Sample Category Title

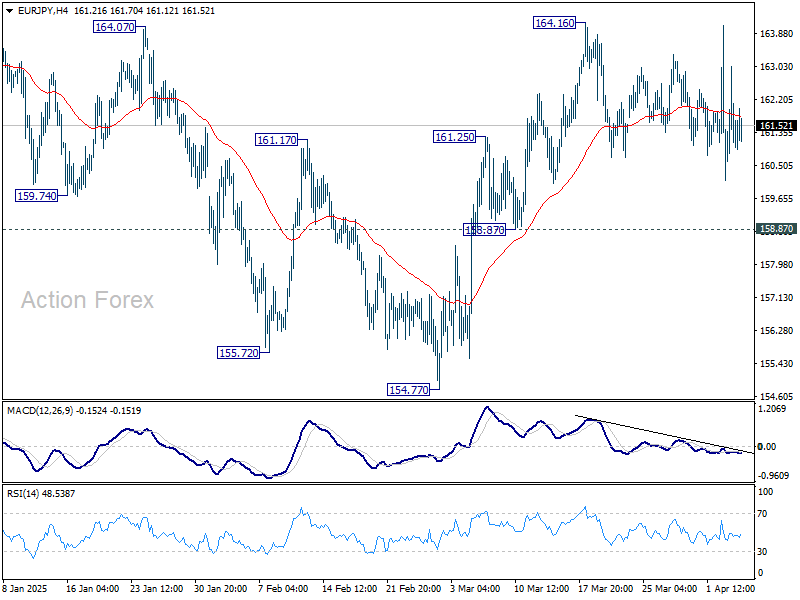

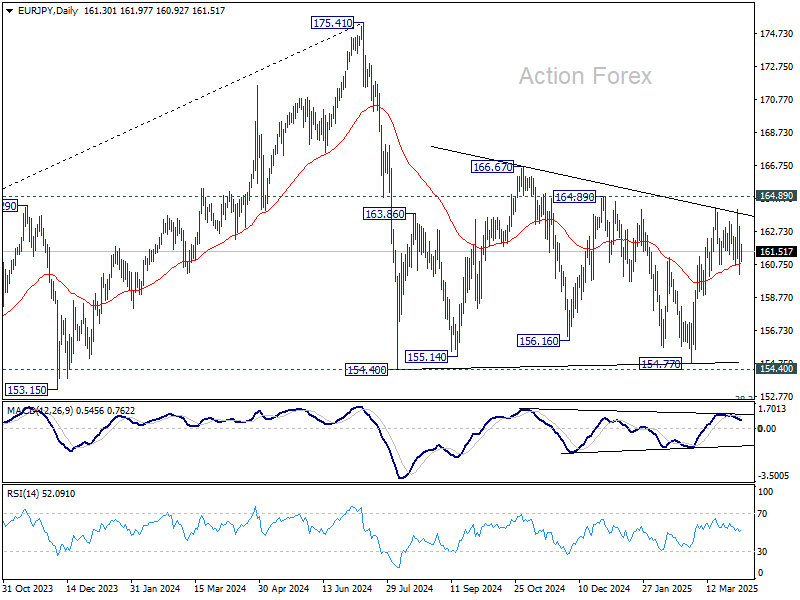

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.01; (P) 161.53; (R1) 162.96; More...

Range trading continues in EUR/JPY and intraday bias remains neutral. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, break of 158.87 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

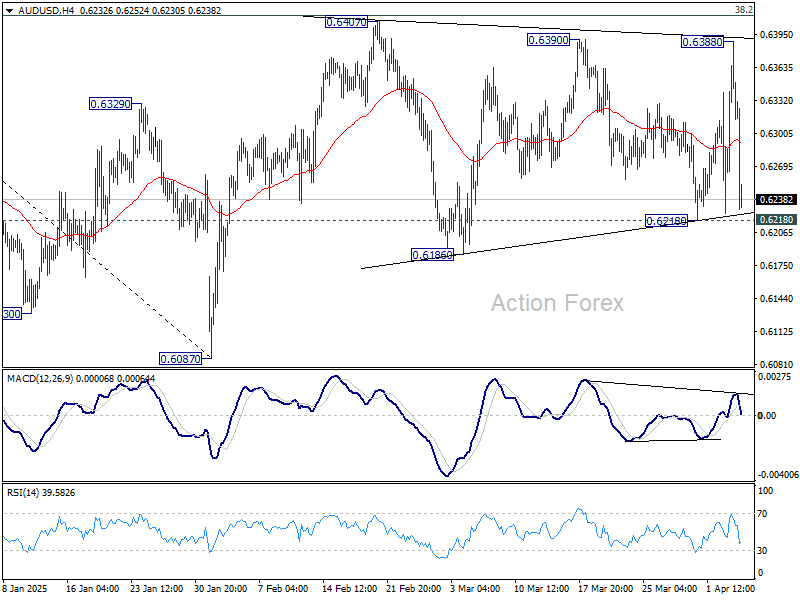

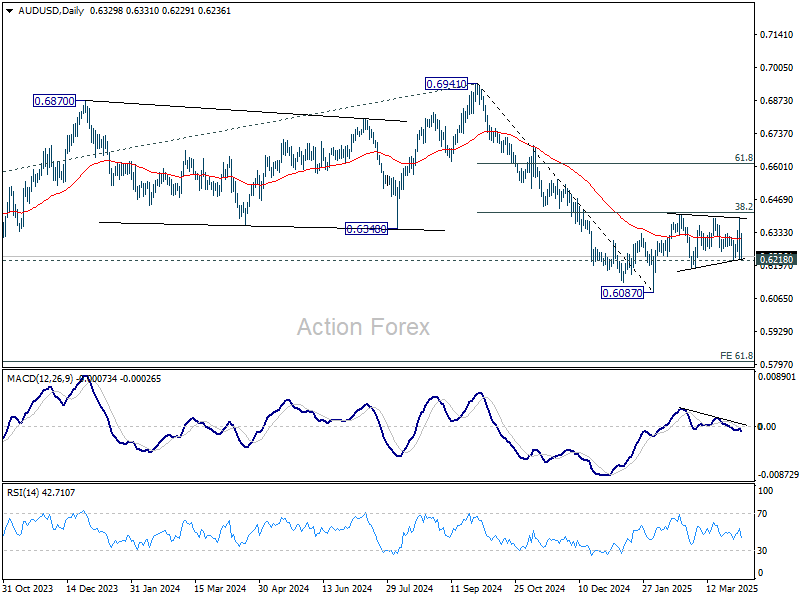

AUD/USD Daily Report

Daily Pivots: (S1) 0.6240; (P) 0.6315; (R1) 0.6403; More...

AUD/USD jumped to 0.6388 but reversed again. Intraday bias remains neutral for the moment. Overall, outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds. Firm of 0.6128 support will argue that corrective pattern from 0.6087 has completed and bring retest of this low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6461) holds.

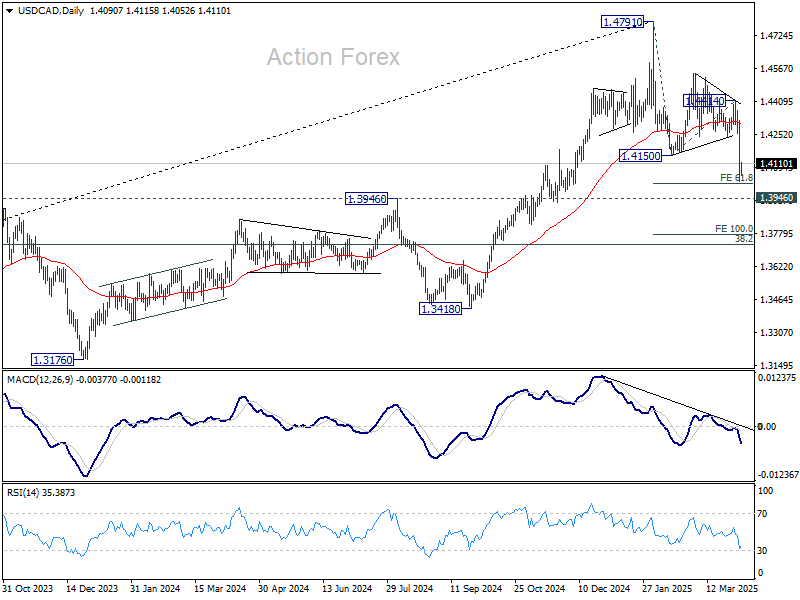

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3978; (P) 1.4148; (R1) 1.4269; More...

Intraday bias in USD/CAD remains on the downside for 61.8% projection of 1.4791 to 1.4150 from 1.4414 at 1.4018. Decisive break there would extend the fall from 1.4791 to 100% projection at 1.3773 next. On the upside, above 1.4158 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.3986). Sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

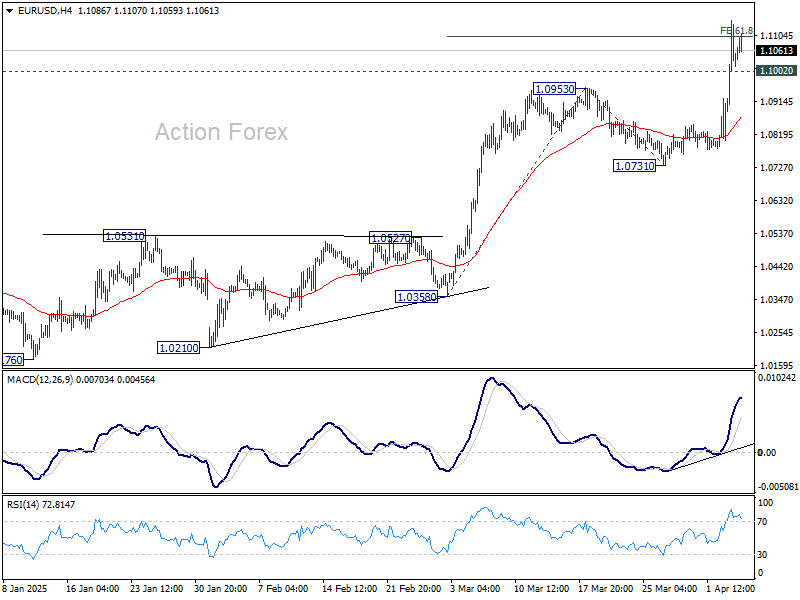

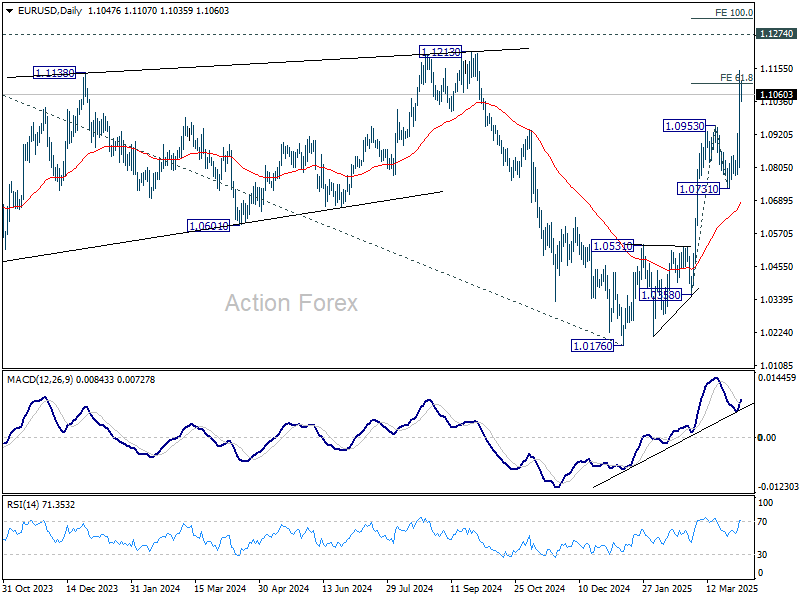

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0855; (P) 1.1001; (R1) 1.1196; More...

Intraday bias in EUR/USD remains on the upside at this point. Sustained trading above 61.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1099 will pave the way to 1.1274 key resistance, and probably further to o 100% projection at 1.1326. On the downside, below 1.1002 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

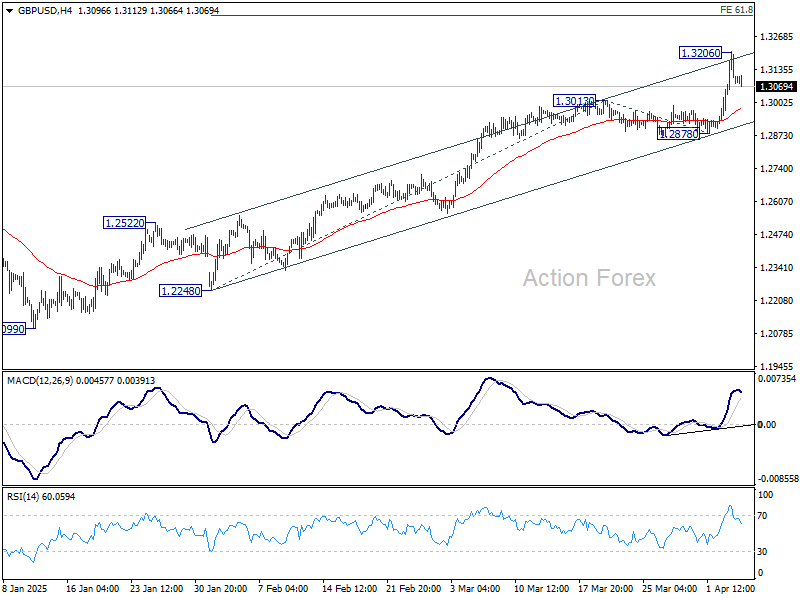

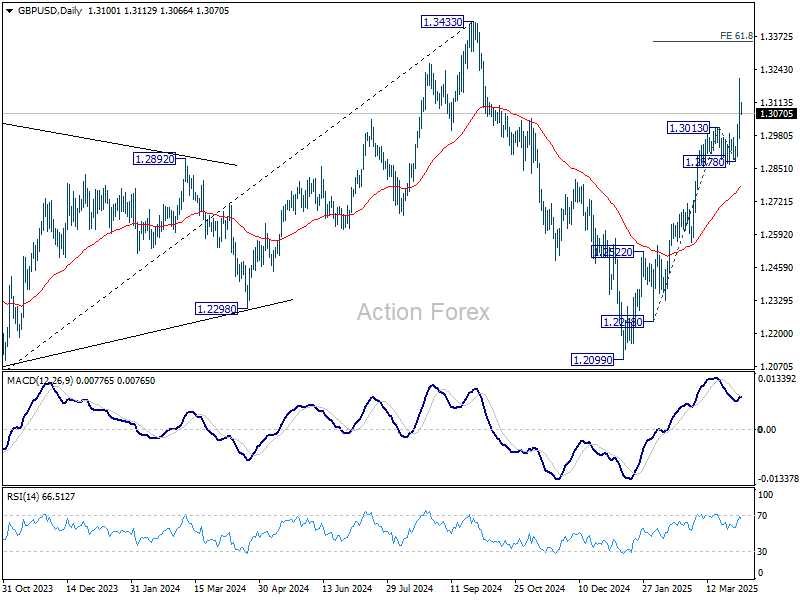

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2980; (P) 1.3094; (R1) 1.3215; More...

A temporary top is formed at 1.3206 with current retreat and intraday bias is turned neutral first. Downside of retreat should be contained above 1.2878 support to bring another rally. Break of 1.3206 will resume the rise from 1.2099 to 61.8% projection of 1.2248 to 1.3013 from 1.2878 at 1.3351.another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

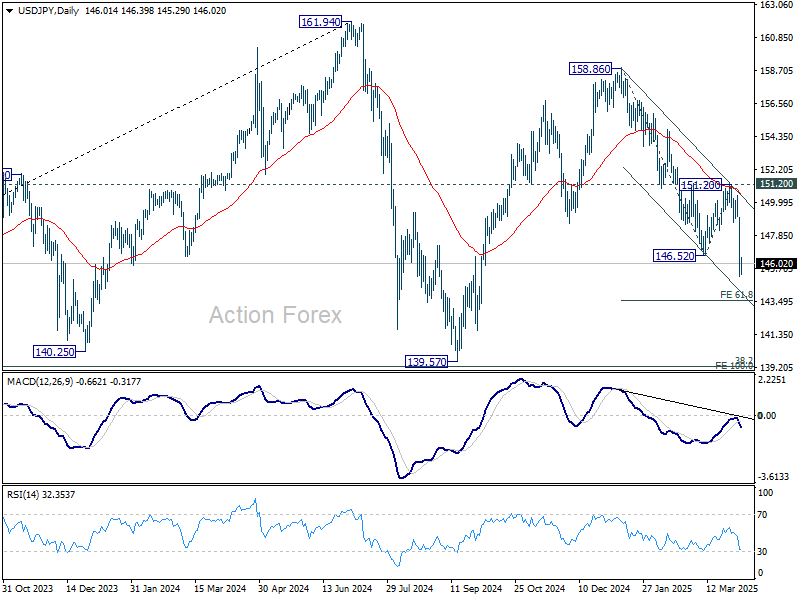

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.41; (P) 146.86; (R1) 148.53; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 is in progress for 61.8% projection of 158.86 to 146.52 from 151.20 at 143.57. On the upside, above 146.76 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited below 151.20 resistance to bring another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US Dollar Fell Off a Cliff

Markets

Financial markets came crashing down yesterday in the aftermath of the Trump administration’s new trade policy. A shocking range of tariffs risks retaliatory measures and could plunge the world into an outright trade war. Recession fears spiked. Stock markets stood at the center of attention with losses in Europe mounting to >3.5%. Wall Street shed some 4% (Dow) to 6% (Nasdaq) in value. The technical picture deteriorated significantly in the likes of the S&P500 (-4.8%, losing the 5500 support area). The US yield curve bull steepened impressively. Front end yields tumbled around 17 bps while longer maturities, also supported by haven flows, dropped 3 bps (30-yr) to 10 bps (10-yr). German Bunds rallied in lockstep with yields easing between 3 (30-yr) to 9.5 bps (5-yr) on a net daily basis. Such front end outperformance stems from markets assuming central banks will come to the rescue with aggressive rate cuts but ignores the fact that the inflation context is completely different than what we’ve been used to prior to the pandemic. Such an initial kneejerk reaction is not abnormal though and could continue in the short run. US rates this morning drop another 4 bps across the curve. Money markets are currently pricing in more than four 25 bps rate cuts this year with a first one fully discounted for June. It’s against this backdrop that Fed chair Powell is to discuss the economic outlook later today. While the central bank has a dual mandate, their primary focus today is still inflation. We think it is way too early for Powell and the Fed to already shift to growth and as such validate current market pricing. It’s a matter of short-term inflation risks vs medium-term growth risks. The Fed still has some credibility to regain after grossly misjudging the post-pandemic CPI surge. It is also against this recessionary backdrop that the US payrolls report will be read. Any downside miss would fuel the fire and add volatility. We think a topside surprise is unlikely given, for example, the weak (employment) details from yesterday’s services ISM. Markets would dismiss it instantly anyway. The US dollar fell off a cliff. A growing recessionary risk premium is the go-to explanation but we suspect more fundamental de-dollarization dynamics are at play too. EUR/USD surged to an intraday high of 1.1144 before closing at 1.105. Ongoing dollar weakness this morning pushes the pair back towards the 1.11 lever though and remains on its way to 1.1214 (2024 high). DXY slid from 103.8 at Tuesday’s close to 101.7 currently. The Japanese yen is the one true safe haven that takes USD/JPY towards a six month low of 145.9. China was among the hardest hit by the US (up to 54%). Its currency dropped to USD/CNY 7.3 at the open before paring losses to 7.28.

News & Views

National Bank of Poland governor Glapinski made a surprise dovish U-turn in the presser one day after Wednesday’s rates status quo (5.75%). Until recently he advocated that no rate cuts should be expected anytime soon. However, yesterday he assessed that softer than expected Q1 inflation figures caused a radical shift the MPC’s outlook. Even as he still wants confirmation on recent softer inflation data, the NBP governor indicated that a first rate cut in May or in the following months is possible. Glapinski also said that that easing may exceed 100 bps this year if the government prevents energy prices from rising. The policy rate might be reduced further to 3.5% next year, in case inflation stays benign. He also indicated to favor one-off rate cuts rater than a series of steps. After even rising marginally on Wednesday, the Polish 2-y swap yield yesterday tumbled from 4.84% to 4.52%. The zloty fell off a cliff with EUR/PLN jumping from the 4.18 area before the press conference to close near 4.225.

Rating agency Fitch downgraded China by one notch to A from A+. The move came after the agency in April last year put the outlook off the country on negative. “The downgrade reflects our expectations of a continued weakening of China's public finances and a rapidly rising public debt trajectory during the country's economic transition.” The outlook is now again set at stable. Fitch expects that sustained fiscal stimulus will be deployed to support growth, amid subdued domestic demand, rising tariffs and deflationary pressures. In this context, Fitch sees “the government debt/GDP to continue its sharp upward trend over the next few years, driven by these high deficits, ongoing crystallisation of contingent liabilities and subdued nominal GDP growth.” The assessment was made before President Trump announced new tariffs on Wednesday, but analysts at the agency indicated that there is headroom at the current rating to accommodate the likely implications for economic growth and fiscal metrics from the tariffs.

Prisoner’s Dilemma

Yesterday saw the worst selloff since the pandemic. Equity markets gave a strong reaction to Trump’s tariff nonsense: the S&P500 lost almost 5% erasing around $2 trillion in market capital, Nasdaq 100 tanked 6% and the Dow Jones dumped 4%. Apple, Amazon, Nvidia, Microsoft, Tesla lost tens and for some hundreds of billions in market cap. Companies that have complex worldwide supply chains like Gap, H&M and Dell saw heavy losses, as well. Gap and Dell lost around 20% of their total market cap in a single session. These are not meme stocks, these are established companies. In Europe, the Stoxx 600 lost more than 2.5%, the Hang Seng index is down by around 1.50% this morning, Nikkei lost more than 17% since January, the treasury yields tanked across continents as investors moved money to safety, gold hit a fresh record, while the US dollar index lost around 1.70%.

The tariff chaos will likely help the euro end the week above the 1.10 mark and sterling above 1.30 against the US dollar. And gains could be sustainable as nations look willing to retaliate. The EU said there will be a strong response that could include measures against American tech giants and limitation on US investments and Canada imposed 25% levies on US-made vehicles. Bloomberg even suggests that the US treasuries are at risk of foreign buyer strike in tariff retaliation!

The global economy has now entered a dark tunnel. No one knows what’s next. For the Europeans, there is some kind of a consensus that the European Central Bank (ECB) would shift toward a more supportive stance than otherwise as long as inflation remains in check. The Swiss National Bank (SNB) is now expected to pull the rates down to 0% and even to the negative territory to – at least – counter the franc’s strength and help exporters with macroprudential measures. For the Federal Reserve (Fed) however, opinions diverge. Some think that the Fed will cut rates aggressively to slow economic slowdown, while others think that the Fed won’t cut at all this year due to rising inflation expectations. Activity on Fed funds futures give reason to the former - the probability of a June cut shot up to around 95% - but the Fed will be less restrictive in its response compared to GFC or pandemic due to inflation.

Pandemic-like supply chain disruption?

The risk of a heavy hit to global supply chains will require very strong reorganization that could take months and even years. As such, it’s not crazy to make parallels with the supply disruption of the pandemic to foresee what could happen next. And if we do that, the answer is clear: the inflation jump that we are about to see could not be ‘transitory’. The Fed could make the bet to cut rates despite heating inflation and to stabilize financial markets. But taming the strong downside revisions to earnings projections when the global supply chains are put under such pressure will be harder. The selloff could accelerate before rebound.

US jobs data doesn’t matter much

The US will reveal its latest jobs data today. On Wednesday, the ADP printed a better-than-expected figure. A consensus of analysts' estimates on Bloomberg suggests that the US economy may have added around 137K new nonfarm jobs last month. Either way, the US economy will soon start feeling the pain of tariffs – as manufacturing jobs won’t come to the US overnight – and the latter makes this week’s report totally uninteresting.

Crude Oil tanks on very bad combo

US crude dived 6% dive yesterday on the tumbling global growth and demand expectations combined with the OPEC+ decision to restore production more than expected. OPEC+ countries yesterday announced that they would bring 411K barrels a day to the market – the equivalent of three-monthly tranches from its previous output restoration plan. As such, the supply / demand fundamentals remain comfortably negative. Obviously, the tariffs will hit the global oil demand much less compared to the pandemic. Yet the upcoming slowdown in global economic activity reinforces the probability of a further slide toward the $50pb level.

DOGE-Driven Layoffs Set the Stage for US Jobs Report

In focus today

In the US, the March Jobs Report finishes off an eventful week. We think nonfarm payrolls growth slowed down to just 110k (from +151k) amid federal layoffs and sharply slowing immigration. The unemployment rate could edge slightly higher to 4.2% although we think tighter labour supply growth will constrain the rate from rising significantly. Average hourly earnings growth likely remained steady at +0.3% m/m SA.

In Sweden, the flash inflation data for March is released (CET 08:00). We expect another substantial increase in food prices, which will elevate underlying inflation, CPIF excluding energy, to 3.2% year-on-year (Feb. 3.0%) according to our forecast. This is slightly higher than the Riksbank's forecast of 3.1%. The high readings complicate policy making for the Riksbank given that the weak recovery, which met another headwind by the tariffs, would justify further rate cuts, in our view.

Economic and market news

What happened yesterday

In the US, ISM services surprised to the downside for March, declining sharply to 50.8 (cons. 53) from 53.5 in February. In contrast to its PMI counterpart released earlier, which pointed to a more positive outlook, this ISM reading showed the softest expansion in the services sector since June last year. The March Challenger Report on layoff announcements showed 275k job cuts in March, a significant increase from 172k in February and the highest value since May 2020. With the government leading all sectors in job cuts, this reading to a large degree reflects the impact of the DOGE plans to eliminate positions in the federal government.

In the euro area, services PMI for March was revised up to 51.0 from 50.4 in the flash release. This is positive news since the services sector is the largest part of the economy, accounting for 74% of GDP. In isolation the final March PMI report supports the hawk camp in the ECB calling for a pause in April. Yet, declining inflation and recent tariff announcements should tip the balance towards a cut in April given downside risks to growth and inflation almost at target.

In Sweden, composite PMI has decreased to 50.6%, primarily due to a drop in the Services PMI, which fell to 49.4 from a revised 50.5 in February. This marks the first contraction of the year and the lowest level since September. All areas of the index declined, with employment - which is for 20% of the Services PMI - remaining below 50 for the eighth consecutive month. The strong performance of the Manufacturing PMI earlier this week is helping sustain the composite index level.

In Norway, housing prices rose 0.1 % m/m (SA) in March, confirming signals of a cooler market after rate cut expectations and some easing of regulation lifted prices towards the end of last year and into 2025. This is weaker than Norges Bank (NB) assumed in the latest MPR at 0.7 % m/m. However, NB has repeatedly stressed that stronger nominal housing prices is first and foremost a correction in real prices back to the 2022-level, and that credit growth remains muted and below income growth. Hence, the figures will not affect monetary policy in the coming months.

Equities: Global equities experienced a severe downturn yesterday, likely for reasons familiar to everyone. A closer examination reveals significant outperformance by defensive sectors compared to cyclicals. While this is not entirely surprising, the fact that markets declined so heavily yet utilities and consumer staples rose was admittedly unexpected. The US markets were hit hardest, which makes a lot of sense given that US consumers are most affected by this situation. The US is also facing the largest revisions to its growth outlook following the implementation of the new US tariff regime. With both uncertainty and recession risk significantly heightened following "liberation day", it is unsurprising to see the VIX spike to a level of 30.

Whether discussing the direction for equities, cyclicals versus defensives, or the level of volatility and implied volatility, it would, in our opinion, look very different without the current political environment in the US. It is quite rare to witness a correction (a drop of more than 10%) in global equities under the current macroeconomic conditions. However, that is the reality with Trump as the US president, and one must act accordingly. In the US yesterday, the Dow was down 4.0%, the S&P 500 fell 4.8%, the Nasdaq declined 6.0%, and the Russell 2000 dropped 6.6%. Asian markets continue to trend lower this morning, and the same is true for futures in Europe and the US.

FI&FX: The dollar index DXY experienced its second biggest loss in one day since the GFC, Nasdaq slumped 6.0% (third biggest one-day loss since GFC) while the broader S&P 500 was down 4.8%. Nikkei -3.6% and equity futures are in red. Treasuries rallied massively lead by the short end of the curve as 2Y is down 30bp since Tuesday's peak. Bullish steepening characterized fixed income across regions. EUR/USD jumped three figures to trade close to 1.11 this morning, USD/JPY dropped from 150 to 146. CHF alongside JPY are the two natural outperformers. SEK initially had a strong day, although gains were erased in the US session. NOK sold off throughout the day as the oil price dropped below USD 70. A sharp selloff of the zloty on quite a remarkable dovish shift from the NBP.

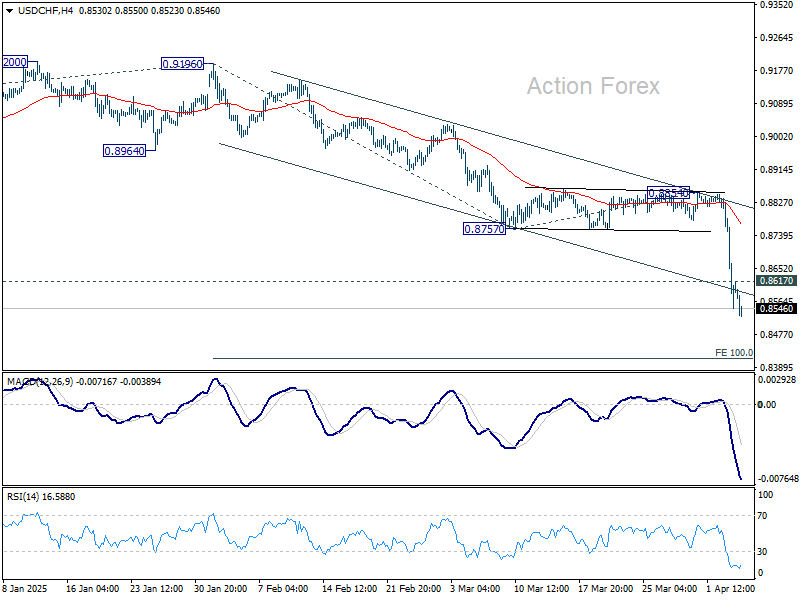

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8483; (P) 0.8658; (R1) 0.8769; More…

USD/CHF's steep decline is still in progress and there is no sign of bottoming yet. Intraday bias stays on the downside for 100% projection of 0.9196 to 0.8757 from 0.8854 at 0.8415. On upside, above 0.8617 minor resistance will turn intraday bias neutral and bring consolidations. But recover should be limited below 0.8757 support turned resistance to bring another fall.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.