Sample Category Title

Tariffs Hit

I won’t make this long or complicated. Trump’s tariff announcement was worse than expected. The universal tariff was set to 10% - in line with expectations - but the tariffs imposed to main trade partners are much higher than that: 34% for China, 20% for Europe and some 24% on Japanese imports. The UK comes out less harmed with a 10% rate, while Vietnam and Lesotho are the hardest hit with tariff rates of 46% and 50% respectively. Of course, Trump said that partners could negotiate with the US to lower these rates, but the tension building into the announcement and the initial shock will be hard to digest for many trade partners and will more likely than not lead to retaliation. China already announced it would restrict investments to the US, Europe already warned there will be retaliation, and Japan said it will protect domestic industries and jobs.

Understandably, the market reaction to the tariff announcement was strongly negative. Vanguard’s S&P500 ETF fell almost 3% in the afterhours trading, the US yields and the dollar tanked, gold and Swiss franc rallied, the USDJPY fell to the lowest levels since November as a result of a swift shift to safety. Crude oil slipped below the $70pb on expectation that the tariffs would hammer global growth and demand, and copper futures – considered as a barometer of global growth - tanked more than 3% after the announcement.

FX markets price retaliation

The pricing in currency markets suggests rising retaliation bets to the US tariffs. The US dollar eased to the lowest level since Trump entered the White House, the lowest levels this year and the lowest levels since mid-October. Not only will the US companies see their costs jump on tariffs – which will boost inflation in the US – but their revenue will probably be hit by retaliatory tariffs as well. The combination of higher inflation – even if it’s transitory – and lower growth will inevitably shake the US exceptionalism. The Federal Reserve (Fed) will have to choose its battle: it will probably choose to support the economy as it considers that the impact of tariffs on inflation would be one-off and short-lived and hopefully partly countered by a sharp economic slowdown. But the supply-chain disruptions could make inflation stickier than expected. If that’s the case, the US will feel the negative impact of tariffs for quite a longtime before it starts seeing any benefits.

Partners will inevitably see their growth impacted, as well. The US tariffs could shave 1% off Eurozone GDP, for example, but the US policies could encourage the European governments to give support to their economies and further ditch whatever is left from the budget discipline. The appreciation of domestic currencies could also help taming inflationary pressures if the US dollar continues to lose value on plunging economic growth in the US.

Indeed, the expectation that the US economy will falter faster than others has been weighing heavily on the US dollar since January. And the tariff announcement sent Cable directly up above the 1.30 psychological mark. The EURUSD trades above the 1.09 level while the USDJPY tanked to 147.

Inside equities, the afterhours trading looked like a bunch of US companies announced disappointing earnings all at once. Apple – that’s still got great exposure to China – tanked more than 7% in the afterhours, Nike also fell by a similar amount, while Nvidia lost more than 5% and Tesla tanked more than 8%.

The futures are deeply in the red with the S&P500 futures pointing at almost 3% losses at the time of writing, while Nasdaq futures point at losses of more than 3%. The European futures are severely down as well, with DAX futures down by nearly 2%. The European exports to the US are seen falling by 50% on tariffs according to Bloomberg analysis.

Interestingly, the Chinese CSI 300 is down by less than 1% (although the Chinese exports to the US are expected to tank by around 80%!).

In the next hours and day, the world’s reaction, likely retaliation and how much effort and money countries will deploy to fight the US back will matter. For now, everyone’s sinking, but the US is going under first.

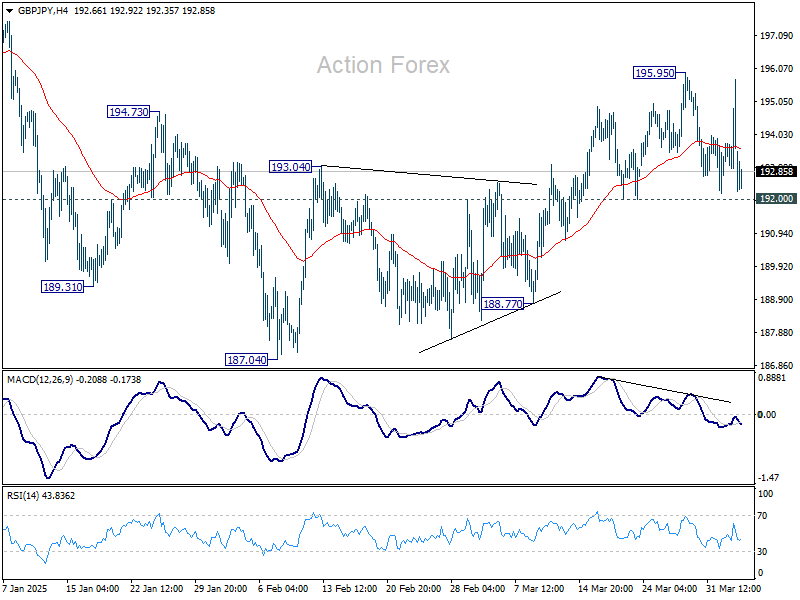

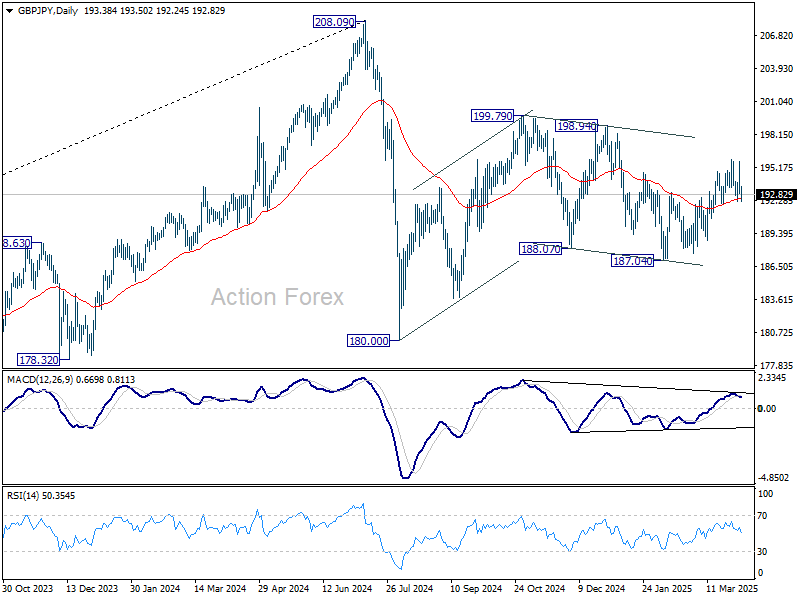

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.90; (P) 194.35; (R1) 195.70; More...

No change in GBP/JPY's outlook as it stays in range below 195.95. Intraday bias remains neutral. On the upside, break of 195.95 will extend the rally from 187.04 once again, to 198.94 resistance. However, firm break of 192.00 support will turn bias back to the downside for deeper fall. Overall, corrective pattern from 180.00 is still extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

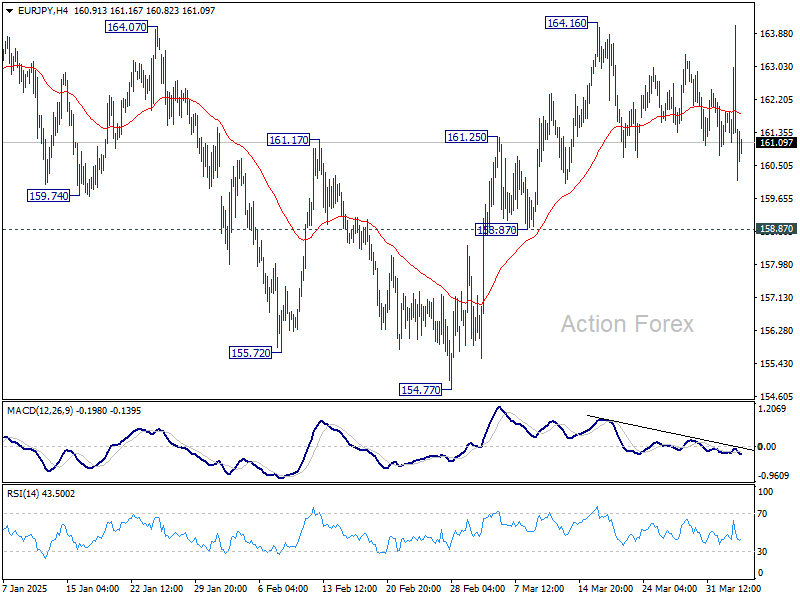

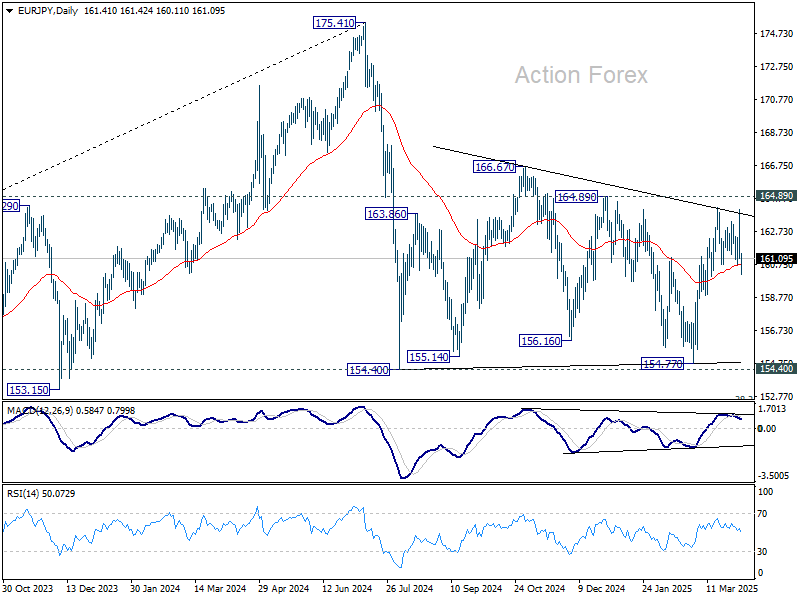

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.82; (P) 162.50; (R1) 163.89; More...

Much volatility was seen in EUR/JPY but it remains largely in range. Intraday bias remains neutral first. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, break of 158.87 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

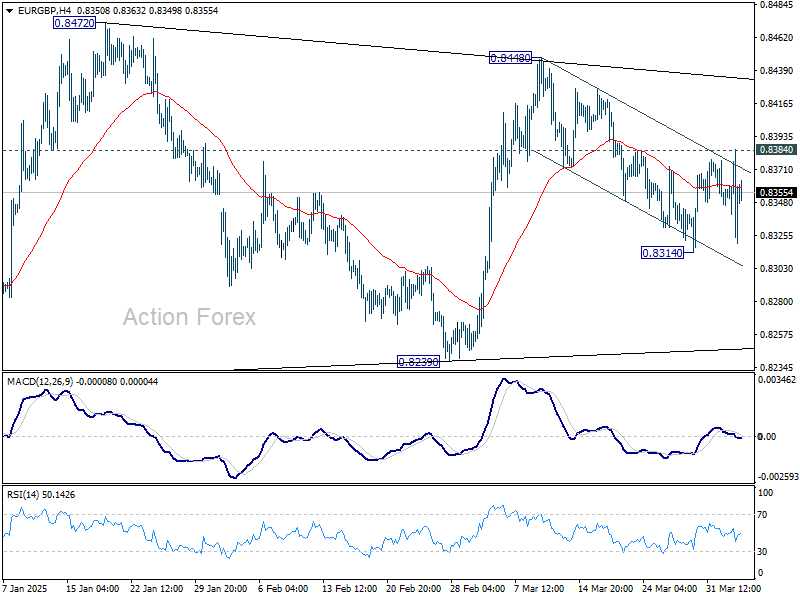

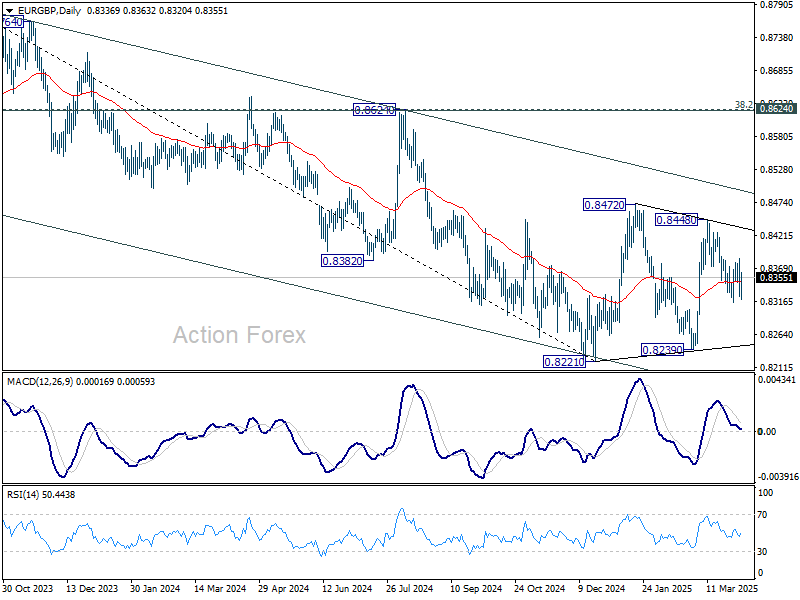

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8320; (P) 0.8354; (R1) 0.8380; More...

EUR/GBP is staying in established range despite some volatility. Intraday bias remains neutral first. On the downside, break of 0.8314 will resume the decline from 0.8448 towards 0.8239 support. Nevertheless, firm break of 0.8384 will argue that fall from 0.8448 is merely a correction and has completed. Retest of 0.8448 should be seen next.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

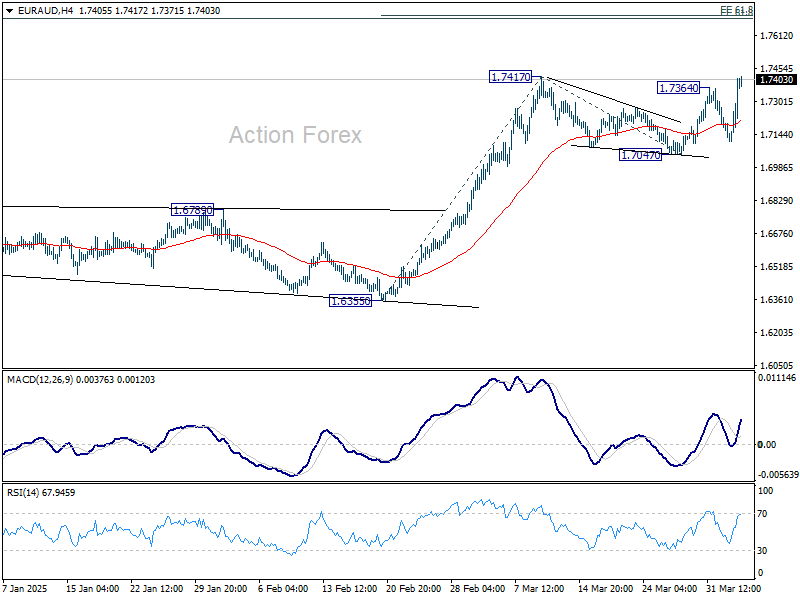

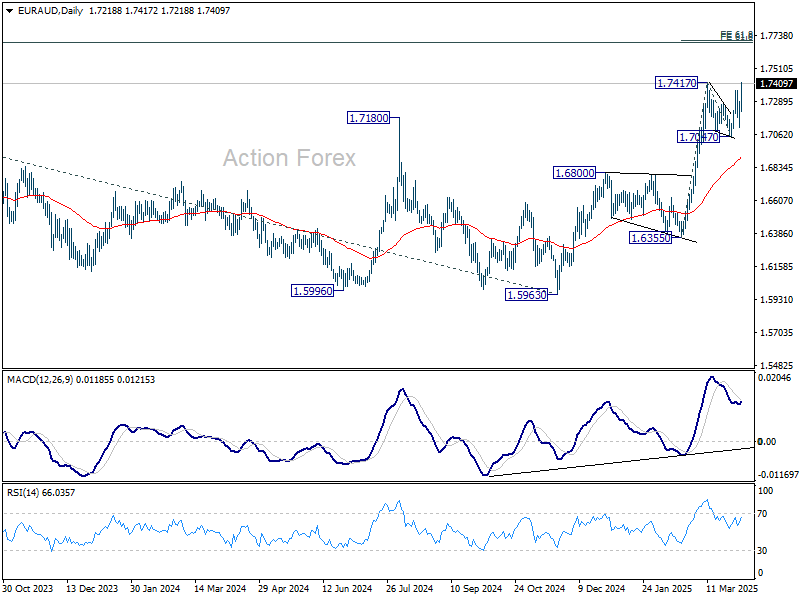

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7138; (P) 1.7217; (R1) 1.7320; More...

EUR/AUD's strong rebound and break of 0.7364 revives the case that consolidation from 1.7417 has already completed at 1.7047. Intraday bias is back on the upside. Firm break of 1.7417 will resume larger up trend, and target 61.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.7703. In any case, outlook will now stay bullish as long as 1.7047 support holds.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming and should target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

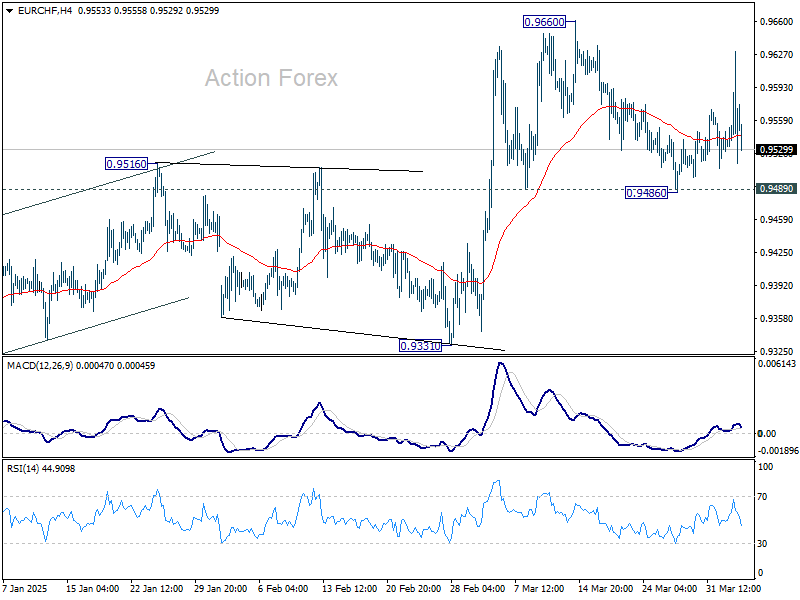

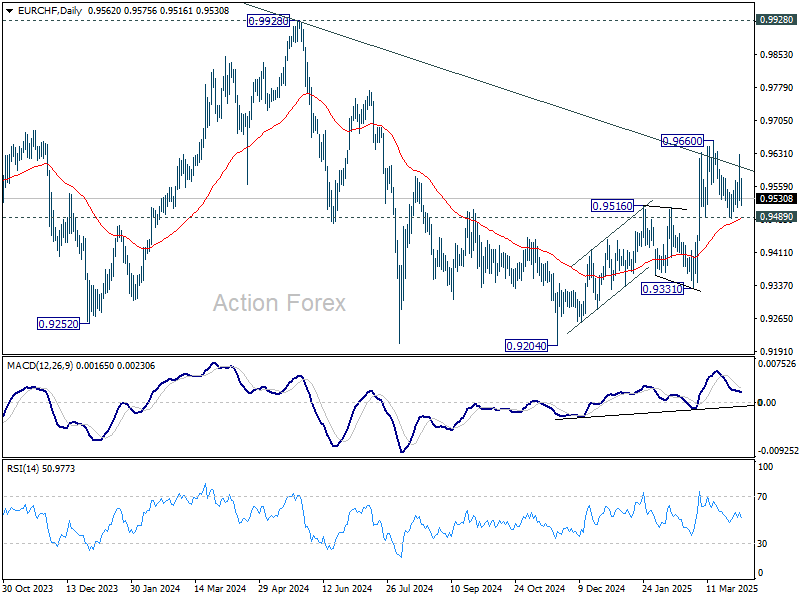

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9519; (P) 0.9576; (R1) 0.9633; More....

EUR/CHF spiked higher to 0.9626 but quickly reversed. Overall, range trading is still in progress and intraday bias remains neutral. On the upside, break of 0.9660 will resume larger rise from 0.9204. However, sustained break of 0.9489 will bring deeper fall back to 0.9331 support next.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9491) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9610) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be seen to 0.9928 key resistance at least.

Interest in the Dollar Declines Amid Trump’s Escalating Trade Wars

The tariffs introduced by Trump yesterday on imports from various countries—20% on the EU, 34% on China, and 46% on Vietnam—have heightened uncertainty in the currency markets. As expected, these measures have contributed to increased volatility in major currency pairs. The actions of the White House administration have led to losses for the dollar, causing concern among investors. The tariffs also affect countries such as Taiwan (32%), Japan (24%), and South Korea (25%), which could significantly impact exchange rates. Amid global economic instability, market participants are focused on how these changes will affect the world economy.

USD/JPY

Yesterday, before Donald Trump's speech, the USD/JPY currency pair was trading near 150.00. Better-than-expected preliminary labour market data and a rise in US industrial orders for February (0.6% versus the forecast of 0.5%) contributed to a slight strengthening of USD/JPY. However, the US President’s announcement of trade tariffs led to sharp market fluctuations and a loss of more than 150 pips for USD/JPY within just a few hours. At present, the pair is trading below 148.00. A technical analysis of USD/JPY suggests a possible test of this year's March lows in the 147.20–146.70 range.

Key events that could influence USD/JPY today:

- 13:00 (GMT+2): OPEC meeting (USA)

- 14:30 (GMT+2): Challenger job cuts report (March) (USA)

- 15:30 (GMT+2): Total number of unemployment benefit recipients (USA)

- 15:30 (GMT+2): Export and import volume (February) (USA)

USD/CAD

The news of tariffs enabled USD/CAD sellers to break below the lower boundary of the medium-term flat corridor 1.4470–1.4260. If the 1.4260 level turns into a support level, a test of this year's February lows around 1.4150 could be expected. A reversal of the downward scenario would be possible if the price strengthens confidently above 1.4470.

Key news that could impact USD/CAD pricing:

- 15:30 (GMT+2): Export volume (February) (Canada)

- 15:30 (GMT+2): Trade balance (Canada)

- 16:45 (GMT+2): Composite PMI by S&P Global (March) (USA)

- 16:45 (GMT+2): Services PMI (March) (USA)

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Stronger and Broader US Tariffs Than Expected

In focus today

In the US, the ISM March Services Index is due for release in the afternoon. Its PMI-counterpart released earlier pointed towards a more positive outlook despite the tariff uncertainty. We will also keep an eye out for the March Challenger Report on layoff announcements. While usually not a market mover it could provide further clarity on the scale of DOGE's federal layoffs.

In the euro area, we receive the final March PMIs. In the past months, the final PMIs have shown unusual revisions of the flash release, which makes them more important to follow. Also in the euro area, we will scrutinize the minutes from the March ECB meeting for any hints of what to expect at the April meeting.

In Sweden, services and composite PMIs are due for release today. The consensus view is for a roughly unchanged figure compared to last month's numbers, like Monday's manufacturing PMI. Furthermore, Riksbank Governor Thedéen participates in a panel discussion regarding EU capital markets. As such, Swedish monetary policy is unlikely to be discussed at length, but there might still be the odd titbit worth keeping an eye out for.

Economic and market news

What happened overnight

In the US, Donald Trump presented a range of new, country-specific tariffs on "Liberation Day". In a move that has resulted in confusion as to the exact country-specific rates, Trump announced tariff rates ranging from 10-60%, depending on the country, with a 10% universal tariff alongside the country-specific duties. The new tariffs were generally stronger and broader than we and markets expected, and sent shockwaves through global markets amid worries that the aggressive duties will slow growth, hit corporate earnings, and increase inflation.

In China, the Caixin PMI services, which is the private survey, surprised to the upside as it rose to 51.9 in March from 51.4 in February. This was mainly driven by increases in domestic demand, as both business activity and new orders picked up and contributed to the strongest growth in the services sector since December.

What happened yesterday

In Denmark, Nationalbanken's (NB) currency interventions in March were released. In line with expectations, NB did not intervene in the foreign exchange market, thereby marking the 26th consecutive month without intervention.

In Poland, the Polish central bank (NBP) kept the leading interest rate unchanged at 5.75%, in line with consensus. We will have to await Governor Glapinski's press conference, scheduled at 15.00 CET today, for more information regarding the NBP's view on rates going forward.

Equities: Asian stock markets are lower this morning, with Japanese markets hit hardest as the currency strengthens as Japan is set to face a 24% tariff. European futures are down as well, while US markets are experiencing the most significant decline due to this massive implicit tax hike for US consumers. The cross assets playbook this morning aligns closely with what we have observed in the trade war escalation over the last one and a half months.

FI&FX: The rumours of soft tariffs ahead of the press conference that gave a lift to equities and US yields going into the press conference proved to be wrong. The outcome was worse than expected and it raises the risk for a US recession. Equity futures plunged with S&P 500 and Nasdaq indicating a deep-red opening. Nikkei is down 3.5%. US treasuries rallied across the curve while the 2s and the 10s are off some 15bp from yesterday's highs. The USD is generally weaker. USD/JPY loses 2% overnight and trades close to 147. EUR/USD adds to initial gains and breaches 1.09. Scandi FX is caught by opposing forces following the Trump announcements: a higher probability of a US recession (negative) vs higher appeal of non-US assets (positive). EUR/SEK at 11.75 and EUR/NOK 11.33.

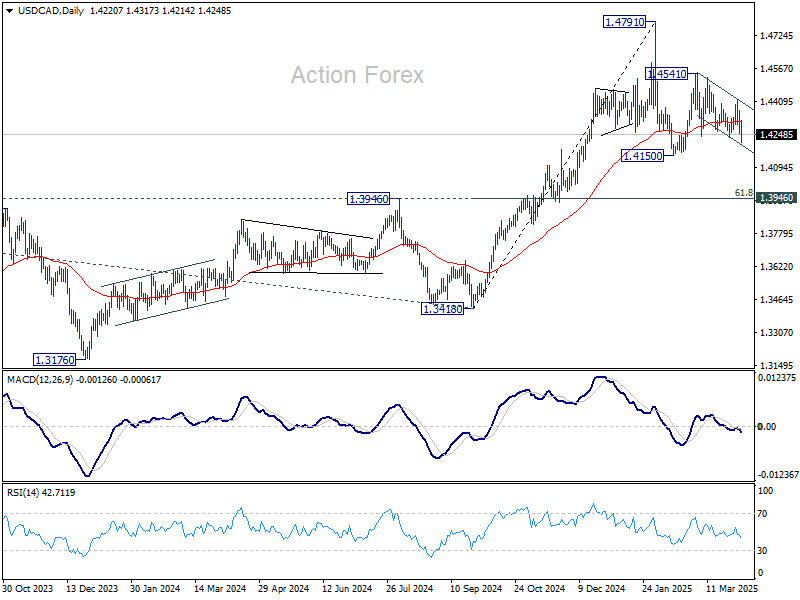

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4264; (P) 1.4339; (R1) 1.4380; More...

Intraday bias in USD/CAD is back on the downside with breach of 1.4234 support. Deeper fall would be seen to 1.4150 low. Overall, corrective pattern from 1.4791 is still extending. Firm break of 1.4150 will confirm the start of the third leg towards 1.3946 cluster support. On the upside, break of 1.4414 will argue that the pattern is still in the second leg. Intraday bias will be turned back to the upside for 1.4541 resistance first.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

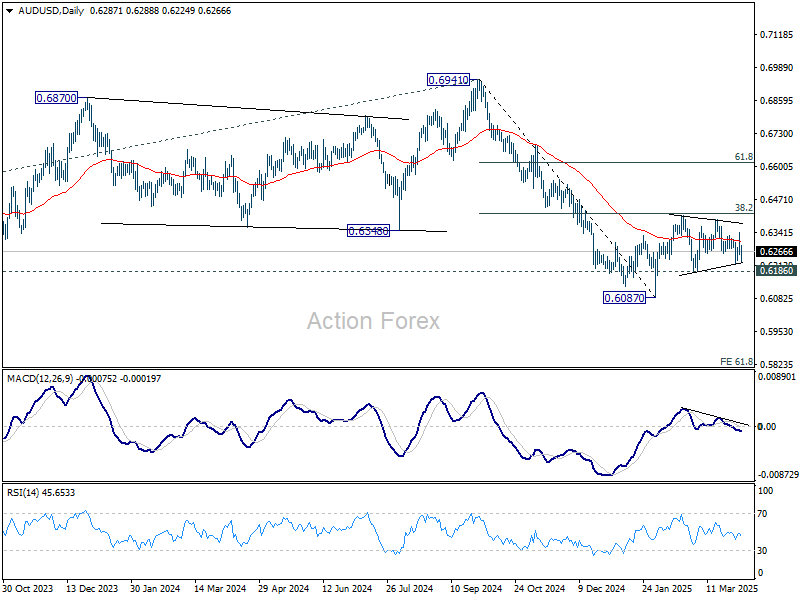

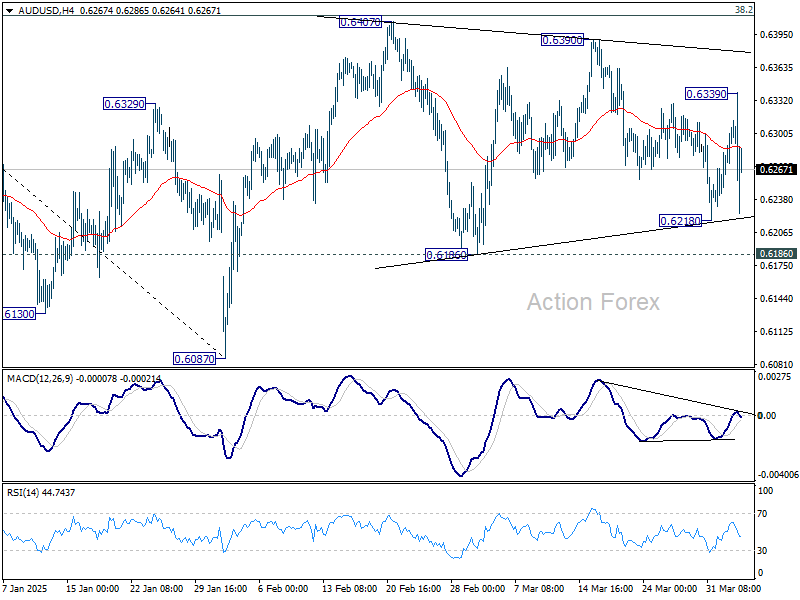

AUD/USD Daily Report

Daily Pivots: (S1) 0.6258; (P) 0.6299; (R1) 0.6341; More...

AUD/USD spiked higher to 0.6339 but quickly reversed. Intraday bias stays neutral for the moment. On the downside, break of 0.6218 will target 0.6186 support first. Firm break there will indicate that corrective pattern from 0.6087 has completed and larger fall from 0.6941 is ready to resume. However, break of 0.6339 will bring stronger rise back to 0.6390/6407 resistance zone instead.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6461) holds.