Sample Category Title

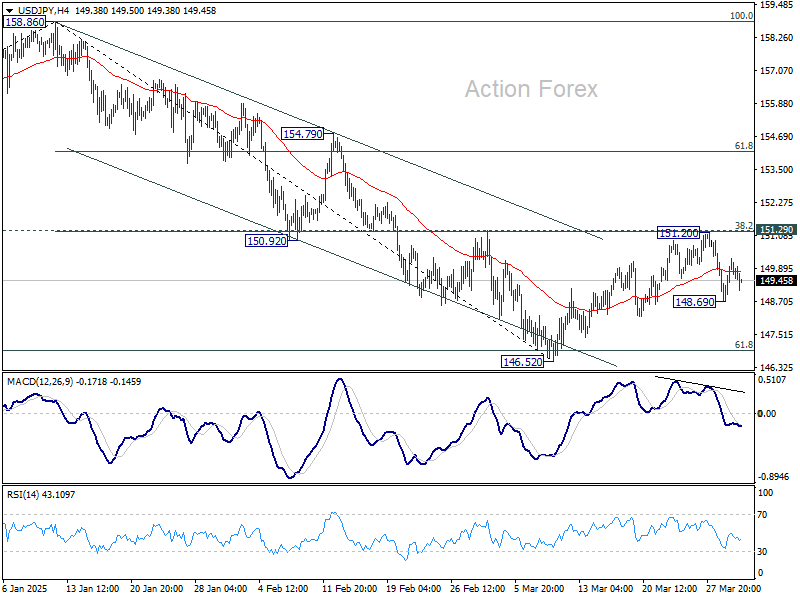

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.02; (P) 149.65; (R1) 150.59; More...

Intraday bias in USD/JPY remains neutral at this point. Outlook is unchanged that corrective rise from 146.52 has completed at 151.20. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

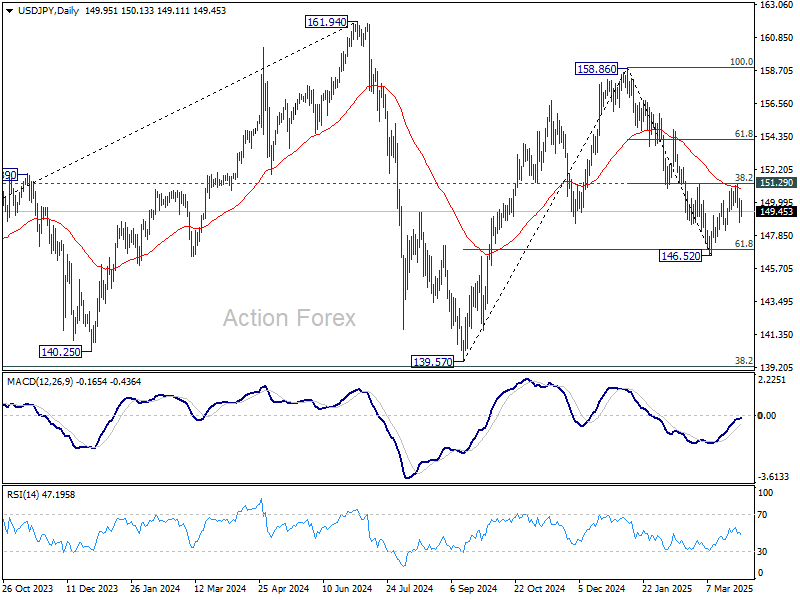

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

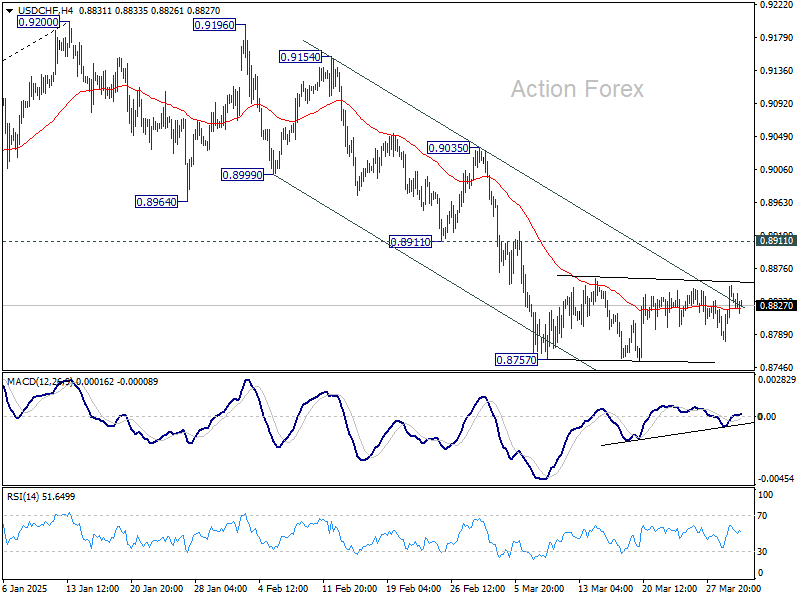

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8798; (P) 0.8827; (R1) 0.8873; More…

Intraday bias in USD/CHF remains neutral as consolidation form 0.8757 is still extending. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

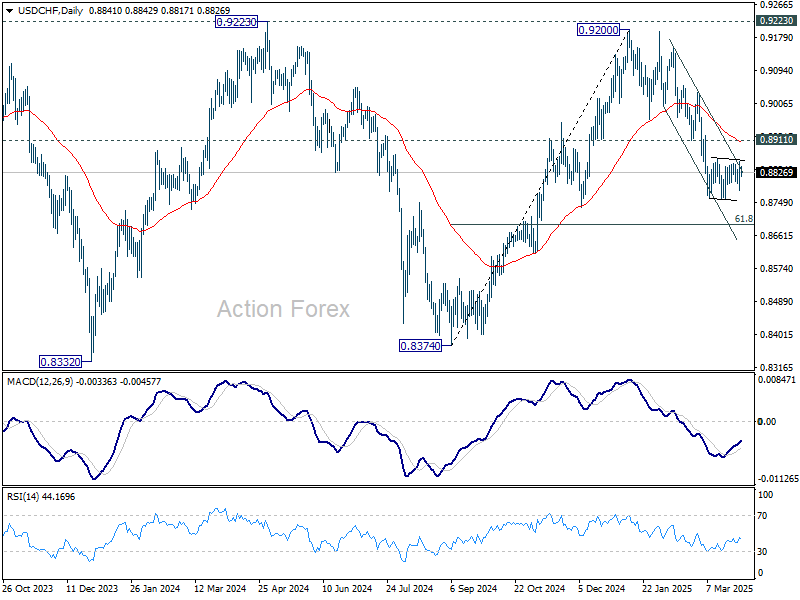

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

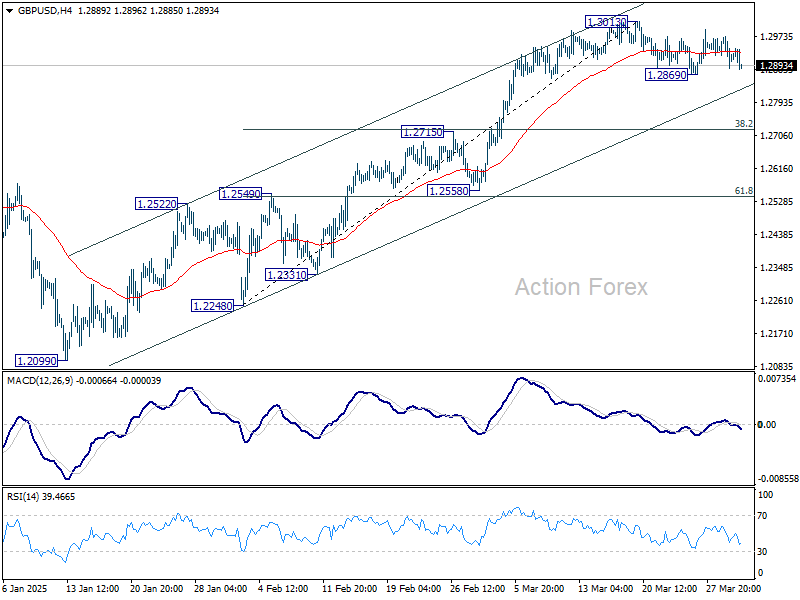

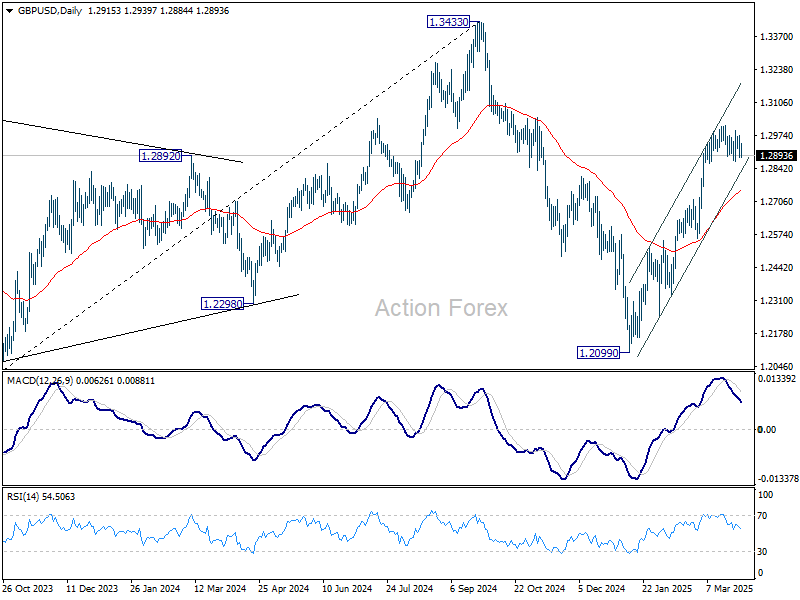

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2879; (P) 1.2925; (R1) 1.2964; More...

No change in GBP/USD's outlook and intraday bias stays neutral. On the downside, below 1.2869 will bring deeper correction. But downside should be contained above 38.2% retracement of 1.2248 to 1.3013 at 1.2721. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

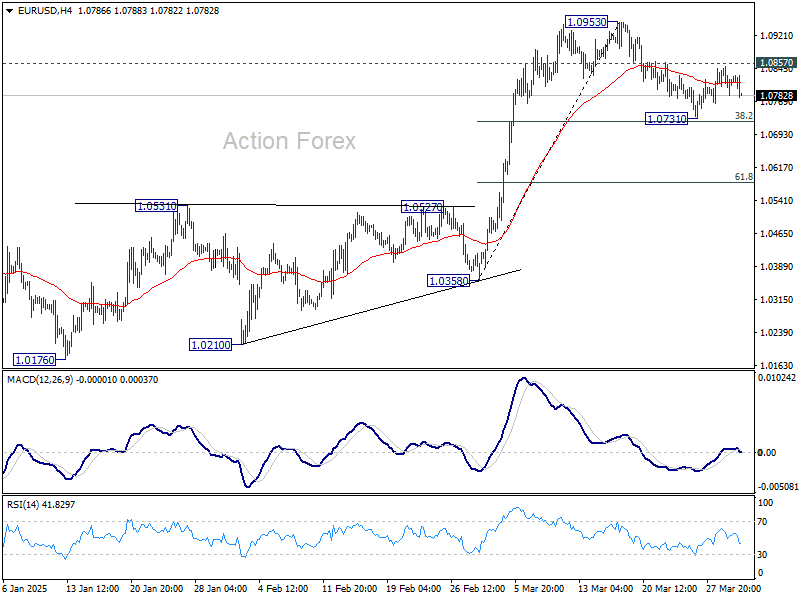

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0816; (R1) 1.0848; More...

EUR/USD dips slightly today but stays well above 1.0731 support. Intraday bias remains neutral first. On the upside, break of 1.0857 resistance will indicate that correction from 1.0963 has completed already. Retest of 1.0953 should be seen first. Firm break there will resume the rally from 1.0176 towards 1.1274 key resistance. However, firm break of 38.2% retracement of 1.0358 to 1.0953 at 1.0726 holds will bring deeper correction to 55 D EMA (now at 1.0645).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Euro Slips on Soft CPI, US 10 Year Yields Sink

Global markets are trading with a mixed tone today as investors brace for the long-awaited reciprocal tariff announcement from the US tomorrow. Asian stocks staged a moderate recovery from Monday’s selloff, while European indexes are also slightly in black. However, US futures are coming under renewed pressure. Meanwhile, Gold continues to shine amid the unease, extending its record-breaking rally and coming just shy of the 3150 mark.

Currency markets remain cautious but active. Selling pressure has rotated toward Euro and Sterling, with the common currency slightly more pressured by today’s lower-than-expected Eurozone core CPI print. Sterling is also softening, along with Loonie.

On the other hand, Yen and Swiss Franc are regaining strength, both benefiting from renewed risk-off flows. Dollar is treading water, with a mixed performance. Aussie and Kiwi are holding their ground for now, underpinned by stronger-than-expected Chinese manufacturing PMI data.

The Washington Post reported that Trump administration is still weighing several options for its tariff rollout, including a sweeping 20% levy on most imports or a country-by-country “reciprocal” model. While no final decision has been made, the scope could significantly alter global supply chains. Markets are likely to remain defensive until more clarity emerges, especially on whether exceptions will be granted and how key trade partners like the EU, China, and Canada will respond.

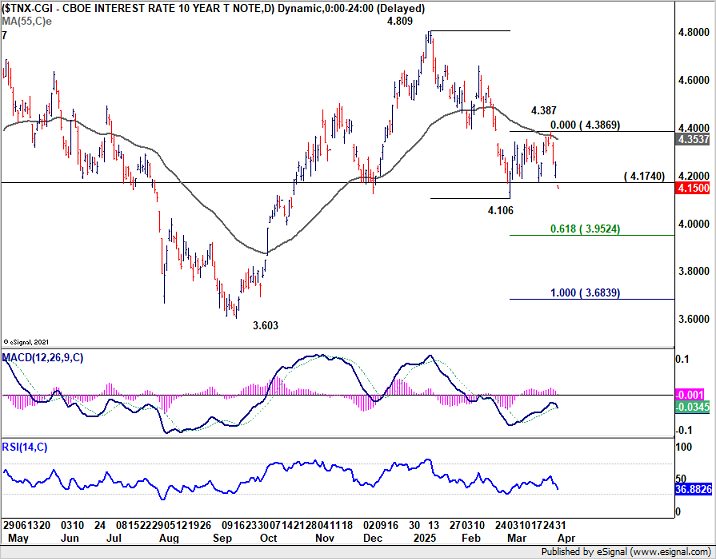

Technically, US 10-year yield capped down through 4.174 support today. A close below the support level should confirmed that corrective recovery from 4.106 has completed at 4.387 after rejection by 55 D EMA. That would set up deeper fall back to 4.106 first. Firm break there will resume the whole decline from 4.809 to 61.8% projection of 4.809 to 4.106 from 4.387 at 3.952, which is below 4% psychological level.

In Europe, at the time of writing, FTSE is up 0.76%. DAX is up 1.24%. CAC is up 0.86%. UK 10-year yield is down -0.055 at 4.634. Germany 10-year yield is down -0.072 at 2.677. Earlier in Asia, Nikkei rose 0.02%. Hong Kong HSI rose 0.38%. China Shanghai SSE rose 0.38%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.016 to 1.504.

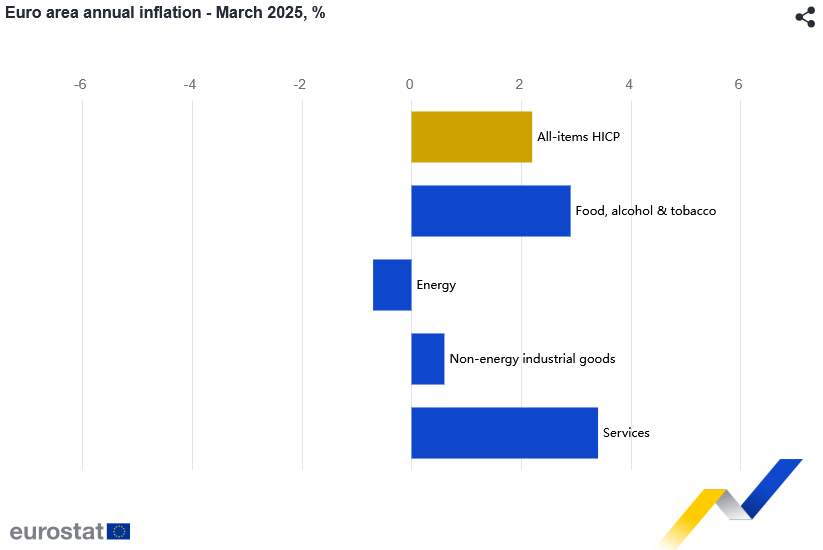

Eurozone CPI falls to 2.2% in Mar, core down to 2.4%

Eurozone headline CPI eased slightly from 2.3% yoy to 2.2% yoy in March, in line with expectations. CPI Core (excluding energy, food, alcohol & tobacco) dropped from 2.6% yoy to 2.4% yoy, undershooting forecasts of 2.5% yoy.

Looking at the composition, services remained the main driver despite moderating to 3.4% from 3.7%. Food, alcohol, and tobacco edged up to 2.9% from 2.7%. Non-energy industrial goods stayed stable at 0.6%, while energy slipped further into deflationary territory at -0.7%.

Eurozone PMI manufacturing finalized at 48.6, greenshoots clouded by tariff frontloading

Eurozone manufacturing showed encouraging signs of recovery in March, with the final PMI Manufacturing reading rising to 48.6, its highest level in 26 months. Output index broke above the 50 mark to 50.5, the first time in growth territory since March 2023. Though still technically in contraction, the steady three-month climb in headline PMI suggests that the worst may be behind for the sector.

Regional breakdowns reveal uneven performance, with Greece leading the bloc at 55.0, while Italy and Austria remain below 47. Germany and France—the two largest Eurozone economies—improved notably, to 48.3 (31-month high) and 48.5 (26-month high) respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, believed some of the recent gains stem from US companies frontloading orders ahead of the looming tariff war, which could mean that part of the improvement may unwind in the coming months.

Still, there are signs of structural tailwinds forming. Speculation is growing that Germany’s ramped-up fiscal spending—particularly on defense and infrastructure—may eventually trickle down into broader Eurozone growth. While those benefits are unlikely to be felt until 2026 or beyond, they offer a potential path to sustained recovery.

BoE’s Greene: Trade War likely disinflationary for UK

BoE Monetary Policy Committee member Megan Greene said today that a trade war involving retaliatory tariffs would likely be "disinflationary" for the UK overall. Though she cautioned against putting too much weight on early modelling at this stage.

Greene pointed out that exchange rates would be a key transmission channel for the effects of global trade tensions. She also noted the possibility that the US dollar's role as the world’s reserve currency could be "undermined a little bit" by the rising uncertainty, adding more unpredictability to how exchange rates, including GBP/USD, could respond.

On domestic inflation expectations, Greene maintained that they "remain anchored" for now but acknowledged the upward drift over the past six months as a growing concern. While she clarified that this is not currently a crisis-level issue—“not flashing red lights”—the trend warrants attention.

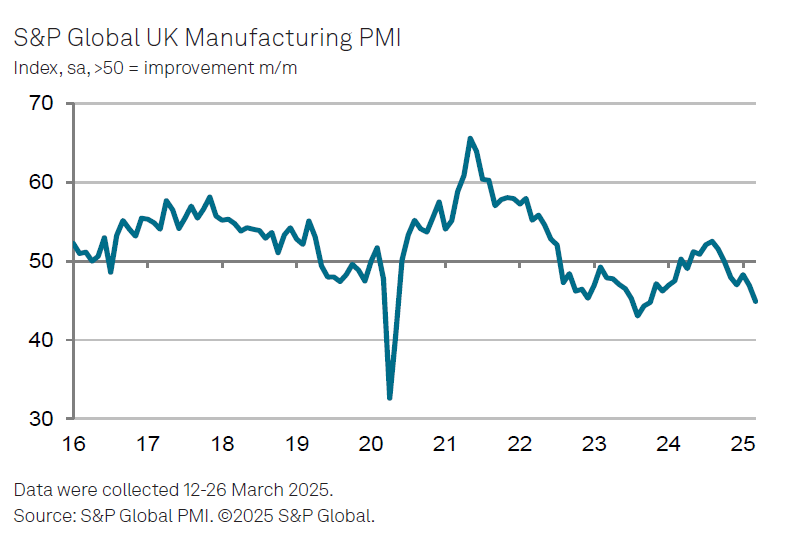

UK PMI manufacturing finalized at 44.9, sector hit on several fronts

UK PMI Manufacturing index was finalized at 44.9 in March, down from 46.8 in February, its lowest level in 17 months. The data showed broad-based weakness, with steep declines in output, new orders, and export business. Business optimism also tumbled to its lowest point since November 2022.

Rob Dobson of S&P Global Market Intelligence noted that new business inflows suffered one of the sharpest drops since the pandemic lockdowns of 2020.

Manufacturers are being "hit on several fronts": weakening domestic demand, rising costs linked to minimum wage and national insurance changes, and a deteriorating global trade backdrop due to mounting geopolitical risks and tariff uncertainties.

RBA stands pat, inflation eases as expected, but outlook clouded

RBA kept the cash rate target unchanged at 4.10% today, in line with broad market expectations. While the central bank welcomed the continued decline in underlying inflation, it emphasized a "cautious" stance due "risks on both sides".

Recent data suggests inflation is easing in line with forecasts, but RBA reiterated that it needs greater confidence that this trend will continue sustainably toward the midpoint of the 2–3% target band.

RBA highlighted "notable uncertainties" around domestic consumption and labor market dynamics. Internationally, there are concerns over the escalating US tariff policy, noting that such developments are already affecting global confidence.

The risk of further tariff expansion or retaliatory measures from other countries could amplify the drag on global activity. Inflation could move in "either direction" depending on how households and firms react to the shifting macroeconomic environment.

Japan's Tankan survey flags manufacturing caution, services hit 33-year high

Japan’s Q1 Tankan survey revealed a mixed outlook for the economy, with sentiment among large manufacturers slipping for the first time in a year. The index fell from 14 to 12, in line with expectations, as steel and machinery producers grew more cautious amid weak global demand, rising input costs, and uncertainty surrounding US tariff policy.

However, manufacturing outlook ticked down just slightly to 12, beating expectations of a sharper decline to 9, indicating that businesses remain cautiously optimistic.

In contrast, Japan’s services sector showed remarkable resilience. The large non-manufacturing index rose from 33 to 35—marking the highest level since 1991. Still, the outlook component was flat at 28, slightly missing forecasts of 29.

Capital expenditure plans were also encouraging, with large firms expecting a 3.1% increase for fiscal 2025, ahead of consensus of 2.9%.

Japan PMI manufacturing finalized at 48.4, weaker domestic and international demand

Japan’s manufacturing sector contracted further in March, with final PMI reading falling to 48.4 from February’s 49.0, marking the lowest level in a year.

According to S&P Global, both output and new orders declined more sharply, reflecting "weaker demand from both domestic and international clients". Employment offered a rare bright spot, as firms increased hiring at the fastest rate in three months.

However, confidence remained muted and below the long-run average. Cost pressures also persisted, with strong increases in both input costs and selling prices, suggesting that "inflationary pressure across the sector remains acute".

China Caixin manufacturing rises to 51.2, jobs and prices Lag

China’s Caixin PMI Manufacturing rose to 51.2 in March, up from 50.8 and marking a four-month high.

According to Wang Zhe of Caixin Insight Group, the upbeat print points to a steady start to the year, suggesting broader signs of recovery in the industrial sector.

Still, challenges remain beneath the surface. The labor market "remained relatively sluggish". In addition, "deflationary pressures persisted", driven by weak domestic demand and cautious sentiment among market participants.

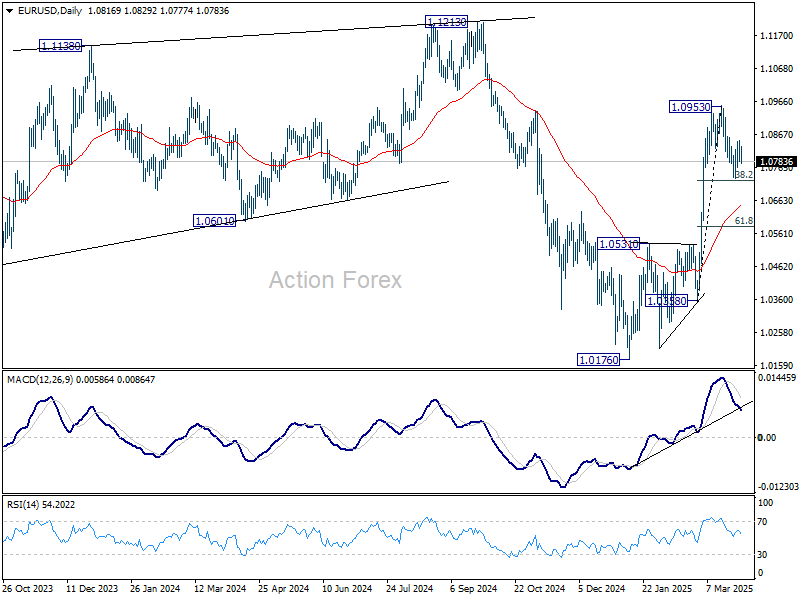

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0816; (R1) 1.0848; More...

EUR/USD dips slightly today but stays well above 1.0731 support. Intraday bias remains neutral first. On the upside, break of 1.0857 resistance will indicate that correction from 1.0963 has completed already. Retest of 1.0953 should be seen first. Firm break there will resume the rally from 1.0176 towards 1.1274 key resistance. However, firm break of 38.2% retracement of 1.0358 to 1.0953 at 1.0726 holds will bring deeper correction to 55 D EMA (now at 1.0645).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Crypto’s Attempt to Stabilise

Market picture

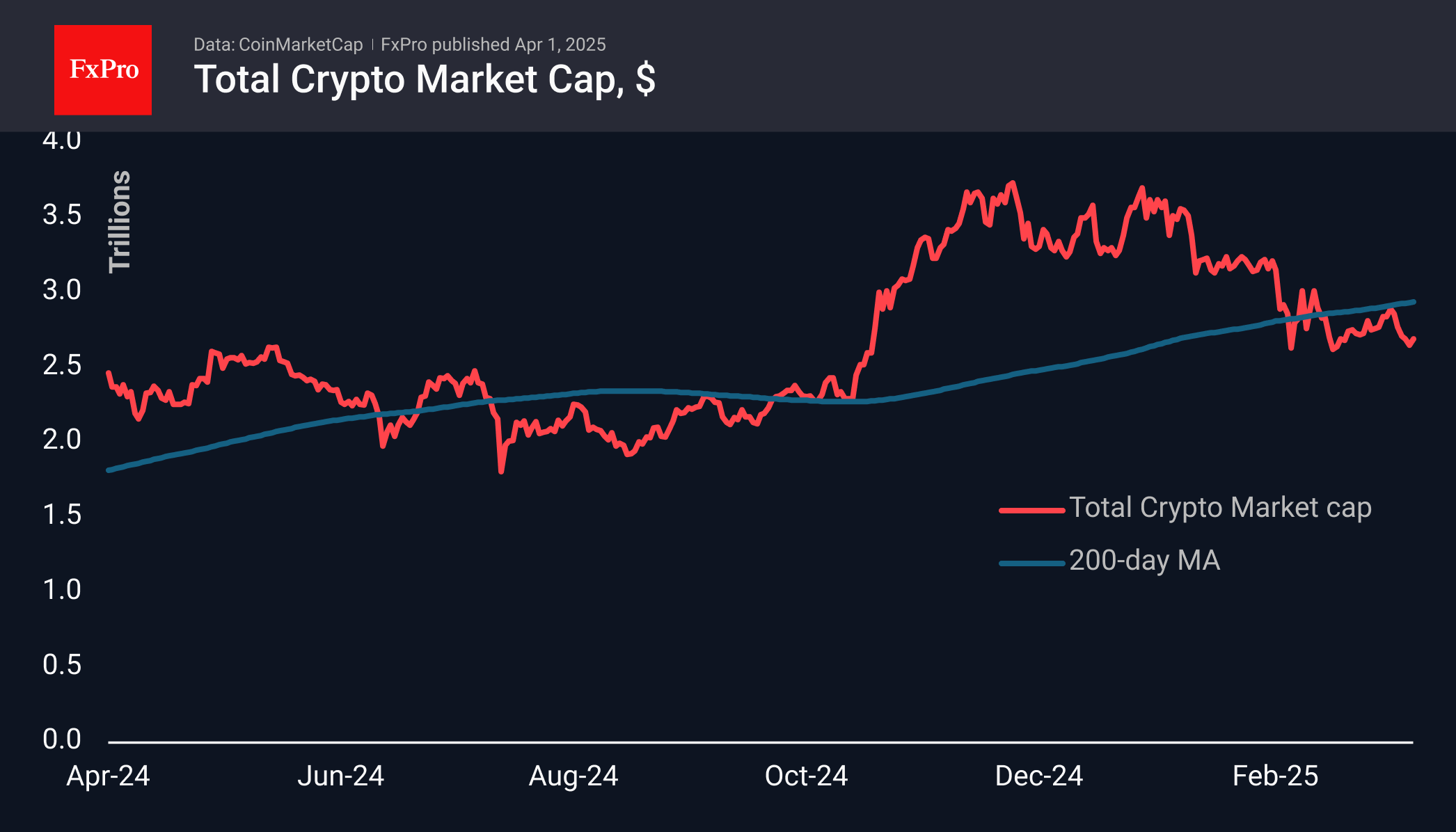

The cryptocurrency market struggled to find its footing on Monday, showing signs of a bullish effort to avoid slipping into a deeper downturn. A late-day rebound in the stock market provided some support, helping push the total market cap up by 1.1% over 24 hours, though it remains down 5% over the past week. From a technical perspective, this is a bounce within a broader downtrend, as trading remains below the 200-day moving average.

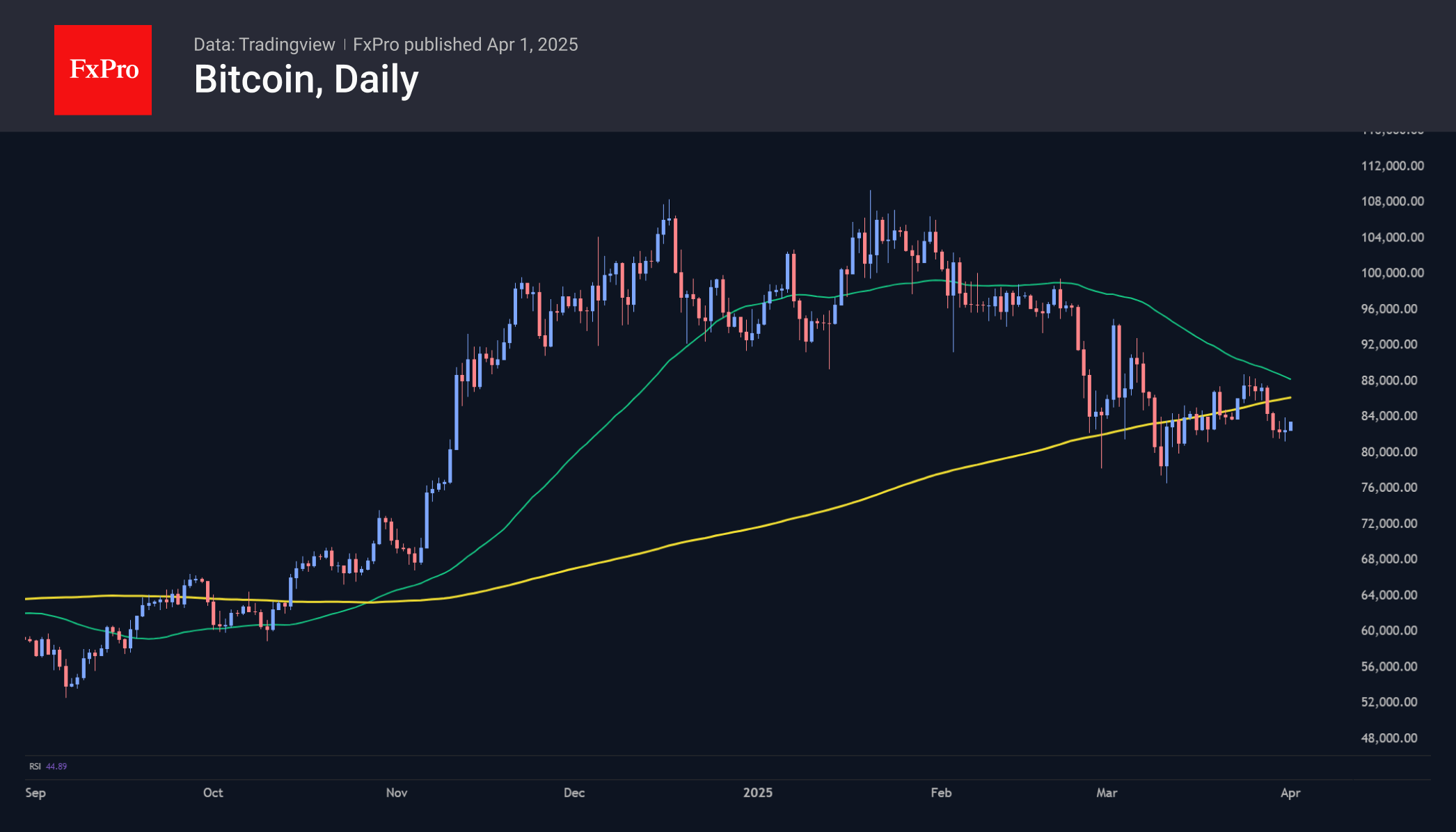

Unsurprisingly, Bitcoin is outperforming altcoins in the current climate. Its dominance has now surpassed 61%—the highest level in four years. Meanwhile, the price is hovering around $83,000, marking a 3% decline for the month. Last week’s attempts at consolidation and recovery were short-lived, leaving Bitcoin in a tightly compressed range. When it eventually breaks out, the move is likely to be significant. The key question is: which direction will it take?

Historically, April has been one of Bitcoin’s strongest months. Over the past 14 years, the month has ended higher nine times and lower five times, with an average rise of 21.6% and an average decline of 8.8%.

Ethereum, often seen as the market’s early warning system, is struggling. It closed March at nearly $1,800, taking it back to levels last seen in late 2023. Over the past month, ETH has dropped below its 200-week moving average and hit its most oversold level in three years. Its market share is now at a five-year low—more a sign of fading momentum than an accumulation phase.

News background

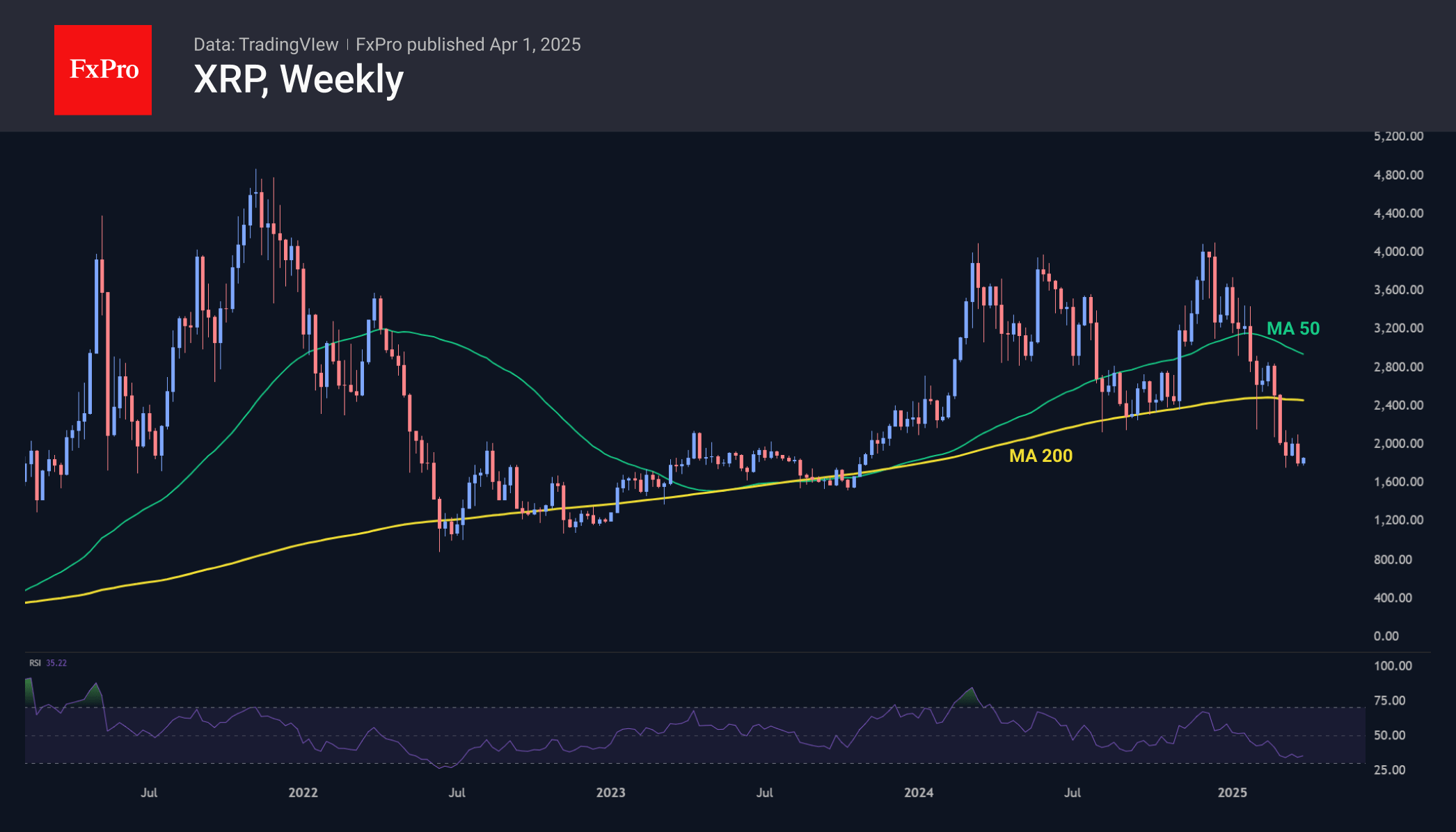

According to CoinShares, global crypto investment funds saw $226 million in inflows last week, following $644 million the week before. Bitcoin attracted the bulk of the investment, with $195 million in inflows, while Ethereum saw $15 million, Solana $8 million, and XRP $5 million.

The Strategy company continues its aggressive Bitcoin accumulation, adding 22,048 BTC for $1.9 billion. The company now holds over 528,000 BTC, worth approximately $43.8 billion at current prices.

Meanwhile, BlackRock CEO Larry Fink warned in his annual letter to investors that the unchecked growth of US government debt and budget deficits could threaten the dollar’s status as the world’s reserve currency. He suggested this could accelerate the shift towards alternative assets like Bitcoin.

BoE’s Greene: Trade War likely disinflationary for UK

BoE Monetary Policy Committee member Megan Greene said today that a trade war involving retaliatory tariffs would likely be "disinflationary" for the UK overall. Though she cautioned against putting too much weight on early modelling at this stage.

Greene pointed out that exchange rates would be a key transmission channel for the effects of global trade tensions. She also noted the possibility that the US dollar's role as the world’s reserve currency could be "undermined a little bit" by the rising uncertainty, adding more unpredictability to how exchange rates, including GBP/USD, could respond.

On domestic inflation expectations, Greene maintained that they "remain anchored" for now but acknowledged the upward drift over the past six months as a growing concern. While she clarified that this is not currently a crisis-level issue—“not flashing red lights”—the trend warrants attention.

Eurozone CPI falls to 2.2% in Mar, core down to 2.4%

Eurozone headline CPI eased slightly from 2.3% yoy to 2.2% yoy in March, in line with expectations. CPI Core (excluding energy, food, alcohol & tobacco) dropped from 2.6% yoy to 2.4% yoy, undershooting forecasts of 2.5% yoy.

Looking at the composition, services remained the main driver despite moderating to 3.4% from 3.7%. Food, alcohol, and tobacco edged up to 2.9% from 2.7%. Non-energy industrial goods stayed stable at 0.6%, while energy slipped further into deflationary territory at -0.7%.

UK PMI manufacturing finalized at 44.9, sector hit on several fronts

UK PMI Manufacturing index was finalized at 44.9 in March, down from 46.8 in February, its lowest level in 17 months. The data showed broad-based weakness, with steep declines in output, new orders, and export business. Business optimism also tumbled to its lowest point since November 2022.

Rob Dobson of S&P Global Market Intelligence noted that new business inflows suffered one of the sharpest drops since the pandemic lockdowns of 2020.

Manufacturers are being "hit on several fronts": weakening domestic demand, rising costs linked to minimum wage and national insurance changes, and a deteriorating global trade backdrop due to mounting geopolitical risks and tariff uncertainties.

Eurozone PMI manufacturing finalized at 48.6, greenshoots clouded by tariff frontloading

Eurozone manufacturing showed encouraging signs of recovery in March, with the final PMI Manufacturing reading rising to 48.6, its highest level in 26 months. Output index broke above the 50 mark to 50.5, the first time in growth territory since March 2023. Though still technically in contraction, the steady three-month climb in headline PMI suggests that the worst may be behind for the sector.

Regional breakdowns reveal uneven performance, with Greece leading the bloc at 55.0, while Italy and Austria remain below 47. Germany and France—the two largest Eurozone economies—improved notably, to 48.3 (31-month high) and 48.5 (26-month high) respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, believed some of the recent gains stem from US companies frontloading orders ahead of the looming tariff war, which could mean that part of the improvement may unwind in the coming months.

Still, there are signs of structural tailwinds forming. Speculation is growing that Germany’s ramped-up fiscal spending—particularly on defense and infrastructure—may eventually trickle down into broader Eurozone growth. While those benefits are unlikely to be felt until 2026 or beyond, they offer a potential path to sustained recovery.