Sample Category Title

Rumblings In Italian Politics Resurface

Notes/Observations

- Snippets of Trump CNBC interview provides volatility; full interview set to be released during NY morning

- Political drama back in Italian politics as key political leaders said to have challenged the Fin Min Tria over state lender state lender Cassa Depositi e Prestiti (CDP)

- China stocks recover on reports that govt could ‘soon’ loosen rules related to wealth management; CNY currency offer worst levels on speculation officials were seeking to stem the drop

- Various emerging central banks said to intervene in FX market to stem currency weakness (India, Indonesia cited)

Asia:

- China PBoC set the Yuan currency midpoint at weakest level since July 2017

- Japan Jun National CPI data registered a slight miss (YoY: 0.7% v 0.8%e); Japan Government Official reiterated stance that consumer prices were rising 'moderately'

- Philippines Central Bank (BSP) Chief Espenilla: Considering 'strong' monetary adjustment at Aug meeting; elevated CPI views highlight second round effect

Europe:

- Italy League party official Borghi (budget committee): too soon to say who Italy will back as candidate for next ECB President. Germany's Weidman’s hawkish ideas that could lead to European disintegration

Americas

- President Trump: Not happy about interest rates going up at the Fed; Strong dollar put the US at a disadvantage - CNBC taped interview excerpts

- White House Sanders: President Trump respected the independence of the Federal Reserve and was not interfering in monetary policy decisions

Economic Data:

- (NL) Netherlands July Consumer Confidence: 23 v 23 prior

- (NL) Netherlands May Consumer Spending Y/Y: 2.9 v 3.0% prior

- (DE) Germany Jun PPI M/M: 0.3% v 0.3%e; Y/Y: 3.0% v 3.0%e

- (NL) Netherlands Jun House Price Index M/M: 0.7% v 0.9% prior; Y/Y: 8.9% v 8.9% prior

- (HU) Hungary May Average Gross Wages Y/Y: 10.9% v 11.2%e

- (JP) Japan Jun Convenience Store Sales Y/Y: +1.1% v -1.2% prior

- (MY) Malaysia Mid-July Foreign Reserves: $104.6B v $104.7B prior

- (ES) Spain May Trade Balance: -€2.2B v -€3.1B prior

- (CN) Weekly Shanghai copper inventories (SHFE): 211.3K v 234.7K tons prior

- (TW) Taiwan Jun Export Orders Y/Y: -0.1% v +7.4%e

- (EU) Euro Zone May Current Account (Seasonally Adj): €22.4B v €29.6B prior; Current Account NSA (unadj): €4.6B v €27.3B prior

- (IT) Italy May Current Account Balance: ?2.2B v €3.0B prior

- (PL) Poland Jun Retail Sales M/M: 3.4% v 1.5%e; Y/Y: 10.3% v 8.1%e; Real Retail Sales Y/Y: 8.2% v 6.8%e

- (RU) Russia Narrow Money Supply w/e July 13th: 10.35T v 10.21T prior

- (UK) Jun Public Finances (PSNCR): £13.3B v £4.7B prior; Public Sector Net Borrowing: £4.5B v £3.6Be, Central Government NCR: £13.6B v £6.9B prior, PSNB ex Banking Groups: £5.4B v £5.0Be

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B indicated in 2020, 2026, 2031, 2033 and 2055 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 flat at 3,470, FTSE +0.1% at 7,693, DAX -0.1% at 12,676, CAC-40 -0.3% at 5,404; IBEX-35 -0.2% at 9,703, FTSE MIB -0.7% at 21,728, SMI +0.3% at 8,962, S&P 500 Futures -0.05%]

- Market Focal Points/Key Themes: European stocks open slightly lower and traded largely sideways as the session progressed towards being slightly positive; consumer discretionary sector supported; automotives stocks underperforming; focus on upcoming interview of US President Trump; risk sentiment muted going into weekend; Colombia closed for holiday; earnings expected in the upcoming US session include Regions Financial, General Electric and Honeywell

Equities

- Consumer discretionary: Hays HAS.UK -4.9%(block sale), Stora Enso STERV.FI -10.7% (results), Wessanen WES.NL -21.6% (results), XXL ASA XXL.NO -18.3% (results)

- Energy: Scatec Solar SSO.NO +4.1% (rsults)

- Financials: Beazley BEZ.UK -5.7% (results)

- Healthcare: Mithra Pharmaceuticals MITRA.BE +3.2% (marketing authorization), Recordati REC.IT +2.9% (analyst action)

- Industrials: Faurecia EO.FR -4.1% (results), Huhtamaki HUH1V.FI -8.2%(results), Skanska SKAB.SE -5.5% (results), SSAB SSABA.SE -5.8%(results), Thales HO.FR +1.0% (results)

- Technology: Tieto TIE.1V.FI -4.7%(results)

Speakers

- Italy key political leaders said to have challenged the Fin Min Tria (Italy PM Conte summoned key party officials for meeting regarding appointments and met with 5-Star leader Di Maio, League Leader Salvini and Fin Min Tria)

- Italy's Dep PM DI Maio (5-Star party leader) stated that he has no clash with Fin Min Tria, never asked him to resign

- Ireland Fin Min Donohoe: backstop must be retained; could only be replaced by something better

- Hungary Fin Min Varga: Period of calm for HUF currency (Forint) was over; looking for new equilibrium level in changed global environment. No need to rewrite the 2019 budget due to weaker HUF currency (Forint). Rise in bond yield required no immediate measures from the AKK debt agency

- India Fin Min Official: Not considering 'immediate' measures to check INR currency (Rupee) decline (**Reminder: RBI was suspected of FX currency intervention to support INR currency (Rupee) at the 69.10 area)

Currencies

- USD was softer for the 1st time this trading week after President Trump commented that the greenback’s strength put the US at a disadvantage. Dealers seemed concern that US might prevent the dollar from strengthening amid the trade row.

- EUR/USD moved off its best levels as some political turbulence in Italy surfaced. Reports circulated that key Italian political leaders had challenged the Fin Min Tria. Dealers also noted commentary from Italy League party official Borghi (budget committee) that expressed his usual euro skeptic views.

- CNY currency recovered from lows amid speculation officials were seeking to stem the drop. Earlier the PBoC set the Yuan reference rate at 6.7671 for its 7th straight weaker yuan fix and the weakest since July 14, 2017.

Fixed Income

- Bund Futures trades at 163.08 flat on the day having hit a high of 163.39, a move back above would target 163.47 then 163.63, with a move below 163 targeting 162.81 then 162.45.

- Gilt futures trades at 124.10 down 5 ticks on the day consolidating the recent run up, with continuing upside targeting 124.18 then 124.44, with a move lower seeing initial support at 123.83 then 123.41.

- Friday's liquidity report showed Thursday's excess liquidity fell from €1.824T to €1.802T. Use of the marginal lending facility dropped from €50M to €45M.

- Corporate issuance saw $5.5B come to market via 4 issuers. For the week ended July 18th Lipper fund flows reported IG funds show inflows of $2B, with High Yield fund show inflows of $260M a second straight week of inflows.

Looking Ahead

- (AR) Argentina Jun Budget Balance (ARS): No est v -7.8B prior

- (BE) Belgium Debt Agency (BDA) announces upcoming OLO auction for Monday, July 23rd

- (PT) Portugal Debt Agency (IGCP) announcement on possible bond auction for Wed, July 25th

- (AR) G20 Finance Ministers meet in Argentina

- (UK) BOE’s Tenreyro

- 05:30 (DE) German Chancellor Merkel holds her annual summer press conference

- 05:30 (ZA) South Africa to sell ZAR600M in I/ L 2029, 2033 and 2050 bonds

- 06:00 (IE) Ireland Jun PPI M/M: No est v 0.8% prior; Y/Y: No est v -3.3% prior

- 06:00 (IE) Ireland May Property Prices M/M: No est v 0.7% prior; Y/Y: No est v 13.0% prior

- 06:00 (US) President Trump interviewed on CNBC (pre-recorded)

- 06:00 (UK) DMO to sell £6.0B in 1-month, 3-month and 6-month bills

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (BR) Brazil mid-July IBGE Inflation IPCA-15 M/M: 0.7%e v 1.1% prior; Y/Y: 4.6%e v 3.7% prior

- 08:00 (UK) Baltic Dry Bulk Index

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:20 (US) Fed’s Bullard (dove, non-voter)

- 08:30 (CA) Canada Jun CPI M/M: 0.0%e v 0.1% prior; Y/Y: 2.3%e v 2.2% prior, CPI Core-Common Y/Y: 1.9%e v 1.9% prior; CPI Core- Median Y/Y: No est v 1.9% prior, CPI Core- Trim Y/Y: No est v 1.9% prior, Consumer Price Index: 133.4e v 133.4 prior

- 08:30 (CA) Canada May Retail Sales M/M: +1.0%e v -1.2% prior; Retail Sales (Ex-Auto) M/M: +0.5%e v -0.1% prior

- 09:00 (BE) Belgium July Consumer Confidence: No est v -3 prior

- 11:00 (EU) Potential Sovereign ratings after EU close (Austria and France Sovereign Debt to be rated by Fitch; Greece, Russia and Czech Sovereign Debt to be rated by S&P

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 15:00 (MX) Mexico Citibanamex Survey of Economists

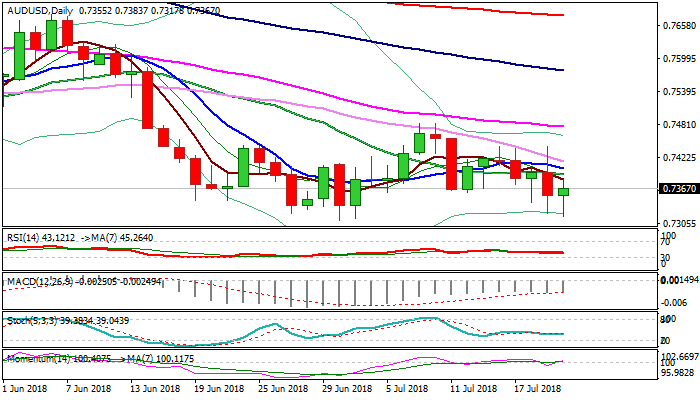

AUDUSD Outlook: Bears To Remain Intact While 10SMA Caps Recovery

The Australian dollar bounced on Friday after hitting three-week low at 0.7317, ticks ahead of key support at 0.7310 (02 July low).

Weaker US dollar gave a breather to Aussie's bears which track the weakness of Chinese yuan (posted new one-year low vs dollar).

Consolidation before breaking below 0.7310 pivot is seen as likely near-term scenario, with extended upticks to be capped by 10SMA (0.7404) to keep bearish structure intact.

Bears need confirmation on close below cracked pivot at 0.7325 (Fibo 61.8% of 2016/2018 0.6825/0.8135 uptrend) to generate bearish signal for fresh leg lower.

Break and close below 0.7310 would confirm and open targets at 0.7150 zone (lows of 24 June 2016 / 02 Jan 2017).

Conversely, close above 10SMA would sideline downside risk and signal stronger recovery.

Res: 0.7383, 0.7404, 0.7416, 0.7442

Sup: 0.7314, 0.7310, 0.7269, 0.7244

USD Weaker After Trump Interest Rate Comments

- Canadian inflation data eyed as BoC ponders more hikes;

- USD weaker as Trump weighs in on Fed monetary policy;

- Independent Fed unlikely to be influenced by Trump views.

It's looking like being a quiet end to the trading week, with the only notable economic releases coming from Canada and it being one of the less eventful days of earnings season.

The Canadian inflation figures will be one interesting takeaway today, after a year in which the central bank has been actively raising interest rates, most recently this month taking the number of hikes to four. The Bank of Canada has been extremely aggressive so early in the tightening cycle having last raised rates prior to this in 2010, especially when you consider that the economy is not exactly firing on all fronts like the US.

Still, inflation is clearly a concern of the BoC with the headline number having surpassed 2% again recently, so traders will be paying close attention to today's numbers. Markets are pricing in a good chance of another rate hike this year and today's numbers, should they meet expectations, could further support this view. While the dollar continues to make loonie, others including the pound and yen haven't been so fortunate, with the BoC seen as being more active going forward despite the threat posed by NAFTA negotiations.

The dollar is taking a bit of a breather today, coming on the back of losses on Thursday afternoon as US President Donald Trump took the unusual decision to weigh in on the Federal Reserve's interest rate policy. President's don't tend to give a view on monetary policy in much the same way that policy makers will shy away from expressing political views as it infringes on the independence of the central bank.

That said, Trump is not known for going along with the acceptable norms so it's hardly surprising that he's weighed in, especially as he tries to deflect attention away from his role in much of what he was complaining about. It's quite clear to most people that part of the reason for the Fed raising rates at the current pace is the tax reform measures passed at the end of last year, when the economy was already running hot.

This is also partially responsible for the dollar rising against other currencies, particularly the yuan and euro, which has suffered further as the President has sought to start a trade war with both. Trump is not one to accept responsibility for such events and now appears to be actively trying to push the blame onto others in a clear attempt to halt the rise in the greenback, the strengthening of which could weigh on the economy and soften the impact of the trade measures he is taking against other countries.

The worry is that he may try to put pressure on policy makers to slow the pace of tightening, which could be a major risk for the economy in the longer run, or explore other alternatives to influence the central bank, even if he has only recently personally selected the Chairman, Jerome Powell. Naturally, the White House attempted to downplay Trump's comments after the event but the damage was done and Trump's views on these matters are clear, even if they are somewhat misleading or misguided. Ultimately, I don't expect the Fed to be influenced but that doesn't mean Trump won't find an alternative way to deal with the issues, even if such solutions are controversial and prove ineffective or self-defeating.

Trade War Topples Yuan

PBoC sets CNY fixing at 6.7671

The Chinese yuan printed a fresh multi-month low on Friday amid heighten worries about the stability of the Chinese economy and the potential negative effects of the trade war with the US. The offshore rate fell as much as 0.65% with USD/CNH climbing as high as 6.8367. In the onshore market, the yuan were slight more moderate with USD/CNY climbing 0.60% to 6.8149. However, the sell-off was short-lived as both rates returned to the closing prices of the previous day. According to the latest rumours, the yuan’s turnaround could be explained by the sale of a large amount of USD by a Chinese bank.

On a trade-weighted basis, the yuan experienced its worst day since June 19 - when it lost 0.60%. So far, the yuan fell 0.52% after the PBoC set the USD/CNY at 6.7671, the lowest level since July 14, 2017. The persistent weakness in the yuan has spark fears about capital flight similar to what happened through 2015 and 2106 when the Chinese currency fell more than 13% against the greenback.

The trade war initiated by Donald Trump came at the worst possible moment for China as the country started the process to deleverage its economy. Against such a backdrop, further weakness in the yuan against the dollar should be expected.

Japan enters in a new trade deal with EU amid positive economic fundamentals

Opening the door for further trade relationships, the EU – Japan trade deal signed on Tuesday is providing a great message against protectionism. Taking into effect in 2019 and with the purpose of eliminating 99% of total tariffs between both blocs, a sum estimated along EUR 1 billion, the EU just signed its largest trade deal, expected to increase EU exports into Japan by over one third (currently estimated at EUR 86 billion). Japan is the second biggest partner in Asia after China and sixth trading partner worldwide.

Japanese nominal June inflation y/y data published at +0.70%, in line with prior month along with a slight increase in core gauge (ex fresh food) at +0.80% (prior: 0.70%) due to higher oil prices suggest that inflation target of 2% remains far, though recent bounce in June trade balance of JPY 721.4 billion (USD 6.5 billion), confirms heathy growth fundamentals. Common inflation drivers such as wage growth, unemployment rate at historical low and weaker JPY confirm the tendency of an acceleration in inflation for the coming periods, along 1% in 3Q. Accordingly, we expect the BoJ to maintain its dovish stance during 31. July 2018 monetary policy meeting.

Trading at 112.46, the USD/JPY is currently trading neutral. The tendency should however favor a slight increase of the pair along 112.60.

EUR/USD Slows Down Near 1.1680

The Euro weakened against the US Dollar on Thursday morning, driven lower by the combined resistance of the 55– and 100-hour SMAs. This fall ended slightly below the weekly S1 at 1.1580 which was followed by a strong 50-pip hourly surge later in the day.

This allowed the pair to surpass the 55-hour moving average, but nevertheless was not enough to continue advancing past the 100– and 200-hour ones.

Even though the direction of technical indicators is pointed upwards, it is unlikely that this 1.1680 area is breached today, as it is likewise strengthened by the 55-, 100– and 200-period (4H) SMAs.

Thus, the general direction of the Euro should be either south down to 1.1550 or sideways in between this significant resistance and the weekly S1 located at 1.16.

GBP/USD Waits For Bullish Breakout

The stronger US Dollar weighted negatively on the GBP/USD exchange rate yesterday morning, as it was pushed even lower down to the weekly S1 at 1.2960—its lowest position since September 2017.

It seems that this week's weakness is caused by fundamental developments from both sides, especially uncertainty around Brexit. This has stopped any attempts to push the Sterling higher even despite trader sentiment being strongly bullish for the past few days.

Two scenarios are possible today. If the 55-hour SMA at 1.30 is breached, the Sterling should aim for the breached channel and the 100-hour SMA at 1.3150.

Conversely, the next southern target is the 61.80% Fibo at 1.29. However, it is not expected that a strong bearish move is apparent today.

USD/JPY Still Weak After Thursday Plunge

The most important development which disrupted the steady sideways movement of the USD/JPY pair was the 52-pip plunge during the second part of Thursday. This resulted in a breakout of the 55– and 100-hour SMAs and two channel lines, being stopped solely by the support of the 55-period (4H) and 200-hour SMAs and the monthly R2 near the 112.35 area.

Technical indicators are bullish for this session, suggesting that this support cluster might hold the pair and thus reverse it back to north. In this case, the upside target is either the psychological 113.00 mark or the weekly R3 at 113.35.

Meanwhile, a successful southern breakout from 112.20 is likely to pressure the US Dollar close to the monthly R1 at 111.50.

XAU/USD Tries To Push Higher

The 55-hour SMA continues to lead the yellow metal lower for the second consecutive week. The strong surge mid-Thursday was followed by two other tests of this line.

A successful breakout should lead to appreciation in this session. The nearest target is the 200-hour SMA at 1,245.00. Technical indicators on the 1H and 4H time-frames are likewise tended northwards.

If looking at patterns, the rate has been fluctuating around the senior channel line for several days, while the dashed junior channel was tested yesterday. It is expected that Gold tries to move towards its upper line.

The nearest support is the monthly S2 at 1,200.00. This is also the pair's lowest position since July 2017 that should work as a very strong support barrier.

EURUSD Neutral Around 1.1650 Level

The euro continues to hold around the 1.1650 level against the greenback, as traders remain undecided about the direction of the US dollar. The EURUSD pair had earlier benefitted from weakness in the US dollar, following comments from President Trump on Thursday. Sellers will continue to target further losses below the 1.1600 level, while buyers will attempt to hold price above the 1.1681 level.

The EURUSD pair is only bearish while trading below the 1.1630 level, key support is found at the 1.1600 and 1.1580 levels.

If the EURUSD pair moves above the 1.1681 level, buyers will likely price towards the 1.1700 and 1.1744 resistance levels.

USDJPY Correction Underway Below 112.80

The US dollar trades to the downside against the Japanese yen currency on Friday, after President Trump’s bearish comments on the value of the US dollar. The USDJPY pair has broken below the key 112.80 level and has so far found strong technical support from just above the 112.00 level. Sellers will target a sustained break below the 112.20 level, while buyers will look to reclaim the 112.80 level.

The USDJPY pair is intraday bearish while trading below the 112.80 level, key support is found at the 112.00 and 111.70 levels.

If the USDJPY pair moves above the 112.80 level, buyers may test towards the 113.00 and 113.40 levels.