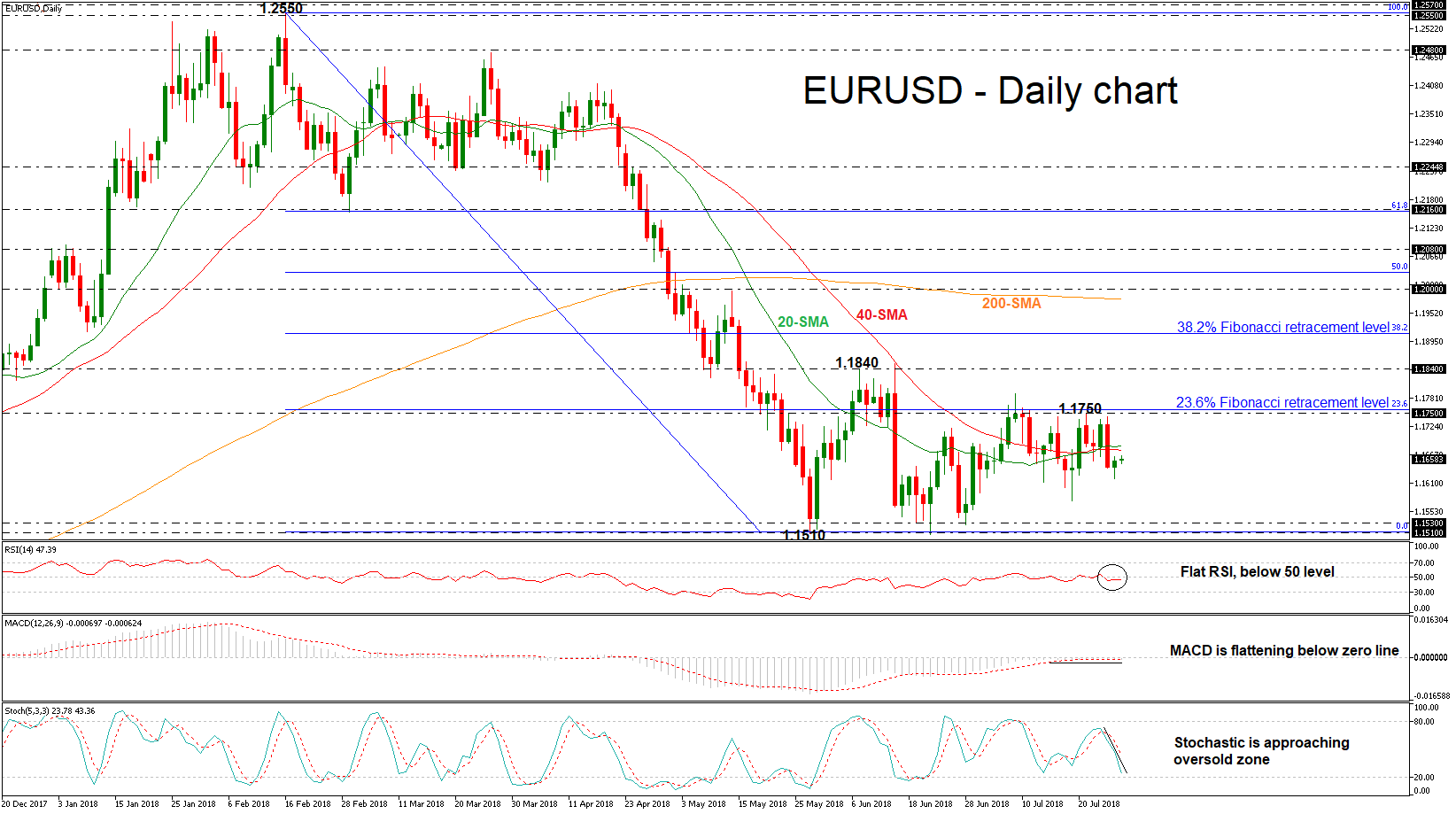

EURUSD Struggles Below 23.6% Fibonacci Mark, Remains Neutral In Short-Term

EURUSD has been remaining below the strong resistance obstacle of the 23.6% Fibonacci retracement level near 1.1760 of the downleg from 1.2550 to 1.1510, since June 14. Moreover, the pair trades around the 20- and 40-simple moving averages (SMAs) in the daily timeframe, indicating a possible sideways channel.

Having a look at the technical indicators, the RSI is flattening slightly below the threshold of 50, while the MACD oscillator failed to jump into the positive territory but still stands above the trigger line. However, the stochastic oscillator is moving lower with strong momentum approaching the oversold zone.

A positive rally is likely to find resistance at the aforementioned strong barrier of the 23.6% Fibonacci mark (1.1760) before being able to re-challenge the 1.1840 key level, taken from the June 7 peak. A jump above this area would help shift the focus to the upside towards the 38.2% Fibonacci of 1.1910. Breaking this level could see a touch of the 1.2000 psychological level, which stands slightly above the 200-SMA in the medium-term.

On the other side, if the price remians below the short-term moving averages, the bearish phase would remain in play especially if the price hit again the 1.1510 – 1.1530 support zone. Clearing this area would see additional losses towards the 1.1300 handle, identified by the high on November 2016.

To conclude, EURUSD would be stuck in a trading range in the short term if it hits again the 1.1840 resistance and reverses lower again. Though, a climb above this level could endorse the scenario for a period of gains.

Yen Holds Firm As Markets Await BoJ, German Inflation Due

Here are the latest developments in global markets:

FOREX: The US dollar index is practically flat on Monday after posting some modest losses in the previous session, failing to capitalize on a strong US GDP print for Q2. Meanwhile, the yen advanced on Friday, as markets positioned for the BoJ’s policy decision, scheduled for the Asian trading session on Tuesday.

STOCKS: Wall Street posted considerable losses on Friday, as soft earnings releases took the wind out of the sails of major indices. The tech-heavy Nasdaq Composite fell by 1.46%, while the S&P 500 and the Dow Jones dipped by 0.66% and 0.30% respectively. Twitter Inc (-20.54%) and Intel Corp (-8.59%) were among the biggest underperformers. Futures suggest another negative open for the major US indices today (S&P, Dow, and Nasdaq 100). Asia was mostly in the red on Monday, with Japan’s Nikkei 225 and Topix declining by 0.74% and 0.43% correspondingly. In Hong Kong, the Hang Seng dropped 0.70%. In Europe, all the major benchmarks were expected to open notably lower today, according to futures.

COMMODITIES: Oil prices dropped on Friday, weighed on by a deterioration in broader risk sentiment – which typically harms risk-sensitive commodities like oil –, as well as an increase in the US oil rig count for the first time in three weeks. Both WTI and Brent are a little higher on Monday, though, rising by 0.49% and 0.22% respectively. In precious metals, gold is down by 0.30% at $1,220 per troy ounce on Monday. The outlook for the yellow metal remains bleak, evident by prices trading just off their lows for the year, at $1,211.

Major movers: Yen holds firm as markets gear for BoJ decision; dollar eases

The yen posted another day of advances against the dollar, euro, and pound on Friday, as investors positioned for the Bank of Japan’s (BoJ) policy decision, due during the Asian trading session Tuesday. Following recent media reports that the Bank may adjust its ultra-loose policy framework in a more hawkish direction, yields on longer-dated Japanese government bonds surged to multi-month highs, lifting the yen.

While markets seem to have positioned for a hawkish tilt, one has to sound a note of caution, as it still appears somewhat early for the BoJ to take such steps. Inflation remains muted, consumer spending is in a soft patch, the economy contracted in Q1, and the outlook for exports is clouded amid trade tensions. On top, any hawkish bites could trigger an outsized rally in the yen, which the Bank will probably be keen to avoid as that could weigh down on inflation. All in all, policymakers seem to have little reason to act at this meeting, and should they disappoint those looking for hawkish changes, the yen may be vulnerable to a sharp downside correction as Japanese bond yields come back down.

Meanwhile, the dollar index dipped somewhat on Friday following the US GDP data for Q2. While the headline GDP number was in line with projections at a robust 4.1% annualized pace, investors seemingly expected something better, evident by the modest tumble in the US currency on the news. It’s going to be a long week for the dollar, with a Fed decision on Wednesday and a US employment report on Friday likely to keep traders busy.

In the UK, the pound slipped as well, unable to draw support from growing expectations that the Bank of England (BoE) will raise its benchmark interest rate at its upcoming policy meeting on Thursday. Looking at market pricing, investors have nearly fully factored in a 25bps rate increase. The probability for such action currently rests at 86% according to UK OIS, so the broader direction in sterling will probably be decided by what signals the Bank sends regarding the pace of future hikes, and not by the rate increase itself.

Day ahead: Eurozone business surveys, German inflation and US pending home sales due

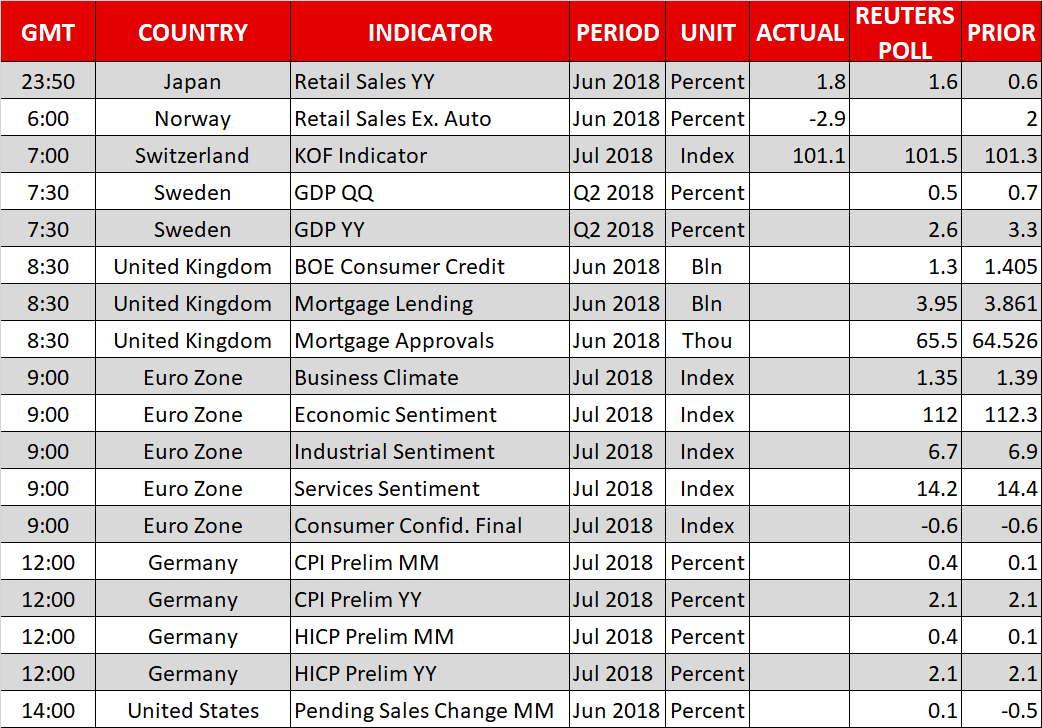

In a busy week in terms of central bank meetings, Monday’s calendar features numerous business surveys out of the eurozone, advance estimates of German inflation for July, and pending home sales data out of the US.

Swedish growth figures for the second quarter will be hitting the markets at 0730 GMT, with economic activity expected to ease relative to the previously tracked quarter.

UK data on June’s consumer credit, mortgage lending & approvals are due at 0830 GMT.

At 0900 GMT, the European Commission’s Directorate General for Economic and Financial Affairs will be releasing numerous surveys gauging business sentiment in the eurozone, all of which are expected to reflect a slight worsening in morale during July relative to June. The final consumer confidence reading for July, again released by the same authority, will also be made public at the same time, with the relevant index anticipated at -0.6, the same as in June and at its lowest since late 2017.

Germany, the eurozone’s largest economy, will be on the receiving end of preliminary inflation data for the month of July at 1200 GMT. Inflationary pressures as gauged by the consumer price index (CPI) are projected to grow by 0.4% m/m, reflecting an acceleration compared to June’s 0.1%, while they’re forecast to expand by 2.1% y/y, the same pace as in June. The Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, will also be attracting attention. It should be kept in mind that these figures are coming one day ahead of the eurozone’s respective numbers and may be seen as giving an indication as far as tomorrow’s release is concerned; in other words, euro pairs may prove sensitive to the release.

Out of the US, pending home sales are expected to increase by 0.1% m/m in June, after declining by 0.5% in May.

US Secretary of State Mike Pompeo, Commerce Secretary Wilbur Ross and Energy Secretary Rick Perry will be speaking at the Indo-Pacific Business Forum at 1230 GMT. Meanwhile, President Trump is scheduled to meet Italian PM Guiseppe Conte at the White House.

In equities, Caterpillar will be releasing quarterly results on Monday.

Lastly, the current week includes numerous central bank meeting that are likely to offer short-term direction in FX (and other) markets; the Bank of Japan, the Federal Reserve and the Bank of England will be concluding their meetings on monetary policy on Tuesday, Wednesday and Thursday respectively.

Technical Analysis: EURUSD looking mostly neutral in the short-term

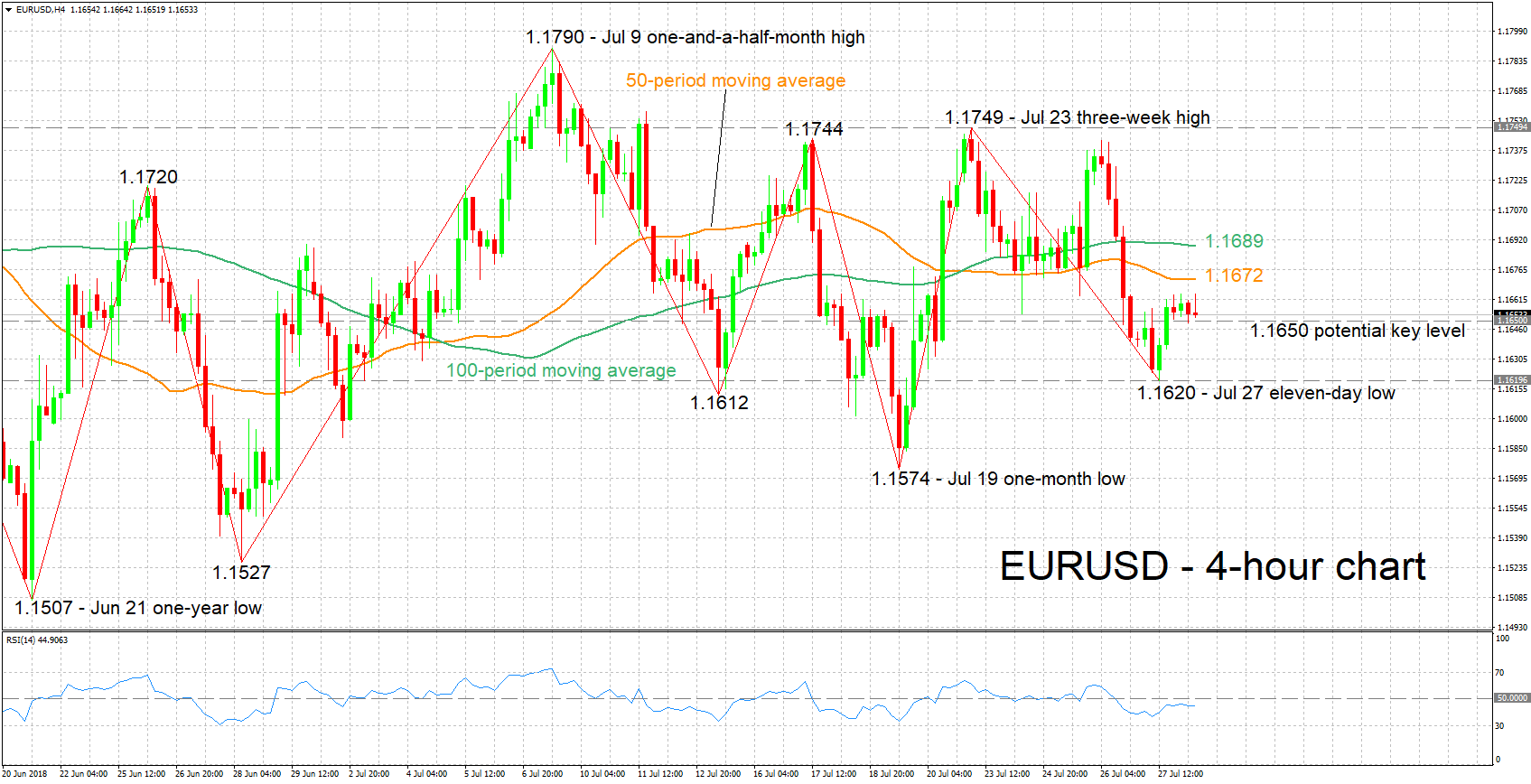

EURUSD is moving sideways after gaining some ground from the 11-day low of 1.1620 hit on Friday. The RSI, which is also moving sideways after a previous rise, is projecting a predominantly neutral picture in the near-term.

Upbeat German inflation data may boost the pair, with resistance to advances potentially taking place around the current levels of the 50- and 100-period moving average lines at 1.1672 and 1.1689 respectively; the region around the latter also encapsulates the 1.17 round figure. Further above, the three-week high of 1.1749 from July 23 would increasingly come into scope.

Conversely, subdued German inflationary pressures could weaken EURUSD. Given a fall below the zone around 1.1650, which was congested in the past, support may come around Friday’s 11-day low of 1.1620, including the 1.16 handle. Steeper losses would turn the attention to the one-month low of 1.1574 posted on July 19.

Eurozone business sentiment data can also spur some movements in the pair.

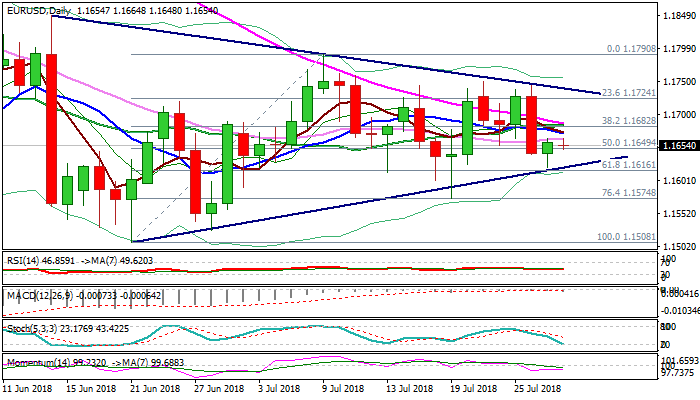

EURUSD Outlook: Daily Cloud / MA’s Weigh Heavily For Renewed Probe Through Triangle Support, Series Of Key Releases This...

The Euro holds in sideways mode and trading within tight range at the beginning of the week and sees little support from last Friday's Hammer, formed after unsuccessful attack at triangle's lower boundary.

Near-term price action remains heavily pressured by thick daily cloud (cloud base lays at 1.1678) and a cluster of daily MA's (between 1.1663 and 1.1687), keeping immediate risk skewed lower, as negative momentum studies support the notion.

Scope for renewed attempt at pivotal supports at 1.1624 (triangle support line) and 1.1616 (Fibo 61.8% of 1.1508/1.1790) exists, with firm break lower needed to generate bearish signal and open way towards troughs at 1.1574 (19 July) and 1.1527 (28 June) which guard key support at 1.1508 (21 June low).

Meanwhile, the single currency may hold in directionless mode, awaiting releases of German labor and EU CPI data on Tuesday, as well as Fed's rate decision, due on Wednesday, which could provide stronger direction signals.

Res: 1.1663, 1.1678, 1.1687, 1.1718

Sup: 1.1648, 1.1624, 1.1574, 1.1527

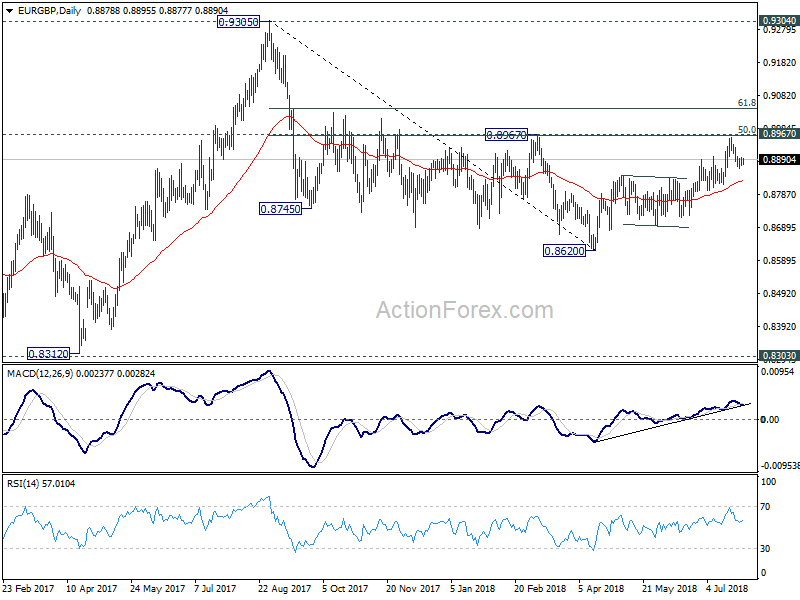

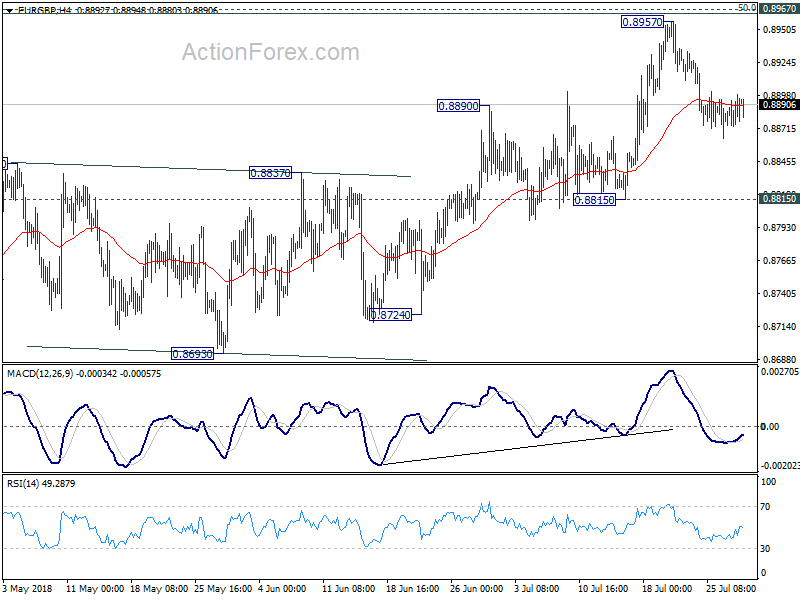

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8879; (P) 0.8891; (R1) 0.8908; More...

Intraday bias in EUR/GBP remains neutral for the moment. As long as 0.8815 support holds, price actions from 0.8957 are seen as a corrective pattern only. On the upside, decisive break of 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) should confirm completion of whole decline from 0.9305. EUR/GBP should then target 61.8% retracement at 0.9043 next.

In the bigger picture, EUR/GBP is staying in long term range pattern from 0.9304 (2016 high). The corrective structure of the fall from 0.9305 to 0.8620 is raising the chance that rise from 0.8312 to 0.9305 is an impulsive move. But we're not too confident on it yet. In any case, we'd stay cautious on strong resistance from 0.9304/5 to limit upside in case of further rally. Meanwhile, if there is another medium term decline, strong support will likely be seen from 0.8303 to contain downside.