Sample Category Title

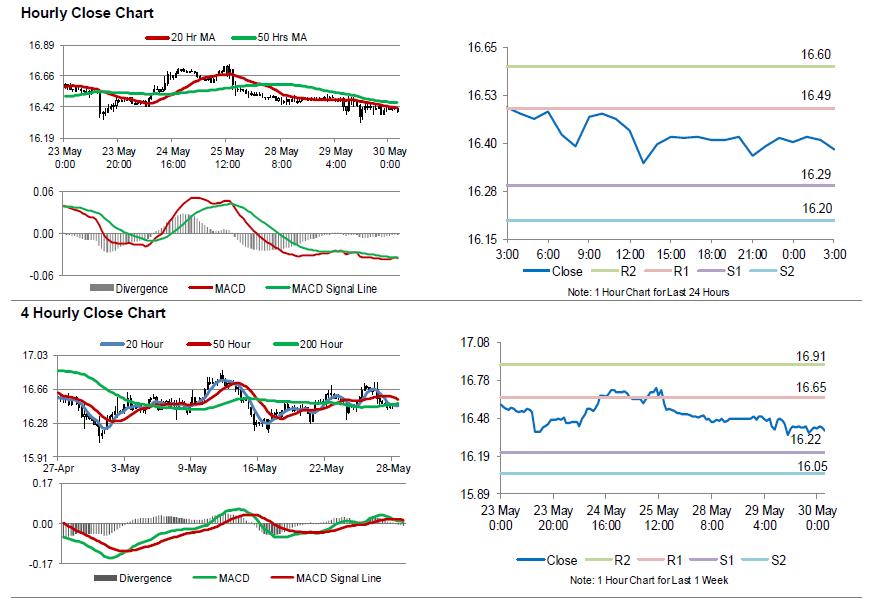

Silver: White Metal Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, Silver rose 0.73% against the USD and closed at USD16.54 per ounce.

In the Asian session, at GMT0300, the pair is trading at 16.52, with silver trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.37, and a fall through could take it to the next support level of 16.22. The pair is expected to find its first resistance at 16.63, and a rise through could take it to the next resistance level of 16.73.

The white metal is trading above its 20 Hr and 50 Hr moving averages

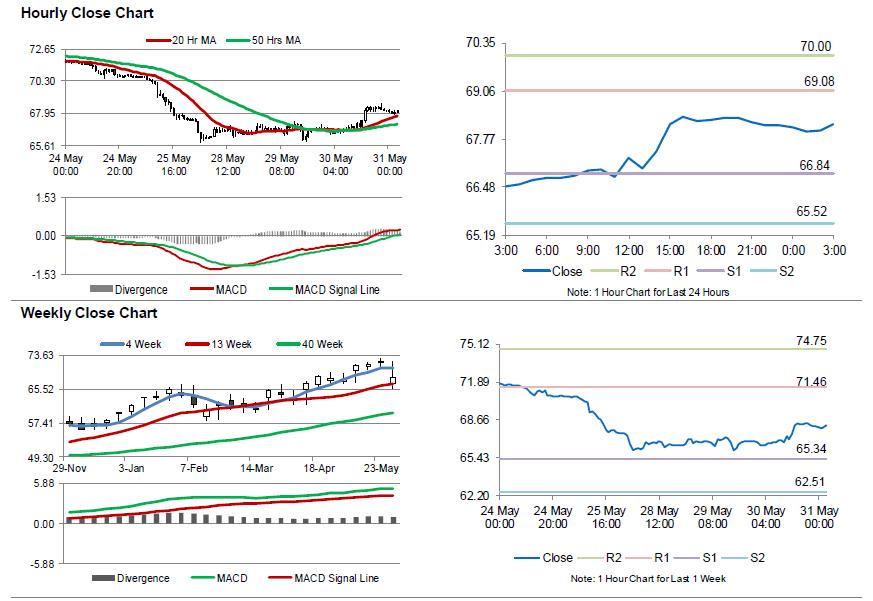

Crude Oil: Oil Tading Higher, Ahead Of EIA’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil rose 1.91% against the USD and closed at USD68.14 per barrel, following reports that OPEC and Russia would stick to their oil supply cuts until the end of 2018.

Separately, the American Petroleum Institute (API) reported that US crude oil inventories rose by 1.0 million barrels to 434.9 million barrels in the week ended 25 May.

In the Asian session, at GMT0300, the pair is trading at 68.17, with oil trading 0.04% higher against the USD from yesterday's close.

The pair is expected to find support at 66.84, and a fall through could take it to the next support level of 65.5. The pair is expected to find its first resistance at 69.08, and a rise through could take it to the next resistance level of 69.99.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

Temporary exemptions to US steel tariffs to end tomorrow

The temporary exemptions from the US steel and aluminum tariffs are set to expire tomorrow. And it's so far uncertain what will happen next. It's widely reported Trump will start imposing the tariffs on EU. The decisions on Mexico and Canada are less certain as NAFTA negotiations continued to drag on. But there are reports that Trump will just go ahead with the tariffs too. Announcement could be made as soon as today.

It's clear that EU, Canada and Mexico are prepared for retaliation. And the US announcement today could finally, formally, starts global trade wars between US and the world. The section 232 national security probe on automobile imports is also waiting on the line. The commerce department has announced to hold two days of public hearing in July for the probe.

The US Chamber of Commerce already criticized the probe and warned that tariffs "would deal a staggering blow to the very industry it purports to protect and would threaten to ignite a global trade war."

BOC Removes “Cautious” Reference, But 2H17 Rate Hikes Experience Suggests Members Can Make Over-Aggressive Judgements

Canadian dollar recorded the biggest one-day rally in two months after BOC’s more hawkish- than- expected statement. Policymakers turned less concerned over the economic outlook. As such, they dropped the words “cautious” and “over time” in the accompanying statement, a sign interpreted by the market as supportive for a rate hike in the near-term. Bets of a rate July rate hike jumped to 65% after the announcement, from less than 50% before that. In our opinion, it might be premature to associate removal of “cautious” at the May meeting to “rate hike coming soon”. Intermeeting dataflow should be the key.

In the concluding statement, BOC suggested that “developments since April further reinforce Governing Council’s view that higher interest rates will be warranted to keep inflation near target”. With the reference, “over time”, dropped, the market expects a rate hike would come soon. Meanwhile, the central bank reiterated that it would “take a gradual approach to policy adjustments, guided by incoming data” and it would “continue to assess the economy’s sensitivity to interest rate movements and the evolution of economic capacity”. However, it removed the reference that the members would “remain cautious with respect to future policy adjustments, guided by incoming data”. This is interpreted as a hawkish shift.

Supporting BOC’s confidence are recent economic developments both in Canada and in the US. At home, inflation would “likely be a bit higher in the near term than forecast in April” as driven by “increases in gasoline prices”. The central bank stressed that it would “look through the transitory impact of fluctuations in gasoline prices”. Moreover, the members acknowledged that “activity in the first quarter appears to have been a little stronger than projected”. They forecast that “solid labour income growth supports the expectation that housing activity will pick up and consumption will continue to contribute importantly to growth in 2018”.

BOC remains confident over US’ outlook, noting that “recent data point to some upside to the outlook for the US economy”. Yet, they also reminded that “ongoing uncertainty about trade policies is dampening global business investment and stresses are developing in some emerging market economies. Global oil prices have been higher than assumed in April, in part reflecting geopolitical developments”.

The overall tone of the statement is more confident than the April one. Note, however, that BOC has no track record of offering “forward guidance” when compared with the Fed. On the contrary, the central bank has a “black mark” of making U-turn after over aggressive tightening. Back in October 2017, BOC expressed genuine concerns over the downside risks to inflation and indicated it would be more “cautious” over future rate hike decisions. In the accompanying statement, it stressed that “while less monetary policy stimulus will likely be required over time, Governing Council will be cautious in making future adjustments to the policy rate”. The abrupt change in the tone was after an unexpected rate in September, following the one in July. The negative impacts of the July rate hike: July GDP stagnating after growing for 8 months in a row, retail sales surprisingly contracting in August, etc. Yet, BOC incurred another rate hike in September before these reports were released. It might be premature to associate removal of “cautious” at the May meeting to “rate hike coming soon”. Dataflow and US trade policy should be closely monitored in the 6-week period from now to the July meeting.

ANZ business confidence: Fairly uninspiring reading

New Zealand ANZ business confidence dropped to -27.2 in May, down from -23.4. That is, a net 27% of businesses are pessimistic about the year ahead. Views on their "own activity" also dipped from 18 to 14.

ANZ noted in the release that "the survey made for fairly uninspiring reading this month, with all aggregate activity indicators flat to falling. The economy still has good tailwinds in the form of fiscal stimulus and the record-high terms of trade, but may be tiring nonetheless."

Meanwhile, ANZ's composite growth indicator, a combination of business and consumer confidence, is consistent with around 2% y/y growth.

Market Morning Briefing: Brent Has Held Well Above The Support At 74.50

STOCKS

Dow (24667.78, +1.26%) did not extend to 23750 following the sharp fall seen on Wednesday and instead rose back to 24750. One possibility could be that the index does not come below 24250 for the next few sessions and instead move up to 25000 and beyond (this could validate a possible triangle formation indicating medium term bullishness), initiating a fresh upmove. Else the index could see another fall from 25000 and remain in the sideways range for some more time.

Dax (12783.76, +0.93%) has also moved up instead of moving down towards 12300 or lower. Although there could be some upmove just now, the downside scope remains open for the medium term while below 12900.

Nikkei (22148.01, +0.59%) has also attempted to rise slightly and is trading above 22000. Note immediate resistance near 22400 which if holds could again push the index back to lower levels in the coming sessions.

Shanghai (3064.35, +0.75%) saw a slight bounce from 3045 and if this holds, the index could again head towards 3100-3150 levels in the near term.

Nifty (10614.35, -0.18%) has room on the downside towards 10500 but the index has moved up from levels above 10500. While the rise continues, the index could head higher towards 10700 or higher by next week. We may keep open a possible test of 10500 on the downside.

COMMODITIES

Brent (77.28) has held well above the support at 74.50 and bounced up from there while WTI (68.10) has moved up too. Brent may target 80 soon while WTI could pause near 69 and re-attempt higher levels in the longer run.

Gold (1302.39) is stable just now and could remain sideways ranged in the 1290-1310 region at least for the next 2-sessions. Thereafter a break above 1310 could initiate some bullishness; else the price could re-test 1300 or lower once again.

Copper (3.0652) moved up instead of testing 3.02 on the downside. While the Chinese Stock index moves up, Copper could find some ranged movement with a possible upside towards 3.10-3.12 levels again. In case the china stock index falls sharply in the near term, it could lead to a sharp fall in Copper too to levels below 3.02. Watch for a rise in Copper prices in the next 2-sessions.

FOREX

Dollar index (94.098), after touching 95 on Tuesday, fell to a low of 94.05 yesterday, thereby breaking support on daily candles. It has two important supports at the 13 day and 21 day moving averages near 93.86 and 93.43 respectively. If it breaks 93.43, the Dollar Index might turn bearish for the medium term. However, while above 93.43, it could again rise to test levels near 95. On the 3 day line chart, 96 is seen as a possible resistance level, which might be the maximum upside the Dollar Index sees in the medium term.

Euro (1.1658), after having seen a low near 1.151 on Tuesday, strengthened to a high near 1.1676 yesterday. The 13 day and 21 day moving averages near 1.1718 and 1.1796 are important resistance levels for the Euro in the near term. A rise past 1.182 could make Euro bullish for the medium term. While below 1.179-1.182, Euro could again dip to test levels near 1.15. On the 3 day line chart, 1.135-1.140 is seen as possible support, which could be the maximum medium term downside that the Euro could see. A break of 1.135-1.140 (less preferred currently) would open up possibility of 1.12.

Dollar Yen (108.69) continues to stay above the 21 weeks MA near 108.14. The 13 months MA near 107.8 could also lend some support. While above 107.8-108.0, Dollar Yen could attempt another upmove towards resistance on weekly candles near 110.5-111.0. However, as we have been mentioning, a break of 107.8 could result in a quick downmove to 106-105 (seen as crucial support on weekly candles).

Euro Yen (126.72): Euro Yen has bounced from support on weekly candles near 125. It could respect the support trendline in the downward channel on weekly candles for sometime. In the near term, if Dollar Yen rises to 109 while Euro attempts 1.171, we get a target of 127.6 on Euro Yen. A further rise towards 109.5 and 1.18 would translate into a test of resistance (earlier support) on weekly candles near 129.

Pound (1.33): Pound is trading near resistance in the downward channel on daily candles. It could now dip from here back towards 1.32. We have been expecting it to gradually move lower over the next 1-2 weeks with the next downside target being near 1.30 (support on weekly candles). A break of 1.30 could imply continued bearishness in the medium term.

Dollar Rupee (67.4325) : Dollar-Rupee may bounce from anywhere between 67.30-10, as the market will have become Oversold by that time.

INTEREST RATES

After political instability in Italy led to a dramatic fall in bond yields on Tuesday, there seems to be some respite in bond markets. German yields have risen slightly while the fall in US yields also seems to have paused. Our earlier projection of 3.2%-3.3% for the US 10 Year yield in the medium term (ie next 2-3 months) might now be a target for the long term (ie by 2018 end).

US 10 Yr Yield (2.84%), 30 Yr (3.01%), 5 Yr (2.67%), 2 Yr (2.41%):

As mentioned yesterday, the US 10 year yield might have some horizontal support near 2.75% which is holding for the time being. However, given the earlier break of crucial support trendline near 2.85%, we could see a gradual downmove towards medium term support near 2.55%. Another dip in Brent towards 73-71 might be the trigger for this fall to 2.55%. If that doesn’t happen, the break of 2.85% would have been a false break.

The German 10 Year yield (0.37%) has risen again and is now trading near support on short term chart.

The German – US 10 Year spread (-2.48%) has seen a strong rise from -2.59% and has again entered the downward channel on medium term chart. However, looking at long term chart, the spread still looks bearish towards long term support near -2.7% in the weeks ahead

China official PMI manufacturing rose to 51.9 as part of short-term fluctuation

The China official PMI manufacturing rose to 51.9 in May, up from 51.4, and beat expectation of 51.4. PMI non-manufacturing rose to 54.9, up from 54.8 and beat expectation of 54.8.

In the release, contributing analyst Zhang Liqun noted that the slight increase in PMI was just "short-term fluctuation" and carries "no trend significance". The rise in export orders showed there is no chance in the growing trend. Rise in purchase prices and ex-factory prices suggested that the decline in PPI could be coming to an end. In short, the data suggested that the economy continued to grow steadily in May.

Italy worries temporarily eased. DOW, S&P 500, NASDAQ gained but show mixed picture

US stocks rebounded broadly overnight as Italy worries eased temporarily. The turning point was anti-establishment Five Star Movement leader Luigi Di Maio's willingness to find someone other than eurosceptic Paolo Savona as economy minister. Savona was vetoed by President Sergio Mattarella who emphasized that "the adhesion to the euro is a choice of fundamental importance". For now, Savona is seen as a sticky point. Senior Five Star lawmaker Laura Castelli was quoted saying "it's astounding that Paolo Savona, a person of great culture and political awareness, has not yet decided to take a step back."

The political turmoil is far from being resolved yet. But at lease for now, the risk of another election, which could be framed by the far-right League as referendum on Euro, appears to be lower. German 10 year bund yield closed at 0.376 yesterday. Italian 10 year bond year closed at 2.903. That is, the spread was still wider than 250.

DOW closed up 306.33pts or 1.26% at 24667.78. The structure of of the rebound from 23344.52 still look like a corrective three wave move that's completed at 25086.49.

S&P 500 closed up 34.15pts or 1.27% at 2724.01. The chart looks better as the dip from 2742.24 was relatively shallower.

NASDAQ closed up 65.86, or 0.89% at 7462.45. The chart is best looking among the three as it didn't bother with Italy much. Rise from 6805.96 has resumed too.

So overall, the picture in US stocks were mixed. But that is expected as the markets are generally in consolidation phase. It's natural for the major indices to be out-of-sync sometimes during a consolidation.

Can AUD/USD Recover Further Above 0.7570?

Key Highlights

- The Aussie recovered recently and moved above the 0.7500 resistance against the US Dollar.

- There is a major bearish trend line in place with resistance at 0.7570 on the 4-hours chart of AUD/USD.

- The US Gross Domestic Product in Q1 2018 increased 2.2% (Prelim), less than the forecast of +2.3%.

- Today in the US, the Initial Jobless Claims for the week ending May 26, 2018 will be released, which is forecasted to decline from 234K to 228K.

AUDUSD Technical Analysis

The Aussie Dollar found support near the 0.7475 level and recovered against the US Dollar. The AUD/USD pair moved above the 0.7500 resistance, but it is facing many hurdles on the upside

Looking at the 4-hours chart, the pair jumped from the 0.7476 low and moved above the 50% Fib retracement level of the last decline from the 0.7590 high to 0.7476 low. The pair also traded above the 0.7525 resistance and the 100 simple moving average (red, 4-hours).

However, there is a crucial resistance near the 0.7560 level and the 76.4% Fib retracement level of the last decline from the 0.7590 high to 0.7476 low. Moreover, there is a major bearish trend line in place with resistance at 0.7570 on the 4-hours chart of AUD/USD.

Therefore, a break above the trend line and 0.7570 is must for more upsides in the near term. On the downside, the broken resistance at 0.7500 is likely to act as a support followed by 0.7480.

Recently in the US, the Gross Domestic Product for Q1 2018 was released by the US Bureau of Economic Analysis. The market was looking for a rise of 2.3% (Prelim). However, the actual result was a bit lower as the GDP grew by 2.2% in Q1 2018. The report added:

Real gross domestic income (GDI) increased 2.8 percent in the first quarter, compared with an increase of 1.0 percent (revised) in the fourth quarter. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, increased 2.5 percent in the first quarter, compared with an increase of 2.0 percent in the fourth quarter.

The overall outcome was positive, but it was below the market expectation, resulting in a minor pullback in the US Dollar versus the Euro, British Pound and Japanese Yen. However, the greenback remains in an uptrend and it could resume it upside move in the near term.

Economic Releases to Watch Today

- Euro Zone CPI for May 2018 (YoY, Preliminary) – Forecast +1.6%, versus +1.2% previous.

- Euro Zone Core CPI for May 2018 (YoY, Preliminary) – Forecast +1.0%, versus +0.7% previous.

- US Initial Jobless Claims – Forecast 228K, versus 234K previous.

China PMI Data Flash

With both China's Manufacturing and Servies PMI's coming in above consensus it suggests manufacturing remains resilient and domestic growth is chugging along. And amid trade and tariff tensions, this should be interpreted positively. at least for the next 20 minutes !!. However, trade fears are up front and centre again following news that the Trump Administration plans to announce that it will proceed with tariffs against the EU, Mexico and Canada Thursday. The knawing concern is that risk sentiment could turn on a dime and by no means does this data suggest we're shielded from the geopolitical firing line just yet. Way to much risk in the markets and far too early in the session to start jumping for joy on the solid China data prints