Sample Category Title

US GDP And BoC Rate Could Spark Market Volatility

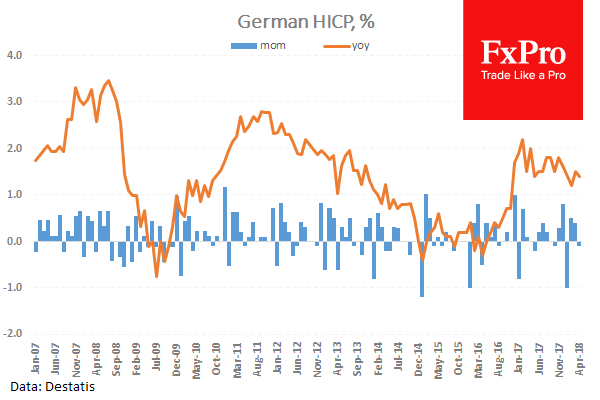

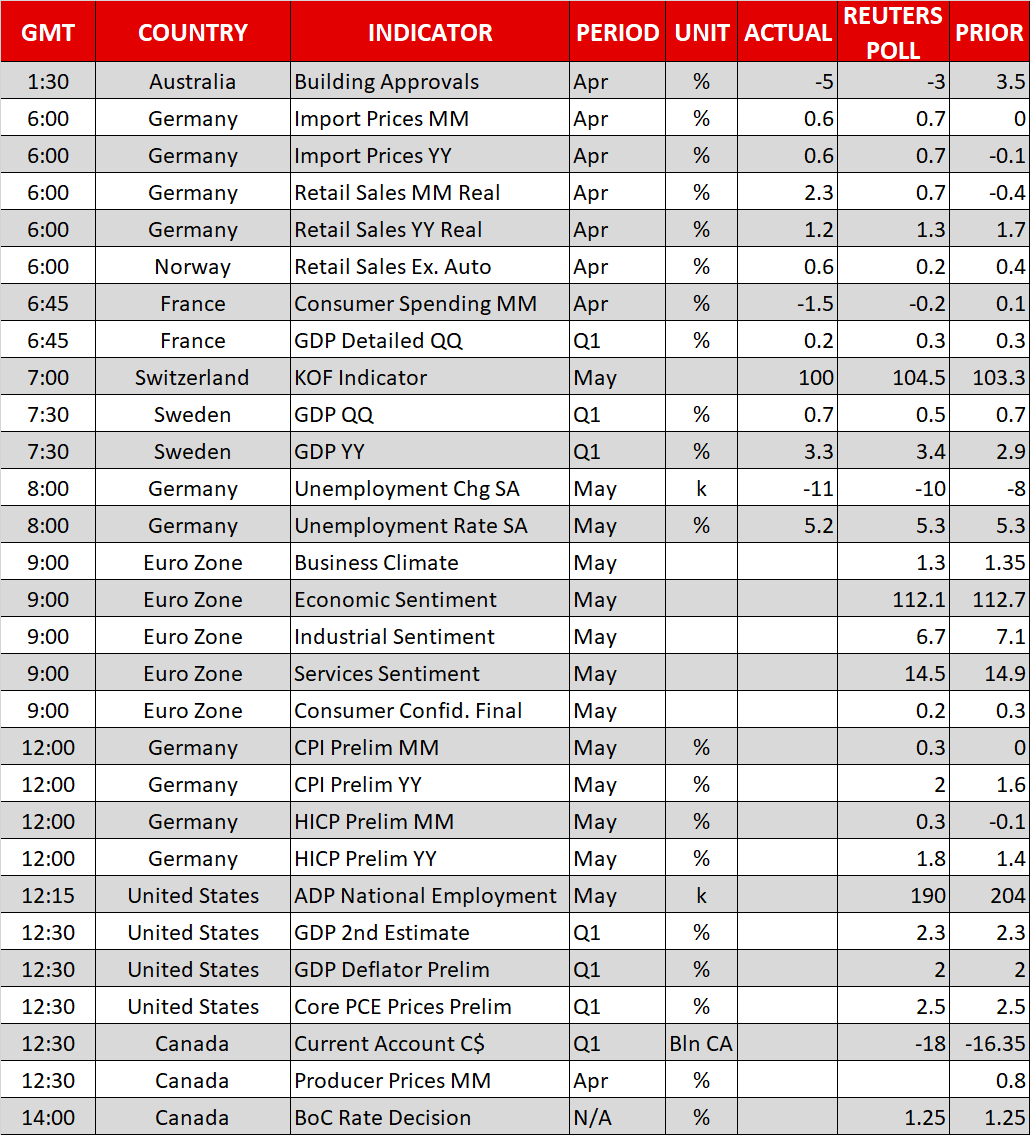

At 12:00 GMT, German Harmonised Index of Consumer Prices (YoY) (May) is expected to come in at 1.8% against a prior reading of 1.4%. Harmonised Index of Consumer Prices (MoM) (May) is expected to be 0.3% from a previous -0.1%. This data is expected to beat the previous reading on a yearly basis with a beat in the monthly reading expected to bring the data back above zero. EUR crosses can be moved by this data.

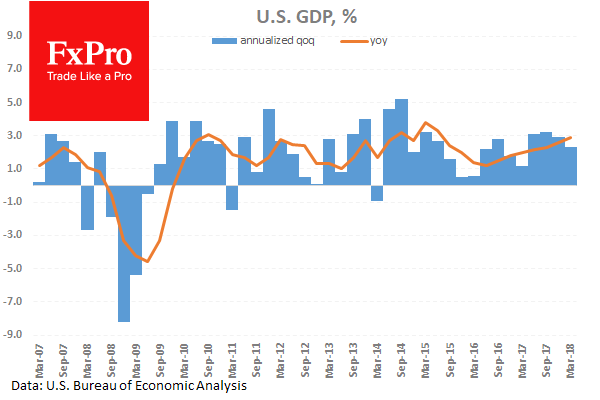

At 13:30 GMT US Gross Domestic Product Annualized (Q1) is expected to be 2.3% from 2.3% previously. This data is holding just above 2% although it has slipped in the last two quarters from 3.3%. Gross Domestic Product Price Index (Q1) is expected to be 2% from 2% previously. This dat has dropped back to 2% after rising above that level for the past two quarters. Personal Consumption Expenditures Prices (QoQ) (Q1) is expected to come in at 2.7% from 2.7% previously. Core Personal Consumption Expenditures Prices (QoQ) (Q1) is expected to be 2.5% from 2.5% previously. Personal consumption data has been rising steadily as Americans spend more on durable goods, consumer products and services. USD crosses may be heavily traded as a result of this data.

At 13:30 GMT US Gross Domestic Product Annualized (Q1) is expected to be 2.3% from 2.3% previously. This data is holding just above 2% although it has slipped in the last two quarters from 3.3%. Gross Domestic Product Price Index (Q1) is expected to be 2% from 2% previously. This dat has dropped back to 2% after rising above that level for the past two quarters. Personal Consumption Expenditures Prices (QoQ) (Q1) is expected to come in at 2.7% from 2.7% previously. Core Personal Consumption Expenditures Prices (QoQ) (Q1) is expected to be 2.5% from 2.5% previously. Personal consumption data has been rising steadily as Americans spend more on durable goods, consumer products and services. USD crosses may be heavily traded as a result of this data.

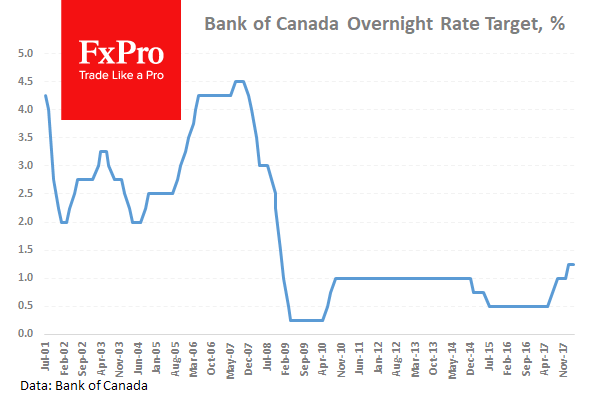

At 21:00 GMT, Bank of Canada Interest Rate Decision and Rate Statement will be released. The Rate Decision is expected to remain at 1.25% after the Bank hike rates in January. The Rate Statement will provide some key insights into the thinking behind today’s decision and future policy. CAD crosses can see spikes in volatility as a result.

Euro Catches Its Breath After Slide, Bank Of Canada Decides

Here are the latest developments in global markets:

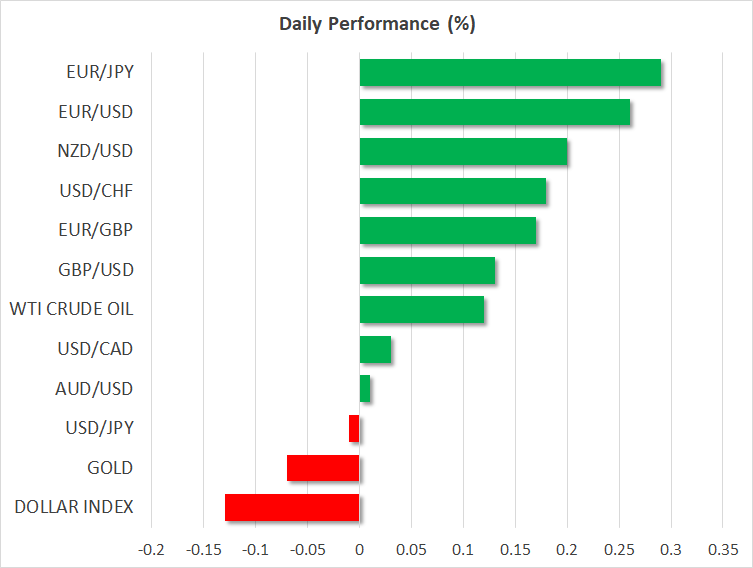

FOREX: The US dollar index is down by roughly 0.1% on Wednesday, giving back some of the gains it posted yesterday, when it touched its highest point since early November. Meanwhile, although the euro posted considerable losses yesterday, it has rebounded somewhat today, trading higher by 0.3% versus the yen and 0.25% against the dollar.

STOCKS: Wall Street was slammed yesterday, with all major US indices posting hefty declines as Italy's political predicament sent shockwaves across financial markets, while US-China trade tensions added another reason for investors not to take much risk. The Dow Jones plunged 1.58%, while the S&P 500 and the Nasdaq Composite declined by 1.16% and 0.50% respectively. That said, sentiment seems to have rebounded a little today, as futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open. Meanwhile, Asian markets were a sea of red. Japan's Nikkei 225 and Topix fell by 1.52% and 1.46% correspondingly, while in Hong Kong, the Hang Seng tumbled 1.55%. In Europe, futures following most of the major benchmarks were in positive territory, with the two exceptions being the UK's FTSE 100 and France's CAC 40.

COMMODITIES: Oil prices were marginally higher on Wednesday. WTI rose by a little more than 0.1%, while Brent climbed by roughly 0.05%, both benchmarks stabilizing a little after posting considerable losses in recent days. Prices have been weighed on by speculation that Saudi Arabia and Russia will “open the taps' soon and raise their output materially, in order to offset any supply losses from Iran and Venezuela. In precious metals, gold is down today but by less than 0.1%, currently trading not far above the $1,296/ounce mark. The yellow metal exhibited a “dead cat bounce' yesterday, briefly spiking higher to re-challenge its 200-day moving average at $1,307, only to find fresh sell orders and edge back down.

Major movers: Euro catches its breath after plunge; trade frictions back in focus

Italian politics remained in the spotlight on Tuesday, with the euro extending its losses and touching fresh multi-month lows against the dollar, the yen, as well as the Swiss franc. Markets continued to price in the possibility of this crisis deepening further, as the early elections that will probably take place this summer are increasingly being framed as an implicit referendum on the euro.

Nonetheless, the leader of the Five Star Movement Luigi Di Maio said yesterday he never sought a euro exit. His remarks helped to stop the bleeding in the currency, and it even managed to rebound slightly in the aftermath, as he probably calmed the nerves of investors worried over an “Italexit' from the euro. As for bond markets, the big story has been a rotation away of periphery EU countries. Money is flowing out of Greece, Spain, Portugal, and of course Italy, and finding its way into Germany, France, the UK, and the US – evident by the former group's government bond yields rising and the latter's declining.

Interestingly, markets are betting that politics will affect monetary policy as well. Investors have pushed back the expected timing of the first 10bps rate increase by the ECB to the fourth quarter of 2019; it was anticipated to come during the second quarter just a few months ago. Across the Atlantic, the implied probability of the Fed raising rates at the June meeting has fallen to 74%, from nearly 100% last month. While this repricing makes sense with respect to the ECB, it appears questionable with regards to the Fed. The US economy is humming along nicely and for policymakers to shy away from pressing the hike button in June, the global outlook may need to deteriorate by much more than what we have seen so far.

On the trade front, the White House warned it will move ahead with plans to impose up 25% tariffs on $50 billion worth of Chinese imports if Beijing does not swiftly address the issue of intellectual property theft. This appears to be one more way for the US administration to raise pressure on China amid ongoing negotiations, though markets largely overlooked it as the Italian narrative dominated headlines.

Day ahead: Bank of Canada decides; German inflation, US ADP report and revised GDP figures also due

Wednesday's calendar features numerous releases of relative importance, as well as a Bank of Canada decision on interest rates.

The eurozone will be on the receiving end of numerous surveys gauging business and consumer confidence during May at 0900 GMT. All surveys are projected to show a deterioration in sentiment relative to the month that preceded.

Germany, the eurozone's largest economy, will see the release of preliminary inflation data for May at 1200 GMT; price pressures are expected to accelerate during the month compared to April's respective figures. Earlier in the day (0800 GMT), May's unemployment rate will be made public out of the country. These figures come a day before the eurozone as a whole sees the release of its corresponding numbers on inflation and unemployment; a data beat may be interpreted as a precursor to tomorrow's releases and help the struggling euro.

However, of more importance for euro pairs are developments in Italian – and to a lesser extent Spanish – politics at the moment.

The US ADP report on positions added to the economy by the private sector is due at 1215 GMT. Analysts anticipate the addition of 190k positions in May, which compares to April's 204k. ADP data are sometimes viewed as a preamble to the more inclusive nonfarm payrolls report (due on Friday), though the two reports do not seem as closely “correlated' lately.

Updated GDP figures for the first quarter of the year will also be made public out of the US at 1230 GMT, with the annualized pace of growth anticipated to be confirmed at 2.3%. Preliminary data on Q1's GDP deflator and on core PCE prices will be released at the same time as well.

Canadian producer price figures for April, as well as current account data for Q1, are on the agenda at 1230 GMT. The lion's share of the attention for positioning on the loonie though will fall on the Bank of Canada's decision on interest rates and accompanying statement, which will be made public at 1400 GMT. No change in rates is expected though a hawkish tilt is most likely to result in an appreciating Canadian dollar and vice versa. It should also be kept in mind that NAFTA talks remain in the background.

The Federal Reserve will be issuing its Beige Book gauging current economic conditions at 1800 GMT.

Oil traders will be paying attention to API weekly data on US crude stocks which are due at 2030 GMT.

A G7 meeting featuring finance ministers and central bankers commences today and will run until June 2. The theme of the meeting is “Investing in Growth that Works for Everyone.' Meanwhile, US Commerce Secretary Wilbur Ross is scheduled to talk at an OECD forum, as well as meet EU trade chief Cecilia Malmstrom in an informal World Trade Organization ministerial in Paris. Later in the week, he will be visiting Beijing; trade developments remain in focus and can drive positioning in currency, equity, bond and commodity markets.

Also of note, is that there are signs that increasingly point towards the direction that a meeting between Trump and North Korea's Kim Jong Un will take place after all later in June.

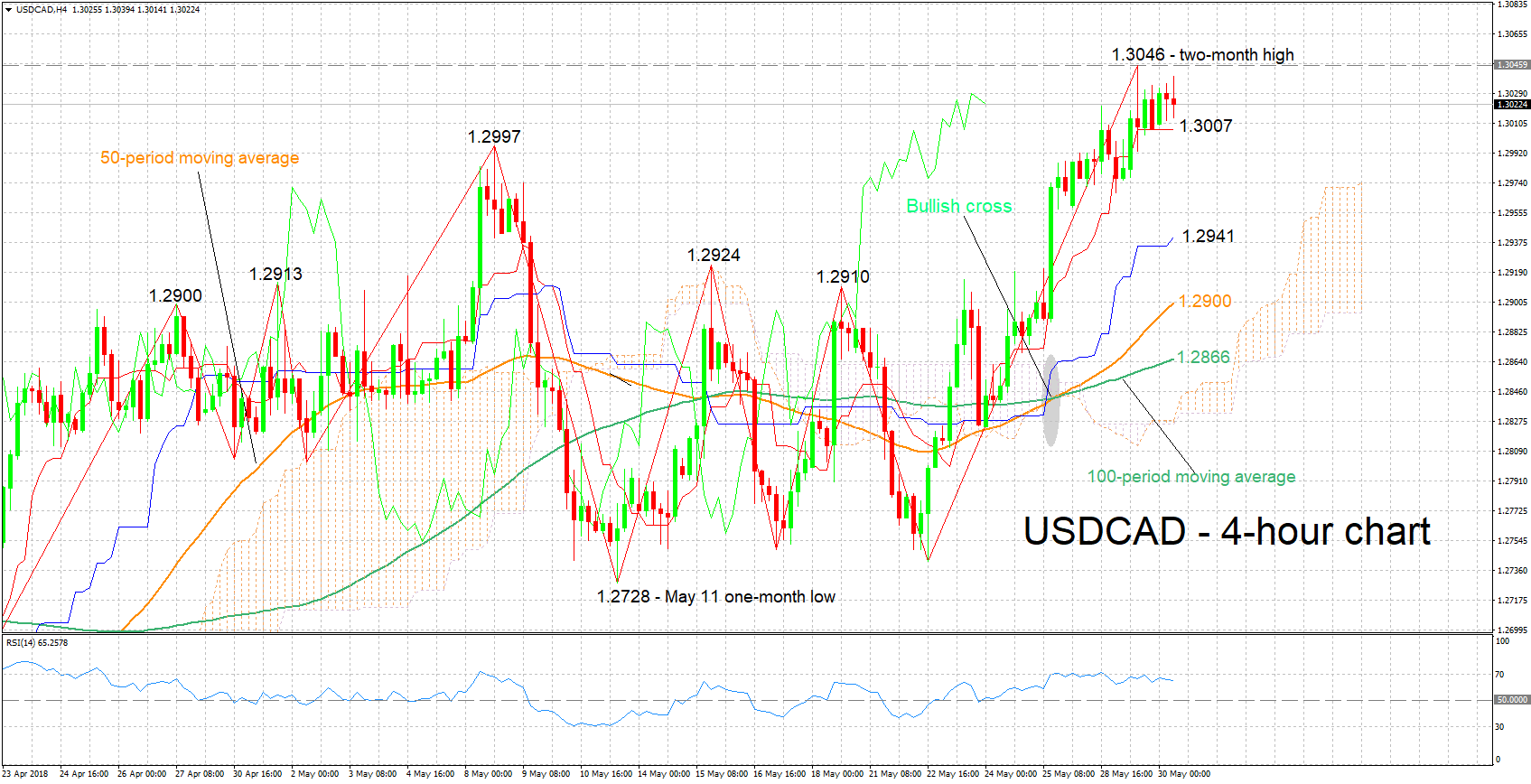

Technical Analysis: USDCAD close to two-month high; bullish bias eases

USDCAD touched a two-month high of 1.3046 on Tuesday, while it is currently trading roughly 25 pips below that level. The Tenkan-sen is above the Kijun-sen in support of a bullish bias. The RSI is in bullish territory, adding to the view for positive short-term momentum, though notice that its advance has stalled – this is an indication of easing positive momentum.

A hawkish message by the Bank of Canada is expected to boost the loonie, pushing USDCAD lower. Support might come around the current level of the Tenkan-sen at 1.3007; the area around this includes the 1.30 round figure, as well as a peak from the past at 1.2997. Further below, additional support could come around the Kijun-sen at 1.2941 (the region around this level encapsulates numerous tops from previous weeks).

Conversely, a dovish BoC is anticipated to push the pair higher. Immediate resistance could take place around yesterday's high of 1.3046, and subsequently around the 1.31 handle.

US releases can also spur positioning on the pair.

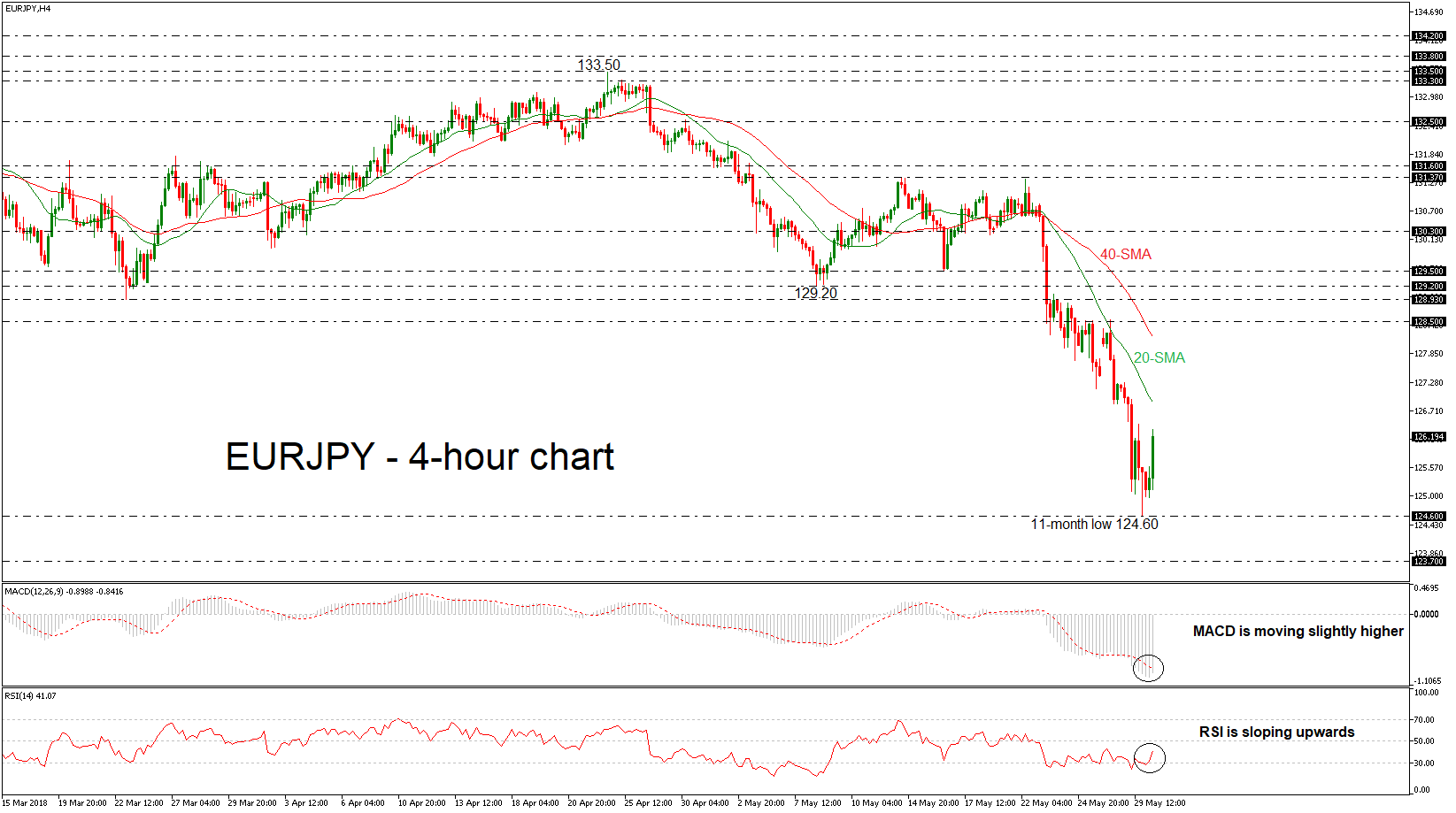

EURJPY Pares Strong Losses, Eases From 11-Month Trough

EURJPY steadied on Wednesday after an aggressive bearish rally in the previous six days. The common currency created an eleven-month low of 124.60 against the Japanese yen on Tuesday, while the price is paring some of the losses over the last couple of hours. The momentum indicators are supportive of the slightly bullish correction.

In the 4-hour chart, the RSI indicator is rising in negative territory and is approaching the threshold of 50. Moreover, the MACD oscillator is moving marginally higher after a strong negative momentum in the previous days.

In case of a further upward attempt, EURJPY would likely meet resistance at the 20-day simple moving average (SMA), currently around 126.85. A break above the 20-day SMA would ease the downside pressure and bring the pair within reach of the 40-day SMA at 128.30. Slightly above this area, prices could hit the 128.50 resistance barrier.

On the flip side, immediate support is being provided by the eleven-month low of 124.60. However, should prices dip lower again, the next support would likely come from the 123.70 barrier, identified by the June 2017 low.

In the medium term, the bearish outlook remains intact since February 2, with the moving averages all pointing downwards.

China warns to take resolute and forceful measures if Trump insists on being arbitrary and reckless

Chinese Foreign Ministry spokeswoman Hua Chunying responded to he strong US statement released yesterday. She said "We urge the United States to keep its promise, and meet China halfway in the spirit of the joint statement."

In addition, Hua warned to take "resolute and forceful" measures to protect its interests if Trump insists on being "arbitrary and reckless" She added that "when it comes to international relations, every time a country does an about face and contradicts itself, it's another blow to, and a squandering of, its reputation,"

OECD projects G20 2018 growth to be 4.0%

In the latest economic outlook report released today, OECD projects 2018-19 global growth to be at around 3.8% while G20 growth would be 4.0%. It noted in the release that "the global economy is experiencing stronger growth, driven by a rebound in trade, higher investment and buoyant job creation, and supported by very accommodative monetary policy and fiscal easing."

However, OECD also warned of "significant risks posed by trade tensions, financial market vulnerabilities and rising oil prices loom large". And it urged that "more needs to be done to secure a strong and resilient medium-term improvement in living standards."

OECD Secretary-General Angel Gurria said that "the economic expansion is set to continue for the coming two years, and the short-term growth outlook is more favourable than it has been for many years." However, "the current recovery is still being supported by very accommodative monetary policy, and increasingly by fiscal easing". Hence, "strong, self-sustaining growth has not yet been attained."

Below is a summary of OECD projections.

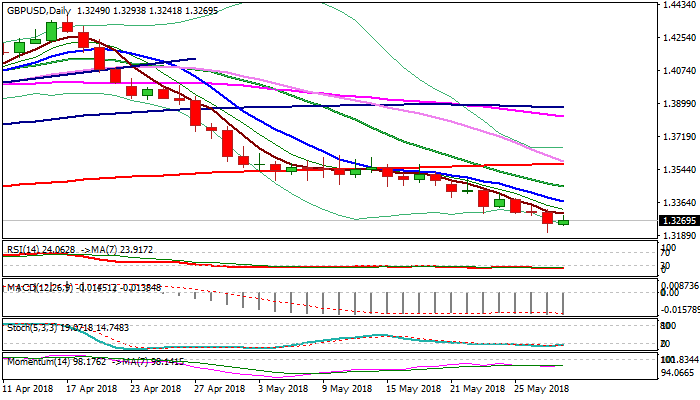

GBPUSD Outlook – Bears Favor Limited Correction Before Resuming

Cable tracks the Euro in early European trading and extends bounce from new multi-month low at 1.3205.

Fresh extension higher pressures 1.33 resistance zone (Tuesday’s intraday high / falling 5SMA) break of which would sideline immediate downside risk and signal further correction.

Falling 10SMA marks key near-term barrier (1.3371) and close above it would provide relief.

Mixed daily techs with sideways moving momentum, bearish MA and north-turning oversold RSI / slow stochastic, support the notion.

However, overall structure remains bearish and current bounce could be seen as positioning for fresh downside.

Early upside rejection under 5SMA would turn immediate focus lower for retest of strong support at 1.3205 (weekly cloud top), violation of which would signal continuation of the downtrend from 1.4376 (17 Apr peak).

Res: 1.3300, 1.3325, 1.3371, 1.3421

Sup: 1.3241, 1.3205, 1.3153, 1.3100

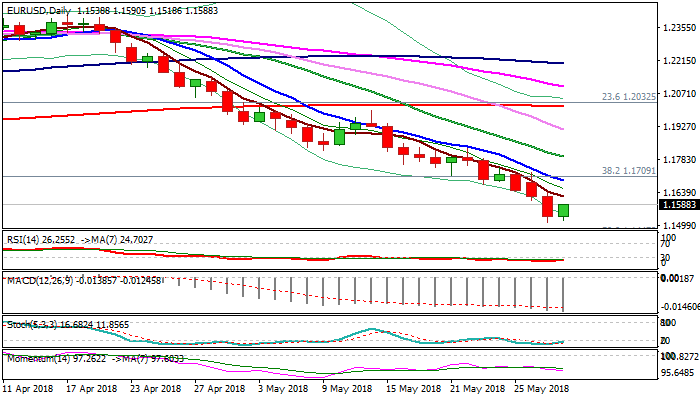

EURUSD Outlook – Bears Are Taking A Breather Before Fresh Attempts Lower

The Euro moved higher from new 10-month low at 1.1509 on Wednesday after rumors that Italy may not force snap election provided temporary relief.

Additional boost to the single currency in early Wednesday's trading came from better than expected German retail sales which rose 2.3% in April, heavily beating forecast for 0.5% rise, in the strongest monthly increase since October 2016.

However, current bounce is seen as positioning for fresh weakness, following failure on initial attack at 1.15 support.

Strong bearish momentum and daily MA's in firm bearish setup, support the notion.

Falling 5SMA (1.1624) is expected to ideally cap recovery, with extended upticks to face strong barriers at 1.1681/95 (broken weekly cloud top / Fibo 38.2% of 1.1996/1.1509, reinforced by falling 10SMA).

Eventual break below 1.15 handle would open Fibo support at 1.1447 (50% retracement of 1.0340/1.2555 rally).

Only break and close above 10SMA would sideline bears for stronger correction.

Today's EU calendar is full with focus turning towards German labor data and Inflation report for May, which could provide further support to the single currency on upbeat releases.

Res: 1.1624, 1.1681, 1.1695, 1.1709

Sup: 1.1500, 1.1447, 1.1402, 1.1370

GBP/USD Time For A Correction?

The GBP has reached the 1.3200 zone as expected and predicted via my latest GBP/USD analysis and FXStreet poll. We can see that bullish divergence has formed and 1.3240-70 is the zone where price might reject to the upside. If 1.3230 holds next targets could be 1.3320, 1.3350 followed by 1.3410. Only the loss of 1.3200 and the break of 1.3185 will possibly initiate a further bearish pressure.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very StrongDaily Resistance)

DL3 – Daily Camarilla Pivot (Daily Support)

DL4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

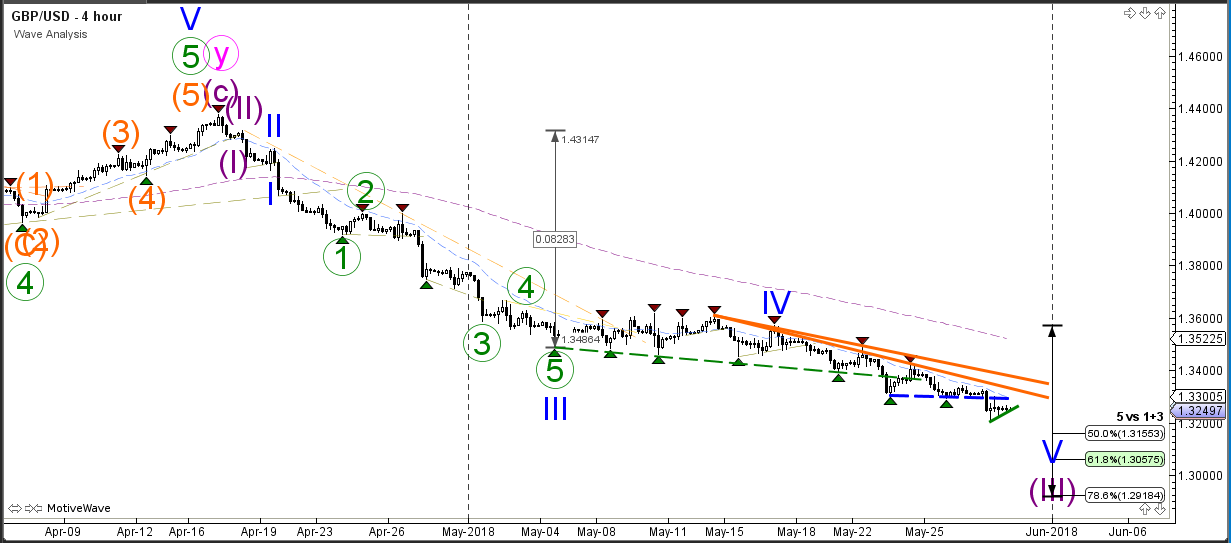

GBP/USD Retraces After Sturdy Bearish Breakout Below 1.3250

The GBP/USD bearish momentum broke below a key round level at 1.3250 and the support trend line of the descending wedge chart pattern (dotted blue). It seems more likely that price is now building a wave 3 impulse (purple) as long as price stays below the resistance trend lines (orange). A bearish continuation could see price move towards the Fibonacci targets of wave 5 (blue).

The GBP/USD ending diagonal pattern is only valid if the GBP/USD retraces back to the 61.8% Fibonacci retracement level of wave 4 (green). A bearish bounce at a shallower Fibonacci levels would indicate that there is no ending diagonal but rather a bearish impulse. In both cases price could continue with the downtrend towards the Fibonacci targets.

EUR/USD Downtrend Drops 150 Pips And Reaches 1.15

The EUR/USD broke below the support trend line of the falling wedge chart pattern. The EUR/USD has now reached a key support zone at the 1.15 psychological round level and is also close to a 50% Fibonacci level of the weekly chart.

The bearish breakout saw the EUR/USD fall from 1.17 earlier this week to 1.15. Whether the round level of 1.15 is strong enough to stop price remains to be seen. A new bearish breakout could aim at 1.1450-1.1475 whereas a bullish bounce and break above the resistance trend lines could finally start a bigger bullish correction.

The EUR/USD broke below the bear flag chart pattern mentioned yesterday and made a strong bearish breakout. It is possible that the EUR/USD is expanding the wave 5 (green) with an expanded 5 waves (orange) but price needs to break below the support trend line (green) and must remain below the bottom of wave 1 (orange) at 1.1607 otherwise a different wave pattern is valid. A break above resistance (red) could finally see a bullish retracement.