Sample Category Title

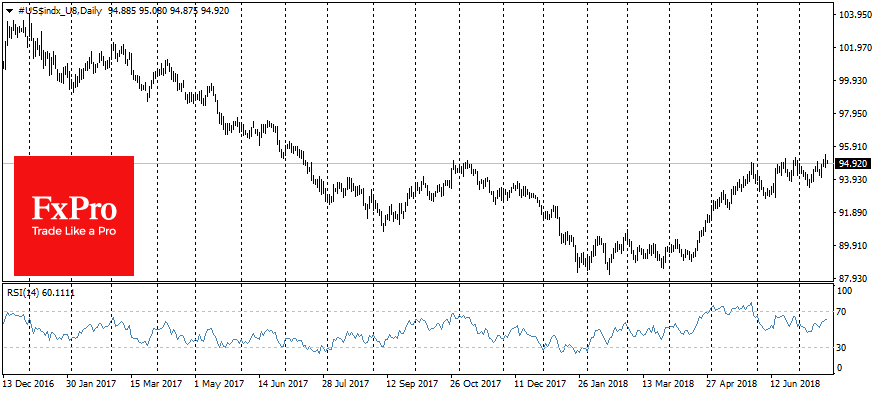

The US Dollar Index Has Updated The Highs

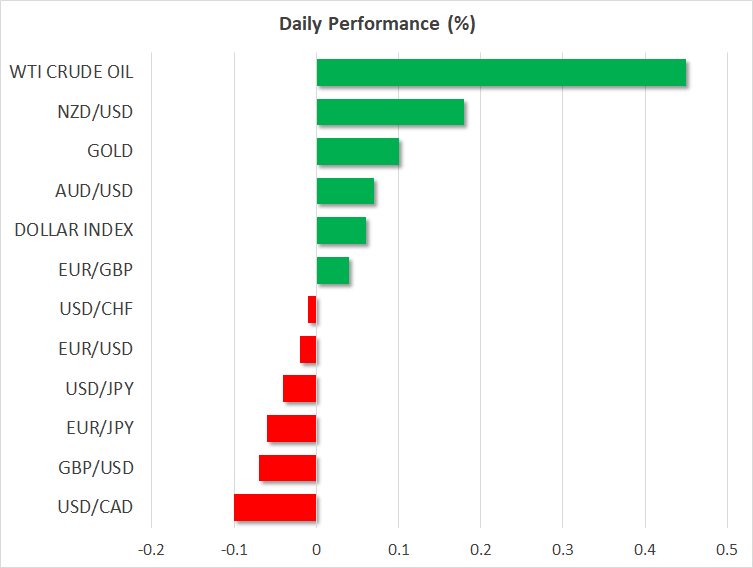

The US currency continued to rise against the basket of major currencies after Powell's, the head of the Fed, positive statements. The US dollar index (#DX) updated the monthly highs and closed in the positive zone (+0.18%). However, the trade war remains the focus of attention. Representatives of the US White House believe that Xi Jinping, President of the People's Republic of China, obstructs negotiations and the achievement of agreements between the countries. At the same time, the EU intends to introduce duties in return on the import of automobiles to the US from Europe. On July 25 representatives from the European Union are going to visit Washington, wheiuniire, most likely, the situation will be clarified.

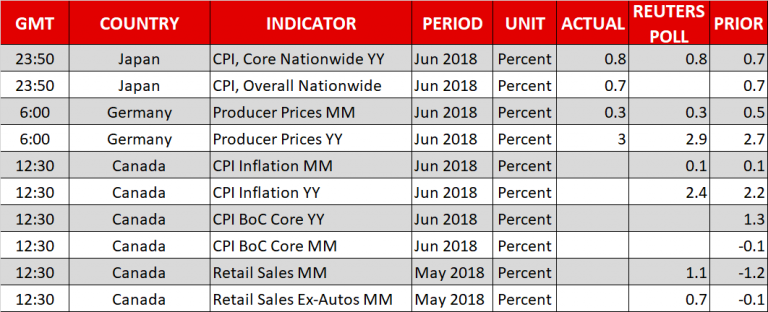

The US dollar is also supported by the index of manufacturing activity from the Federal Reserve Bank for July, published yesterday, which counted to 25.7 and was above the forecasted value of 21.6. Also yesterday, data on the volume of retail sales in the UK for June were published: the indicator dropped to -0.5%, while experts expected +0.1%. Today we expect important statistics from Canada.

The "black gold" prices are moderately growing. At the moment, futures for the WTI crude oil are testing a mark of $68.35 per barrel.

Market Indicators

Yesterday, sales were observed on the US stock market: #SPY (-0.38%), #DIA (-0.49%), #QQQ (-0.50%).

At the moment, the yield of 10-year US government bonds is at the level of 2.84-2.85%.

The news feed on 2018.07.20:

Reports on inflation and retail sales in Canada at 15:30 (GMT+3:00).

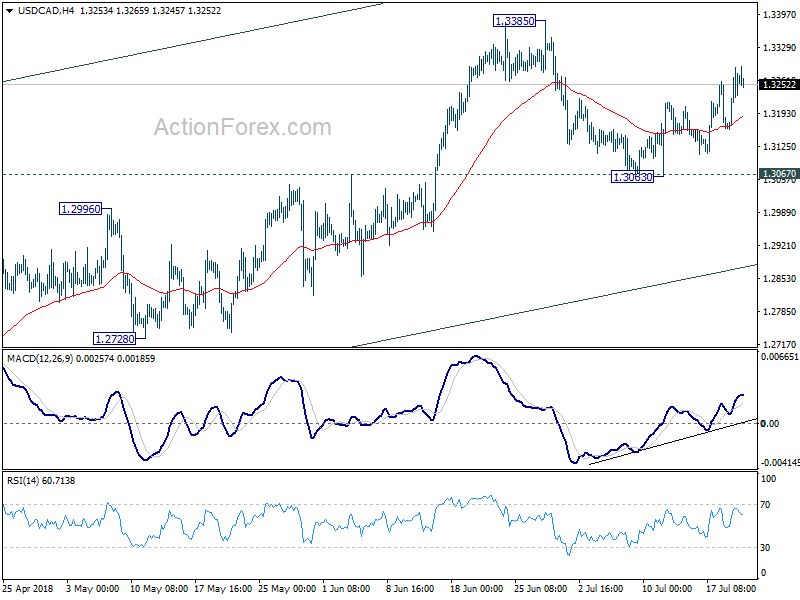

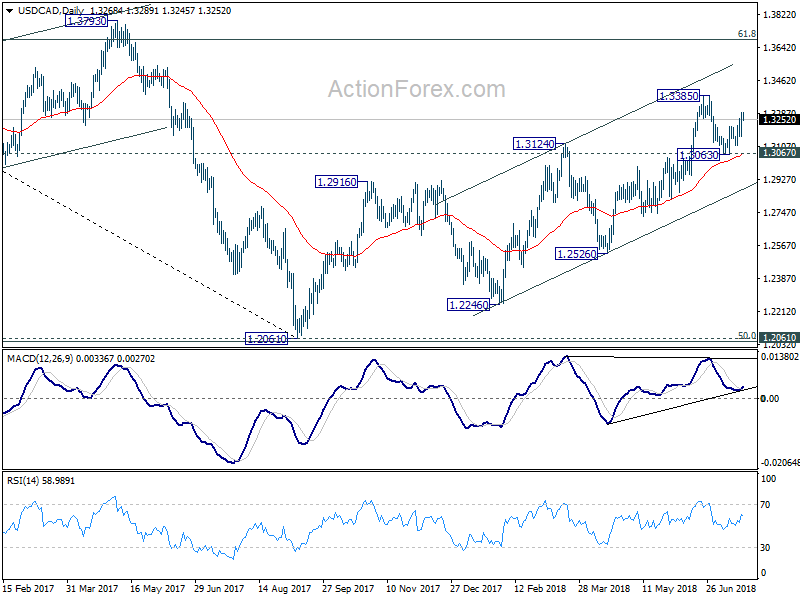

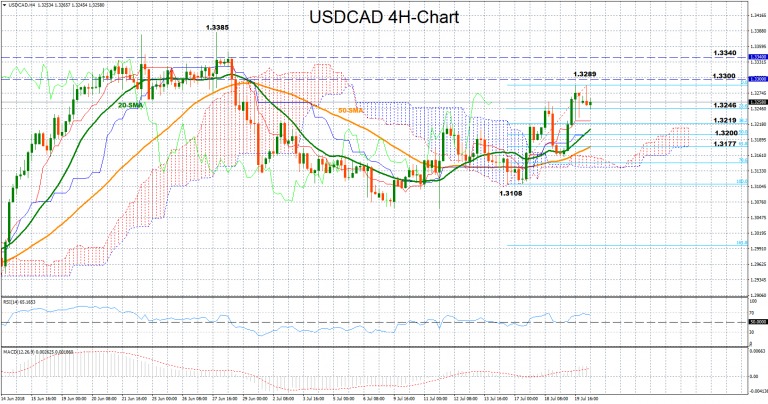

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3187; (P) 1.3240; (R1) 1.3320; More...

Intraday bias in USD/CAD remains on the upside for 1.3385 resistance. Decisive break there would resume larger rally from 1.2061 to 1.3685 fibonacci level. In case of another fall, we'd still expect strong support from 1.3067 resistance turned support to contain downside.

In the bigger picture, as long as channel support (now at 1.2870) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

USD Defense Following Trump’s Comments Will Probably Be Short-Lived

The dollar index reached the one-year highs on Wednesday due to the demand for safe assets. USDX reached level 95.43 on Thursday, breaking the peak levels from November and May-June. However, Trump's comments have caused pressure on the American currency, throwing the dollar from the recently achieved highs.

U.S. president in an interview CNBC noted that the yuan “was dropping like a rock”, and the rising dollar and higher interest rates raise concerns about the potential impact on the economy. The strengthening of the currency makes the production of local companies comparatively expensive, which is able to slow growth.

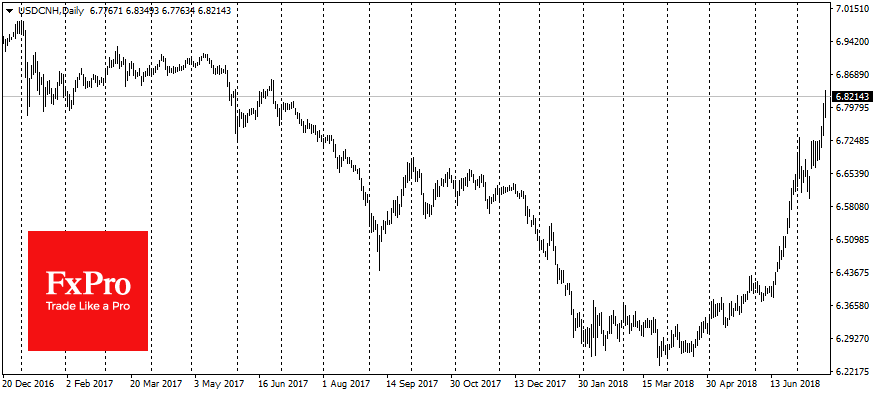

At the same time, the weakening of the dollar has not yet unfolded the demand for protective assets, including bonds, and the decline in shares. On Thursday and Friday morning fears about the escalation of trade wars between USA and China caused a new easing of yuan, as well as pressure on the stock markets.

On Friday morning the yuan sank to new lows compared to the last 13 months. Since the beginning of the month CNY lost 3%, and for three months of active sales it sagged 9%. Chinese largest companies also remain under pressure on Friday morning, despite the weakness of the national currency, which often supports stocks.

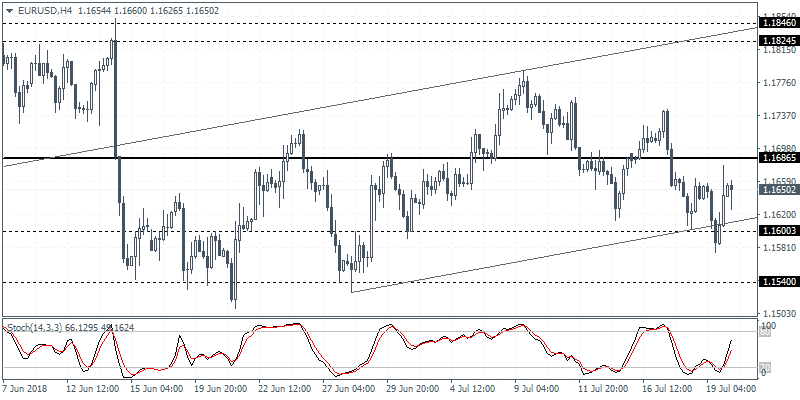

The EURUSD pair fell on Thursday to 1.1575 but rose to 1.1676 due to market reaction to the Trump's comments. At the moment the pair stabilized around 1.1650. For the year from January 2017 to January 2018 EURUSD added more than 20%, on accelerating eurozone growth and low inflation in the US, but half of this increase was erased in the first half of this year, when fears around trade wars and a more stringent tone of the Fed caused an increase in demand for the U.S. currency.

It is not necessary to overestimate the influence of comments of the U.S. President. Previously, it was limited and short-lived. He has repeatedly expressed such a point of view, but it did not prevent the Fed to tighten the policy and it even increased its pace. It should also be remembered that similar comments in Davos at the beginning of the year caused an immediate reaction to the weakening but had no long-term consequences. The American dollar soon after the similar comments of Trump and Mnuchin stopped a month-long fall and soon turned to growth.

Dollar Steps Back After Trump Comments, Yuan Drops To Fresh Lows On Trade War Concerns

Here are the latest developments in global markets:

FOREX: The US dollar posted losses across the board during Friday's Asian trading; extending the retreat from its highs which started on Thursday. The dollar sell-off was more of a corrective nature for now and was sparked by criticism of the Federal Reserve's rate hikes by President Donald Trump. The Chinese yuan also dropped, as USDCNY crossed above the 6.80 threshold before coming back down.

STOCKS: Wall Street indices closed negative on Thursday and while the sell-off initially carried over to Asia, many indices managed to trade in the green later. Worries that a looming trade war could have wider repercussions such as a weaker Chinese currency remained a concern –, particularly for Asian stock markets. Europe was expected to open lower by around 0.1-0.2% after a dull session on Thursday.

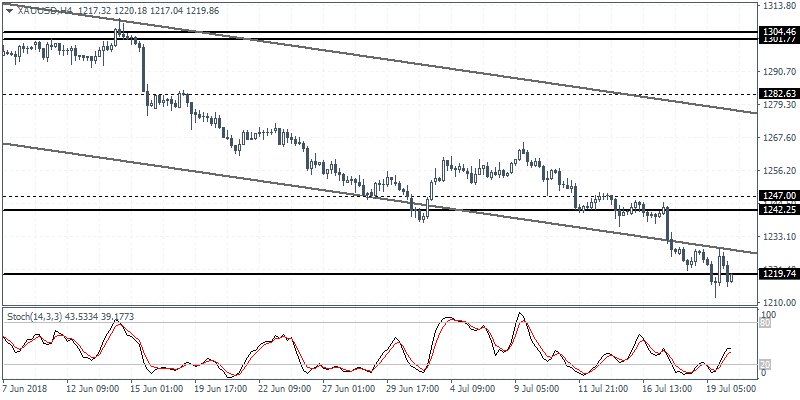

COMMODITIES: Gold found the chance to rebound from its 1-year low of $1215 an ounce registered the previous day, taking advantage of the weakness of the US dollar. Gold was trading around $1222 an ounce at the time of writing. Oil was consolidating its gains from the previous day, as WTI traded above $68 a barrel. Oil traders were looking forward to the Baker Hughes rig count later in the day to get a better picture of US supply prospects.

Major movers: Antipodeans snap back after sustained losses; dollar/yen back below 113 and euro/dollar above 1.16

The US dollar sold off despite a fresh near 50-year low in weekly initial jobless claims announced the previous day. The trigger for some more profit-taking on the greenback was provided by President Trump, who criticized the Fed's rate hikes as they could damage the economy. Although US presidents generally shy away from criticizing monetary policy, it is too early to say that Trump's comments will have any meaningful significance for policymakers. They are unlikely to have an impact but it would also be a mistake to discount the damage to the central bank independence a potential “politicization” of the interest rate debate could do. The White House issued a statement following Trump's comments saying that the President “respected the central bank's independence”, he was “not interfering with policy decisions” and was just “reiterating his long-held views on interest rates”. For a dollar that had been perhaps overbought lately, this provided a convenient excuse for taking profits.

Another big currency story was the fresh 1-year low by the Chinese yuan. Dollar/yuan climbed to 6.8128 before dropping back below 6.80 at around 6.7940 because of rumored intervention by state-owned banks. The fact that the yuan could not hold during a session that the US dollar was generally weak, might signal that there is potential for further weakness in the Chinese currency. Indeed there is speculation that the Chinese government might be using the yuan as a weapon in the trade wars, but it is perhaps even more likely that the prospect of a trade war with the US has caused selling of Chinese assets and therefore a market-driven decline in the yuan.

Antipodeans such as the kiwi and the aussie took advantage of the dollar's weakness to recover a part of their recent losses. One suspects that the recovery would have been even bigger, had it not been for the negative story of the yuan depreciation, which could weigh on countries that export to China.

In other economic news, Japanese inflation for June remained quite low; 0.7% year-on-year for the national headline rate and 0.8% for the core rate. These inflation numbers show that the Bank of Japan is unlikely to be in any hurry to curtail its massive monetary stimulus program.

Day ahead: Canada reports on inflation and retail sales; G20 meeting kicks off in Buenos Aires

Friday's economic calendar will feature Canadian CPI and retail sales figures, while the global trade turmoil will continue to feed risk-off sentiment as the US shows no appetite to pull back its protectionist tariff measures, whereas the EU and China seek ways to defend their interests.

At 1230 GMT, Statistics Canada is expected to show that overall consumer prices have risen by 2.4%year-on-year in June, 0.2 percentage points faster than in May when the headline CPI stood at 2.2%. Given that Bank of Canada aims to keep the total CPI inflation at the 2.0% midpoint of a target range of 1-3.0% over the medium-term, markets could increase speculation that policymakers are preparing another 25bps rate hike in coming months. The soonest such a rate hike could be delivered would be at the October or December meeting where investors give a chance of 43% and a 54% respectively. While there are is no forecast available for the core, median, or trimmed mean CPI measures, these will be closely reviewed as the central bank uses these volatility-free indices to identify changes in the inflation trend.

Canadian retail sales, which are considered an ideal proxy for household spending, will also be under the spotlight at the same time. After a 1.2% decline in April, analysts believe that retail sales have rebounded substantially by 1.2% m/m in May. If this is the case, that would be the strongest growth registered since December 2017. In the absence of automobiles, the core equivalent is also projected to recover, rising by 0.7% m/m after falling by 0.1% in the previous month.

Should retail sales increase more than analysts predict, signaling that the previous downturn could be temporary and instead inflationary pressures are heating up, something that could be also proved if CPI figures beat forecasts today, the loonie, which is set to close in the red for the second consecutive week, could erase losses. Alternatively, in the wake of disappointing prints which could reduce odds for further stimulus reduction, the loonie could once more find itself under pressure.

Still, trade uncertainties remain a high risk for the loonie as Canada has already started paying steel and aluminum import tariffs to the US, while the NAFTA story continues to hold in the dark as Canada and Mexico have no intentions to leave the pact despite the US pushing to trim the free-trade agreement and sign separate deals with its Canadian and Mexican counterparts. Therefore, trade issues are something policymakers will seriously consider before proceeding with further stimulus reduction.

Developments on the trade front could create headlines during the weekend (or next week) as the Group of 20 finance ministers and central bank presidents will be gathering in Buenos Aires in Argentina, where trade issues might be high on the agenda. The atmosphere though might not be positive as tariff-affected countries are expected to express their frustration over the US import tariffs on steel and aluminum and the retaliatory responses the measures created. Note that at the March G20 meeting, financial representatives criticized protectionism and called for further dialogue which so far had minimal effect.

Meanwhile in oil markets, Baker Hughes is scheduled to issue its report on the numbers of active rigs for oil drilling at 1700 GMT.

In equity markets, earnings season continues with General Electric Corporation being among companies to release quarterly results before the opening bell. Expectations are for the company to post a decline in second-quarter profits.

Technical Analysis: USDCAD could move sideways in short-term

USDCAD is currently in neutral mode, hovering above the Ichimoku cloud near one-month highs in the four-hour chart. While both the RSI and the MACD hold in bullish territory, the former above 50 and the latter above zero and its red signal line, both seem to be slowing down, hinting that the neutral phase might continue in the short-term. Still any upside or downside surprises in Canadian inflation and retail sales figures later today could bring some spikes to the market.

Should the pair head lower in the wake of an upbeat report, nearby support could be found around the 23.6% Fibonacci retracement of 1.3246 of the upleg from 1.3108 to 1.3289. Further downside below that level could then bring the 38.2% Fibonacci of 1.3219 into view, while steeper declines could also break the 1.3200 round level (50% Fibonacci) to test the 61.8% Fibonacci of 1.3177.

Alternatively, a data miss could bring gains to the US dollar, sending the price probably above the 1.3300 round level, where bulls could stop to retest the area around 1.3350, a strong resistance in June. If the price manages to overcome that obstacle, then attention could turn towards the one-year high of 1.3385 unlocked on June 26.

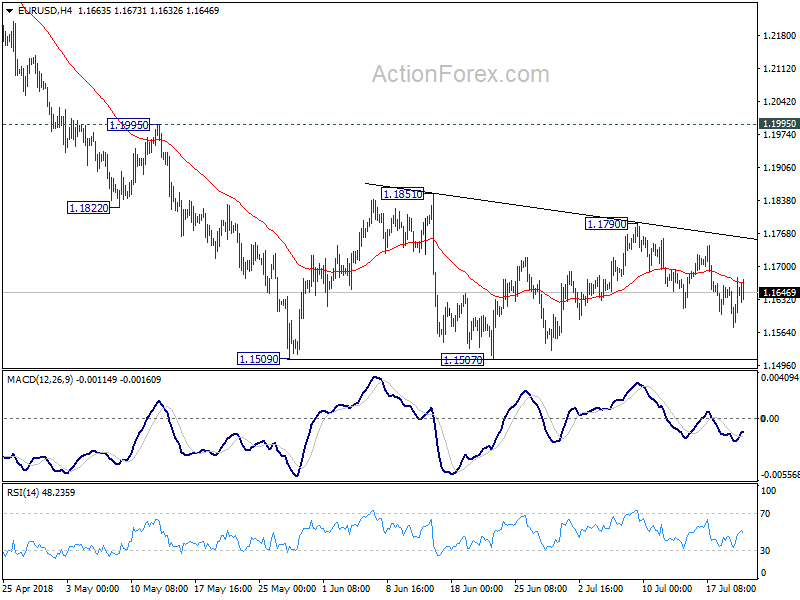

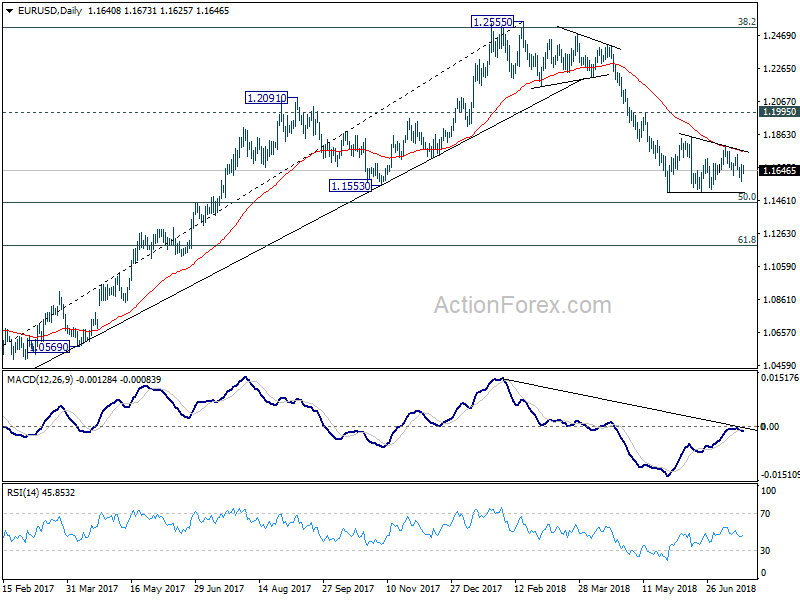

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1586; (P) 1.1631 (R1) 1.1688; More.....

EUR/USD lost downside momentum again as seen in 4 hour MACD. Intraday bias is turned neutral gain. Overall outlook remain bearish and downside breakout is expected, sooner or later. Firm break of 1.1507 will resume whole decline from 1.2555, through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186. On the upside, in case of another rise as consolidation extends, upside should be limited by 1.1851 resistance to bring fall resumption eventually.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

XAUUSD Intraday Analysis

XAUUSD (1219.86): Gold prices continued to extend the declines as price action slipped below the 1219 region. The doji candlestick on the 4-hour chart was followed by a bullish close. While price action managed to pull back from the lows, the current gains could see a move to the upside. Gold prices could be seen rallying to 1242 level of support where resistance is likely to be established. To the downside, failure to clear the 1219 region could signal further declines in gold prices which could push the price of the precious metal lower to 1200.

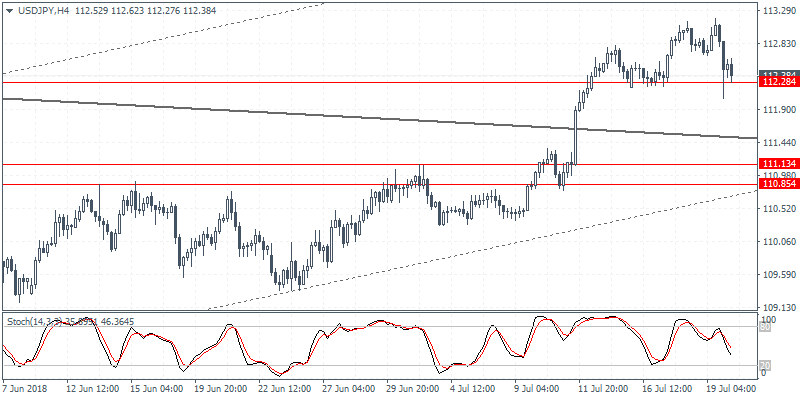

USDJPY Intraday Analysis

USDJPY (112.38): The USDJPY currency pair fell briefly below 112.28 support before recovering back. The rebound of this level failed to see the currency pair make any major gains. Therefore, we expect to see the U.S. dollar extending the declines against the yen. A break down below 112.28 could signal a near-term decline to the lower support at 111.13 - 110.85 regions. In the near-term, the currency pair could be seen maintaining a sideways range within the levels.

EURUSD Intraday Analysis

EURUSD (1.1650): The EURUSD currency pair drifted lower on Thursday as price action touched intraday lows of 1.1575. However, the currency pair managed to recover to close slightly higher from the open. The consolidation in the currency pair is expected to continue and the rebound off 1.1600 is expected to keep price action supported to the upside in the near term. The resistance at 1.1686 could be tested in the near term. A break above this level is required in order to ascertain the upside bias in the near term.

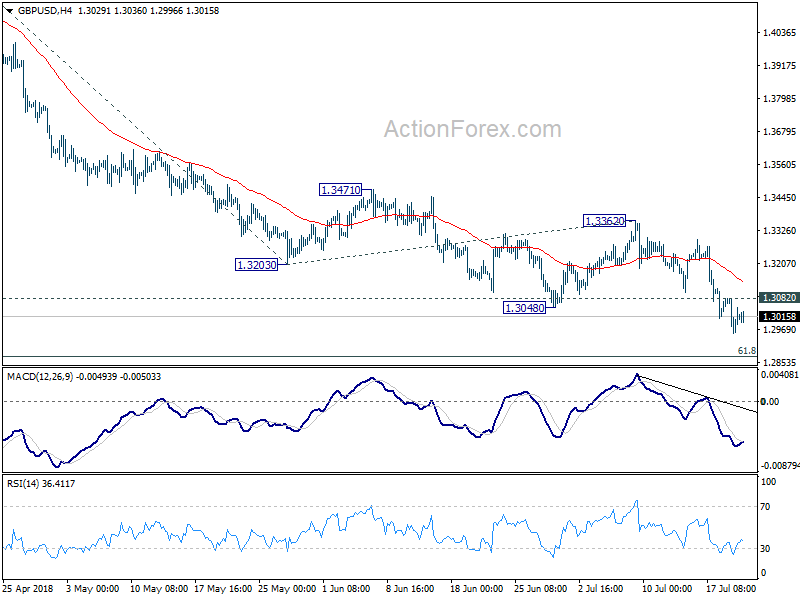

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2953; (P) 1.3019; (R1) 1.3079; More...

Intraday bias in GBP/USD remains on the downside with 1.3082 minor resistance intact. Current fall should target 61.8% projection of 1.4376 to 1.3203 from 1.3362 at 1.2637 next. On the upside, above 1.3082 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 1.3362 resistance to bring fall resumption.

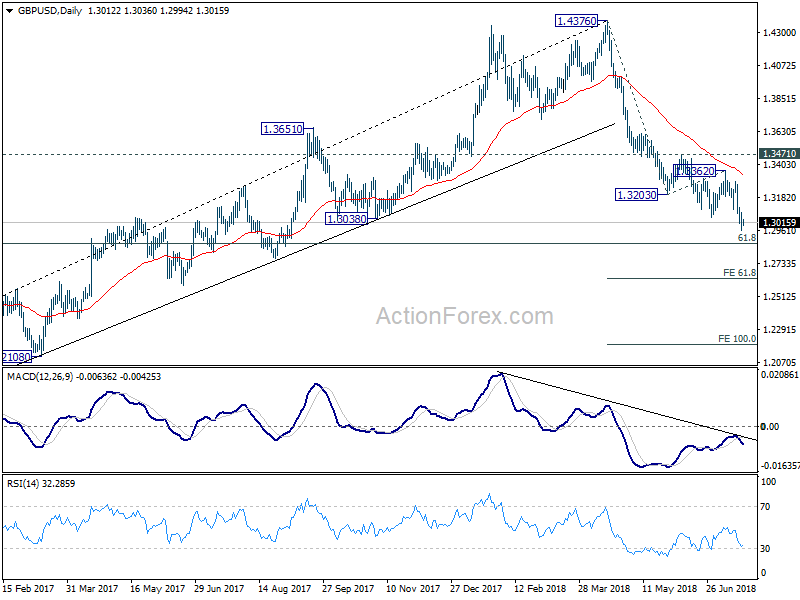

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Canada Retail Sales And Inflation

The U.S. dollar was trading mixed on Thursday. After initially posting strong gains, the greenback eased towards the close of the day. Economic data showed that UK's retail sales fell 0.5% on the month missing estimates of a 0.1% increase. In the U.S., the Philly Fed manufacturing index rose to 25.7 on the indexbeating estimates of 21.6.

The economic data for the day ahead will see the release of the German PPI figures. Economists forecast that producer prices rose 0.3% on the month, marking a slower pace of increase compared to 0.5% registered the month before.

In the NY trading session, Canada will be releasing its inflation and retail sales figures. Headline inflation rate as measured by CPI is expected to advance 0.1% on the month, marking the same pace of increase as the month before. Retail sales are tipped to rise 1.0% on the month following a 1.2% decline the month before. Core retail sales are expected to advance 0.6% after posting a 0.1% decline in the previous month.