Sample Category Title

Bank Of Canada Next

Wednesday May 30: Five things the markets are talking about

The Bank of Canada (BoC) is expected to leave its benchmark interest rate unchanged (+1.25%) during its policy meeting today (10:00 am EDT) amid concern over slowing housing markets and stalled Nafta trade negotiations.

However, market consensus expects the BoC’s next rate increase to come in July, as long as Q2 economic growth looks strong and housing markets begin to stabilize.

Note: The BoC has lifted its key rate three-times since last summer, most recently in January. Last month, Canadian policy makers said further rate increases would likely be warranted over time, but added that the BoC would remain cautious and use incoming economic data to guide their decisions.

Currently, Canadian house prices are cooling in many cities following the introduction of tougher mortgage financing rules earlier this year. Sales of existing homes have fallen nearly -3% in April y/y, while prices on an annual basis rose at the slowest pace in nearly a decade.

Net result, a slight softening in recent economic data along with uncertainty over trade with the U.S is expected to keep the BoC on hold.

Elsewhere, the sovereign bond market is showing signs of stabilization overnight after the impressive rout in Italian debt sent investors seeking the exit doors. U.S Treasuries have fallen back with the ‘mighty’ dollar as the haven bid subsided, the EUR has climbed and Euro stocks are somewhat steady.

In technical terms, the market is catching its breath while the prospect of snap Italian elections – which could effectively become a referendum on the ‘single’ unit – continues to threaten, the market sees the intraday selloff as overdone while the timing of any vote remains unclear.

On tap: E.U trade chief Cecilia Malmstrom and U.S Commerce Secretary Ross are scheduled to meet today in an informal WTO meet in Paris. Bank of Canada (BoC) monetary policy announcement at 10:00 am EDT.

1. Stocks mixed results

In Japan, the Nikkei tumbled to six-week low overnight after political turmoil in Italy sparked concerns over the stability of the eurozone, hitting financial and exporter shares in particular. The Nikkei ended -1.5% lower and managed to stay above its 75-day moving average, which has become the index’s immediate support level. The broader Topix fell -1.4%.

Down-under, Aussie stocks did not fall as much as others in the region as the S&P/ASX 200 fell for the eight consecutive session. It dropped -0.5% as financials shed -1.4% and hit a 18-month low amid the global selloff seen amid worries about Italy and the subsequent slump in U.S Treasury yields. In S. Korea, the Kospi was one of Asia’s bigger decliners overnight. The Kospi fell -2%, the most since late March and an eight-week closing low, as Samsung slid a further -3.5%. That put the week’s drop to date at -6.1%.

In Hong Kong, stocks fell to a three-week closing low overnight; with investor sentiment dampened by the political crisis in Italy and renewed fears over a Sino-U.S. trade war. The Hang Seng index fell -1.4%, while the China Enterprises Index lost -1.6%.

In China, equities fell the most in more than two months overnight, with the Shanghai Composite Index hitting a 19-month closing low, amid a global selloff provoked by global geopolitical worries. The blue-chip CSI300 index fell -2.1%, while the Shanghai Composite Index dropped -2.5%.

In Europe, regional bourses have opened broadly flat with a hint of positivity. Waning concerns over periphery elections supports is supporting stocks, with Italy and Spain outperforming core Europe.

U.S stocks are set to open in the ‘black’ (+0.2%).

Indices: Stoxx50 -0.1% at 3,424, FTSE +0.1% at 7,642, DAX +0.4% at 12,711, CAC-40 -0.6% at 5,406; IBEX-35 +0.3% at 9,555, FTSE MIB +0.8% at 21,517, SMI -0.3%, S&P 500 Futures +0.2%

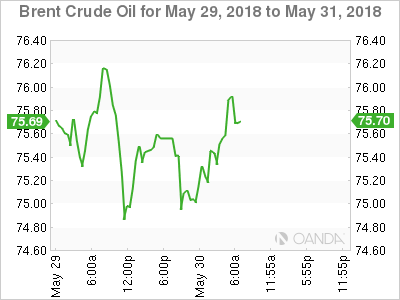

2. Oil slips, as threat of OPEC boost weighs, gold lower

Oil has slipped again overnight, under pressure from expectations that OPEC will pump more and as Italy’s political crisis increased investors’ aversion to risk.

Brent is down -3c at +$75.36 a barrel, after trading as low as $74.81 earlier. U.S crude is up +3c at +$66.76.

Brent crude has dropped -$5 from its four-year high of +$80.50 a barrel on May 17, after reports that OPEC and Russia may increase supply at next month’s OPEC meeting (June 22), reversing policy after 17-months of cutting supplies.

Note: OPEC and non-OPEC producers have had a pact to curb output by about -1.8m bpd since January 2017. The cutbacks have largely removed excess global inventories.

Amid concerns the price rally has gone too far, Saudi Arabia and Russia are discussing raising OPEC and non-OPEC oil output by around +1m bpd.

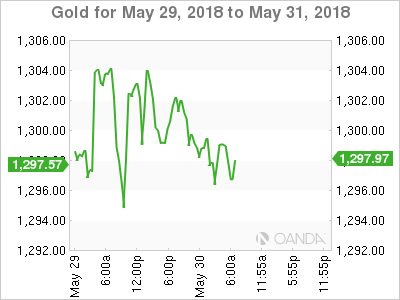

Ahead of the U.S open, gold prices have edged a tad lower overnight as a robust U.S dollar weighed on the market, but concerns about political turmoil in Italy and Sino-U.S trade conflict is limiting losses. Spot gold is -0.2% lower at +$1,296 per ounce, while U.S gold futures for June delivery are down -0.3% at +$1,295.40 per ounce.

3. Yield trading not for the faint of heart

Italian bond are rebounding, with the 10-year yield falling as much as -19 bps, to +2.98% as global panic eases. The U.S. benchmark bonds have given up some of yesterday’s gains to send yields back above +2.80%.

Italian government bond yields have pushed away from their multi-year highs from yesterday as the market uses the opportunity to snap up cheap paper.

The two-year government bond, the focus of recent selling, was down -33 bps at +2.095%, having hit its highest level in five-years in early trading.

Note: The closely watched Bund/BTP 10-year bond yield spread has tightened -13 bps to +269 bps compared to yesterday’s close of +283 bps.

Elsewhere, the yield on U.S 10-year Treasuries has climbed + 7 bps to +2.85%, the biggest increase in more than two-weeks. In Germany, the 10-year Bund yield has climbed +7 bps to +0.33%, the first advance in more than a week and the largest surge in almost six weeks. In the U.K, the 10-year Gilt yield has gained +6 bps to +1.197%, the biggest climb in almost two-weeks.

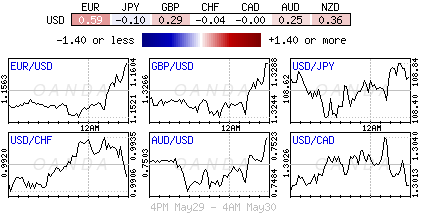

4. Dollar bulls book some profit

The overnight session has seen a slight reversal in the recent risk aversion flows, with the ‘big’ dollar subject to consolidation as some of its interest rate support has eased with the U.S yield curve flattening. Despite Italian and Spanish political uncertainty, there seems to be less volatility in their respective yield curves.

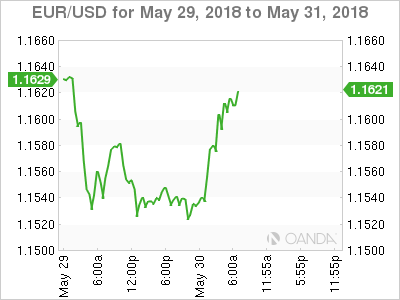

Earlier this morning, Euro inflation data for May appears to have provided some support for the ‘single’ unit. The EUR/USD has moved back above the psychological €1.16 handle (€1.1615) to recover from its recent ten-month lows.

GBP/USD little changed at £1.3266 while USD/JPY trades atop of ¥108.78 ahead of the N.Y open.

In EM markets, the TRY has jumped +0.6% to $4.5211, the strongest in more than a week.

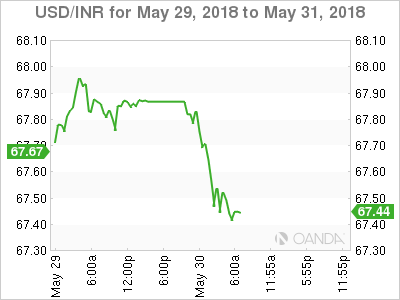

5. Indonesia raises interest rates again

Indonesia’s central bank raised its benchmark interest rate for the second time in two-weeks, in their latest attempt to tame the effects of a stronger dollar.

Bank Indonesia (BI) has lifted the seven-day reverse repo rate to +4.75% from the previous +4.5%, a move that had been widely expected.

Note: It had earlier raised the rate by +25 bps on May 17.

This move is being considered as a pre-emptive, front-loading and ahead-of-the curve policy response.

The INR has strengthened +0.1% outright after falling to a three-year low last week, driven by a broad-based advance in the ‘big’ dollar.

Note: The INR has depreciated -3% outright so far this year, despite BI spending billions of dollars to curb that slide. The currency fell as much as -4.5% for the year at its low last week.

Euro Recovers As German Retail Sales Sparkles

EUR/USD has recorded considerable gains in the Wednesday session. Currently, the pair is trading at 1.1616, up 0.66% on the day. On the release front, German retail sales jumped 2.3%, crushing the estimate of 0.5%. In France, Consumer Spending declined 1.5%, well off the estimate of 0.2%. Preliminary GDP dropped to 0.2%, shy of the estimate of 0.3%. Later in the day, Germany releases Preliminary CPI, which is expected to rise to 0.3%. In the US, the key event is Preliminary GDP, with an estimate of 2.3%. We’ll also get a look at employment numbers, with ADP nonfarm payrolls expected to drop to 191 thousand.

German retail sales were unexpectedly strong in April, with a sharp gain of 2.3%. This reading ended a nasty streak of four declines. The gain is the strongest since December, and raises hopes that second quarter growth will rebound after a sluggish first quarter. Inflation is also expected to improve, with German Preliminary CPI forecast to rise to 0.3% in May after a flat reading of 0.0% in April. The story in France, the second largest economy in the eurozone, was not as bright. Consumer spending plunged 1.5% in April, marking a 3-month low. Preliminary GDP fell to 0.2% in March, down from 0.6% a month earlier.

On Tuesday, the euro dropped to its lowest level since July 2017, in response to the political turmoil in Italy. The trouble began when President Sergio Mattarella vetoed a ministerial choice of the two parties which were expected to form a coalition, the League Nord and the Five Star Movement. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. However, there are reports that the League and Five Start Movement could get another kick at the can to form a government. Another possibility is that Italy will hold a snap election. It’s doubtful if another election would change the political landscape, so Matterella will likely huddle with political leaders and make a supreme effort to avoid another general election.

5-Star is finding a point of compromise for economy minister

Reuters reported that a source close to the anti-establishment 5-Star Movement that it's trying to find "a point of compromise on another name" as economy minister. The rejection by President Sergio Mattarella on anti-euro Paolo Savona as economy minister triggered this week's political turmoil. If 5-Star can find someone acceptable by pro-Euro Mattarella, with far-right League or not, there is a possibly of finally forming a government. And it should be recalled that Five Star leader Luigi Di Maio said they never sought to leave the Euro via facebook comments.

Prime Minister-designate Carlo Cottarelli is currently the technocrat that's supposed to lead the government until a new election. He also said that "new possibilities have emerged for the birth of a political government." And, "these circumstances, also considering the market tensions, have caused me to wait for further developments."

On the other hand, League leader Matteo Salvini poured cold water on the notion and urged another election. He said, "the earlier we vote the better because it's the best way to get out of this quagmire and confusion."

The development is another factor that's calming the Euro today.

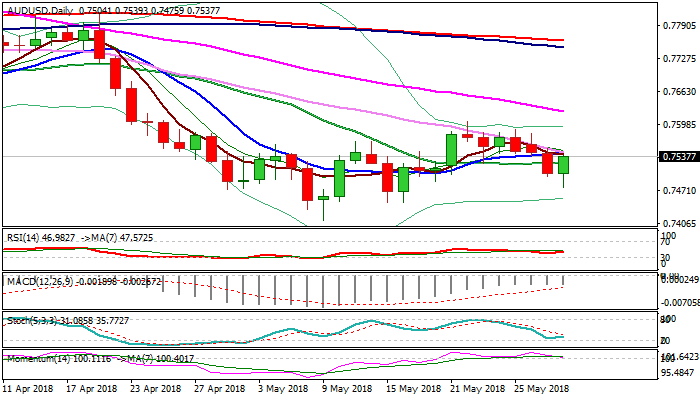

AUDUSD Outlook – Recovery Extends And Pressures Key 30SMA Barrier

The Aussie dollar strengthened in European session on Wednesday after hitting new two-week low at 0.7475 in Asia on downbeat Australian building approvals which fell 5% in Apr, undershooting forecast for 2.9% fall.

Fresh recovery was supported by weaker greenback and probes above initial pivots at 0.7525 (Fibo 38.2% of 0.7605/0.7475 / 4-hr cloud base), pressuring key barriers at 0.7540 zone (converged 10/30SMA’s).

Recovery attempts in past over one week were capped by falling 30SMA with repeated failure to signal an end of recovery phase and risk fresh weakness.

Falling momentum is probing into negative territory and maintains bearish setup along with daily MA’s in bearish configuration.

Conversely, close above 30SMA (the first since 18 Apr) would generate bullish signal for stronger recovery.

Res: 0.7540, 0.7565, 0.7590, 0.7605

Sup: 0.7506, 0.7475, 0.7447, 0.7412

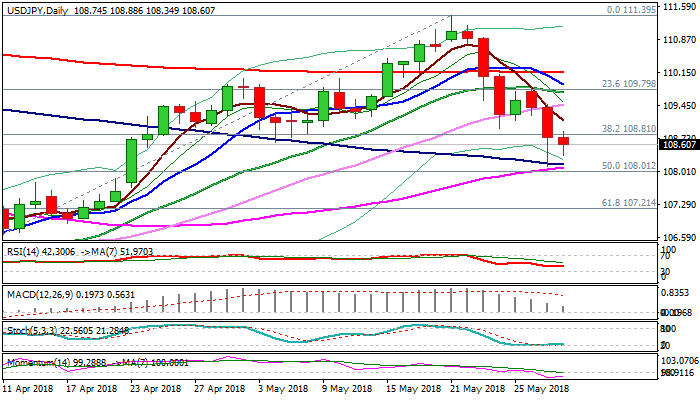

USDJPY Outlook: 30SMA Should Cap Extended Upticks To Keep Bearish Bias Intact

The pair holds above strong 108.15/00 support zone (converging 100/55SMA's/50% of 104.63/111.39 ascend) on Wednesday and consolidating losses of past two days. Tuesday's strong downside rejection (daily low at 108.11) signals bears require consolidation before fresh extension lower. Recovery attempts were so far unable to clearly break above initial barrier at 108.81 (broken Fibo 38.2%), keeping intact 30SMA (109.45) which is expected to cap extended upticks. Eventual break below 108 pivot would expose top of rising daily cloud (107.60) and another strong support at 107.21 (Fibo 61.8% of 104.63/111.39).

Res: 108.81, 109.11, 109.45, 109.71

Sup: 108.34, 108.15, 108.00, 107.60

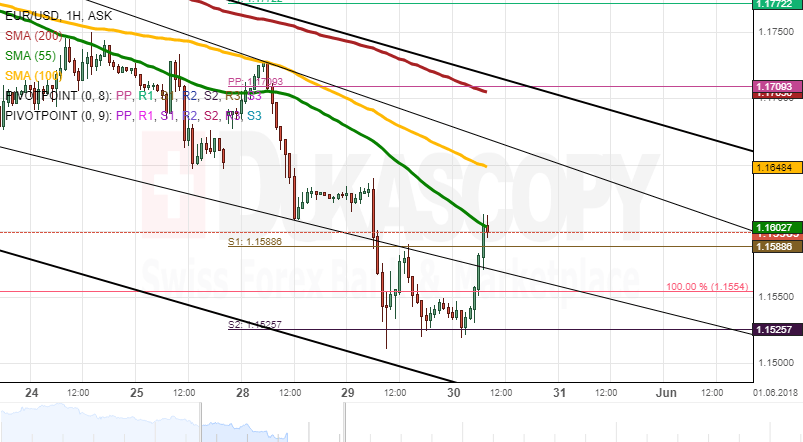

EUR/USD Analysis: Influenced Strongly By Fundamentals

Political uncertainty in Italy continues to weigh heavily on the common European currency. Despite starting the day with low volatility on Tuesday, bears grew in strength mid-session and consequently pushed the pair 88 pips lower. This fall was stopped by the weekly S2 at 1.15255. This level is likewise a new ten-month low for the rate.

Technical indicators are located in the oversold territory. This should point to a soon recovery. However, it seems that the given political uncertainty is dominating over any technical signals this week, suggesting that the pair might still edge lower down to the bottom channel line or the weekly S3 at 1.1450 and 1.1405, respectively.

In terms of resistance, the Euro faces the 55– and 100-hour SMAs circa 1.16. This level should not be surpassed in this session.

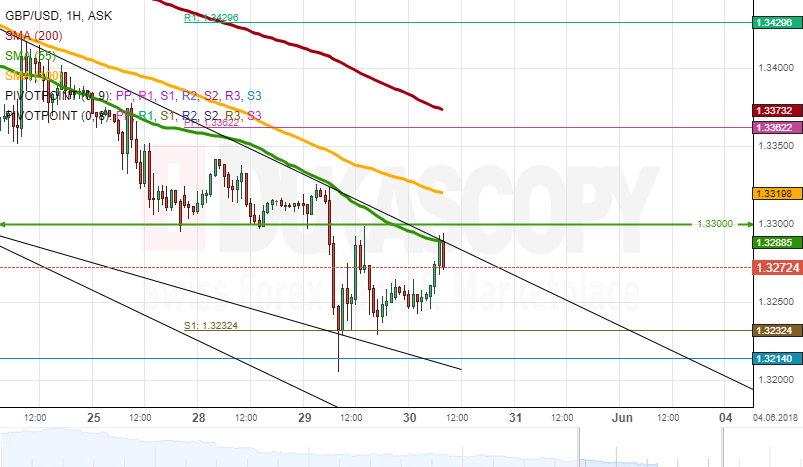

GBP/USD Anlaysis: Fails To Accelerate

The Pound was driven by downside risks against the US Dollar on Tuesday. The 55-hour SMA proved to be an unbreakable barrier for the rate, thus sending the Sterling past the psychological 1.33 level until support at the weekly S1 at 1.3232 was found.

The pair has failed to breach this moving average on several occasions during the past two weeks which shows that the Pound generally remains under the bearish influence. Some downside potential is still apparent in the market.

Even though technical indicators on the 1H chart are starting to recover, longer time-frames still lag behind. This suggests that gains could be limited today. The nearest resistance that is expected to hold firm is set by the 55– and 100-hour SMAs at 1.33. Meanwhile, support is provided by the weekly S2 at 1.3165.

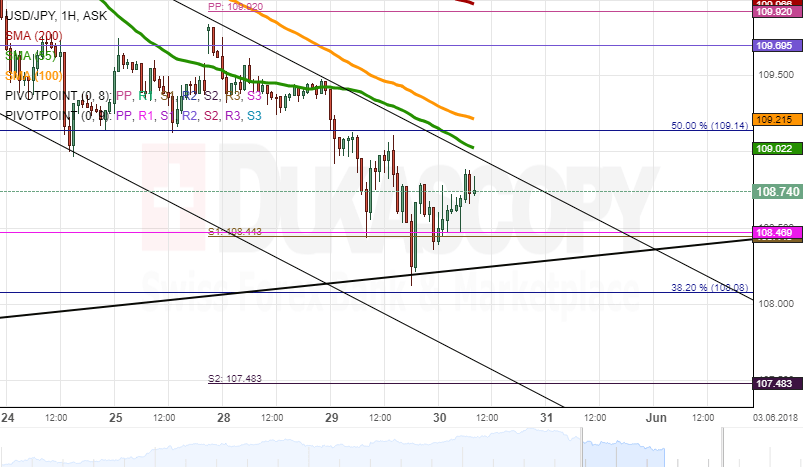

USD/JPY Analysis: Touches Senior Channel

Then Yen was strengthened by risk-averse investors on Tuesday. This resulted in the USD/JPY exchange rate falling 116 pips down to the 108.20 area. Further decline was stopped by the strong support of the 55– and 100-day SMAs and the 38.20% Fibonacci retracement.

It is expected that this southern barrier, likewise reinforced by the senior channel line, remains intact today, thus showing some upside potential for bulls. In line with this scenario, the Greenback should approach the 55– and 100-hour SMAs and the 50.0% Fibonacci line at 109.15.

In case bulls push the pair above this territory, the following notable resistance is the 200-hour moving average and the weekly PP at 109.95. This level should likewise serve as the daily high.

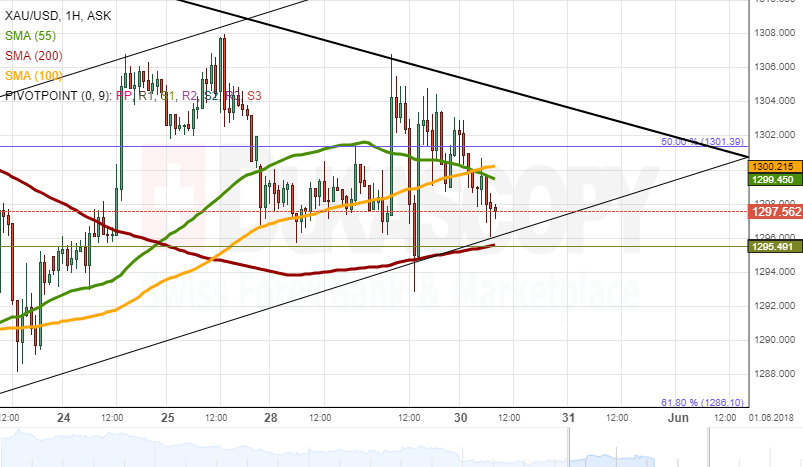

Gold Analysis: Lingers Near 1,300.00

The XAU/USD exchange rate has remained stable for the second consecutive day. Tuesday's trading session showed larger volatility if compared with the preceding day, but the price nevertheless remained near the 1,300.00 area.

Gold has once again approached the upper boundary of a seven-week channel and it seems that it might be ready to make a breakout north. However, technical indicators suggest that bears could take over the market today. This could likewise be confirmed by the fact that Gold breached the support of the 55– and 100-hour SMAs early today.

In case the 200-hour SMA at 1,295.00 is breached, a fall should continue until the senior channel and the 61.80% Fibo retracement at 1,285.00. Conversely, gains are likely to be capped at 1,315.00.

NZD/CAD 4H Chart: Breakout Likely

After hitting the monthly pivot point at the 0.87 mark mid-May, the New Zealand Dollar changed its sentiment against the Canadian Dollar and began a new wave up. As a result, the rate gained 2.78%.

However, these gains were limited by the 200– hour simple moving average which provided a strong resistance for the pair. Also, the NZD/CAD pair has reached the 50.00% Fibonacci retracement level. This retracement can be measured by connecting the low at 0.87 and the high at 0.92.

Everything being equal, a breakout could be expected through the upper boundary of a descending channel where the 200-hour SMA and the weekly PP is located.