Sample Category Title

EUR/USD – Euro Under Pressure, Dips Below 1.16

EUR/USD is lower in the Thursday session, following the downward trend which has marked much of the week. Currently, the pair is trading at 1.1602, down 0.31% on the day. On the release front, there or no eurozone or German indicators. In the U.S, unemployment claims is expected to rise to 220 thousand. The Philly Fed Manufacturing Index is expected to climb to 21.6 points. On Friday, German PPI is expected to dip to 0.3% and the eurozone current account surplus is forecast to narrow to EUR 27.2 billion.

The tariff slugfest between the U.S and its major trading partners has raised serious concerns not just with investors, but with Federal Reserve policymakers as well. The Federal Reserve Beige Book for July, released on Wednesday, was rife with references to ‘tariffs’. This trend started in the April Beige Books after President Trump threatened in March to impose tariffs on China. Most of the twelve Fed regional districts referred to tariffs in their individual reports, which make up the Beige Book. Some Fed policymakers have also voiced their concern over the impact that tariffs could have on the U.S economy and is an issue the Fed will have to take into consideration, as it mulls over rate policy for the next six months.

Fed Reserve Chair Jerome Powell reaffirmed his positive outlook on the U.S economy in testimony before the Senate Banking Committee earlier this week. Powell said that he expected the labor market to remain tight and inflation to stay close to the Fed’s target of 2 percent for the next several years. Powell added that the Fed would continue to gradually raise interest rates. Lawmakers appeared satisfied with current monetary policy, but Powell did face some pointed questions regarding the escalating trade war, which has raised concerns that economy could take a downturn if the tariff battles continue.

A milestone was reached on Thursday, as Eurozone Final CPI reached the 2.0% threshold in the June release. On an annualized basis, Final CPI also came in at 2.0%. This marks the highest level since February 2017. As the ECB prepares to wind up its asset-purchase program, the markets are looking for clues about a possible rate hike. Such a move would likely have a significant impact on the markets, as the ECB last raised rates back in 2011. If inflation levels continue to rise, there will be more pressure on the ECB to consider a rate hike sooner rather than later.

Dollar surges as US-China trade spat heats up again

Dollar rises broadly today as trade spat between US and China heated up again. It's started yesterday when Trump's economic advisor Larry Kudlow blamed Chinese President Xi Jinping for for holding back the trade deal with the US. The timing of such accusation is a bit odd, sounding like it's out of nothing. Nevertheless, it doesn't occupy a lot of air time except that such comments triggered some nerves of Chinese government officials. For the Americans, their focuses seem to be staying on Trump's summit with Putin.

Anyway, Chinese Foreign Ministry Hua Chunying said in a regular press briefing today that Kudlow "unexpectedly distorted the facts and made bogus accusations is shocking and beyond imagination." And, "the United States' flip-flopping and promise-breaking is recognized globally." And, "in the face of people all over the world, it is shocking that the relevant US officials have turned black and white and reversed it."

She added that "the US behavior can only seriously damage its own reputation once again, and it is completely unhelpful to solve the problem." Hua also reiterated China's position that "do not want to fight, not afraid to fight."

Trade war has so far been supporting Dollar. And it seems like, the more noise, the more strength for the greenback.

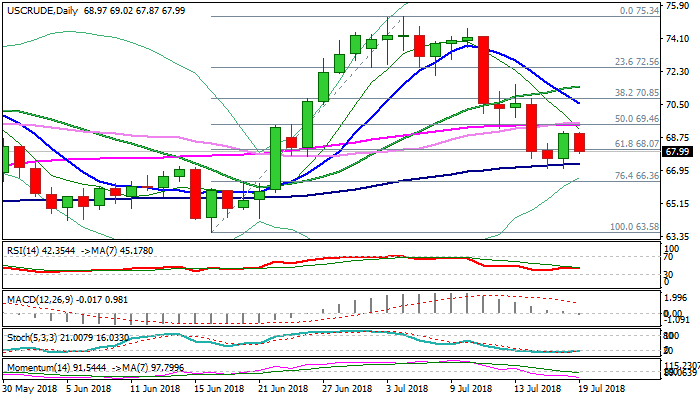

WTI OIL Outlook: Comes Under Renewed Pressure On Oil Stocks Build / Increase Of US Output

WTI oil price fell on Thursday after recovery attempts from $67.02 double-bottom (also 100SMA) stalled on negative news that increased pressure on oil prices.

Unexpected strong rise in oil inventories (EIA report showed build of 5.8 million barrels in the past week, against forecasted draw of 3.6 million barrels and previous week’s massive 12.6 million barrels draw), increase in US oil production which hit 11 million barrels per day and also higher output from the biggest world oil producers, pushed oil prices lower.

Fresh weakness turns focus lower again for test of key supports at $67.02, break of which would generate strong signal of continuation of steep downtrend from $75.34 (04 July high).

Bearish techs and fundamentals continue to produce strong pressure, however, consolidation above $67.02 pivots may extend as daily studies overbought.

Double upside rejection at $69.04 marks strong resistance which should limit upticks and keep intact upper pivot at $69.45 (55SMA).

Res: 68.50, 69.02, 69.45, 70.00

Sup: 67.32, 67.02, 66.36, 65.71

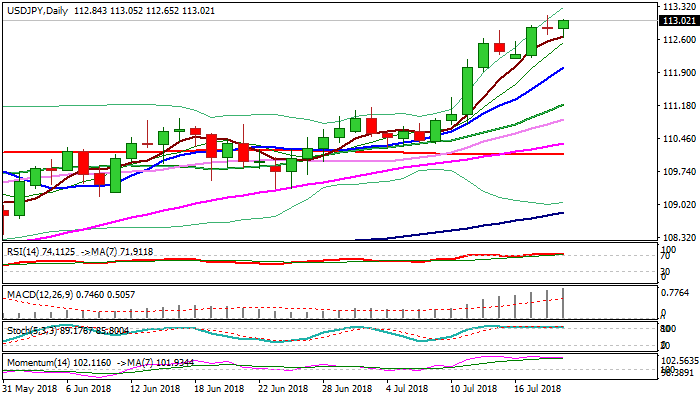

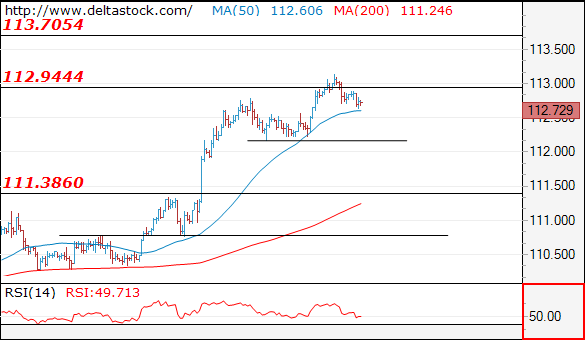

USDJPY Outlook: Bullish Outlook Remains Intact After Wednesday’s Doji

The pair is regaining traction and probes again above 113 barrier on Thursday, pressuring previous day’s new multi-month high at 113.13 and sidelining downside risk signaled by Wednesday’s Doji with long upper shadow.

Near-term bias remains bullish despite persisting overbought conditions and looks for test of a cluster of strong barriers at 113.38 (2018 high) and 113.63/74 (Dec 2017 highs).

Rising 5SMA which marks our initial support (currently at 112.67) contained today’s downside attempts and continues to track the advance.

Only firm break below 5SMA and today’s close in red would sideline bulls and generate initial signal of reversal.

Res: 113.13, 113.38, 113.63, 113.74

Sup: 112.65, 112.19, 112.01, 111.70

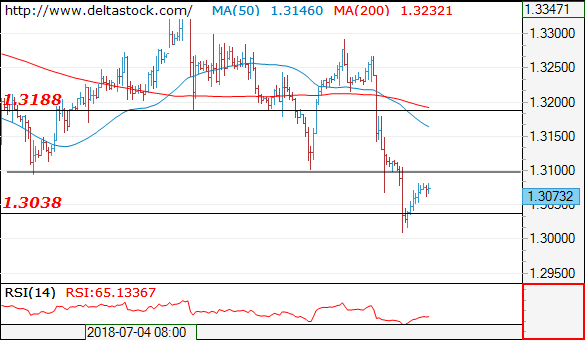

Pound Hammered As U.K Retail Sales Disappoint

The British Pound was immediately attacked by sellers on Thursday morning after retail sales tumbled -0.5% in June, well below the 0.2% market expectation.

With wage growth disappointing and inflation cooling as well, is this really the right environment to raise interest rates? Market expectations over the Bank of England raising interest rates next month are now likely to be heavily diminished and this can already be reflected in the Pound’s bearish price action.

With the Sterling highly sensitive to monetary policy speculation, further losses may be witnessed as investors scale back bets of a rate hike this quarter.

The GBPUSD has plunged to a 10-month low below 1.2990 this morning and has scope to extend losses as long as bears can maintain control below 1.3000. If the Dollar continues to appreciate, the next key level of interest can be found around 1.2950.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

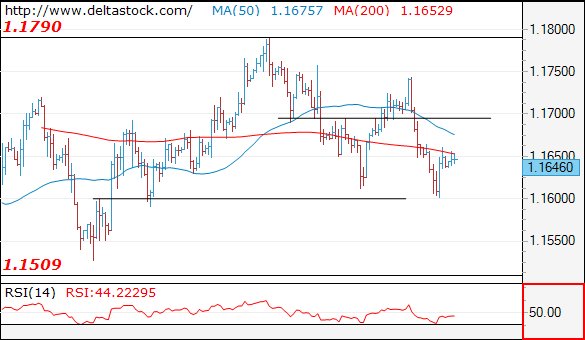

EUR/USD

Current level - 1.1646

The rebound above 1.1600 is corrective in nature, thus preceding a slide towards 1.1510. Key resistance lies at 1.1700.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1700 | 1.1750 | 1.1600 | 1.1510 |

| 1.1700 | 1.1830 | 1.1510 | 1.1300 |

USD/JPY

Current level - 112.72

The outlook is positive above 112.60 static support, for a renewal of the upmove, towards 113.70 zone. Crucial on the downside is 112.17.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.70 | 114.50 | 112.60 | 111.40 |

| 114.50 | 114.50 | 112.17 | 109.30 |

GBP/USD

Current level - 1.3073

The rebound after 1.3010 is corrective and the resistance around 1.3100 should cap the upside, for another leg downwards, to 1.2920.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3100 | 1.3460 | 1.3010 | 1.3010 |

| 1.3190 | 1.3620 | 1.2920 | 1.2770 |

Sterling lower after retail sales miss, but loss is limited

Sterling suffers some selloff after worse than expected June retail sales data.

Retail sales including fuel dropped -0.5% mom, well below expectation of 0.2% mom growth. For the year, Sale including fuel rose 2.9% yoy, missing expectation of 3.7% yoy.

Retail sales excluding fuel dropped -0.5% mom, well below expectation of 0.2% mom growth. For the year, Sale excluding fuel rose 3.0% yoy, missing expectation of 3.5% yoy.

While the pound dips broadly after the release, selloff is not too serious. In particular, Australian Dollar reversed earlier gains and takes New Zealand Dollar lower with it.

ZAR Tumbles Ahead Of SARB Decision

SARB Rate Decision to stay on hold amid stronger USD

As the economy is giving signs of recovery, the South African Central Bank (SARB) is expected to maintain its Repo rate unchanged during today’s monetary policy meeting. Chairman of the Federal Reserve Jerome Powell positive views for the US economic growth outlook made in front of the United States Congress gave the greenback a strong boost at the expense of EM currencies.

Jerome Powell 2-days discussion confirmed that the US economy is growing at a faster pace than previously anticipated, while Q2 2018, despite escalating trade sanctions declarations among commercial partners, remained the strongest in the year, thus signaling that further monetary policy tightening would not be a problem for the economy. The address remained however vague for what concerns escalating trade conflict and its potential impact on Q3 GDP growth pace, in the case of full tariff implementation measures from all trade parties.

The announcement gave the dollar a strong boost against major peers and particularly against EM currencies. And the rally is certainly not going to come to an end for now. Since the South African economy is recovering from political tumult since Zuma resignation in February and starts regaining confidence, rumors concerning discord within the governing African National Congress party emerge, as pro-Zuma members are planning a fight-back strategy, thus causing further uncertainty issues in the country.

Due to positive economic data and particularly on the front of domestic consumption as well as manufacturing activities, the SARB is expected to give the economy some relief, maintaining its Repo rate at 6.50% (unchanged since 28. March 2018), despite continued rise in inflation data (CPI y/y +4.60%).

Currently trading at 13.3638, USD/ZAR is expected to strengthen after the SARB announcement, approaching the 13.50 range.

BoE Hike Still Priced in Despite More Disappointing UK Data

- GBP bounces back after data driven selling;

- Traders still convinced of rate hike despite week of bad releases;

- US earnings, data and Fed speakers eyed.

European markets are trading in the red early in the session on Thursday, with the FTSE 100 the only major index in the green, supported by weakness in the pound after the release of some more disappointing data for the UK.

The UK retail sales data this morning may have dealt another major blow to the Bank of England’s hopes of raising interest rates in August, bringing an end to what has likely been a very frustrating week for policy makers. In recent weeks it has appeared that the Monetary Policy Committee had once again come around to the idea that raising interest rates in August is appropriate after plans in May were derailed by a frustratingly weak first quarter, something policy makers appeared to have correctly assumed would prove to be a temporary lull.

The data this week may have thrown another spanner in the works, with labour market figures showing a tight labour market by uninspiring wage growth, core inflation falling below 2% and now modest retail sales growth in what was expected to be a stellar month. This is clearly not the platform policy makers were hoping for when preparing investors for a rate hike but they may still seize the opportunity before it’s taken away from them for a prolonged period.

There may well be a strong feeling in the MPC that the central bank should have pushed ahead with a hike in May and stood by its belief that weather had a negative but temporary impact on the economy which would have given it the freedom to be patient through the rest of the year. Instead, it now finds itself in a position were the most recent data hasn’t been great and Brexit talks are not progressing as hoped, meaning it would make far more sense to hold off until November, something that would likely result in another backlash against the policy of forward guidance.

While holding off would make sense, there is clearly a view in the markets that this will not happen and the central bank may stick to plans to hike in two weeks. Despite numerous setbacks this week, a hike is still currently 68% priced in and after initial selling, the pound is showing some resilience and holding above 1.30 against the dollar. It seems traders are awaiting any hint from the BoE that plans have been put on hold again, at which point the resilience will likely break and possibly aggressively.

Over in the US, futures are tracking the majority of Europe lower, with the major indices currently seen opening around a tenth of one percent lower. This comes after Federal Reserve Chair Jerome Powell once again gave an upbeat assessment of the economy on Wednesday, in his appearance in front of the House Financial Services Committee. With the Fed on a quite clear and consistent course on interest rates, there wasn’t a huge amount learned in either appearance that we already didn’t know.

Today it’s looking a little quiet for the US. There are a couple of pieces of data that traders will be looking out for ahead of the open – Philly Fed manufacturing index and jobless claims – and we’ll also hear from Powell’s colleague at the Fed, Randal Quarles. With the season now up and running, there’ll also be a big focus on US earnings with 21 companies reporting including Microsoft and BNY Mellon.

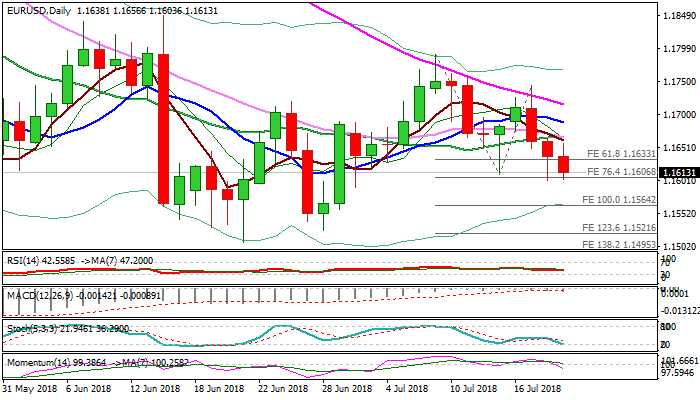

EURUSD Outlook: Fresh Weakness From Recovery Tops Turns N/T Focus Lower

The Euro holds in red for the third straight day and pressures again Wednesday's spike low at 1.1601, after recovery attempts from here ran out of steam at 1.1660 and left hourly double-top before falling back. Fresh weakness nearly fully retraced 1.1601/60 correction, signaling continuation of bear-phase from 1.1790 high. The pair is currently riding on the third wave of five-wave cycle from 1.1790 and eyeing target at 1.1564 (FE100%) to confirm wave principles. Weakness from double-rejection at the base of thick daily cloud could extend towards key supports at 1.1527 (28 June trough) and 1.1508 (21 June low). Fresh bearish momentum is building and adding to negative daily techs. Converged 20/30SMA's mark solid resistance at 1.1660 zone, which is expected to keep the downside protected.

Res: 1.1665, 1.1678, 1.1696, 1.1729

Sup: 1.1601, 1.1564, 1.1527, 1.1508