Sample Category Title

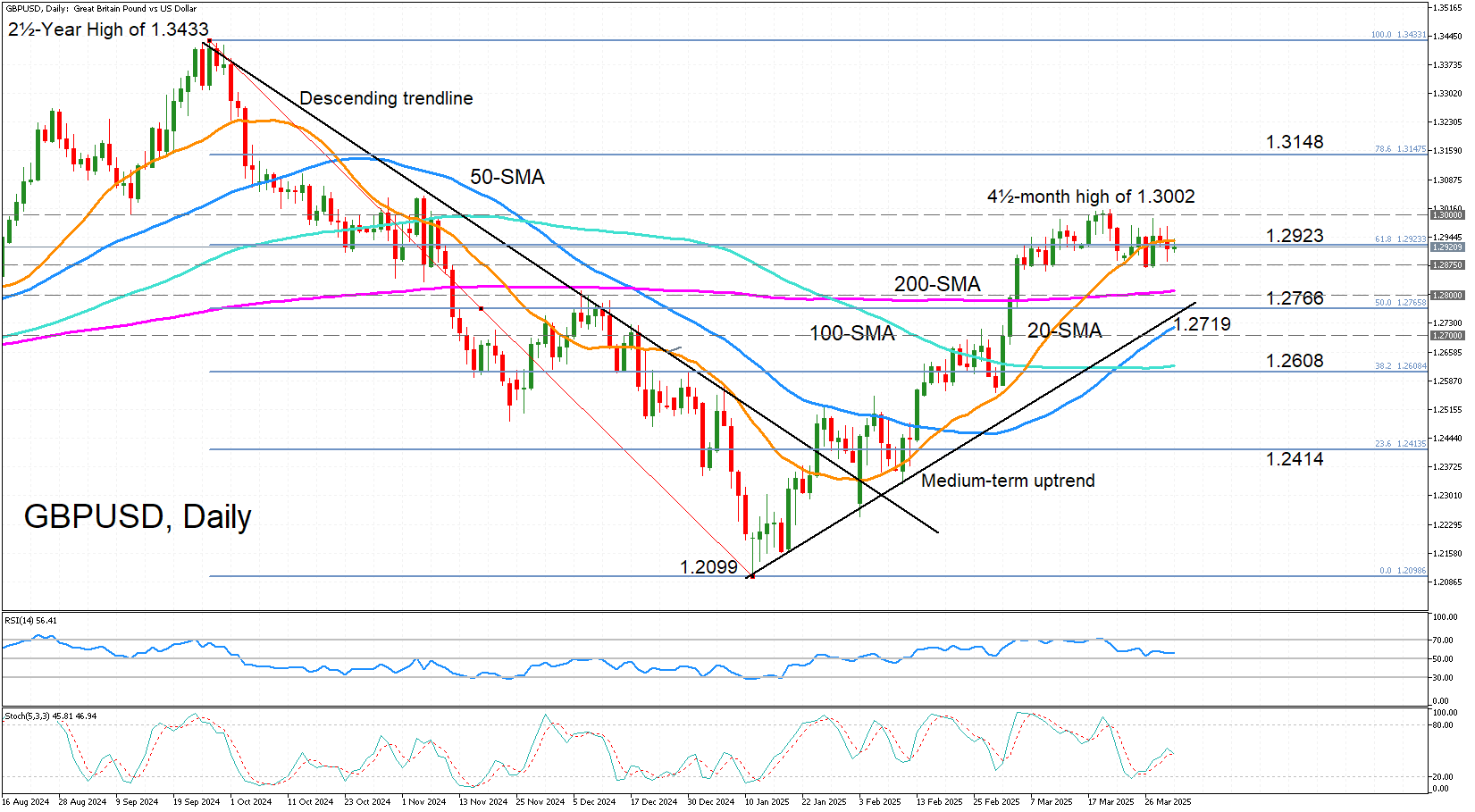

GBP/USD Turns Sideways as 20-SMA Blocks Advances

- GBP/USD faces tough resistance around 20-SMA and 61.8% Fibonacci.

- Positive momentum appears to be waning.

GBPUSD continues to consolidate after the rebound from the January low of 1.2099 ran out of steam around the 1.3000 area in mid-March. Uncertainty surrounding Trump’s tariffs is likely making it difficult for the bulls to charge ahead with confidence even as the recent UK economic data have been satisfactory.

Following the pullback, the 20-day simple moving average (SMA) initially acted as support but has now risen above the price action to cap any gains. Slightly beneath it is the 61.8% Fibonacci retracement of the September 2024-January 2025 downleg at 1.2923 and together with the 1.2875 level, they are acting as a strong support base for the pair.

The momentum indicators suggest a neutral bias in the near term, as the RSI has flatlined slightly above the 50 mark and the stochastics lack direction too.

Should GBPUSD slip below 1.2875, there’s likely to be further support just above the 1.2800 level where the 200-day SMA is slowly ascending. The 50% Fibonacci stands ready to halt steeper declines at 1.2766, while the 50-day SMA is another challenge for the bears at 1.2719. Even lower, the 100-day SMA is forming a tough support barrier together with the 38.2% Fibonacci just above 1.2600.

If, however, the bullish forces re-energize and manage to push the price above the 20-day SMA, and more importantly, above the crucial 1.3000 resistance, GBPUSD might be able to rally all the way until the 78.6% Fibonacci of 1.3148 before targeting the September 2024 peak of 1.3433, which was a two-and-a-half-year high.

All in all, GBPUSD looks set to consolidate for a while longer, but a drop below 1.2875 would increase the downside risks, endangering the medium-term uptrend, while a climb above 1.3000 would reinforce it.

DAX Declining in an Impulsive Structure, According to Elliott Wave Perspective

The $DAX appears to be tracing a five-wave impulsive decline from its recent high on March 18, 2025. In Elliott Wave theory, an impulsive structure consists of five distinct waves. Wave 1, 2, 3, 4, and 5 as motive wave moves the direction of the prevailing trend, which in this case is downward. This pattern indicates a strong, directional move, with waves ((i)), ((iii)), and ((v)) being motive (driving the decline) and waves ((ii)) and ((iv)) serving as countertrend corrections.

Starting from the March 18 peak, wave ((i)) likely initiated the downturn which ended at 22723.19. It was followed by a corrective wave ((ii)) rebound towards 23204.59. Wave ((iii)), typically the longest and most powerful in an impulsive sequence, should push the index lower with momentum. A smaller corrective wave ((iv)) is then expected to follow, offering a brief bounce. Then wave ((v)) should complete the structure, potentially finding a bottom. The impulsive nature suggests that each motive wave ((i)), ((iii)), ((v))) subdivides into its own five-wave pattern, reinforcing the bearish outlook.

Key levels to watch include support zones where prior corrections have held. Exact targets however depend on the unfolding wave lengths and Fibonacci relationships. Expect further downside until the fifth wave concludes. Afterwards, a larger corrective rally could emerge. This view aligns with sentiment for a continued near-term decline in the $DAX, driven by an impulsive bearish sequence.

DAX 60 Minutes Elliott Wave Chart

DAX Video

https://www.youtube.com/watch?v=oRarZrEtf7Y

Brent Crude Oil Price Rises Above $71

Brent crude oil is trading above $71 per barrel today, marking its highest level since late February. As shown on the XBR/USD chart, the price surged by approximately 2.6% on the last day of March.

Why Has Oil Risen?

Bullish sentiment in the market is driven by the US President’s stance on Russia and Iran. According to Trading Economics:

➝ Trump has vowed to impose tariffs of 25–50% on buyers of Russian oil if he believes Moscow is obstructing his efforts to end the war in Ukraine. This could put pressure on key importers such as India and China.

➝ He has also threatened Iran with further tariffs and airstrikes until the country agrees to abandon its nuclear weapons programme.

The rise in Brent crude prices appears to reflect traders’ concerns over potential disruptions to global oil supply chains.

Technical Analysis of XBR/USD

In early March, oil formed a bullish Double Bottom pattern (see the lows on 5 and 11 March), followed by an upward trend within a rising channel (marked in blue).

Notably, the XBR/USD chart shows that the price:

➝ Has moved into the upper half of the channel.

➝ Broke through key resistance at around $70.25, a level that previously acted as support multiple times (as indicated by the arrows).

As a result, the median of the channel, reinforced by the $70.25 level, may now serve as support, keeping Brent crude within the blue channel. However, market direction will likely depend on the news cycle, particularly sharp statements from the White House.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Extends Record as Tariff Uncertainties Prevail

March is over, the pain is probably not. Global equity markets kicked off the week on a negative note ahead of the so-called Liberation Day, April 2nd, the day the Trump administration will reveal the reciprocal tariffs to the rest of the world. Based on the strategy adopted by the White House since the beginning of Trump’s second term, tomorrow’s announcement will likely by exaggerated, overdone, buzzy and nerve-wrecking to make the others fear, react and negotiate.

The Stoxx 600 tanked 1.5% yesterday, the S&P500 gapped lower though the index rebounded from the March 13th low to close the session some 0.55% higher while Nasdaq 100 fell to the lowest levels since September before closing near flat. As such, both the S&P500 and Nasdaq 100 posted their worst quarterly performance in about two years: the high valuations – especially the high tech valuations – came down and capital flew toward the non-tech, and non-US parts of the market. Invesco’s S&P Low Volatility index – that includes low volatility names like Coca-Cola and P&G gained 1.36% yesterday and is up by almost 7% since the beginning of the year. The Stoxx 600 on the other hand gained more than 10% at some point this quarter – by the beginning of March – yet shed almost half of the gains as the narrative went from ‘the jump in government spending will boost growth’ to ‘tariffs will hit earnings’. Note that the index slipped below its major 38.2% Fibonacci retracement on the ytd rally yesterday, into the bearish consolidation zone, hinting that the selloff could continue. In Japan, the Nikkei remains under pressure this morning, as the carmakers there are also skeptical about what the tariff day will bring on the table. In the UK, the British FTSE 100 index seems weather the tariff selloff better than the major peers – the index actually posted 5% gains in Q1 – that’s its best performance since the end of 2022, but here as well, the index tested the major 38.2% Fibonacci retracement yesterday, pointing that the British blue-chip index is also on the verge of falling into a medium-term bearish consolidation zone.

European futures hint at recovery, but risks prevail

From here, there are many possible scenarios – obviously – but the most likely two are 1. US tariffs sound more reasonable than many fear and global indices rebound on relief until the next tantrum. Or 2. The tariffs are unreasonable – like the 200% levies that Trump threatened the European alcoholic beverage makers with – and the world is pushed into a deeper chaos. The majority of investors appear to be hedging against the second scenario: gold prices continue their journey to the north with little hesitation, the price of an ounce of gold is trading above $3140 this morning and the USDCHF resists into the 0.8850 level.

Elsewhere, the US dollar’s tentative to recover losses yesterday remained weak as the index posted a fifth session of lower lows and lower highs – confirming that sentiment remains comfortably bearish into Liberation Day. The EURUSD was bid below the 1.08 level. The Italian CPI update came in higher than expected while inflationary pressures in Germany eased in March. The eurozone aggregate data is due later this morning and is expected to have eased in March toward the European Central Bank’s (ECB) 2% target. The lower the inflation print, the stronger the ECB policy support, the stronger the ECB’s policy support, the stronger the euro . Across the Channel, Cable is waiting in ambush below the 1.30 level, any further retreat in the US dollar would push the pair above the critical 1.30 resistance. In Japan, the USDJPY is back below the 150 mark. The pair couldn’t clear the critical 151/151.50 resistance zone, including the 50-DMA and the major 38.2% Fibonacci retracement on ytd retreat. Even though the Bank of Japan (BoJ) expectations softened due to tariff uncertainty, policymakers’ willingness to support economic growth and the dollar’s broad-based weakness keeps the outlook in favour of the yen.

While we are in Asia, the latest Caixin manufacturing PMI hinted that manufacturing in China grew faster than expected in March, pointing that the government’s efforts to boost production may be paying off. The CSI 300 index is offered into the 50-DMA but the Hang Seng is up by around 0.56% at the time of writing, as the tech giants including Alibaba and Tencent are better bid after an ugly Monday.

In Australia, the Reserve Bank of Australia (RBA) kept its cash rate unchanged as broadly expected. The RBA decision combined with good news from China and a broad-based USD weakness gives support to the AUDUSD this morning. But the gloomy global growth outlook will likely keep the upside limited.

Speaking of global growth... Crude oil bulls shrugged off concerns about slowing global growth, instead focusing on potential supply disruptions from Russia and Iran. Prices surged nearly 3.5% yesterday, clearing the key $70 per barrel mark and the 50-DMA, reinforcing bullish momentum. U.S. crude is now testing the critical 38.2% Fibonacci retracement level—typically a gateway to a medium-term uptrend. However, despite the technical setup, a sustained bullish reversal remains hard to justify given the broader headwinds in global trade.

Tankan Survey Supports Further BoJ Hikes

In focus today

In the US, both ISM March Manufacturing index and February JOLTs turnover report will be released in the afternoon. Consensus expects ISM to remain steady from the previous month, and while global manufacturing indicators have generally edged higher, regional US data has pointed towards a weaker reading amid trade uncertainty. The Fed pays close attention to the JOLTs job openings as a key labour demand indicator.

In the euro area, we receive March inflation data. Inflation in France, Spain, and Germany has come in slightly lower than expected while Italy surprised on the upside. We thus expect the euro area HICP inflation to decline from 2.3% y/y to 2.1% y/y, which is mainly due to energy and services inflation. Though more ECB officials appear ready to accept an April rate cut pause, the declining inflation still paves the way for an ECB cut in April in our view. Also in the euro area, we receive data on unemployment, which we expect to continue to show a strong labour market with an unemployment rate of 6.2%.

In Denmark, we receive flash private sector earnings for Q1. Nominal earnings rose by 4.6% y/y in Q4, resulting in real earnings growth of 2.9% y/y. We anticipate substantial nominal wage growth for 2025Q1, which will continue the trend of real wage growth, albeit at a slower pace than observed over the past year and a half.

In Sweden, we get PMI for the manufacturing sector at 8.30 CET. Last month's print came in at 53.5, where all sub-components except for inventories contributed on the upside (i.e. new orders, production employment and delivery times). We expect a reading again around the 53-level, which would be in line with the readings over the past five months.

Economic and market news

What happened overnight

In Australia, the Reserve Bank of Australia (RBA) held its Cash Rate unchanged at 4.10% in line with consensus, after a 25bp cut on the February meeting. RBA revealed growing confidence that inflation is moving towards the midpoint of its 2-3% goal, but highlighted downside risks to domestic activity. Markets price in 2-3 cuts for the rest of 2025.

In Japan, the big quarterly Tankan business survey came in mixed this morning with large manufacturers business sentiment declining to index 12 from 14 in Q4, the lowest reading in a year. The survey was compiled ahead of Trump's auto import plans last week. Large non-manufacturing business conditions increased from 33 to 35, the highest reading since 1991, supported by a spending pickup but importantly also a record-high number of foreign visitors. Inflation expectations edged higher on both a 1, 3 and 5Y horizon as the outlook for wage growth this year continues to look strong. Largely the survey aims nicely with BoJ's plans to hike further, although the impact from tariffs on the key auto industry is still unclear.

In China, the Caixin PMI manufacturing, which is the private survey, surprised slightly to the topside, coming in at 51.2 in March (cons. 51.1), up from 50.8 in February. This marked the highest reading since November, driven by improved demand conditions and the highest growth in foreign sales in 11 months.

What happened yesterday

In Germany, HICP inflation declined more than expected to 2.3% y/y in March (cons: 2.4% y/y) from 2.6% y/y. Note it was a "low" 2.3% reading (2.27% y/y). The decline was due to energy inflation that declined from -1.6% y/y to -2.8% y/y and services that fell to 3.4% y/y from 3.8% y/y. Especially the decline in services inflation is important for the ECB as that part has been very sticky in the past year.

In Denmark, 2024 Q4 GDP was revised up to 1.8% q/q from 1.6% q/q in the flash release, while the growth rate for 2024 was revised up by 0.1 p.p. to 3.7% y/y. The industry, especially the pharma sector, was still the main driver of growth. We expect more from other parts of the economy in 2025.

In Norway, the labour market organisations in the manufacturing sector, which act as a blueprint for the rest, have agreed on a wage growth of 4.4% for 2025. This is marginally below Norges Bank's (NB) estimate from the monetary policy report in March (4.5%) and shows that wage growth is decreasing even though the labour market remains tight. There is therefore room for monetary policy to gradually become less restrictive, allowing NB to eventually cut rates as they have signalled.

Equities: Global equities experienced a decline again yesterday. However, this session differed from many of the prior trade war-driven sessions, as the US ended higher for most indices and, contrary to Friday's session, indices ended close to daily highs. Consequently, both Europe and, notably, Asia underperformed yesterday.

In terms of industries and sectors in the US, 21 out of 25 industries saw gains yesterday, indicating a somewhat broad-based lift. Nonetheless, there was a significant defensive outperformance, suggesting that while some investors might venture to buy the dip, they are doing so in the less risky parts of the market. Similarly, the VIX rose despite the S&P 500 being 0.55% higher yesterday.

Unless you have special insight into the thoughts of the US president, as an investor, you will typically approach this cautiously. Yesterday's marginal improvement in risk sentiment was purely related to speculation that Liberation Day tomorrow might be slightly less severe than consensus believes.

In the US yesterday, the Dow rose by 1.0%, the S&P 500 by 0.6%, while the Nasdaq fell by 0.1% and the Russell 2000 by 0.6%.

Asian markets are mostly higher this morning, with catch-up moves particularly in export and manufacturing-heavy South Korea and Taiwan. We link this to the ongoing tariff questions, despite the PMIs released this morning.

European futures are higher this morning, while US futures are lower.

FI&FX: US equities were off for a rough start but firmed throughout the session. S&P 500 closed at +0.55%, though with tech falling behind. US 2s10s bear flattened with the short end rising 5bp and the 10y closing at 4.21%. Hawkish ECB rumours gave a lift to German 2yrs but did not help EUR/USD much. The cross gradually fell back toward 1.08. USD/JPY remains stuck around 150. EUR/SEK climbed toward 11.86 while month-end trading was part of the equation. NOK erased initial losses vs the EUR and closed flat on the day at 11.36. Scandies will take direction from tariff announcements and the SEK could be vulnerable to dividends.

More ECB Officials Appear Ready to Accept an April Rate Pause

Markets

Friday’s nasty market sell-off dragged into yesterday’s Asian and European trading as traders hit the panic button in the run-up to tomorrow’s tariff announcement by US president Trump. It’s planned as a Rose Garden event at the White House at 3 pm Washington time (9pm CET), but we wouldn’t be surprised to see headlines arriving earlier via the POTUS’ social media platforms. Trump yesterday said that he settled on a plan. Whether it will be the long-flagged reciprocal tariffs or a final U-turn towards a 20% global tariff thus remains unclear. Yesterday’s sell-off gradually slowed as US dealings got under way with even some rebound action into the close. The tech-heavy Nasdaq index was 2.7% weaker at its worst intraday moment, to eventually close the session virtually unchanged compared with Friday’s closing levels. The S&P 500 (+0.55%) and Dow Jones (+1%) even ended with gains. European equity futures this morning also suggest a somewhat firmer start after suffering 1%+ losses for the third time in four trading sessions yesterday. US Treasuries faded somewhat into the close, but the return action was less outspoken than in equities. Daily changes on the US yield curve varied between -2.8 bps and -5.7 bps with the curve bull flattening. German Bunds underperformed with curve moves between +2.7 bps (2-yr) and -1.1 bp (30-yr). The German 10-yr yield technically tested 2.65% support. The front end suffered a setback after Bloomberg published an article suggesting that more ECB officials appear ready to accept an April rate pause. EUR/USD at the same time moved back from the 1.08 area to a close near 1.0820. “Dovish officials still see the need for further loosening, but may not insist on a seventh reduction since June if their more hawkish colleagues want additional time to assess the data, the people said. They stressed, however, that the meeting is two and a half weeks away and the thinking may yet shift.” We hold firmly to our view of a final 25 bps (to 2.25%) tactical rate cut before sticking to a long pause. EMU money market rates remain to aggressive in our view, discounting sub-2% ECB policy rate by the end of the year. April EMU CPI numbers, up for release today, aren’t expected to alter that view in light of already published national figures. Consensus expect headline inflation to pick-up to 0.6% M/M with the annual reading dipping from 2.3% to 2.2%. Core inflation is set to slow from 2.6% to 2.5%. The US eco calendar contains February JOLTS job openings (7.65mn expected from 7.74mn) and the March manufacturing ISM (49.5 from 50.3). The probability is low that they’ll directionally steer markets ahead of the big event risk dubbed “Liberation Day”.

News & Views

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 4.1% after an inaugural rate cut in February. At the press conference, Governor Bullock indicated that the decision was a consensus one and that the RBA didn’t explicitly discuss a rate cut. In its policy statement the central bank signaled a cautious approach. Recent information suggests that underlying inflation continues to ease, but that the board needs to be confident that inflation will return to the midpoint of the 2-3% target range on a sustainable basis. Private domestic demand is recovering, but some business continue reporting weakness. The labour market remains tight and productivity hasn’t picked up resulting in ongoing high labour costs. International uncertainty remains elevated and might impact inflation in either direction. The Bank concludes that monetary policy remains restrictive, but governor Bullock indicated that it wasn’t as restrictive as has been the case at others. In this respect, the RBA hasn’t made up its mind on a May rate cut. Even so, the market sees slightly less than 70% chance of a May rate cut. The Aussie dollar underperformed yesterday on overall risk-off, but regains slightly ground this morning (AUD/USD 0.6261).

The BoJ this morning published its quarterly Tankan business outlook. The headline large manufacturing conditions index eased to 12 from 14, but this remains a decent level. The outlook in the sector eased only modestly to 12 from 13. The large non-manufacturing index improved from 33 to 35 (outlook 28 unchanged). Big firms expect capex to increase 3.1% this FY, marginally softer than expected. Firms still also expect inflation to rise to 2.5% in the year ahead and still to stay at 2.3% in five years (both higher compared to previous report). This suggests that inflation expectations are anchored near the BOJ target and should support a further normalization of monetary policy. USD/JPY trades little changed near 150 this morning.

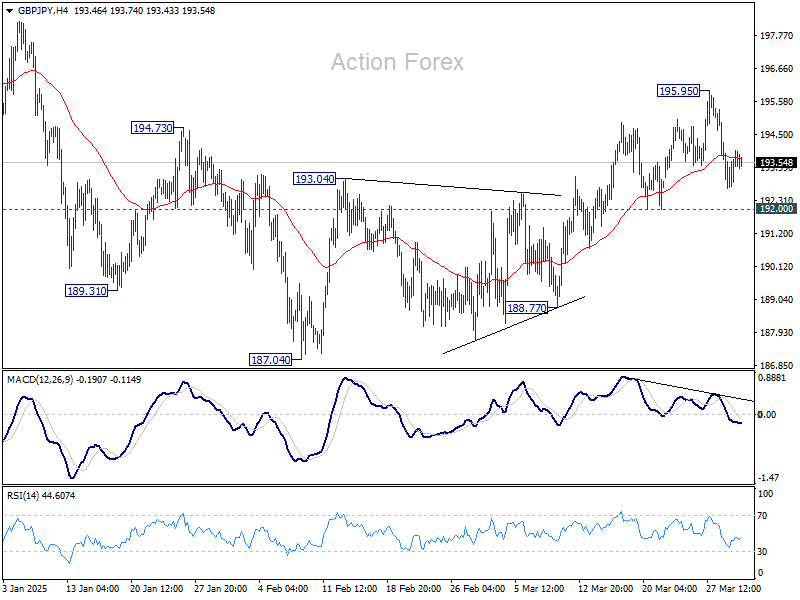

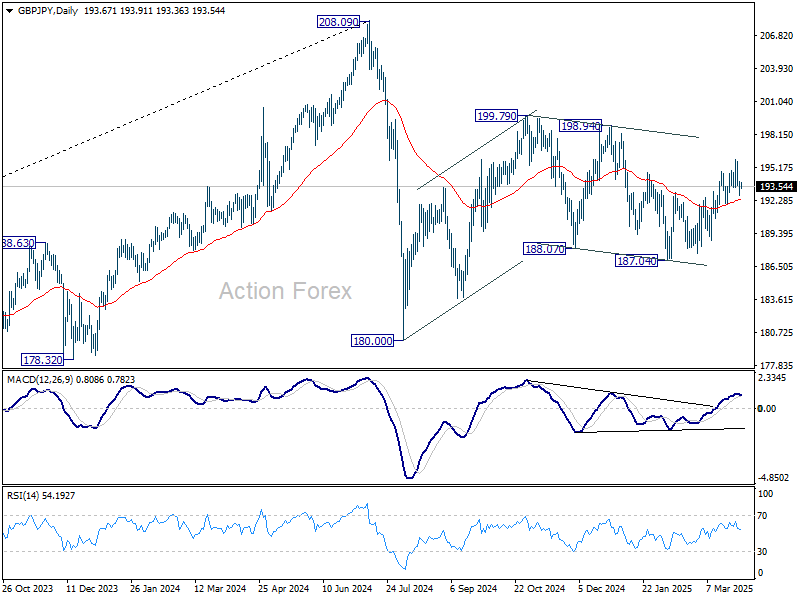

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.96; (P) 193.49; (R1) 194.24; More...

No change in GBP/JPY's outlook and intraday bias stays neutral. On the upside, break of 195.95 will extend the rally from 187.04 once again, to 198.94 resistance. However, firm break of 192.00 support will turn bias back to the downside for deeper fall. Overall, corrective pattern from 180.00 is still extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

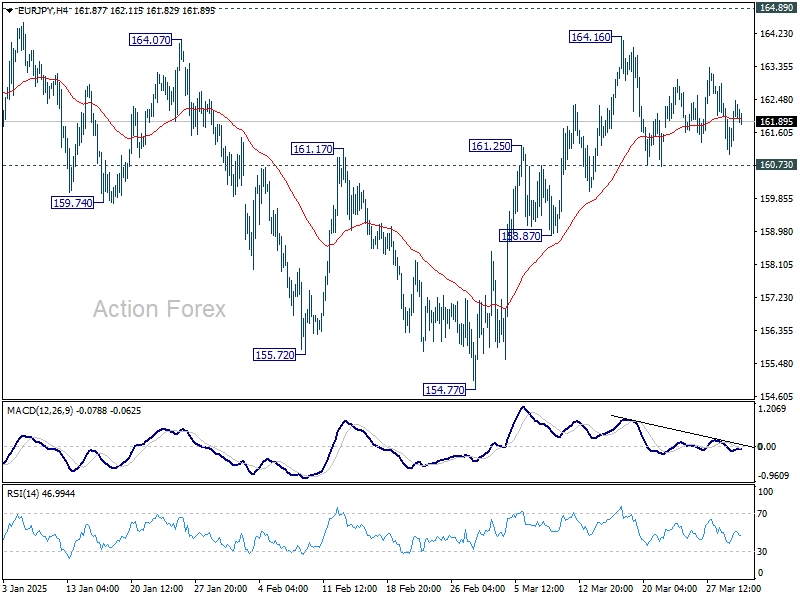

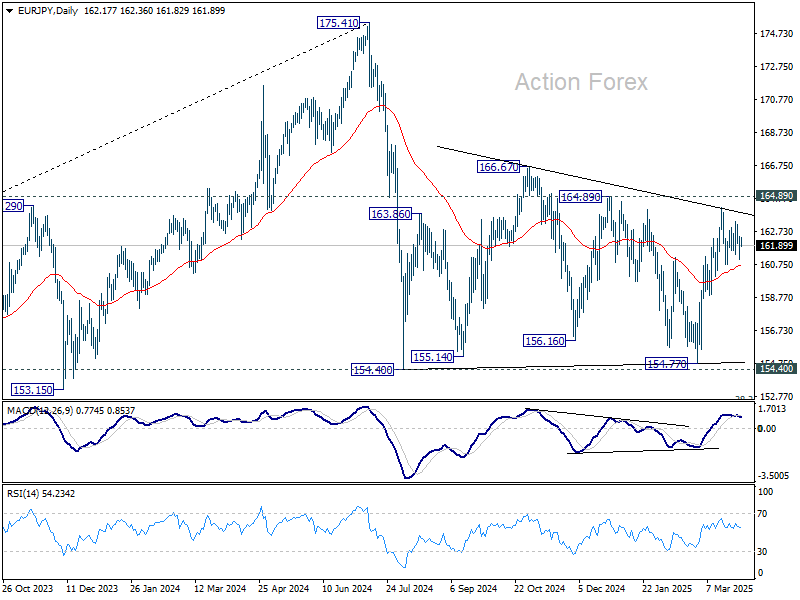

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.30; (P) 161.90; (R1) 162.74; More...

Range trading continues in EUR/JPY and intraday bias stays neutral. Further rise is in favor as long as 160.73 support holds. Above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, break of 160.73 will turn bias back to the downside for 158.87 support and below. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

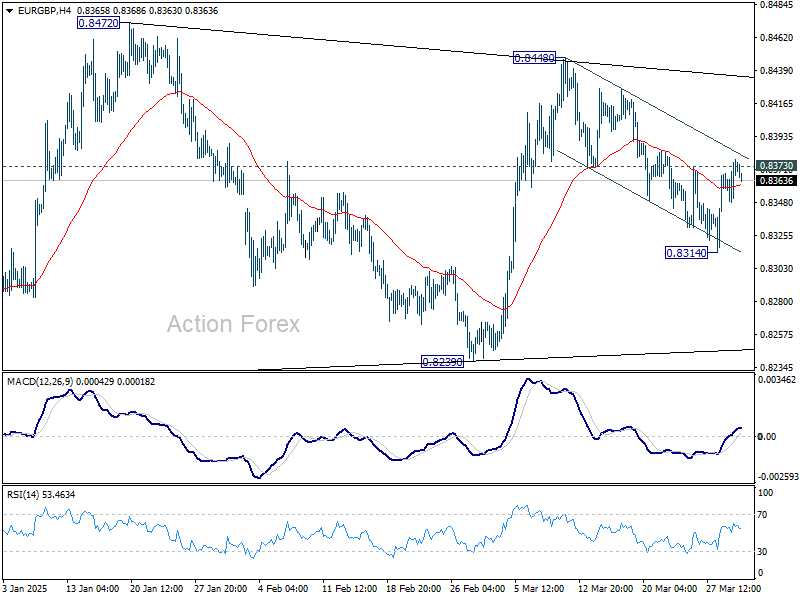

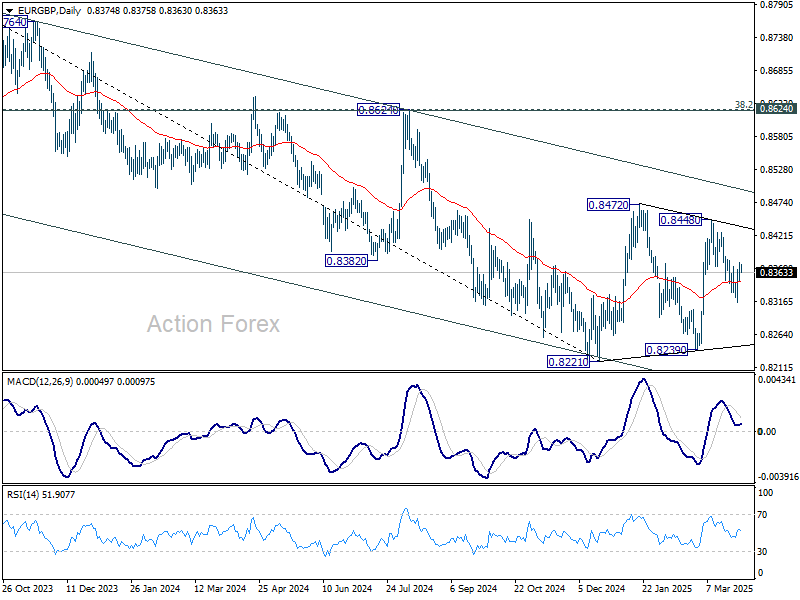

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8356; (P) 0.8367; (R1) 0.8385; More...

Intraday bias in EUR/GBP stays neutral at this point. On the downside, below 08314 will bring deeper fall back to 0.8239 support. However, firm break of 0.8373 minor resistance will argue that fall from 0.8448 is merely a correction and has completed. Retest of 0.8448 should be seen next.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

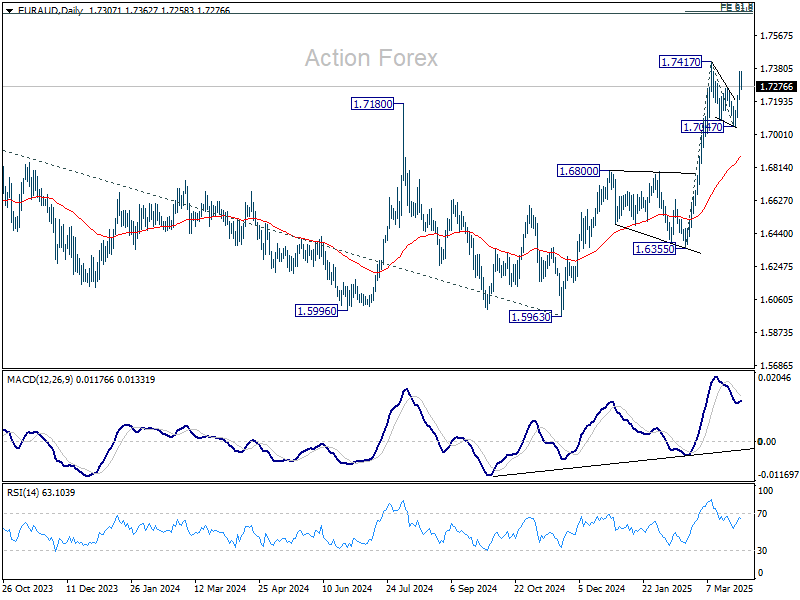

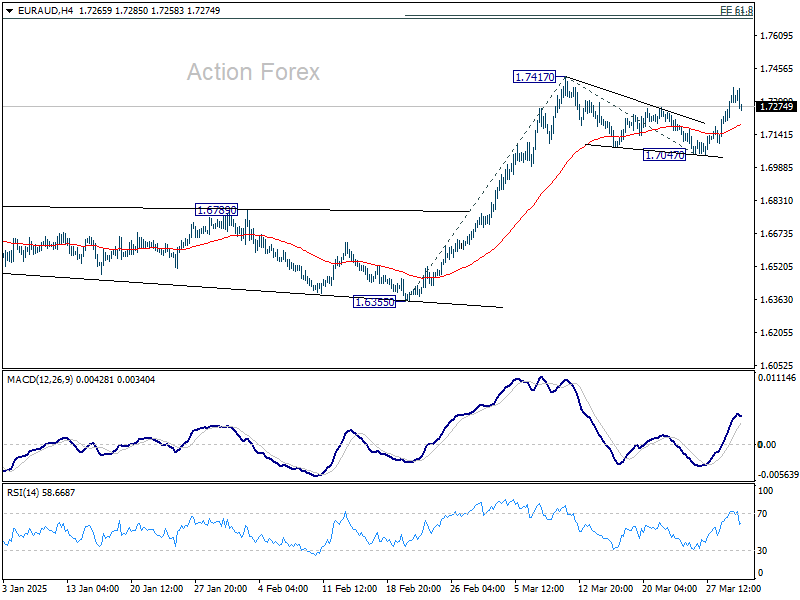

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7223; (P) 1.7295; (R1) 1.7385; More...

Intraday bias in EUR/AUD remains on the upside for retesting 1.7417 high. Firm break there will resume larger up trend, and target 61.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.7703. For now, risk will stay on the upside as long as 1.7047 support holds, in case of retreat.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming and should target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.