Sample Category Title

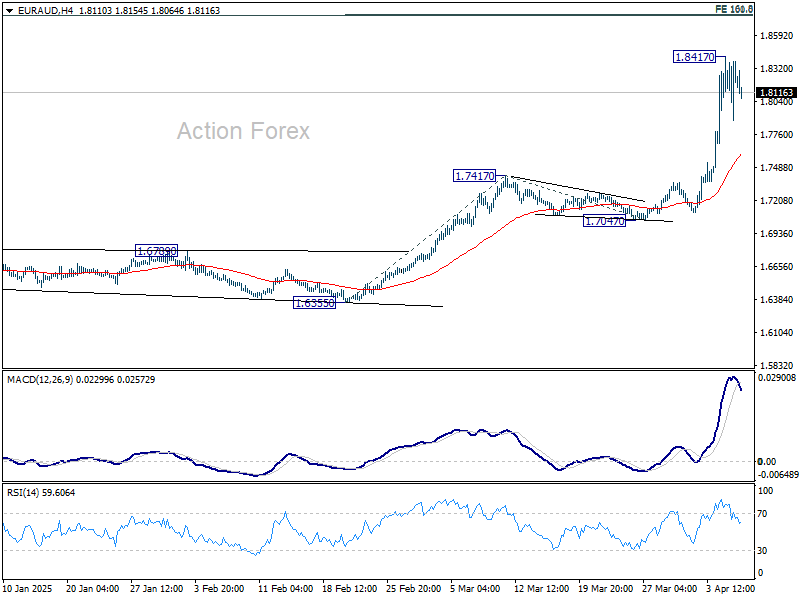

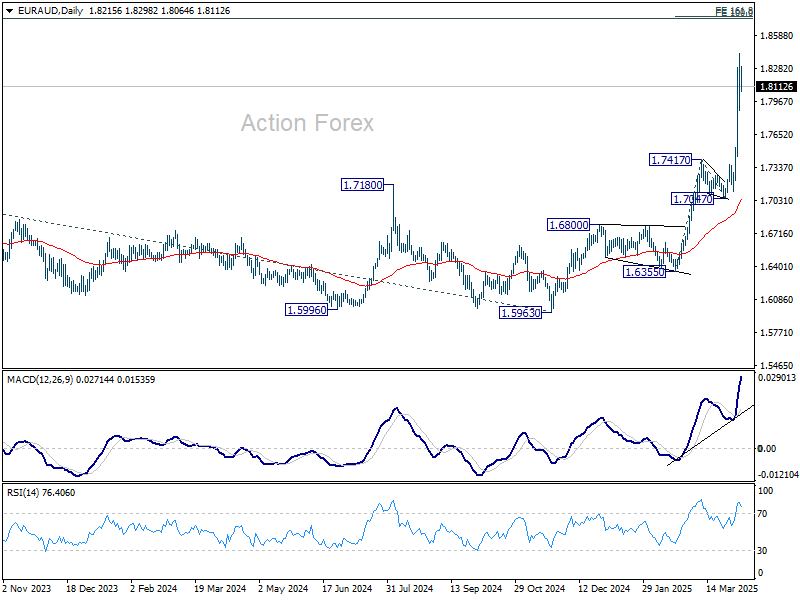

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7923; (P) 1.8174; (R1) 1.8467; More...

A temporary top is formed at 1.8417 with current retreat and intraday bias in EUR/AUD is turned neutral. Downside of consolidations should be contained above 1.7417 resistance turned support. Above 1.8417 will resume larger up trend to 161.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.8765 next.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Outlook will remain bullish as long as 1.7062 resistance turned support holds (2023 high) even in case of deep pullback.

Elevated Market Volatility Probably to Stay for Some Time to Come

Markets

(Interest rate) markets yesterday faced extreme intraday volatility. Swings in US Treasury yields amounted from more than 43 bps for the 2-y to ‘only’ 33 bps at the very long end of the curve (30-y). German yields whipsawed about 25 bps across the curve intraday. UK gilt yields saw similar swings, even slightly more at the very long end (30-y 28 bps move). In the end, US yields in a bear steepening move finished the day between 11 (2-y) and 21 (30-y) bps higher. The German curve also steepened with yields in a daily perspective changed between -5.0 bps (2-y) and + 3.7 bps (30-y). In this high-volatility environment, Bunds again outperformed swaps. Intra-EMU spreads also again widened, albeit modestly (Italy 10-y +6 bps). Anyway, the moves occurred as there was little in the way of ‘hard’ political or economic news. At least there was no clear reason/guide for market to get a more crystallized view on what to expected from reaction function of the Fed (or other central bankers) going forward. For now, Fed members (Goolsbee, Kugler) in the first place warned on the inflationary impact of tariffs. However, longer term visibility for the Fed probably is as low as it is for markets. It remains impossible for investors to make any educated guess on what to expect from the US/Trump Tariff policy or a fortiori on the longer term impact for growth and/or inflation inside and outside the US. The US and China are on collision course as president Trump vowed to add another tariff-layer of 50% in reaction to China matching the 34% reciprocal levy on Chinese imports into the US (cf infra). For some other countries, the US is signaling preparedness to negotiate (Japan, Isreal). Even so, it is remains vague what the Trump administration exactly wants to scale back tariffs, if they have the intention to do so anyway. The EU at the same time advocates a ‘carrot-and-stick’ approach, advocating negotiations, but at the same time preparing countermeasures if they fail. At least for now, you don’t have the impression that it will be easy to find a workable and sustainable compromise anytime soon. In this respect, elevated market volatility probably is here to stay for some time to come. US equities yesterday closed a volatile session a ‘little changed’ (-0.23%). However, this probably is more an indication of agnosticism rather than suggesting a genuine bottoming out process. The Eurostoxx still closed 4.55% lower. FX markets, at for the major FX cross rates also took a more agnostic view. The DXY TW USD index gains modestly (103.25 from 103.5) admittedly also amid intraday swings. USD/JPY gained from about 147 tot 147.8. EUR/USD eased to close at 1.091. Smaller, less liquid currencies mostly declined substantially. In this respect, we mention sterling underperformance. EUR/GBP jumped sharply (close 0.857) and this occurred amid strong underperformance of the very long and of the UK yield curve (30-y+ 20.5 bps!).

Asian equities this morning mostly show modest gains, with Japan outperforming (Nikkei +5.75%). US and European futures also suggest a positive open. Even so, gains are very limited compared to recent losses. The eco calendar is again very thin. So, headlines/rumours on trade/tariff issues will continue to drive price swings. For now, the steepening trend on yield markets, including the US, might continue. This in theory might cap further USD gains.

News & Views

Chinese monetary authorities during this morning’s daily fixing let the Chinese currency weaken beyond the closely watched USD/CNY 7.20 barrier. The 7.2038 fixing level was the weakest for the yuan since September 2023 and triggered instant depreciation within the allowed 2% deviation margin at the open. USD/CNY gapped higher to 7.337 before paring the gains slightly to 7.33 currently. The move by the central bank suggests China is willing to use its currency as a shock absorber in the escalating trade war with the US. Just yesterday, president Trump threatened to impose an additional 50% import taxes on China in a response to the latter’s retaliatory tit-for-tat 34% tariff announcement last Friday. Any further CNY depreciation will likely be (managed to be) gradual though since authorities are wary for potential capital outflows and wider financial instability.

The European Commission is proposing counter-tariffs as high as 25% on a range of US goods in retaliation to the US levies on aluminum and steel, Reuters reported yesterday. The document seen by the news agency made no mention of bourbon, which the EC had earmarked for a 50% tariff. That prompted a backlash by Trump, who threatened a 200% response to EU alcoholic drinks if the EC would push it through. The European levies go into force April 15. Deliberations on how to react to the US across-the-board 20% tariff announced last week are ongoing.

The Dumbest Trade War in History

Monday was rough across global financial markets. European stocks posted wild slides: the DAX traded nearly 10% lower compared to Friday’s close, the Stoxx 600 dropped more than 6%, the Swiss SMI lost over 5%, and US markets opened sharply down. But suddenly, the trend reversed. Markets rebounded on rumours that Donald Trump could delay part of the tariffs set to kick in tomorrow. The S&P 500 jumped by around 8% on that wave of optimism—only to fall again by 5% as the White House clarified it was all a misinterpretation. In the end, the S&P 500 closed the session with a minor 0.23% dip, and the Nasdaq even eked out a 0.19% gain.

But intraday volatility is at levels not seen since the Covid-era selloff. The VIX index shot up to 60 yesterday. Yes, we briefly touched that level last summer when traders rushed to unwind carry positions, but the feeling on the trading floor was: a day from Covid.

This morning, futures are in better shape—we’re seeing 1–2% gains across Europe and the US—but volatility remains too high to inspire much optimism.

Crazy vol

We’re facing an avalanche of headlines: who’s ready to negotiate, who’s not, what did Trump say, what did he mean… it’s nearly impossible to predict the next move. US Senator Elizabeth Warren called it the “dumbest trade war” in history, pointing out that this turmoil isn’t caused by a virus or a housing collapse—it’s man-made and potentially fixable by simply rolling back tariffs. For now, Trump stands his ground, while world leaders oscillate between retaliation and negotiation. Meanwhile, big investors, US bank bosses, and even Elon Musk—the First Friend—are voicing criticism. Maybe internal pressure in the US will eventually shift the course.

And the Fed?

Of course, the magnitude of this market selloff brings the Federal Reserve (Fed) into the conversation. The central bank is trapped between a rock and a hard place: above-target inflation on one side, rising recession risks on the other. The Fed is being asked to choose—fight inflation or stabilize markets. I believe that if the selloff worsens, the Fed will be forced to prioritize the latter. Market consensus is quietly shifting toward the possibility of four rate cuts this year—double the number expected before Liberation Day.

Bond investors are confused too. Hints of a deal—or even a tariff delay—could spark a risk rebound, leading to a sharp unwinding of dovish Fed bets and renewed selloffs in bonds. BoFA’s MOVE index, which tracks bond market volatility, is surging.

In FX

The US dollar was better bid yesterday, but it's under pressure again this morning. Trade worries are having the opposite effect of what analysts originally expected. The euro is consolidating just below the 1.10 mark, despite heavy market losses. Some investors argue that an isolated US could actually boost appetite for the euro as a trade and reserve currency. Commodity currencies, however, are suffering: the AUDUSD briefly dipped below 60 cents—the lowest level since Covid. The Chinese, for their part, are letting the yuan weaken to offset tariff-related competitiveness losses.

One hope is that the worst is already priced in and that markets can only rebound from here. But the problem is: the worst keeps getting worse, and there’s no reasonable limit in sight at the White House.

Hopes of Stabilization Brewing

In focus today

In the US, the NFIB's Small Business Optimism index is scheduled for release. Additionally, focus will be on any softening of the Trump administration's trade policy stance or any verbal intervention from the Fed.

In Denmark, we will receive February's industrial production figures. January saw an 11.9% decline (SA), an unusually large drop even for Denmark's volatile industrial production. Despite the uncertainty surrounding the drivers - this decline likely does not indicate a fundamental shift in Danish manufacturing.

The day also features a string of ECB speakers, which could add some nuances on their thinking following the recent tightening of financial conditions.

Economic and market news

What happened overnight

In the US, President Trump announced direct talks with Iran regarding Tehran's nuclear program, scheduled for Saturday. Amid heightened tensions, Trump warned of significant risks for Iran if negotiations fail. Iran currently rejects the approach for direct talks.

In China, the commerce ministry has pledged to implement further retaliatory measures if President Trump proceed with his threat to impose an additional 50% tariff on Chinese goods. China asserts its readiness to "fight to the end".

What happened yesterday

In the US, rumours of a 90-day tariff pause led to a significant rally in equities yesterday afternoon. The rumours were later debunked by the White House, but the market action clearly emphasized the significance any softening of the trade policy stance could have. Later, President Trump threatened to impose a 50% additional tariff on China due to its retaliatory measures announced on Friday. These new tariffs could be effective tomorrow alongside the retaliatory tariffs announced last week.

In the euro area, investor confidence declined in the first survey following Trump's tariff hammer. The Sentix investor confidence indicator fell sharply from -2.9 to -19.5, marking its lowest level since October 2023. Conducted between 3 April and 5 April, this survey provides an early indication of what to expect from other sentiment indicators. For additional insights, see Euro Area Macro Monitor, 7 April.

In Sweden, The March budget outcome for the central government showed a result in line with the forecast. The accumulated deviation since the latest borrowing report therefore still amounts to a net borrowing requirement of SEK 4.8bn (i.e. slightly larger deficit than forecasted). On top of this, the SNDO will have to add the recently presented fiscal stimulus, including the announced increased defence spending, when they present the next borrowing report on 22 May. We expect the increased borrowing requirement will result in the SNDO raising the SGB auction volumes.

In geopolitics, the European Commission has proposed a "zero-for-zero" tariff for industrial goods to avert a trade war with the US, as EU ministers focus on negotiations while preparing targeted countermeasures. With impending US tariffs of 25% on steel, aluminium, cars, and 20% on other goods, the EU plans to impose 25% tariffs on a range of goods taking effect between 15 April and 1 December, depending on the product. Bourbon, wine and dairy products have been removed from the tariff list following lobbying by EU members to protect their alcohol industries. EU governments are expected to approve the list on Wednesday. Von der Leyen has reaffirmed the EU's remained commitment to negotiation efforts with the US, while signalling readiness to retaliate against the tariff increases, reflecting a consistent approach in managing trade tensions.

Equities: What a ride in equities. European and Nordic markets started and ended the day in a sharp fall. Intraday moves were extraordinary, as a misunderstanding of a tariff pause temporarily sent equities higher - only to fall back again when White House refuted the report. Most European and Nordic indices closed around -5%, with Stoxx 600 down -16% since peak and other surfing close to bear market territory. This was a capitulation session without a clearcut preference between sectors and styles. Investors sold what they could, even typical safe havens like telcos and gold prices. Just like what is typically the case after a capitulation session, futures markets are indicating a 2% rebound today.

The US session was very different. Indexes close to unchanged, with S&P 500 -0.2%. Investors stopped trading on the recession risk and started trading on the rising yields. Hence, sector performance was different, with yield sensitive sectors like real estate and utilities selling off while oversold cyclicals like banks and Mag 7 outperforming (and some sectors even in green!). In fact, 157 of the 500 S&P companies were higher. US futures are 1-2% higher this morning and as so, on track to outperform Europe the last month.

Asian markets are in big moves today, with Nikkei 225 rising 5% on what seems like successful negotiations with Trump. Chinese and Korean equities mildly higher as well, despite the new tariff threats.

FI&FX: Risky assets were under pressure from the beginning of the week, as the Chinese retaliatory tariffs and Trump's firm stance on implementing aggressive tariffs over the weekend led to sour sentiment. However, the mood changed drastically in the afternoon due to the - presumably - fake news that the US administration is considering a 90-day tariff pause. Even though the rumours were quickly debunked, hopes for a less severe outcome of the trade war supported equities for the remainder of the session with the S&P 500 turning a -5% initial drop into a marginal decline of just 0.2%. The DXY index gained 0.5% throughout the session, while haven currencies such as JPY were slightly weaker. Trump's threats of assigning an additional 50% tariff on Chinese goods only led to a modest 0.5% rise in USD/CNY. In scandies FX, yesterday saw a 1.5% rise in EUR/NOK, while EUR/DKK rose to the highest level since 2020. EUR/SEK was close to unchanged. The US Treasury curve bear-steepened with the 10Y yield rising almost 20bp throughout the session. Brent is slightly higher at USD65/bbl. Asian equities are significantly up this morning with NIKKEI 225 recording a 6% rise, while Chinese indices have gained 1-2%. European equity futures point towards a 2.5% rise at the market opening.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8541; (R1) 0.8621; More...

Intraday bias in EUR/GBP remains on the upside for the moment. Current rise from 0.8221 is in progress for 0.8624 key cluster resistance next. Decisive break there will be an important indication of larger bullish trend reversal. On the downside, below 0.8520 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, the break of medium term channel resistance is a bullish signal. Down trend from 0.9267 (2022 high) could have completed at 0.8221, just ahead of 0.9201 key support (2022 low). Firm break of 0.8624 cluster resistance (38.2% retracement of 0.9267 to 0.8221 at 0.8621) will confirm this bullish case and target 61.8% retracement at 0.8867 next. Nevertheless, rejection by 0.8624 will keep medium term outlook neutral at best.

Markets Stabilize as Tariff War Enters Complex Negotiation Battles

Global market sentiment is showing tentative signs of stabilization. The tone improved slightly as US Treasury Secretary Scott Bessent signaled that for countries choosing not to retaliate, the US has already reached a "maximum tariff level," which could gradually be rolled back. However, this was far from a green light for relief, as the broader picture of US trade strategy continues to unfold.

What’s becoming increasingly clear is that the US administration's goals extend well beyond mere tariff reductions. Washington is also targeting non-tariff trade barriers such as government subsidies, currency policies, and broader regulatory practices. This shift complicates trade negotiations significantly, especially as each partner country faces vastly different economic and political constraints. The complexity will likely prolong the path to resolution.

Different countries are responding in markedly different ways. China has chosen confrontation, swiftly imposing its own 34% retaliatory tariffs and now faces a threat from US President Donald Trump of an additional 50% levy if Beijing doesn’t back down in the coming days. China’s commerce ministry rebuked the threat, accusing the US of “blackmail,” signaling that neither side is ready to concede. The world’s two largest economies appear headed for a more protracted and damaging showdown.

In contrast, the EU is walking a more calibrated line. While the European Commission did announce a narrow set of retaliatory tariffs on Monday evening—targeting the original US steel and aluminum duties—it has held off for now on countering the broader reciprocal measures. EU trade chief Maros Sefcovic reiterated the bloc’s openness to negotiations, proposing a “zero-for-zero” approach for industrial goods. Still, he warned that the EU would not “wait endlessly,” and a broader retaliatory package is expected by the end of April.

The situation with Japan is fluid too. While Tokyo has so far avoided direct retaliation, it’s clear that the US expects major concessions. Treasury Secretary Bessent confirmed that upcoming talks with Japan will cover not only tariffs but also non-tariff trade barriers, government subsidies, and even currency policy. How Japan responds in this multi-dimensional negotiation will be critical, especially as the minority government faces domestic political pressure and a fragile recovery.

Amidst this backdrop, traders are being cautioned to remain vigilant amid rising market noise and disinformation. False rumors—such as claims the US might delay its tariffs by 90 days or that Fed had called an emergency meeting—circulated widely but were promptly debunked.

In the currency markets, Swiss Franc is currently the strongest one for the week, followed by Loonie, and then Aussie. Sterling is the worst performer, followed by Yen and then Kiwi. Dollar and Euro are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 5.51%. Hong Kong HSI is up 1.58%. China Shanghai SSE is up 0.91%. Singapore Strait Times is down -1.54%. Japan 10-year JGB yield is up 0.0119 at 1.234. Overnight, DOW fell -0.91%. S&P 500 fell -0.23%. NASDAQ rose 0.10%. 10-year yield rose 0.170 to 4.155.

Fed's Kugler: Anchoring inflation expectations must remain top priority

Fed Governor Adriana Kugler emphasized the importance of keeping inflation expectations well anchored in comments delivered to a Harvard economics class.

She reaffirmed the Fed’s commitment to the 2% inflation target and stressed "It should be a priority to make sure that inflation doesn't move up".

Kugler also noted that economic activity in the first quarter may have been stronger than previously anticipated, driven by consumer front-loading ahead of expected tariff hikes.

While the full extent of tariff-related cost pass-through is yet to be seen, she acknowledged the financial strain such developments could place on households. That, she argued, is "exactly why we think we need to keep focus on that."

Fed's Goolsbee: Must rely on hard data, no simple playbook for stagflation risks

Chicago Fed President Austan Goolsbee expressed concern that escalating trade tensions—through tariffs, retaliations, and potential counter-retaliations—could recreate the turbulent economic conditions of 2021–2022 when inflation was "raging out of control."

In an interview with CNN, he warned that if the tariff threats materialize to their full extent, especially if met with proportionate responses, the US economy risks slipping back into a period of high inflation and stagnating growth.

However, Goolsbee also acknowledged that the situation remains fluid. He noted that negotiations could yet defuse the tension, especially if they result in new trade agreements. Referring to Treasury Secretary Scott Bessent’s optimism about a coming “golden age of trade.”

If stagflation begins to take hold, Goolsbee stressed, the Fed's response would not be straightforward. The appropriate policy path would depend heavily on how growth and inflation evolve in the coming months.

“Our job is to look at the hard data,” he said, underlining that in a scenario where both growth weakens and prices surge, there’s no “generic answer” to guide monetary policy.

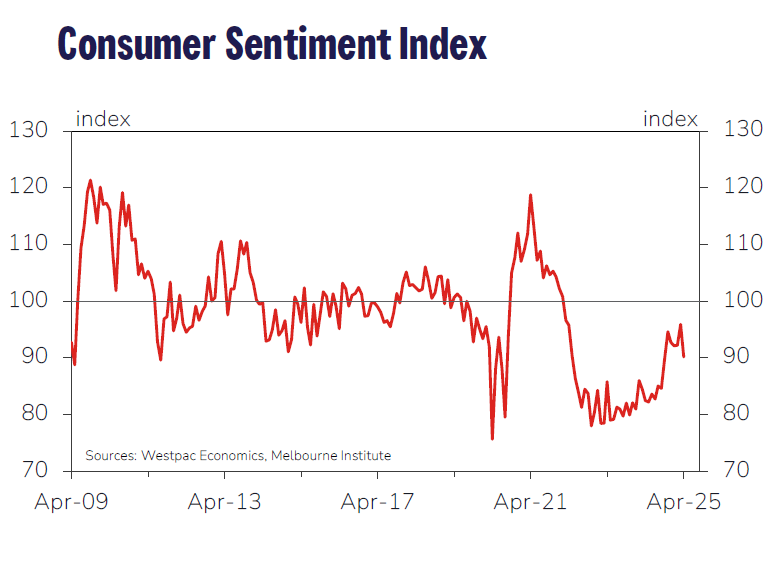

Aussie Westpac consumer sentiment slumps post-tariff shock; RBA seen tilting toward May rate cut

Australia’s Westpac Consumer Sentiment index plunged -6.0% in April, dropping from 95.9 to 90.1. The steep fall was notably skewed by the timing of the survey in relation to US announcement of reciprocal tariffs on April 2.

Respondents surveyed before the announcement showed only a modest dip in sentiment to 93.9. Those surveyed after reported a sharp drop of nearly 10% to 86.6. .

The sub-indices measuring sentiment towards the economy were particularly hard-hit, with the outlook for the next 12 months falling -5.7% to 90.5, and the 5-year outlook slipping back by -3.0%

With RBA set to meet on May 19-20, Westpac believes the weakening external backdrop, coupled with softer inflation, will push RBA to deliver another 25 bps rate cut. RBA is likely to become "much more focused on downside risks to growth than lingering questions about inflation".

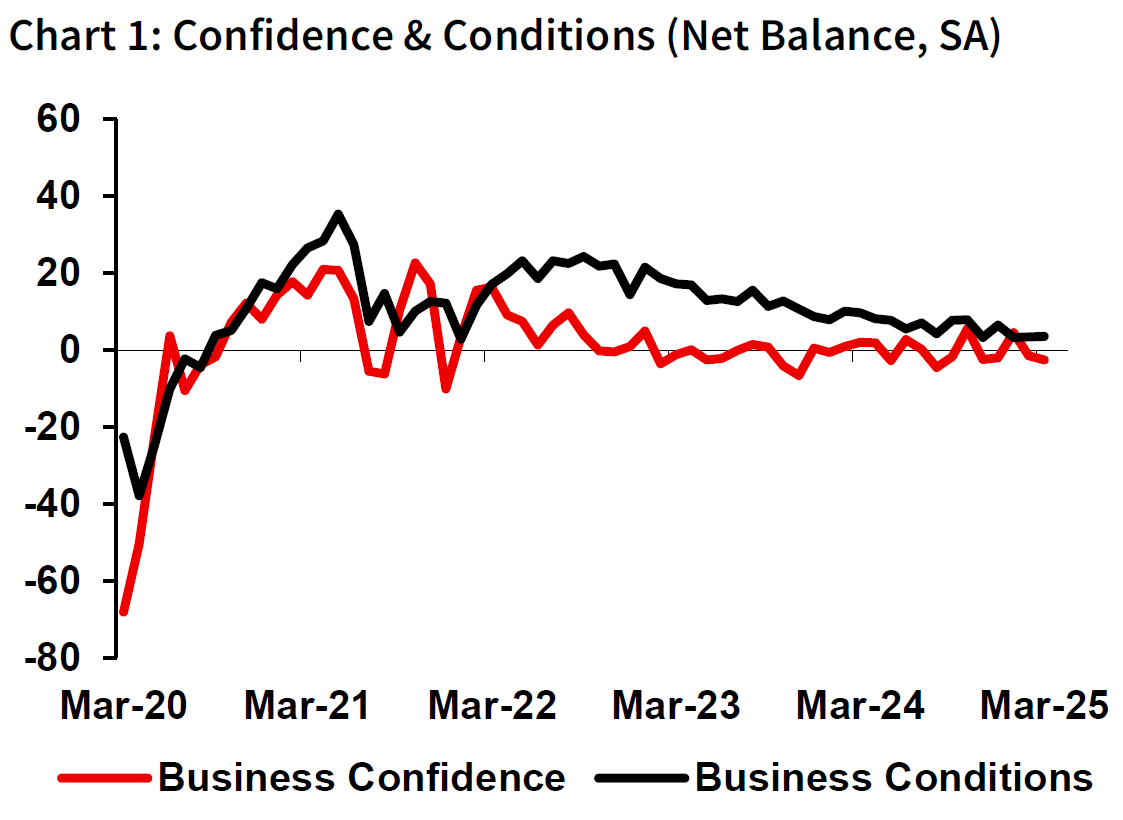

Australia NAB business confidence dips to -3 ahead of tariff impact

Australia’s NAB Business Confidence index dipped slightly from -2 to -3 in March, remaining firmly in negative territory. Business Conditions, however, edged up from 3 to 4, a modest improvement that still leaves them slightly below average overall.

Cost pressures remained broadly stable, with purchase costs rising 1.4% in quarterly equivalent terms and product price growth holding at 0.5%. Labour cost growth eased slightly.

NAB Chief Economist Sally Auld noted that conditions continue to vary across industries, with the services sector faring best while manufacturing and retail remain under pressure.

Importantly, this data predates the escalation of the global trade dispute, particularly the reciprocal tariff measures announced in early April. As Auld cautioned, these developments could "flow through to forward looking measures in the next survey.”

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8541; (R1) 0.8621; More...

Intraday bias in EUR/GBP remains on the upside for the moment. Current rise from 0.8221 is in progress for 0.8624 key cluster resistance next. Decisive break there will be an important indication of larger bullish trend reversal. On the downside, below 0.8520 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, the break of medium term channel resistance is a bullish signal. Down trend from 0.9267 (2022 high) could have completed at 0.8221, just ahead of 0.9201 key support (2022 low). Firm break of 0.8624 cluster resistance (38.2% retracement of 0.9267 to 0.8221 at 0.8621) will confirm this bullish case and target 61.8% retracement at 0.8867 next. Nevertheless, rejection by 0.8624 will keep medium term outlook neutral at best.

Australia NAB business confidence dips to -3 ahead of tariff impact

Australia’s NAB Business Confidence index dipped slightly from -2 to -3 in March, remaining firmly in negative territory. Business Conditions, however, edged up from 3 to 4, a modest improvement that still leaves them slightly below average overall.

Cost pressures remained broadly stable, with purchase costs rising 1.4% in quarterly equivalent terms and product price growth holding at 0.5%. Labour cost growth eased slightly.

NAB Chief Economist Sally Auld noted that conditions continue to vary across industries, with the services sector faring best while manufacturing and retail remain under pressure.

Importantly, this data predates the escalation of the global trade dispute, particularly the reciprocal tariff measures announced in early April. As Auld cautioned, these developments could "flow through to forward looking measures in the next survey.”

Aussie Westpac consumer sentiment slumps post-tariff shock; RBA seen tilting toward May rate cut

Australia’s Westpac Consumer Sentiment index plunged -6.0% in April, dropping from 95.9 to 90.1. The steep fall was notably skewed by the timing of the survey in relation to US announcement of reciprocal tariffs on April 2.

Respondents surveyed before the announcement showed only a modest dip in sentiment to 93.9. Those surveyed after reported a sharp drop of nearly 10% to 86.6. .

The sub-indices measuring sentiment towards the economy were particularly hard-hit, with the outlook for the next 12 months falling -5.7% to 90.5, and the 5-year outlook slipping back by -3.0%

With RBA set to meet on May 19-20, Westpac believes the weakening external backdrop, coupled with softer inflation, will push RBA to deliver another 25 bps rate cut. RBA is likely to become "much more focused on downside risks to growth than lingering questions about inflation".

Fed’s Goolsbee: Must rely on hard data, no simple playbook for stagflation risks

Chicago Fed President Austan Goolsbee expressed concern that escalating trade tensions—through tariffs, retaliations, and potential counter-retaliations—could recreate the turbulent economic conditions of 2021–2022 when inflation was "raging out of control."

In an interview with CNN, he warned that if the tariff threats materialize to their full extent, especially if met with proportionate responses, the US economy risks slipping back into a period of high inflation and stagnating growth.

However, Goolsbee also acknowledged that the situation remains fluid. He noted that negotiations could yet defuse the tension, especially if they result in new trade agreements. Referring to Treasury Secretary Scott Bessent’s optimism about a coming “golden age of trade.”

If stagflation begins to take hold, Goolsbee stressed, the Fed's response would not be straightforward. The appropriate policy path would depend heavily on how growth and inflation evolve in the coming months.

“Our job is to look at the hard data,” he said, underlining that in a scenario where both growth weakens and prices surge, there’s no “generic answer” to guide monetary policy.

Fed’s Kugler: Anchoring inflation expectations must remain top priority

Fed Governor Adriana Kugler emphasized the importance of keeping inflation expectations well anchored in comments delivered to a Harvard economics class.

She reaffirmed the Fed’s commitment to the 2% inflation target and stressed "It should be a priority to make sure that inflation doesn't move up".

Kugler also noted that economic activity in the first quarter may have been stronger than previously anticipated, driven by consumer front-loading ahead of expected tariff hikes.

While the full extent of tariff-related cost pass-through is yet to be seen, she acknowledged the financial strain such developments could place on households. That, she argued, is "exactly why we think we need to keep focus on that."