Sample Category Title

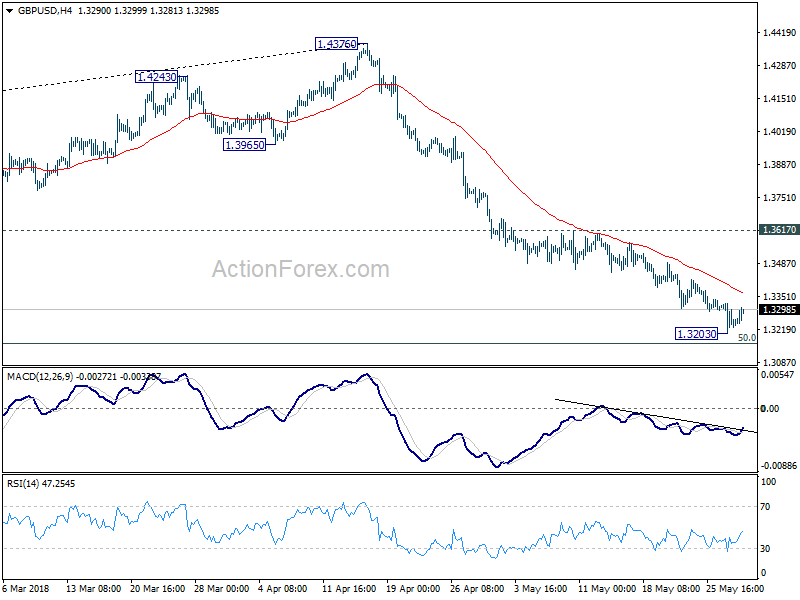

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3197; (P) 1.3263; (R1) 1.3322; More...

A temporary low is in place at 1.3203 in GBP/USD and intraday bias is turned neutral first. Some consolidations could be seen. But even in case of recovery, near term outlook will remain bearish as long as 1.3617 resistance holds. Fall from 1.4376 is expected to resume later. Below 1.3203 will target 50% retracement of 1.1946 to 1.4376 at 1.3161 first. Break will target 61.8% retracement at 1.2875 next.

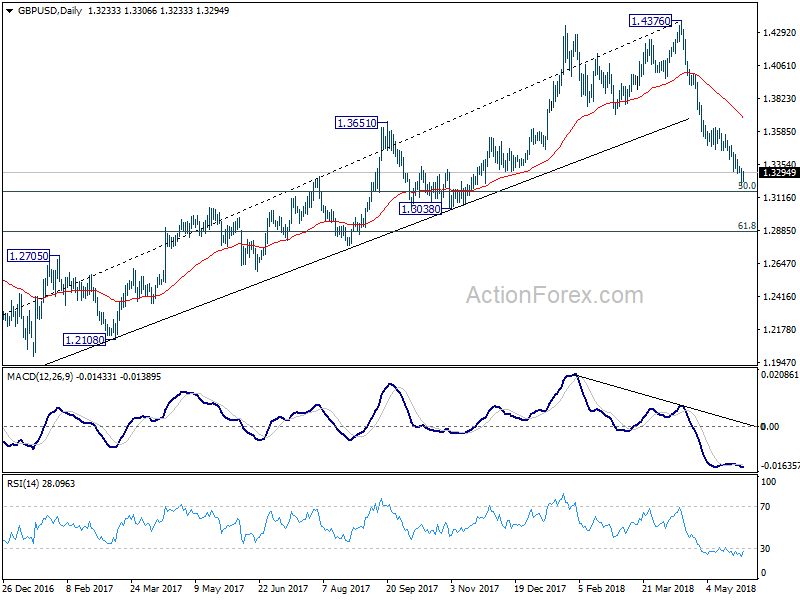

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3730) holds, even in case of strong rebound.

WTI Futures Consolidating after Aggressive Bearish Rally; Bullish in Medium Term

West Texas Intermediate (WTI) futures are on course for the second day of gains, which have driven the price towards the upper boundary of the narrow range with a resistance level of 67.30 and support barrier of 65.75. The trading range has been standing since Monday while the oil dropped below the 67.30 hurdle and started a sideways move.

The RSI is currently increasing positive momentum towards its neutral threshold of 50 after an exit from oversold levels, while the MACD is rising in the negative territory, both hinting that the next move in prices could be on the upside rather than on the downside. Furthermore, the stochastics indicate that a rebound is not far off since the oscillators are nearing overbought levels. Still, this is more likely to happen when the % K line forms a bullish cross with the %D line.

If the price bounces up and surpasses the upper boundary, immediate resistance could be at the 67.60 barrier. A significant leg above this region could send prices towards the 40-simple moving average in the 4-hour chart, currently at 69.56.

Conversely, should the market extend losses, support could be met near the 65.75 obstacle, which holds near the ascending trend line. Steeper decreases, though, could drive WTI south towards the 64.00 handle, shifting the bullish medium-term outlook to bearish.

Overall, crude oil started an aggressive bearish run over the previous week, however, the price has managed to hold above the ascending trend line that has been developing since February 8.

US: Q1 Growth Little Changed in Second Estimate

The American economy grew by 2.2% (annualized) in the first quarter according to the BEA's second estimate. That was a tick lower than the advanced estimate, but right in line with what we were expecting.

Consumer spending remained soft at 1.0% annualized (down from 1.1% in the advanced estimate). Recall that the first quarter pause in spending came after a very healthy Q4, where spending grew by 4% driven by post-hurricane related re-stocking activity.

On a more positive note, business investment was revised up from 7.3% to 9.2%. Investment in structures led the way, up 14.2% (from 12.3% in the advanced estimate). Spending on equipment was also revised up to 5.5% (from 4.7%), as were outlays on intellectual property, which jumped 10.9% annualized (from +3.6%in the advanced release).

Residential investment was revised down in Q1, to a 2% decline, after initially being reported as flat. For perspective, that came after a 12.8% surge in Q4.

Partially offsetting the upward boost from business investment were smaller positive contributions from inventory building (+0.1%-pts versus 0.4%-pts) and net exports. A slight downward revision to exports and upward revision to imports meant trade added 0.1 percentage points to growth rather than 0.2 in the advanced estimate.

Key Implications

All in, these were rather uneventful revisions. Upward revisions to business spending were offset by lower contributions from trade and inventories, with very slightly weaker consumer spending tipping overall GDP growth down a tick. A slight downward revision to growth in the first quarter does not change the story for the economy, which involves residual seasonality holding back growth in Q1, but then likely to see quarterly growth of close to 3% through the remainder of the year. Abstracting from quarterly volatility the U.S. economy grew at 2.8% on a year-on-year basis in the first quarter – well above it's potential, and a marked acceleration from 2% at the beginning of last year. There is little debate that the US economy has been doing very well.

The Fed has already discounted the somewhat slow start to the year. There is nothing in today's revision to alter their view. Barring some dramatic unforeseen event, it's all systems go for a rate hike in two weeks' time. Beyond June, we expect the Fed to raise rates once more this year. Given the recent improvement in inflation there is upside risk to that view, but it is being tempered by continued plans to impose import tariffs. These have negative consequences for business confidence and our outlook for investment.

Canadian Dollar Edges Higher, BoC Up Next

The Canadian dollar continues has steadied on Wednesday, after posting losses for a six straight day. In the North American session, USD/CAD is trading at 12974, down 0.% on the day. On the release front, it’s a busy day on both sides of the border. In the US, Preliminary GDP came in at 2.2%, just shy of 2.3%. ADP nonfarm payrolls dropped sharply to 178 thousand, well off the estimate of 191 thousand. In Canada, the current account deficit jumped to C$19.5 billion, above the estimate of C$18.1 billion. The Raw Materials Price Index dropped to 0.7%, well below the forecast of 2.1%. All eyes are on the Bank of Canada, which is expected to stay on the sidelines and hold the benchmark rate at 1.25%. On Thursday, Canada will release GDP and the US publishes Personal Spending and unemployment claims.

The Canadian dollar remains under pressure this week. The currency has declined 1.4 percent in the month of May and dropped to a 2-month low on Tuesday. There could be further headwinds for the dollar on Wednesday, if, as expected, the Bank of Canada holds interest rates at 1.25 percent. Inflation has moved closer to the BoC target of 2 percent and economic growth has been steady, so the bank may opt for the sidelines when policymakers meet on Wednesday. However, with the Federal Reserve widely expected to raise rates next month, the Canadian dollar will be less attractive to investors. Meanwhile, the growing political crisis in Italy has unnerved investors, which could hurt minor currencies like the Canadian dollar, which tends to lose ground when risk appetite is weak.

Investors are also keeping a close eye on the on-again off-again summit between the U.S and North Korean leaders. President Trump and North Korean leader Kim Jong-un are scheduled to meet in Singapore on June 12, but curiously, neither side will confirm whether the meeting is on. Last week, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the White House has since sent a team to Singapore and a senior North Korean official is on his way to Washington to meet with Secretary of State Mike Pompeo. If there is confirmation that the meeting is on, investor risk appetite could rise and push the Canadian dollar to higher ground.

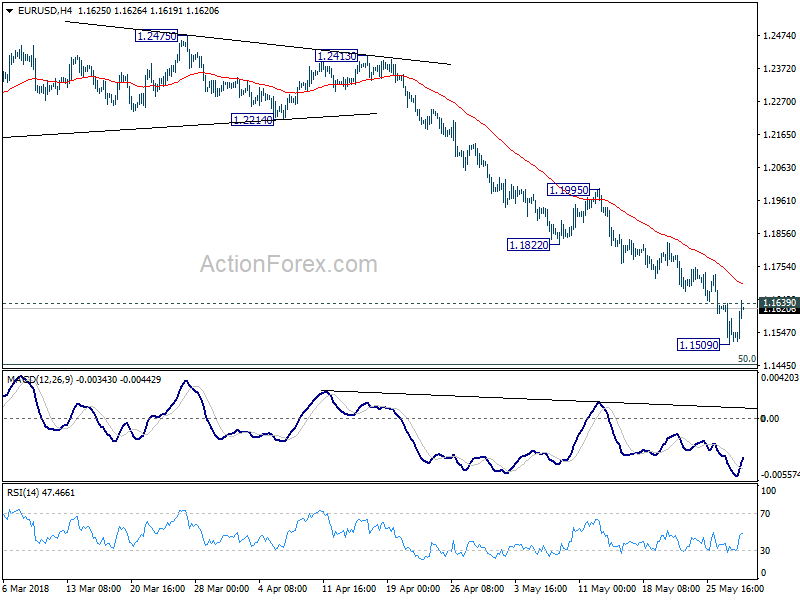

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1485; (P) 1.1563 (R1) 1.1616; More.....

Breach of 1.1639 minor resistance indicates temporary bottoming in EUR/USD at 1.1509. Intraday bias is turned neutral for consolidation. Stronger recovery could be seen to 4 hour 55 EMA (now at 1.1700) and possibly above. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. break will target 61.8% retracement at 1.1186 next.

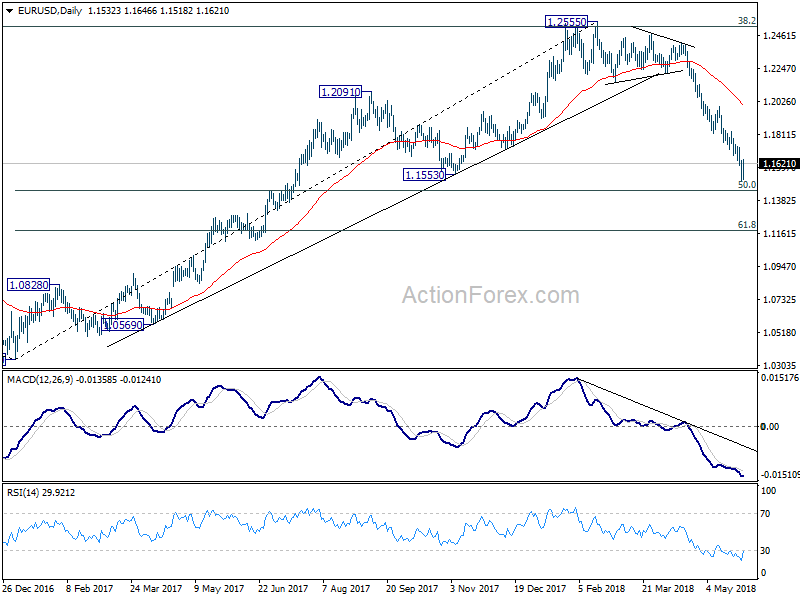

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Recovers on Revived Hope of Italy Government Formation, Robust German Data

Euro recovers broadly today as markets digest the over-stretched decline. Negative sentiments over Italian political turmoil recedes mildly as there is revived hope of a non-anti-euro government. Italy 10 year yield pull back below 3% handle while German bund yields is back above 0.35 at the time of writing. But it should be noted that German-Italian spread remains above 250bps, suggesting much nervousness among investors. Nonetheless, the common is also supported by a batch of robust economic data. In particular, German CPI accelerated much more than expected in May and that should ease some of ECB policymakers' worries.

Dollar, on the other hand is broadly pressured together with the Japanese yen. Markets won't forget that the US is in trade tension with many other countries/regions, even its own allies. NAFTA talk is going nowhere and there is no positive news regarding trade talk with EU. The steel tariff temporary exemption is going to expire on Friday and retaliations from Canada, Mexico and the EU are waiting on the line. Trump also made an about turn and issued a strong statement regarding China yesterday, indicating very little intention to carry on with negotiation. Or at least, trade war is suddenly back on after US put it on hold for just two weeks.

BoC is widely expected to keep interest rate unchanged at 1.25% today. Given the uncertainty around NAFTA, steel tariffs and the upcoming auto tariffs, the central is unlikely to give any hint on the timing of the next hike. Governor Stephen Poloz possibly doesn't have a clue himself too.

Quick update: BoC stands pat and maintains interest rate unchanged at 1.25% as widely expected. The most important part of the statement is that "developments since April further reinforce Governing Council's view that higher interest rates will be warranted to keep inflation near target." This is more hawkish than generally expected and shows that BoC is rather confident to continue with tightening, even though the timing of the next hike is still uncertain. Full statement here.

Five-Star is finding a point of compromise for economy minister

Reuters reported that a source close to the anti-establishment 5-Star Movement that it's trying to find "a point of compromise on another name" as economy minister. The rejection by President Sergio Mattarella on anti-euro Paolo Savona as economy minister triggered this week's political turmoil. If 5-Star can find someone acceptable by pro-Euro Mattarella, with far-right League or not, there is a possibility of finally forming a government. And it should be recalled while being highly critical, 5-Star has never committed themselves to leaving Euro. And its leader Luigi Di Maio said they never sought to leave the Euro via facebook comments earlier this week.

Prime Minister-designate Carlo Cottarelli is currently the technocrat that's supposed to lead the government until a new election. He also said that "new possibilities have emerged for the birth of a political government." And, "these circumstances, also considering the market tensions, have caused me to wait for further developments."

On the other hand, League leader Matteo Salvini poured cold water on the notion and urged another election. He said, "the earlier we vote the better because it's the best way to get out of this quagmire and confusion." The news that anti-euro League is not interested, but is pushing for election again is also sentiment supportive.

German CPI accelerated to 2.2%, unemployment rate hit record low

Data from Eurozone are generally positive today. German CPI accelerated to 0.5% mom, 2.2% yoy in May, up from 0.0% mom, 1.6% yoy, and beat expectation of 0.3% mom, 1.9% yoy. Retail sales rose much more than expected by 2.3% mom in April versus consensus of 0.5% mom. Import price index rose 0.6%, below expectation of 0.7% mom.

German unemployment dropped -11k in May. Unemployment rate dropped to 5.2%, hitting the lowest level on record since reunification in 1990. Labour Office head Detlef Scheele said in a statement that "unemployment and underemployment have decreased again, employment within the scope of the social security system keeps rising and labour demand is still high." And, "the upward trend on the labour market is continuing, albeit at a slower pace than in the winter months."

Eurozone business climate rose to 1.45 in May, up from 1.39 and beat expectation of 1.30. Economic confidence dropped to 112.5, down from 112.7 but beat expectation of 112.0. Industrial confidence dropped to 16.8, down from 7.3 but met expectation. Services confidence dropped to 14.3, down from 14.7 but met expectation. Consumer confidence was finalized at 0.2.

French GDP was the main disappointment as it's revised down to 0.2% qoq in Q1, down from 0.3% qoq. But that's considered the "past" already.

For Q2, the set German data are rather robust and should ease much concerns of ECB policy makers, in particular the CPI figure.

Swiss KOF dropped to 100, back at long term average

Swiss KOF economic barometer dropped to 100 in May, down from 103.3 and missed expectation of 104.7. KOF noted that the Barometer is back at its "long-term average after over two years of above average values". And that "indicates a normalization of economic development". The decline was "mainly driven by the negative development of the indicators for manufacturing and the construction sector."

Dollar receives no special support from a batch of mixed data.

ADP report showed private sector jobs grew 178k in May, below expectation of 190k. Prior month's figure was also revised down from 204k to 163k. Q1 GDP growth was revised down from 2.3% to 2.2% qoq. GDP price index was revised down from 2.0% to 1.9%. Wholesale inventories rose 0.0% versus expectation of 0.5% in April. Trade deficit narrowed slightly to USD -68.2B, from USD -68.3B.

From Canada, IPPI rose 0.5% mom in April while RMPI rose 0.7% mom. Current account deficit widened to CAD -19.5B in Q1. Focus will turn to BoC rate decision.

China warns to take resolute and forceful measures if Trump insists on being arbitrary and reckless

Chinese Foreign Ministry spokeswoman Hua Chunying responded to the strong US statement released yesterday. She said "we urge the United States to keep its promise, and meet China halfway in the spirit of the joint statement." In addition, Hua warned to take "resolute and forceful" measures to protect its interests if Trump insists on being "arbitrary and reckless" She added that "when it comes to international relations, every time a country does an about face and contradicts itself, it's another blow to, and a squandering of, its reputation."

The White House issued strong worded statement regarding trade relationship with China yesterday. From a fact sheet titled "President Donald J. Trump is Confronting China's Unfair Trade Policies", it's said that "China has consistently taken advantage of the American economy with practices that undermine fair and reciprocal trade." And it accused that "China has aggressively sought to obtain technology from American companies and undermine American innovation and creativity." Simultaneously, there's another statement outlining the Steps to Protect Domestic Technology and Intellectual Property from China's Discriminatory and Burdensome Trade Practices.

OECD projects G20 2018 growth to be 4.0%

In the latest economic outlook report released today, OECD projects 2018-19 global growth to be at around 3.8% while G20 growth would be 4.0%. It noted in the release that "the global economy is experiencing stronger growth, driven by a rebound in trade, higher investment and buoyant job creation, and supported by very accommodative monetary policy and fiscal easing."

However, OECD also warned of "significant risks posed by trade tensions, financial market vulnerabilities and rising oil prices loom large". And it urged that "more needs to be done to secure a strong and resilient medium-term improvement in living standards."

OECD Secretary-General Angel Gurria said that "the economic expansion is set to continue for the coming two years, and the short-term growth outlook is more favourable than it has been for many years." However, "the current recovery is still being supported by very accommodative monetary policy, and increasingly by fiscal easing". Hence, "strong, self-sustaining growth has not yet been attained."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1485; (P) 1.1563 (R1) 1.1616; More.....

Breach of 1.1639 minor resistance indicates temporary bottoming in EUR/USD at 1.1509. Intraday bias is turned neutral for consolidation. Stronger recovery could be seen to 4 hour 55 EMA (now at 1.1700) and possibly above. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds..

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Financial Stability Report | ||||

| 22:45 | NZD | Building Permits M/M Apr | -3.70% | 14.70% | 13.00% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -1.10% | -1.00% | ||

| 23:50 | JPY | Retail Trade Y/Y Apr | 1.60% | 0.90% | 1.00% | |

| 01:30 | AUD | Building Approvals M/M Apr | -5.00% | -3.00% | 2.60% | 3.50% |

| 05:00 | JPY | Consumer Confidence May | 43.8 | 43.9 | 43.6 | |

| 06:00 | EUR | German Retail Sales M/M Apr | 2.30% | 0.50% | -0.60% | |

| 06:00 | EUR | German Import Price Index M/M Apr | 0.60% | 0.70% | 0.00% | |

| 06:45 | EUR | French GDP Q/Q Q1 P | 0.20% | 0.30% | 0.30% | |

| 07:00 | CHF | KOF Leading Indicator May | 100 | 104.7 | 105.3 | 103.3 |

| 07:55 | EUR | German Unemployment Change May | -11K | -10K | -7K | -8K |

| 07:55 | EUR | German Unemployment Claims Rate May | 5.20% | 5.30% | 5.30% | |

| 09:00 | EUR | Eurozone Business Climate Indicator May | 1.45 | 1.3 | 1.35 | 1.39 |

| 09:00 | EUR | Eurozone Economic Confidence May | 112.5 | 112 | 112.7 | |

| 09:00 | EUR | Eurozone Industrial Confidence May | 6.8 | 6.8 | 7.1 | 7.3 |

| 09:00 | EUR | Eurozone Services Confidence May | 14.3 | 14.3 | 14.9 | 14.7 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | 0.2 | 0.2 | 0.2 | |

| 12:00 | EUR | German CPI M/M May P | 0.50% | 0.30% | 0.00% | |

| 12:00 | EUR | German CPI Y/Y May P | 2.20% | 1.90% | 1.60% | |

| 12:15 | USD | ADP Employment Change May | 178K | 190k | 204k | 163K |

| 12:30 | CAD | Current Account Balance Q1 | -19.50B | -$18.15b | -$16.35b | |

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.50% | 0.60% | 0.80% | |

| 12:30 | CAD | Raw Materials Price Index M/M Apr | 0.70% | 2.10% | ||

| 12:30 | USD | Wholesale Inventories M/M Apr P | 0.00% | 0.50% | 0.30% | |

| 12:30 | USD | GDP Annualized Q/Q Q1 S | 2.20% | 2.30% | 2.30% | |

| 12:30 | USD | GDP Price Index Q1 S | 1.90% | 2.00% | 2% | |

| 12:30 | USD | Advance Goods Trade Balance Apr | -68.2B | -71.2B | -68.3B | |

| 14:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | ||

| 18:00 | USD | Federal Reserve Beige Book |

Dollar gets no support as ADP employment missed expectation

Dollar remains generally weak in early US session and receives no special support from a batch of mixed data.

ADP report showed private sector jobs grew 178k in May, below expectation of 190k. Prior month's figure was also revised down from 204k to 163k. Q1 GDP growth was revised down from 2.3% to 2.2% qoq. GDP price index was revised down from 2.0% to 1.9%. Wholesale inventories rose 0.0% versus expectation of 0.5% in April. Trade deficit narrowed slightly to USD -68.2B, from USD -68.3B.

From Canada, IPPI rose 0.5% mom in April while RMPI rose 0.7% mom. Current account deficit widened to CAD -19.5B in Q1. Focus will turn to BoC rate decision.

German CPI accelerated to 2.2%, unemployment rate hit record low

Data from Eurozone are generally positive today. German CPI accelerated to 0.5% mom, 2.2% yoy in May, up from 0.0% mom, 1.6% yoy, and beat expectation of 0.3% mom, 1.9% yoy. Retail sales rose much more than expected by 2.3% mom in April versus consensus of 0.5% mom. Import price index rose 0.6%, below expectation of 0.7% mom.

German unemployment dropped -11k in May. Unemployment rate dropped to 5.2%, hitting the lowest level on record since reunification in 1990. Labour Office head Detlef Scheele said in a statement that "unemployment and underemployment have decreased again, employment within the scope of the social security system keeps rising and labour demand is still high." And, "the upward trend on the labour market is continuing, albeit at a slower pace than in the winter months."

Eurozone business climate rose to 1.45 in May, up from 1.39 and beat expectation of 1.30. Economic confidence dropped to 112.5, down from 112.7 but beat expectation of 112.0. Industrial confidence dropped to 16.8, down from 7.3 but met expectation. Services confidence dropped to 14.3, down from 14.7 but met expectation. Consumer confidence was finalized at 0.2.

French GDP was the main disappointment as it's revised down to 0.2% qoq in Q1, down from 0.3% qoq. But that's considered the "past" already.

For Q2, the set German data are rather robust and should ease much concerns of ECB policy makers, in particular the CPI figure.

CAC Steady Despite Soft French Numbers

The CAC index has steadied on Wednesday, after recording five consecutive losing days. Currently, the CAC is at 5423, up 0.01% on the day. On the release front, key French indicators disappointed. Consumer Spending declined 1.5%, well off the estimate of 0.2%. Preliminary GDP dropped to 0.2%, shy of the estimate of 0.3%. In the US, the key event is Preliminary GDP, with an estimate of 2.3%. On Thursday, inflation indicators will be in focus, as France and the eurozone release CPI reports.

Is the bleeding over? The CAC index has hit some strong headwinds, declining 3.6% since May 23. Investors have reacted negatively to the continuing political turmoil in Italy, the Eurozone’s fourth-largest economy. The drama started when President Sergio Mattarella shocked the political establishment, rejecting the choice for finance minister of the two parties which were expected to form a coalition, the League Nord and the Five Star Movement. Mattarella said he could not support the nomination of a finance minister who was in favor of Italy leaving the eurozone. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. However, there are reports that the League and Five Start Movement could get another kick at the can to form a government. Another possibility is that Italy will hold a snap election. It’s doubtful if another election would change the political landscape, so Matterella will likely huddle with political leaders and seek a compromise in order to avoid another general election.

Investors are also keeping a close eye on the on-again off-again summit between the U.S and North Korean leaders. President Trump and North Korean leader Kim Jong-un are scheduled to meet in Singapore on June 12, but curiously, neither side will confirm whether the meeting is on. Last week, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the White House has since sent a team to Singapore and a senior North Korean official is on his way to Washington to meet with Secretary of State Mike Pompeo. If there is confirmation that the meeting is on, traders can expect global stock markets to gain ground.

DAX Recovers As German Consumer Spending Jumps

The DAX has moved higher in Wednesday session, after two consecutive losing sessions. Currently, the DAX is at 12,762, up 0.75% on the day. In economic news, German retail sales jumped 2.3%, easily beating the estimate of 0.5%. Later in the day, Germany releases Preliminary CPI, which is expected to rise to 0.3%. In the US, the key event is Preliminary GDP, with an estimate of 2.3%.

European stock markets are seeing red and the DAX is down 2.2% this week, despite rebounding on Wednesday. The decline is in response to the continuing political drama in Italy, the Eurozone’s fourth-largest economy. The drama started when President Sergio Mattarella stunned the nation, rejecting the choice for finance minister of the two parties which were expected to form a coalition, the League Nord and the Five Star Movement. Mattarella said he could not support the nomination of a finance minister who was in favor of Italy leaving the eurozone. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. However, there are reports that the League and Five Start Movement could get another kick at the can to form a government. Another possibility is that Italy will hold a snap election. It’s doubtful if another election would change the political landscape, so Matterella will likely huddle with political leaders and seek a compromise in order to avoid another general election.

German retail sales were unexpectedly strong in April, with a sharp gain of 2.3%. This reading ended a nasty streak of four declines. The gain is the strongest since December, and raises hopes that second quarter growth will rebound after a sluggish first quarter. Inflation is also expected to improve, with German Preliminary CPI forecast to rise to 0.3% in May after a flat reading of 0.0% in April. The story in France, the second largest economy in the eurozone, was not as bright. Consumer spending plunged 1.5% in April, marking a 3-month low. Preliminary GDP fell to 0.2% in March, down from 0.6% a month earlier.