Sample Category Title

Canadian Dollar Slides on Soft Employment Report

The Canadian dollar has posted considerable losses in the Thursday session. Currently, USD/CAD is trading at 1.3266, up 0.73% on the day. On the release front, Canadian ADP Nonfarm Employment Change plunged, posting a reading of -10.5 thousand. This was the first decline of 2018. In the U.S, manufacturing and employment data were better than expected. The Philly Fed Manufacturing Index climbed to 25.7, easily beating the estimate of 21.6 points. Unemployment claims dropped to 207 thousand, better than the estimate of 220 thousand. On Friday, the focus is on consumer indicators. CPI is expected to remain pegged at 0.1%, while retail sales are expected at 0.6%, which would be the first gain in 2018. Traders should be prepared for movement from the Canadian dollar in the North American session.

The tariff slugfest between the U.S and its major trading partners has raised serious concerns not just with investors, but with Federal Reserve policymakers as well. The Federal Reserve Beige Book for July, released on Wednesday, was rife with references to ‘tariffs’. This trend started in the April Beige Books after President Trump threatened in March to impose tariffs on China. Most of the twelve Fed regional districts referred to tariffs in their individual reports, which make up the Beige Book. Some Fed policymakers have also voiced their concern over the impact that tariffs could have on the U.S economy and is an issue the Fed will have to take into consideration, as it mulls over rate policy for the next six months.

With trade tensions hovering, investors are keeping a close eye on the Canadian manufacturing sector. There was excellent news earlier in the week, as Manufacturing Sales in May rebounded with a gain of 1.4%, after a 1.3% decline a month earlier. Last week, the Bank of Canada raised rates by a quarter-point last week, to 1.50%. This is the highest level since December 2008. Will we see more rate hikes in 2018, as will likely be the case in the U.S? The BoC rate statement said that “higher rates will be needed” in order to keep inflation close to the target of 2 percent. Policymakers are keeping a close eye on the simmering trade war, which has seen Canada and the U.S impose tariffs on each other’s products. If the Canadian economy can escape the trade war relatively unscathed, we could see another rate hike at the BoE policy meeting in September.

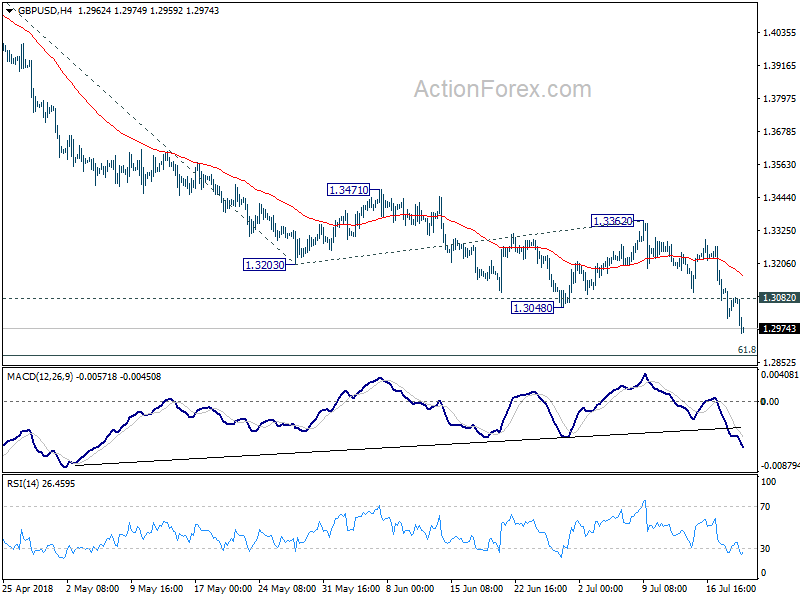

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3009; (P) 1.3072; (R1) 1.3135; More...

GBP/USD's decline continues to as low as 1.2956 so far. Intraday bias stays on the downside for 1.2874 fibonacci level first. Sustained break there will carry larger bearish implications. In that case, next near term target is 61.8% projection of 1.4376 to 1.3203 from 1.3362 at 1.2637. On the upside, above 1.3082 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 1.3362 resistance to bring fall resumption.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

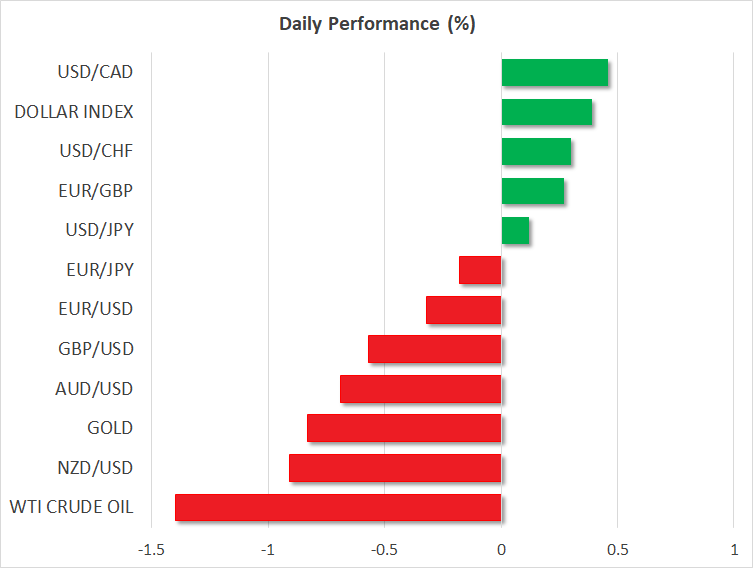

Dollar Surges as Trade War Takes Back the Stage, Pushed Further by Stellar Job Data

Dollar is trading as the strongest one today as trade spat intensifies again. For whatever reasons, the greenback has been supported by intensifying trade tension between US and other countries. Further buying is seen in Dollar in early US session after another set of stellar job data. Meanwhile Japanese Yen is trading as the second strongest as risk aversion is coming back. On the other hand, Australian dollar reversed earlier job data triggered against, on risk aversion, and follows New Zealand Dollar as the second weakest. Sterling suffered more selling today after UK retail sales miss.

Technically, GBP/USD drops through 1.3 handle and it's on track to 1.2874 fibonacci level in near term. USD/JPY breached 113.13 as recent rally resume but momentum is a bit unconvincing. EUR/USD is having downside bias for 1.1507 low but it's still, relatively resilient. A focus now is whether AUD/USD will drop through 0.7309 low to resume larger down trend. Gold is on track to 1200 psychological as selloff accelerates, and could hit the level before within this week.

Dollar rally extends as initial jobless claims dropped to lowest since 1969

Dollar rally extends in US session after another set of stellar job data. Initial jobless claims dropped -8k to 207k in the week ended July 14, beating expectation of 221k. That's also the lowest level since December 6, 1969. The four-week moving average of initial claims dropped -2.75k to 220.5k. Continuing claims rose 8k to 1.751m in the week ended July 7. Four-week moving average of continuing claims rose 6.25k to 1.736m. Also from the US, Philly Fed business outlook rose sharply to 25.7 in October, well above expectation of 20.6.

China: US officials have turned black and white and reversed it

Dollar rises broadly today as trade spat between US and China heated up again. It's started yesterday when Trump's economic advisor Larry Kudlow blamed Chinese President Xi Jinping for for holding back the trade deal with the US. The timing of such accusation is a bit odd, sounding like it's out of nothing. Nevertheless, it doesn't occupy a lot of air time except that such comments triggered some nerves of Chinese government officials. For the Americans, their focuses seem to be staying on the Trump's summit with Putin.

Anyway, Chinese Foreign Ministry Hua Chunying said in a regular press briefing today that Kudlow "unexpectedly distorted the facts and made bogus accusations is shocking and beyond imagination." And, "the United States' flip-flopping and promise-breaking is recognized globally." And, "in the face of people all over the world, it is shocking that the relevant US officials have turned black and white and reversed it." She added that "the US behavior can only seriously damage its own reputation once again, and it is completely unhelpful to solve the problem." Hua also reiterated China's position that "do not want to fight, not afraid to fight."

EU Malmstrom preparing a list of rebalancing measures for US auto tariffs

EU Trade Commissioner Cecilia Malmstrom said today that while she hoped Commission President Jean-Claude Juncker's visit to the US on July 25 could ease trade tensions, the EU is prepared for retaliation. She said that "if the U.S. would impose these car tariffs that would be very unfortunate. We are preparing together with our member states a list of rebalancing measures there as well. And this we have made that clear to our American partners." And she added that "it is done in the same way as with steel and aluminum."

Also, regarding Juncker's visit, she said it's to "try to establish a good relations, try to see how we can de-escalate the situation, avoiding it going further and see if there is a forum where we can discuss these issues." She added that "we don't go there to negotiate anything."

Juncker himself said he's "upbeat and related" ahead of the trip to Washington. He also emphasized that "we will continue to react tit-for-tat to the provocations that might be thrown at us." And, "when it comes to trade, the European Union, its internal market, its single market, form an indivisible unity and it's the Commission that is in charge of articulating trade policy. All efforts to divide the European Union are in vain."

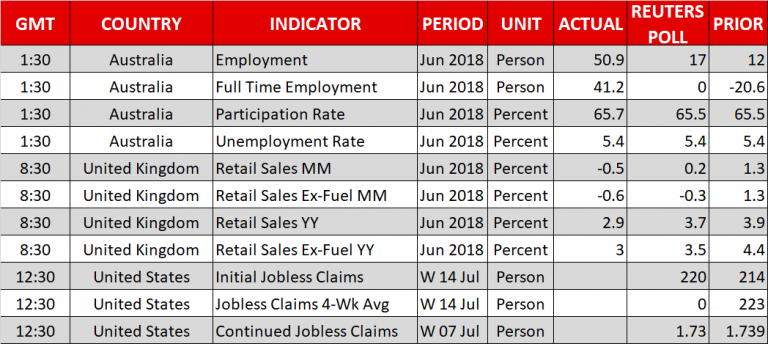

Sterling falls after worse than expected June retail sales data

Retail sales including fuel dropped -0.5% mom, well below expectation of 0.2% mom growth. For the year, Sale including fuel rose 2.9% yoy, missing expectation of 3.7% yoy. Retail sales excluding fuel dropped -0.5% mom, well below expectation of 0.2% mom growth. For the year, Sale excluding fuel rose 3.0% yoy, missing expectation of 3.5% yoy.

While the UK delivered a string of weaker than expected data this week, markets are still firm on expectation of an August BoE hike. Overall, Q2 was still a solid quarter. However, BoE policymakers will still have PMIs to watch in around two weeks time. That could give more insight on whether the momentum in Q2 is being carried forward to Q3.

Australian Dollar jumped on strong job data but reversed on risk aversion

Australian Dollar surges broadly as June employment data came in strong on all front. However, the Aussie reversed as dragged down by risk aversion. Headline job grow jumped to 50.9k seasonally adjusted , well above expectation of 16.6k. Prior month's figure was also revised slightly up by 12k to 13.5k. Full time jobs grew 41.2k while part time jobs also rose 9.7k. Together with the surge in full time jobs, total hours worked rose 0.6%

Unemployment rate remained unchanged at 5.4%. But without rounding, it's actually the at its lowest since November 2012. Labor force participation rate rose 0.2% to 65.7%. Employment to population ratio also rose 0.2% to 62.1%.

Also from Australia, NAB Quarterly Business Confidence dropped to 7 in Q2.

Japan logged JPY 721.4B surplus in June, exports grew 19th straight month

Japan trade balanced turned back into surplus at JPY 721.4B in June, above expectation of JPY 534.2B. Total exports rose 6.7% yoy, slightly below expectation of 7.0% yoy. But imports rose just 2.5% yoy, below expectation of 5.3% yoy.

Total exports logged a 19th straight month of growth. Rising trade tension with the US is not having much realized impact so far. Exports to China rose 11.1% yoy, to EU rose 9.3% yoy. Meanwhile, exports to US dropped -0.9% yoy.

Japan is still facing impacts from US steel and aluminum tariffs and threats on auto tariffs. The the blockbuster trade deal with EU just signed earlier this week should provide enough optimism to offset those threats.

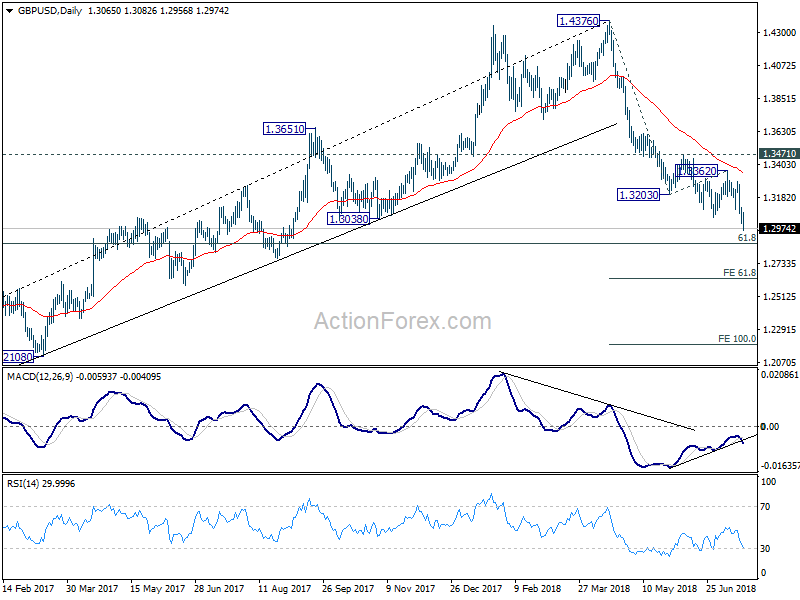

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3009; (P) 1.3072; (R1) 1.3135; More...

GBP/USD's decline continues to as low as 1.2956 so far. Intraday bias stays on the downside for 1.2874 fibonacci level first. Sustained break there will carry larger bearish implications. In that case, next near term target is 61.8% projection of 1.4376 to 1.3203 from 1.3362 at 1.2637. On the upside, above 1.3082 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 1.3362 resistance to bring fall resumption.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3471 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jun | 721.4B | 534.2B | -578.3B | -580.5B |

| 01:30 | AUD | NAB Business Confidence Q2 | 7 | 7 | 8 | |

| 01:30 | AUD | Employment Change Jun | 50.9K | 16.6K | 12.0K | 13.4K |

| 01:30 | AUD | Unemployment Rate Jun | 5.40% | 5.40% | 5.40% | |

| 06:00 | CHF | Trade Balance (CHF) M/M Jun | 2.59B | 3.22B | 2.76B | 2.81B |

| 08:30 | GBP | Retail Sales M/M Jun | -0.50% | 0.20% | 1.30% | |

| 12:30 | USD | Initial Jobless Claims (JUL 14) | 207K | 221K | 214K | 215K |

| 12:30 | USD | Philadelphia Fed Business Outlook Jul | 25.7 | 20.6 | 19.9 | |

| 14:00 | USD | Leading Index Jun | 0.50% | 0.20% | ||

| 14:30 | USD | Natural Gas Storage | 51B |

GBPUSD Outlook: Cable Slides Below 1.30 Handle after Downbeat Data; Fibo Support at 1.2865 is Coming in Focus

Cable trades below 1.30 handle ahead of start of the US session on Thursday, following fresh bearish acceleration on downbeat UK retail sales data, released earlier today.

Retail sales fell well below expectations in June (m/m -0.5% vs 0.1% and upward-revised May figure at 1.4%, while core retail sales m/m came at -0.6%, falling below -0.3% f/c and 1.4% previous).

Weak data further soured negative sentiment, already hit by poor labor data on Tuesday and downbeat UK inflation data on Wednesday.

The pair is in steep descend which extends into third consecutive day, with strong bearish signal anticipated on final break and close below key supports at 1.3049/00 (28 June former low / psychological support).

Bears now eye targets at 1.2929 (Fibo 138.2% projection) and 1.2905 (05 Sep 2017 low), with stronger acceleration lower, expected to attack next pivotal support at 1.2865 (Fibo 61.8% of 1.1930/1.4376, 2016/2018 uptrend).

Caution on oversold daily studies which warn of corrective action in coming sessions.

Broken supports at 1.3000/49 are now reverted to resistances, which should ideally keep the upside protected.

Res: 1.3083; 1.3118; 1.3136; 1.3189

Sup: 1.3009; 1.3000; 1.2905; 1.2865

Dollar rally extends as initial jobless claims dropped to lowest since 1969

Dollar rally extends in US session after another set of stellar job data. Initial jobless claims dropped -8k to 207k in the week ended July 14, beating expectation of 221k. That's also the lowest level since December 6, 1969. The four-week moving average of initial claims dropped -2.75k to 220.5k.

Continuing claims rose 8k to 1.751m in the week ended July 7. Four-week moving average of continuing claims rose 6.25k to 1.736m.

Also from the US, Philly Fed business outlook rose sharply to 25.7 in October, well above expectation of 20.6.

Sterling Plunges to Fresh 10-Month Lows after UK Retail Sales Disappoint

Here are the latest developments in global markets:

FOREX: Sterling tumbled by 0.69% against the greenback on Thursday, hitting a fresh 10-month low of 1.2970 in the wake of worse-than-expected retail sales figures out of the UK. Month-on-month retail sales dropped 0.5% in June from 1.4% in May, missing market expectations of a 0.2% gain. On a yearly basis, the index increased 2.9% versus 3.7% expected and May’s mark of 4.1%. Yet, the report revealed that quarter-on-quarter retail sales growth was the strongest since Q1 2004. The dollar index versus six major currencies added 0.47% to its performance, registering a one-year high of 95.55. An upside movement was seen in dollar/yen on Thursday as well, with the pair trading higher by 0.12%, surpassing the 113.00 handle again. On the other hand, euro/dollar was down by 0.27%, near the 1.1600 key level. In the antipodean sphere, aussie/dollar reversed earlier gains, edging sharply lower (-0.76%) to 0.7342, while kiwi/dollar plunged by 0.93% to 0.6730, paring the gains of the previous three days. Meanwhile, dollar/loonie rose by 0.50% to 1.3233.

STOCKS: European equities were trading mostly lower on Thursday with an exception the Euro STOXX 50 and the British FTSE 100 index , which advanced by 0.20% and 0.07% respectively at 1130 GMT. The pan-European Stoxx 600 dived by 0.13% with basic materials and utilities leading losses. The German DAX 30 and the Italian FTSE MIB were also moving down, by 0.45%, and 0.35% respectively. Also, the Spanish IBEX 35 declined by 0.35% and the French CAC 40 lost 0.51%. Futures on the Dow, S&P 500 and Nasdaq 100 traded higher yesterday and are pointing to a higher open today on Wall Street.

COMMODITIES: Oil prices dropped considerably today after an unexpected rise in US crude stockpiles yesterday. The report also showed that US output hit record highs at 11mn barrels per day. West Texas Intermediate (WTI) crude oil plummeted by 1.25% near $68 per barrel, erasing some of Wednesday’s gains. In addition, London-based Brent plunged by 1.32% to around $72. In precious metals, gold prices dropped by 0.83% to $1,216.2 per ounce, silver dipped by 1.82%, while copper tumbled by 3%, all of them recording new 1-year lows.

Day ahead: US Philly Fed Manufacturing index pending; Japan reports on inflation

Data releases will be relatively light in the remainder of the day, with Philadelphia’s Fed Manufacturing Index being a key delivery investors will pay attention to confirm the Fed’s chief recent upbeat assessment on the US economy. Trade headlines will be in focus as well, as the US keeps the pressure on China and the EU with scope to persuade its allies to soften their trade restrictions on US products.

Following Jerome Powell’s two-day testimony on Wednesday and Thursday, in which the Fed chief highlighted that the US economy could bear higher interest rates this year and trade risks will not keep the central bank from proceeding accordingly, the Federal Reserve Bank of Philadelphia is scheduled to publish its manufacturing index at 1230 GMT, adding further evidence on the country’s economic performance. According to forecasts, the index compiled by a survey from 250 manufacturers in the Philadelphia district, has bounced from 19.9 to 21.5 in July, remaining near the average of the past two years; a sign that the industry is growing at a healthy pace – as long as the measure holds above zero. In the event of an upward surprise, the dollar could expand well into the 113 handle and even reach fresh peaks. Initial jobless claims for the week ending July 14 will be out at the same time, although the greenback has shown little reaction to the data in the past few months.

In the trade front, the tariff turmoil continues to weigh in the background, maintaining some degree of risk-off sentiment in the markets. Yesterday the White House National Economic Council Director, Larry Kudlow, blamed China for stalled trade talks, with China’s foreign ministry saying today that it doesn’t want a trade war but it’s not afraid of one, pointing its finger to the US instead. Regarding relations with Mexico, Kudlow characterized negotiations as a “promising avenue”, a week after the US Secretary of State Michael Pompeo, traveled to Mexico to meet with both Mexico’s current administration and incoming president.

Elsewhere, Japan will see inflation readings early in the Asian session at 2330 GMT, with forecasts being for a slight pickup in consumer prices. Particularly, analysts expect the nationwide core CPI to inch up by 0.1 percentage points in June to 0.8%, remaining far below the BoJ’s 2% price target.

As for today’s public appearances, a meeting between the Russian Energy Minister Alexander Novak and Chinese officials in China to discuss energy cooperation could attract some interest, while in Buenos Aires in Argentina, the ECB Executive member, Benoit Coeure will be participating at the G20 finance ministers and central bank governors and deputies meeting, which will conclude on July 22.

In equity markets, the earnings season continues with Microsoft Corporation being among companies to release quarterly results after the market close.

Into US sesson: Dollar strong again while Gold hits 1215

Entering into US session, Dollar is trading as the strongest one as US-World trade war comes back to spotlight. Yen follows as the second strongest as major global equities lose ground, except UK. Australian Dollar reversed job data inspired gains and is trading as the second weakest, following New Zealand Dollar, on risk aversion. Sterling is the third weakest after retail sales disappointment. Also, not that the China Yuan is also extending recent decline on trade tension, with USD/CNH (Chinese Yuan offshore) hitting one year high.

In other markets, Nikkei closed slightly down by -0.13% today, Hong Kong HSI closed down -0.38%. China Shanghai SSE composite closed down -0.53% at 2772.55. At the time of writing, DAX and CA are down -0.43% and -0.49% respectively. FTSE is support by selloff in the British Pound and is up 0.16%. WTI crude oil is stabilizing above 68, at 68.2 now.

Spot gold drops through 1220 handle to as low as 1215 so far. It's on course for 1205.02 support as near term target. But in the end, we'd expect at least a take on 61.8% retracement of 1046.54 to 1375.15 at 1172.06 at least.

UK Data Continues To Disappoint

Notes/Observations

- UK Retail sales disappoints and further erodes BOE Aug rate hike hopes

- China officials seek to avoid a trade war but stress it is not afraid of one

Asia:

- Japan Jun Trade Balance saw Exports to US register its 1st decline in 17 months (¥0.7B v ¥0.5Be

- Australia Jun Employment Change: +50.9K v 16.5Ke (21st month of gains); Unemployment Rate: 5.4% v 5.4% prior

- China FX Regulator SAFE Spokesman Wang Chunying: China US rate differential was not vital in affecting capital flows. Cross border flows to be impacted by the China/US interest rate spread. Reiterated forex reserves were ample and able to cope with challenges.

- BoJ daily bond buying operation saw its cut its buying of 10-25 year and over 25-yr JGBs maturities (Note: In the past, BoJ officials have stated that daily bond buying operations were not intended to signal monetary policy changes)

Europe:

- EU said to be preparing 'rebalancing measures' in case automobile tariffs go into effect

- EU’s Moscovici: An escalation in trade tensions, no matter from which side, would have serious consequences for the economy, including for financial markets

- Swiss Fin Min Maurer reiterated govt stance that CHF currency (Franc) remained overvalued against the euro, but we can live with this Americas

- Fed Beige Book: Economic activity rose moderately to modestly in 10 of 12 districts. Manufacturers in all Districts expressed concern about tariffs and in many Districts reported higher prices and supply disruptions that they attributed to the new trade policies

- Fed Chair Powell Congress testimony: reduction of Fed balance sheet to take 3 or 4 years; goal is to return it to mostly Treasury holdings. Inflation risks were now roughly balanced, though I'm slightly more worried about lower inflation

- Mexico Econ Min Guajardo: moving from NAFTA to bilateral talks would be difficult, like starting from zero; still wanted a 3-party NAFTA deal

- President Trump and his economic advisor Kudlow both stated they were making progress in talks with Mexico and that it might be easier to do a trade deal with Mexico and then later with Canada

Energy:

- OPEC/Non-Opec compliance declined to 120% in June, down from 147% in May

- OPEC said to be considering options to defend against US effort to push anti-cartel law - press

Economic Data:

- (NL) Netherlands Jun Unemployment Rate: 3.9% v 3.8%e

- (CH) Swiss Apr Trade Balance (CHF): 2.6B v 2.8B prior; Real Exports M/M: 0.5% v 0.3% prior; Real Imports M/M: -0.4% v +4.0% prior

- (CZ) Czech May Export Price Index Y/Y: -1.5% v -3.9% prior; Import Price Index Y/Y: -2.3% v -5.3% prior

- (CZ) Czech Jun PPI Industrial M/M: 0.6% v 0.4%e; Y/Y: 2.9% v 2.6%e

- (UK) Jun Retail Sales (Ex-Auto/Fuel) M/M: -0.6% v +0.1%e; Y/Y: 3.0% v 3.7%e

- (UK) Jun Retail Sales (including Auto/Fuel) M/M: -0.5% v 0.2%e; Y/Y: 2.9% v 3.5%e

- (HK) Hong Kong Jun Unemployment Rate: 2.8% v 2.8%e (matches lowest level since Jan 1998)

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €4.55B vs. €4.0-5.0B indicated range in 2023, 2026, 2028 and 2033 Bonds

- Sold €1.289B in 0.35% July 2023 SPGB; Avg yield: 0.313% v 0.336% prior; Bid-to-cover: 1.56x v 1.61x prior

- Sold €831M in 5.90% July 2026 SPGB; Avg Yield: 0.953% v 1.073% prior; Bid-to-cover: 1.40x v 1.94x prior

- Sold €1.337B in 1.40% Apr 2028 SPGB; Avg yield: 1.308% v 1.406% prior, Bid-to-cover: 1.47x v 2.19x prior

- Sold €1.089B in 2.35% July 2033 SPGB; Avg Yield: 1.798% v 1.830% prior; Bid-to-cover: 1.37x v 1.99x prior

- (FR) France Debt Agency (AFT) sold total €7.487B vs. €6.5-7.5B indicated range in 2021 and 2024 Oats

- Sold €3.291B in 0.0% Feb 2021 Oat; Avg Yield: -0.44% v -0.46% prior; Bid-to-cover: 2.40x v 3.25x prior

- Sold €4.196B in 0.0% Mar 2024 Oat; Avg Yield: 0.01% v 0.03% prior; Bid-to-cover: 1.95x v 1.97x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 386.5, FTSE +0.2% at 7689, DAX -0.4% at 12716, CAC-40 -0.4% at 5425, IBEX-35 -0.1% at 9743, FTSE MIB -0.2% at 21,929, SMI +0.2% at 8951, S&P 500 Futures -0.2%]

- Market Focal Points/Key Themes: European Indices trade mostly lower across the board led by the French CAC and German Dax. The FTSE outperforms on the continued weakness in Cable which dipped below $1.30 at fresh 10 month lows. Corporate earnings was the dominant theme with Publicis a notable decliner after missing estimates, Babcock, Dorma and Kaba, Sports Direct and Wartsila among other names declining sharply following results. SAP reported a beat on Revs and raised outlook, but a slight miss on EPS sees the shares trade lower. To the upside, Volvo outperforms after strong results, with ABB and Alstom other notable names rising. Looking ahead to the US morning key earnings include Travelers, BNY, Keycorp, Danaher and Philip Morris among others.

Movers

- Consumer Discretionary Sports Direct [SPD.UK] -7.4% (Earnings), Publicis [PUB.FR] -7.5% (Earnings) -Healthcare

- Morphosys [MOR.DE]+3.6%, Galapagos [GLPG.BE]+2.3% ( sign global license agreement for MOR106 with Novartis; To receive €95M up front payment)

- Technology SAP [SAP.DE] -1% (Earnings)

- Industrials Dorma+Kaba [DOKA.CH] -15% (Earnings), ABB [ABBN.CH] +5% (Earnings), Babcock [BAB.UK] -9% (Earnings), Wartsila [WRT1V.FI] -7% (Earnings)

- Materials Anglo American [AAL.UK] -1.5% (Earnings)

Speakers

- UK Brexit Min Raab reiterated stance that govt needed to prepare for all eventualities in Brexit and must intensify the negotiations. To set out details of the no-deal plan shortly. Banks were confident that they could withstand all outcomes

- EU official stated that UK White paper was a starting point, it was detailed yet unclear. EU will not produce an official response to UK White Paper

- EU Trade Min Malmstrom confirmed that the EU was preparing a list of rebalancing measures if US imposed auto tariffs

- Poland Central Bank Zubelewicz: Rate hike was likely when core CPI was over 2%. Believed that a weaker PLN currency (Zloty) spook against extending MPC’s 'wait-and-see' mode. Core inflation forecast should not exceed 1.5% and it’s July forecast was worrisome and had more central bankers talking of a rate hike

- Poland Central Bank's Garner saw the potential of a rate hike in early 2019/ Tightening cycle could see 50bps in rate increases

- Russia Central Bank: July CPI seen between 2.4-2.6% (**Note: Russia has 4.0% inflation target)

- Indonesia Central bank Policy Statement noted that its policy stance remained hawkish and was in-line with effort to boost attractiveness. To monitor both domestic and global economic developments and improve the use of hedging to maintain IDR currency (Rupiah) stability

- China Foreign Ministry spokesperson Hua Chunying reiterated stance that does not want a trade war but not afraid of one. Had made the utmost in effort to avoid escalation of trade frictions. US accusations that China was stalling trade talks is groundless

- China Commerce Ministry (MOFCOM): China forced to take countermeasures on $200B tariff. Reiterated view that was confident to address all external shocks

Currencies

- USD maintained a firm tone in the session again.

- EUR/USD continued to hold within the July trading range of 1.16-1.17 area

- GBP/USD posted fresh 10-month lows under the 1.30 handle as the currency has been weighed down by back of a mix of weaker-than-expected UK data and UK political uncertainties. UK Retail sales disappointed and further eroded BOE Aug rate hike hopes Dealers noted that the likelihood of intensified Brexit-related political turmoil in the autumn was one reason why the BOE might still raise interest rates in August rather than November. Dealers noted of a 1.30 option that was poised to expire on Thursday.

Fixed Income

- Bund Futures trade 3 ticks higher at 162.85 as payers embrace Bund weakness and deal positioning. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.67 higher by 1 tick as UK retail sales comes in softer than expected. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Thursday's liquidity report showed Wedenesday's excess liquidity fell from €1.849T to €1.824T. Use of the marginal lending facility dropped from €45M to €50M.

- Corporate issuance saw the brace of bank deals keep the primary market active

Looking Ahead

- (AR) G20 Finance Ministers begin multi-day meeting in Argentina

- UK Brexit Sec Rabb and EU’s Barnier press conference on latest round of negotiations

- (BR) Brazil July CNI Industrial Confidence: No est v 49.6 prior

- (PT) Portugal May Current Account: No est v -€0.3B prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

- 05:30 (UK) DMO to sell £2.0B in 1.75% July 2057 Gilts

- 05:50 (FR) France Debt Agency (AFT) to sell €1.25-1.75B in I/L 2025, 2030 and 2047 Bonds (Oatei)

- 06:00 (IE) Ireland Q1 Current Account: No est v €14.9B prior

- 06:00 (IE) Ireland Q1 GDP Q/Q: 0.7%e v 3.2% prior; Y/Y: 5.7%e v 8.4% prior

- 06:45 (US) Daily Libor Fixing

- 07:30 (TR) Turkey Jun Central Bank TCMB Survey of Expectations

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) July Philadelphia Fed Business Outlook: 21.5e v 19.9 prior

- 08:30 (US) Initial Jobless Claims: 220Ke v 214K prior; Continuing Claims: 1.73Me v 1.739M prior

- 08:30 (CA) Canada Jun ADP Payrolls Report: No est v 2.9K prior

- 08:30 (CL) Chile Central Bank Traders Survey

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (RU) Russia Gold and Forex Reserve w/e July 13th: No est v $459.6B prior

- 09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to keep Interest Rates unchanged at 6.50%

- 09:00 (US) Fed's Quarles (hawk, FOMC voter) on alternative reference rates

- 10:00 (US) Jun Leading Index: 0.4%e v 0.2% prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (CO) Colombia May Trade Balance: -$0.2e v -$0.3B prior; Total Imports: $4.3Be v $4.2B prior

- 11:00 (US) Treasury announcement for upcoming 2-year, 5-year and 7-year note auctions

- 13:00 (US) Treasury to sell $13B in 10-Year TIPS Reopening

- 19:30 (JP) Japan Jun National CPI Y/Y: 0.8%e v 0.7% prior; CPI Ex Fresh Food (core) Y/Y: 0.8%e v 0.7% prior, CPI Ex Fresh Food, Energy (core-core) Y/Y: 0.4%e v 0.3% prior

China Market Monitor: Unabated Weakening Of The CNY

The CNY continues to weaken against the USD. We see a clear risk of further depreciation and continue to recommend a hedging of receivables.

USD/CNY fixing by PBoC also creeping higher. However, this is mostly a reflection of market moves rather than a deliberate attempt to weaken the currency. Indeed, the USD/CNY is fixed stronger than yesterday’s closing level, which suggests the People’s Bank of China (PBoC) aims to dampen the depreciation as part of the ‘countercyclical factor’ of the fixing. CNH money market rates have been stable, however, which indicates the PBoC is not making any strong attempt to stop the CNY weakening, as it is increasingly allowing the markets to determine the currency as long as it does not risk causing instability. CNY weakness is a natural response to monetary policy easing.

Chinese stocks, bond yields and metal prices continue to decline

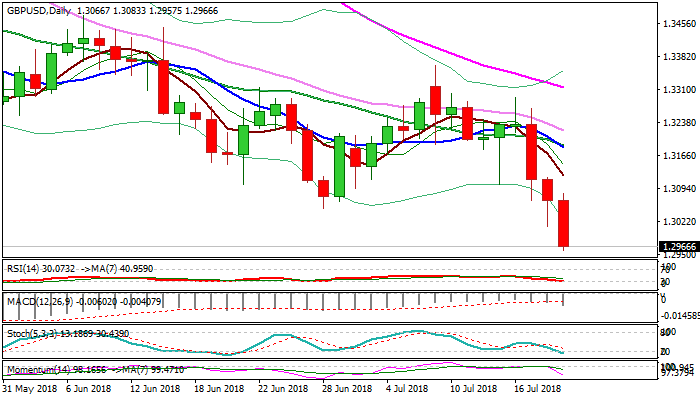

GBPUSD Under Pressure Below 1.3030 Level

The British pound has fallen to yet another 2018 trading-low against the US dollar this morning after United Kingdom Retail Sales turned negative for the month of June. The GBPUSD pair briefly traded below the 1.3000 level, finding support just before the 1.2980 level. Sellers will look for further losses below the 1.2980 level, while buyers will look to move the price back above the 1.3030 resistance level.

The GBPUSD pair is strongly bearish while trading under the 1.3030 level, key technical support is found at the 1.2980 and 1.2940 levels.

If the GBPUSD pair moves above the 1.3030 level, buyers will likely target the 1.3050 and 1.3082 resistance levels.