Sample Category Title

USDCHF Outlook: Stands At The Back Foot And Pressures Key Supports

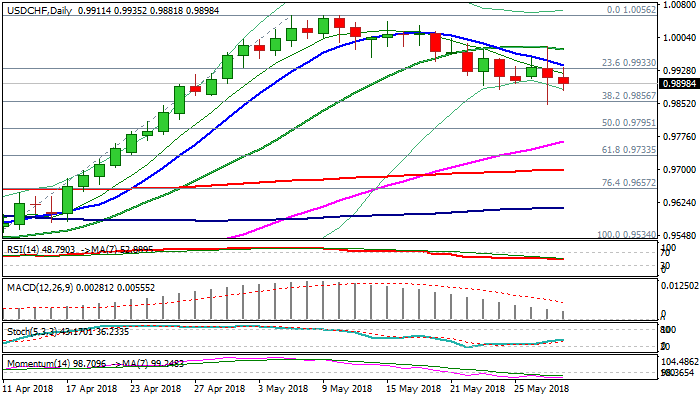

The pair remains in red on Wednesday but holds above Tuesday's low at 0.9850, when strong bearish acceleration cracked key supports at 0.9881 (top of weekly cloud) and 0.9856 (Fibo 38.2% of 0.9534/1.0056 upleg) but failed to clearly break lower. Political crisis in Italy triggered risk aversion which boosted safe-haven Swiss franc. Bearish setup of 10/20SMA's and weak momentum maintain pressure for renewed probe through 0.9881/56 pivots, with firm break lower to generate strong bearish signal for extension of pullback from 1.0056 peak. Bears can extend towards next key supports at 0.9725 (Fibo 38.2% of 0.9190/1.0056 ascend) and 0.9700 (top of rising daily cloud). Falling 10SMA (0.9939) caps today's action and marks strong barrier which should continue to limit and keep bears in play. SNB chief Jordan's speech, due later today is also in focus.

Res: 0.9939, 0.9957, 0.9976, 1.0000

Sup: 0.9881, 0.9850, 0.9795, 0.9763

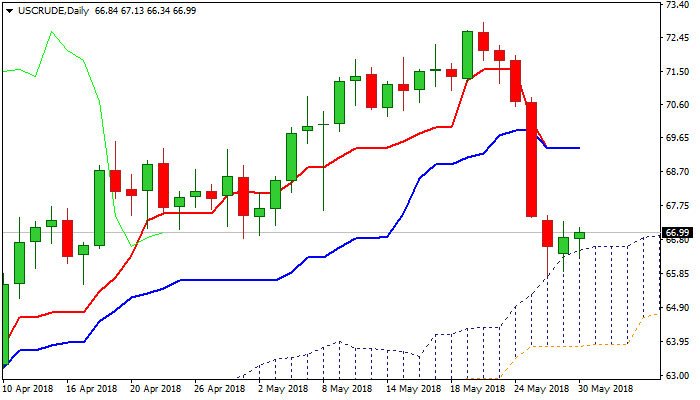

WTI Oil Outlook: Basing Attempt Above Rising Daily Cloud, Weekly Crude Stocks Data Eyed For Fresh Signals

Basing attempts are seen on daily chart as oil price holds for the third straight day above the top of rising daily cloud which so far contained steep fall in past few days. Profit-taking could boost the price and signal reversal on break above rising 55SMA ($67.20) and $67.47 (Fibo 23.6% of $72.89/$65.79) to expose next pivots at $68.22 (top of thick hourly cloud) and $68.50 (Fibo 38.2% of $72.89/$65.79 fall). Slow stochastic is turning up in oversold territory and supports the notion, but south-heading momentum daily MA's in bearish configuration maintain pressure and warn of recovery stall. US weekly crude stocks data are in focus for fresh direction signals, after oil prices suffered heavy losses on fears of increase of output from main world oil producers. Releases are delayed one day due to US holiday, with API data due later today, while EIA is going to release its weekly report on Thursday. Bearish scenario requires final break and close below daily cloud top ($66.50) and also close below $66.04 (Fibo 61.8% of $61.80/$72.89) to generate strong bearish signal for continuation of fall from $72.89 (22 May low).

Res: 67.20, 67.49, 68.28, 68.50

Sup: 66.50, 66.04, 65.79, 65.55

Markets Pare Losses As Italy Tries To Resolve Political Stalemate

- Five Star and Lega Reopen Discussions on Forming Government;

- BoC Decision and US Data Eyed.

US futures are paring losses ahead of the open on Wednesday, similar to the moves we’re seeing in Europe as political uncertainty in Italy continues to act as a drag on risk appetite.

It looked as though we were headed for fresh elections as early as July, with negotiations between Five Star Movement and Lega having failed after President Sergio Mattarella vetoed their choice of Finance Minister. Carlo Cottarelli – a former IMF economist - was tasked with forming a temporary government until further elections are called, ideally next year, but that appears to have failed before it got started.

While early elections will arguably be very beneficial to the populist parties, who will cite the rejection of its choice of Finance Minister as evidence of Brussels interference and an abuse of the democratic will of the people, it seems one last attempt to form a government is being discussed. The parties seem unwilling to hold an election in July and have no desire to wait until next year.

If a government can be formed that receives the stamp of approval from Mattarella and is therefore seen as not posing a threat to Italy’s place in the eurozone, then this will come as a relief to markets in the near-term. Longer-term risks remain though and both parties will likely use recent events as a platform to drum up opposition to the euro with the end goal of holding its own referendum, something eurozone leaders will understandably fear after the UK result in 2016.

While the situation in Italy will likely continue to be a driver of market sentiment, there are plenty of data releases that will be of interest to traders today as well as an interest rate decision from the Bank of Canada. While the central bank is not expected to hike interest rates at the meeting, at least one more is priced in for this year and possibly a second so the statement that accompanies the decision will be monitored closely.

We’ll get an early look at US employment in May today, with ADP releases its estimate ahead of the official jobs report on Friday. While this is typically not entirely reliable as an estimate of the non-farm payrolls figure, it could give us some insight into whether markets are well positioned or not. We’ll also get a revised GDP reading for the US for the second quarter, which is expected to be unchanged at 2.3% on an annualised basis.

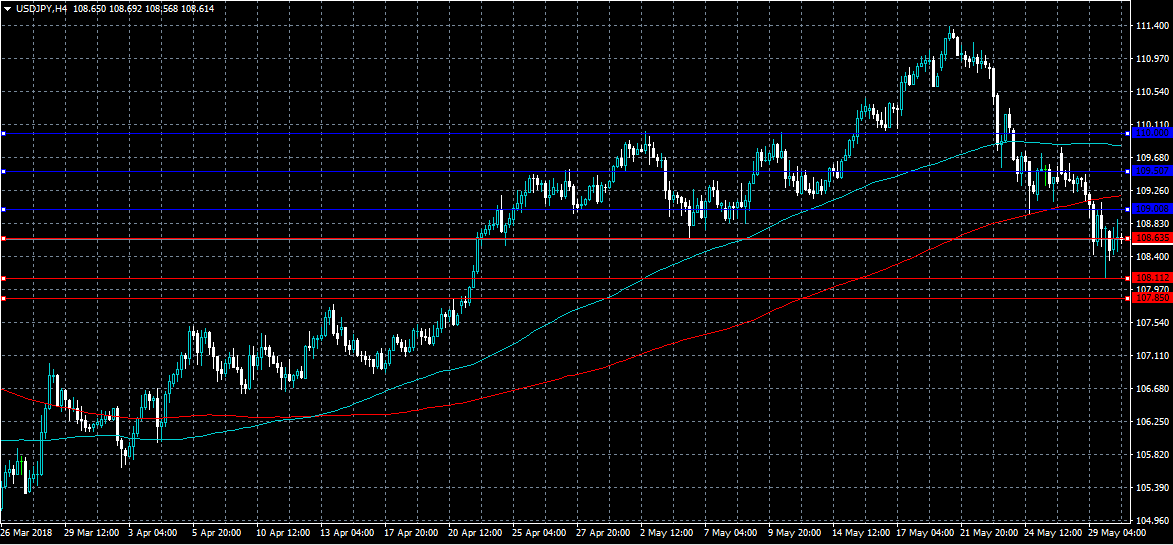

USDJPY Still Under Pressure Below 109.00

The US dollar continues to trade to the downside against the Japanese yen currency, as investors flock to safe-haven currencies, which is helping to underpin yen demand. The USDJPY pair currently trades around the 108.60 level, with price earlier falling to a fresh monthly-low, hitting 108.11. Traders now look towards a slew of market moving economic data from the United States economy.

The USDJPY pair remains strongly bearish while trading below the 109.00 level, further losses towards 108.11 and 107.85 remain likely.

If USDJPY buyers move price back above 109.00 level, we may see a correction towards the 109.50 and 110.00 levels.

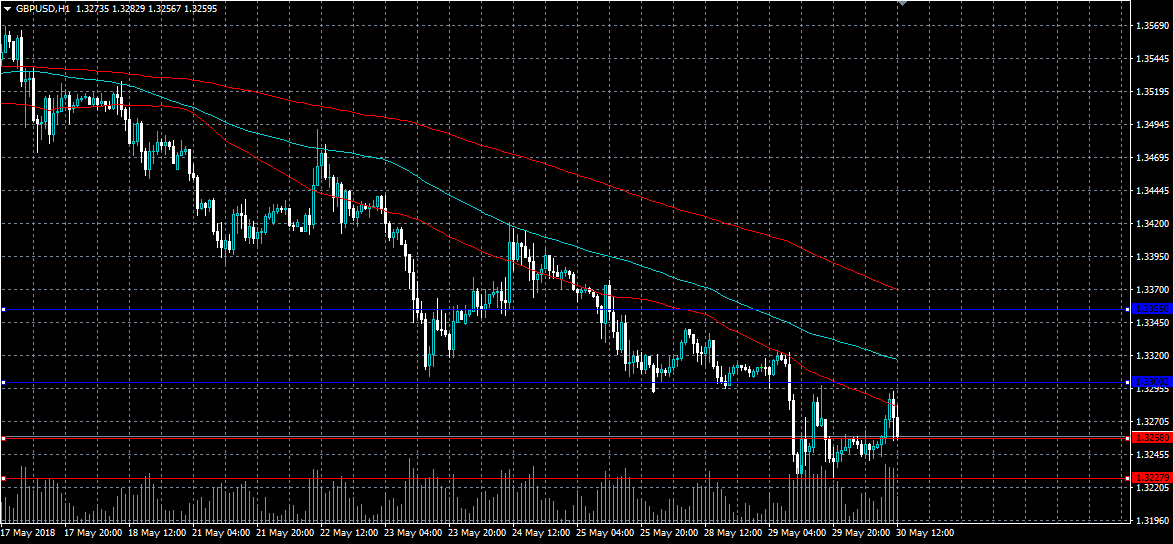

GBPUSD Strong Rehection From 1.3300 Level

The British pound remains under selling pressure against the greenback, after price was strongly rejected from the 1.3300 level during the European trading session. The GBPUSD pair currently trades back towards the 1.3258 support level, as bearish downside pressures persist. Traders now look towards the release of key Inflation, Jobs and GDP data from the United States economy.

The GBPUSD pair is strongly bearish while trading below the 1.3300 level, key intraday support is located at the 1.3258 and 1.3200 levels.

If the GBPUSD pair moves above the 1.3300 level, we may see price bounce towards the 1.3355 and 1.3370 resistance levels.

Euro Continues Recovery As Italy Looks For Early Elections, BoC Rate Decision Ahead

Here are the latest developments in global markets:

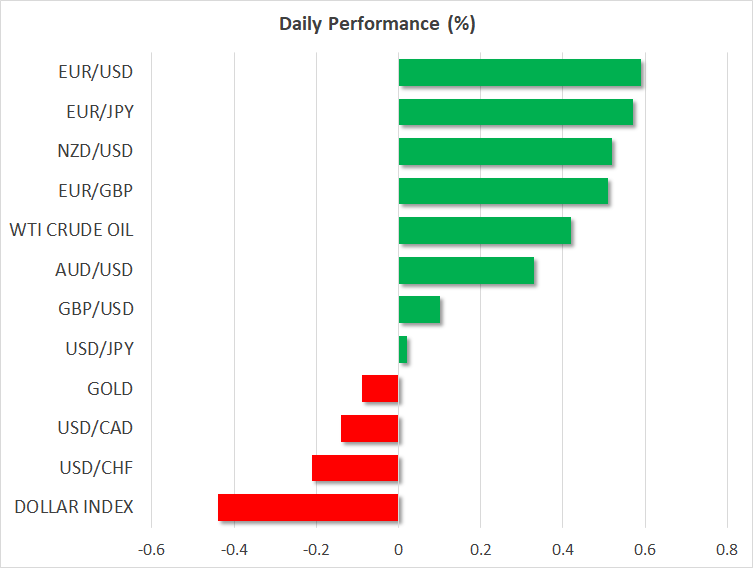

FOREX: The single currency rebounded on Tuesday’s 10-month low near 1.1500 against the greenback (+0.67%) as concerns about Italy’s political crisis remains in focus and there is a chance of new elections taking place on July 29. In data, economic sentiment in the Euro area came in slightly higher than expected in May at 112.5 but below the April’s mark of 112.7. Pound/dollar traded higher by 0.14% to 1.3269 following the 6-month low of 1.3203 that it posted on Tuesday. Dollar/yen rose above its intraday low of 108.34 and entered positive ground (+0.05%) before the announcement of the second estimate of Q1 GDP. The dollar index against a basket of six major currencies headed down by 0.42% following three consecutive green days. The antipodean currencies traded higher, with aussie/dollar up at 0.7534 (+0.40%) and kiwi/dollar climbing to 0.6938 (+0.49%). Dollar/loonie moved lower by 0.19% near 1.3000 ahead of the BOC interest rate decision later in the day. Meanwhile, dollar/Turkish lira plunged by 1.39% to 4.4871.

STOCKS: European equities were in the green at 1130 GMT except the French CAC 40 which eased by 0.09%, set to complete the six straight bearish day. The benchmark European STOXX 600 rose by 0.22% following five red days. The blue-chip Euro STOXX 50 was up by 0.23%, while the German DAX 30 increased by 0.71%. The Spanish IBEX 35 gained 0.93%, while the British FTSE 100 advanced by 0.33%. In the US, even though the S&P, Dow Jones, and the Nasdaq all plunged yesterday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices edged up during the European trading session on Wednesday, paring the previous week’s losses but remaining elevated from the six-week low reached on Monday. WTI was up by 0.31% near the $67 handle, while Brent crude jumped by 0.54% to $75.81. In precious metals, gold edged marginally lower by 0.03% as concerns about the political turmoil in Italy and an escalation in the China-US trade conflict failed to lift prices.

Day ahead: Bank of Canada to stand pat on rates; German inflation in focus

The economic calendar will be busy in terms of data releases later in the day, while a rate decision in Canada and political conditions in Italy will be in the spotlight as well.

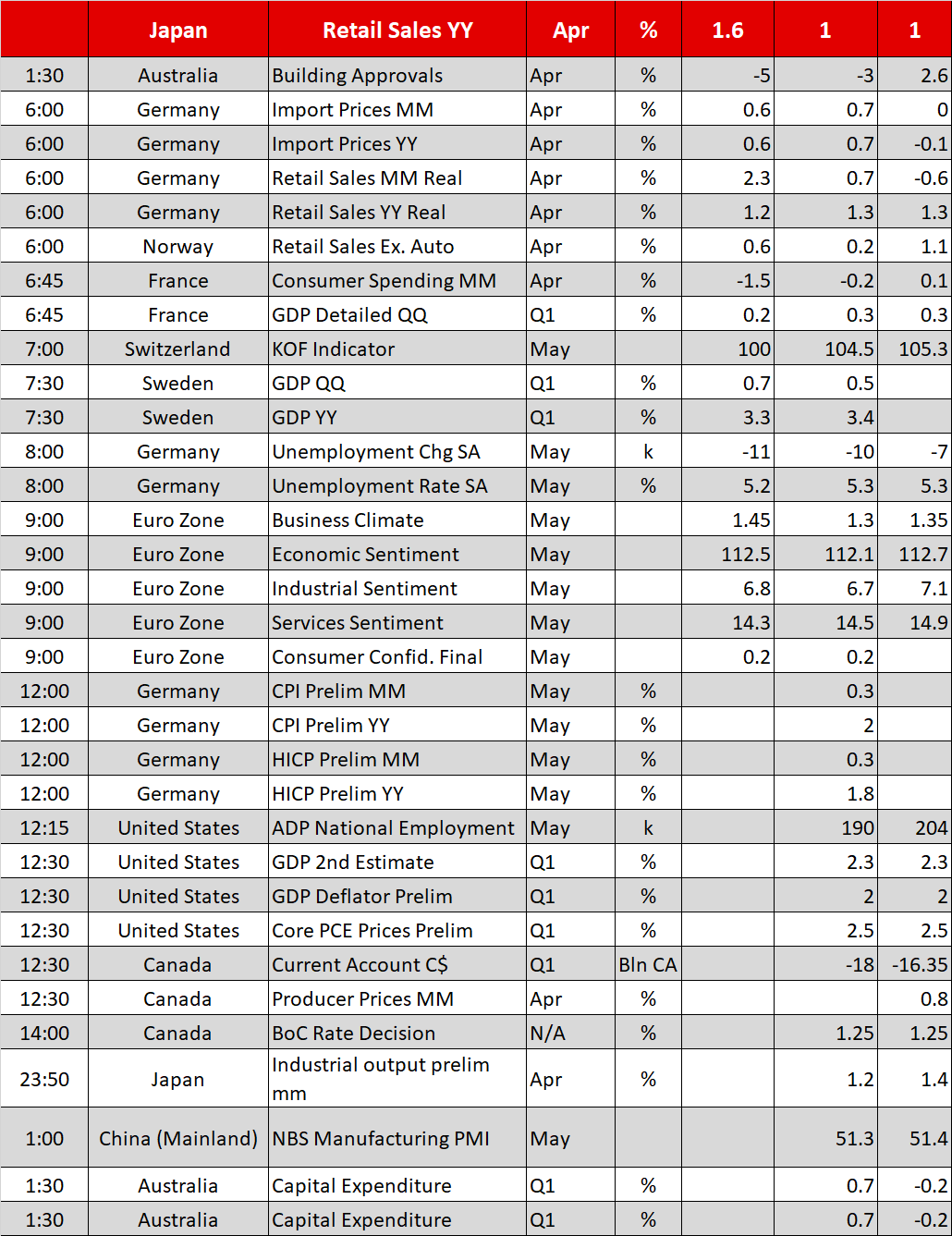

At 1200 GMT, Germany, the EU’s largest economy, will publish preliminary readings on inflation for the month of May and forecasts are for the numbers to show an improvement after remaining steady in the past two months. Particularly the headline consumer price index (CPI) is expected to climb from 1.6% to 2.0% y/y, reaching the highest level since February. The harmonized CPI, which is comparable to other EU countries, is seen higher as well, at 1.8% y/y compared to 1.4% in April. In case the data surprise to the upside, investors could turn more optimistic that Thursday’s Eurozone flash inflation figures could also rise, helping the euro to recover.

Yet the political turmoil in Italy could limit any potential gains in the common currency on fears the Italian President Sergio Mattarella could dissolve parliament and call for fresh elections as soon as July 29 in the next couple of days according to sources with knowledge. Recall that over the weekend, Mattarella rejected the choice for the minister of economy proposed by the populists parties, but it is being reported today that these anti-establishment parties, the Five-Star Movement and the League party, were pushing efforts again to form a government.

A few minutes later, at 1215 GMT, the ADP research institute in the US will release its national employment report for the month of May, two days before the government’s famous nonfarm payrolls come into light. The report regarding the US nonfarm private sector is expected to indicate a slowdown in the number of people being employed, with analysts projecting a rise of 190k jobs, less than the 204k increase seen in the previous month. The data could be a good indication of what investors could expect from the government’s nonfarm payrolls,which measures employment changes both in the private and public nonfarm sectors.

Staying in the US, the second estimates on Q1 GDP growth and PCE prices will attract attention at 1230 GMT, with analysts waiting for both measures to confirm their initial estimates: GDP growth to stand at 2.3% on an annualized basis and PCE prices to rise by 2.5% y/y. Traders will also keep a close eye at the Fed’s Beige book which states current economic conditions in 12 Fed districts at 1800 GMT.

Meanwhile in Canada, stats on producer prices and the current account will be available at 1230 GMT, but the Bank of Canada’s monetary policy meeting due at 1400 GMT will be the main headline of the day. Analysts anticipate the central bank to hold interest rates unchanged at 1.25% for the fifth time despite a strong labor market and inflation around the target. Factors such as uncertainties around NAFTA and US trade protectionism in general are likely to keep policymakers cautious, while households’ overloaded debt obligations could also remain a concern. Still, any hawkish messages out of the rate statement following the decision could increase chances for stimulus reduction later this year. Note that the markets are currently pricing in two rate hikes coming in July and December. No press conference or financial projections are scheduled for this meeting.

In oil markets, the American Petroleum Institute will give an insight on US crude stocks for the week ending May 25 at 2030 GMT.

Elsewhere, industrial production figures out of Japan will come under review at 2350 GMT, while early on Thursday, Chinese manufacturing PMI (0100 GMT), New Zealand’s ANZ business confidence (0100 GMT) and Australia’s capital expenditure readings (0130 GMT) will be released.

Any developments on the trade front will be closely watched during the day after China warned the US today it would retaliate if the US was looking to start a trade war. This followed yesterday’s announcements that Washington’s threats of imposing import tariffs on $50 billion Chinese products were still open. Note that the US Commerce Secretary, Wilbur Ross will fly to Beijing this week in an effort to increase US exports to China.

In other economic events, G7 finance and development ministers, as well as central bank governors will meet today on the theme of “investing in growth that works for everyone”. The meeting will end on June 2.

Into US session: Oversold Euro recovers broadly, markets won’t forget there are US trade tensions

Euro is making a strong come back today as market digest recent sharp losses. EUR/USD breached 1.1639 minor resistance while EUR/JPY break 126.43. Both developments suggest temporary bottoming. Though, they're far from reversing recent down trend. And, at the time of writing, German (0.369) and Italy (2.864) yield spread are still close to 250, which suggests much nervousness in the markets.

Though, the news that 5-Star Movement is trying to find a point of compromise for economy minister is supporting sentiments. At least, they're working on forming a government again. And while being highly critical, 5-Star has never committed themselves to leaving Euro. The news that anti-euro League is not interested, but is pushing for election again is also sentiment supportive. Additionally, Eurozone data released today are not bad.

Yen and Dollar, on the other hand, are trading broadly lower. Yen weaken on rebound in German, UK and US yields. Meanwhile, Dollar is weak as markets won't forget that the US is in trade tension with many other countries/regions, even its own allies. NAFTA talk is going nowhere and there is no positive news regarding trade talk with EU. The steel tariff temporary exemption is going to expire on Friday and retaliations from Canada, Mexico and the EU are waiting on the line. Trump also made an about turn and issued a strong statement regarding China yesterday, indicating very little intention to carry on with negotiation.

For the week, Euro remains the weakest one, followed by Sterling. New Zealand Dollar and Japanese Yen are the strongest ones.

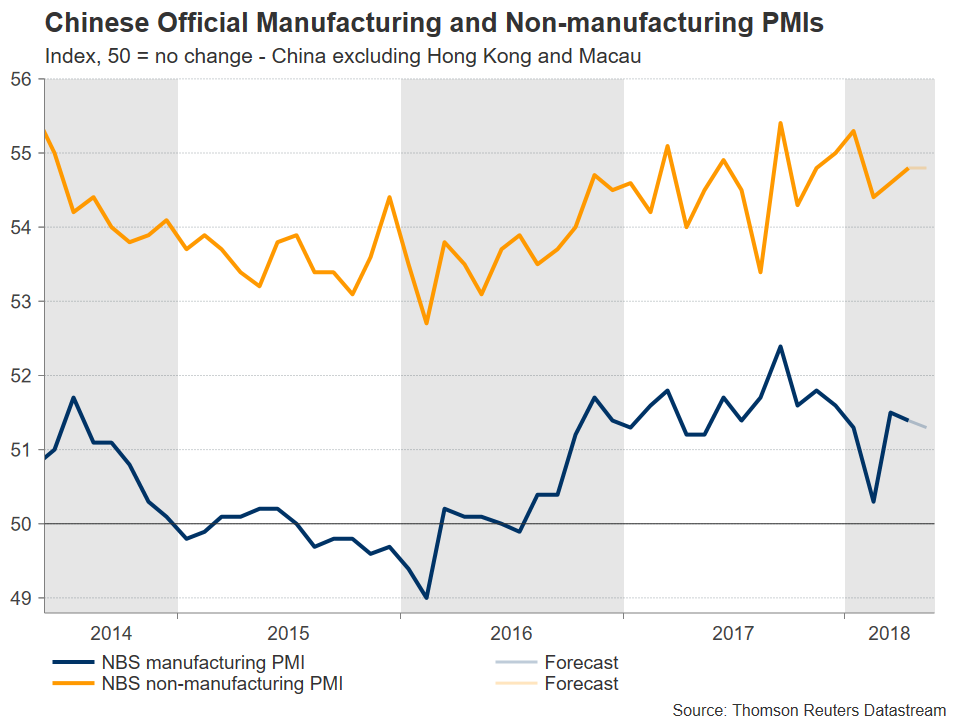

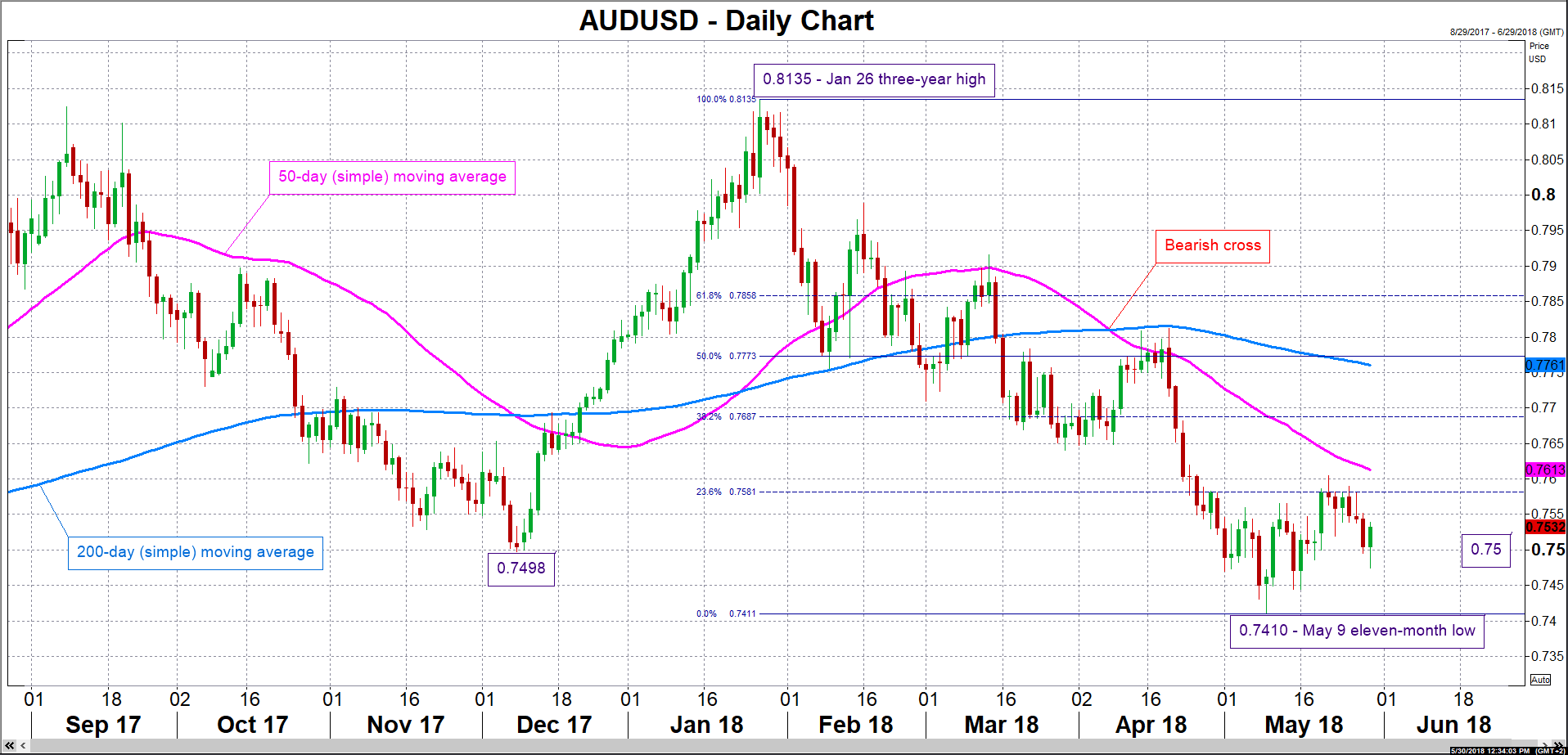

Chinese PMIs Due With Trade Developments Remaining In The Background, Aussie Also Attracts Attention

Chinese official PMI data for May are scheduled for release on Thursday at 0100 GMT. Manufacturing activity, which is expected to attract most interest, is anticipated to marginally ease though still remain in expansion territory. In the bigger picture, besides data releases, trade talks between the US and China continue taking place and have the capacity to act as market movers.

Data releases due on Thursday are projected to show China’s official manufacturing PMI coming in at 51.3 from April’s 51.4, and the respective non-manufacturing (services) PMI remaining at 54.8 for the second straight month; a reading above 50 denotes sectoral expansion. Despite the services sector gaining greater prominence over the last number of years as part of the efforts to rebalance – and might be argued to diversify – the Chinese economy, the data on manufacturing activity are expected to be gathering more interest than those on non-manufacturing PMI.

Should the number on manufacturing indeed be released above 50, this would constitute nearly two straight years of expansion in the sector as gauged by the purchasing managers’ index and attest to the resilience of the world’s second largest economy, despite fears for a slowdown in 2018. Such fears are partly owed to efforts by the Communist party to rein in excessive debt levels that could eventually lead to a credit crisis.

The private Caixin/Markit manufacturing and non-manufacturing PMI figures, which focus on small and mid-size businesses, as opposed to the official data which are broader in nature, are due on Friday and Tuesday next week correspondingly, and will also be attracting attention. The Caixin manufacturing PMI is forecast to mirror the move in the official data, ticking down to 51.0 from April’s 51.1. Related to the Caixin data, it is notable that some analysts are warning that rising credit defaults are signaling growing pressure on small and medium-sized firms.

In FX markets, Australia’s close economic ties with China – the former is the latter’s largest export and import partner – have rendered the Australian dollar a liquid proxy for China’s economy. In this respect, besides the yuan, the aussie will also be monitored as the PMI data go public; a strong Chinese economy is seen as aussie-positive.

A data beat might lead to buying interest for the aussie/dollar pair. Resistance to advances could come around the 23.6% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7581, with the region around this point also encapsulating the 0.76 round figure. Stronger bullish movement might meet additional barriers around the current level of the 50-day moving average line at 0.7613 and the 38.2% Fibonacci mark at 0.7687. Weaker-than-anticipated figures on the other hand, could put AUDUSD under downside pressure. Support to losses might initially emerge around the 0.75 handle – the area around this level includes a bottom from December at 0.7498 – with steeper losses increasingly bringing into focus the 11-month low of 0.7410 recorded on May 9.

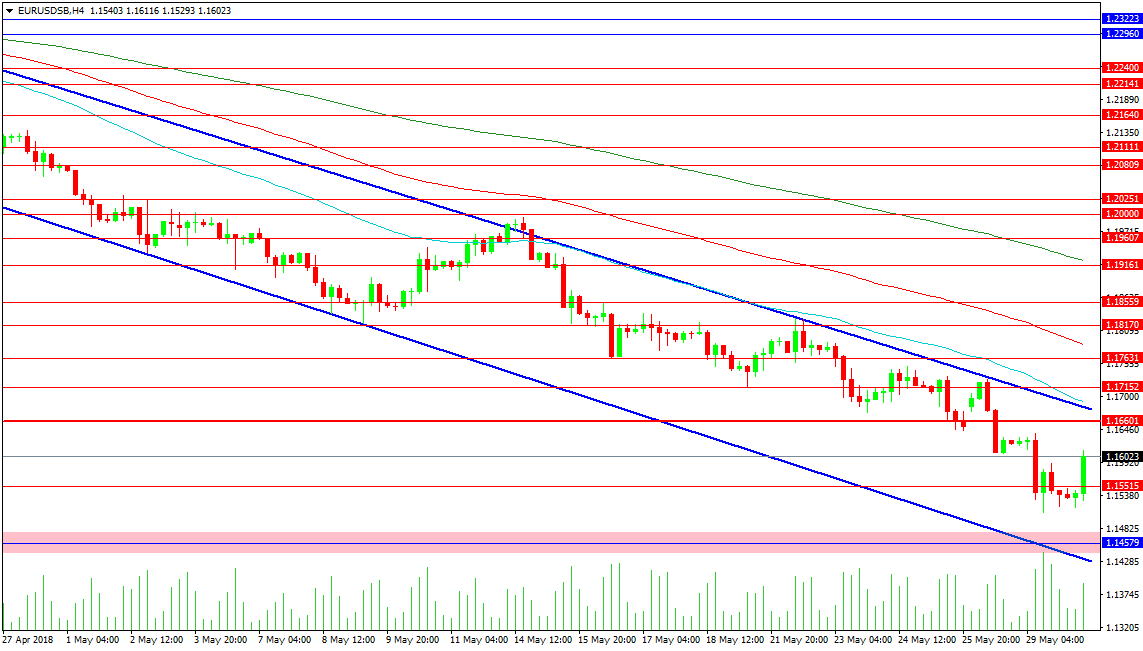

Forex Analysis: EURUSD and NZDUSD

The EURUSD pair has slipped to the levels of July 2017 just ahead of 1.15000 support. The pair is having a relief rally this morning but price is still trading inside the down trend of recent weeks. Yesterday’s low was 1.15096 and a loss of this supporting area would see prices extend towards 1.14579 which represents an area of support that could see buyers step in. The channel bottom comes in at 1.14280 today with 1.14000 support close-by. Bearish traders would welcome a rejection of resistance with a retracement higher working out oversold conditions.

The channel top is at the 1.16800 level today with price currently trading above 1.16000. The 50 period MA is found close to the channel top at 1.16922 presenting a barrier to any break above that area. Given the oversold conditions the ability of this area to hold price could be weak, with a short squeeze taking price above 1.17000 to the 100 period MA at 1.17868. This area would provide a junction for traders to either continue with fresh shorts or attempt to take price to higher levels. The selloff has been deepened by the Italian Political Crisis so traders will need to stay abreast of the situation there.

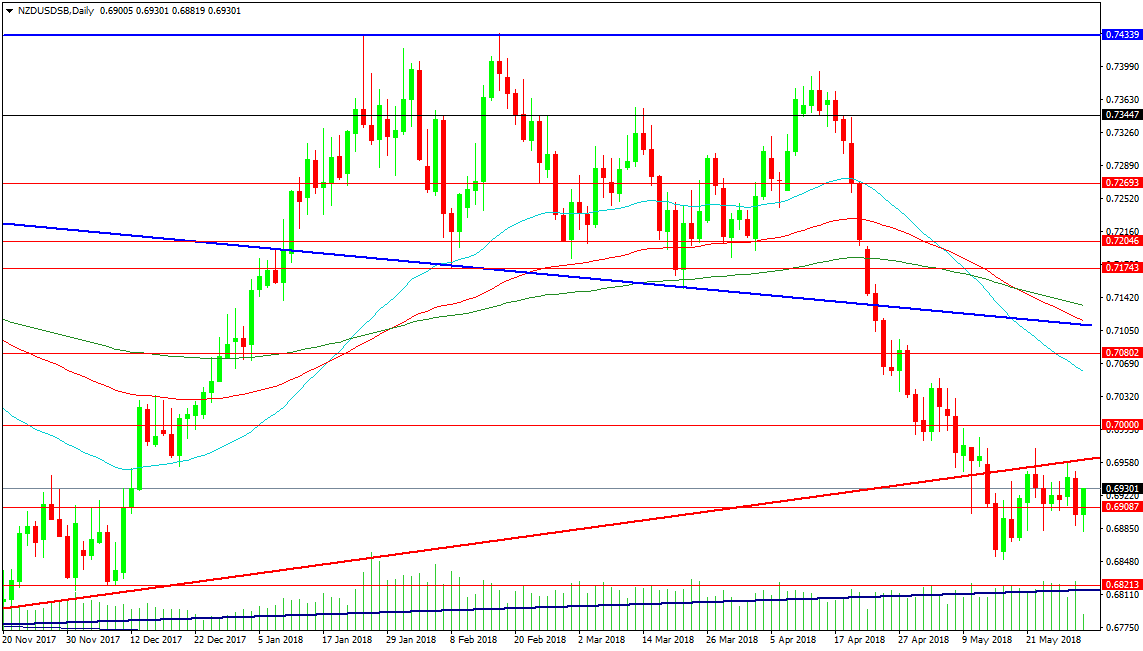

NZDUSD

The NZDUSD pair is consolidating below the broken red support trend line since the middle of May. The consolidation is centred on 0.69000 and the breakout should provide traders with an opportunity to engage with the market. A break under 0.68500 could see the supporting long term blue trend line tested at 0.68165 with a loss of this area targeting 0.67000 and 0.66430 in extension. The Double top pattern at 0.74340 played out very well and once the target area was hit at 0.69150 the momentum in the move lower has stalled leading to the sideways price action we now find price in.

A retracement higher would first need to overcome the red trend line at 0.69613 followed by the 0.70000 level. This would lead on to the falling 50 DMA at 0.70596 and the more resistive blue trend line at 0.71105. This line has the 100 DMA at 0.71166 and the 200 DMA at 0.71337 providing close support. A break out towards the recent highs faces resistance at 0.72000 and 0.74000 before the double top level is retested.

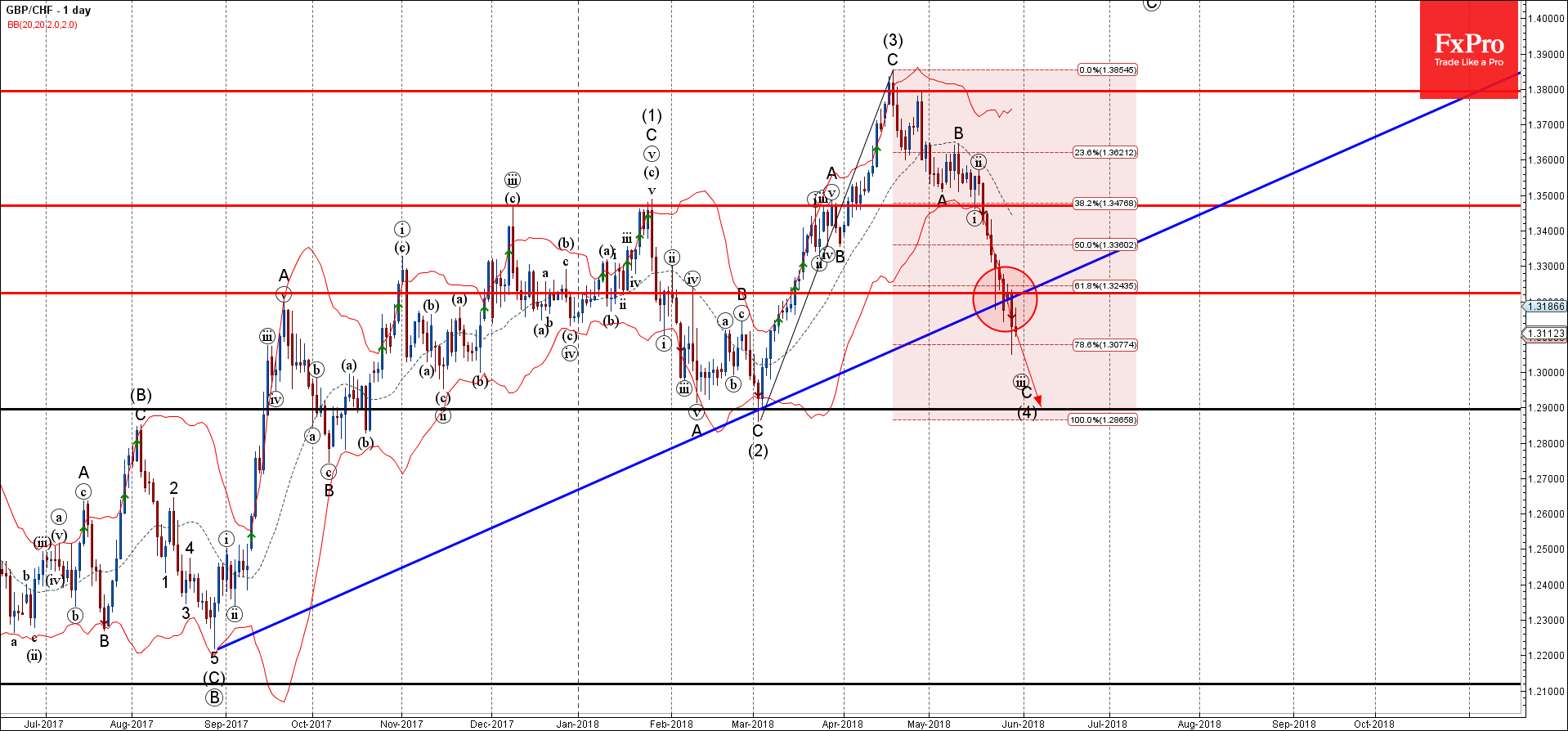

Forex Analysis: GBPCHF Wave Analysis

GBP/CHF falling inside short-term impulse wave C

Further decline are likely

GBP/CHF continues to fall inside the short-term impulse wave C, which belongs to the medium-term ACB correction (4) from the middle of April.

The price earlier broke through the support zone lying between the support level 1.3220, support trendline from the end of August and the 61.8% Fibonacci retracement of the previous strong upward impulse (3) from March.

The breakout of the aforementioned support zone accelerated the active impulse wave C – increasing the probability the price will continue to fall toward the next key support level 1.2900 (low of the previous wave (2)).