Sample Category Title

Dollar Pressured as Markets Betting on a Dovish Fed

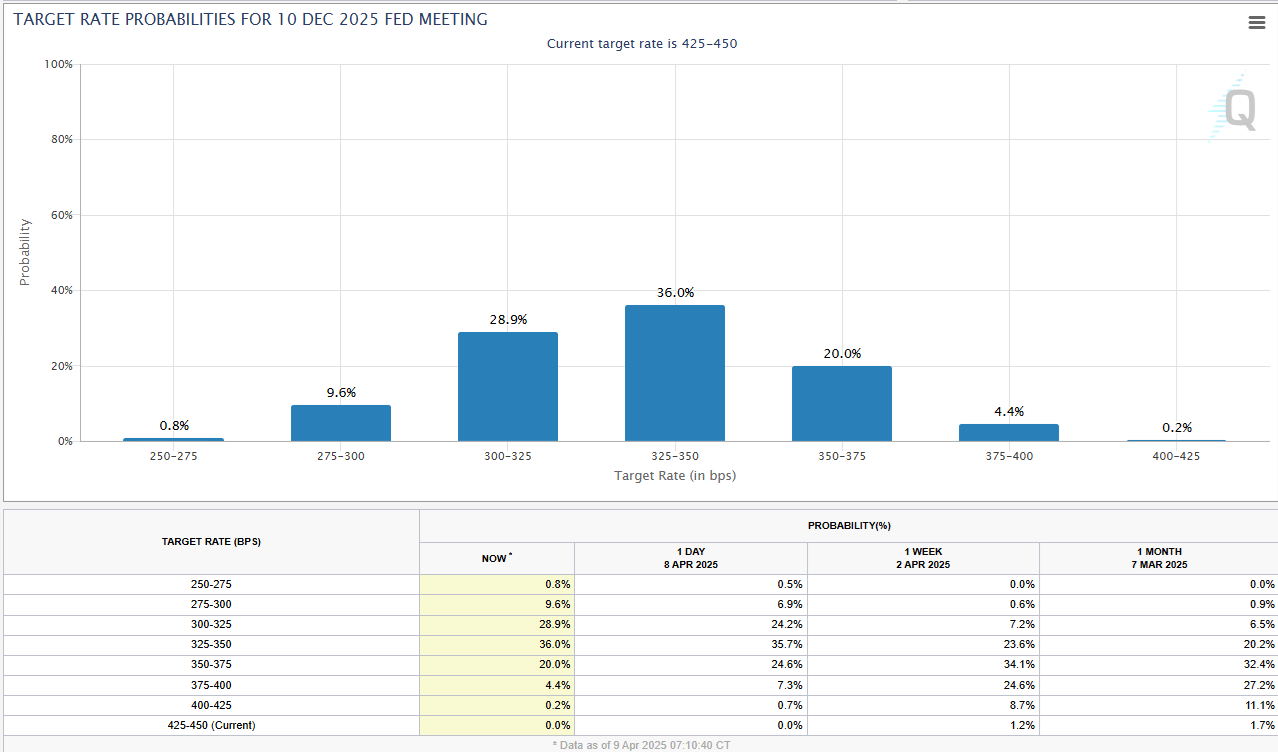

Over the past week, the probability of a key Fed rate cut in May jumped from 11% to 47% and reached nearly 60% on Tuesday.

Market now pricing 100-point rate cut to 3.25%-3.50% with 75% probability.

For year-end, the market now sees the prevailing scenario as a 100-point rate cut to 3.25%-3.50% or lower with a 75% probability, although a month ago, those odds were barely above a quarter.

This could be a technical move reflecting a flight to defensive short-term government bonds. The jump in 10- and 30-year long-term government bond yields, which typically fall along with declining short-term yields, supports this hypothesis.

Such erratic movements increase pessimism about the outlook for equities, where liquidation of margin positions may continue or intensify.

While this is usually favourable for the dollar, we are now seeing increased pressure on the US currency due to the sell-off in equities and long-term bonds.

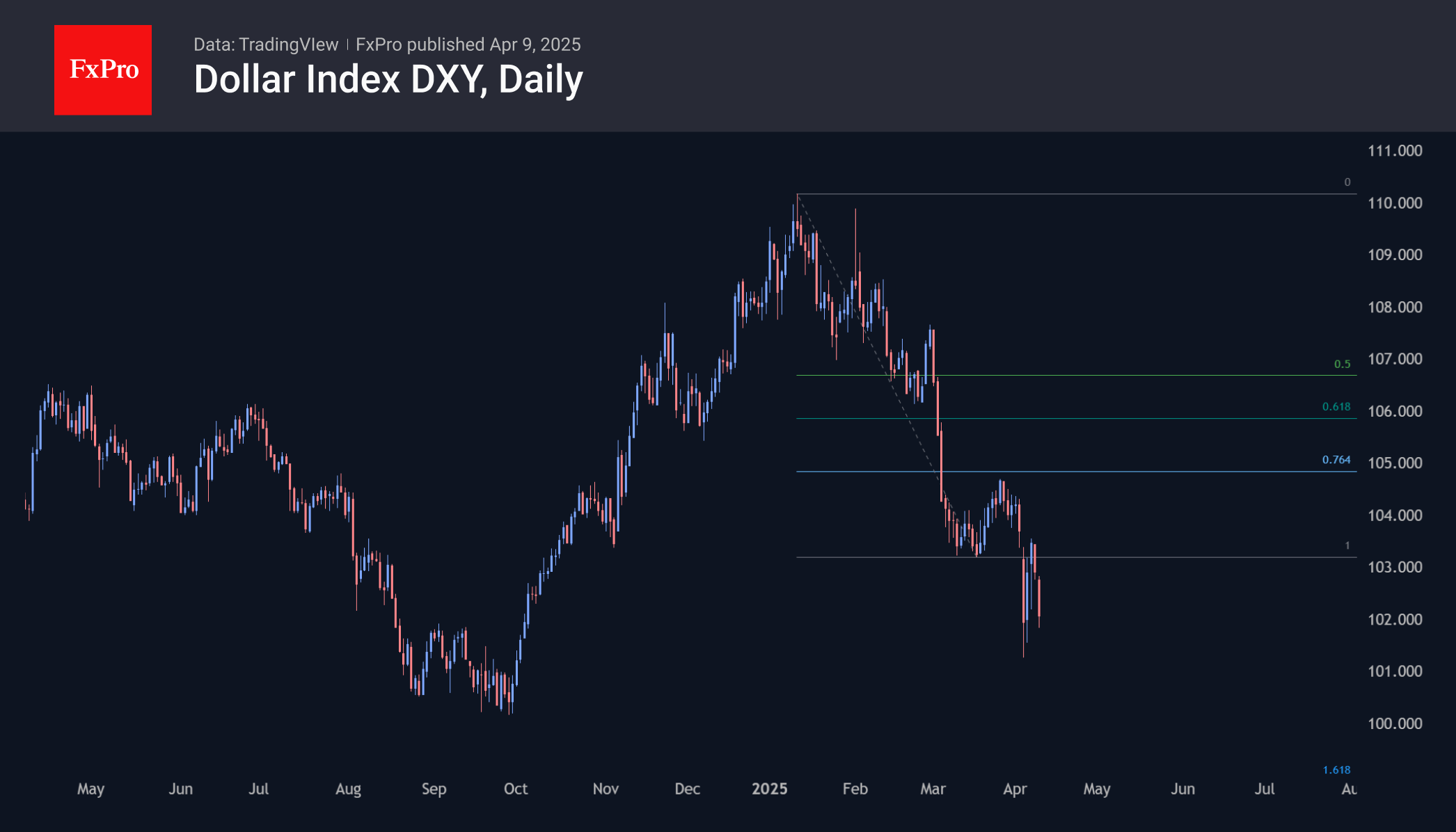

Dollar index has already been in an active decline phase since early April

Technically, the dollar index has already been in an active decline phase since early April, having broken sharply below the March support area. The rebound at the start of the week only closed the gap without changing the pattern, which suggests a fall to the 99 area – almost 3% from current levels.

Although other major economies are also expected to accelerate rate cuts, markets tend to play down the changes in the US first. This has caused the dollar to rise before the rate hike cycle begins in 2022 and fall before the first cuts in 2024 and 2020. In terms of stress and uncertainty, the current situation resembles March 2020.

EUR/USD Outlook: Euro Benefits from US-China Escalation, Markets Price in April ECB Rate Cut

- EUR/USD has risen due to escalating US-China trade tensions, despite markets anticipating an ECB rate cut in April.

- China has announced tariffs on US goods in response to US tariffs, increasing fears of further trade war escalation, Euro becomes a beneficiary.

- Technically, EUR/USD is testing resistance at the 1.1100 hurdle and approaching overbought levels, suggesting a retracement may be on its way.

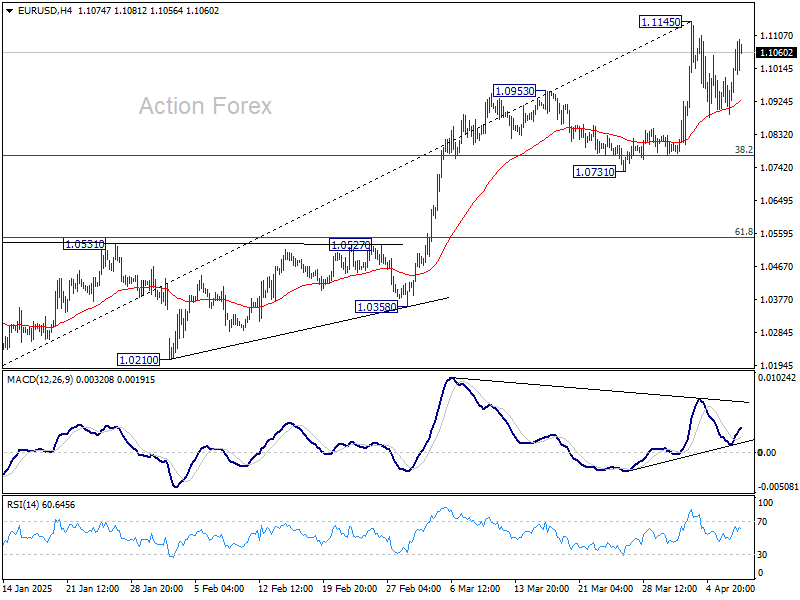

EUR/USD has been on a good run this week and jumped this morning as tensions between the US and China escalated. The latest escalation has left the US Dollar and in particular the US Dollar index on the back foot.

The DXY is testing last week's lows at the time of writing and this has helped EUR/USD rise despite markets pricing an ECB rate cut in April.

US Dollar Index Daily Chart, April 9, 2025

Source: TradingView

The performance of the Euro has surprised me to say the least. This morning we saw traders fully price ECB rate cuts in April for the first time. This was followed by Morgan Stanley lowering the Euro area's 2025 GDP forecast to 0.8% vs prior forecast of 1.0% while also saying that they expect the ECB benchmark rate to reach 1.5% in December 2025 vs the prior forecast of June 2026.

This was further echoed by a Reuters report which stated that the European Central Bank (ECB) now expects Trump’s tariffs to hurt the Eurozone's growth more than first thought. Sources say the earlier estimate of a 0.5 percentage point impact is too low, with one suggesting it could exceed 1 percentage point.

These are supposedly dovish moves for the Euro which under normal circumstances might have seen a market reaction. However, given the dynamics around the trade war markets have been focusing elsewhere. We have discussed this at length of late, the trade war overshadowing economic data releases and news. This trend seems to be intact for now.

US-China trade war escalates

US President Donald Trump's additional tariffs on China went into effect yesterday with China refusing to bow to President Trump's wishes. Instead Chinese authorities through the Finance Ministry announced that it will impose additional tariffs of 84% on US goods to come into effect on April 10.

The news sent risk assets like S&P 500 tumbling this morning as fears ramp up over further escalation. China added more firm to the unreliable list as China's Premier Li chaired a symposium on the economic situation with experts and businesses.

Premier Li acknowledged that while external factors may cause pressure the Government is ready to deal with it. Premier Li also touched on expanding local demand, something he called a long-term goal.

The Federal Reserve (Fed) will release the minutes from its March meeting later today. However, since this meeting happened before the tariff announcements, traders might not pay much attention to it as tariffs continue to dominate the discourse.

If this is the case, expect any further tit-for-tat between US-China to lead to potential EUR strength against the US dollar based on recent history.

Technical Analysis on EUR/USD

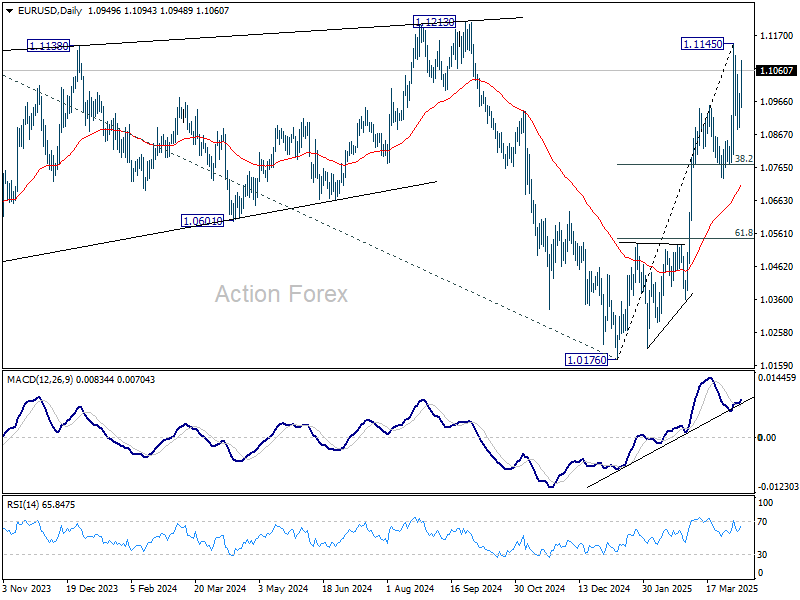

EUR/USD Daily Chart, April 9, 2025

Source: TradingView.com

Looking at the EUR/USD daily chart, the pair is on course for a third successive day of gains.

The pair is currently testing an area of resistance at the 1.1100 hurdle, can the rally continue?

There is definitely scope for further upside but I think that will require a prolonged standoff between the US-China. Any deal that may arise between the two could send EUR/USD tumbling..

As we have seen above, tariffs are having an impact on everything from growth to monetary policy at present.

Looking at the period 14-RSI and it is approaching overbought levels once more. This means that a retracement the likes of which occurred on April 3 could repeat itself.

This is definitely worth monitoring moving forward.

OAU-PRS-236-MarketPulse-variant1-Square

Key levels to pay attention to

Support

- 1.1000

- 1.0948

- 1.0900

Resistance

- 1.1100

- 1.1200

- 1.1250

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0901; (P) 1.0946; (R1) 1.1004; More...

Range trading continues in EUR/USD and intraday bias remains neutral. More consolidations could be seen, but in case of another retreat, downside should be contained by 38.2% retracement of 1.0176 to 1.1145 at 1.0775. On the upside, above 1.1145 will resume the rally from 1.0176 to 1.1213/74 key resistance zone next.

In the bigger picture, fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

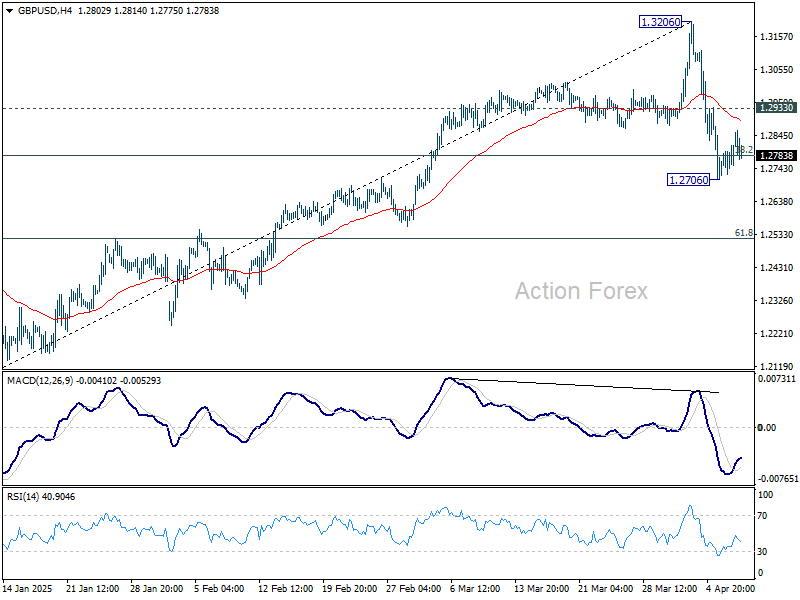

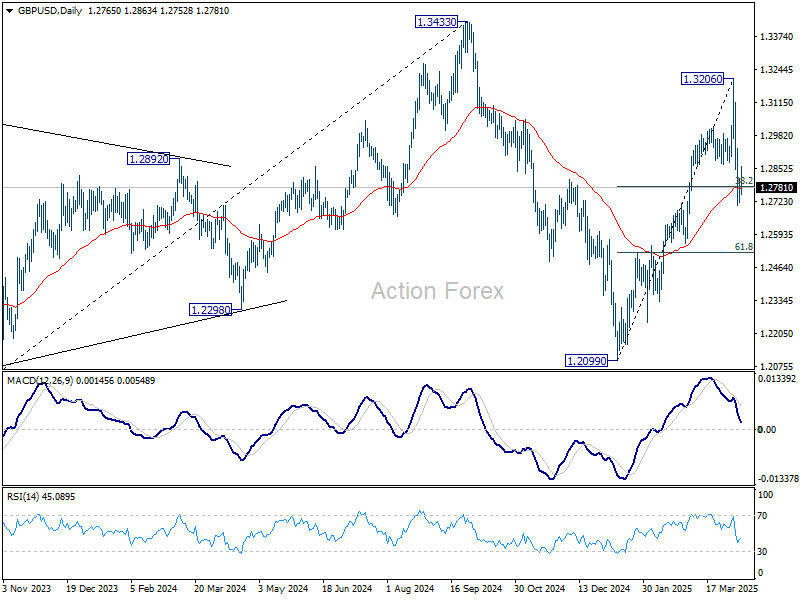

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2713; (P) 1.2764; (R1) 1.2815; More...

GBP/USD is staying in consolidation above 1.2706 and intraday bias remains neutral. Risk will stay on the downside with 1.2933 minor resistance intact. Break of 1.2706 will resume the decline from 1.3206 to 61.8% retracement of 1.2099 to 1.3206 at 1.2522. Nevertheless, firm break of 1.2933 will bring stronger rebound back to retest 1.3206 high.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

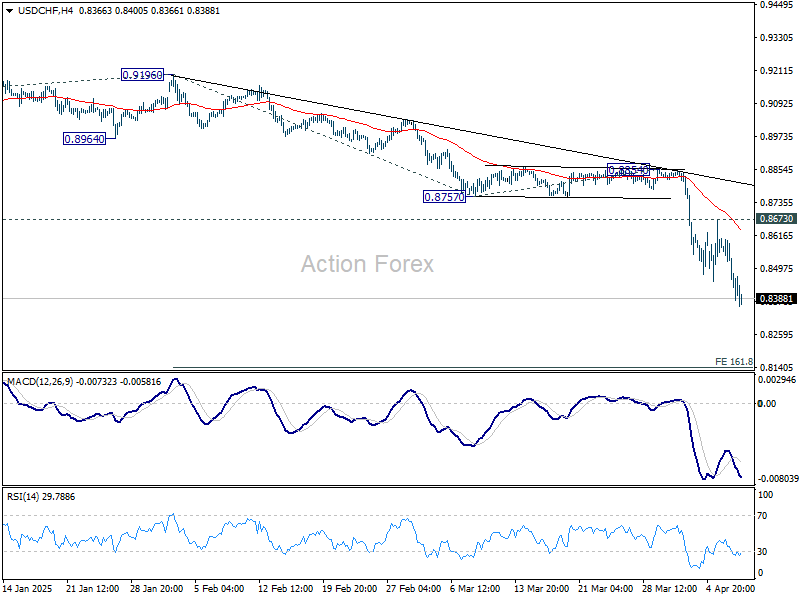

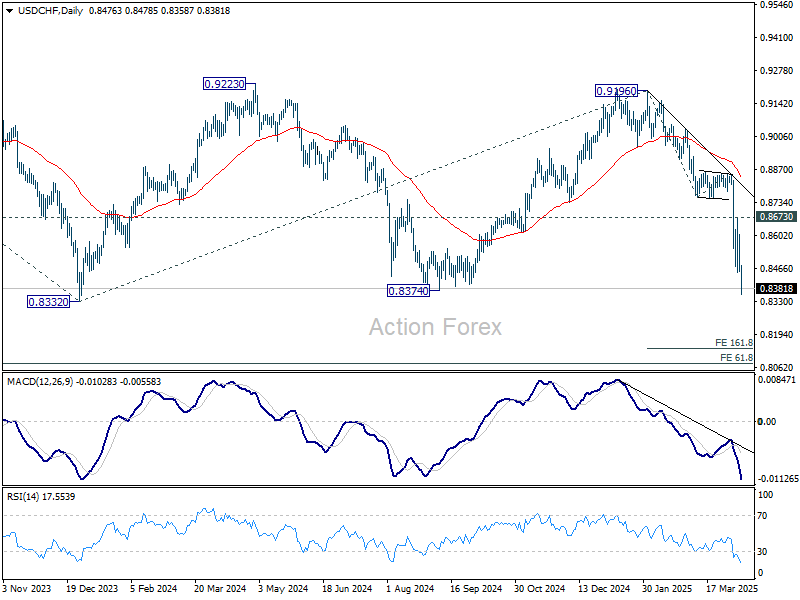

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8416; (P) 0.8518; (R1) 0.8581; More…

Intraday bias in USD/CHF remains on the downside at this point. Current fall from 0.9196 is in progress. Sustained break of 0.8332/8374 key support zone will confirm larger down trend resumption. Next near term target is 161.8% projection of 0.9196 to 0.8757 from 0.8854 at 0.8144. On the upside, break of 0.8673 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

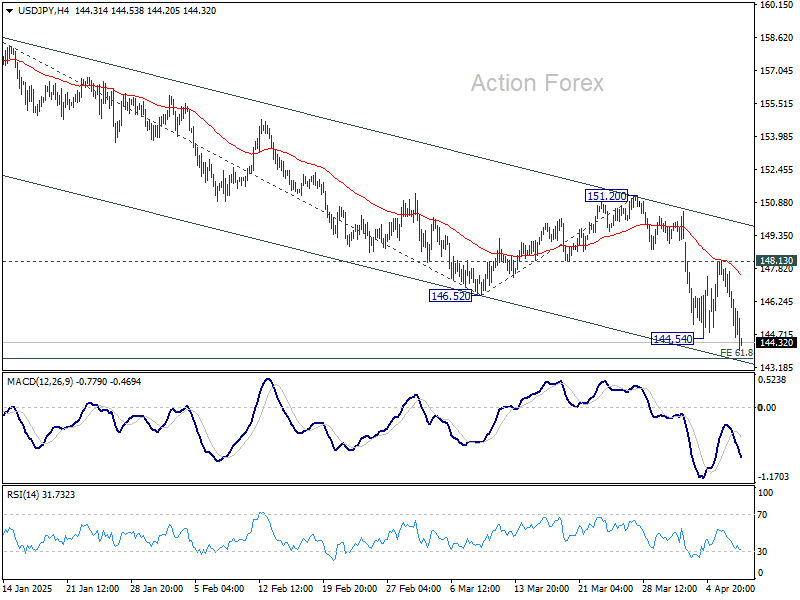

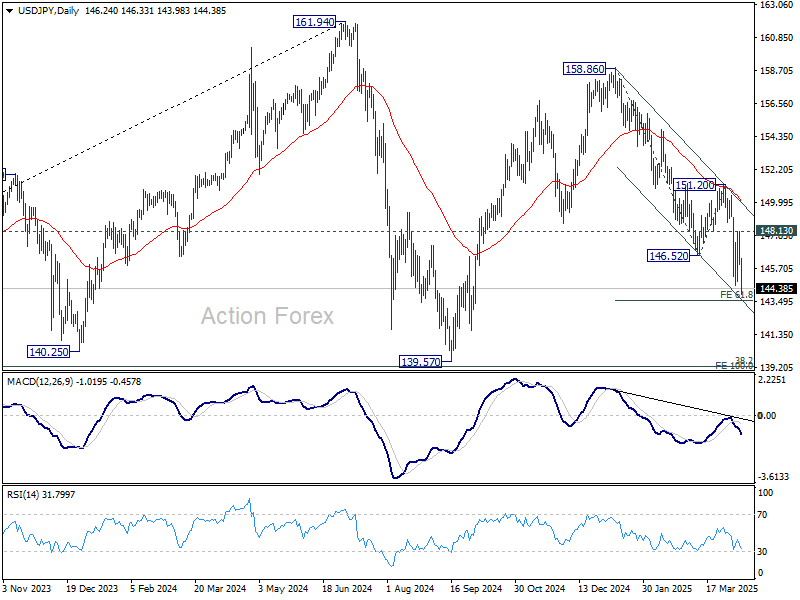

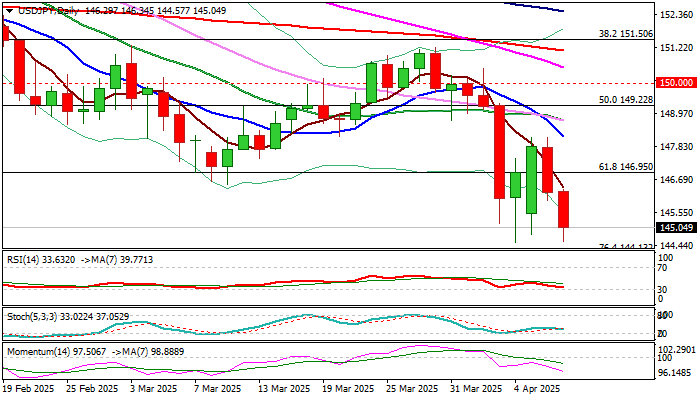

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.46; (P) 146.79; (R1) 147.61; More...

Intraday bias in USD/JPY is back on the downside with break of 144.54 support. Fall from 158.86 is resuming to 158.86 to 146.52 from 151.20 at 143.57. Break there will target 139.57 low. On the upside, break of 148.13 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

From Trade War to Bond Shock: Global Markets Face Multi-Front Crisis

The relentless selling pressure in global markets shows no sign of abating, with European stocks and US futures once again under fire today. China’s latest retaliatory move to hike tariffs on US goods from 34% to 84% has reignited investor fears, just as the US implemented its own increase to a staggering 104% on Chinese imports. The ongoing trade war escalation between the world’s two largest economies is now moving rapidly from trade tension to a global financial shock.

China is clearly signaling it has no intention of backing down. Beyond higher tariffs, Beijing’s commerce ministry added multiple US entities to an export control list and labeled several more as “unreliable.” It also filed a pointed complaint with the WTO, accusing Washington’s “reckless move” of destabilizing global trade.

An unusual element of this market meltdown is the rare simultaneous collapse of all major US assets: stocks, Dollar, and Treasuries. In particular, yields on the 10-year note have surged back above 4.4%, up from 3.9% just last week. This sharp move has sparked fears of forced liquidation, margin calls on leveraged positions, which could drastically tighten up liquidity in the markets.

Market watchers have floated multiple theories as explanations for the sudden jump in yields. Some see it as a predictable consequence of the US push to reduce bilateral trade imbalances, which may curb or even reverse foreign demand for American debt. Besides, Treasuries could become a retaliatory tool in a geopolitical standoff. While each theory differs in detail, all point to an erosion of liquidity and confidence in a market once considered the bedrock of global finance.

Technically, 10-year yield's break above 4.387 resistance is alarming. It suggests that fall from 4.809 has completed as a three-wave corrective move at 3.886. Risk will now stay heavily on the upside as long as 55 D EMA (now at 4.321) holds. Further rally could be seen back to 4.809 resistance. Firm break there could pave the way back to 4.997 high.

In the currency markets, Dollar is again the worst performer of the day. Sterling and Kiwi trail close behind, the latter pressured further by RBNZ’s rate cut and its dovish forward guidance. Yen and Swiss Franc are once again the preferred safe havens, with the Aussie showing surprising resilience—likely more a pause in its decline than a sign of strength. Euro and Loonie sit somewhere in the middle.

At the time of writing, FTSE is down -3.57%. DAX is down -4.03%. CAC is down -4.07%. UK 10-year yield is up 0.199 at 4.818. Germany 10-year yield is down -0.005 at 2.622. Earlier in Asia, Nikkei fell -3.93%. Hong Kong HSI rose 0.68%. China Shanghai SSE rose 1.31%. Singapore Strait Times fell -2.18%. Japan 10-year JGB yield rose 0.003 to 1.282.

ECB’s Villeroy: Trade uncertainty threatens financial stability, strengthens case for rate cut

French ECB Governing Council member Francois Villeroy de Galhau warned today that mounting economic uncertainty from escalating trade tensions is posing risks to financial stability, particularly increasing credit risks for some financial institutions.

While he emphasized the resilience of French banks, he noted that leveraged hedge funds could come under significant liquidity pressure.

Writing in his annual letter to President Macron, Villeroy assured that both Bank of France and ECB are “fully mobilised” to safeguard financial stability and ensure adequate liquidity.

Speaking to journalists, Villeroy said the recent US announcement of sweeping “reciprocal” tariffs only adds to the case for further monetary easing. “We still have room to cut rates,” he stated.

ECB’s Knot: Trade war a stagflationary shock, inflation impact will rise over time

Dutch ECB Governing Council member Klaas Knot warned today that the escalating trade war constitutes a “negative supply shock” and should be considered “stagflationary” in nature.

Knot also cautioned that as time progresses, the economic impact is more likely to "more inflationary rather than deflationary".

ECB’s priority, he said, is to monitor how and when these tariffs start to meaningfully affect economic activity and corporate decision-making. However, next week’s policy meeting would be too soon to revise projections.

Knot also noted that despite the growing market stress, financial market functioning has so far been "preserved". He credited the hedge fund sector's proactive deleveraging for this resilience, saying they were well-prepared for the turbulence and capable of meeting margin calls—unlike in past market episodes.

BoJ’s Ueda: Rate hikes still on table, but trade uncertainty clouds outlook

BoJ Governor Kazuo Ueda reaffirmed today that the central bank remains open to further rate hikes if Japan’s economic recovery continues as projected. He added that current trends in both the economy and inflation are "roughly in line" with BoJ’s forecasts.

He added that the policy board will make decisions with a "without pre-conception" mindset, and assess whether the outlook materializes as expected.

However, Ueda flagged growing concerns over trade developments globally, warning of "heightening uncertainty over developments in each country's trade policy".

"We need to pay due attention to risks," he warned.

RBNZ cuts 25bps, trade barriers as downside risk to both growth and inflation

RBNZ delivered a widely expected 25bps cut in the Official Cash Rate, bringing it to 3.50%. The policy statement highlighted that the recently announced global trade barriers create "downside risks to the outlook for economic activity and inflation" in New Zealand.

The central bank noted that with inflation close to the midpoint of its target range, it is in the "best position" to respond to economic shifts. RBNZ added it has "has scope to lower the OCR further as appropriate", depending on how the impact of tariffs evolves.

This leaves the door wide open for further easing, particularly if global economic headwinds intensify or domestic data disappoints.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.46; (P) 146.79; (R1) 147.61; More...

Intraday bias in USD/JPY is back on the downside with break of 144.54 support. Fall from 158.86 is resuming to 158.86 to 146.52 from 151.20 at 143.57. Break there will target 139.57 low. On the upside, break of 148.13 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

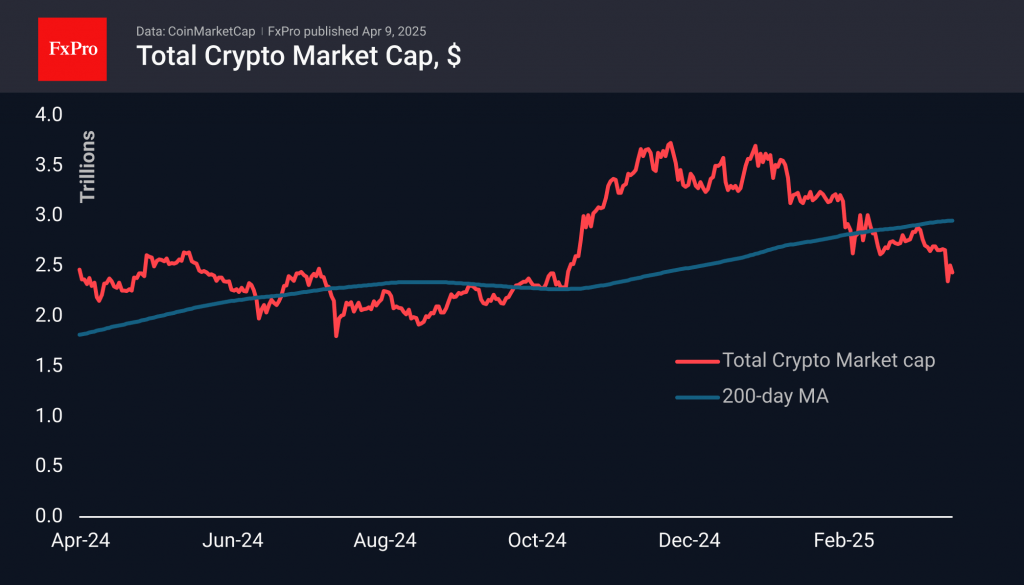

Crypto Market Has Returned to This Week’s Lows

Market Picture

Crypto market capitalisation declined more than 2% in 24 hours to $2.46 trillion. As was the case at the beginning of the week, the intraday dip below $2.40 trillion attracted buyers. As is often the case, an important resistance level became support. From around these levels, we saw the start of the rally after Trump’s election, and now the fightback is intensifying again, as seen in the increased trading volumes.

Crypto market sentiment was at its lowest point in the last five weeks, with the corresponding index to 18 (extreme fear) declining. By the index’s design, these levels are buying opportunities. However, it is much more prudent to buy when the index is confidently moving out of the extreme fear zone.

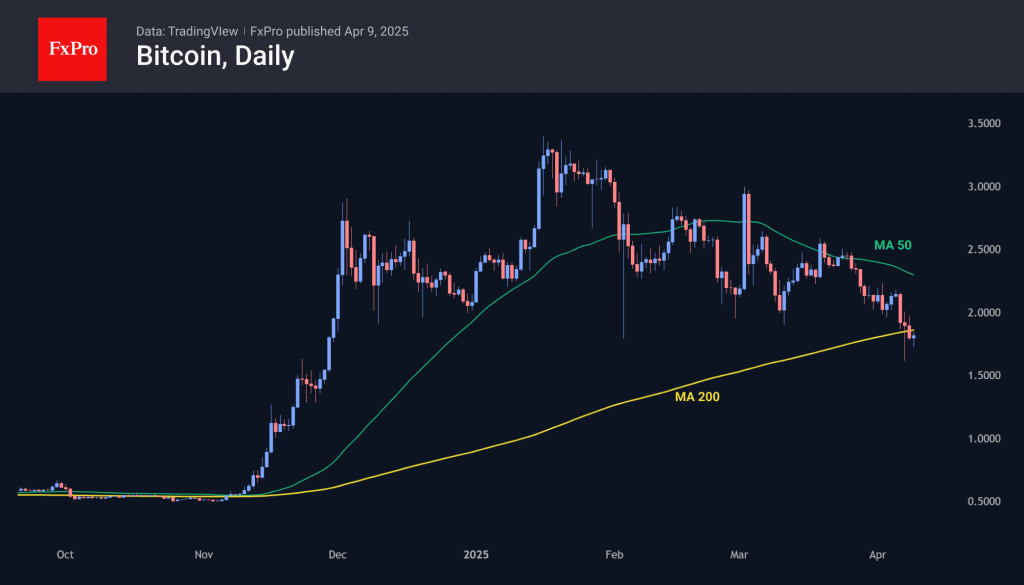

Bitcoin was down to $75K early in the day, approaching Monday’s lows and echoing the dynamics of U.S. stock indices. Selling is starting from increasingly lower levels, with the RSI index above the oversold area on daily timeframes. This fails to attract buyers on dips and sets up a wait-and-see approach.

XRP is testing its 200-day average, having pulled back to the $1.82 area, 45% cheaper than its peak price in January, and back to the 2021 highs. A failure under this line could accelerate the sell-off of the fourth-largest cryptocurrency.

News Back ground

Bernstein noted that Bitcoin has proved more resilient amid tariff turbulence in markets than during previous crises. The first cryptocurrency is still worth investing in as a means of saving in the long term.

Bitcoin could collapse to $10,000, warns Bloomberg Intelligence senior strategist Mike McGlone. This could happen as part of a global correction in financial markets. According to the analyst, “the entire crypto space needs to be cleaned up, just as it was with the dot-com bubble.”

Ethereum’s fall below its realised price ($2200) indicates panic among owners of the second most capitalised cryptocurrency, which historically serves as a bullish signal for the medium term, CryptoQuant notes.

Built-in Telegram Wallet will soon be available to US users. The service will be launched in the second quarter of 2025.

USDJPY Reruns to Full Bearish Mode on Fresh Risk Aversion

Bears returned to play and fully reversed the recent bounce from new multi-month low (144.55), with strong bearish signals being developed on daily chart (double recovery rejection / bull-trap above converged daily Tenkan/Kijun-sen).

Deterioration outlook on the latest sharp increase of tariffs for all Chinese imports to the US and anticipated adequate counter measures from China, revived risk aversion and provided fresh boost to traditional safe haven yen.

Bears dented new low (144.55, posted last Friday) and eye immediate 144.13 (Fibo 76.4% of 139.57/158.87) violation of which to expose 141.64 (Sep 30 higher low) which guards key supports at 140.00/139.57 (psychological / 2024 low).

Former low at 146.53 (Mar 11) and broken Fibo 61.8% (146.95) reverted to resistances which should cap the upside and keep fresh bears alive.

Res: 146.60; 147.48; 148.19; 148.90

Sup: 145.18; 144.13; 143.65; 142.97

ECB’s Villeroy: Trade uncertainty threatens financial stability, strengthens case for rate cut

French ECB Governing Council member Francois Villeroy de Galhau warned today that mounting economic uncertainty from escalating trade tensions is posing risks to financial stability, particularly increasing credit risks for some financial institutions.

While he emphasized the resilience of French banks, he noted that leveraged hedge funds could come under significant liquidity pressure.

Writing in his annual letter to President Macron, Villeroy assured that both Bank of France and ECB are “fully mobilised” to safeguard financial stability and ensure adequate liquidity.

Speaking to journalists, Villeroy said the recent US announcement of sweeping “reciprocal” tariffs only adds to the case for further monetary easing. “We still have room to cut rates,” he stated.