Sample Category Title

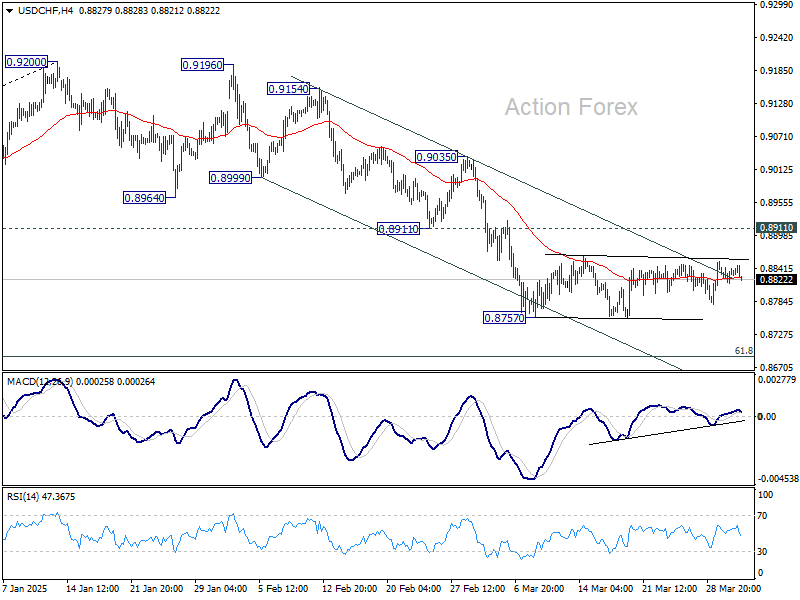

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8819; (P) 0.8835; (R1) 0.8854; More…

Intraday bias in USD/CHF stays neutral for the moment. Consolidation from 0.8757 is still in progress. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

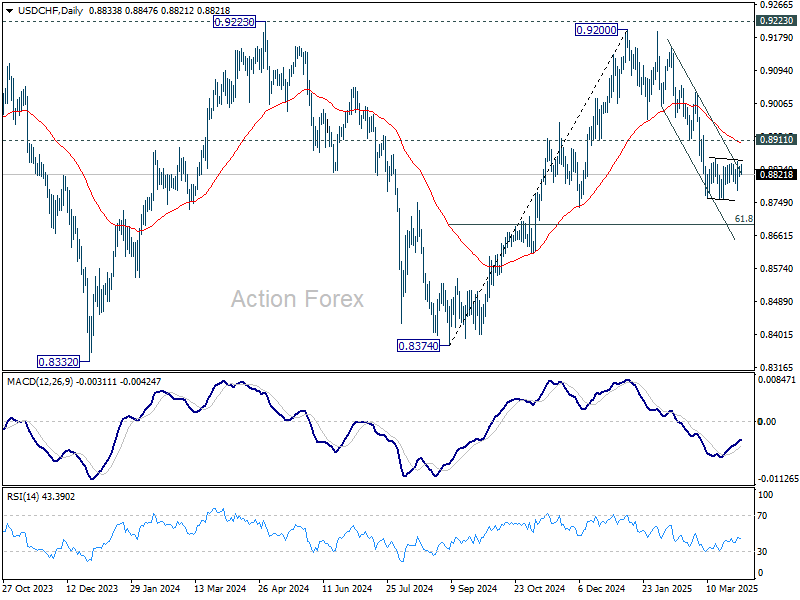

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

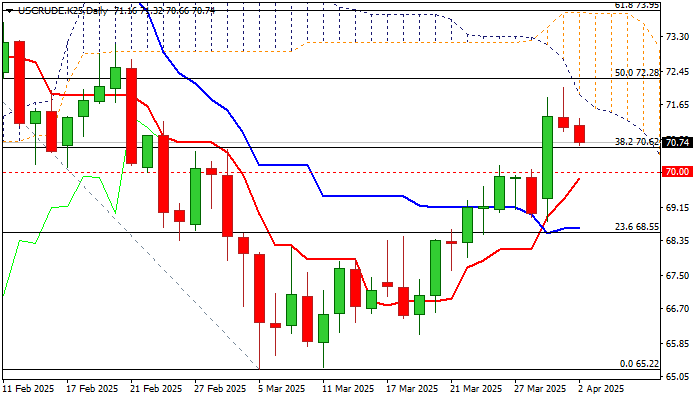

WTI Price Consolidates Under New Multi-Week High

WTI oil price is trading under new five-week high ($72.08, posted on Tuesday) after the price rallied 2.8% on Monday (the biggest daily gain since Jan 15).

Slight easing so far looks more like a consolidation rather than stronger profit-taking as markets turned to quiet mode and await the verdict about tariffs from US President Trump (due later today).

Positive factors that boost oil demand were threats from the US on imposing the secondary tariffs on buyers of Russian oil, better than expected China’s recent economic data which boost hopes for stronger demand from the world’s number one oil importer and growing tensions between the US and Iran.

OPEC+ will meet on Thursday and expect to stick to plans for further output increase from May that would partially counter the impact of supportive factors.

All eyes are now on President Trump’s tariff announcement, which is likely to be the key driver.

Market are expected to be volatile, and reaction will directly depend on size and scope of new tariffs.

Aggressive tariff rhetoric would further fuel fears of economic slowdown and inflation rise, which would have a negative impact short-term outlook and deflate oil price.

Conversely, softer than expected Trump’s stance on tariffs would keep larger bulls in play and provide fresh support to oil price.

Technical studies are mixed on daily chart, as positive momentum remains strong and north-heading daily Tenkan-sen is diverging from daily Kijun-sen after forming a bull-cross, while the price action remains weighed by falling and thickening daily Ichimoku cloud (base lays at $71.58).

Good supports lay at $70.69/62 (100DMA / broken Fibo 38.2%) followed by $70 zone (psychological, reinforced by rising daily Tenkan-sen).

Daily cloud base marks initial barrier, followed by $72.08 (new high) and $72.28/50 (50% retracement of $79.35/$65.22 / 200DMA).

Res: 72.08; 72.28; 72.50; 73.12.

Sup: 70.62; 70.42; 70.00; 69.70.

Australian Dollar Rally Continues, Trump Tariffs Loom

The Australian dollar has posted strong gains for a second straight day. In the European session, AUD/USD is trading at 0.6306, up 0.47% on the day.

RBA holds rates but hints at further cuts if trade tensions worsen

The Reserve Bank of Australia maintained the cash rate at 4.10% on Tuesday, in a move that was widely expected by markets. Still, the Australian dollar reacted positively, gaining 0.48% on Tuesday.

The RBA statement noted that underlying inflation continued to ease in line with the Bank's forecast, but the Board "needs to be confident that this progress will continue" so that inflation remains sustainable at the midpoint of the 2%-3% target band.

The statement said there was "significant" uncertainty over global trade developments, pointing to the threat of further US tariffs and possible counter-tariffs from targeted countries.

The central bank's decision was made in the midst of a hotly contested election campaign, and a rate cut would likely have been attacked by the opposition parties as political interference.

In a press conference after the meeting, Governor Michele Bullock acknowledged the uncertainty over the global outlook due to US trade policy but sought to assure the markets by saying that Australia was "well placed" to weather the potential storm of a global trade war.

Markets bracing for Trump tariffs

US President Trump has not specifically targeted Australia with any tariffs but China is Australia's number one trading partner and a US-China trade war would inflict damage on Australia's economy.

The new US tariffs are expected to be announced later today and take effect on Thursday. The financial markets remain volatile as investors look for some clarity from Washington about the tariffs, as it remains unclear which countries will be targeted and the extent of the tariff rates.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6297. Above, there is resistance at 0.6315

- 0.6264 and 0.6246 are the next support levels

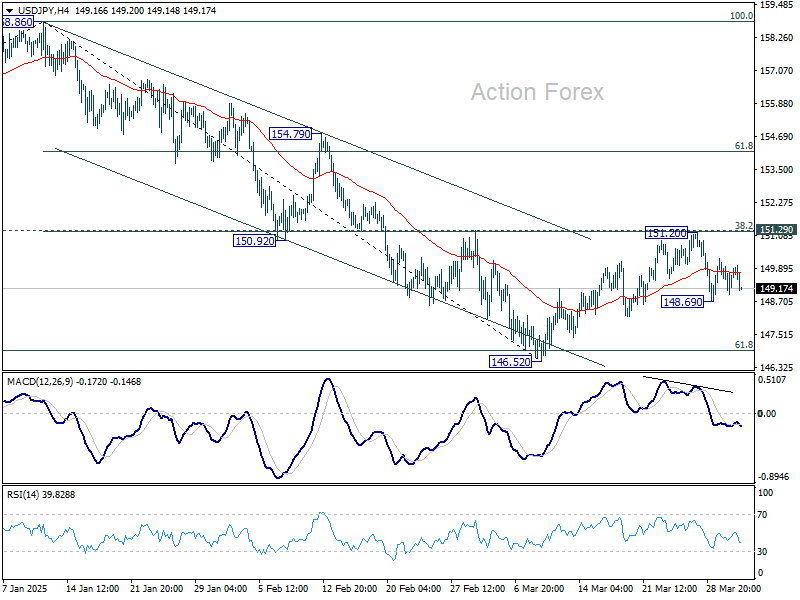

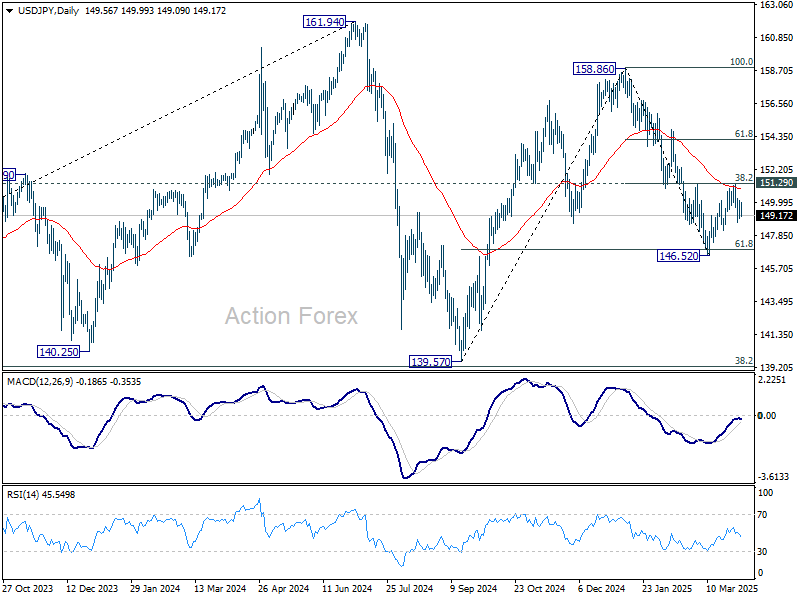

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.58; (R1) 150.19; More...

Range trading continues in USD/JPY and outlook is unchanged. Intraday bias remains neutral at this point. Corrective rise from 146.52 could have completed at 151.20 already. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Investors Await Clarity as Trump’s Trade Plan Nears Unveiling

Risk-off sentiment has returned to European markets and US futures as traders await the long-anticipated announcement of the United States’ reciprocal tariffs, scheduled for 2000 GMT. After months of speculation and political posturing, today is expected to bring the concrete details of US President Donald Trump’s sweeping reciprocal tariffs plan. Markets are hoping for clarity on which countries and sectors will be affected, the magnitude of the levies, when they will take effect, and whether any exemptions will be granted.

While the announcement itself may provide clarity to a certain extent, hopefully, it’s far from the end of the story. A big unknown remains how major trading partners, especially the European Union, will respond. Retaliatory measures are expected, but the scale, scope, and timing remain uncertain. And beyond that, markets are already looking to Washington’s next move—will the US escalate further if other nations push back?

On the more hopeful side, many still believe that this will eventually culminate at the negotiating table, where barriers are eased rather than raised. Historically, tariff wars have led to tough talks and eventual compromises. However, any such diplomatic resolution would likely be a long process and do little to ease near-term volatility or economic strain.

Pessimists, on the other hand, are concerned that the true aim of the US isn’t merely reciprocity, but reshoring manufacturing and breaking long-standing trade norms. These goals require very different approaches and outcomes. The former could lead to quick concessions, the latter a prolonged and potentially damaging realignment of global supply chains.

There is a chance of a short-term relief rally in stocks if today's announcement is less severe than feared. However, any bounce could be short-lived. For S&P 500, downside risks remain dominant as long as 5786.95 resistance holds. The larger corrective fall from 6147.47 would still be in play. Next target would be 38.2% retracement of 3491.58 to 6147.47 at 5132.89 after the recovery, if any, completes.

In currency markets, Kiwi and Aussie are leading today followed by Sterling. while Loonie lags behind at the bottomed, followed by Dollar, and Swiss Franc. Euro and Yen are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.87%. DAX is down -1.63%. CAC is down -0.91%. UK 10-year yield is down -0.043 at 4.609. Germany 10-year yield is down -0.036 at 2.661. Earlier in Asia, Nikkei rose 0.28%. Hong Kong HSI fell -0.02%. China Shanghai SSE rose 0.05%. Singapore Strait Times fell -0.37%. Japan 10-year JGB yield fell -0.025 to 1.479.

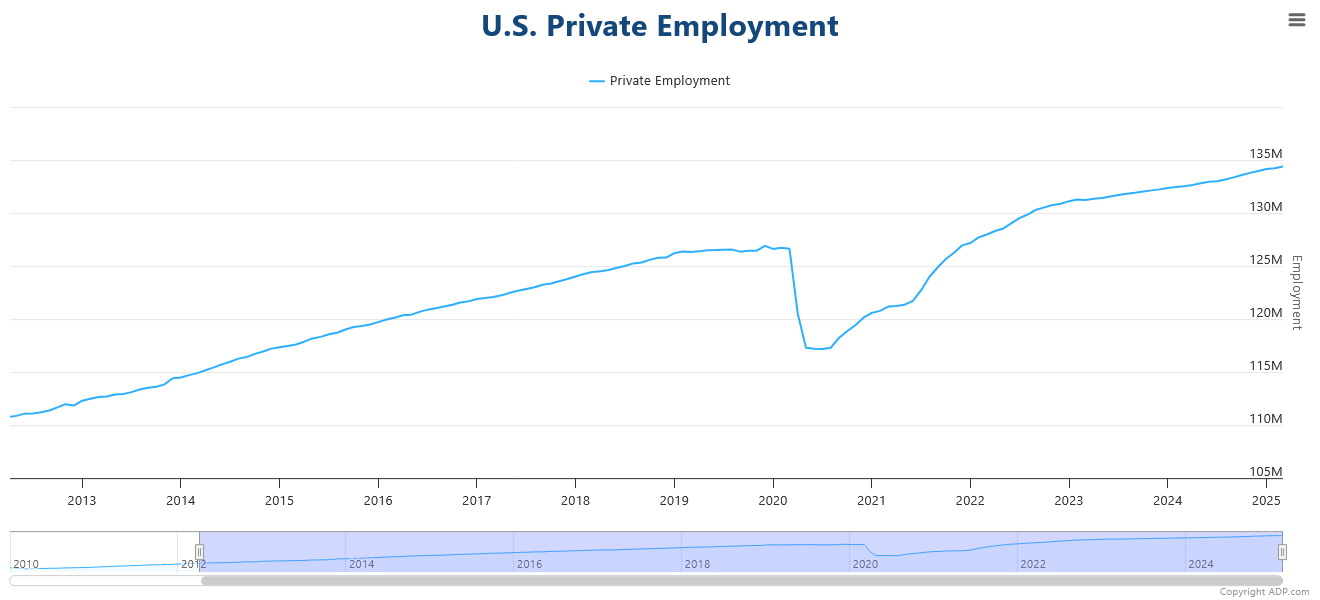

US ADP jobs grow 155k, pay growth cools further

US ADP private sector employment rose by 155k in March, exceeding expectations of 120k. There were 24k positions added in goods-producing sectors and 132k in services.

Employers of all sizes contributed to the growth, with small firms leading the way, adding 52k jobs, followed by large and medium-sized businesses with 59k and 43k respectively.

Despite the strong employment numbers, wage growth continued to decelerate. Year-over-year pay gains slowed to 4.6% for job-stayers and 6.5% for job-changers. The premium for switching jobs fell to 1.9 percentage points—the lowest in the series since September.

ADP Chief Economist Nela Richardson commented that despite "policy uncertainty and downbeat consumers," the headline job number was a positive indicator for the economy and businesses of all sizes.

ECB's Lagarde: Tariffs harmful globally, often lead back to negotiation table

ECB President Christine Lagarde warned that the global effects of US-led tariffs will be “negative,” though the extent of the damage depends heavily on the scope, duration, and targeted products.

In an interview with Ireland’s Newstalk radio, she emphasized that the broader implications for global trade and growth would vary, but the potential for lasting disruption is real.

Lagarde also noted that history shows such trade escalations often end in talks rather than prolonged battles.

“Quite often those escalation of tariffs, because they prove harmful, even for those who inflict it, lead to negotiation tables,” she said, suggesting that any initial damage might eventually give way to diplomatic resolutions and the removal of trade barriers.

ECB's Schnabel: Trade fragmentation risks rekindling inflation, hitting growth

ECB Executive Board member Isabel Schnabel warned today that a global trade war could cause a sharp resurgence in inflation and weigh heavily on growth.

In a speech, she highlighted that a severe disruption in global trade flows could lift inflation by several percentage points in the early years.

She added that even a "mild decoupling" scenario would still have a meaningful impact—adding up to 1% to inflation and taking years to unwind.

BoJ's Ueda: US tariffs pose short-term inflation risk, long-term growth uncertainty

BoJ Governor Kazuo Ueda said today that the ramifications of US tariff policy remain "highly uncertain" and could significantly affect global trade.

Speaking to Japan’s parliament, Ueda emphasized that the ultimate impact would depend on the "range and scale" of the tariffs being implemented. He also noted that beyond trade flows, a key concern lies in "how the tariffs could affect the sentiment and spending of households and companies."

Ueda further highlighted that while US inflation may rise in the short term due to higher import costs, the longer-term effect is less predictable. He suggested that elevated tariffs could eventually weigh on US economic growth, which in turn might dampen inflationary pressures over time.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.58; (R1) 150.19; More...

Range trading continues in USD/JPY and outlook is unchanged. Intraday bias remains neutral at this point. Corrective rise from 146.52 could have completed at 151.20 already. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US ADP jobs grow 155k, pay growth cools further

US ADP private sector employment rose by 155k in March, exceeding expectations of 120k. There were 24k positions added in goods-producing sectors and 132k in services.

Employers of all sizes contributed to the growth, with small firms leading the way, adding 52k jobs, followed by large and medium-sized businesses with 59k and 43k respectively.

Despite the strong employment numbers, wage growth continued to decelerate. Year-over-year pay gains slowed to 4.6% for job-stayers and 6.5% for job-changers. The premium for switching jobs fell to 1.9 percentage points—the lowest in the series since September.

ADP Chief Economist Nela Richardson commented that despite "policy uncertainty and downbeat consumers," the headline job number was a positive indicator for the economy and businesses of all sizes.

ECB’s Schnabel: Trade fragmentation risks rekindling inflation, hitting growth

ECB Executive Board member Isabel Schnabel warned today that a global trade war could cause a sharp resurgence in inflation and weigh heavily on growth.

In a speech, she highlighted that a severe disruption in global trade flows could lift inflation by several percentage points in the early years.

She added that even a "mild decoupling" scenario would still have a meaningful impact—adding up to 1% to inflation and taking years to unwind.

ECB’s Lagarde: Tariffs harmful globally, often lead back to negotiation table

ECB President Christine Lagarde warned that the global effects of US-led tariffs will be “negative,” though the extent of the damage depends heavily on the scope, duration, and targeted products.

In an interview with Ireland’s Newstalk radio, she emphasized that the broader implications for global trade and growth would vary, but the potential for lasting disruption is real.

Lagarde also noted that history shows such trade escalations often end in talks rather than prolonged battles.

“Quite often those escalation of tariffs, because they prove harmful, even for those who inflict it, lead to negotiation tables,” she said, suggesting that any initial damage might eventually give way to diplomatic resolutions and the removal of trade barriers.

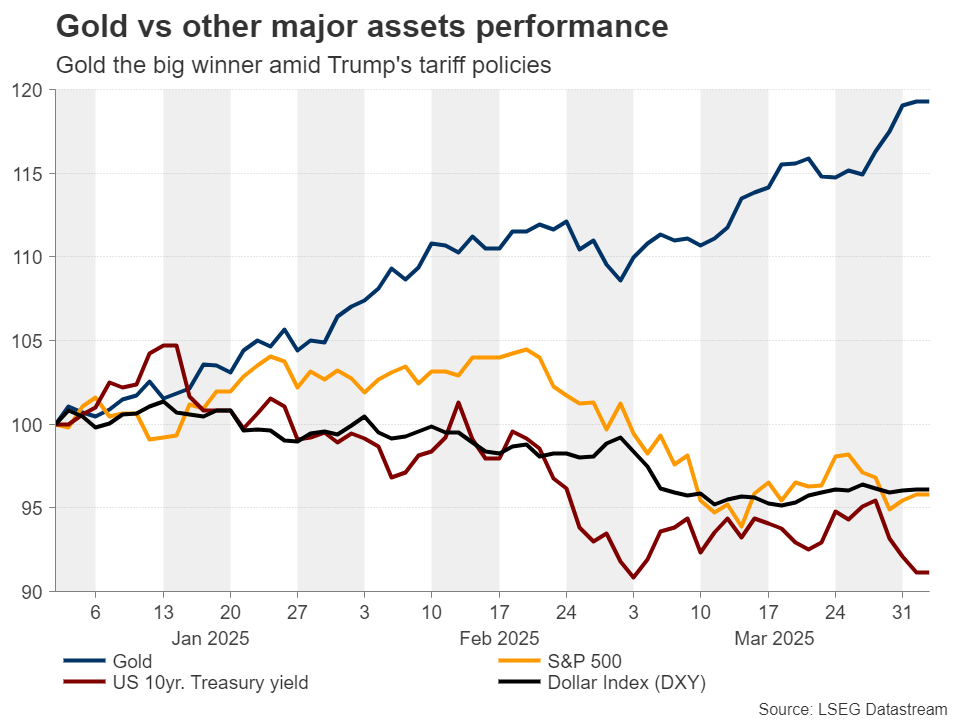

Gold acts as safety shelter amid Trump’s tariff chaos

- Gold gains nearly 20% year-to-date due to safe-haven flows.

- Trump’s tariff policies are fueling inflation and recession fears.

- Investors expect three quarter-point rate cuts by the Fed in 2025.

- But regardless of the Fed’s stance, gold may be destined to climb higher.

Tariffs are fueling Gold’s engines

Gold has been the best performing asset year-to-date, gaining nearly 20% and breaking record high after record high. The S&P 500, Treasury yields, and the US dollar are in the red, with Bitcoin suffering even more.

At this point it is worth noting that recently, equities have been positively correlated with the US dollar. The reason why this has been the case is the same reason why gold has been flying sky high, and it is no other than recession fears due to Trump’s tariff rhetoric and policies, as well as the broader uncertainty his policies are generating.

Although reports around a week ago suggested that Trump will adopt a softer and more flexible stance than previously anticipated on April 2, when the reciprocal tariffs are scheduled to take effect, the US President himself said last Wednesday that he is planning to proceed with a 25% levy on imported cars and light trucks on April 3. Duties on auto parts will take effect on May 3. And as if this was not enough, during this weekend, a report hit the wires saying that Trump will consider higher tariffs against a broader range of countries, as he aims at correcting trade imbalances against the US.

Recession fears intensify ahead of “Liberation Day”

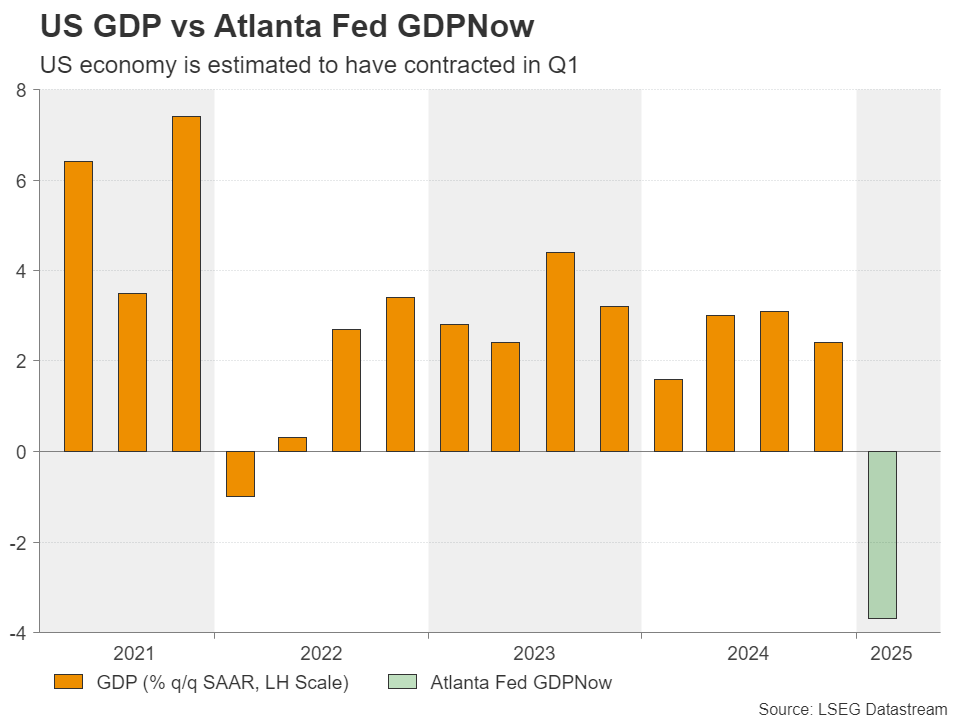

Initially, investors were afraid that tariffs would refuel inflation. However, although this still may be the case, they have lately shifted their focus on the impact Trump’s trade policies may have on the world’s largest economy. Following the latest toughening of Trump’s stance, Goldman Sachs is now projecting a 35% probability of a recession in the next 12 months, while the Atlanta Fed has revised down its GDPNow model estimate for Q1 to -3.7%.

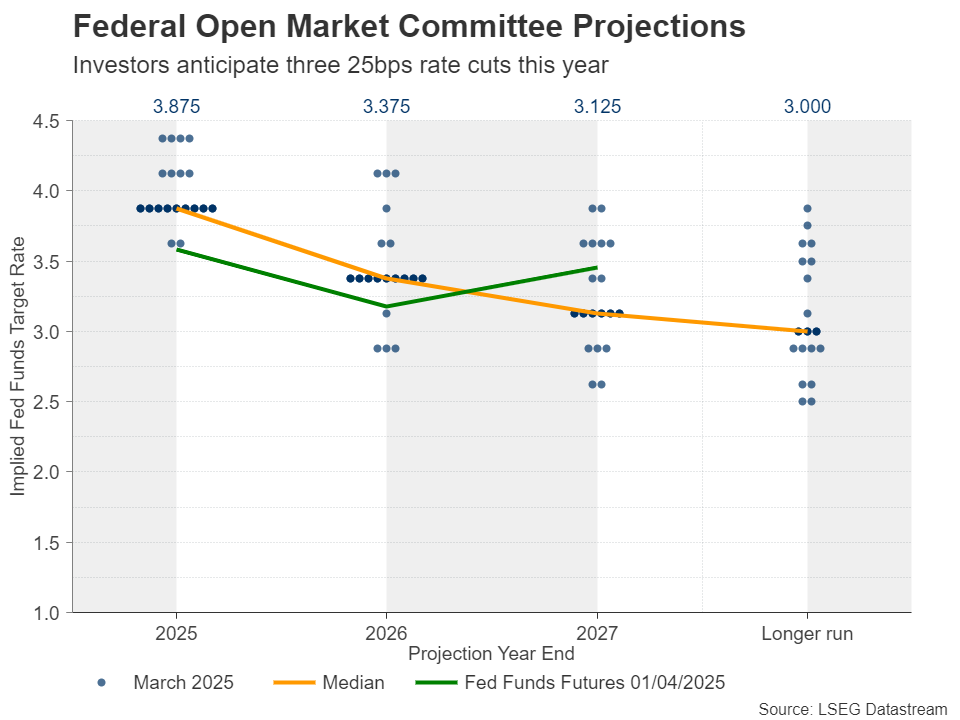

The heightening concerns about deep wounds in US economic activity have prompted investors to bring back to the table some of the rate cut bets they recently removed. Currently, they are pencilling in around 75bps worth of additional rate cuts by the end of the year, even though the Fed’s latest dot plot continued pointing to only two quarter point reductions.

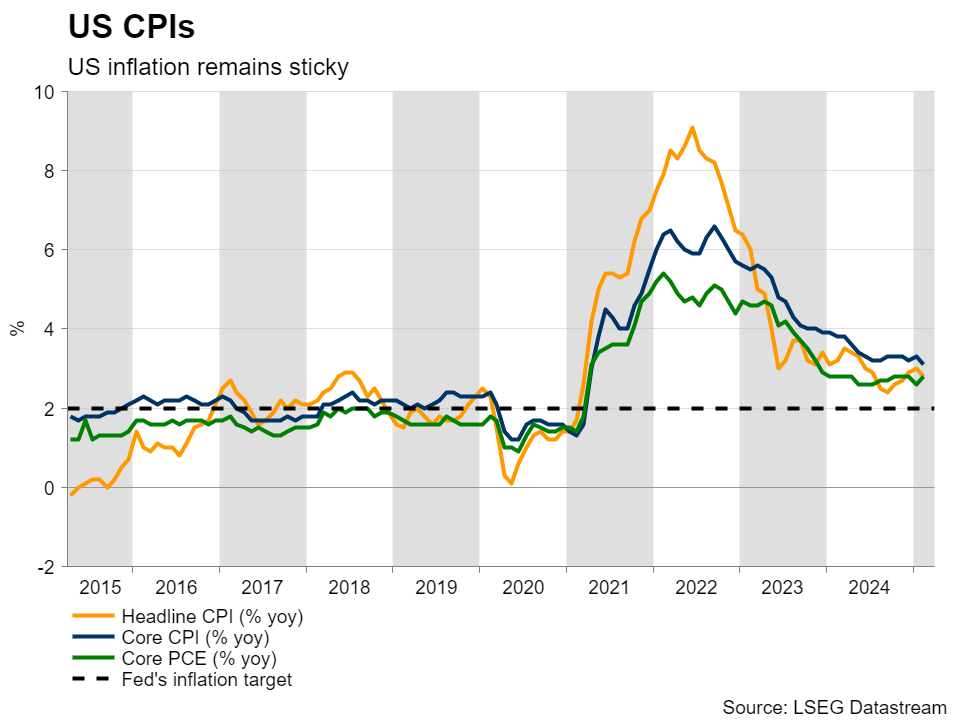

And indeed, with the core PCE price index, the Fed’s favorite inflation metric, surging to 2.8% y/y in February, the path of monetary policy from here onwards is far from being crystal clear. The Fed may find itself between a rock and a hard place. On the one hand, they need to safeguard the economy, and on the other, they need to make sure that inflation does not get out of control again.

Gold could continue exploring uncharted territory

Either way, in the current landscape, it may be a win-win situation for gold. If the Fed decides to hold interest rates steady, investors may become even more worried, as high borrowing costs could be an extra drag for the economy. They could then buy more gold due to its safe-haven status. On the other hand, an accelerating rate reduction process may reduce even further the opportunity cost for holding the precious metal, which is again positive.

The fact the Peoples’ Bank of China (PBoC) continued buying gold in February for the fourth straight month may be another important factor underpinning gold. Chinese officials may be willing to continue adding to their reserves in an attempt to further loosen their dependency to the US dollar in order to minimize the economic damages from an escalating trade war between the world’s two largest economies.

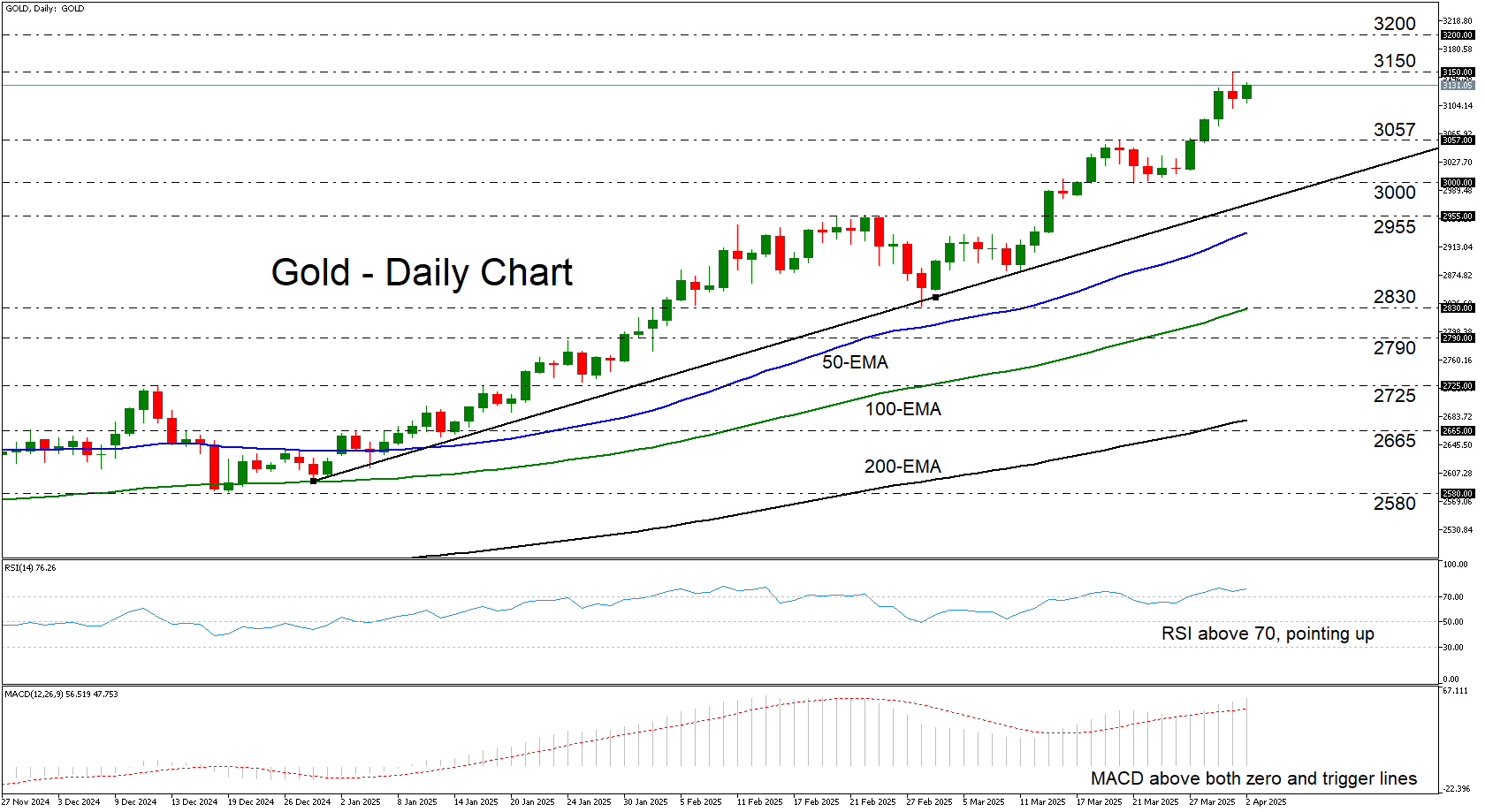

Correction is likely, but broader uptrend remains well intact

From a technical standpoint, gold hit a new record high near $3,150 on April 1, before pulling back. The prevailing uptrend remains well intact and very strong, with both the RSI and the MACD pointing to strong upside momentum.

The announcement of tariffs today and tomorrow may result in a “sell the fact” market reaction, but the uncertainty about Trump’s future trade policies may allow the bulls to jump back into the action from near the $3,067 zone, marked by the inside swing high of March 20. If this is the case, a rebound could aim for another test near the all-time high of $3,150, the break of which could allow extensions towards the $3,200 zone. That zone is the 261.8% Fibonacci extension level of the October 30 – November 14 correction.

For the outlook to start shifting to bearish, a decisive dip below the round number of $3,000 may be needed. Such a move would confirm a lower low on the daily chart, as well as the break below the near-term uptrend line drawn from the low of December 30. This scenario may materialize if Trump’s actions turn out to be way softer than what he initially signalled.

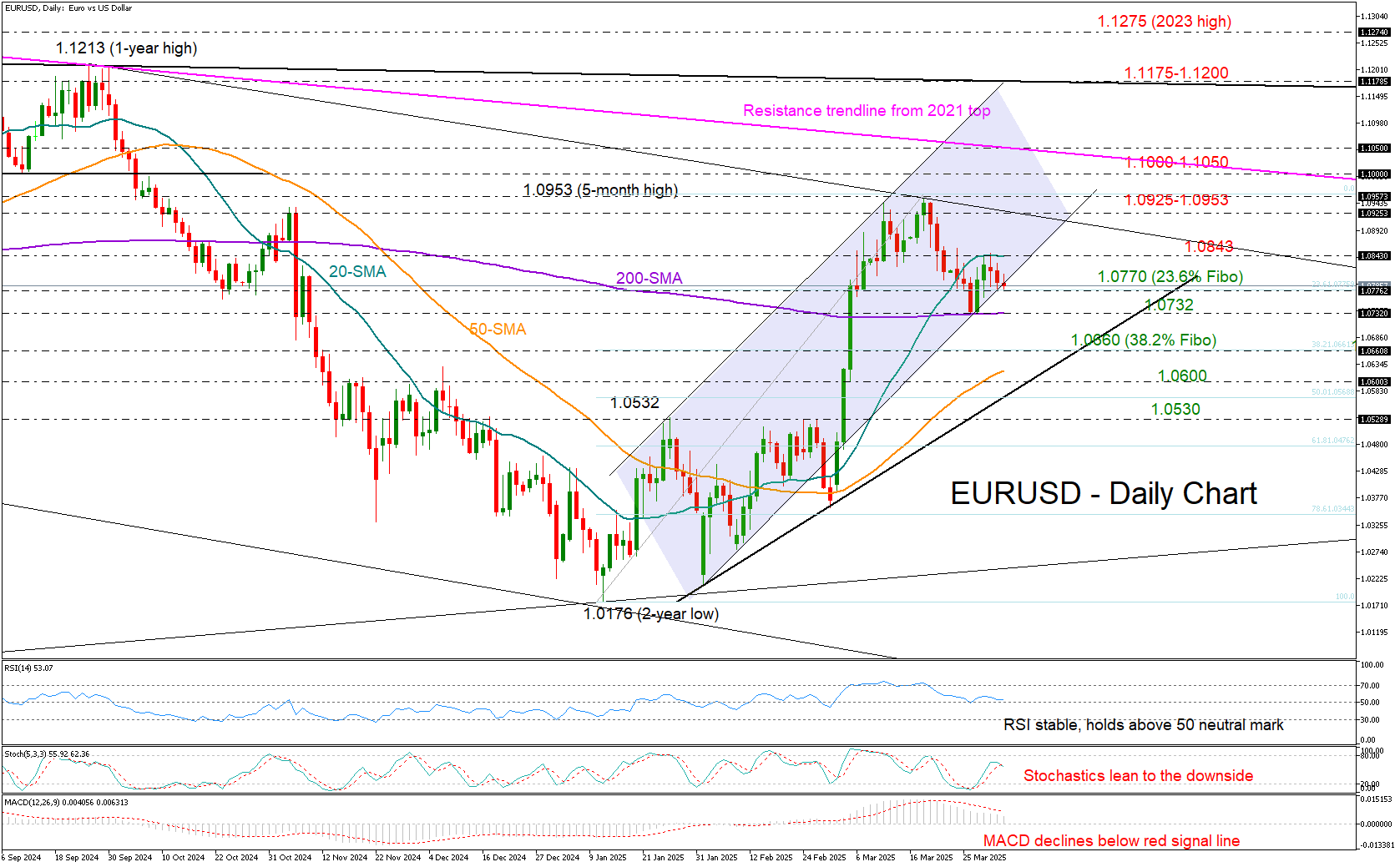

EUR/USD on the Edge as US Tariffs Decision Nears

- EURUSD’s recovery attempt stalls near 20-SMA.

- Short-term outlook is fragile; support at 1.0732-1.0770.

EURUSD held a muted tone, struggling to break past the 1.0800 mark as traders braced for the upcoming US reciprocal tariffs set to be unveiled on Wednesday night. Uncertainty lingers over whether the US president will adopt a conciliatory approach or escalate tensions with a hardline trade stance, potentially igniting fresh concerns in an already fragile geopolitical landscape.

From a technical standpoint, the pair could face renewed downside pressure if support around 1.0770 – where the lower boundary of a bullish channel and the 23.6% Fibonacci retracement level of the latest upward move reside – fails to hold. A sharper bearish signal could emerge if the price dips below the 200-day SMA, which acted as a floor last week at 1.0732. A decisive close beneath this level could activate fresh selling orders, pushing the pair toward the 38.2% Fibonacci retracement at 1.0660 or down to the tentative support trendline near 1.0600. If selling momentum intensifies, the next key destination could be the 1.0530 region.

While the downward tilt in technical indicators sends a cautionary signal, the RSI has yet to cross below its neutral 50 mark, leaving room for a potential rebound. If the price manages to break through resistance at the 20-day SMA around 1.0840, bullish momentum could return, shifting focus toward the 1.0925-1.0950 range. A further advance past this zone would bring the 1.1000-1.1050 resistance area into play, and a breakout here could accelerate gains toward the 2024 highs near 1.1175-1.1200.

In summary, EURUSD remains trapped in a neutral zone, and unless it firmly establishes support above 1.0732, the risk could tilt back to the downside.