Sample Category Title

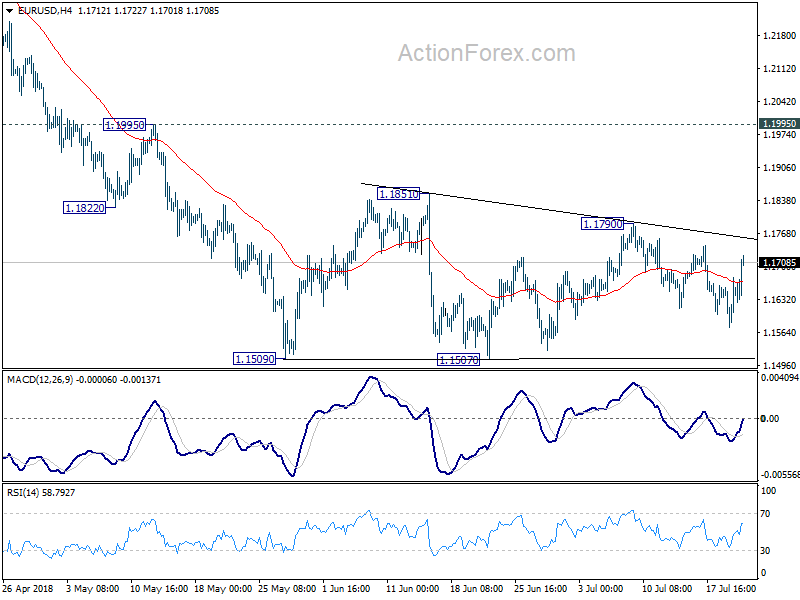

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1586; (P) 1.1631 (R1) 1.1688; More.....

EUR/USD is staying in range below 1.1790 despite a strong rebound today. Intraday bias remains neutral first. Overall outlook remain bearish and downside breakout is expected, sooner or later. Firm break of 1.1507 will resume whole decline from 1.2555, through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186. On the upside, in case of another rise as consolidation extends, upside should be limited by 1.1851 resistance to bring fall resumption eventually.

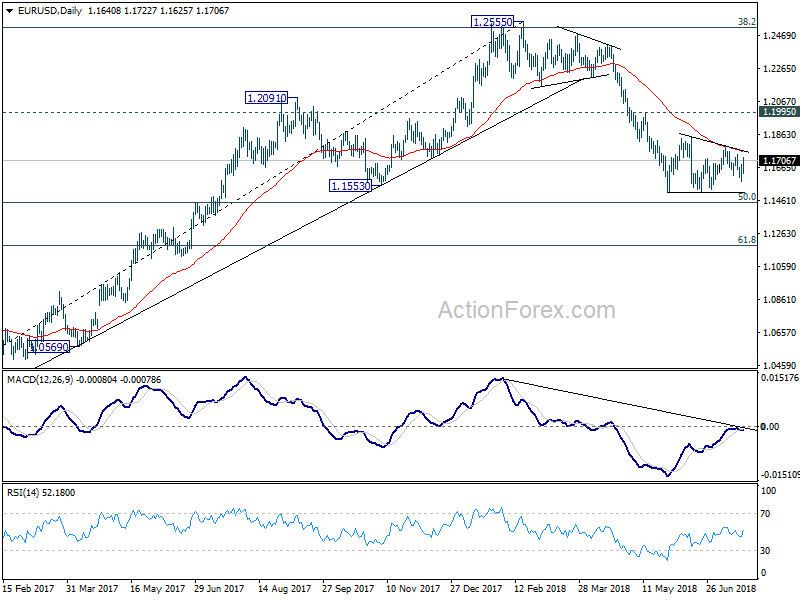

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

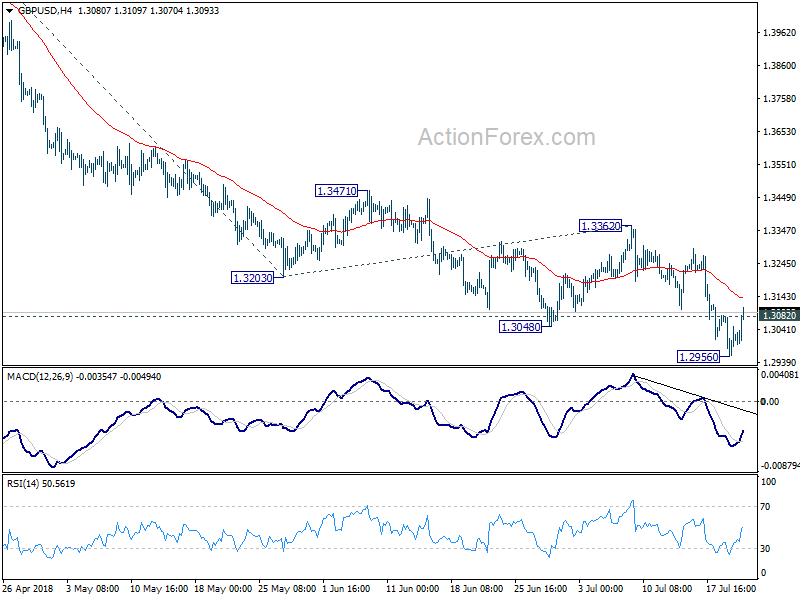

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2953; (P) 1.3019; (R1) 1.3079; More...

GBP/USD's strong recovery and break of 1.3082 suggests that a temporary low is formed. Intraday bias is turned neutral to bring some consolidation Stronger recovery could be seen. But upside should be limited well below 1.3362 resistance to bring fall resumption. Break of 1.2956 will resume the fall fro 1.4376 to 61.8% projection of 1.4376 to 1.3203 from 1.3362 at 1.2637 next.

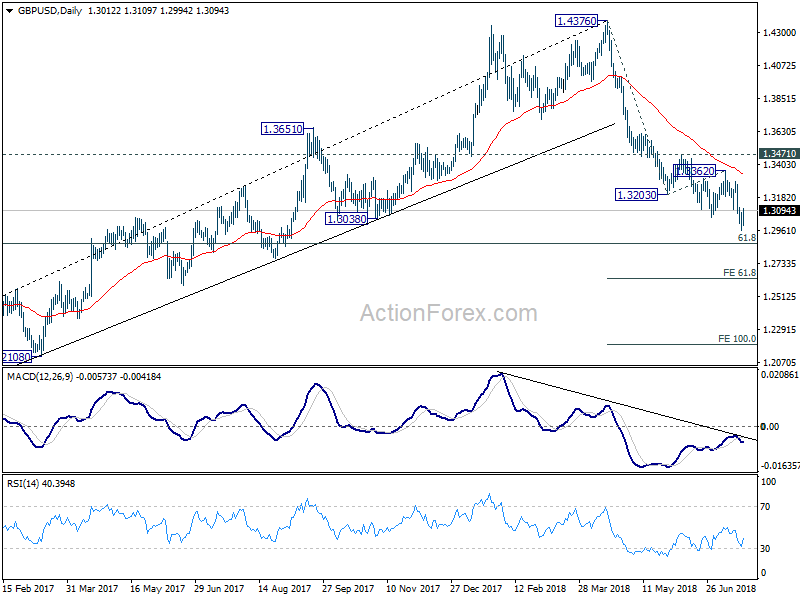

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

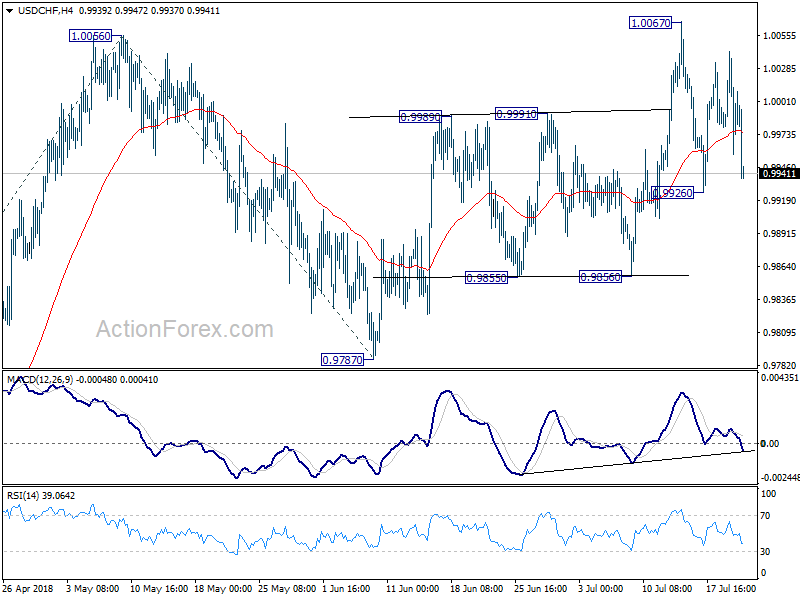

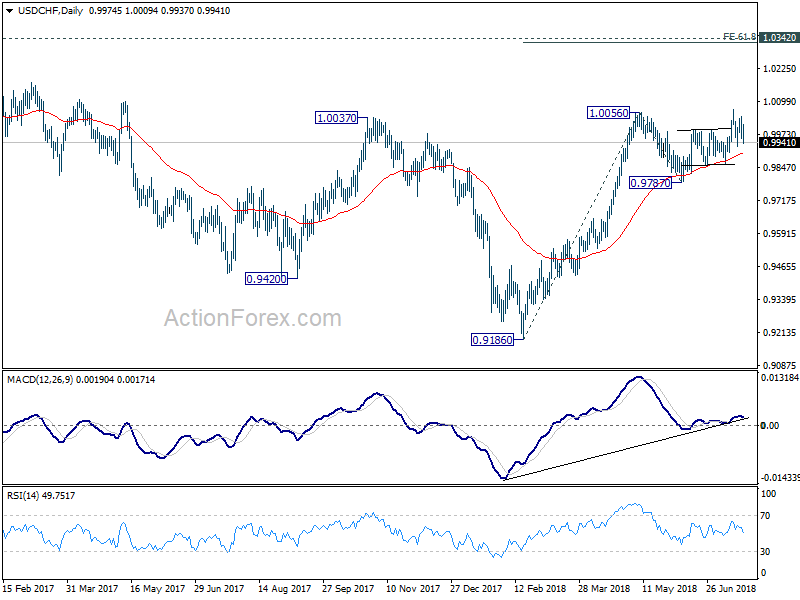

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9953; (P) 0.9998; (R1) 1.0037; More...

USD/CHF drops sharply in early US session but stays in range of 0.9926/1.0067 and intraday bias remains neutral. On the upside, break of 1.0067 resistance will resume the larger rise from 0.9186. USD/CHF should then target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, break of 0.9926 will dampen the bullish view again. The pair could target 0.9856 support for deeper decline.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. After drawing support from 55 day EMA, it's now resuming for 1.0342 key resistance. For now, we'd still cautious on strong resistance from there to limit upside. Meanwhile, break of 0.9787 support is needed to signal completion of the rise. Otherwise, outlook will remain bullish even in case of deep pull back.

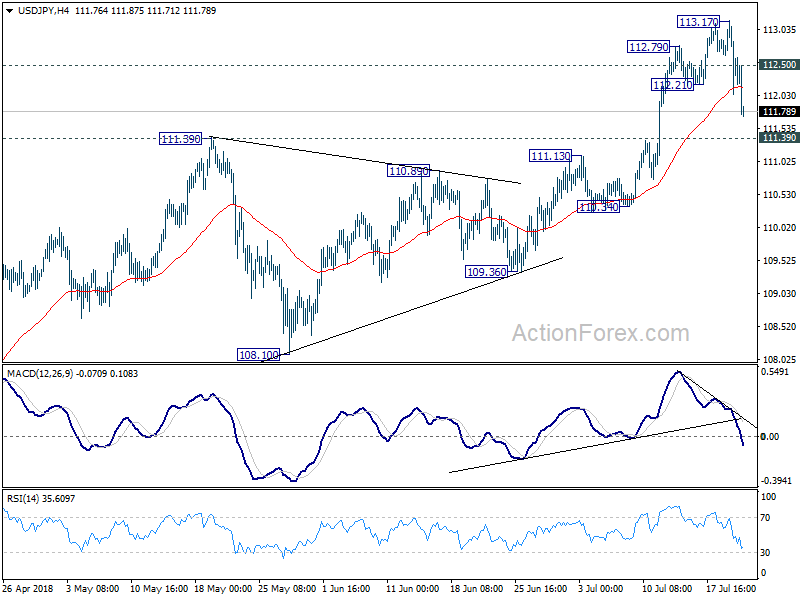

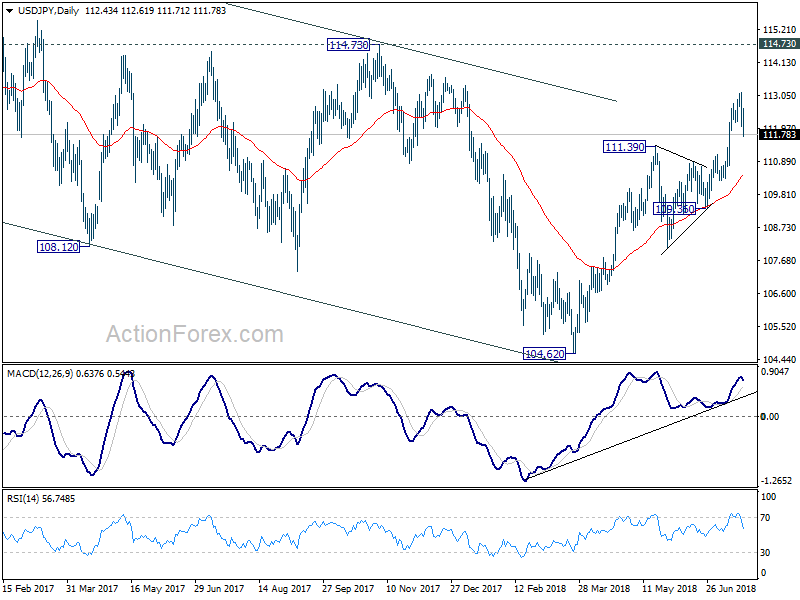

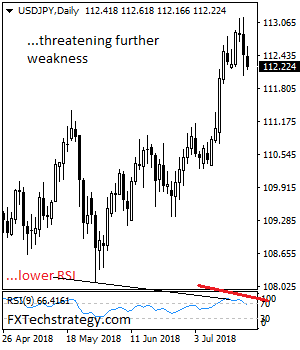

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.94; (P) 112.58; (R1) 113.10; More...

Intraday bias in USD/JPY remains mildly on the downside as the correction from 113.17 extends. Deeper fall could be seen but downside should be contained by 111.39 resistance turned support to bring rebound. On the upside, above 112.50 minor resistance will bring retest of 113.17 first.

In the bigger picture, current development, with the solid break of medium term channel resistance from 118.65 (2016 high), affirm our view that corrective fall from there has completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will now be the preferred case as long as 119.36 support holds.

Canada: Consumer Prices Up 2.5% in June, Core Measures Average 2%

Consumer prices were up 2.5% year-on-year in Canada in June, up from 2.2% in May and above the consensus forecast for 2.3%. Adjusted for seasonal patterns, prices rose 0.1% month-on-month.

Several items saw price growth accelerate year-on-year, led by energy prices at 12.4% (from 11.6%). The only category to see inflation slow was household operations, which fell 0.1% (y/y) from +0.3% in May.

The Bank of Canada's core measures edged up. CPI-trim and CPI-median both rose to 2.0% (from 1.9% previously), while CPI-common was unchanged at 1.9%.

Key Implications

Following a soft report last month, inflation regained its stride in June. Price growth is right on target, with evidence of firming in several categories. Energy prices will remain volatile, and lower prices for telephone services are still weighing on inflation. Looking through that, inflation is consistent with a healthy economy operating close to full potential.

Downside risks to trade remain at the fore, but the economic data are increasingly making the case for further Bank of Canada rate hikes. With a positive retail sales report, and the upside surprise on inflation, the odds of one more hike this year have risen.

May Thaw Brings Canadians Back to the Shops

Canadian retail sales climbed 2.0% in May, a solid recovery from April's (revised) 0.9% drop, which Statistics Canada attributed to inclement weather in many parts of the country. The sales gain was all due to more goods being sold, as constant-dollar sales were also up 2%.

The growth was largely a function of a recovery of motor vehicle and parts sales (+3.7%) and gasoline stations (+4.3%). Nominal sales excluding these categories were up 0.9%.

Most trade categories saw sales rise in May, with the exception of the sizeable food and beverage category, where sales fell 2.1% on weakness at supermarkets.

E-commerce sales, reported on a year-on-year basis, continued to roar ahead, up 16.9%, more than tripling the 5.5% yearly pace marked by overall sales.

Regionally, Quebec (+3.0%) and Ontario (+2.6%) did the heavy lifting, although sales rose in most (7 of 10) provinces.

Key Implications

The May thaw seems to have not only hit April's ice, but also consumers wallets. A rebound was to be expected given the weather effects that kept some Canadians at home in April, but the jump in May more than made up for this set-back.

It is important not to get too carried away with this data – keep in mind that retail sales activity only captures about a fifth of overall consumer spending. Taking a longer-term view, the six month trend in this indicator is effectively in line with its long-run average, while the trend in volumes is effectively flat.

Still, the strong showing in May sends our Q2 real GDP tracking to a robust 2.9% – basically in line with the Bank of Canada's most recent forecast. To that end, the fact that consumer spending on cars remains healthy despite rising borrowing costs suggests that the tightening cycle still has lots of room to run.

British Pound Higher Despite Higher UK Deficit

The British pound has steadied on Friday, after posting losses for most of the week. In the North American session, the pair is trading at 1.3067, up 0.42% on the day. On the release front, Britain’s debt widened to GBP 4.5 billion, higher than the estimate of GBP 3.6 billion. There are no U.S indicators on the schedule.

Soft British indicators this week have weighed on the pound, which has declined 1.2% this week. Employment data was weaker than expected on Tuesday, and this was followed by a soft CPI release a day later. On Thursday, retail sales declined 0.5%, surprising the markets which had expected a gain of 0.1%. This marked the first decline since March. The weak numbers have dampened expectations that the BoE will raise interest rates at its August meeting. With the May government continuing to squabble over Brexit and negotiations with the EU at a standstill, the pound could face further headwinds and drop under the symbolic 1.30 level.

The tariff slugfest between the U.S and its major trading partners has raised serious concerns not just with investors, but with Federal Reserve policymakers as well. The Federal Reserve Beige Book for July, released on Wednesday, was rife with references to ‘tariffs’. This trend started in the April Beige Book after President Trump threatened in March to impose tariffs on China. Most of the twelve Fed regional districts referred to tariffs in their individual reports, which make up the Beige Book. Some Fed policymakers have also voiced their concern over the impact that tariffs could have on the U.S economy and is an issue the Fed will have to take into consideration, as it mulls over rate policy for the next six months.

USDJPY: Pulls Back, Weakens

USDJPY - The pair remains biased to the downside on further corrective weakness. On the downside, support lies at the 112.00 level where a break if seen will aim at the 111.50 level. A cut through here will turn focus to the 111.00 level and possibly lower towards the 110.50 level. On the upside, resistance resides at the 113.00 level. Further out, we envisage a possible move towards the 113.50 level. Further out, resistance resides at the 114.00 level with a turn above here aiming at the 114.50 level. On the whole, USDJPY faces further downside pressure.

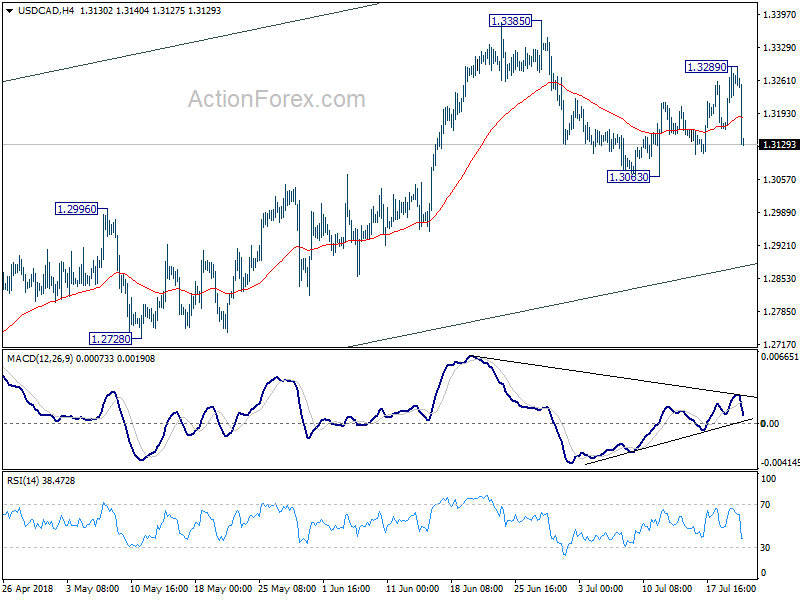

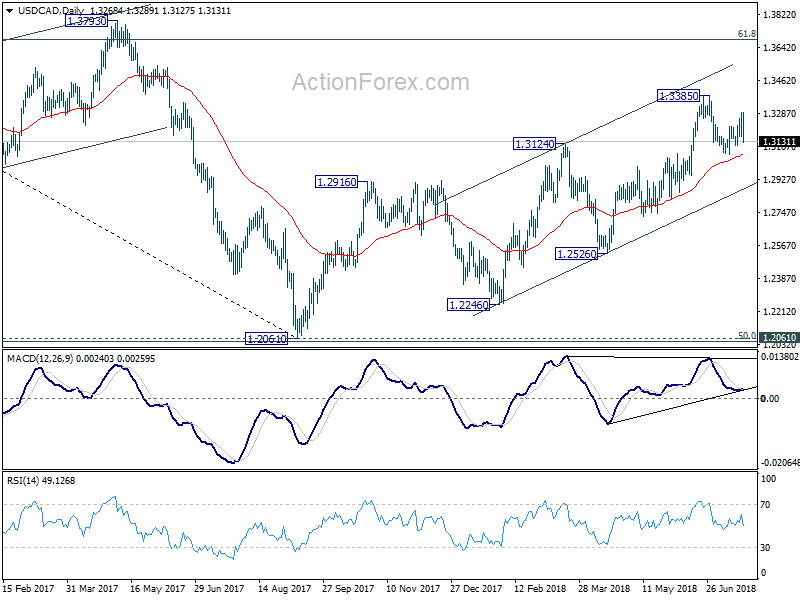

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3187; (P) 1.3240; (R1) 1.3320; More...

USD/CAD's sharp decline suggests that a temporary top is at least formed at 1.3289. But it's staying above 1.3063 so far and intraday bias is turned neutral first. On the downside, break of 1.3063 will extend the corrective decline from 1.3385 with another falling leg. USD/CAD should then target channel support (now at 1.2880). For now, we'd expect strong support from there to bring rebound. On the upside, above 1.3289 will bring retest of 1.3385 high instead.

In the bigger picture, as long as channel support (now at 1.2880) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

Dollar Sharply Lower as Trump’s Reliable Ally Challenges Him on Tariffs, Canadian Dollar Jumps on Strong Data

Dollar suffers steep selloff in the early US session as WSJ reports that Senate Finance Committee Chairman Orrin Hatch sent a letter to Trump requesting him to reconsider his trade policies. And Hatch warned that GOP senators may be ready to risk a legislative confrontation with Trump if he doesn't reverse course. Hatch is a seven-term Utah Republican Senator who's seen as a reliable Trump ally.

Earlier today, CNBC released a video on the interview of Trump at the White House taken yesterday. Trump complained again the the US has been "ripped off by China for a long time". And he's "ready to go to 500", referring to tariffs on USD 500B of Chinese imports. That's nearly all of the USD 505.5B Chinese imports in 2017. And he pledged that he's "not doing this for politics" but "to do the right thing for the country".

Separately, White House economic adviser Larry Kudlow laid the blame on Chinese President Xi Jinping again. He said, "the problem here is Xi. He doesn't want to move, and they've offered the U.S. absolutely ... no options regarding the issue of (intellectual property) theft and forced technology transfer."

The timing of these rhetorics and the interview is a bit odd. But after all, we'll soon know whether these stories will continue to develop, or the American's focuses will be back on the relationship of their President and Russia and Vladimir Putin quickly.

Canadian Dollar jumps on stellar retail sales, CPI accelerated

Canadian Dollar surges sharply in early US session after stellar retail sales data. Headline retail sales rose 2.0% mom in May versus expectation of 0.0% mom. That's more than offset -1.2% mom contraction in April. Ex-auto sales also jumped 1.4% mom, well above expectation of 0.5% mom.

Headline CPI accelerated to 2.5% yoy in June as expected. CPI core common was unchanged at 1.9% yoy. CPI core median rose 0.1% to 2.0% yoy. CPI core trim rose 0.1% to 2.0% yoy.

The set of data gives a nod to BoC's rate hike earlier in the month and it's hawkish stance.

German Merkel: Can't rely on the superpower of the US

German Chancellor Angela Merkel said in a news conference that the Germany "can't rely on the superpower of the United States. And the auto tariffs are "a real threat to the prosperity of many in the world". Also, the "usual framework" of the world is "under strong pressure at the moment" before of the US. Though, she maintain that "transatlantic working relationship, including with the U.S. president, is crucial for us and I will carry on cultivating it".

For the EU, Merkel said it's in a "transformation process". And, "it recognizes the seriousness of the situation, but it hasn't yet been resolved whether we are going to rise to the challenges quickly enough." She pointed to the "big economic challenge, and one day certainly also military, from the strengthening of China". And, the EU must also deal with the relationship with Russia.

Released in European session, German PPI rose 0.3% mom, 3.0% yoy in June. Eurozone current account surplus narrowed to EUR 22.4B in May. UK public sector net borrowing rose to GBP 4.5B in June.

Japan core CPI rose 0.8% yoy but mainly driven by energy

Released from Japan, the all items CPI rose 0.1% mom, 0.7% yoy in June. Core CPI, all item less fresh food, rose 0.1% mom, 0.8% yoy. Core core CPI, all item less fresh food and energy, has indeed dropped -0.1% mom and rose 0.2% yoy.

The set of data should be rather disappointing for the BoJ. The decline in core core CPI suggests that inflation was mainly driven by the surge in energy costs. There wasn't much of press pressure elsewhere. It's remains a long road to meet its 2% inflation target. And there is no light on when the central could withdraw the massive stimulus.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3187; (P) 1.3240; (R1) 1.3320; More...

USD/CAD's sharp decline suggests that a temporary top is at least formed at 1.3289. But it's staying above 1.3063 so far and intraday bias is turned neutral first. On the downside, break of 1.3063 will extend the corrective decline from 1.3385 with another falling leg. USD/CAD should then target channel support (now at 1.2880). For now, we'd expect strong support from there to bring rebound. On the upside, above 1.3289 will bring retest of 1.3385 high instead.

In the bigger picture, as long as channel support (now at 1.2880) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jun | 0.80% | 0.80% | 0.70% | |

| 04:30 | JPY | All Industry Activity Index M/M May | 0.10% | 0.00% | 1.00% | |

| 06:00 | EUR | German PPI M/M Jun | 0.30% | 0.20% | 0.50% | |

| 06:00 | EUR | German PPI Y/Y Jun | 3.00% | 2.90% | 2.70% | |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 22.4B | 27.2B | 28.4B | 29.6B |

| 08:30 | GBP | Public Sector Net Borrowing Jun | 4.5B | 3.7B | 3.4B | 3.9B |

| 12:30 | CAD | Retail Sales M/M May | 2.00% | 0.00% | -1.20% | |

| 12:30 | CAD | Retail Sales Ex Auto M/M May | 1.40% | 0.50% | -0.10% | |

| 12:30 | CAD | CPI M/M Jun | 0.10% | 0.30% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Jun | 2.50% | 2.50% | 2.20% | |

| 12:30 | CAD | CPI Core - Common Y/Y Jun | 1.90% | 1.90% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Jun | 2.00% | 1.90% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y Jun | 2.00% | 1.90% |