Sample Category Title

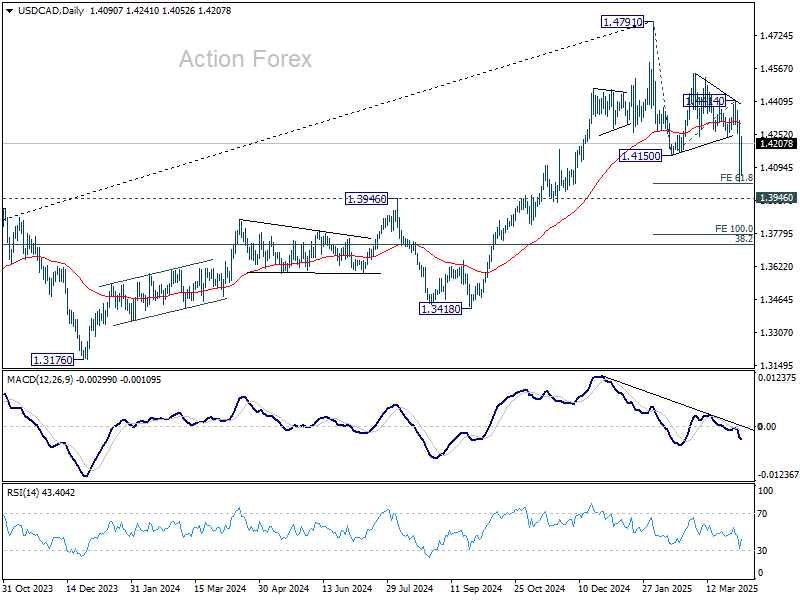

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3978; (P) 1.4148; (R1) 1.4269; More...

USD/CAD rebounded ahead of 61.8% projection of 1.4791 to 1.4150 from 1.4414 at 1.4018, and intraday bias is turned neutral. For now, risk will remain on the downside as long as 1.4414 resistance holds. Break of 1.4026 will target 1.3946 key support next. Nevertheless, break of 1.4414 will indicate that fall from 1.4791 has completed as a correction only.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.3986). Sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

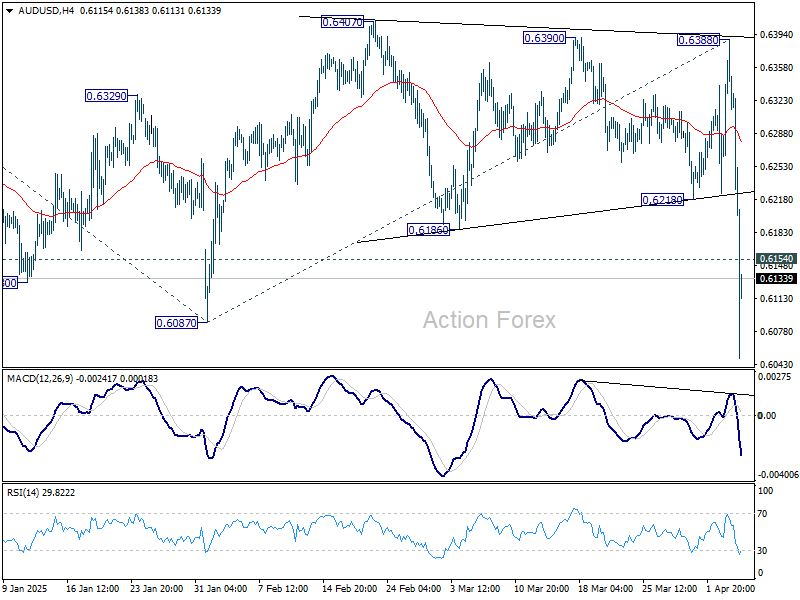

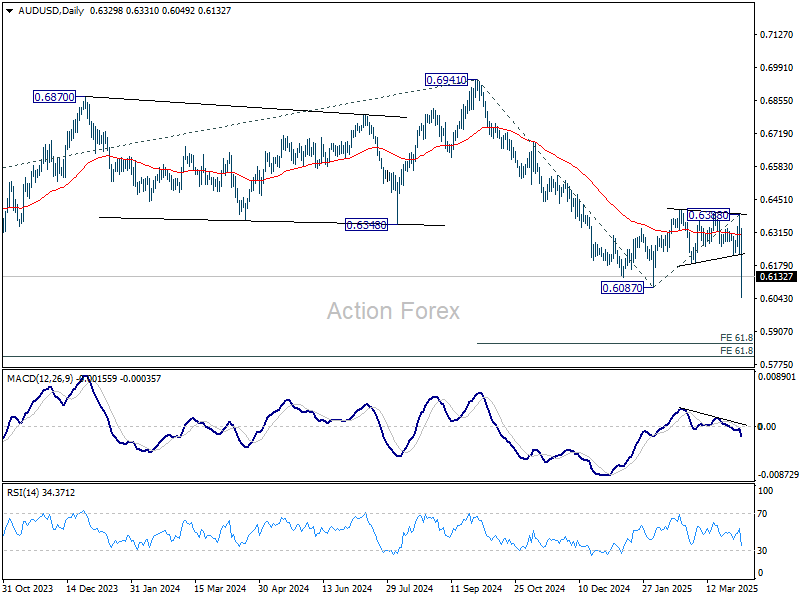

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6240; (P) 0.6315; (R1) 0.6403; More...

AUD/USD's steep decline today and breach of 0.6087 support indicates resumption of whole fall from 0.6941. Intraday bias is back on the downside. Next target is 61.8% projection of 0.6941 to 0.6087 from 0.6388 at 0.5860. On the upside, above 0.6154 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.

China Retaliates, Risk Sentiment Collapses as Market Turmoil Deepens

Risk aversion deepened across global markets today as China unveiled a forceful response to the sweeping US tariffs announced earlier this week. Beijing will impose an additional 34% tariff on all US goods starting April 10, in a move that effectively escalates the trade war into a full-scale economic confrontation. China sent the signal that it's prepared to endure economic pain to counter US pressure. The Chinese Commerce Ministry justified the decision on grounds of national security and international obligations, but the timing and scope leave no doubt it’s a retaliatory measure.

US stock futures plunged in response, with DOW pointing to another 1000-point drop at the open. Wall Street’s mood was already fragile after a volatile week driven by tariff headlines, and the market’s inability to find relief even after a much stronger-than-expected non-farm payrolls report highlights the depth of the panic. Traders are rushing into US Treasuries, pushing the 10-year yield below the key 3.9% level, a sign of rising demand for safe havens amid intensifying uncertainty.

In the currency markets, Aussie has taken the hardest hit, tumbling sharply after China’s retaliation was announced. Kiwi followed as the second-worst performer. Loonie also weakened notably after domestic employment data showed a surprise job loss in March, though it remains a distant third among the day’s laggards.

On the flip side, Swiss Franc extended its stellar run to lead the pack again today. Yen is also well supported, though not quite matching the Franc’s gains. Euro remains relatively firm, continuing to draw strength as a liquid alternative to Dollar amid global uncertainty. Meanwhile, Sterling and Dollar are holding in the middle of the pack.

In Europe, at the time of writing, FTSE is down -3.50%. DAX is down -3.46%. CAC is down -3.22%. UK 10-year yield is down -0.092 at 4.439. Germany 10-year yield is down -0.145 at 2.511. Earlier in Asia, Nikkei fell -2.75%. Japan 10-year JGB yield fell -0.195 to 1.156. Singapore Strait Times fell -2.95%. Hong Kong and China were on holiday.

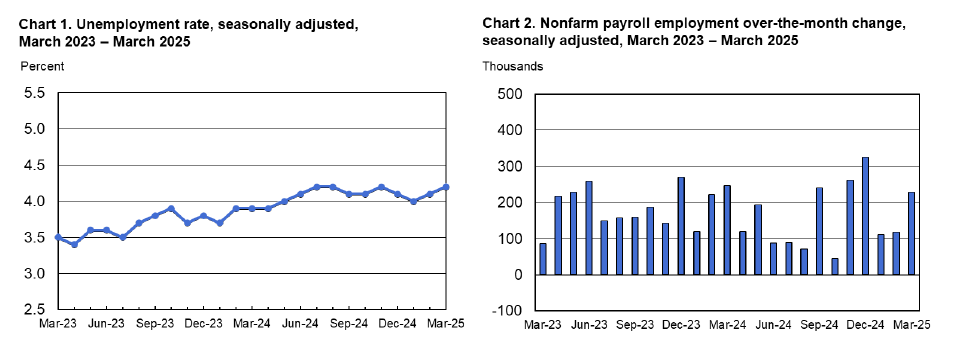

US NFP grows 228k, unemployment rate ticks up to 4.2%

US labor market showed unexpected strength in March, with non-farm payrolls rising by 228k, well above the consensus estimate of 128k. Growth was also notably stronger than the prior 12-month average of 158k.

The robust job gains highlight continued resilience in hiring, even amid heightened uncertainty surrounding trade policies and financial conditions.

Unemployment rate ticked up slightly from 4.1% to 4.2%, marking the upper end of its recent range, though the increase was accompanied by a modest uptick in labor force participation to 62.5%.

Average hourly earnings rose 0.3% month-over-month, aligning with expectations, suggesting that wage pressures remain steady.

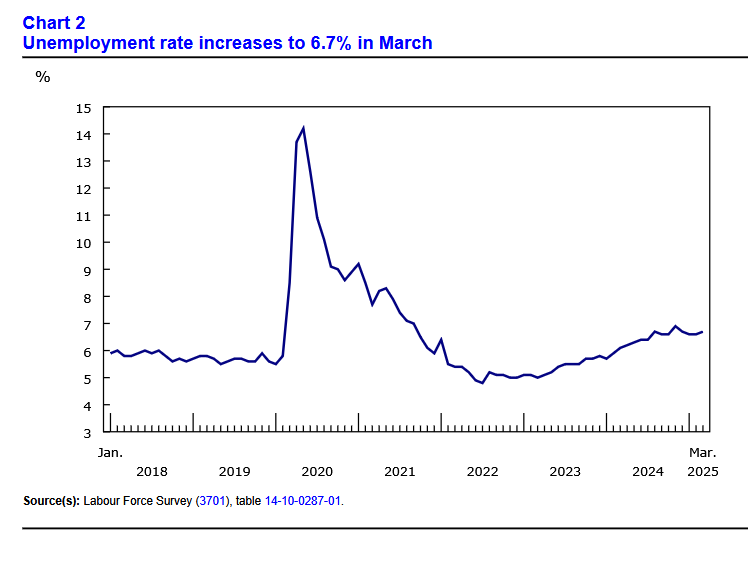

Canada posts surprise -32.6k job loss

Canada’s labor market delivered a sharp disappointment in March, with employment falling by -32.6k, well below expectations of a 10.4k gain.

This marked the first monthly job loss since January 2022 and was driven by a steep decline in full-time positions, which dropped by 62k. Employment rate dipped 0.2 percentage points to 60.9%.

The unemployment rate ticked up to 6.7%, in line with expectations. Wage growth slowed to 3.6% yoy from 3.8% yoy in February.

BoJ's Ueda: US tariffs likely to pressure Japan’s economy

BoJ Governor Kazuo Ueda warned that the 24% tariffs imposed by the US on Japanese goods could have broad implications. He emphasized that heightened uncertainty over the economic outlook may weigh on corporate sentiment and trigger volatile market behavior. This, in turn, could place "downward pressure on global and Japanese economies".

Meanwhile, Ueda noted that the effect on inflation remains uncertain, as the tariffs could either suppress prices by weakening demand or push them higher through supply chain disruptions.

Despite these concerns, Ueda maintained a cautiously optimistic view on Japan’s economy. He pointed out that corporate sentiment remains positive, and capital expenditure plans are stronger than in the same period of prior years.

He referred to the latest Tankan survey as supportive of BoJ's baseline view that Japan’s economy is "recovering moderately". Still, Ueda noted that the survey, conducted from late February to March 31, may not have fully captured the impact of the US tariff announcements.

BoJ Deputy Governor Shinichi Uchida, also speaking at the session, reiterated that the central bank remains committed to adjusting rates if the likelihood of achieving its 2% inflation target increases.

Uchida emphasized that future policy decisions will be made on a meeting-by-meeting basis, based on updated forecasts, "without any preconception".

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6240; (P) 0.6315; (R1) 0.6403; More...

AUD/USD's steep decline today and breach of 0.6087 support indicates resumption of whole fall from 0.6941. Intraday bias is back on the downside. Next target is 61.8% projection of 0.6941 to 0.6087 from 0.6388 at 0.5860. On the upside, above 0.6154 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.

Canada posts surprise -32.6k job loss

Canada’s labor market delivered a sharp disappointment in March, with employment falling by -32.6k, well below expectations of a 10.4k gain.

This marked the first monthly job loss since January 2022 and was driven by a steep decline in full-time positions, which dropped by 62k. Employment rate dipped 0.2 percentage points to 60.9%.

The unemployment rate ticked up to 6.7%, in line with expectations. Wage growth slowed to 3.6% yoy from 3.8% yoy in February.

US NFP grows 228k, unemployment rate ticks up to 4.2%

US labor market showed unexpected strength in March, with non-farm payrolls rising by 228k, well above the consensus estimate of 128k. Growth was also notably stronger than the prior 12-month average of 158k.

The robust job gains highlight continued resilience in hiring, even amid heightened uncertainty surrounding trade policies and financial conditions.

Unemployment rate ticked up slightly from 4.1% to 4.2%, marking the upper end of its recent range, though the increase was accompanied by a modest uptick in labor force participation to 62.5%.

Average hourly earnings rose 0.3% month-over-month, aligning with expectations, suggesting that wage pressures remain steady.

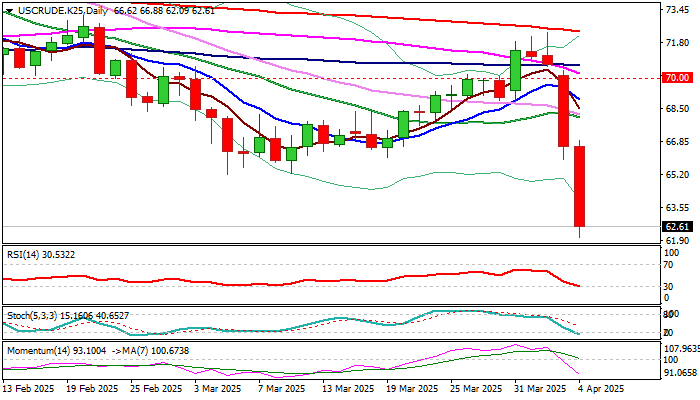

WTI Oil: Bears Hold Grip After Massive Losses in Past Two Days

WTI oil price remains in a steep fall for the second straight day and hits the lowest levels since December 2021 on Friday, after US tariffs rattled global markets and soured sentiment.

Unexpected decision of OPEC+ group to increase production above consensus from May, added to strong bearish outlook.

Oil prices fell around 11% in less than two days, on track for the worst week since the first week of October 2023.

Key longer-term supports at $62.42/$61.79 (lows of Dec/Aug 2021 that formed a higher base on monthly chart) are under increased pressure.

Firm break of these levels to signal further weakness with immediate target at $60.00 (psychological), loss of which to expose $53.87 (Fibo 61.8% of $6.52/$130.48 uptrend).

Bears show so far limited signs of fatigue despite recent massive losses, however oversold daily studies and Friday’s profit taking may keep bears on hold for some time.

According to current situation, upticks are likely to be limited and offer better levels to re-enter firmly bearish market.

Former base at $65.22/25 (Mar 5/11) act as resistance which should limit recovery action.

Res: 63.00; 64.49; 65.22; 65.98.

Sup: 62.00; 61.70; 60.86; 60.00.

Yen Pummels US Dollar, Nonfarm Payrolls Next

The Japanese yen has extended its gains on Friday. In the European session, USD/JPYis trading at 145.44, down 0.52% on the day. The yen is trading at its strongest level since September 2024.

US nonfarm payrolls expected to drop

Investors are still digesting the massive losses sustained in the financial markets, but will have to shift and focus on today's US nonfarm payrolls. The market estimate stands at 135 thousand, lower than the February gain of 151 thousand. The US labor market has been softening at a gradual pace and the Fed is hoping that trend continues.

Federal Reserve policymakers were looking at two rate cuts this year, but President Trump's bombshell tariff announcement will force the Fed to re-examine its growth and inflation forecasts.

What can we expect from the Fed?

That is no simple question, as the tariffs have sent the equity markets tumbling and deep uncertainty hangs in the air. The tariffs will boost inflation but also dampen growth, making for a tricky balance for the Fed. The money markets expect a slower US economy to dictate rate policy rather than inflation and that could mean as many as four cuts in 2025 if the economy tips into a recession.

Japan's household spending recovered in February with a gain of 3.5% m/m, after a 4.5% decline in January. This crushed the market estimate of 0.5% and was the strongest pace of growth since March 2022. The Bank of Japan is keeping a close eye on consumption as it determines when to raise interest rates and it is unclear how the new US tariffs will affect consumer confidence and spending.

WTI Oil Technical Outlook: Bears Gaining Strength for a Major Bearish Breakdown

- Global recession risk has triggered a significant drop in oil prices.

- WTI crude is now facing a negative double whammy from weak external demand and excess supplies built up.

- WTI crude is now breaching below a key major range support at US$65.40.

Since our last publication, the price actions of West Texas Oil CFD (a proxy of the WTI crude oil futures) have staged the expected corrective rebound sequence and rallied by 7.2% to print an intraday high of US$72.48/barrel on 2 April (a whisker below the US$73.50 medium-term resistance highlighted in our report) before the announcement of “US Liberation Day” reciprocal trade tariffs.

The West Texas Oil CFD has shaped a significant bearish reversal ex-post “US Liberation Day”, and plummeted by 6% on 3 April, its worst daily loss since early September 2022.

Headwinds from weak demand and excess supply

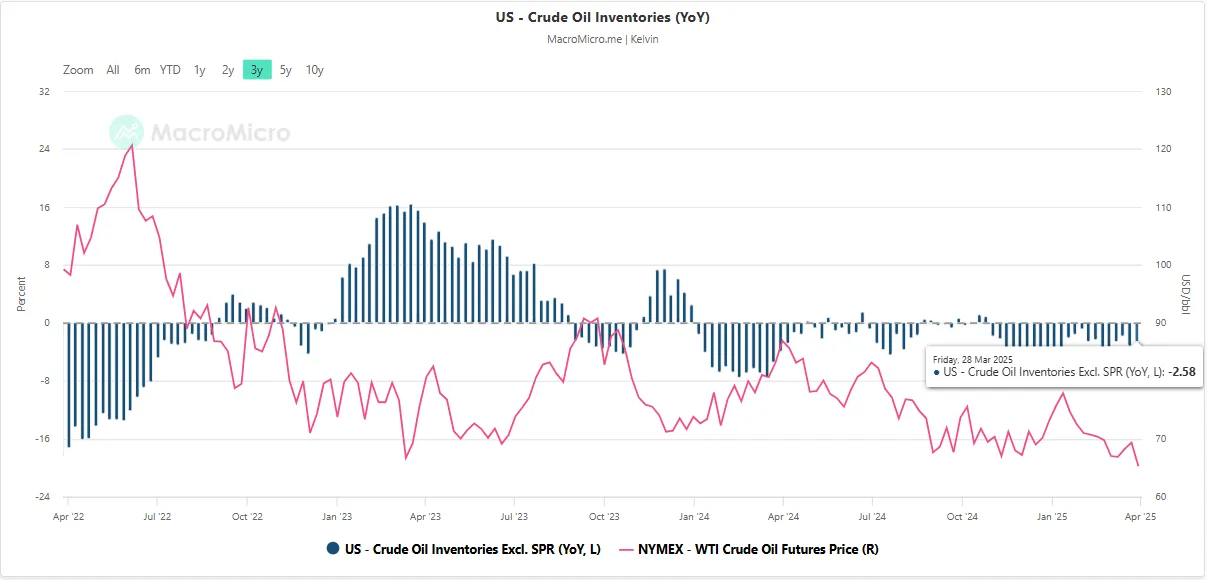

Fig 1: EIA US crude oil inventories excluding SPR (y/y change) with WTI crude oil futures as of 28 Mar 2025 (Source: MacroMicro)

WTI crude has a negative double whammy hit caused by demand and supply factors. Firstly, the rising probability of a stagflation environment in the US has triggered a global recession alarm, in turn, weakening demand for oil as business activities slow down.

Secondly, OPEC+ producers have agreed to boost the cartel's oil output by 411,000 barrels per day next month, coupled with a recent lesser magnitude of drawdown of US crude oil inventories seen in the past three weeks that may add another layer of downside pressure in oil prices.

The growth of US crude oil inventories excluding the Strategic Petroleum Reserve (SPR) on a year-on-year basis has an indirect correlation with the movement of WTI crude oil, as build-up in oil inventories puts downside pressure on oil prices.

Since 13 December 2024, the drawn down of US crude oil inventories (excluding SPR) has slowed down from -5.11% y/y to -2.58% y/y as of 28 March 2025 based on data from the US Energy Information Administration (EIA) (see Fig 1).

US 65.40 key support is looking vulnerable

Fig 2: West Texas Oil CFD medium-term trend as of 4 Apr 2025 (Source: TradingView)

Current intraday price actions of the West Texas Oil CFD (a proxy of the WTI crude oil futures) have recorded a further drop of 3.2% on Friday, 4 April, and breached below the major “Descending Triangle” range support of US$65.40 at this time of writing (see Fig 2).

In addition, the daily MACD trend indicator has just flashed out a bearish crossover condition, and inched below its centreline, which increases the probability of a major bearish breakdown below the US$65.40 major range support.

A daily close below US$65.40 may trigger the start of a medium-term bearish impulsive down move sequence to expose the next medium-term support zone of US$$60.20/58.80.

However, a clearance above the US$72.50 medium-term pivotal resistance (also the key 200-day moving average) invalidates the bearish scenario to kickstart another round of choppy corrective rebound phase for the next medium-term resistances to come in at US$76.00 and US$80.30

Markets Eye US, Canada Job Reports, US Dollar Steadies

The Canadian dollar has taken a break after an impressive three-day rally, in which the currency climbed about 2%. In the European session, USD/CAD is trading at 1.4148, up 0.39%. On Thursday, the Canadian dollar touched 140.26, its strongest level since December.

US nonfarm payrolls expected to dip

The hottest financial news is understandably the wave of selling in the equity markets, but there are some key economic releases today as well. The US and Canada will both release the March employment report later today.

The US releases nonfarm payrolls, with the markets projecting a gain of 135 thousand, after a gain of 151 thousand in February. This would point to the US labor market cooling at a gradual pace, which suits the Federal Reserve just fine. The Fed will also be keeping a watchful eye on wage growth, which is expected to tick lower to 3.9% y/y from 4.0%. The unemployment rate is expected to hold at 4.1%.

The employment landscape is uncertain, with the DOGE layoffs and newly-announced tariffs expected to dampen wage growth in the coming months.

Canada's employment is expected to improve slightly to 12 thousand, after a negligible gain of 1.1 thousand in February. Unemployment has been stubbornly high and is expected to inch up to 6.7% from 6.6%.

Canada vows retaliatory tariffs against US

US President Donald Trump's tariff bombshell on Wednesday did not impose new tariffs on Canada, but trade tensions continue to escalate between the two allies. Canada said it would mirror the US stance and impose a 25% tariff on all vehicles imported from the US that do not comply with the US-Canada-Mexico-Canada free trade deal. The US has promised to respond to any new tariffs against the US, which could mean a tit-for-tat exchange of tariffs between Canada and the US.

US/Canada Technical

- USD/CAD has pushed above resistance at 1.4088 and 141.26. The next resistance line is 1.4170

- 1.4044 and 1.4006 are the next support levels

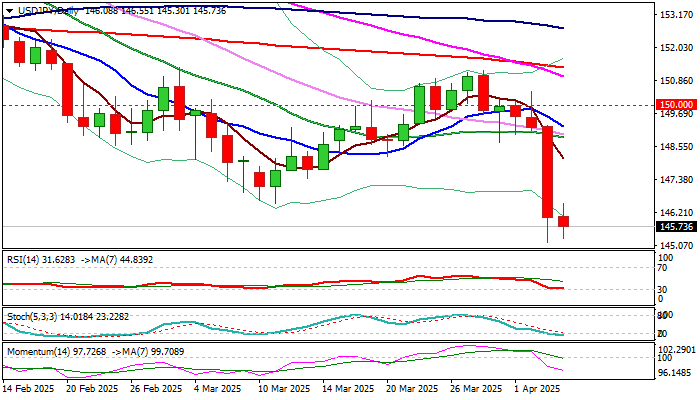

USD/JPY: Bears Take a Breather But Recovery Likely Limited

USDJPY edged higher on Friday morning, showing a partial recovery of Thursday’s 2.1% drop (the biggest daily drop since 1 May 2024).

Long lower shadows of daily candles of today/Thursday) point to growing bids) although recovery is unlikely to accelerate as fundamentals remains favorable for safe haven Japanese yen.

Risk aversion is on the rise and continues to prompt traders into safety, while dollar remains under strong pressure from tariffs and hopes of more dovish Fed’s stance on interest rates, although the central bank will remain extremely cautious and base its future decisions on economic conditions.

Release of US March labor data will be key economic event today, with non-farm payrolls likely slowing in March, but forecasts point to still steady conditions and more negative impact from mass firing of public sector workers to likely show in coming months.

Fresh bears look for weekly close below broken pivots at 146.95/53 (Fibo 61.8% of 139.57/158.87/Mar 11 low respectively) to validate bearish signal (the pair is on track for a weekly loss of about 2.5%) and focus next targets at 144.13 (Fibo 76.4%) violation of which to unmask140.00/139.27 (psychological/Fibo 38.2% of larger 102.59/161.95 uptrend) in extension.

Initial resistance at 146.60 (Marr 11 former low / Fibo 23.6% of 153.20/145.18 bear-leg) holds for now and should ideally cap upticks.

Res: 146.60; 147.48; 148.19; 148.90.

Sup: 145.18; 144.13; 143.65; 142.97.