Sample Category Title

Yen falls broadly as BoJ strengthens the framework for continuous powerful easing

Yen is sold off sharply after BoJ announced the "Strengthening the Framework for Continuous Powerful Monetary Easing".

10 year JGB yields hit as high as 0.115 earlier today but breaches below 0.07 after BoJ release.

10 year JGB yields hit as high as 0.115 earlier today but breaches below 0.07 after BoJ release.

On Yield Curve Control framework BoJ voted 7-2 on the following decision. Firstly, short term interest rate target is held unchanged at -0.1%. Secondly, 10 year JGB yield target is maintained at around 0%. But, "yields may move upward and downward to some extent mainly depending on developments in economic activity and prices". The annual pace of monetary expansion is kept at around JPY 80T. BoJ also noted that "in case of a rapid increase in the yields, the Bank will purchase JGBs promptly and appropriately".

Y Harada and G Kataoka dissented the above decision. Harada said allowing long term yields to move upward and downward was to some extent "too ambiguous". Kataoka continued his push to broaden the target to JGB of 10-years and longer.

BoJ also added forward guidance on interest rate. It said "the Bank intends to maintain the current extremely low levels of short- and long-term interest rates for an extended period of time, taking into account uncertainties regarding economic activity and prices including the effects of the consumption tax hike scheduled to take place in October 2019."

Reversal in NASDAQ and S&P 500 coming after steep selloff

The steep selloff in US stocks in the past two days is significantly raising the chance of near term reversal. NASDAQ closed down -107.42 pts or -1.39% over night to 7630.00. It's down -3.82% from record intraday high as 7933.31. Bearish divergence condition in daily MACD shows notable loss in upside momentum. It's now in a tentative support zone with 55 day EMA at 7623.45, and 38.2% retracement of 6926.97 to 7933.31 at 7548.88. While some support could be seen here, the strength of subsequent recovery will reveal whether the index is heading further down.

It's a bit early to confirm. But we'd like to point out the bearish divergence condition in weekly MACD and RSI too. A firm break of the above mentioned 7548.88 fibonacci level will raise the chance of medium term correction. And fall from 7933.31 could extend to 38.2% retracement of 4209.76 to 7933.31 at 6510.91 before completion.

S&P 500 also closed down -16.22 pts or -0.58% to 2802.60 overnight. It's starting to lose some upside momentum approaching 2827.87 resistance. We'd maintain the view that choppy rise from 2532.69 is a corrective move. And it's likely the second leg of the medium term corrective pattern from 2872.87. Hence even in case of another rise, upside should be limited by 2827.87 to bring near term reversal. Break of 2795.14 support will be the first sign of such reversal . And firm break of channel support (now at 2751) should confirm.

Looking at the longer time frame, when the corrective pattern from 2872.87 extends, it should target 38.2% retracement of 1810.10 to 2872.87 at 2466.89 before completion.

Market Morning Briefing: Euro Yen Could Dip Below Support

STOCKS

Although the indices have risen in the near term, there are resistances overhead which poses threat for the medium term. If the resistances hold, the bears could gain strength and reverse the current uptrend. Need to be cautious at current levels.

Dow (25306.83, -0.579%) surprisingly fell from just above 25500 instead of moving up further. Especially after the long sideways range in the last 6-months, we had expected the index to gain bullish strength and rally towards 26000. We need to see if the index moves back in the next few sessions or falls below 25250 to resume range trade below 25250.

Dax (12798.20, -0.48%) has dipped slightly but is within a near term channel uptrend as seen on the daily candles. While support near 12700 holds, Dax could again move back to 12900-13000 in the medium term.

Nikkei (22470.58, -0.33%) has scope on the downside towards 22000 in the near term. But the index could spend some time in the 22200-22800 region before coming off to lower levels. Looking at the 3-day candle chart, Nikkei seems to making a medium term top followed by a sharp down move in the coming weeks.

Shanghai (2863.99, -0.18%) is trading just below resistance zone of 2950-2900 which is likely to hold and keep the index lower for the near term. If the resistance holds strong, Shanghai could come off towards 2800 or lower in the near term.

Nifty (11319.55, +0.37%) is nearing long term resistance near 11400-11500 region and if that holds, we could see a sharp correction from there towards 11000 or lower in the medium term. We advise to remain cautious and to keep a close watch of price action in the 11400-11500 region.

COMMODITIES

Nymex WTI (70.14, +0.01%) and Brent (75.44, +0.63%) have both bounced from support levels on the longer term charts and look bullish in the medium term. Brent could move up towards 78 while WTI may rise towards 72.

Gold (1229.920, -0.13%) is in a sideways range and may continue for some more time before it decides on further direction.

Copper (2.7925, +0.02%) may see a dip towards 2.70 before again rising back towards 2.90 in the longer run.

FOREX

Euro (1.1707): Euro again moved up yesterday, seeing a high near 1.1720. It could test resistance near 1.174 on daily candles today and then again dip back towards lower levels. Our expectation has been that the BoJ and FOMC meets this week could weaken the Euro (provided there is a hawkish tilt to both the Central Banks' policy statements). If that happens, support at 1.1625-1.1600 could be tested in the next 2-3 sessions. A break of this support by next week is also a possibility.

Dollar Index (94.38): Dollar Index fell yesterday and is currently testing support near 94.30-35 on daily candles. We are currently expecting this support to hold and for the FOMC meet tomorrow to strengthen the Dollar Index. If that happens, a rise from current support towards 95.0-95.5 is likely. As mentioned yesterday, the 95.5-96.0 resistance zone is important and a breach above that is uncertain. If it happens, it could make the Index bullish for the next 1-2 months.

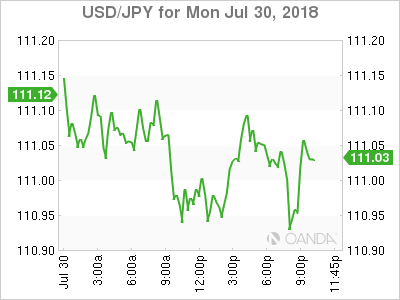

Dollar Yen (110.99): As markets await the BoJ policy (expected anytime now), Dollar Yen continues to trade quietly near the trendline support at 111. Higher up, there is crucial resistance near 112.5 on weekly candles. Lower down, there are interim supports at 110.5 and 110.0. If the BoJ initiates or indicates any sort of tightening to its monetary policy, then we could see Yen strengthen towards 110 in the next 1-2 sessions. Currently, this view is more preferred.

Euro Yen (129.93): Euro Yen could dip below support (129.75-129.50) on daily candles once again today, as the EURUSD is expected to move lower from resistance while Dollar Yen could also dip. A dip towards 1.16 and 110 for EURUSD and Dollar Yen respectively imply a target near 127.5 for Euro Yen. Crucial horizontal support on weekly line chart near 127 would have to be broken for medium term bearishness to be confirmed.

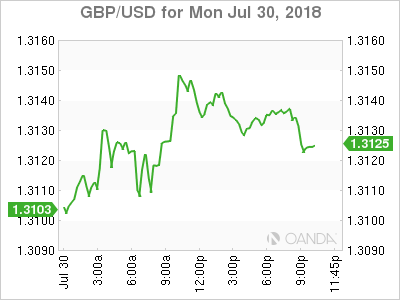

Pound (1.3120): The BOE meeting on Thursday is expected to see a historic rate hike, which seems to have been already factored in by the markets. Even though the broader trend for Pound looks bearish, we still need to see if Pound can decisively break below the 89 weeks MA (1.312) and then, below the horizontal support near 1.3050 on weekly candles. A break below these levels could even happen this week, in spite of the BOE policy release.

Dollar Rupee (68.675): Dollar Rupee is likely to trade sideways. A test of 68.50 could be expected while Nifty strengthens towards 11400

INTEREST RATES

Repeating yesterday's comment: The FOMC and BoJ meetings will be crucial for yields. Last week's surge in global bond yields was primarily due to rumours that the BoJ might be thinking of bringing in some tightening to its loose monetary policy. Any such indication in its policy today could lead to a further bond selloff, thereby raising US and Japanese yields. Moreover, the FOMC is expected to be hawkish (although a rate hike is not expected in this meet).

Japanese 10 year yield (0.09%) is still trading slightly above resistance on short-term chart. The breach of resistance could sustain if the BoJ indicates any tightening in today's policy statement.

US 10 year yield (2.97%), 30 Year (3.10%), 5 Year (2.85%), 2 Year (2.66%):

The US 5 year yield has broken above horizontal resistance near 2.82%-2.83%. Moreover, the US 10 year yield might just break above 3% if the BoJ and FOMC both appear hawkish to the markets. The possibility of the US 10 year yield testing 2.85%-2.80% on the downside is now reducing.

German 10 year bond yield (0.45%) – The German 10 year yield is testing crucial resistance near 0.45% on short term chart and could dip from here. In case it breaches 0.45%, it could become bullish towards 0.55%-0.60%.

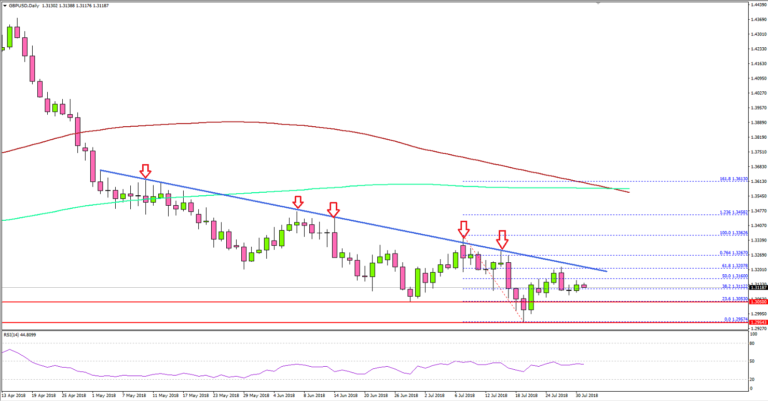

GBP/USD: Here Is Why Upsides Are Limited

Key Highlights

- The British Pound faced a strong resistance near 1.3200 against the US Dollar.

- There is a significant bearish trend line in place with resistance at 1.3185 on the daily chart of GBP/USD.

- UK's Mortgage Approvals in June 2018 were 65.619K, more than the forecast of 65.500K.

- Today, the Euro Zone Gross Domestic Product figure for Q2 2018 (Preliminary) will be released, which is forecasted to grow 0.4% (QoQ).

GBPUSD Technical Analysis

The British Pound attempted a recovery above 1.3180 against the US Dollar. However, the GBP/USD pair faced a strong resistance near 1.3190-1.3200, which prevented further gains.

Looking at the daily chart, the pair formed a low near 1.2960 and bounced back. However, the upside move faced a tough challenge near a significant bearish trend line with current resistance at 1.3185.

Moreover, the pair failed to break the 61.8% Fibonacci retracement level of the last drop from the 1.3362 high to 1.3258 low. The pair declined back below 1.3150 and is currently consolidating losses.

It seems like the trend line resistance is a crucial barrier for more upsides above 1.3200 in GBP/USD. Should there be a daily close above 1.3200 and the trend line, the pair may move into a bullish zone. The next resistances are at 1.3300 and 1.3360.

On the downside, an initial support awaits near 1.3055, below which, the pair could revisit the last swing low of 1.2960.

Recently in the UK, the Mortgage Approvals reading for June 2018 was released by the Bank of England. The market was looking for 65.500K compared with the last reading of 64.526K.

The actual result was positive as the Mortgage Approvals were 65.619K, and the last reading was revised to 64.684K. The report added that:

The annual growth rates of consumer credit and mortgage lending were unchanged in June, at 8.8% and 3.2% respectively. The amount of money held by UK households increased by £3.7 billion in June, slightly above its recent average.

The GBP/USD may perhaps move higher, but a daily close above 1.3200 and bearish trend line is must for further upsides in the near term.

Economic Releases to Watch Today

- Euro Zone Gross Domestic Product Q2 2018 (Preliminary) (QoQ) – Forecast 0.4%, versus 0.4% previous.

- German Retail Sales for June 2018 (MoM) – Forecast +1.0%, versus -2.1% previous.

- German Retail Sales for June 2018 (YoY) – Forecast +1.5%, versus -1.6% previous.

- Germany's Unemployment Change for July 2018 – Forecast -10K, versus -15K previous.

- Germany's Unemployment Rate for July 2018 – Forecast 5.2%, versus 5.2% previous.

- US Personal Income for June 2018 (MoM) – Forecast +0.4%, versus +0.2% previous.

- US Core Personal Consumption Expenditure for June 2018 (MoM) – Forecast +0.1%, versus +0.2% previous.

New Zealand ANZ business confidence dropped to 10 year low, economy feels increasingly late in the cycle

New Zealand ANZ business confidence index dropped to -45 in July, down -5 pts. That's the lowest level since May 2008. Own activity index dropped -5 pts to 4, lowest since May 2009. Sub-indicators were weak across the board, and retail is the least

confident sector.

ANZ noted in the release that "this economy feels increasingly late in the cycle". While fiscal stimulus and strong terms of trade will support growth, "sustained low business confidence increases the risk that firms will delay investment and hiring decisions". "The Road ahead is looking less assured, and risks of a stall have increased.

Also from down under, New Zealand building permits dropped -7.6% mom in June. Australia building approvals rose 6.4% mom in June.

China PMI manufacturing dropped to 51.2, short term downward pressure emerged

The official China PMI manufacturing dropped -0.3 to 51.2 in July, below expectation of 51.3. Official PMI services dropped -1.0 to 54.0, missed expectation of 55.0. Analyst Zhang Liqun noted in the release that despite the slight decline in the PMI index, "steady growth of the economy remained unchanged". However, "short term downward pressure has emerged".

Looking at the details, eight of the sub-indices declined in the month. They include production, new order, purchase volume, import, purchase price, ex-factory price, suppliers delivery, production and operation expectation, New export orders, was unchanged but in contraction region at 49.8. The data set is seen by some as the first sign of impact from increasing trade tension with the US.

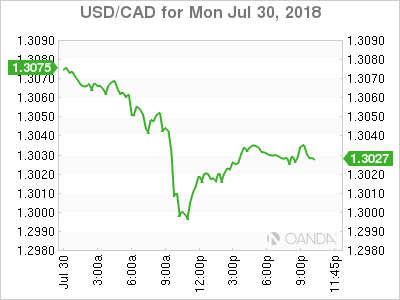

CAD dives as Canada rejected from US-Mexico NAFTA talks

Canadian Dollar drops sharply on a report by the National Post that it's rejected from the senior level NAFTA talks between the US and Mexico, which will be held later this week. Quoting unnamed source, the report noted that the request by Canadian Foreign Affairs Minister Chrystia Freeland to join the meeting was ignore or spurned outright by US Trade Representative Robert Lighthizer. And Lighthizer is planning not to involve Canada unless the latter make some major concessions.

Separately, it's reported that the US and Mexico will hold ministerial-level NAFTA trade talks on Thursday in Washington. According to a Mexican source quoted by Reuters, there will be "technical meetings probably until Wednesday and a ministerial meeting on Thursday."

USD/CAD rebounds strongly on the news, just ahead of near term channel support. While 1.3092 minor resistance is breached, there is no follow through buying yet. Focus is now on this resistance level.

US Dollar Lower on Monday Ahead of Central Bank Announcements

The US dollar is lower against most major pairs on Monday. The week will feature a host of central bank policy announcement that kick off with the Bank of Japan (BOJ) on Monday night. The Fed is not expected to tweak monetary policy on Wednesday, but the statement could end up being positive for the USD. The Bank of England (BoE) is heavily anticipated to hike by 25 basis points, but uncertainty about Brexit could make the central bank hesitate on pulling the trigger as a No Deal exit from the EU is gaining as a likely outcome. Jobs data is also scheduled to be released at the end of the week with all signs pointing to another strong U.S. non farm payrolls (NFP) report, higher wages and a lower unemployment rate in America.

The Japanese yen is trading lower ahead of the central bank announcement. The BOJ was not firmly on the market’s radar until it recently stepped up its rate of interventions in the fixed income market and hinted at a clear yield curve control policy. The possibility of a lower inflation forecast to a more reasonable 1 percent level could also be part of the central bank’s announcement.

The British pound is higher ahead of the Bank of England (BoE) rate announcement on Thursday. The central bank is expected to make Super Thursday a little bit more super with a 25 basis points rate hike.

Brexit uncertainty is keeping the pound under pressure, but the US dollar fall has allowed the GBP to move into positive territory. The Fed is not expected to announce a change in monetary policy, although a hawkish statement could support the USD on Wednesday.

The Canadian dollar appreciated versus the US on Monday. Oil prices are above $70 combined with the softness of the US dollar and NAFTA optimism have taken the loonie higher at the start of the week.

Wall of Worry Builds around the US Tech Sector

US equity markets continue to absorb Facebook’s swoon which is weighing down FAANG’s ahead of Apple earnings announcement on Tuesday. Indeed the markets heavyweight champions are having a rough day, but US markets pruned much of their losses as bank stocks and surging oil prices boosted producers. But all eyes will remain on NASDAQ as the Wall Street wall of worry continues to build around the tech sector.

Interest rate markets are predictably in flux ahead of the numerous central bank announcements this week with the BOJ tomorrow, the US FOMC on Wednesday and the BOE on Thursday. No one is expecting any rate changes, but as always the statements will be closely analysed for any shifts in policy.

But the US dollar is still suffering a bit of a GDP hangover after squeezing higher vs G-10 peers on whisper numbers that were running exceptionally hot. But in the GDP aftermath, the USD bears continue to remind that 4.1% print was below consensus but more significantly, core PCE came in below expectations And while the GDP print keeps the Fed on a path for two more rate hikes in 2018, the markets are not buying in wholeheartedly given the lack of inflationary pressures.

Oil Markets

Oil markets are starting the week on a very positive tone with prices trading bid throughout the NY session as supply concerns are making headlines once again Both Brent and WTI contracts are seeing strong support after three UK oil fields, Alwyn, Dunbar and Elgin are shutting down due to labour strikes. All the while middle east geopolitical tensions recur as Saudi Arabia continues to halt their shipments via the vital Red Sea shipping lanes as ongoing attacks from Houthi rebels take their toll.

Also, Trump’s auto plan continues to influence prices as the rollback in US efficiency requirements is projected to increase fuel consumption by some 500 K barrels per day.

Gold Markets

The markets are trying to turn bullish on the hope for some type of relief rally, but prices remain entirely at the fate of the US dollar. The Yuan has continued to weaken throughout the day and has pressured prices lower. It’s taking little to spook gold longs suggesting as the markets remain decidedly bearish ahead of the critical central bank decisions.

Currency Markets

Not making much of current price actions given summertime liquidity feel to FX markets as the subtle ebb and flows are more apt to little more than position driven given the tricky calendar of events in the days ahead. And to complicate matters, month end is approaching with quant signals suggesting USD selling portfolio adjustments.

USDJPY still hovering around 111 ahead of the highly anticipated BoJ policy meeting. And while it’s unlikely the BoJ will lay a summertime hawkish horror story on the markets, there has been enough noise to suggest that something is afoot. And while USDJPY could gap higher on the lack of hawkish inference, but the markets will likely continue to bank on a fall review which should temper upside moves. At this point, the general market consensus is for a downgrade on CPI forecast to 1.5 % from 2 %

USDCAD with WTI surging, its been playing positively into CAD trading sub 1.300 before midday profit-taking set in and WTI traded off intraday highs.

EURUSD: The Euro has been trading firmer today on the back of higher EU Zone yields suggesting we could see a move to the top side of the current ranges.

GBPUSD: Cable has been rangy” but with the lack of Brexit noise Sterling shorts are being pared.

AUDUSD: The Aussie short remains a crowded trade but with month-end dollar selling likely to develop into month end shorts are getting covered.

USDCNH Spot continues to move higher even though the fix was lower than market expectation. There is little news, but the lack of progress on the trade war front coupled with little pushback from the PBoC suggests the USDCNH has room to run higher.

USDMYR: Oil prices have been mildly supportive, but the MYR continues to be weighed down by the weaker Yuan and uncertainty over trade war. But with the plethora of central banks taking the stage this week. The local trader is waiting to take their cues from both BoJ and the FOMC forward guidance.

Eco Data 7/31/18

[php_everywhere instance="1"]