Sample Category Title

Dollar dives as Senator Hatch threatens Trump with legislative confrontation for tariffs policies

Dollar suffers steep selloff in the early US session as WSJ reports that Senate Finance Committee Chairman Orrin Hatch sent a letter to Trump requesting him to reconsider his trade policies. And Hatch warned that GOP senators may be ready to risk a legislative confrontation with Trump if he doesn't reverse course. Hatch is a seven-term Utah Republican Senator who's seen as a reliable Trump ally.

As we pointed out before, Dollar has been benefiting from Trump's confrontation trade war threats. It remains to be seen if it's true. But it looks like no trade war, no dollar rally.

Canadian Dollar jumps on stellar retail sales, CPI accelerated

Canadian Dollar surges sharply in early US session after stellar retail sales data. Headline retail sales rose 2.0% mom in May versus expectation of 0.0% mom. That's more than offset -1.2% mom contraction in April. Ex-auto sales also jumped 1.4% mom, well above expectation of 0.5% mom.

Headline CPI accelerated to 2.5% yoy in June as expected. CPI core common was unchanged at 1.9% yoy. CPI core median rose 0.1% to 2.0% yoy. CPI core trim rose 0.1% to 2.0% yoy.

Now, it really looks like BoC was correct to hike and stays hawkish.

German Merkel: Can’t rely on the superpower of the US

German Chancellor Angela Merkel said in a news conference that the Germany "can't rely on the superpower of the United States. And the auto tariffs are "a real threat to the prosperity of many in the world". Also, the "usual framework" of the world is "under strong pressure at the moment" before of the US. Though, she maintain that "transatlantic working relationship, including with the U.S. president, is crucial for us and I will carry on cultivating it".

For the EU, Merkel said it's in a "transformation process". And, "it recognizes the seriousness of the situation, but it hasn't yet been resolved whether we are going to rise to the challenges quickly enough." She pointed to the "big economic challenge, and one day certainly also military, from the strengthening of China". And, the EU must also deal with the relationship with Russia.

Dollar Reacts Little on Fresh Trade Threats; Canadian CPI & Retail Sales Pending

Here are the latest developments in global markets:

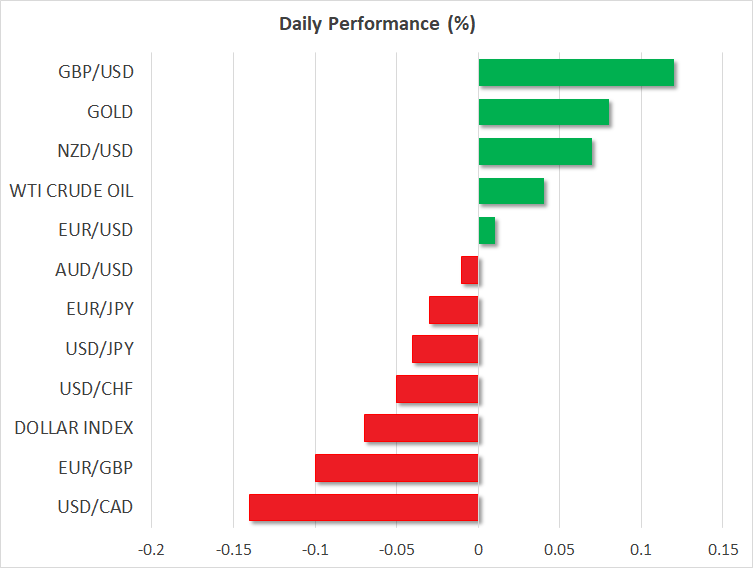

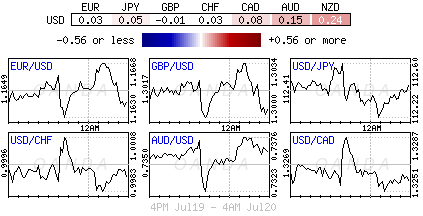

FOREX: The US dollar was trading lower against the Japanese yen on Friday, though by not much, at 112.40 (-0.07%) remaining below the 1-year high of 113.15 reached on Thursday as investors kept in mind Trump’s criticism made on Thursday about higher US interest rates and a stronger dollar. Renewed US trade warnings against China today did little to move the pair (see below). The dollar index against a basket of currencies moved down by 0.05% after the bounce off the 1-year high of 95.65. The weakness of the greenback, drove euro/dollar and pound/dollar higher by 0.03% and 0.18% respectively. The antipodean currencies were mixed today, with aussie/dollar losing 0.01% to trade at 0.7358 and kiwi/dollar advancing by 0.09% to 0.6749. Moreover, dollar/loonie headed lower by 0.15% ahead of the release of Canadian CPI and retail sales figures later in the day.

STOCKS: European stocks were trading lower on Friday, as autos and bank stocks dropped amid a new escalation in trade tensions. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 were lower by 0.54% and 0.66% respectively. The German DAX 30 tumbled by 0.83%, the French CAC 40 plunged by 0.97%, the Spanish IBEX 35 slipped by 0.60% and the British FTSE 100 dipped by 0.40%. The Italian stocks were also on the backfoot (-0.47%), facing additional pressure from political divisions in Italy. US stock futures were in a sea of red.

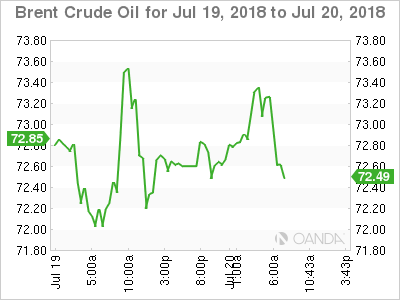

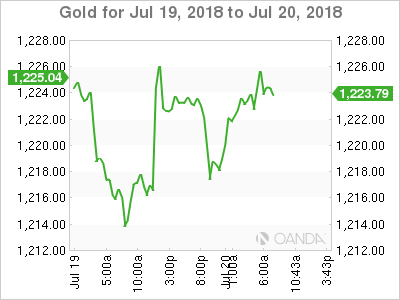

COMMODITIES: Oil prices rose today; however, the weekly session remains negative. West Texas Intermediate (WTI) crude oil traded higher by 0.30% at $69.67 per barrel, while London-based Brent surged by 0.43% to $72.89 per barrel. In precious metals, gold and silver bounced off one-year lows, with the former being up by 0.14% at $1,223.70 per ounce and the latter 0.81% higher.

Day ahead: Canada reports on inflation and retail sales; G20 meeting kicks off in Buenos Aires

Friday’s economic calendar will feature Canadian CPI and retail sales figures, while the global trade turmoil will continue to feed risk-off sentiment as the US shows no appetite to pull back its protectionist tariff measures, whereas the EU and China seek ways to defend their interests.

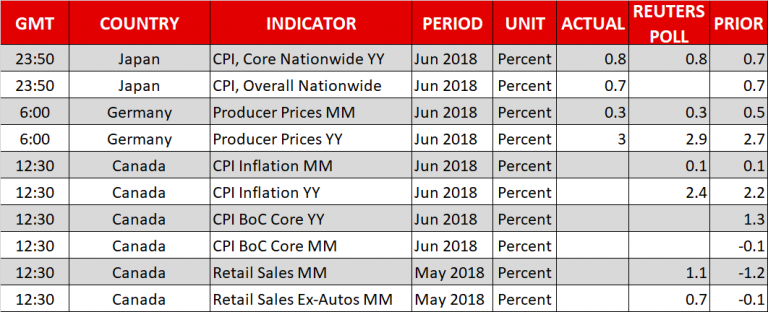

At 1230 GMT, Statistics Canada is expected to show that overall consumer prices have risen by 2.4% year-on-year in June, 0.2 percentage points faster than in May when the headline CPI stood at 2.2%. Given that Bank of Canada aims to keep the total CPI inflation at the 2.0% midpoint of a target range of 1-3.0% over the medium-term, markets could increase speculation that policymakers are preparing another 25bps rate hike in coming months. The soonest such a rate hike could be delivered would be at the October or December meeting where investors give a chance of 43% and a 54% respectively. While there are is no forecast available for the core, median, or trimmed mean CPI measures, these will be closely reviewed as the central bank uses these volatility-free indices to identify changes in the inflation trend.

Canadian retail sales, which are considered an ideal proxy for household spending, will also be under the spotlight at the same time. After a 1.2% decline in April, analysts believe that retail sales have rebounded substantially by 1.2% m/m in May. If this is the case, that would be the strongest growth registered since December 2017. In the absence of automobiles, the core equivalent is also projected to recover, rising by 0.7% m/m after falling by 0.1% in the previous month.

Should retail sales increase more than analysts predict, signaling that the previous downturn could be temporary and instead inflationary pressures are heating up, something that could be also proved if CPI figures beat forecasts today, the loonie, which is set to close in the red for the second consecutive week, could erase losses. Alternatively, in the wake of disappointing prints which could reduce odds for further stimulus reduction, the loonie could once more find itself under pressure.

Still, trade uncertainties remain a high risk for the loonie as Canada has already started being subject to steel and aluminum import tariffs to the US, while the NAFTA story continues to hold in the dark as Canada and Mexico have no intentions to leave the pact despite the US pushing to trim the free-trade agreement and sign separate deals with its Canadian and Mexican counterparts. Therefore, trade issues are something policymakers will seriously consider before proceeding with further stimulus reduction.

Developments on the trade front could create headlines during the weekend (or next week) as the Group of 20 finance ministers and central bank presidents will be gathering in Buenos Aires in Argentina, where trade issues might be high on the agenda. The atmosphere though might not be positive as tariff-affected countries are expected to express their frustration over the US import tariffs on steel and aluminum and the retaliatory responses the measures created. In the meantime, the US unleashed fresh warnings towards China, threatening to punish all imports from China, worth $505bn per year. Note that at the March G20 meeting, financial representatives criticized protectionism and called for further dialogue which so far had minimal effect.

Meanwhile in Eurozone, Italian politics moved to the forefront, pushing Italian stocks to negative territory after reports that the Italian Deputy Prime Ministers, Luigi Di Maio, and Matteo Salvini, had asked for the resignation of the Minister of Economy Giovanni Tria if he did not back government nominees to lead key companies. While the statements were denied on Friday, the news reminded investors that political divisions within the Italian government are still a risk for the markets. In other concerns, comments from Italy’s Head of the budget committee at the Lower House Claudio Borghi, written on Italy’s daily newspaper” The Corriere della Sera”, stated that “Italy will come out of the Euro sooner or later”, adding to the bearish sentiment.

In Northern Ireland, UK Prime Minister, Theresa May, will reiterate that a border infrastructure down the Irish sea is unacceptable, while at the same time the EU Brexit negotiator, Michel Barnier will be delivering EU’s position on the Brexit plan approved in Chequers. Barnier will speak to the media after his meeting with 27 EU ministers.

In oil markets, Baker Hughes is scheduled to issue its report on the numbers of active rigs for oil drilling at 1700 GMT.

As of today’s, public appearances, St. Louis Fed President, James Bullard (non-voting member this year), will be giving a presentation on the U.S. economy and monetary policy before the Glasgow Chamber of Commerce at 1220 GMT.

Trump Attacks King Dollar, Gold Edges Up

One would have expected U.S President Donald Trump’s criticism of the Federal Reserve’s policy to heavily punish the Dollar and drawopportunistic bears into the vicinity.

However, the Greenback remains somewhat supported despite easing from yearly peaks with prices trading above 95.00 as of writing. While Trump’s comments on how he was “not thrilled” by the Federal Reserve’s interest rate rises could create a sense of uncertainty over Washington’s Dollar policy, it is unlikely to derail the Fed from gradually raising interest rates. Trump’s verbal intervention is likely to hit a brick wall, as heightened rate hike expectations ensure that the Dollar reigns supreme across currency markets.

Focusing on the technical picture, the Dollar Index is bullish on the daily and weekly charts. A solid weekly close above the 95.00 resistance level could seal the deal for further upside, with 96.00 and 96.40 acting as points of interest. Alternatively, a move back below 95.00 may invite a decline towards 94.30 higher low.

Currency spotlight – GBPUSD

Sterling weakness was a dominant market theme this week thanks to an appreciating Dollar, disappointing U.K economic data, fading expectations of a BoE rate hike and continuing Brexit uncertainty.

Matters could be exponentially worsened for the battered Pound today, if the European Union rejects Theresa May’s Brexit white paper. Such a scenario is likely to heavily damage buying sentiment towards the currency as fears of a hard Brexit intensify.

The GBPUSD continues to fulfil the prerequisites of a bearish trend on the daily charts as there have been consistently lower lows and lower highs. A weekly close below the 1.3000 level could invite a decline towards 1.2950 and 1.2870. Alternatively, a technical rebound towards 1.3115 may offer an opportunity for bears to jump back into the game.

Commodity spotlight – Gold

A broadly stronger Dollar has offered nothing but pain to Gold which is set to conclude the trading week negatively.

The aggressive depreciation witnessed in recent days continues to highlight how the precious metal remains heavily influenced by the Dollar’s performance and U.S rate hike speculation. With Jerome Powell reinforcing market expectations over the Fed gradually raising rates, Gold is likely to remain vulnerable despite trade tensions weighing on sentiment. With regards to the technical picture, the precious metal is heavily bearish on the daily timeframe. Sustained weakness below $1236 could encourage a decline toward $1209 and $1200, respectively.

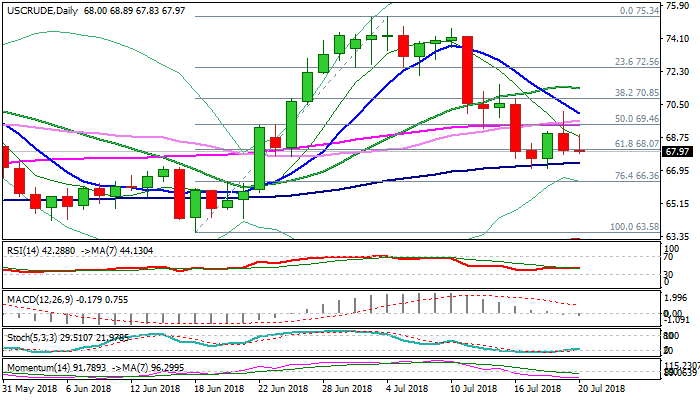

WTI Oil Outlook: No Clear Direction While The Price Ranges Between 100 & 55SMA’s

WTI oil price moved higher on Friday as news that Saudi Arabia would reduce exports in August, sidelined fears of oversupply in oil market. Near-term action is congested between $67.02 and $70.16 and showing no clear direction as daily techs are giving mixed signal. Steep fall from $74.67 was contained by rising 100SMA with double-bottom left at $67.02, but recovery action stalled at $70.16 on Thursday. Subsequent pullback left bearish daily candle with long upper shadow which signaled strong upside rejection and generated negative signal. Price is holding between 100SMA ($67.39) and 55SMA ($69.37) which mark initial pivots with break of either side to generate fresh direction signal. Overall structure is bearishly aligned and oil is on track for the second weekly close in red, which keeps near-term bias with bears. Eventual break below 100SMA would signal continuation of larget downtrend and expose next target at $66.36 (Fibo 76.4% of $63.58/$75.34 rally). Falling 10 SMA caps and maintains negative tone (currently at $70.01) and only close above here would ease downside risk.

Res: 68.89, 69.37, 69.79, 70.01

Sup: 67.79, 67.39, 67.02, 66.36

USD Too Strong For POTUS

Dollar outperformance continued this week supported by Fed Chair Powell's semi-annual testimony. However, USD Too strong for POTUS, and dollar rally has paused. UK inflation less than expected and Politics remained in the spotlight.

Technical Analysis

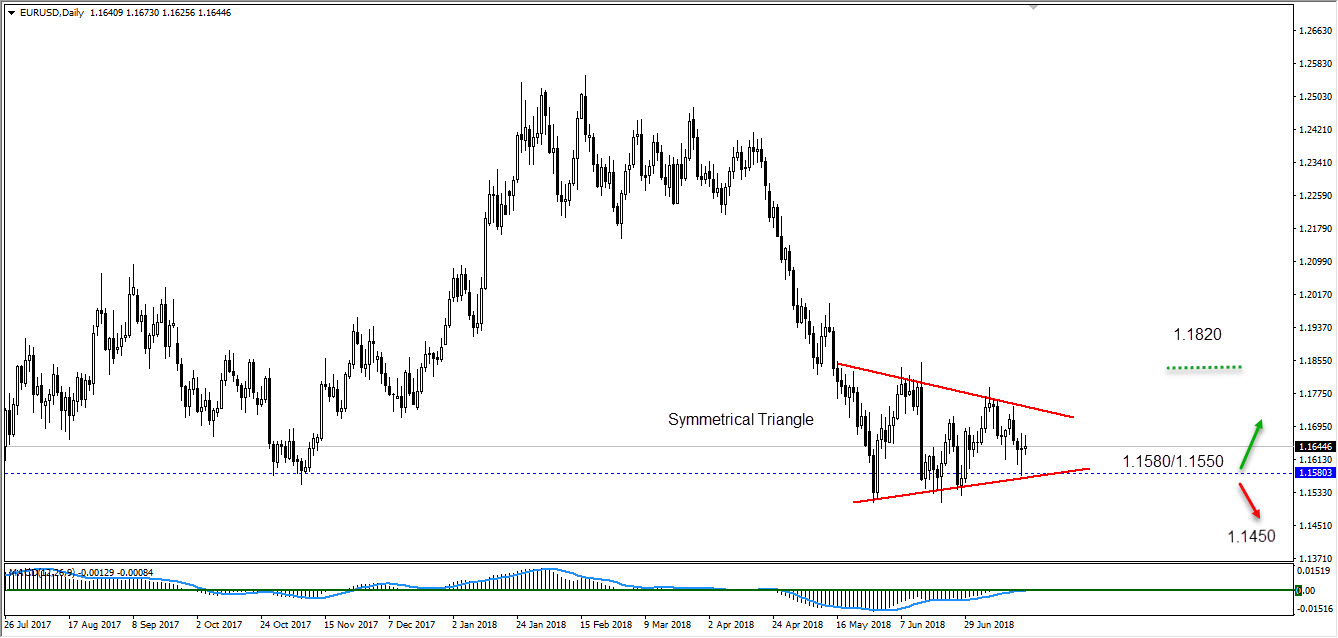

EUR/USD

The pair is trading within symmetrical triangle. We believe the support at 1.1580/1.1550 will hold and market will move toward 1.1820.

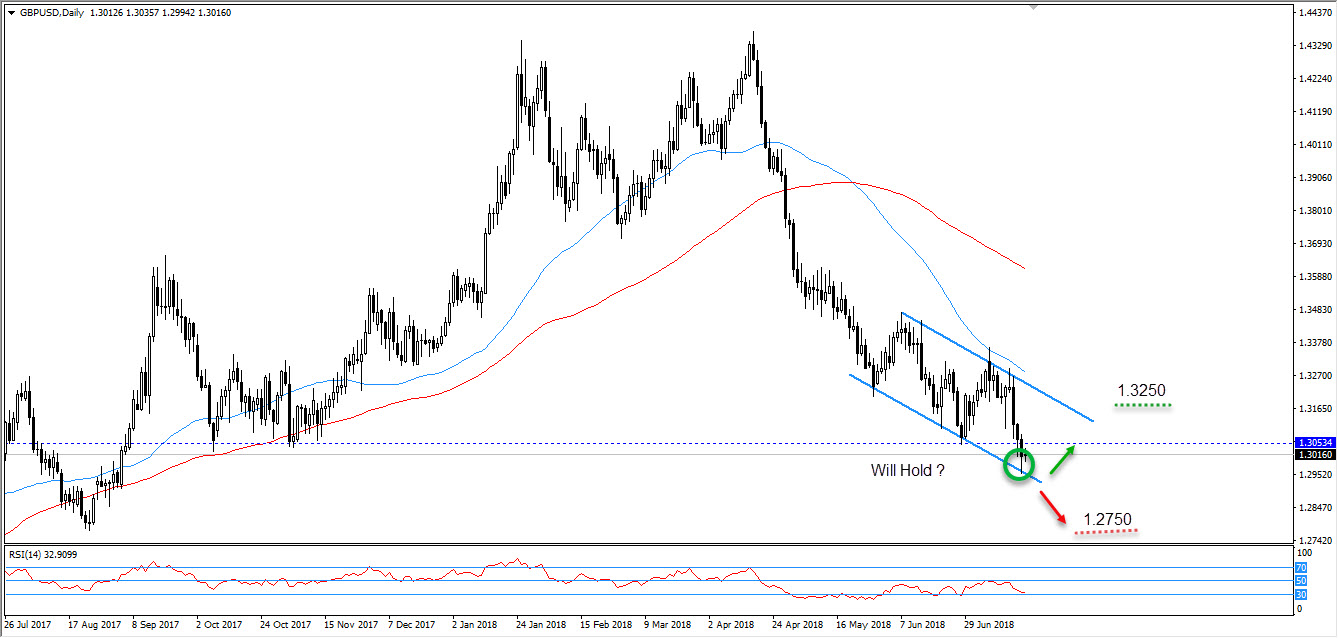

GBPUSD

We have moved into a significant region of support between 1.30 and 1.29, with 1.2935 a major level area to watch. If market kept trading above that level a correction wave toward 1.3120/1.3180 is expected.

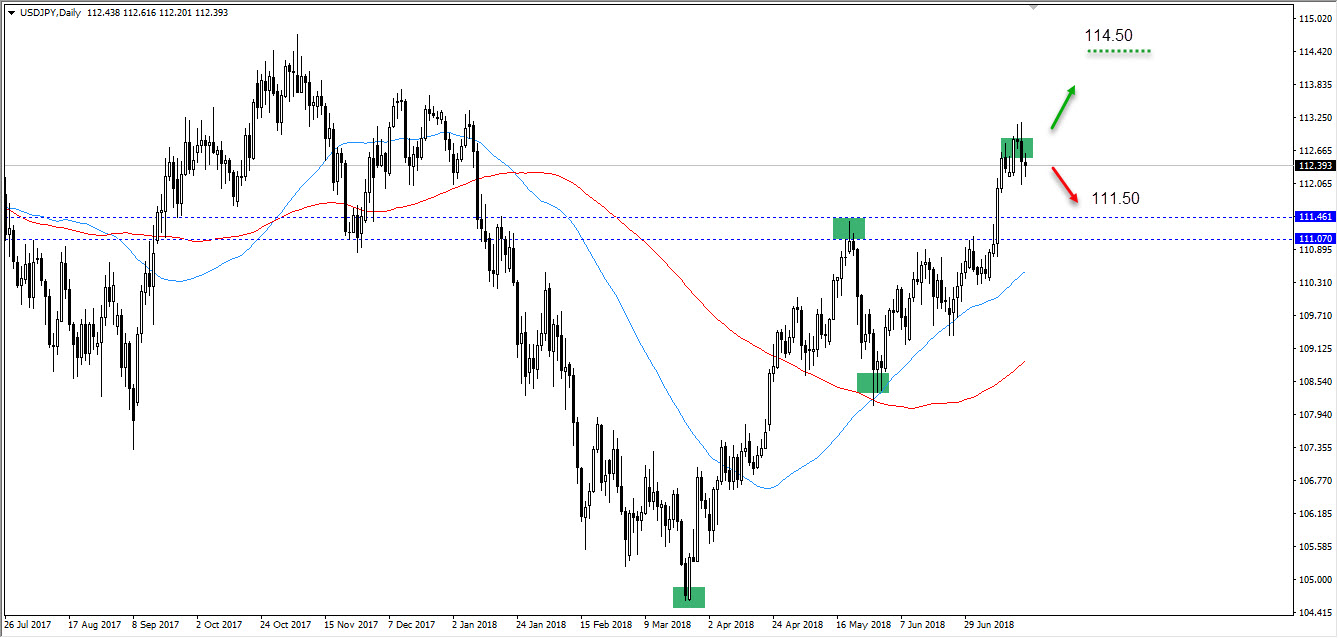

USDJPY

Prices remain around mid-range, after falling from 112.80 resistance level. We could see a re-test of the previous top at 111.50/111.20.

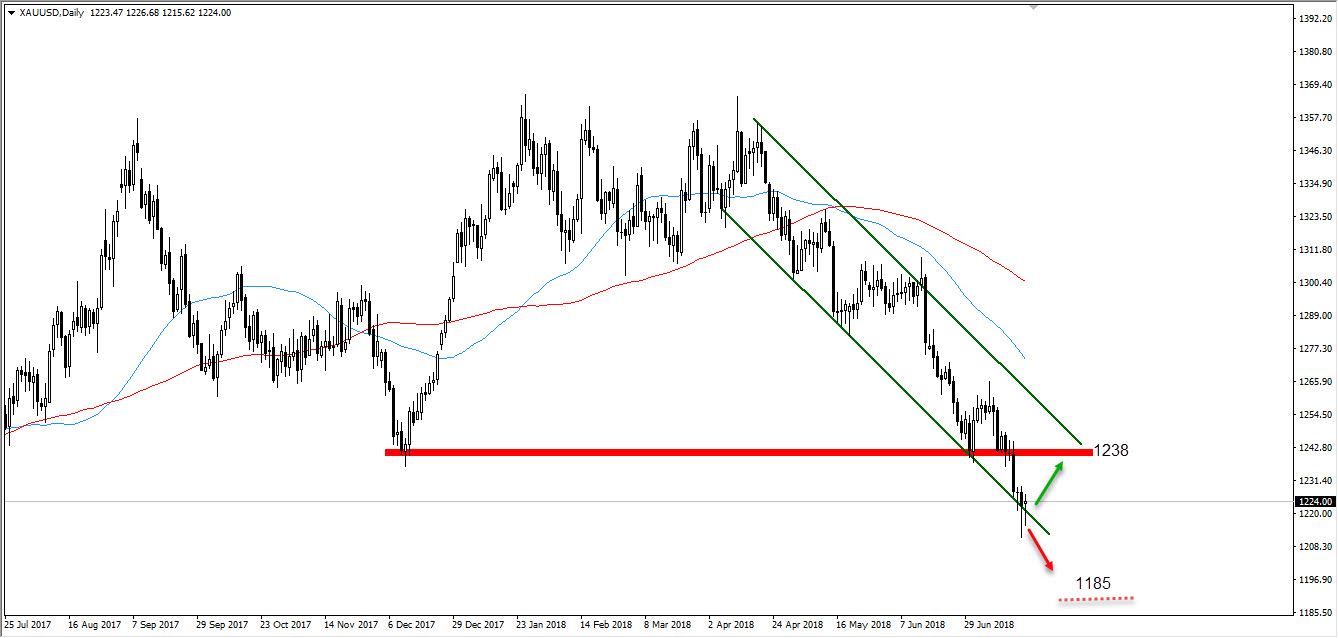

XAUUSD

Bearish Bias, despite we can see a corrective move toward 1232, however, it would be considered an opportunity for shorting gold to target 1205/1208 support levels.

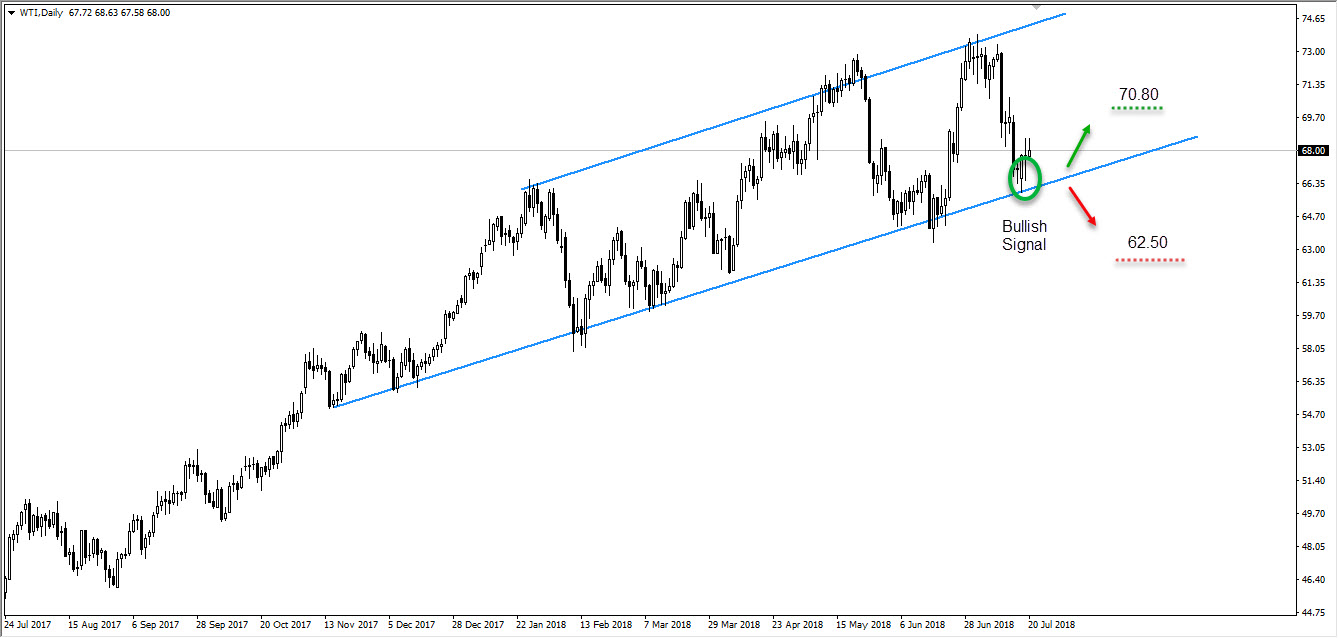

WTI

Rebound from the weak up- trend. Continuation for the bullish move is expected to target the resistance at 70.50 as long as the market is trading above 66.20.

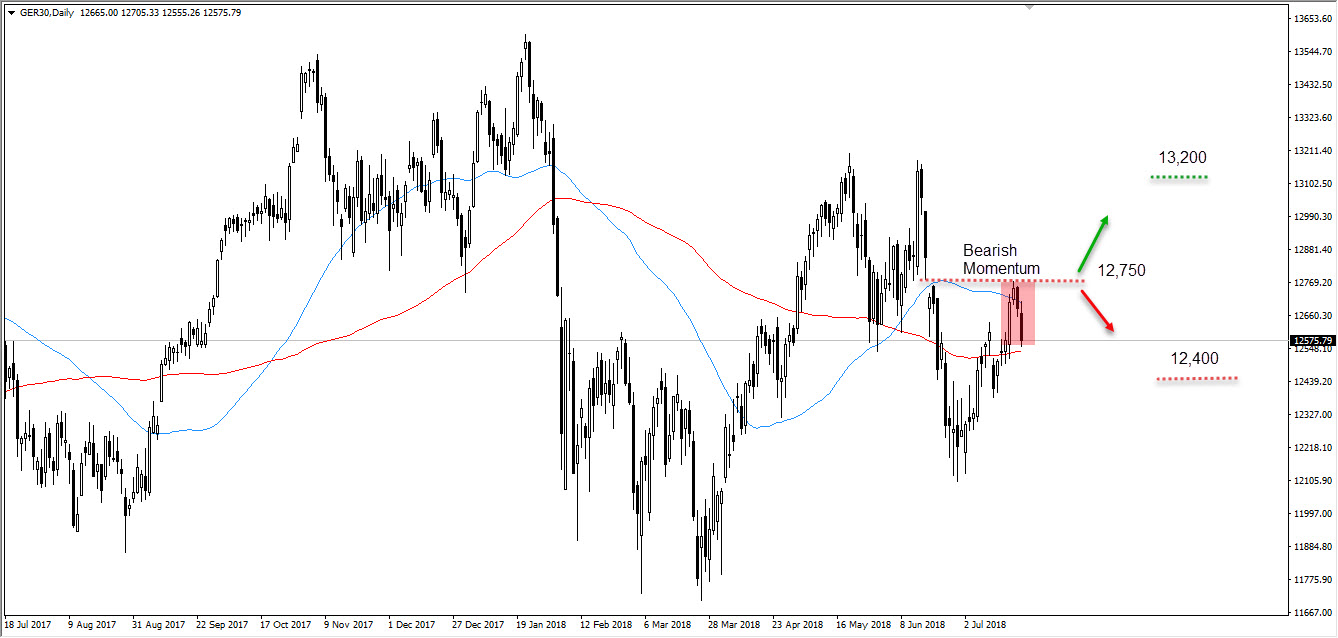

DAX

Continuing its downtrend after market failed to break the resistance level at 12750. We are looking for a move back towards 12,400/12350 as part of a medium-term range.

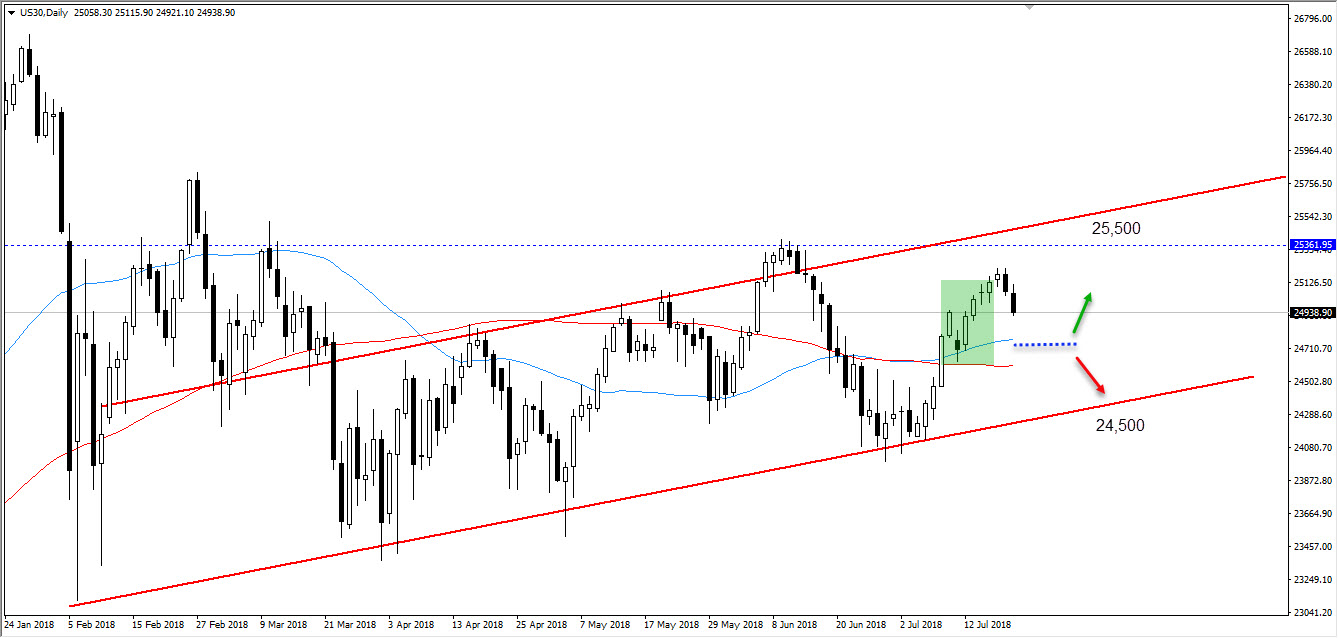

DOW Jones

Prices have pushed through support level and with momentum still in bull mode there is room to test the next resistance region (Channel resistance level ) between 25,250 and 25,380.

It’s War – Trade And Currency

Friday July 20: Five things the markets are talking about

Euro equities start the day on the back foot despite most Asian bourses finding a little traction to close out their week. Nevertheless, a weaker Chinese yuan and trade uncertainty continues to weigh on global markets.

The manipulation of the yuan's value, considered by many, is being used as a direct response to President Trump's actions on global trade and protectionism.

With uncertainty continuing to dominate markets, it's becoming a lot more difficult to ignore the Chinese yuan moves in the face of a potential currency war.

The yuan hit a 12-month low outright early Friday after authorities guided its official exchange rate down by -0.9% to ¥6.7671, the largest retreat in two-years. The currency has fallen -2.3% against the dollar this month alone.

Chinese actions have prompted Trump to publically express his own dissatisfaction with the Fed's monetary policy.

The U.S Presidents comments yesterday, on the dollar and monetary policy, depart from a convention in which sitting Presidents have refrained from expressing views specifically on their own currency and interest rates.

Strap in, be prepared, some of these currency moves may not make sense from an economic and monetary policy perspective – some prices will be guided by covert actions and Twitter rants!

Further falls in the yuan will only heighten worries about capital flights from China like the one investors witnessed three-years ago.

1. Stocks mixed results

In Japan, equities slipped overnight in choppy trading as Chinese yuan moves knocked investor sentiment. The Nikkei share average fell -0.29%, while the broader Topix shed -0.26%. However, both indexes posted their second consecutive weeks of gains.

Down-under, Aussie shares ended the week higher thanks to gains in financials. The S&P/ASX 200 index closed up +0.37%, and tacked on +0.3% for the week. In S. Korea, the Kospi stock index erased early falls to close higher as Chinese shares rebounded. The index closed +0.3% higher.

In China, stocks rebounded overnight, erasing this week's losses as investors piled into financial shares on rumoured reports that suggested looser-than-expected asset management rules. The blue-chip CSI300 index rose +1.9%, while the Shanghai Composite Index gained +2%.

In Hong Kong, shares also closed higher, but lower for the week. The Hang Seng index ended +0.8% higher, while the China Enterprises Index closed up +1.5%. For the week, Hang Seng still lost over -1%.

In Europe, regional bourses have opened slightly lower and are trading largely sideways. Expect risk sentiment to remain muted going into the weekend.

U.S stocks are set to open little changed.

Indices: Stoxx50 flat at 3,470, FTSE +0.1% at 7,693, DAX -0.1% at 12,676, CAC-40 -0.3% at 5,404; IBEX-35 -0.2% at 9,703, FTSE MIB -0.7% at 21,728, SMI +0.3% at 8,962, S&P 500 Futures -0.05%

2. Oil prices rally, but set for weekly drop on oversupply, trade worries

Crude prices are a tad better bid, but remains set for a weekly drop on concerns about oversupply and the ongoing Sino-U.S trade conflict, the world's two biggest oil users.

Brent oil had has climbed +27c, or +0.4% to +$72.85 a barrel, while U.S West Texas Intermediate (WTI) crude is up +29c, or +0.4%, at +$69.79 a barrel.

However, both benchmarks are on track for their third consecutive weekly loss, with Brent set to decline -3.3% and WTI to fall by -1.8%.

Prices have fallen on emerging evidence of higher production from Saudi Arabia and other members of the OPEC as well as Russia and the U.S.

Ahead of the U.S open, Gold prices have advanced in volatile trade overnight, after hitting a one-year low Thursday, as the U.S dollar eased from its 12-month highs. Spot gold is trading at +$1,224.55 an ounce. Yesterday, it fell to its weakest since July last year at +$1,211.08 an ounce.

3. Sovereign yields little changed

This week has seen U.S three-month T-bill yields back up above the +2% mark for the first time since June 2008, just before the global financial crisis erupted in earnest.

Higher yields reflect anticipated further Fed hikes. Currently, there is a +90% probability of another +25 bps increase, to +2%-2.25%, at the Sept. 25-26 meeting of the FOMC. A further hike, to +2.25%-2.50%, has about a +65% chance.

Elsewhere, the yield on 10-year Treasuries has increased +1 bps to +2.84%. In Germany, the 10-year Bund yield has decreased -1 bps to +0.32%, the lowest in more than a week, while in the U.K, the 10-year Gilt yield has declined less than -1 bps to +1.185%, the lowest in almost seven months.

Market confidence in the Fed's monetary policy will not be shaken by Trump's criticism of the central bank raising interest rates.

4. Dollar drifts from 12-month highs

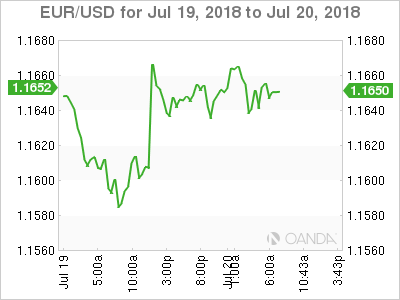

In the last session for the week, the ‘mighty' USD is a tad softer for the first time in five sessions after Trump commented that the greenback's strength put the U.S at a disadvantage.

EUR/USD (€1.1645) has moved off its best levels on renewed political concerns in Italy. Commentary from Italy League party official Borghi (budget committee) again expressed his usual EUR sceptic views.

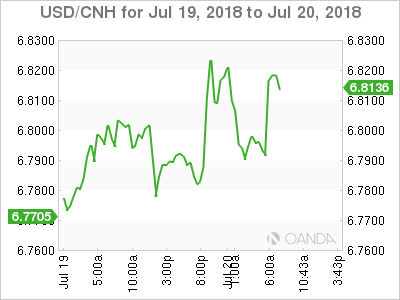

CNY (¥6.8154) trades atop of new lows despite market speculation that officials were seeking to stem the drop. Earlier the PBoC set the Yuan reference rate at €6.7671 for its seventh straight weaker yuan fix and the weakest since July 14, 2017.

5. ECB watch

With little or no significant data in the coming few sessions, the market will focus on whether the European Central Bank (ECB) will give details on its reinvestment policy under its asset purchasing program when they meet next Thursday (July 26).

Officials revealed last month that they would likely halve asset purchases in Q4, before ending them at year-end.

Market speculation has grown that the ECB may look to reinvest more into longer-dated bonds to maintain the QE portfolio's maturity profile.

Dealers will also be looking for more detail to last months statement that interest rates would stay at current levels “at least through the summer of 2019.”

USD/CAD – Canadian Dollar Steadies Ahead Of Key Consumer Data

The Canadian dollar has posted slight gains in the Friday session. Currently, USD/CAD is trading at 1.3240, down 0.22% on the day. On the release front, the focus is on consumer indicators. CPI is expected to remain pegged at 0.1%, while retail sales are expected at 0.6%, which would be the first gain in 2018. Traders should be prepared for movement from the Canadian dollar in the North American session. There are no US indicators on the schedule.

Bank of Canada policymakers will be keeping a close eye on Friday’s retail sales and inflation data. The Bank raised interest rates last month and said that further hikes could be on the way. An additional rate hike will be dependent on the strength of key indicators, as well as the fact that the Federal Reserve is likely to raise rates in September and perhaps December as well. With the Canadian dollar trading close to 13-month lows, BoC policymakers will have to raise rates or risk having the Canadian currency lose more ground due to interest rate differential with the United States.

The tariff slugfest between the U.S and its major trading partners has raised serious concerns not just with investors, but with Federal Reserve policymakers as well. The Federal Reserve Beige Book for July, released on Wednesday, was rife with references to ‘tariffs’. This trend started in the April Beige Book after President Trump threatened in March to impose tariffs on China. Most of the twelve Fed regional districts referred to tariffs in their individual reports, which make up the Beige Book. Some Fed policymakers have also voiced their concern over the impact that tariffs could have on the U.S economy and is an issue the Fed will have to take into consideration, as it mulls over rate policy for the next six months.

Trump threatens to impose tariffs on all Chinese imports, full interview

Trump spoke with CNBC anchor Joe Kernen on an interview yesterday at the White House. There he complained again the the US has been "ripped off by China for a long time". And he's "ready to go to 500", referring to tariffs on USD 500B of Chinese imports. That's nearly all of the USD 505.5B Chinese imports in 2017. And he pledged that he's "not doing this for politics" but "to do the right thing for the country".

Here is the full interview:

https://www.youtube.com/watch?v=UmPcmh8hnY4

White House economic adviser Larry Kudlow laid the blame on Chinese President Xi Jinping again. He said, “the problem here is Xi. He doesn’t want to move, and they’ve offered the U.S. absolutely ... no options regarding the issue of (intellectual property) theft and forced technology transfer.”