Sample Category Title

Fed’s Goolsbee: Tariff shock far exceeds expectations; Daly calls for caution

Chicago Fed President Austan Goolsbee and San Francisco Fed President Mary Daly both sounded cautious overnight amid rising uncertainty from the unfolding global tariff war.

Goolsbee highlighted the unexpected magnitude of the tariff impact, calling them a “way bigger” shock than anticipated. He likened them to a "negative supply shock" and acknowledged that Fed's appropriate policy response is unclear.

He warned of ripple effects through slower consumer and business activity, especially in a post-pandemic economy still scarred by past inflationary surges.

Meanwhile, Daly struck a more measured tone, noting that while she is "a little concerned" about the inflationary effects of tariffs, she emphasized Fed's current policy is well-positioned and policymarkers can "just tread slowly and tread carefully."

"The thing that's really important is you stay steady in the boat while you think about not what's happening over the last two days, but the net effect of the slate of changes that any administration wants to take," she added.

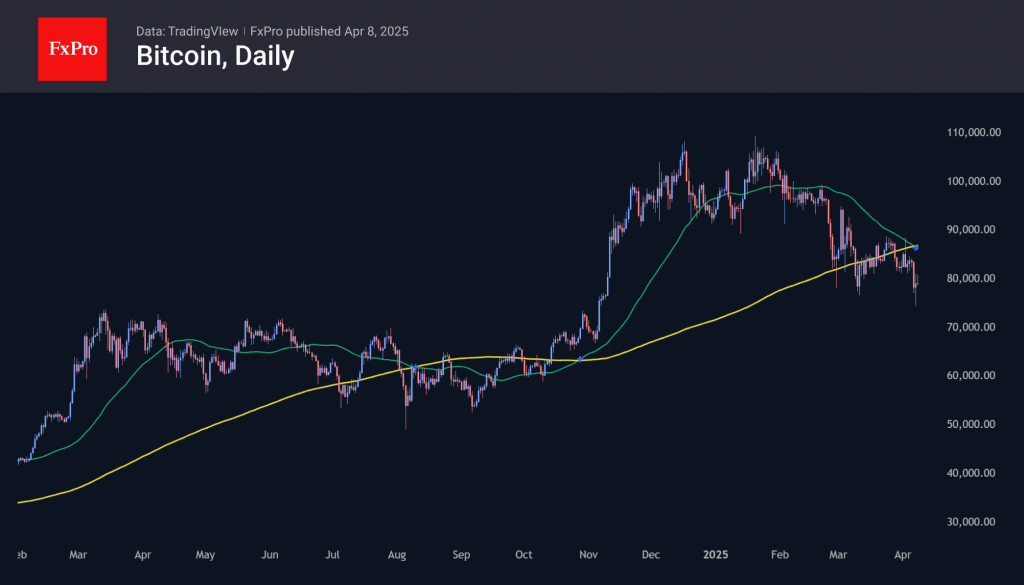

Bitcoin Stuck In The Struggle Zone—Will It Break Free?

Key Highlights

- Bitcoin price started a recovery wave after a sharp drop to $75,000.

- BTC is trading below a connecting bearish trend line with resistance at $81,500 on the 4-hour chart.

- Ethereum price declined heavily and even tested the $1,420 zone.

- WTI crude oil prices started a consolidation phase near $60.00.

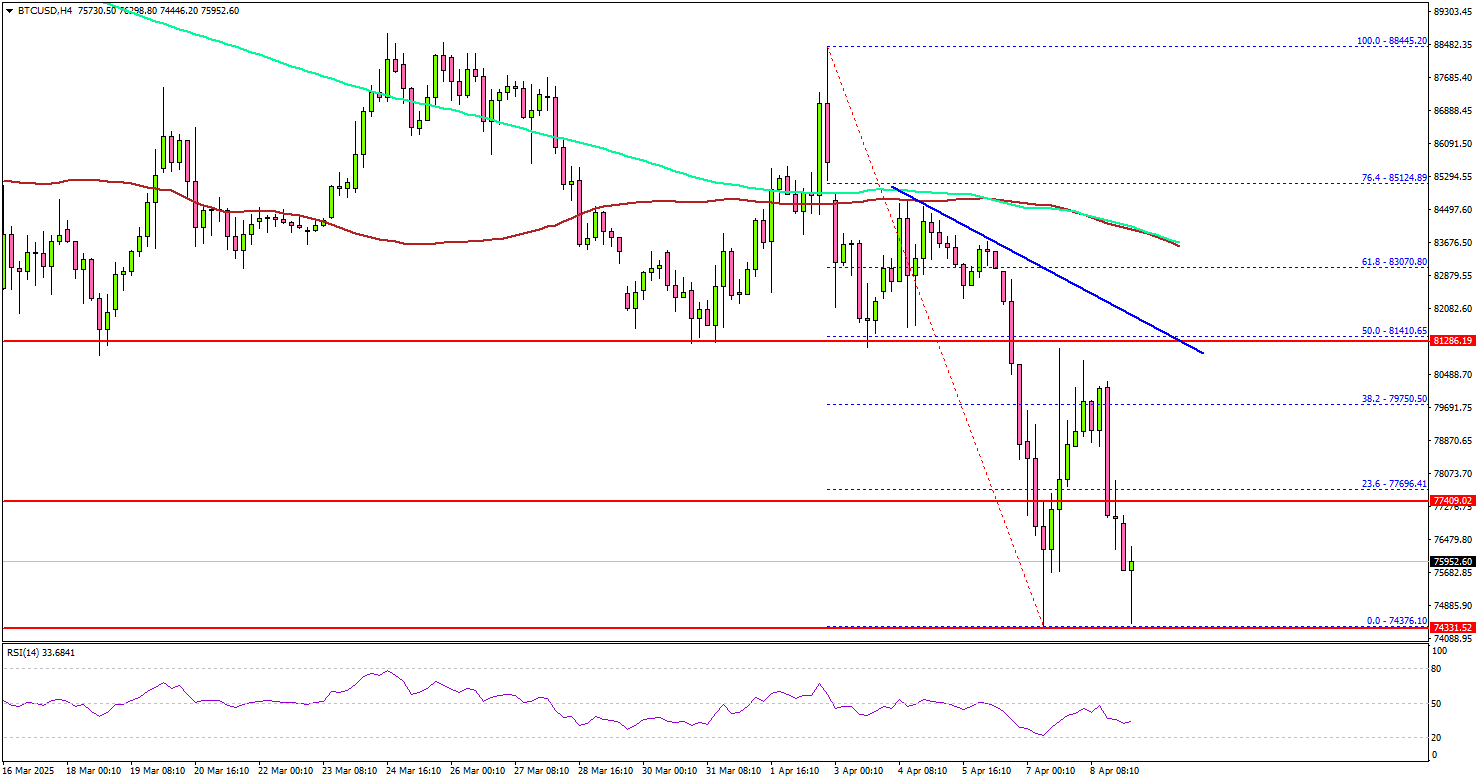

Bitcoin Price Technical Analysis

Bitcoin price started a major decline below $85,000 against the US Dollar. BTC declined below $80,000 and tested $75,000 before the bulls appeared.

Looking at the 4-hour chart, the price settled below the $82,000 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). A low was formed at $74,376 and the price started an upside correction.

There was a move above the $78,000 level. The price climbed above the 38.2% Fib retracement level of the downward move from the $88,445 swing high to the $74,376 low.

On the upside, the price could face resistance near the $81,500 level. There is also a connecting bearish trend line forming with resistance at $81,500 on the same chart. The trend line is close to the 50% Fib retracement level of the downward move from the $88,445 swing high to the $74,376 low.

The next key resistance is $83,000. The main resistance could be $85,000. A successful close above $85,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $88,000 level. Any more gains might call for a test of $90,000.

Immediate support is near the $78,000 level. The next key support sits at $76,800. A downside break below $76,800 might send Bitcoin toward the $75,000 support. Any more losses might send the price toward the $73,200 support zone.

Looking at Ethereum, there was a major decline below $2,000 and $1,800 before the bulls appeared near the $1,420 level.

Today’s Economic Releases

- FOMC Minutes.

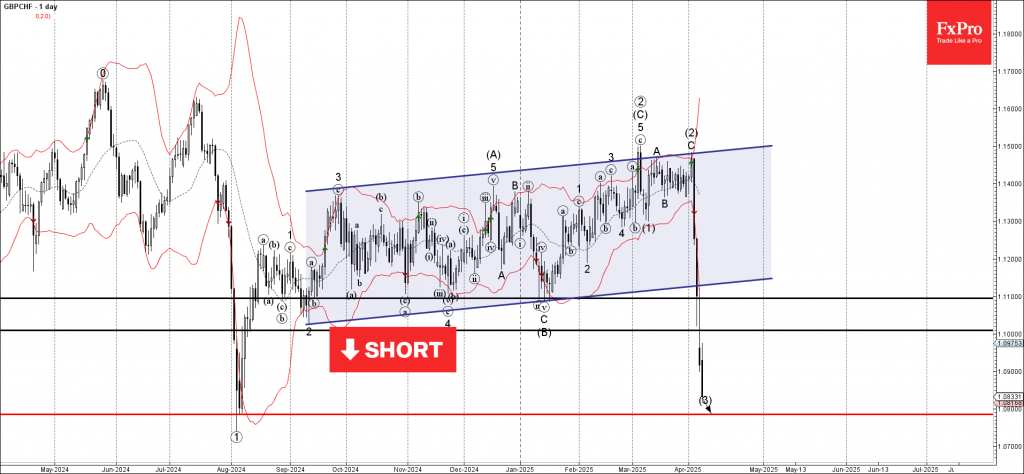

GBPCHF Wave Analysis

GBPCHF: ⬇️ Sell

- GBPCHF broke the support zone

- Likely to fall to support level 1.0785

GBPCHF currency pair recently fell sharply through the support zone between the support levels 1.1000 and 1.1100. The breakout of this support zone was preceded by the breakout of the daily up channel from September.

The breakout of these support levels accelerated the active intermediate impulse wave (3) from the start of August.

Given the strongly bullish Swiss franc sentiment seen recently, GBPCHF currency pair can be expected to fall to the next support level 1.0785, the target price for the completion of the active intermediate impulse wave (3).

WTI Wave Analysis

WTI: ⬇️ Sell

- WTI broke the long-term support zone

- Likely to fall to support level 55.00

WTI crude oil recently broke the long-term support zone set between the support levels 60.00 and 65.00. This support zone has stopped all downward corrections from the middle of 2021.

The breakout of this support zone accelerated the active downward impulse wave 3, which belongs to the intermediate impulse wave (3) from the start of 2024.

Given the strong downtrend seen on the weekly WTI charts, WTI crude oil can be expected to fall to the next support level 55.00, the target price for the completion of the active impulse wave (3).

CADCHF Wave Analysis

CADCHF: ⬇️ Sell

- CADCHF reversed from pivotal resistance level 0.6050

- Likely to fall to support level 0.5935

CADCHF currency pair recently reversed from the resistance zone between the pivotal resistance level 0.6050 (former monthly low from March) and the 50% Fibonacci correction of the downward impulse from the start of April.

The downward reversal from resistance level 0.6050 continues the active impulse wave iii of the intermediate impulse wave (3) from the end of November.

Given the clear daily downtrend and the strongly bullish Swiss franc sentiment seen today, CADCHF currency pair can be expected to fall to the next support level 0.5935.

Gold (XAU/USD) Grinds Above $3000/oz. Are Bulls Ready to Take Charge?

- Gold (XAU/USD) is trading above $3000/oz, facing resistance but showing bullish signals.

- Tariff developments and US President Trump's comments are key drivers of market sentiment and gold prices.

- Gold ETF flows were strong in Q1 2025, with a record $21 billion inflow, but April data will be crucial.

- Technical analysis indicates key support levels at 3000, 2982, and 2950, and resistance at 3025 and 3050.

Gold prices have been on a grind higher this morning but apprehension and caution are still evident across financial markets. Gold's decline after President Trump's ‘liberation day’ tariffs were announced did come as a surprise to many but I for one had feared that a lot of the tariff risk had been priced in.

If I am honest however, I did not see such a sharp selloff even if markets had already priced in the tariff announcement. Since the drop, Gold's attempts at a recovery have been met with persistent selling pressure.

There does seem to be a disconnect between Gold and historical trends or price drivers. What I mean by this is that Gold is usually sensitive to moves by the US Dollar, however over the past 12-18 this was not the case. This has continued now with the tariff announcement as traditional safe havens like the CHF and JPY benefitted while what I would consider the most traditional safe haven, Gold struggled.

The factors for this could be endless but today we are seeing a similar story. Comments from US President Donald Trump have helped spur on risk assets as the US President spoke about making tariff deals. President Trump said that a delegation from South Korea is on its way and that he is waiting for China who in his words said ‘China also wants to make a deal, badly’.

This has given risk assets a boost but at the same time Gold has also enjoyed a largely positive day thus far. Tariffs risks no donut persist, but for the time being sentiment does seem to have improved.

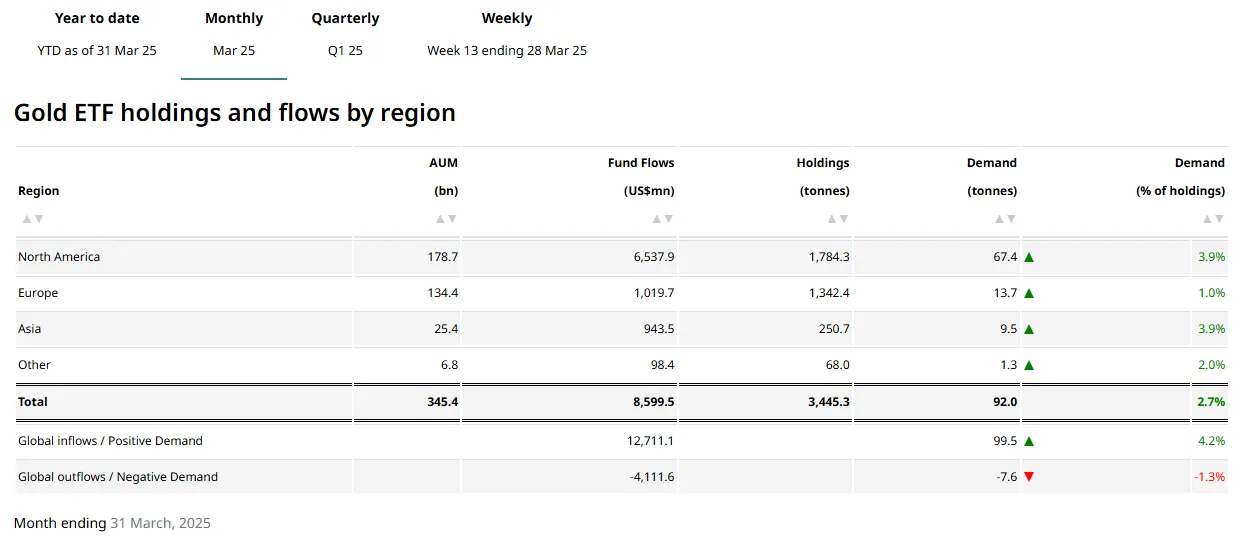

Gold ETF March report; Flows were high but April data will be more intriguing

Gold ETF flows have been discussed in a few of my articles of late, with the World Gold Council releasing the March report earlier in the day. I did not expect too many surprises though as tariff announcements came out in April. The next issue should give us more insights on that and how Gold ETF flows fared in the days after the tariff announcement.

When it comes to March and Q1 as a whole, ETF flows were strong.

Gold-backed ETFs saw a strong $8.6 billion inflow in March, pushing total Q1 inflows to $21 billion (226 tons). This was the second-largest quarterly inflow in dollar terms, just behind Q2 2020's $24 billion (433 tons). North America and Europe made up 83% of these inflows, with 61% and 22% shares, respectively. Asia contributed 16%, which is impressive considering it only holds 7% of global assets under management (AUM).

Europe’s Q1 inflows of $4.6 billion were its best since Q1 2020. With rising gold prices, global AUM hit a new record high of $345 billion, up 13% in March and 28% for the quarter. Collective gold holdings also grew by 92 tons in March, reaching 3,445 tons by the end of the month. This is the highest level since May 2023 and just 470 tons below the all-time record set in October 2020.

Source: World Gold Council

Given the selloff now in early April and depending where Gold ends the month, I will be very curious to gauge the data next month.

For now and the rest of the week, I expect tariff developments to be the main driving force of market sentiment and Gold as well.

Technical Analysis - Gold (XAU/USD)

From a technical analysis standpoint, Gold prices have edged their way higher since yesterday's lows at 2956.

The daily candle closed around the support level at 2982 before a bullish move in the Asian session leaves Gold trading 1% up for the day at the time of writing.

For now immediate resistance at 3025 has held firm with 3048/3050 the next key level to pay attention to.

The RSI period 14 on the daily timeframe is flashing a bullish signal as it crosses above the 50 neutral level which could hint at a shift in momentum. It will however depend on how the daily candle closes and see if it maintains the momentum and finishes above the 5o handle.

Today the 3000 psychological level has held firm and will need to form a base if bulls are to take control and revisit the early April highs.

If the 3000 handle gives way, 2982 and 2950 will catch my attention as potential areas of support.

Gold (XAU/USD) Daily Chart, April 8, 2025

Source TradingView

Support

- 3000

- 2982

- 2950

Resistance

- 3025

- 3050

- 3075

New Zealand’s Central Bank Expected to Lower Rates by a Quarter-Point

The New Zealand dollar has rebounded on Tuesday. NZD/USD is trading at 0.5615, up 1.3% on the day. This follows a 5% plunge over the past two days.

RBNZ widely expected to cut rates

The Reserve Bank of New Zealand is widely expected to lower interest rates by a quarter-point at its rate meeting on Wednesday. The markets have priced in a quarter-point cut at 75% and a jumbo half-point cut at 25%. The cash rate currently stands at 3.75%

The RBNZ slashed rates by a half-point in February, a response to weak economic growth and an inflation rate of around 2%, the midpoint of its target band.

The market meltdown and escalation in trade tensions due to new US tariffs could force the RBNZ to lower rates faster and deeper than previously expected. There is massive uncertainty in the air and the central bank will have to re-evaluate inflation and growth expectations, given the tariff turmoil.

There is growing talk of a global recession, which would badly hurt New Zealand's export-reliant economy. China is New Zealand's largest trade partner and the escalating trade tensions between the US and China could turn into a New Zealand nightmare. China has imposed 34% reciprocal tariffs on the US, drawing a threat from President Trump that he will counter with a 50% tariff if the Chinese tariff is not removed.

The RBNZ is dealing with the tariff crisis without Governor Adrian Orr, who suddenly resigned last month in the middle of his five-year term. The government has appointed Christian Hawkesby as Governor for a six-month term, after serving as the acting governor after Orr resigned.

NZD/USD Technical

- NZD/USD pushed above resistance at 0.5565 and tested resistance at 0.5623. The next resistance line is 0.5704

- 0.5484 and 0.5426 are providing support

Sunset Market Commentary

Markets

Core bonds lost ground today. Bunds underperformed US Treasuries, switching places with yesterday. The moves’ sizes differ from Monday too. The violent intraday swings back then made way for a steady and solid rise in German rates with gains varying between 4.4 and 9 bps in a bear flattening move. The jury’s still out, though, whether yesterday marked the low point (especially at the front) against the backdrop of the highly unpredictable trade narrative. ECB’s Simkus on the matter said that the US tariff announcement was much more disappointing than thought; Germany’s Nagel said it significantly worsened the global outlook and for VP de Guindos it represents a paradigm shift. The former hasn’t made up his mind for April yet but in any case ruled out the need to talk about a 50 bps cut. Money markets aren’t contemplating such a move either. Rates in the US add 3.4-7 bps across the curve. Comments from US Treasury Secretary Bessent helped somewhat by keeping the door for negotiations open (‘Tariffs will be a melting ice cube if [trade talks are] successful’) in the same vein as Japan’s push for trade talks this morning triggered a 6% rise in the Nikkei stock index. The 10-yr crawls back above the 4.2% support-turned-into resistance zone. Simply looking at the chart is baffling. In mere hours the most watched and traded 10-yr bond yield erased the 35 bps loss since Trump’s Liberation Day. Today’s gains included, it’s even as if nothing happened. Rising risk premia as a buffer for the huge uncertainty hold sway and are (at least partially) compensating for any growth-related downward pressures. European long-term yields enjoy a floor for similar reasons. Today’s eco calendar contained no major releases but we do look out for tonight’s 3-yr auction and even more tomorrow’s 10-yr and Thursday’s 30-yr sale. They’ll be closely watched for signs whether or not global investor appetite for US debt is already abating. FX markets are basically a mirror image of yesterday, when small and less liquid currencies were dumped and most majors including the dollar and the euro (as well as CHF for risk aversion reasons) gained. The US greenback today underperforms global peers, allowing EUR/USD even with a lackluster euro to eke out a small gain to 1.095. EUR/GBP briefly rose towards 0.86 before fatigue kicked in after the recent stellar rally. The pair currently hovers little changed around 0.856. GBP/USD does bounce back marginally from the 1.27 area to 1.277. The Aussie and kiwi dollar top the leader board while CHF is extending its recent bull run. China’s yuan closed at the weakest level since September 2023. This morning’s fixing suggests authorities are ready and willing to use the currency as a trade war tool. Stock markets trade firm in the green but that doesn’t compensate much for the sharp declines nor does it change the dire technical picture. The EuroStoxx50 adds about 3%, WS opens with similar gains.

News & Views

After elevated inflation figures in January and in February, March inflation in Hungary came in on the softer side of expectations. Prices were unchanged M/M with the Y/Y-measure declining from 5.6% to 4.7%. In its flash analysis, the central bank (MNB) indicated that while overall inflation stabilized M/M, core inflation still rose by 0.3% but slowed to 5.7% Y/Y. The measure ex indirect taxes slowed to 5.4% from 6.0%. CPI ex processed food eased to 5.3% from 5.9%. Still, sticky price inflation rose marginally from to 5.9%. The annual inflation of tradables rose 0.6% M/M to 2.6% Y/Y. The annual prices of market services eased to 8.6%, largely attributable to the unwinding of the effect of last year’s backward-looking repricing. Prices rose by 0.6% M/M, reflecting accommodation and catering services. Banking and telecommunications services fees remained broadly unchanged. Food price inflation decreased to 6.2%, partially affected by profit margin caps introduced mid-March. HUF 2-y swap yields today declined 9.0 bps after the release as markets again ponder the chances of the MNB further reducing the policy rate below 6.5% in the second half of this year and/or early next year. Of course, aside for the inflation development, this remains highly conditional on the performance of the forint, which weakened back above EUR/HUF 400 in recent risk-off move.

After easing on the European reflation trade last month, the Swiss franc currently again strengthens closer to the key EUR/CHF 0.92/0.93 support area (currently 0.935). At last month’s policy meeting, the SNB could be relatively confident that inflation could stabilize in the lower part of the 0.0%/2.0% inflation target range. Recent strengthening of the franc including its impact on inflation however might force the SNB again to consider FX interventions or easing the policy rate back to 0% or even back into negative territory (currently 0.25%).

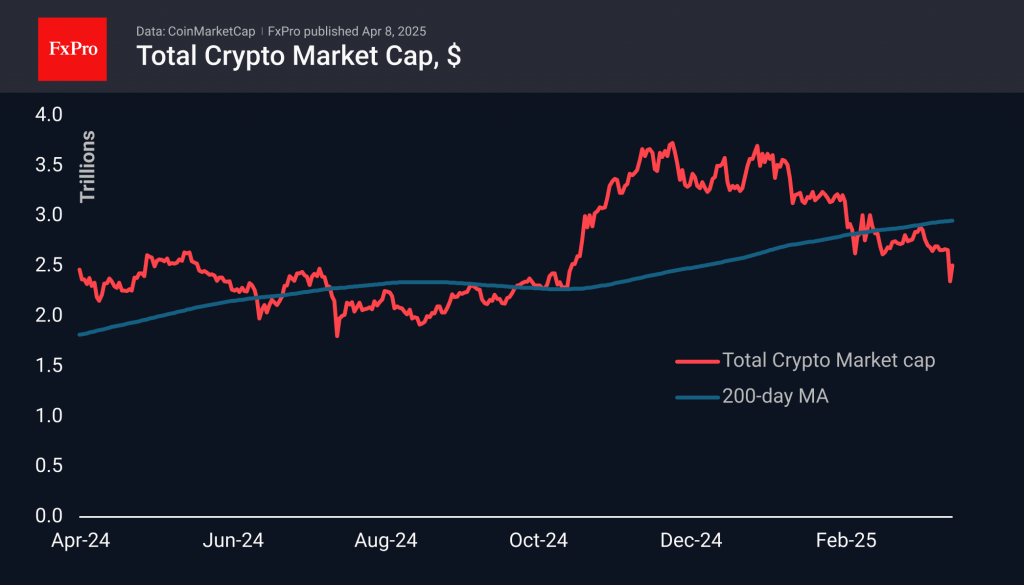

Crypto: A More Subdued Decline, Not Yet a Reversal

Market Picture

The cryptocurrency market found its footing on Monday with the start of active trading in Europe. However, that rebound from the $2.37 trillion level to $2.55 trillion appears to be losing steam. Even at current levels, the decline over the past seven days is over 8%. Without reliable signs of a reversal in the stock markets, the upward momentum could quickly fade. It looks like we are not seeing a reversal but only a stabilisation of the decline.

Bitcoin slipped below $75k at the start of the week, bouncing briefly above $80k on Monday and Tuesday. The technical picture for Bitcoin remains tragic. Earlier this month, a death cross formed when the 50-day average dipped below the 200-day. Last year, a similar signal had the opposite effect, recording a low a couple of days before the signal. But in the last couple of months, the downward trending 50-day has been acting as an effective resistance. In case of a market reversal, a consolidation above the 86k level, where it is now, would be an important signal of a break in the downtrend.

News background

According to CoinShares, global investments in crypto funds fell by $240 million last week after two weeks of inflows. Bitcoin investments decreased by $207 million, Ethereum by $38 million, Sui by $5 million, and Solana by $2 million, while XRP investments increased by $4.5 million and Toncoin by $1 million.

Coinshares suggests that the outflow of funds from cryptocurrencies is likely a response to recent news of US trade duties that pose a threat to economic growth.

Binance Research noted that macroeconomic factors like trade policy and rate expectations are increasingly driving cryptocurrency market behaviour, temporarily overshadowing underlying demand dynamics. Bitcoin’s correlation with traditional assets tends to rise during times of acute stress but weakens as conditions normalise.

Bitcoin’s hash rate surpassed the 1 ZH/s (zeta hash) mark for the first time in history. On 5 April, mining difficulty hit a record high (ATH) at 121.51 T. Meanwhile, the profitability of mining is under serious pressure due to falling BTC value and transaction fees.

Strategy company reported unrealised losses of $5.91 billion for Q1 2025.