Sample Category Title

Elliott Wave Analysis: Nikkei Pullback Remains In Progress

Nikkei short-term Elliott wave view suggests that the rally to 23060 on May 20 high ended Intermediate wave (1) as an impulse. Down from there, the index is pulling back in Intermediate wave (2) pullback to correct cycle from March 23, 2018 low in 3, 7 or 11 swings before the rally resumes. The decline from 23060 high is unfolding as Elliott wave double three structure.

Double three is a 7 swing pattern, which is a combination of two corrective patterns, including Flats, Triangles, Triple three, Zigzag etc. The two corrective patterns combine together to form the double three structure. In the case of Nikkei, the decline from 23060 high to 22075 low ended Minute wave ((w)). The internals of Minute wave ((w)) unfolded as a Zigzag structure where Minutte wave (a) ended at 22475, Minutte wave (b) ended at 22640, and Minutte wave (c) of ((w)) ended at 22075.

From 22075 low, the bounce to 22560 high ended Minute wave ((x)) recovery as zigzag structure. The Index has since made a new low below 22075 and shows 5 swings bearish sequence from May 20 high (23060). Please note that 5 swing sequence is not the same as 5 waves impulse. 5 swing sequence refers to the swing count and refers to 7 swing WXY (double three structure). The 5 swing sequence favors more downside & confirms Minute wave ((y)) lower has started. The internals of Minute wave ((y)) is also unfolding as a Zigzag structure where Minutte wave (a) ended at 21920. Near-term, while bounces fail below 22560 high, expect the Index to see another extension lower towards 21350 – 21579, which is 100%-123.6% Fibonacci extension area of Minute ((w))-((x)). Afterwards, expect the Index to at least see a 3 waves bounce. We don’t like buying the Index.

Nikkei 1 Hour Elliott Wave Chart

Equities Decline As Sentiment Declines On Trade Fears And EU Political Turmoil

General Trend:

- Asian equity markets track declines in US and Italian equities, politics and trade concerns weigh

- Financials track declines in Italy’s banking sector

- US suggests trade war with China is ongoing; US Soybean Futures extend losses

- Shanghai Property index drops over 1%; Local press warned about property bubbles

- Chinese shares listed in HK hit 4-month low; MSCI expected to add China large-cap A-shares to EM index at the end of this week

- Japan retail sales rebound in April: Government previously said that Q1 weakness was temporary

- Yen trades generally lower amid ‘risk-off’; EUR/JPY tests ¥125

- 10-year bond yields in Australia, New Zealand and South Korea track Tuesday’s drop in US Treasury yields; US 30-year Treasury Futures decline in Asia after over 1.5% gain on prior session

- Indonesia Central Bank expected to raise rates at today’s ‘additional’ meeting

- Australia Q1 CAPEX data due for release on Thursday

- Upcoming US data in focus: May ADP report, second reading of Q1 GDP

Headlines/Economic Data

Japan

- Nikkei 225 opened -1.4%; closed -1.5%

- TOPIX Iron & Steel index -2.4%, Securities -1.9%, Electric Appliances -1.7%, Marine Transportation -1.4%

- Megabanks track declines in Italian financial sector

- Automakers trade generally lower, Toyota declines over 1.5%

- (JP) Japan Apr Department Store, Supermarket Sales y/y: -0.8% v 0.2%e

- (JP) JAPAN APR PRELIM RETAIL SALES M/M: 1.4% V 0.5%E; Retail Trade y/y: 1.6% v 1.0%e

- (JP) BoJ Gov Kuroda: Urgent to explore why prices and wages still feel sluggish - BoJ-IMES Conference

- Leopalace21, [-10%], 8848.JP Discloses construction defects: 38 of 290 buildings may be in violation of law

- (JP) Nikkei looks at Japan's fight against deflation, noting the 4 key indicators tracked by the government have stayed positive for at least three straight quarters through March

Korea

- Kospi opened -0.4%

- (KR) According to US intelligence report North Korea leader Kim is not going to give up nuclear weapons soon, but is open to allowing US businesses - press

- Posco, 005490.KR To build a lithium-ion cathode plant in southwestern region to meet the growing market demand on rechargeable battery

- (KR) South Korea Apr Department Store Sales y/y: -0.2% v 5.4% prior; Discount Store Sales y/y: -4.5% v 1.0% prior

- (KR) North Korea said to have tested torpedo during talks with South Korea and the US (timing uncertain) – South Korean Press

- (KR) South Korea Q1 Short Term External Debt: $120.5B v $115.9B prior

China/Hong Kong

- Hang Seng opened -1.2%, Shanghai Composite -1.3%

- Hang Seng Materials index -1.7%, Property/Construction -1.6%, Financials -1.5%, Industrial Goods -1.5%

- (CN) White House to proceed with plans to impose 25% tariffs on $50B worth of imported goods from China - press - Final list of Chinese imports to 25% tariff will be announced on Jun 15th (US session)

- (CN) China Researcher reiterates yuan currency (CNY) to fluctuate in two ways - China Securities Journal (CSJ)

- (CN) China must curb property speculation in some cities - China Daily

- (CN) China said to be carrying out nationwide spot checks on shadow banking companies – China Securities Journal (CSJ)

- (CN) China PBoC sets yuan reference rate at 6.4207 v 6.4021 prior (weakest setting since Jan 18th)

- (CN) China PBoC Open Market Operation (OMO): Injects CNY270B in 7-day, 14-day and 28-day reverse repos v CNY180B in 7-day and 28-day prior; Net: injects CNY70B v CNY50B prior

- (CN) Global Times Op Ed: US announcement of plans to go ahead with China tariffs, sends a clear message that the China/US trade dispute will be a long term issue

Australia/New Zealand

- ASX 200 opened -0.4%, closed -0.5%

- ASX 200 Financials index -1.4%, Telecom -0.9%, Resources -0.5%, REIT -0.5%; Utilities +1.6%

- (NZ) Reserve Bank of New Zealand (RBNZ) Semiannual Financial Stability Report: New Zealand’s financial system have not changed materially in the past six months; financial system is resilient

- (NZ) RBNZ Gov Orr: No decision on loan-to-value ratios (LVRs) likely until at least next financial stability report

- (NZ) RBNZ Dep Gov Bascand: General picture is very moderate house price outlook; outlook for house price inflation of avg of 2-3% in next few years

- (NZ) New Zealand Apr Building Permits m/m: -3.7% v 13.0% prior

- (AU) AUSTRALIA APR BUILDING APPROVALS M/M: -5.0% V -3.0%E; Y/Y: 1.9% V 4.1%E

North America

- US equity markets ended lower: Dow -1.6%, S&P500 -1.2%, Nasdaq -0.5%, Russell 2000 -0.2%

- S&P500 Financials -3.3%

- (US) US Treasury Official: G-7 Finance Ministers to meet in Canada on May 31-June 2nd, Italy and the volatility in emerging markets to be on the agenda

- GLD SPDR Gold Trust ETF daily holdings +0.4% at 851.45 metric tonnes

- (US) President Trump: Mexico will pay for the wall, they do nothing to help us, HHS Sec coming out with healthcare plan in 2 weeks - rally

Europe

- (IT) Italy PM-designate Cottarelli said to mull giving up mandate and allow for possible election on July 29th

- (IT) Italy's Five Star leader Di Maio: impeachment of the president is no longer on the table - Italian press

- (UK) May BRC Shop Price Index y/y: -1.1% v -1.0% prior (largest decline since Jan 2017)

Levels as of 02:00ET

- Hang Seng -1.6%; Shanghai Composite -1.5%; Kospi -2.1%

- Equity Futures: S&P500 -0.1%; Nasdaq100 -0.2%, Dax -0.2%; FTSE100 -0.3%

- EUR 1.1549-1.1519; JPY 108.78-108.35; AUD 0.7509-0.7476;NZD 0.6915-0.6883

- Jun Gold +0.1% at $1,299/oz; Jul Crude Oil -0.3% at $66.53/brl; Jul Copper -0.4% at $3.04/lb

German Inflation Is Due For Release, In Advance Of The Euro Area Figure Tomorrow

Market movers today

The key focus in the financial markets will be on the next steps in the Italian political drama after yesterday's sell-off, which is increasingly impacting global financial markets. The former IMF employee Carlo Cottarelli is due to go the president's office, most likely to acknowledge that he cannot form a government. This opens the possibility for new elections or renegotiations for a Five Star/League coalition government.

be on possible Chinese reaction to the US announcement that the US will impose limits on Chinese tech investment and go ahead with 25% tariffs on Chinese imports.

In terms of economic releases, the US PCE core in April is due out. Based on CPI, PCE core rose +0.1% m/m in April, which would lower the inflation rate to 1.8% y/y from 1.9%. We still believe there are upside risks to US inflation, as the total policy mix has become easier.

German inflation is due for release, in advance of the euro area figure tomorrow.

Selected market news

Italy remains the focal point in financial markets with large intraday movements in European fixed income markets observed yesterday and also in major EUR crosses, e.g. EUR/USD and EUR/CHF. The German government also spoke on the matter, with the German Finance Minister Scholz quoted as saying 'I know that the Italian people are very pro-European', in a Bloomberg Television interview in Berlin on Tuesday. 'So I think we could be optimistic, though there is a political debate about building a new government. But this is something that will not change the more pro-European approach of the Italians.'

The US market has also undergone a vast repricing over the past couple of days with the 10Y US yield falling close to 2.80% yesterday - about 30bp from the peak. In addition, US equity markets tracked the decline in European equity markets yesterday, falling around 1-1.5%.

Saudi Arabia, Kuwait and the UAE are said to be planning to meet on Saturday to discuss a new strategy for the oil market ahead of the 22 June regular OPEC meeting. The news follows comments from Saudi Arabia and Russia last Friday that they will propose OPEC begin raising crude output from H2.

In the US, a timeline for imposing USD50bn in import tariffs on China was laid out yesterday. A final list of covered imports is planned to be released by 15 June and imposed afterwards. Proposed restrictions on investments and export controls will announced on 30 June and implemented afterward.

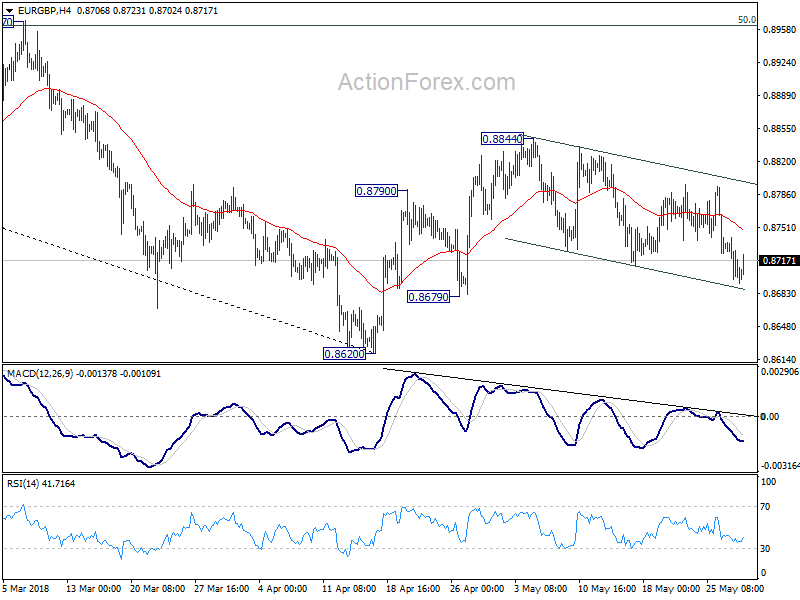

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8688; (P) 0.8715; (R1) 0.8732; More...

The choppy decline from 0.8844 is in progress and focus is on 0.8679 support. Break there will indicate completion of the rebound form 0.8620. And intraday bias will be turned back to the downside for this support. Whole decline from 0.9305 will likely be resuming too. On the upside, break of 0.8844 will resume the rebound from 0.8620. That will also revive the case of larger bullish reversal. EUR/GBP should target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963).

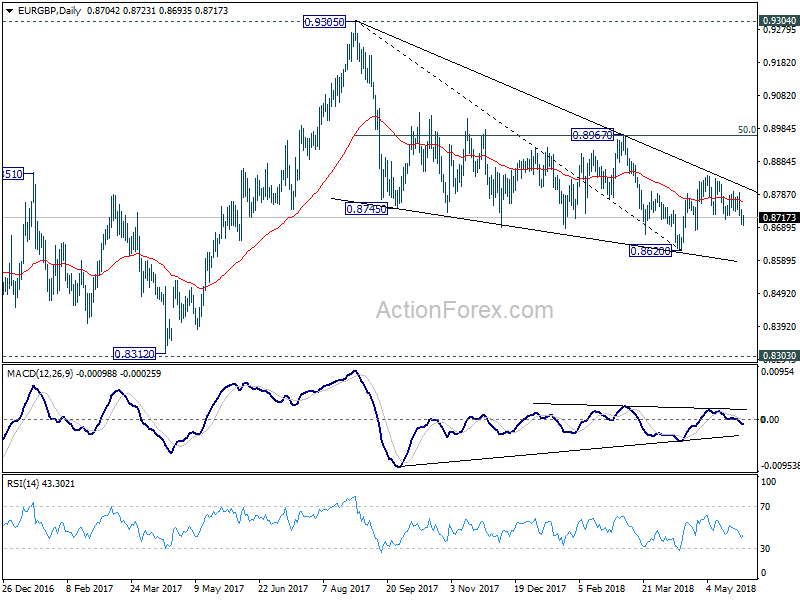

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

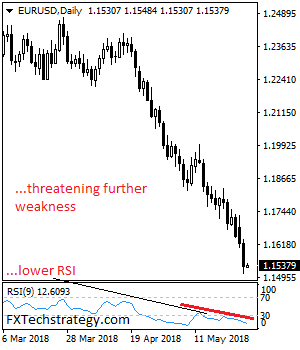

EURUSD – Bearish, Looks To Weaken Further

EURUSD - The pair remains weak and vulnerable to the downside as it extended its weakness on Tuesday. On the upside, resistance comes in at 1.1600 level with a cut through here opening the door for more upside towards the 1.1650 level. Further up, resistance lies at the 1.1700 level where a break will expose the 1.1750 level. Conversely, support lies at the 1.1550 level where a violation will aim at the 1.1500 level. A break of here will aim at the 1.1450 level. Below here will open the door for more weakness towards the 1.1400. All in all, EURUSD faces further downside pressure.

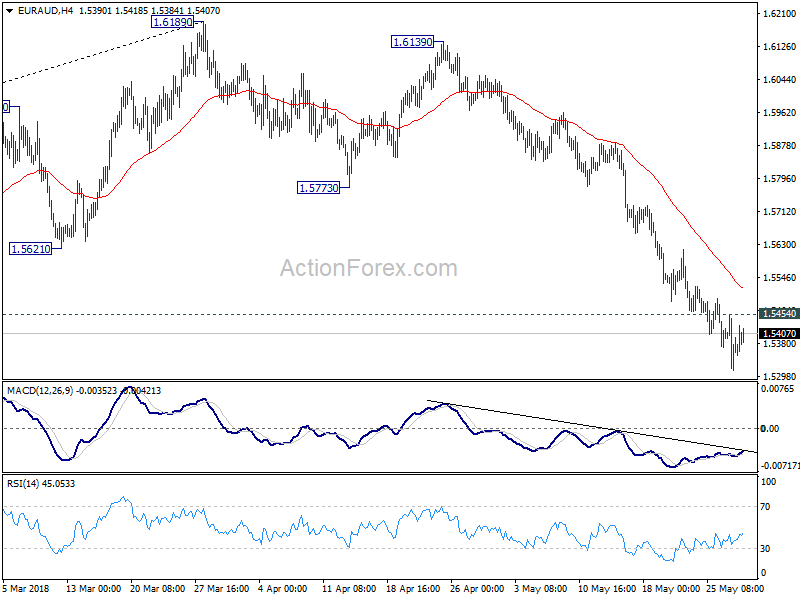

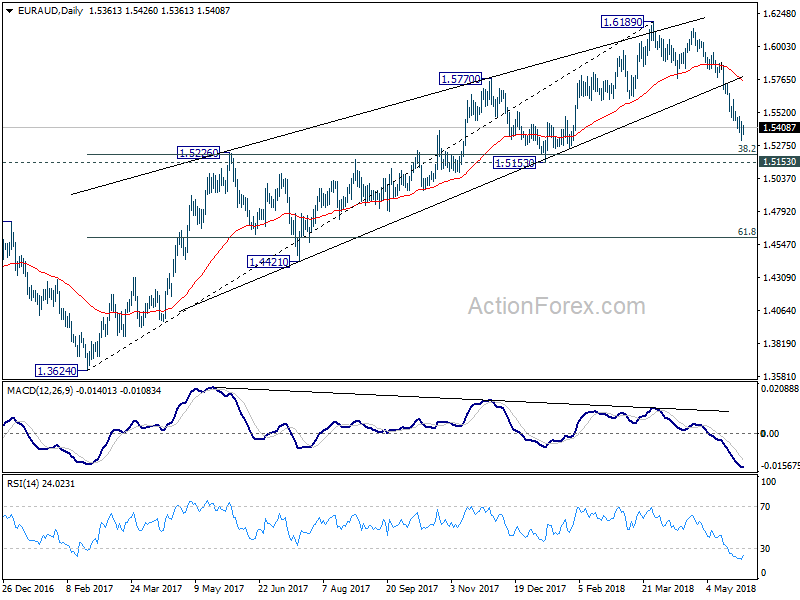

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5306; (P) 1.5382; (R1) 1.5448; More....

With 1.5454 minor resistance intact, intraday bias in EUR/AUD stays on the downside. Current fall from 1.6189 should target 1.5153 key support level next. On the upside, above 1.5454 minor resistance will turn intraday bias neutral and bring consolidation, before staging another decline.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

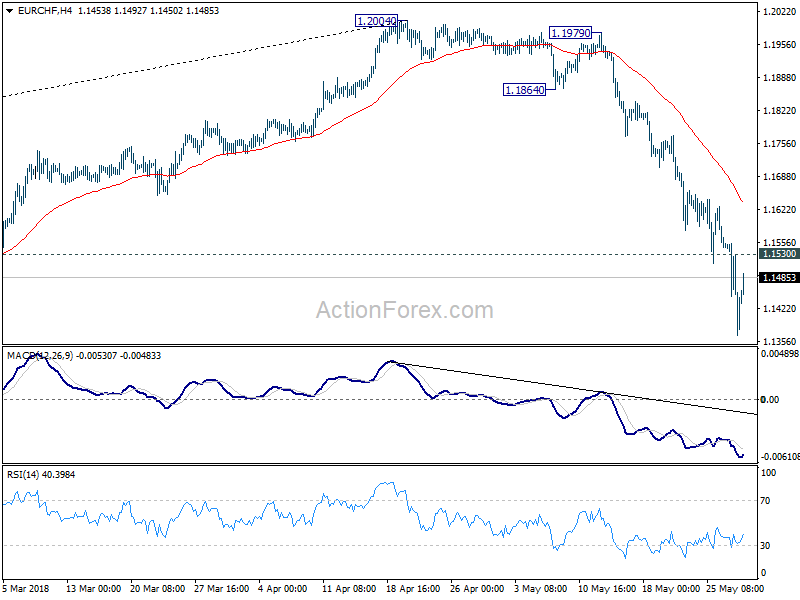

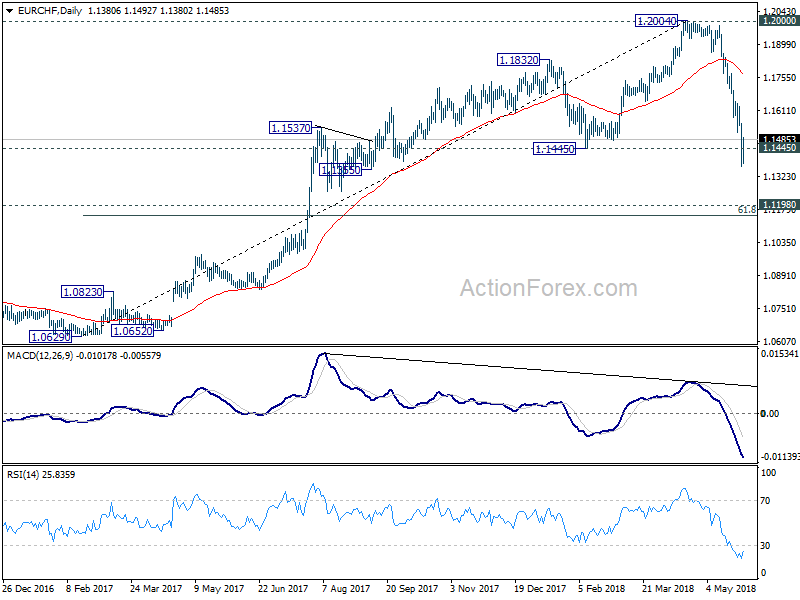

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1352; (P) 1.1454; (R1) 1.1540; More....

EUR/CHF breached 1.1445 support to as low as 1.1366 and recovered. There is no clear sign of bottoming yet and intraday bias stays on the downside. Sustained trading below 1.1445 will target next key support zone between 1.11543 and 1.1198. On the upside, above 1.1530 will turn intraday bias back to the upside and bring recovery first.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. The cross has met 1.1445 already, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern. However, sustained break of 1.1445 will target next key cluster level at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154.

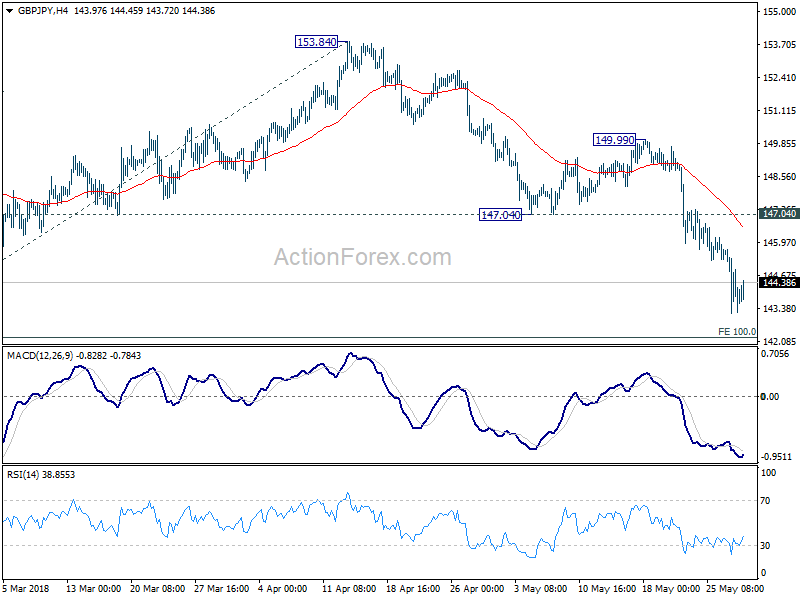

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.99; (P) 144.36; (R1) 145.54; More...

GBP/JPY turned sideway after reaching as low as 143.18. But there is no sign of bottoming yet. Intraday bias stays on the downside. Current falls should target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next. Break there will target key cluster level at 139.29. On the upside, break of 147.04 support turned resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

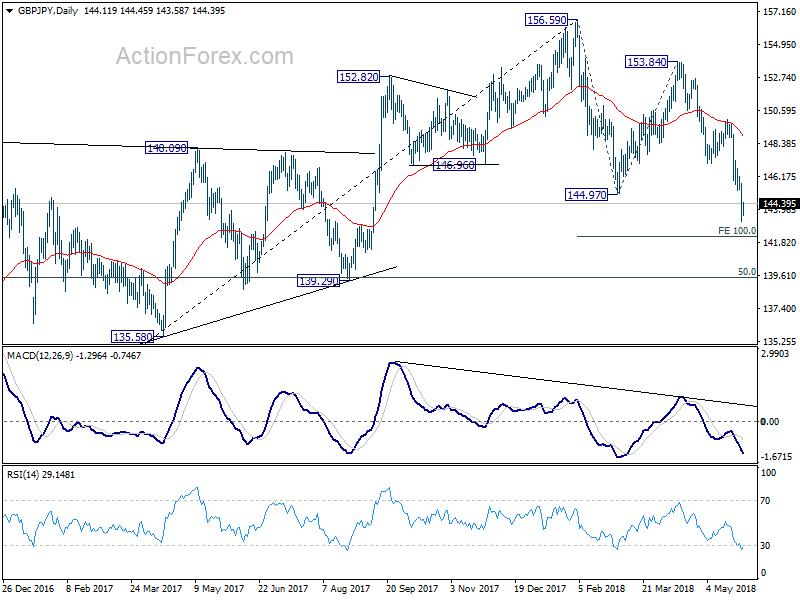

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

Euro Trading On A Weaker Footing, Ahead Of Key Economic Releases Across The Euro-Zone

For the 24 hours to 23:00 GMT, the EUR declined 0.75% against the USD and closed at 1.1541, as deepening political instability in Italy continued to dent investor sentiment.

In economic news, French consumer confidence index surprisingly remained steady at a level of 100.0 in May, defying market consensus for a rise to a level of 101.0.

Meanwhile, Italy’s consumer confidence index declined more-than-expected to a level of 113.7 in May, hitting its lowest level in 9 months and compared to market expectations for a fall to a level of 116.5. The index had registered a revised reading of 116.9 in the previous month.

Macroeconomic data released in the US showed that the CB consumer confidence index climbed to a 3-month high level of 128.0 in May, meeting market expectations and suggesting that robust labour market and improving business conditions continue to lighten Americans’ economic outlook. The index had registered a revised level of 125.6 in the prior month.

In other economic news, the nation’s Dallas Fed manufacturing business index advanced to a level of 26.8 in May, beating market expectations for a rise to a level of 23.0. The index had registered a level of 21.8 in the previous month.

Separately, the St. Louis Federal Reserve (Fed) President, James Bullard, stated that the central bank should be cautious in raising interest rates further unless economic data surprises to the upside, as inflation expectations remain somewhat low.

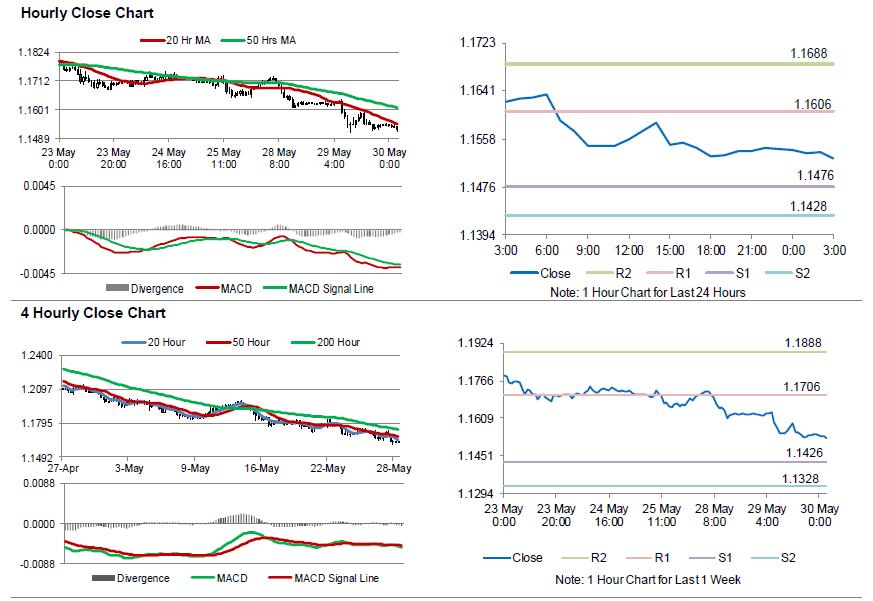

In the Asian session, at GMT0300, the pair is trading at 1.1524, with the EUR trading 0.15% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1476, and a fall through could take it to the next support level of 1.1428. The pair is expected to find its first resistance at 1.1606, and a rise through could take it to the next resistance level of 1.1688.

Trading trend in the Euro today is expected to be determined by the release of Germany’s flash inflation figures and unemployment rate data, both for May, slated to release in a few hours. Later in the day, investors would look forward to the release of US 1Q GDP numbers, ADP employment change for May, advance goods trade balance for April as well as the Fed’s Beige Book report.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

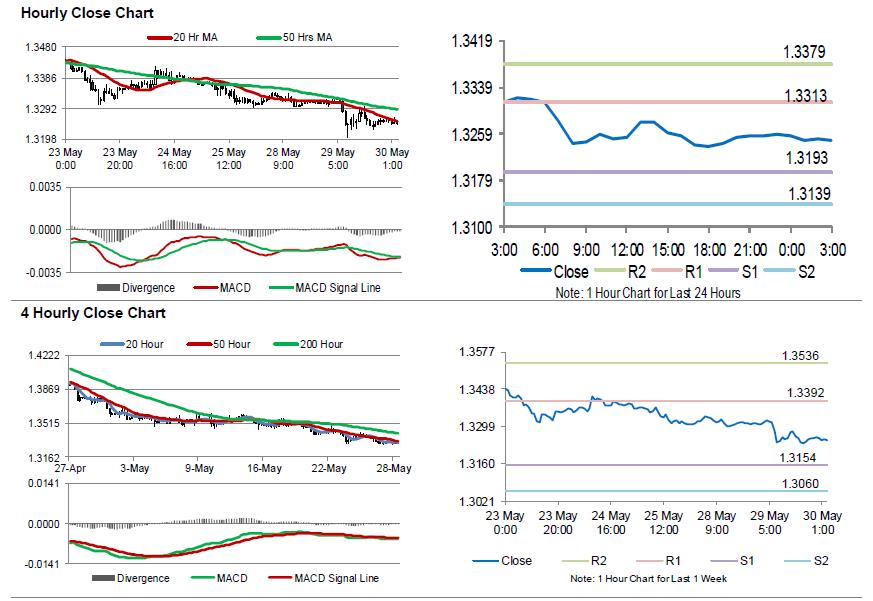

Pound Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.39% against the USD and closed at 1.3258.

In the Asian session, at GMT0300, the pair is trading at 1.3247, with the GBP trading 0.08% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3193, and a fall through could take it to the next support level of 1.3139. The pair is expected to find its first resistance at 1.3313, and a rise through could take it to the next resistance level of 1.3379.

Moving ahead, traders would await the release of UK’s GfK consumer confidence index for May, slated overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.