Sample Category Title

Into US session: Yen soft aft traders prepare for BoJ disappointment, Swiss Franc strong

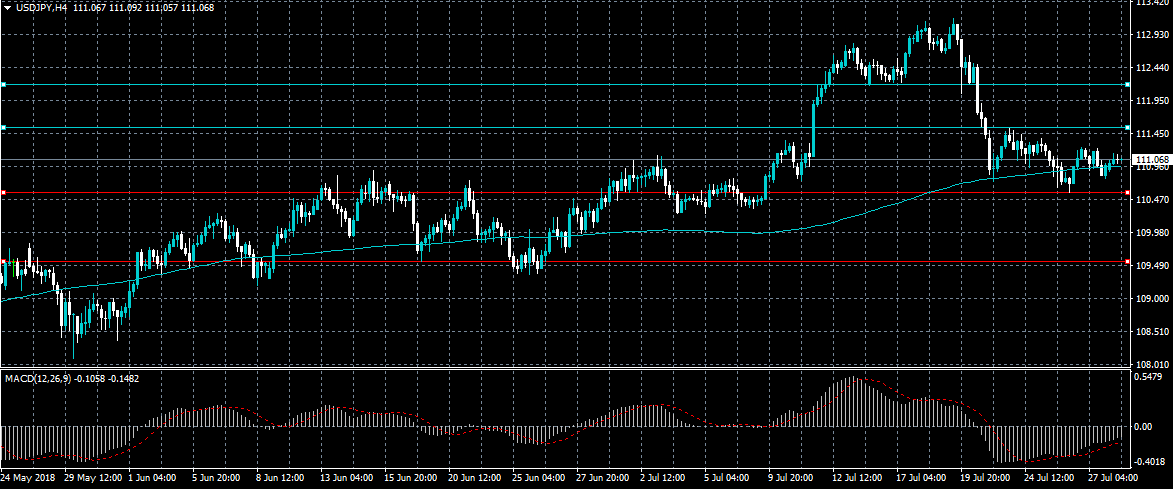

The forex market came into live in European session with Euro and Swiss Franc surging broadly. On the other hand, Yen is soft despite resilience in JGB yield and mild risk aversion. 10 year JGB yield closed up 0.021 at 0.103.

Nikkei closed down -0.74%, Hong Kong HSI down -0.25%, China Shanghai SSE down -0.16%, Singapore Strait Times down -0.54%. In Europe, FTSE is flow. But DAX and CAC are down more than -0.1% at the time of writing.

An explanation for Yen's softness is that traders could be preparing for disappointment from BoJ tomorrow.

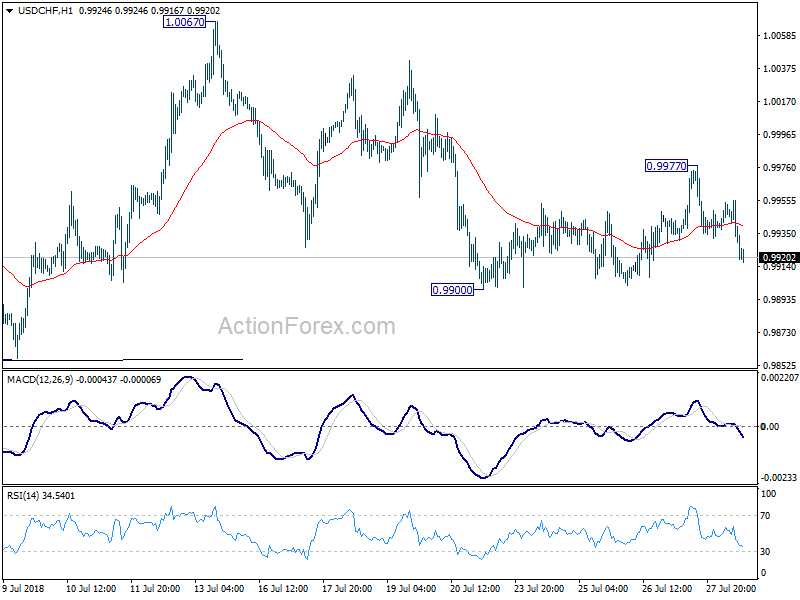

Meanwhile, current development now put 0.9900 in USD/CHF into focus. Break there will resume the fall from 1.0067 and target 0.9856 support next.

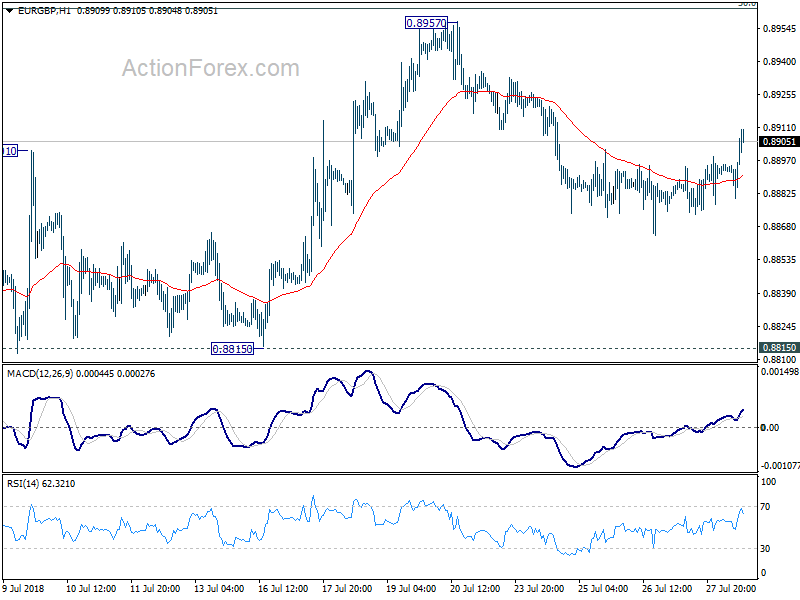

EUR/GBP also staged a strong rebound and could be heading back to 0.8957 high.

DAX Ticks Lower, German CPI Next

The DAX index has posted slight losses in the Monday session. Currently, the DAX is at 12,845, down 0.18% on the day. On the release front, today’s key event is German Preliminary CPI, which is expected to climb to 0.4%. Investors will be keeping a close eye on Tuesday’s indicators. Germany releases retail sales and the eurozone publishes CPI and GDP reports.

The DAX had one its best weeks of the year, climbing 2.8 percent and touching its highest level since mid-June. Investors responded positively to a meeting between EU Commission President Jean-Claude Juckner and U.S. President Trump that went better than expected. The two leaders agreed to take concrete steps to eliminate tariffs and improve the trade relationship between the U.S and the EU, which has been battered in recent weeks. Most importantly, Trump agreed to hold off on threatened tariffs against European car manufacturers, which pushed car manufacturers and bank shares higher and boosted the DAX.

It was more of the same from the ECB, which maintained its monetary policy at its Thursday policy meeting. The main refinancing rate remained at 0.0%, where it has been pegged since January 2016. In a policy statement, policymakers reiterated that rates would remain at current levels “through the summer of 2019”, and “as long as necessary to boost inflation to the target of just under 2.0%. There has been some quibbling among analysts as to the exact meaning of “through the summer”, but what is clear is that the ECB plans to keep rates at a flat 0.00% after winding up its bond-purchase scheme at the end of the year. Low interest rates are bullish for stocks, and the DAX responded with gains on Thursday after the ECB statement. Still, a rate hike seems likely sometime in 2019. The exact timing of a rate increase will depend on the strength of the eurozone economy and inflation levels – if the second half of 2018 is marked by stronger growth and higher inflation, there will be pressure on the ECB to raise rates earlier rather than later in 2019.

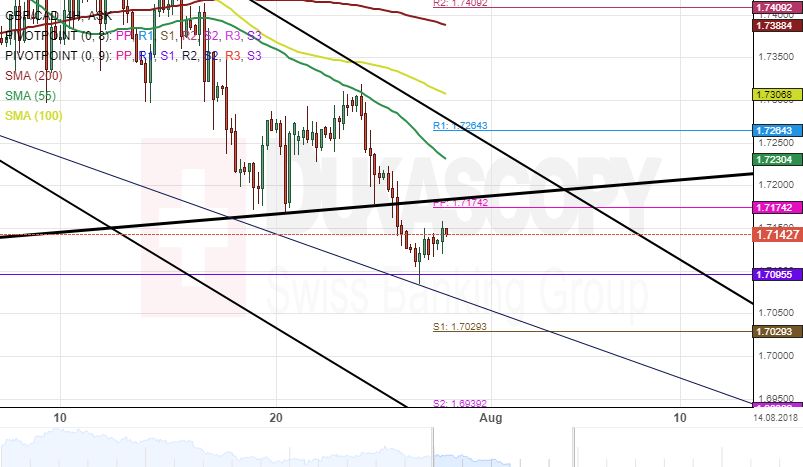

GBP/CAD 4H Chart: Bearish Market

The British Pound has been losing strength against the Canadian Dollar in a steep descending channel. This movement has been guided by a four-month downtrend channel.

During the past few days, a breakout through the lower border of an ascending trendline had occurred as can be seen on the chart. Furthermore, the 55-hour simple moving average has been directing the currency pair lower since July 16.

Technical indicators flash bearish signals on both the 4H and the daily time-frame. This could suggest that the GBP/CAD currency exchange rate is likely to continue moving In the descending channel during the following trading sessions.

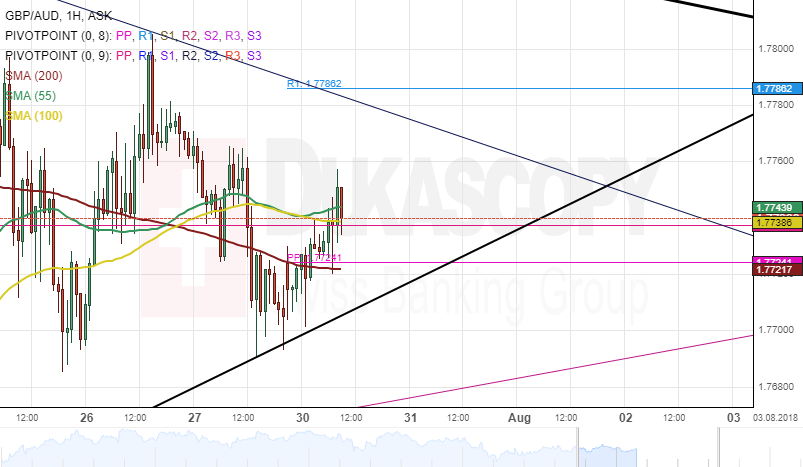

GBP/AUD 4H Chart: Stranded Between Support And Resistance

The GBP/AUD currency pair has been trading in a triangle-Like formation since early July. The Pound Sterling tested the upper boundary on July 12 and reached the bottom border two weeks ago.

The exchange rate is currently stranded between SMAs and pivot points. The 55– and 100-hour SMA and the monthly PP was providing resistance at 1.7739, while the 200– hour simple moving average and the weekly pivot point were providing support at 1.7722.

Everything being equal, a breakout is likely to occur within this session. Technical indicators favour bearish breakout.

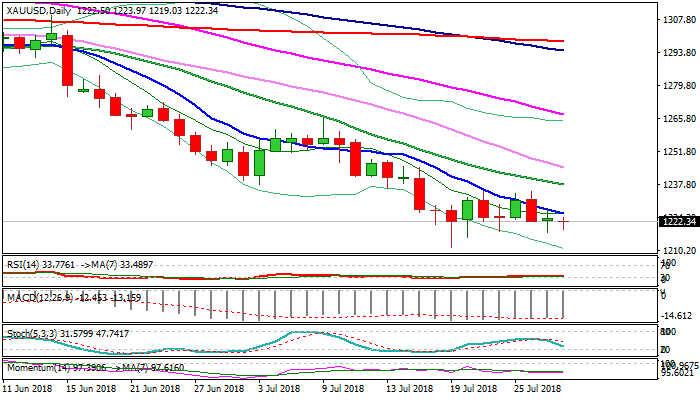

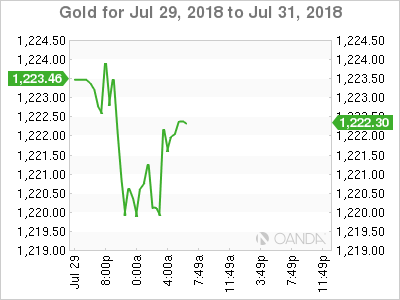

XAUUSD Outlook: Directionless N/T Mode But Bias Remains Negative, FOMC In Focus

Spot Gold holds within tight range on Monday after Friday's trading ended in Doji candle but maintains bearish bias as daily techs remain in full bearish configuration. Monday's action holds above Friday's low at $1217 but upside attempts were limited under falling 10SMA ($1225) which maintains bearish pressure and marks initial resistance. US Federal Reserve are ending two-day policy meeting on Wednesday and expected to signal rate hike in September, as US data remain solid. The latest release, US Q2 GDP showed the fastest growth pace since 2014 but the greenback showed limited reaction on upbeat data, as traders doubt the sustainability of growth. According to the technical studies, negative outlook could be expected while the price remains capped by falling 10SMA. Scenario sees retest of key supports at $1215/11 (Fibo 61.8% of larger $1122/$1366 rally/19 July low) clear break of which would signal continuation of broader downtrend from $1366 double-top. Alternatively, close above 10SMA would ease bearish pressure but sustained break above $1235 double-top (23/26 July highs) would generate stronger reversal signal.

Res: 1225, 1229, 1235, 1238

Sup: 1219, 1217, 1215, 1211

EUR/USD – Euro Slightly Higher, Investors Await German CPI

EUR/USD has started the weeks with slight gains. In the Monday session, the pair is trading at 1.1686, up 0.25% on the day. On the release front, today’s key event is German Preliminary CPI, which is expected to climb to 0.4%. In the U.S, Pending Home Sales is forecast to rebound with a gain of 0.4%, after two straight declines. Tuesday will be busier on both sides of the pond. Germany releases retail sales and the eurozone publishes CPI and GDP reports. The U.S will publish consumer spending and inflation indicators, as well as CB Consumer Confidence.

U.S numbers were sharp on Friday, but the dollar couldn’t gain ground against the euro. Advance GDP, the first of three GDP reports in the second quarter, posted a strong gain of 4.1%, just shy of the forecast of 4.2%. This was much stronger than the gain of 2.2% in Q1 and marked the strongest quarter of economic growth since 2014. As well, UoM Consumer Sentiment dipped lower to 97.9 but still beat the estimate of 97.1 points.

There were no surprises from the ECB, which made no changes to monetary policy at its Thursday meeting. The main refinancing rate remains at 0.0%, where it has sat since January 2016. In a policy statement, policymakers reiterated that rates would remain at current levels “through the summer of 2019”, and “as long as necessary to boost inflation to the target of just under 2.0%. There has been some discussion as to the exact meaning of “through the summer”, but what is clear is that the ECB plans to keep rates at a flat 0.00% after winding up its bond-purchase scheme at the end of the year. This weighed negatively on the euro, which dropped 0.07% on Thursday. The exact timing of a rate hike will depend on the strength of the eurozone economy and inflation levels – if the second half of 2018 is marked by stronger growth and higher inflation, there will be pressure on the ECB to raise rates earlier rather than later in 2019.

Gold Trades In Consolidation Area In Short-Term, Bearish Mode In Medium-Term

Gold has been consolidating since July 19 and has been stuck below the 23.6% Fibonacci retracement level near 1235 of the downleg from 1309 to 1211.38. The price holds within the upper boundary of the 1235 resistance and the lower boundary of the 1218 support barrier, while it also stands below the 20- and 40-simple moving averages in the near-term.

Turning to the technical indicators, the MACD oscillator is falling below the zero and trigger lines strengthening its momentum. Additionally, the stochastic oscillator is heading lower towards the oversold zone, while the moving averages in the 4-hour chart are ready for a bearish crossover.

If price action remains slips lower, there is scope to challenge the 1218 support. A drop below this area would take the price closer to the one-year low (1211.38), endorsing the longer term bearish structure. Further losses would open the way towards the 1204 support level, taken from the low on July 2017.

However, if the market extends gains to the upside, the next level to have in mind is the 1235 resistance barrier, which stands near the 23.6% Fibonacci mark. A jump above this area could drive the price until the next immediate resistance of 1238, penetrating the descending trend line to the upside. Should price move higher, it would touch the 38.2% Fibonacci of 1248.67.

Overall, the precious metal has been holding within a significant downward movement since June 14, indicating that the price remains in a bearish mode in the medium term.

G7 FX Moves Look To Central Banks For Direction

Monday July 30: five things the markets are talking about

Stocks begin a new week under pressure, as investors mull over some lofty corporate earnings and a number of key policy meetings.

A host of G10 central banks are on tap to offer their monetary policy decisions – the Bank of Japan (BoJ), Reserve Bank of India (RBI), Bank of England (BoE) and the Federal Open Market Committee (FOMC).

Up until last week, capital markets were not expecting any changes to the BoJ's policy. Nonetheless, Japanese policy committee are supposedly mulling over some adjustments to policy to help their banking sector – 10-year JGB yields have backed up from +0.035% to +0.10% in anticipation of tomorrow's announcement.

Elsewhere, the BoE is expected to increase its policy rate by +25 bps even amid Brexit gloom, while the RBI is 50/50 on higher rates. The Fed is expected to leave its fed funds rate unchanged. However, look for any indications that U.S policy makers are shying away from two-more interest-rate hikes before the end of this year.

In currencies, the onshore yuan extended last week's slump, while the 'big' dollar ticked higher alongside U.S Treasury yields as metals decline while crude oil prices advance.

On the fundamental front, it's a heavy week for economic data with the week ending with Friday's U.S non-farm payrolls (NFP).

On tap: BoJ monetary policy (July 30/31), CAD GDP, U.S consumer confidence & NZD employment (July 31), Fed monetary policy, GBP manufacturing PMI & AUD Trade balance (Aug 1), BoE monetary policy, U.K inflation report & AUD retail sales (Aug 2), CAD Trade balance & U.S non-farm payroll (NFP) (Aug 3)

1. Stocks see 'red'

In Japan, stocks closed lower overnight as possible changes this week in the BoJ's monetary policy weighed on sentiment, while quarterly earnings were also in focus. Japan's Nikkei share average closed down -0.74%, while the broader Topix fell -0.43%.

Down-under, Australia's S&P/ASX 200 closed down -0.4% following Friday's 11-year closing high, with health care down -1.1%. In S. Korea, the Kospi stock index and the won weakened overnight ahead of key central bank meetings and U.S inflation and payrolls data. At close, the index was down -0.06%.

In Hong Kong and China, stock indexes closed weaker overnight, pressured by a slump in healthcare shares. In Hong Kong, the Hang Seng index ended down -0.25%, while the Hang Seng China Enterprises index was unchanged. In China, the blue-chip CSI300 index fell -0.2%, while the Shanghai Composite Index slipped -0.1%.

In Europe, regional bourses trade a tad lower, tracking their Asian counterparts as bond yields rise.

U.S stocks are set to open in the 'red' (-0.1%).

Indices: Stoxx600 -0.2% at 391.2, FTSE -0.2% at 7683 DAX – 0.2% at 12831, CAC-40 -0.40% at 5492, IBEX-35 flat at 9870, FTSE MIB -0.1% at 21,932, SMI +0.1% at 9183, S&P 500 Futures -0.1%

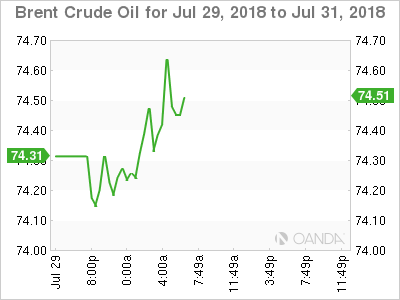

2. Oil prices edge higher but trade row caps gains, gold lower

Oil prices are better bid with the U.S benchmark WTI moving higher after a month of declines, but gains remain capped as the fallout from trade tensions weigh on markets.

Brent crude futures rose +13c, or +0.2% to +$74.42 – it rose +1.7% last week, the first gain in four. U.S West Texas Intermediate (WTI) crude futures are up +31c, or +0.5%, at +$69 a barrel. WTI fell -1.3% on Friday.

The U.S economy grew at its fastest pace in nearly four-years in Q2, but trade tensions remain high between U.S and China despite an easing between the U.S and the E.U.

Last Thursday, Saudi Arabia said that it was “temporarily halting” all oil shipments through the strategic Red Sea shipping lane of Bab al-Mandeb after an attack on two oil tankers by Yemen's Iran-aligned Houthi movement.

Note: An estimated +4.8M bpd of crude oil and refined petroleum products flow through this waterway towards Europe, the U.S and Asia.

According to Baker-Hughes data last week, U.S. energy companies added three oilrigs in the week to July 27, the first time in the past three weeks that drillers have increased activity.

Ahead of the U.S open, gold prices have eased a tad on a former U.S dollar ahead of key central bank meetings and U.S inflation and payrolls data this week. Spot gold is down about -0.3% at +$1,219.70 an ounce. U.S. gold futures are also -0.3% lower at +$1,219 an ounce.

3. Yields back up

Japanese government bond prices fell overnight, with the benchmark 10-year yield touching its highest level in 18-months as the market tries to test the BoJ's intention ahead tomorrow's decision.

Higher yields has forced the BoJ to conduct a “special bond buying operation” to stem rising bond yields amid growing expectations that Japanese policy makers could adjust its policy. On Friday the BoJ lowered the yield to +0.10% – still, the 10-year JGB yield rose to as high as +0.11% earlier this morning, in defiance of the BoJ's apparent defence line.

Note: Some believe that the BoJ could possibly announce it would allow larger moves in the JGB market by loosening its interpretation of its policy target of “around zero percent” in the 10-year yield.

Elsewhere, the yield on 10-year Treasuries rallied +1 bps to +2.96%. In Germany, the 10-year yield decreased -1 bps to +0.40%. In the U.K, the 10-year yield fell -1 bps to +1.282%, the biggest fall in more than a week.

4. Dollar in control

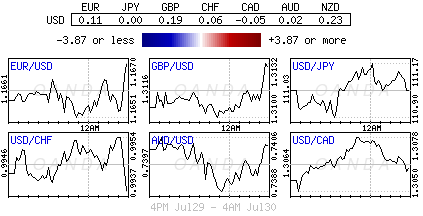

Major currency pairs are trading in a tight range as the markets focus turns to central bank meetings this week.

EUR/USD (€1.1663) is steady as a plethora of German States reports their July CPI data, which for the most part saw the year-over-year above the consensus for the national reading. The 'single' unit could not find much traction, despite the 10-year Bund hitting a six-week high near +0.43%.

USD/JPY (¥111.10), again its steady and holding above the psychological ¥111 handle ahead of tomorrow's BoJ rate decision. Overnight, the BoJ conducted a fixed-rate JGB Bond Purchase operation – an unlimited amount of 5 to 10-year JGB's at +0.10% (its third operation within the past week).

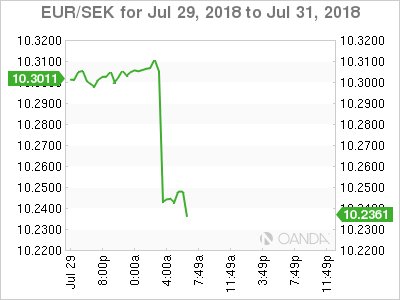

Elsewhere, the EUR/SEK (€10.2419) fell by -0.6% as Sweden Q2 preliminary GDP beat expectations and kept the timeframe intact for the Riksbank to hike rates around year-end.

5. U.K consumer lending stable in June

U.K data this morning showed that the British consumer borrowing remained broadly stable last month, which would suggest another month of steady growth in household spending.

Bank of England (BoE) data showed banks lent £5.4B to consumers in June, net of repayments, a touch higher than the £5.3B in May.

Borrowing on credit cards and other unsecured forms of lending was flat at £1.6B, while mortgage lending inched higher.

Digging deeper, the number of new home loans approved by lenders in June also rose compared with May, to +65,619.

Note: An uptick in mortgage lending offer signs that potential homeowners may be seeking to finalize their purchases before further hikes in borrowing costs this week.

The BoE is expected to lift its benchmark interest rate to +0.75% (Aug 2).

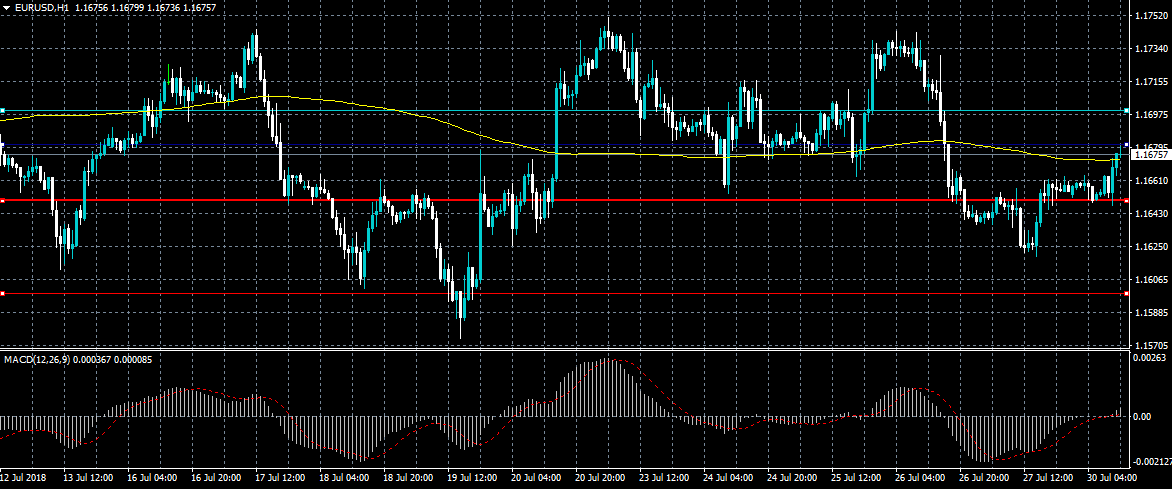

EURUSD Only Intraday Bullish Above 1.1681

The euro has started to gain ground against the US dollar currency after German CPI data came in better than expected this morning. The greenback has also started to shed recent gains after US President Donald Trump threatened a government shutdown over the border wall. Buyers may now attempt to move price towards the 1.1724 resistance level, while sellers will target losses below the 1.1650 level.

The EURUSD pair is bullish while trading above the 1.1680 level, key resistance is found at the 1.1724 and 1.1750 levels.

If the EURUSD pair falls below the 1.1650 level sellers will likely target the 1.1630 and 1.1600 levels.

USDJPY Range Bound Ahead Of BoJ Decision

The US dollar remains range-bound against the Japanese yen, ahead of Tuesday’s key monetary policy decision from the Bank of Japan. The USDJPY pair is awaiting a break from the one-hundred pip trading channel between the 110.55 and 111.55 levels. Medium-term sellers will be looking to target the 109.54 level while USDJPY buyers will be aiming to regain bullish momentum above the 113.00 level.

The USDJPY pair is only bullish while trading above the 111.55 level, further upside towards the 112.20 and 113.00 levels seems possible.

If the USDJPY pair moves below the 110.55 level, sellers will likely test towards the 110.00 and 109.54 support levels.