Sample Category Title

Japan’s Retail Trade Sharply Rebounded In April, Whereas Large Retailers’ Sales Surprisingly Dipped In The Same Month

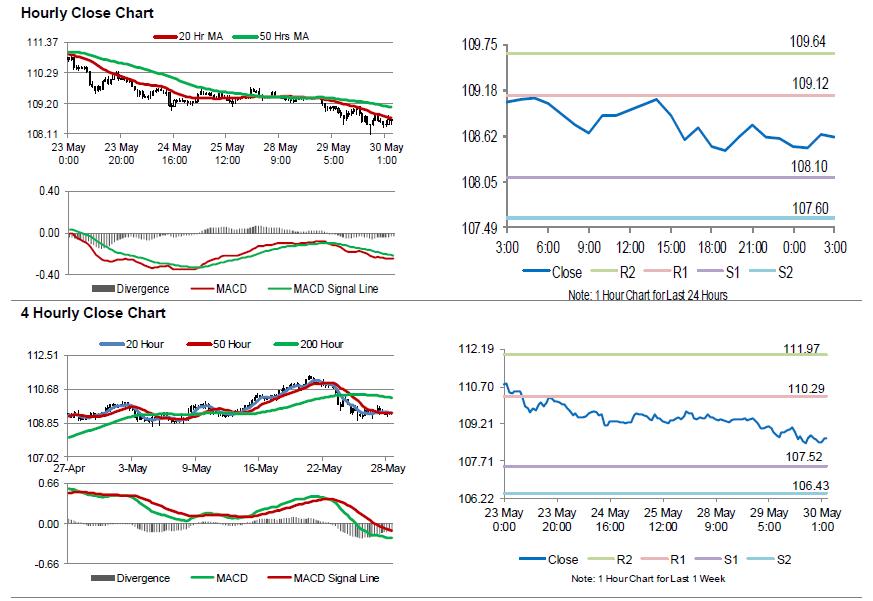

For the 24 hours to 23:00 GMT, the USD declined 0.78% against the JPY and closed at 108.58.

The Japanese Yen gained ground against the USD, as political turmoil in Italy boosted demand for the safe haven currency.

In the Asian session, at GMT0300, the pair is trading at 108.61, with the USD trading slightly higher against the JPY from yesterday's close.

Overnight data indicated that Japan's retail trade rebounded 1.4% a monthly basis in April, beating market expectations for a rise of 0.5%. In the prior month, retail trade had recorded a drop of 0.7%. On the other hand, the nation's large retailers' sales unexpectedly dropped 0.8% on a monthly basis in April, confounding market consensus for an advance of 0.2%. Large retailers' sales had registered a revised similar rise in the prior month.

The pair is expected to find support at 108.10, and a fall through could take it to the next support level of 107.60. The pair is expected to find its first resistance at 109.12, and a rise through could take it to the next resistance level of 109.64.

Going ahead, market participants would focus on Japan's industrial production data for April, due to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

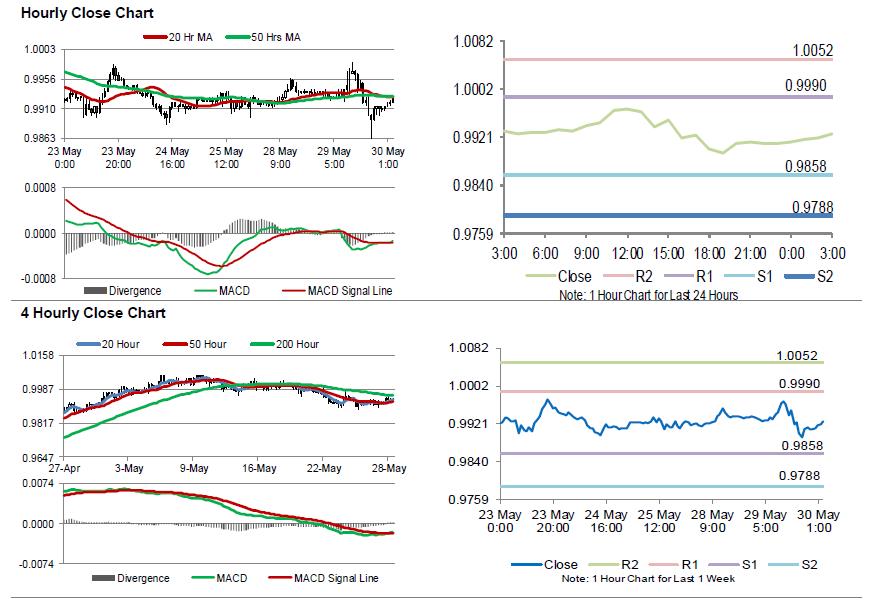

Swiss Trade Surplus Widened Beyond Expectations In April

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the CHF and closed at 0.9910.

On the data front, Switzerland’s trade surplus widened more-than-expected to CHF2.3 billion in April, after registering a revised surplus of CHF1.7 billion in the preceding month. Market participants had anticipated the nation’s trade surplus to widen to CHF2.2 billion.

In the Asian session, at GMT0300, the pair is trading at 0.9927, with the USD trading 0.17% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9858, and a fall through could take it to the next support level of 0.9788. The pair is expected to find its first resistance at 0.9990, and a rise through could take it to the next resistance level of 1.0052.

Moving ahead, traders would closely monitor Switzerland’s ZEW expectations index and KOF leading indicator for May, set to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

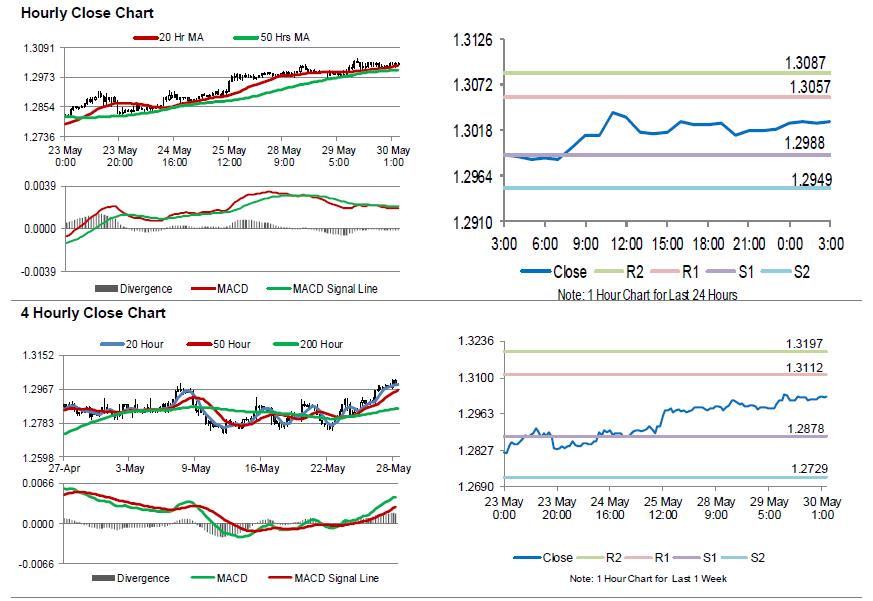

Loonie Trading On A Weaker Footing, Ahead Of BoC”s Interest Rate Decision

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.3020.

In the Asian session, at GMT0300, the pair is trading at 1.3028, with the USD trading 0.06% higher against the CAD from yesterday''s close.

The pair is expected to find support at 1.2988, and a fall through could take it to the next support level of 1.2949. The pair is expected to find its first resistance at 1.3057, and a rise through could take it to the next resistance level of 1.3087.

Later in the day, all eyes would be on the Bank of Canada''s (BoC) monetary policy decision. Investors widely expect the central bank to stand pat on interest rates.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

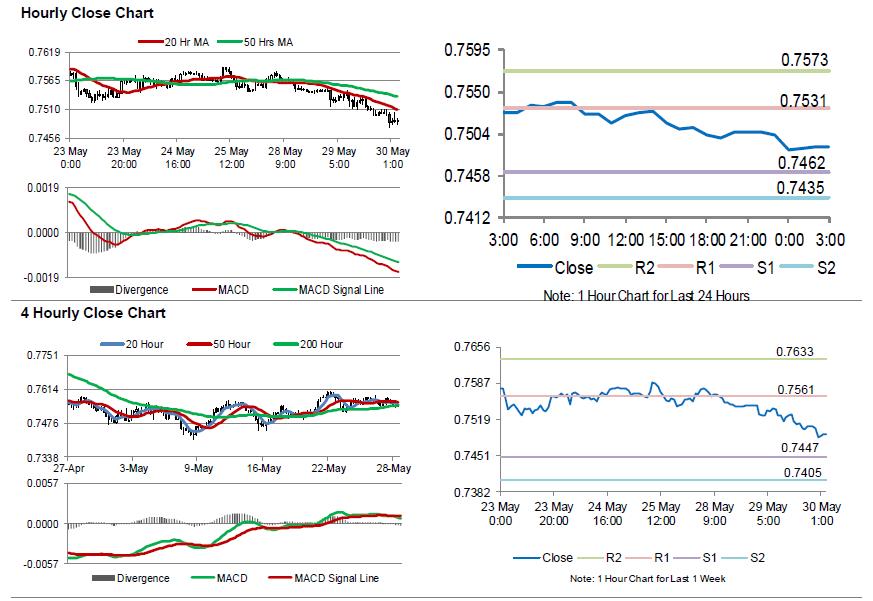

Australia’s Building Approvals Plunged In April

For the 24 hours to 23:00 GMT, the AUD declined 0.58% against the USD and closed at 0.7502.

LME Copper prices declined 0.65% or $44.5/MT to $6841.5/MT. Aluminium prices declined 0.96% or $44.5/MT to $2260.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7490, with the AUD trading 0.16% lower against the USD from yesterday's close.

Early morning data showed that Australia's seasonally adjusted building approvals retreated more-than-anticipated by 5.0% MoM in April, weighed by a sharp plunge in apartments. Market participants had envisaged building approvals to drop 3.0%, after registering a revised gain of 3.5% in the previous month.

The pair is expected to find support at 0.7462, and a fall through could take it to the next support level of 0.7435. The pair is expected to find its first resistance at 0.7531, and a rise through could take it to the next resistance level of 0.7573.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

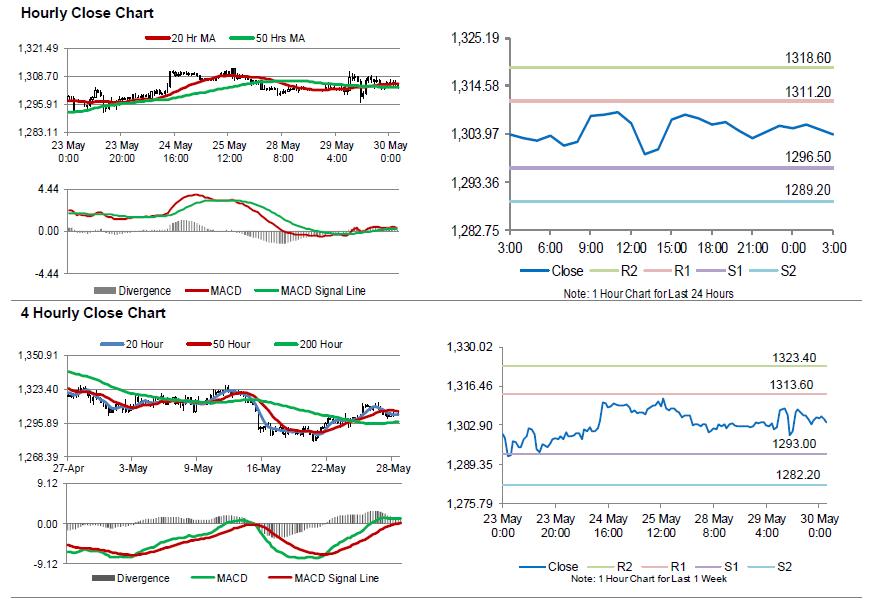

Gold: Yellow Metal Reverses Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, Gold rose 0.16% against the USD and closed at USD1304.50 per ounce, as a broad weakness in global equities increased demand for the precious yellow metal as an alternative investment.

In the Asian session, at GMT0300, the pair is trading at 1303.80, with gold trading 0.05% lower against the USD from yesterday’s close.

The pair is expected to find support at 1296.50, and a fall through could take it to the next support level of 1289.20. The pair is expected to find its first resistance at 1311.20, and a rise through could take it to the next resistance level of 1318.60.

The yellow metal is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

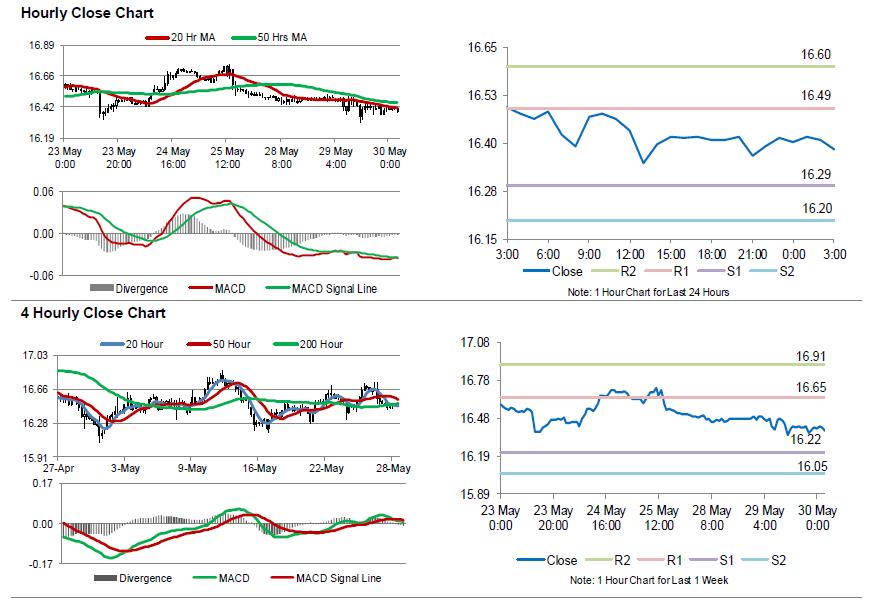

Silver: White Metal Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, Silver declined 0.42% against the USD and closed at USD16.42 per ounce.

In the Asian session, at GMT0300, the pair is trading at 16.39, with silver trading 0.18% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.29, and a fall through could take it to the next support level of 16.20. The pair is expected to find its first resistance at 16.49, and a rise through could take it to the next resistance level of 16.60.

The white metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

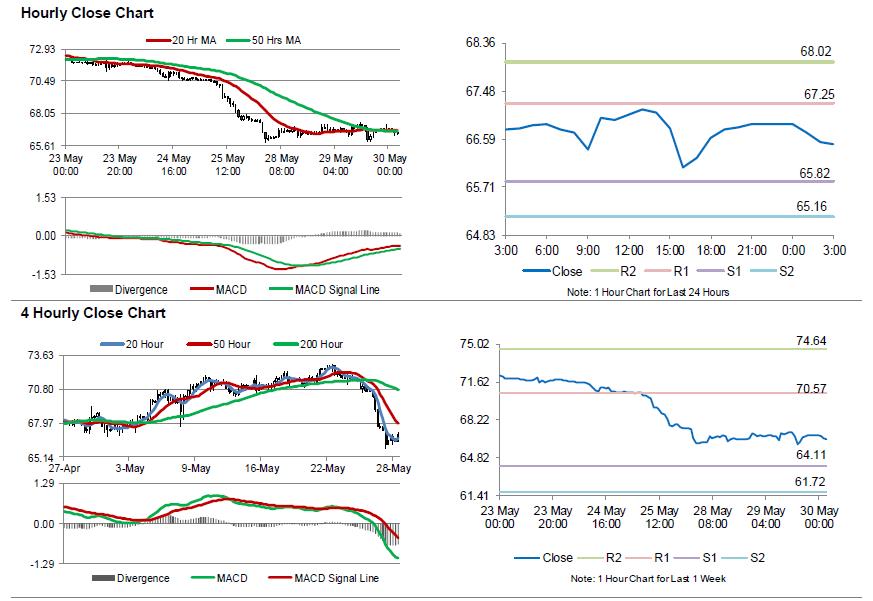

Crude Oil: Oil Trading On A Weaker Footing, Ahead Of API’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil declined 0.18% against the USD and closed at USD66.86 per barrel, on reports that OPEC and Russia are considering increasing crude production by 1.0 million barrels per day.

In the Asian session, at GMT0300, the pair is trading at 66.49, with oil trading 0.55% lower against the USD from yesterday's close.

The pair is expected to find support at 65.82, and a fall through could take it to the next support level of 65.16. The pair is expected to find its first resistance at 67.25, and a rise through could take it to the next resistance level of 68.02.

Crude oil is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

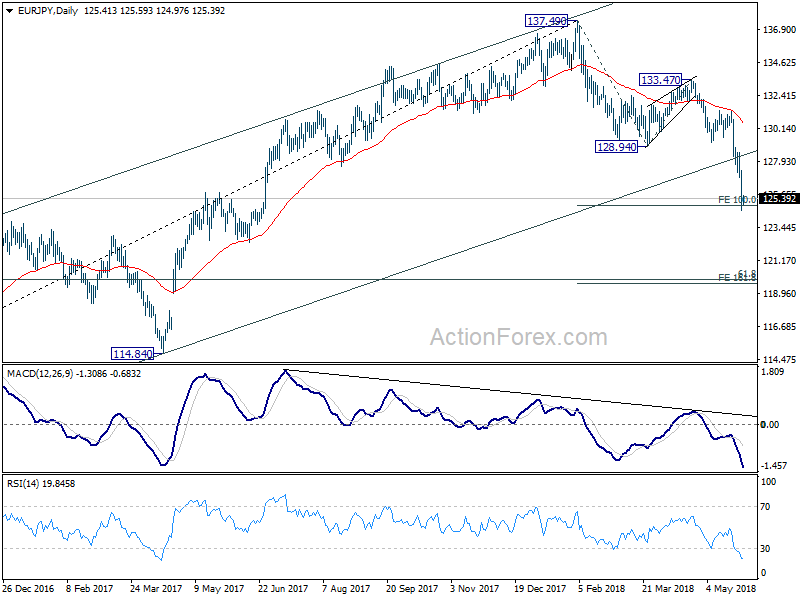

Market Morning Briefing: Euro Yen Has Fallen Very Quickly Towards 125

STOCKS

After trading in the small, sideways and narrow region, Dow (24361.45, -1.58%) finally moved down to indicate further bearishness in the coming sessions towards 23750. Near term resistance on the weekly charts have held well and there is enough room on the downside just now. View is bearish for the coming sessions.

Dax (12666.51, -1.53%) continues to move down after breaking the uptrend last week. 12200-12000 levels could again be the downside target for the coming sessions.

Nikkei (21972.53, -1.73%) has also broken below the 22400 mark and shown first signs of bearishness. While the fall continues, Nikkei could be headed towards 21600.

Shanghai (3064.94, -1.78%) also moved down below 3100 to test 3050 on the downside. An immediate bounce from 3050, if not seen could turn bearish for the medium to long term for Shanghai. Watch price action near 3050.

Following the bearish trend of the other global indices, the Nifty (10633.30, -0.52%) could also see a sharp fall in today’s session targeting 10550 or even lower. Near term looks bearish for Nifty.

COMMODITIES

65.60/70 is immediate support for WTI (66.48) as visible on the daily charts. While that holds, the crude price could bounce back towards 68-69 levels in the coming sessions. A break below 65.60, if seen would make the crude price vulnerable to a sharp fall towards 64 or lower.

Brent (74.91) has immediate support near 74.50 which may hold for now, else Brent could test lower support near 73.50-73.70 region.

Gold (1299.10) is almost stable. Although there is support visible on the 3-day and weekly charts, there is possibility of the price moving down to test 1280. A break below 1280, if seen would be bearish for Gold in the medium term opening up chances of 1260-1250 on the downside. For now we could see some trade in the 1280-1310 region.

Copper (3.0520) is trading lower and looks bearish towards 3.02. Watch price action near 3.02; if it fails to bounce from 3.02, it could be headed towards 3.00-2.95 in the medium term.

FOREX

Dollar index (94.95) touched 95 yesterday, slightly earlier than we had expected. The political turmoil in Italy seems to have spurred the demand for Dollars relative to the Euro, thereby leading to this quick strengthening. We had earlier mentioned that the 89 weeks MA near 95.63 could be a possible extension beyond 95. After that, the Dollar should dip. If it breaches 95.63, we would have to revisit this hypothesis and look for higher levels. In today’s session, a dip to 94.6 could take place before another rise towards 95.

Euro (1.1525) has been severely impacted by the political crisis in Italy and saw a low near 1.151 yesterday. It is now trading near our downside target of 1.155-1.145. 1.144 is the 89 weeks MA and could produce a bounce. On the 3 day line chart, 1.135-1.140 is also seen as possible support. Hence the downside might just extend even below 1.145. Let’s wait and watch.

Dollar Yen (108.58) did test the 21 weeks MA near 108 yesterday. As we mentioned yesterday, this could be a crucial level and a break of the same could lead to a phase of bearishness for Dollar Yen. With investors jittery regarding the Italy crisis, Yen might strengthen since it is considered as a safe asset. A break of 108 could result in a quick downmove to 106-105 (seen as crucial support on weekly candles).

Euro Yen (125.13): Euro Yen has fallen very quickly towards 125 (support on weekly candles), against our expectation of a fall by next week. This is a crucial support level and if this is broken as well, the next downside target could be as low as 120 (seen as support on 3 day line chart).

Pound (1.3248): As per our expectation of a test of levels near 1.32, Pound did test a low of 1.3205 yesterday. It could move lower over the next 1-2 weeks with the next downside target being near 1.30 (on weekly candles). A break of 1.30 could imply continued bearishness in the medium term.

Dollar Rupee (67.865) : Look for range trade between 67.60-68.20.

INTEREST RATES

The political instability in Italy has led to investors moving away from equity towards safer debt, and that has in turn, led to a dramatic fall of bond yields globally. Our earlier projection of a medium term target of 3.2%-3.3% for the US 10 Year yield might now need downward revision.

US 10 Yr Yield (2.82%), 30 Yr (3.00%), 5 Yr (2.63%), 2 Yr (2.34%):

The US 10 year yield saw a low near 2.75% yesterday and has risen from there. We believe there could be some support near 2.75% which could push the 10 Year towards 2.9% again. However, if 2.75% is broken, the US 10 year would move further down to test medium term support near 2.6%-2.5%.

The US 30 Year alongside could see a test of 2.9% if the US 10 year breaks 2.75%.

The German 10 Year yield (0.26%) could get some support near 0.18%-0.19% and could rise back up from there.

Re-emergence of Monetary Policy Divergence II – High – Yield Currencies

In our report last week, we pointed out that monetary policy divergence between the Fed and other major central banks has re-emerged since April. While economic developments in the first several months of the year have reinforced FOMC’s commitment to continue gradual rate hike as planned, other major centrals are either keen on sticking to the accommodative monetary policies adopted in the aftermath of the global financial crisis or staying very cautious in implementation rate hike. This report seeks to analyze how the divergence has affected the movement of some traditional high-yield currencies.

Australia: RBA has kept the cash rate at a record low of 1.5% for almost 2 years. The market does not expect another rate hike until 2019. RBA’s minutes for the May meeting affirmed that it has no urgency to raise rates. The members acknowledged the economic growth momentum, expecting stronger growth “over the following couple of years” would “reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate”. However, they remained cautious over the pace of wages growth and inflation, forecasting both to only improve gradually as “spare capacity in the economy was expected to be reduced only slowly”. This assessment has direct impact on the monetary policy outlook. Noted explicitly, the RBA saw no “strong case for a near-term adjustment in monetary policy” as “as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual”.

Hailed as high-yield currency, Aussie had been a dominant player in carry trade, a strategy involving borrowing in a low-yielding currency to fund investments in higher-yielding assets elsewhere. Indeed, Australian yields have been above those of the US over the past four decades. The chart below shows that the only time that 10-year Australian yield trading below that of the US was during 4Q78- 3Q81 period, as well as some time in 2Q98. We notice that a similar trend re-emerged in February this year has been building up more sophisticatedly over the past two months. The direction of AUDUSD has a history of trading the yield differentials of the currency pair, despite derailment from time to time. AUDUSD rallied in January this year although AU-US yield differential has begun to fall. This was mainly driven by the broad-based weakness in the US dollar as the White House attempted to talk down the greenback, accompanied with less exciting economic dataflow. However, currency pair has reversed trend since February, displaying positive correlation with the deepening of negative yield differential between Australian and US bonds.

New Zealand: RBNZ’s monetary policy stood still in May with the OCR unchanged at 1.75%. The message delivered by the central bank came in slightly more dovish than expected. The central bank revised lower its inflation forecasts slight for coming quarters slightly, pushing backward the time that inflation would reach the +2% target to 4Q20, from 3Q20 prior. On the monetary policy outlook, RBNZ noted that interest rates would stay at “expansionary level for a considerable period of time”, in order to achieve the goal of maximum and sustainable employment, and low and stable inflation. The most dovish part of the message was that it indicated that “the direction of our next move is equally balanced, up or down”. This was compared with the March reference that “monetary policy remains easy in the advanced economies but is gradually becoming less stimulatory”.

From the perspective of yield differential, AUD has the capability to outperform NZD. Despite the lack of urgency to act, RBA continued to hold the view that “the next move in the cash rate will be up, not down”. This comes in contrast with RBNZ’s “balanced” view of future rate direction. Adding to the dovish hint, RBNZ discussed unconventional monetary policy at a bulletin article released on May 23. It indicated that the unconventional monetary policies adopted by some major central banks were “successful in easing financial conditions”. It added that there were “emerging research suggests they boosted inflation and activity”. Referring to RBNZ’s monetary policy, the central bank suggested that, with a policy rate at 1.75%, there is “significant further room to ease monetary policy in a conventional way, and conventional monetary policy remains effective in influencing inflation and activity”.

Canada: Following two rate hikes in 2017 and one more in January this year, BOC has kept its powder dry since then. Recently, the central bank has cautiously noted that future monetary policy change would be “guided by incoming data” and directed by the future of trade policy. In our preview for the May meeting, we noted that April’s inflation data was mixed, instead of dovish as some judged. First quarter growth report might show accelerating momentum of economic expansion. Although payrolls surprisingly contracted in the latest point, the unemployment rate has stayed at multi-decade low. The macroeconomic picture does not entirely go against rate hike. The Achilles heel is the highly uncertain outlook trade policy. US’ abrupt launch of national security investigation into car and truck imports is partly targeting NAFTA re-negotiation. The investigation might lead to new US tariffs similar to those imposed on imported steel and aluminum in March. The aim of this act is to threaten Canada and Mexico, pressuring them to make concessions in the new NAFTA.

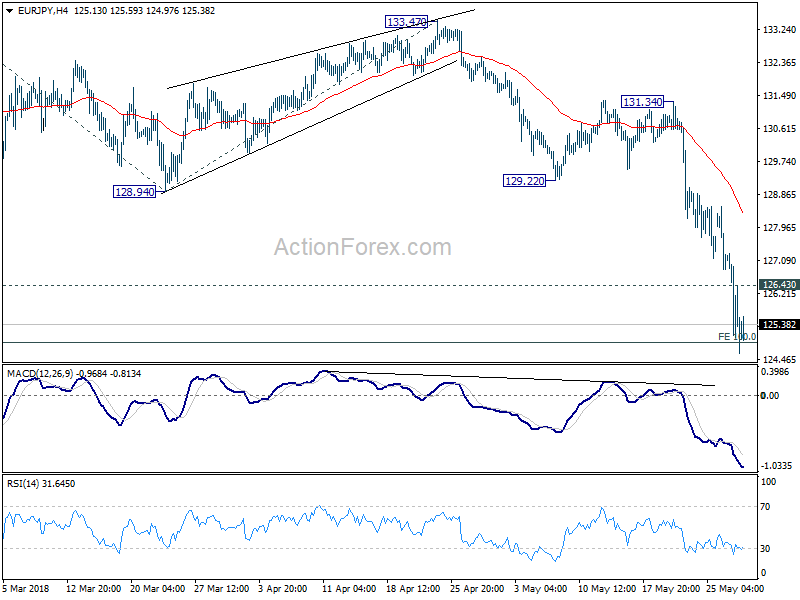

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.30; (P) 125.80; (R1) 126.99; More....

EUR/JPY reached as low as 124.61 so far and breached 100% projection of 137.49 to 128.94 from 133.47 at 124.92. There is no sign of bottoming yet despite oversold condition in both 4 hour and daily RSI. Intraday bias remains on the downside. Sustained trading below 124.92 will pave the way to 161.8% projection at 119.63 next. On the upside, above 126.83 minor resistance will turn intraday bias neutral and bring consolidation first. But near term outlook will remain bearish as long as 128.94 support turned resistance holds.

In the bigger picture, the case of medium term trend reversal continues to build up. That is rise from 109.03 (2016 low) could have completed at 137.49 already. This is supported by bearish divergence in daily MACD current downside acceleration, as well as the break of 38.2% retracement of 109.03 to 137.49 at 126.61. Deeper decline should be seen to 61.8% retracement at 119.90 and below. This will be the preferred case as long as 128.94 support turned resistance holds.