Sample Category Title

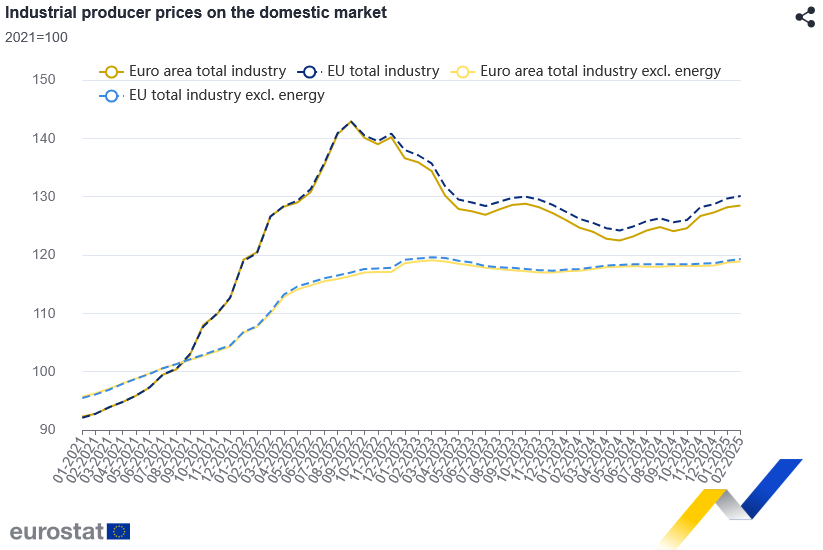

Eurozone PPI rises 0.2% mom, 3.0% yoy in Feb

Eurozone PPI rose 0.2% mom and 3.0% yoy in February. The monthly gain was primarily driven by a 0.4% mom increase in prices for intermediate goods, alongside smaller rises in energy (0.2% mom) and capital goods (0.2% mom) prices. Prices for durable consumer goods slipped slightly, down -0.1% mom, while non-durable consumer goods posted a mild 0.1% mom uptick. Excluding energy, total industrial prices increased by 0.2% mom.

Across the broader EU, PPI rose 0.3% mom on the month and 3.1% yoy. The strongest monthly gains were recorded in Estonia (+9.5%), Romania (+4.8%), and Bulgaria (+2.5%), while declines were seen in Ireland (-4.9%), France, and Slovakia (both -0.8%).

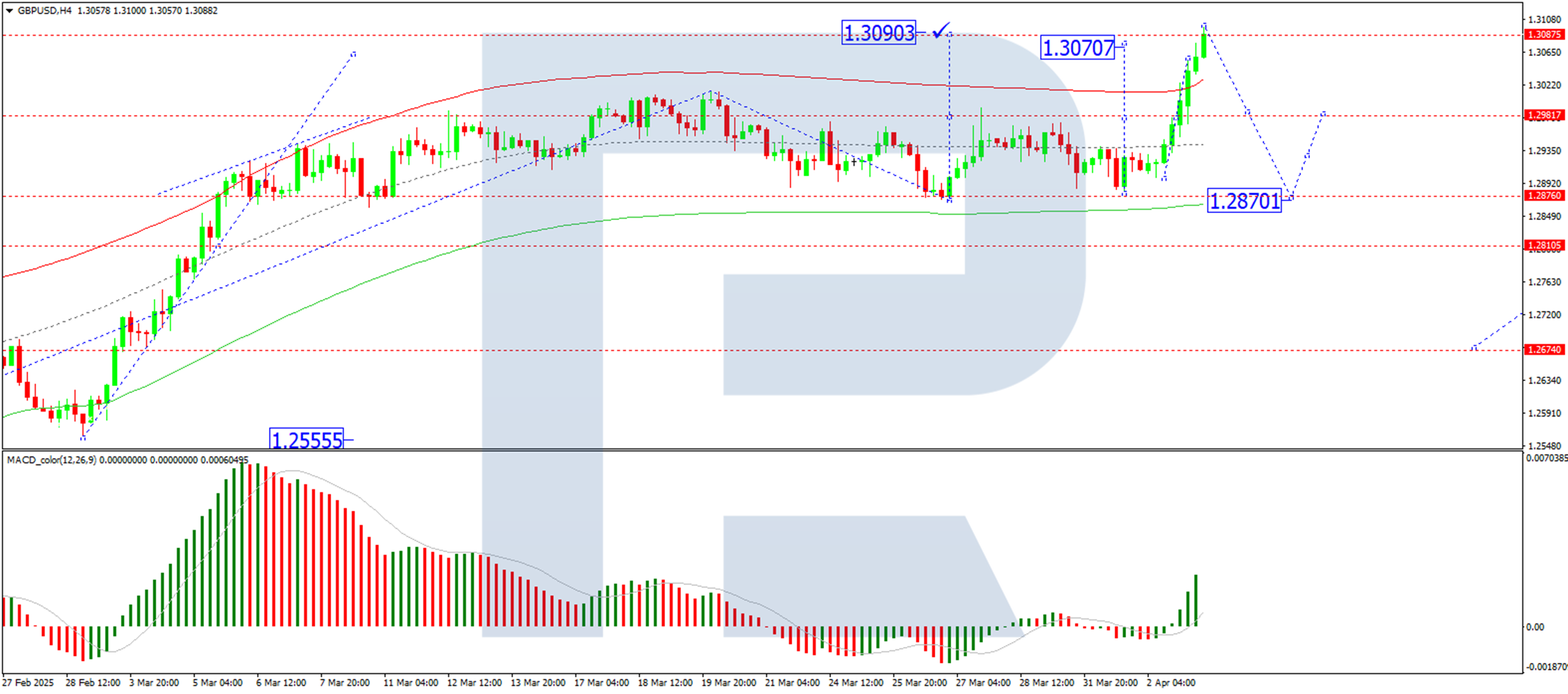

GBP/USD Hits 21-Week High: The Pound Outperforms Its Peers

The GBP/USD pair climbed to 1.3064 on Thursday, marking a 2.46% gain over the past four weeks and a 2.87% increase against the US dollar over the last 12 months. The British pound continues to strengthen, outperforming many of its major counterparts.

Key factors driving the GBP/USD rally

The UK is closely monitoring developments in US tariffs, which could have significant implications for its economy. While the new tariffs potentially threaten global trade, the UK remains in a relatively favourable position compared to the EU, Canada, China, and Mexico.

Reasons for the UK’s advantage:

- The US baseline tariff rate for the UK is just 10% – the lowest among major US trading partners

- The UK’s trade relationship with the US is relatively balanced, with a smaller share of reciprocal trade, reducing immediate risks

However, uncertainty looms. Policymakers anticipate a possible reversal of US tariffs, but the broader impact remains unpredictable, whether on inflation, global GDP, or trade dynamics.

Technical analysis of GBP/USD

H4 chart perspective

- The pair has broken through 1.2988, surging towards 1.3095

- A pullback to retest 1.2988 (now acting as support) could occur before another upward push towards 1.3103.

- MACD confirmation: the signal line remains above zero and is trending upwards, supporting bullish momentum

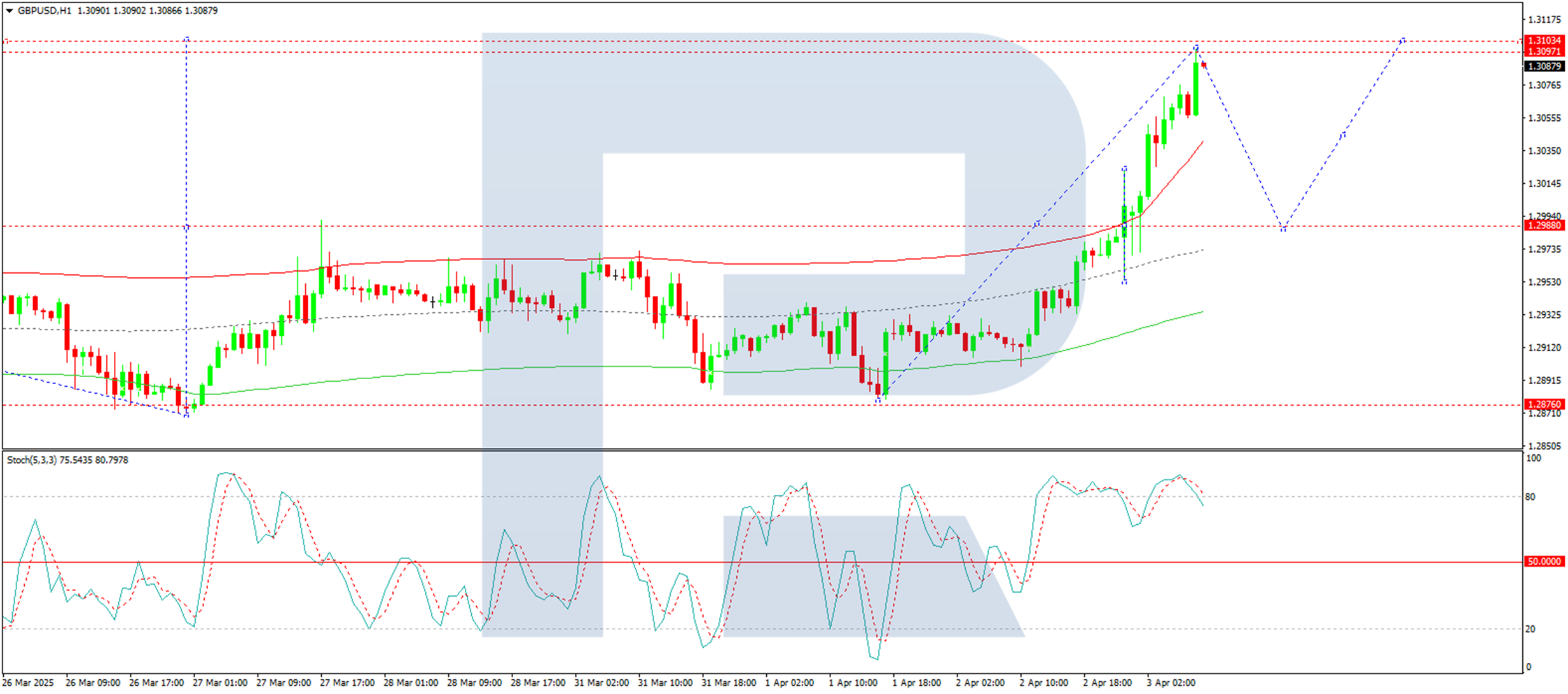

H1 chart perspective

- After consolidating around 1.2988, the pair broke higher, targeting 1.3095

- Once this level is reached, a correction back to 1.2988 could follow

- Stochastic indicator: the signal line is above 80 but turning downwards, suggesting a potential near-term exhaustion.

Conclusion

The pound’s resilience against the dollar reflects both fundamental strength and technical momentum. While the UK benefits from a less exposed trade stance, traders should watch tariff developments and key technical levels to gauge the next significant move.

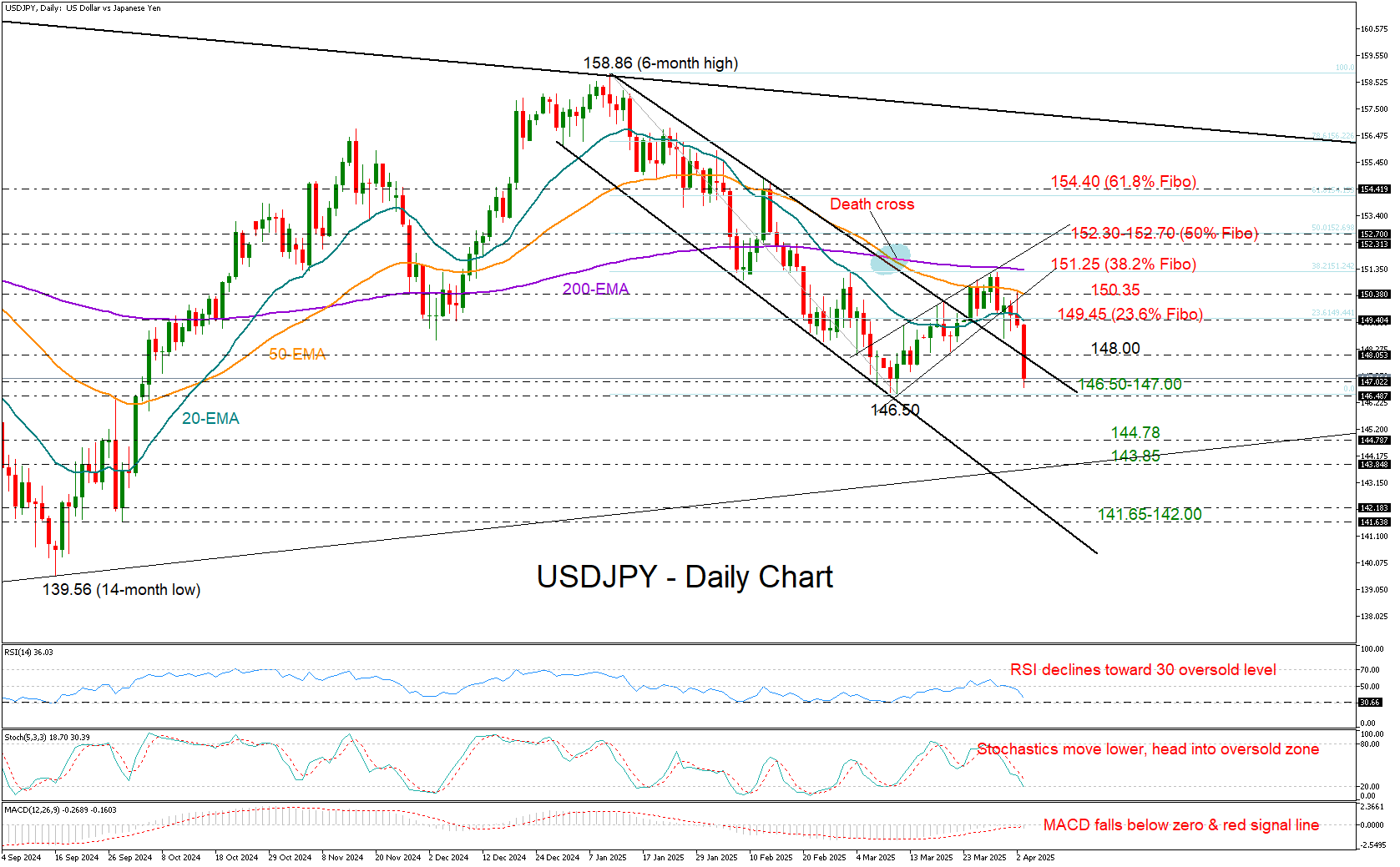

USD/JPY Sinks as US Tariffs Cause Headache

- USDJPY loses 1.7% as US tariffs stress investors.

- Short-term outlook becomes gloomier.

- More losses expected below 146.50.

USDJPY slumped to 147.79, experiencing its worst daily drop (-1.7%) since the summer of 2024, as Trump's reciprocal tariffs turned out stricter than expected in some regions, including China. This development has heightened investor concerns over the implications of US trade policy.

With attention shifting to potential retaliatory actions against the US, USDJPY may struggle to find support. However, sellers will wait for a close below 147.00 and the March low of 146.50 to reinforce a bearish outlook. In this case, the pair could undergo an aggressive decline toward 143.85, unless the 144.78 territory provides a footing beforehand. A deeper drop could push the price into the 141.65–142.00 constraining zone, last seen in September 2024.

The short-term risk has deteriorated as the technical indicators drifted lower, with the MACD falling below its red signal line in the negative area and the gap between the 50-day and 200-day exponential moving averages (EMAs) further widening following the death cross, the price could stay trapped in a bearish trajectory.

However, a temporary pause in the decline cannot be ruled out in the coming sessions, as the RSI and stochastic oscillator approach oversold levels. If the price manages to hold above the upper boundary of the bearish channel near 148.00, a rebound could retest the 20-day EMA at 149.45. Additional increases from there may encounter resistance at the 50-day and 200-day EMAs at 150.40 and 151.25, respectively. Beyond that, the recovery phase could stall near the 152.30 barrier.

In summary, USDJPY may face challenging sessions ahead, with further losses anticipated once the bears break below 146.50. Conversely, a close above 148.00 could generate fresh upside momentum.

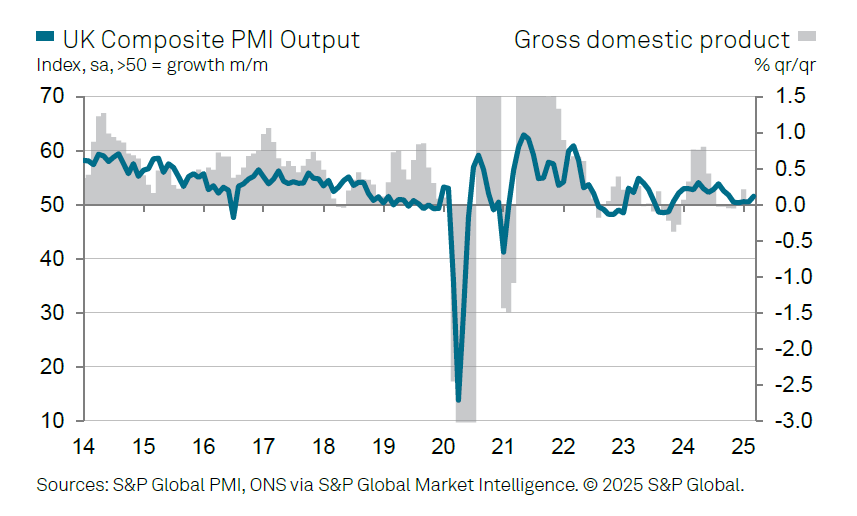

UK PMI services finalized at 52.5, outlook and employment subdued

UK PMI Services was finalized at 52.5 in March, up from 51.0 in February, marking the highest level since August 2024. PMI Composite also improved to 51.5, a five-month high.

The modest recovery in overall business activity was driven primarily by strength in the technology and financial services sectors, according to Tim Moore at S&P Global. However, this was offset by notable weakness in manufacturing, which experienced its steepest decline in output since October 2023.

However, service providers expressed limited optimism about the near-term outlook, with confidence levels hovering near two-year lows. The labor market also continued to show signs of strain, with March marking the sixth consecutive month of job losses due to hiring freezes and redundancies.

Price pressures remain a concern. The inflation indicators within the survey suggest that cost and pricing pressures in the services sector are still running significantly hotter than the pre-pandemic decade.

USD/CHF Falls to Its Lowest Level in Nearly Five Months

Today, the exchange rate of one US dollar against the Swiss franc dropped below 0.87000 francs—its lowest level since early November 2024.

Since the start of 2025, the USD/CHF pair has declined by more than 4%.

Why Is USD/CHF Falling Today?

On one hand, the US dollar is weakening against other currencies due to Trump’s decision to implement the previously announced tariffs on international trade, as mentioned in our previous post.

On the other hand, the Swiss franc is gaining strength due to its appeal as a safe-haven asset. Furthermore, this morning’s release of the Consumer Price Index (CPI) showed that inflation in Switzerland remains at zero, increasing the franc’s value at a time when tariff conflicts pose risks to the global economy.

Technical Analysis of the USD/CHF Chart

Since the start of 2025, the USD/CHF pair has been following a downward trajectory, highlighted by a declining channel (marked in red), with the following key points:

→ The median line has shifted from support to resistance, as indicated by the arrows.

→ The price broke through the March support level around 0.8757, accelerating the decline.

→ The lower boundary of the channel provided support this morning, slowing bearish momentum.

It is possible that the 0.8757 level will act as resistance in April 2025. However, the future direction of USD/CHF will largely depend on news developments, particularly statements from global leaders regarding tariffs in international trade.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

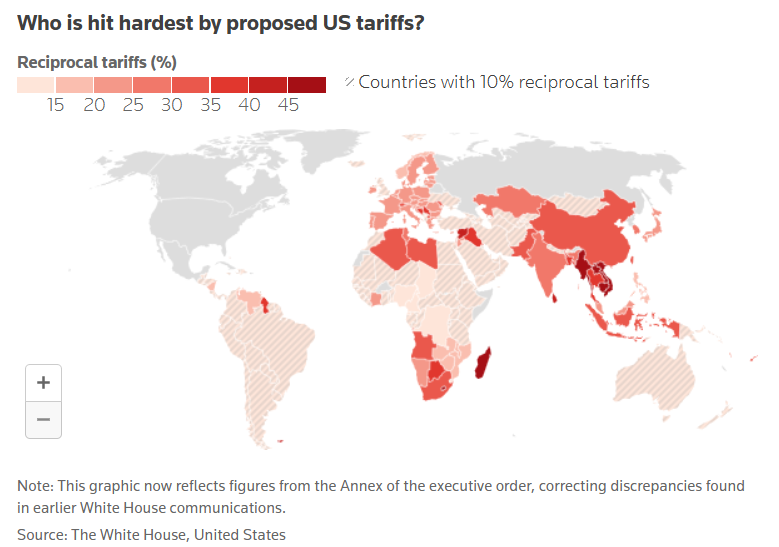

S&P 500 Index Hits 2025 Low Following Trump’s Tariff Announcement

As shown on the S&P 500 Index (US SPX 500 mini on FXOpen) chart, the benchmark US stock index dropped below 5,450 points for the first time in 2025. This decline reflects the US stock market’s reaction to the tariffs imposed by the White House on international trade.

According to Reuters:

→ President Donald Trump announced a 10% tariff on most goods imported into the United States, with Asian countries being hit the hardest.

→ This move escalates the global trade war. "The consequences will be devastating for millions of people worldwide," said European Commission President Ursula von der Leyen, adding that the 27-member EU bloc is preparing to retaliate if negotiations with Washington fail.

Financial Markets’ Reaction to Trump’s Tariffs

→ Stock markets in Beijing and Tokyo fell to multi-month lows.

→ Gold hit a new all-time high, surpassing $3,160.

→ The US dollar weakened against other major currencies.

The S&P 500 Index (US SPX 500 mini on FXOpen) is now trading at levels last seen in September 2024, before Trump's election victory.

Investor sentiment appears to have turned bearish, with growing concerns over the impact of Trump's tariffs, as fears mount that they could slow down the US economy and fuel inflation.

Technical Analysis of the S&P 500 Index (US SPX 500 mini on FXOpen)

The bearish momentum seen yesterday signals a continued correction, which we first identified in our 17 March analysis.

At that time, we mapped out a rising channel (blue) that began in 2024, suggesting that selling pressure might ease near its lower boundary. However, Trump's policy decision has reinforced bearish confidence, and now the price may continue fluctuating within the two downward-sloping red lines. This suggests that the long-term blue growth channel is losing its relevance.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

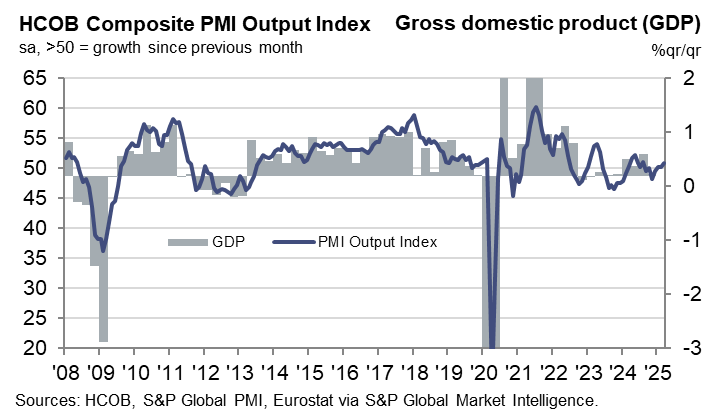

Eurozone PMI composite finalized at 50.9, steady but shaky

Eurozone’s private sector continued to show signs of stabilization in March, with PMI Composite finalized at 50.9 — the highest in seven months — up from February's 50.2. PMI Services was finalized at 51.0, up from prior month's 50.6.

Among the major economies, Germany stood out with a 10-month high at 51.3, while France remained in contraction despite improving to a five-month high at 48.0.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, acknowledged that recession fears that loomed late last year are now giving way to cautious optimism. The Eurozone has managed to stay in growth territory for three straight months.

Still, he warned that this fragile recovery could be easily thrown "off course again" by external shocks — namely, the newly announced US reciprocal tariffs.

ECB’s Nagel and Stournaras warn of economic fallout from US tariffs

Bundesbank President Joachim Nagel issued a strong warning today, saying the US administration's new tariff measures "endanger global economic stability."

Nagel emphasized the need for strong alliances and fewer trade barriers to tackle today’s global challenges, adding that the US is pursuing a "completely different direction" with economic policies that could leave many losers—especially within its own borders.

Echoing these concerns, Greek ECB Governing Council member Yannis Stournaras said the US tariffs are expected to weigh on Eurozone GDP growth rate by 0.3% to 0.4% in the first year, though he noted that the broader inflation outlook remains unaffected.

Stournaras added that the US tariffs were “not an obstacle” to an ECB rate cut in April.

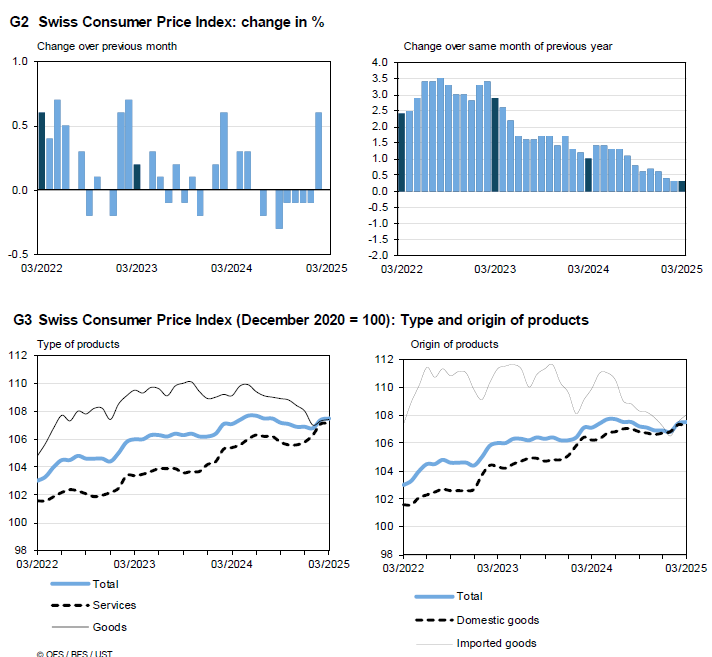

Swiss CPI unchanged at 0.3% yoy in Mar, misses expectations

Swiss consumer inflation remained subdued in March, with headline CPI unchanged on the month, below the expected 0.1% mom rise. Core CPI (excluding fresh and seasonal products, energy and fuel) rose just 0.1% mom. The breakdown showed a -0.1% mom decline in domestic product prices, offset somewhat by a 0.5% mom rise in prices of imported products.

On an annual basis, headline CPI held steady at just 0.3% yoy, missing expectations for an uptick to 0.5% yoy. Core inflation also remained unchanged at 0.9% yoy. The slight increase in domestic product inflation from 0.9% yoy to 1.0% yoy suggests some persistence in local cost pressures. But overall imported inflation remains deeply negative at -1.7% yoy, down from -1.5% yoy.

By Keeping Threat of Even Higher Tariff Rates Alive, We Enter a Prolonged Period of Uncertainty

Markets

The US government published the groundwork of its new trade policy. The baseline is a 10% across-the-board levy on all imports, effective April 5th. The tariff rate is higher for countries who charge the US more than 20% (including FX manipulation and trade barriers; based on calculations by the US administration). In those cases, the US from now on charges discounted reciprocal tariffs (on top of existing tariff rates) amounting to approximately half of the tariffs charged to the US. In case of the European Union, the White House calculated an average 39% tariff rate charged to the US, translating into a discounted reciprocal tariff of 20%. The reciprocal tariffs take effect April 9th. Ahead of the announcement, Treasury Secretary Bessent told lawmakers that tariffs are a cap and that countries can take steps to push them down. However, the reference to “discounted” reciprocal tariffs suggests that the US government has leeway to move levels in both directions with the universal rate being a floor and the White House’s calculated tariff rate to the US (including FX manipulation and trade barriers) being the real cap (ie double the current discounted reciprocal tariff rate). It will be interesting to see whether and how fast the needle moves if countries threaten to retaliate. The EU for now framed it as “preparing for further countermeasures to protect our interests and our businesses IF negotiations fail”.

The initial market response is risk-off with stock futures sinking 2%-3% and core bond futures rallying. By keeping the threat of even higher tariff rates alive, we enter a prolonged period of uncertainty which can further damage (risk) sentiment. The new trade paradigm is expected to both raise inflation (short term) and hit growth (medium term). Up until now, the Fed prioritized upside inflation risks over downside growth risks. That’s still our main scenario, with Fed Chair Powell speaking about the economic outlook tomorrow evening. The market reaction is one with the onus on the “STAG” rather than the “FLATION” part of the story. It helps explaining new USD-weakness, propelling EUR/USD from the 1.08 area to intermediate resistance (YtD top) at 1.0955. We still target a return to 1.1214. The trade-weighted dollar (DXY; 102.80) already lost support (YtD low) at 103.20, paving the way for full technical retracement towards the 2024 low at 100.16. Risk-off outweighs a 24% Japanese reciprocal tariff rate with USD/JPY falling from 149+ to 147. China gets slapped with an additional 34% rate on top of the 20% already in place, hurting CNY. USD/CNY rises from 4.27 to 4.2950, approaching the YTD high around 7.33 (weakest CNY-levels since 2007). More short term volatility will obviously be name of the game with the dust still settling and awaiting the reaction function of nations and the US going forward from the current set-up. In order to restore some market equilibrium, much will probably depend on how “final” current announced tariff rates are.

News & Views

The National Bank of Poland yesterday left its policy rate unchanged at 5.75%. This level is still deemed conductive to meeting the NBP’s (2.5%) inflation target. However; the NBP acknowledged recent softer than expected inflation, even as inflation still remains elevated due to implemented increases in administered prices. Inflation in the first quarter was 4.9%, while the NBP expected it to peak at 5.4%. The NBP still sees wage growth running at a high level, but enterprise data point to lowering wage growth. Q1 activity also was weaker than expected. The NBP expects inflation to remain above the NBP target ‘in the coming months’ (was ‘this year’ in the March statement). In the second half of 2025 there will be a further rise in regulated energy prices. The NBP signals uncertainty on how ongoing high inflation will affect inflation expectations and wages. Despite the softer bias in the MPC statement, the Polish 2-y swap yield rose marginally (4.85%). The zloty strengthened from the EUR/PLN 4.18+ area to close near 4.17. Recently some members opened the debate on the timing of a first rate cut. However, governor Glapinski didn’t see room for rate cuts anytime soon. He will address the press this afternoon.

US Senate Republicans published a budget blueprint that should lay the groundwork for the 2017 Trump tax cuts at about $4tn to be extend and include additional tax reductions of $1.5tn. The proposal also aims to raise the debt ceiling by $5tn. The proposal is planned to be presented for a vote later this week. It then still needs to be brought in line with a House proposal and while reaching an agreement on necessary spending cuts as well. The nonpartisan Committee for a Responsible Federal Budget estimates the Senate budget measure could add about $5.8tn to the US debt in the next decade.