Sample Category Title

Sunset Market Commentary

Markets

Bond markets had a volatile ride today. The Italian-related risk-off trade initially continued and even accelerated. The Italian yield curve bear flattened. The 2-yr yield rose from 1% in the opening to 2.5% around European noon. The Italian 10-yr yield rose from 2.7% to 3.2% over the same time span with a peak at 3.4%. The German Bund continued to be safe haven with the German 10-yr yield at one stage 18 bps lower (!) and testing 0.18% support. The panic move suggests final repositioning to latest developments and could be technically labelled as an exhaustion move. We will now probably enter the campaign phase with opposition parties saying that Lega-5SM want a euro-exit and Lega-5SM saying they were denied their democratic right of governing. Recent polls suggest growing support for especially Lega (27% from 17% in March) while 5SM currently remains the biggest party (29.5% from 32.5%). The Italian 2-yr and 10-yr yields respectively returned to 2.3% and 3% at the time of writing. The German 10-yr yield is back near opening levels around 0.33%. Daily changes on the German yield curve range between -2.3 bps (2-yr) and +1.3 bps (30-yr). The decline in US yields is larger, catching up after yesterday’s Memorial Day Holiday. They vary between -2.8 bps (2-yr) and -5.5 bps (5-yr). 10-yr yield spread changes vs Germany widen 37 bps for Italy, 40 bps for Greece, 14 bps for Portugal, 10 bps for Spain and 5 bps for Ireland.

Today, the price action on global markets and in FX trading in particular was quite similar to yesterday. Markets were in some kind of wait-and-see mode in Asia. However, any uptick in Italian related (risky) assets initially was still considered an opportunity to offload this kind of risk. Italian equities declined and BTP’s fell off a cliff. More than was the case earlier this week, the move spilled over to other asset classes including the euro. Interest rate differentials between the US and Germany weren’t that much of a good guide for EUR/USD trading as Treasuries had still some catching up repositioning to do after yesterday’s US holiday. However, the combined blow-out of Italian government bond spreads and at the same time a new sharp decline in the 10-y German yield was a clear pointer of ongoing investor panic. EUR/USD tumbled from the 1.1640 area at the start of European dealings to fill bid in the 1.1510 area just before noon. From there, some easing in the ‘Sell-Italy’ trade kicked in. EUR/USD found a new short-term balance in the mid 1.15 area. So the 1.1554 MT support was broken intraday. EUR/USD (currently again 1.1580) tries to close above this barrier. Despite the risk-off sentiment, the gain of the yen (against the dollar) remained modest. USD/JPY spiked lower during the morning session but rebounded to the 109 area.

There was again little in the way of UK specific news today. The focus for sterling was also on the developing economic story in Italy. As was the case yesterday, EUR/GBP more or less followed the intraday trading dynamics of the headline EUR/USD currency pair. However, the intraday range stayed modest given the wild swings on other markets. EUR/GBP dropped temporary to the 0.87 area, but reversed about half of the intraday loss later in the session. (Currently 0.8720 area.) The EUR/GBP cross remains within the established technical barriers. For now sterling is still no preferred beneficiary of the Italian/EMU tensions.

News Headlines

The governor of the Bank of Italy has warned that the country was “a few short steps away” from losing the “asset of trust”, a rare intervention by the central bank into a political crisis that underlined the risk Rome faces as it stumbles to new elections. (FT)

German wages rose by 2.5% on average Y/Y in the first quarter, data showed, a sharp rise on late 2017 that supports expectations that consumers will remain a key driver of growth in Europe's largest economy. (Reuters)

US consumer confidence rose to 128.0 in May

US Conference Board consumer confidence rose to 128.0 in May, up from revised 125.6 in April, met expectations.

Conference Board noted in the release that:

- Consumer confidence increased in May after a modest decline in April,

- Consumers' assessment of current conditions increased to a 17-year high (March 2001, 167.5), suggesting that the level of economic growth in Q2 is likely to have improved from Q1.

- Consumers' short-term expectations improved modestly, suggesting that the pace of growth over the coming months is not likely to gain any significant momentum.

- Overall, confidence levels remain at historically strong levels and should continue to support solid consumer spending in the near-term.

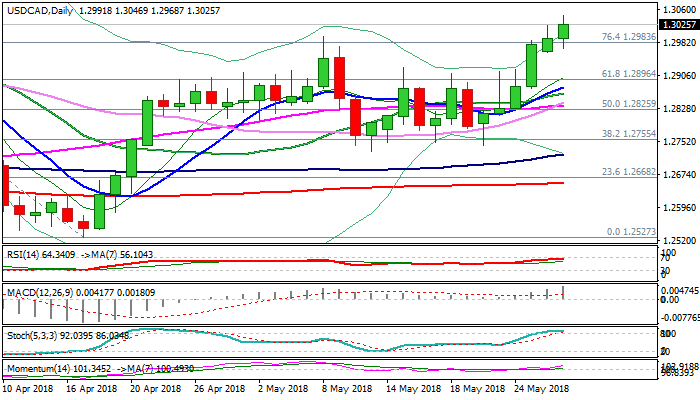

USDCAD – Close Above 1.30 Beeded to Signal Further Advance

The USDCAD pair extends bull-leg from 1.2742 (22 May low), trading in green for the sixth consecutive day and establishes above psychological 1.30 barrier, which was cracked on Monday but bulls failed to close above. Strong bullish momentum and multiple bull-crosses of daily MA's maintain bullish sentiment which requires close above 1.30 level (where the pair last traded two months ago) for extension towards key barriers at 1.3124/31 (2018 high posted on 19 Mar/Fibo 61.8% of 1.3793/1.2061 descend respectively). Broken top of thickening weekly cloud (1.2927) marks solid support which is expected to limit extended downticks.

Res: 1.3046; 1.3076; 1.3100; 1.3131

Sup: 1.3000; 1.2968; 1.2924; 1.2896

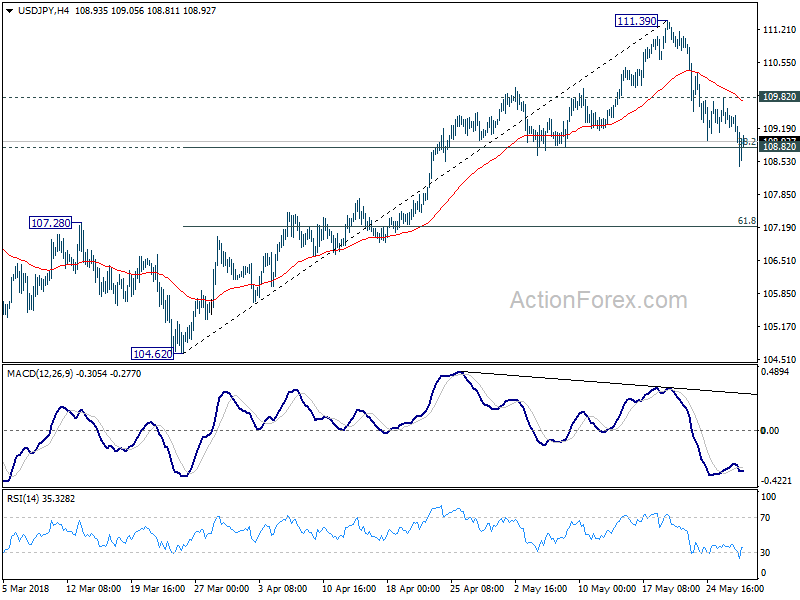

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.13; (P) 109.52; (R1) 109.80; More...

USD/JPY drops to as low as 108.41 so far today and there is no sign of bottoming yet. Sustained trading below 108.82 cluster support (38.2% retracement of 104.62 to 111.39 at 108.80) will dampen our bullish view. And USD/JPY is probably not reversing the larger decline from 118.65 yet. In that case, deeper fall will be seen to 61.8% retracement at 107.20 and possibly below. Nonetheless, strong rebound from the current level, followed by break of 109.82 will revive near term bullishness and bring retest of 111.39 first.

In the bigger picture, for now, we're holding on to the view that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 108.82 will dampen the bullish outlook and revive the case of a break of 104.62 low before medium term bottoming.

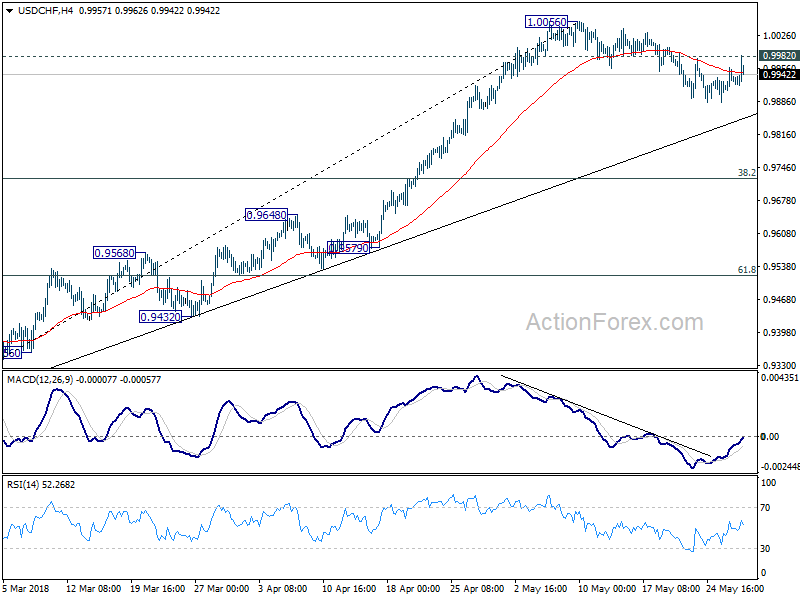

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9905; (P) 0.9931; (R1) 0.9963; More...

Despite breaching 0.9977 minor resistance, there is no follow through buying yet. Intraday bias in USD/CHF remains neutral first. For now, we're still treating price actions fro 1.0056 as a near term correction. Hence even in case of another fall, downside should be contained by trend line (now at 0.9853) to bring rebound. Above 0.9982 should bring retest of 1.0056 high. However, sustained break of the trend line will argue that it's a larger scale correction and will target 0.9724 fibonacci level.

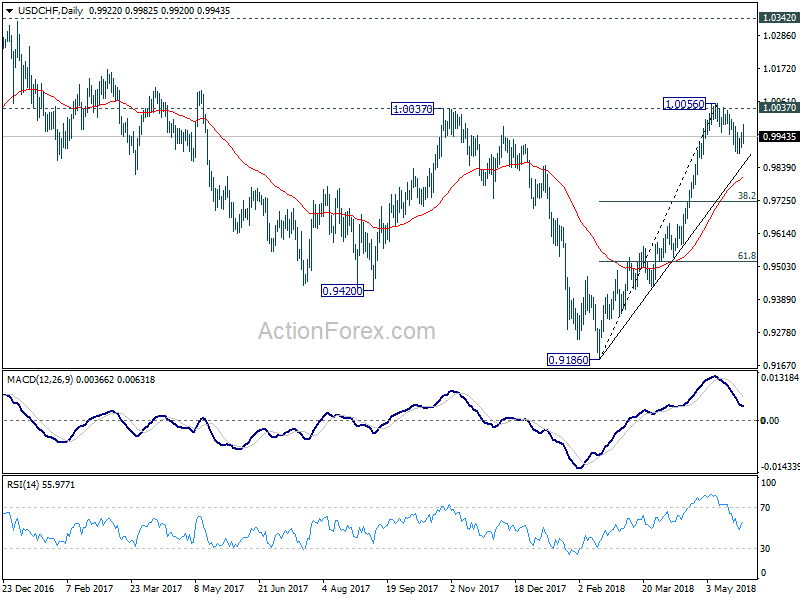

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

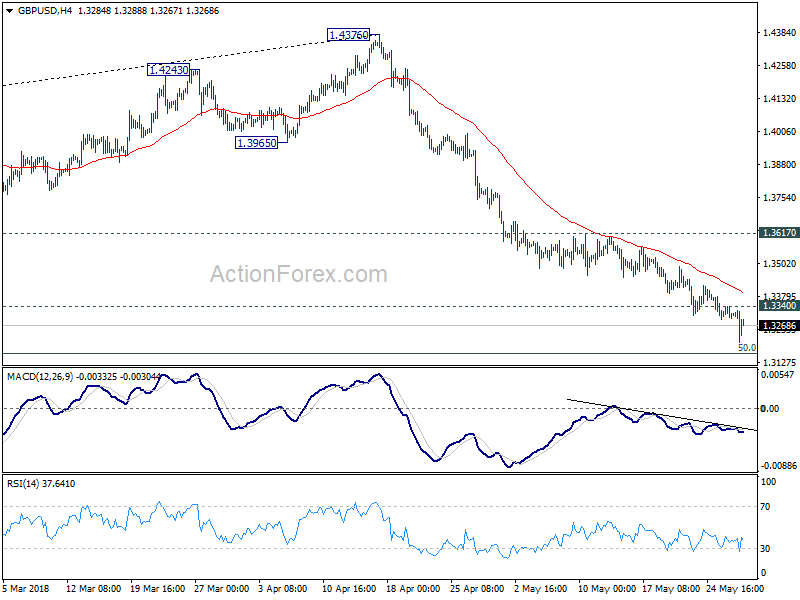

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3315; (R1) 1.3337; More...

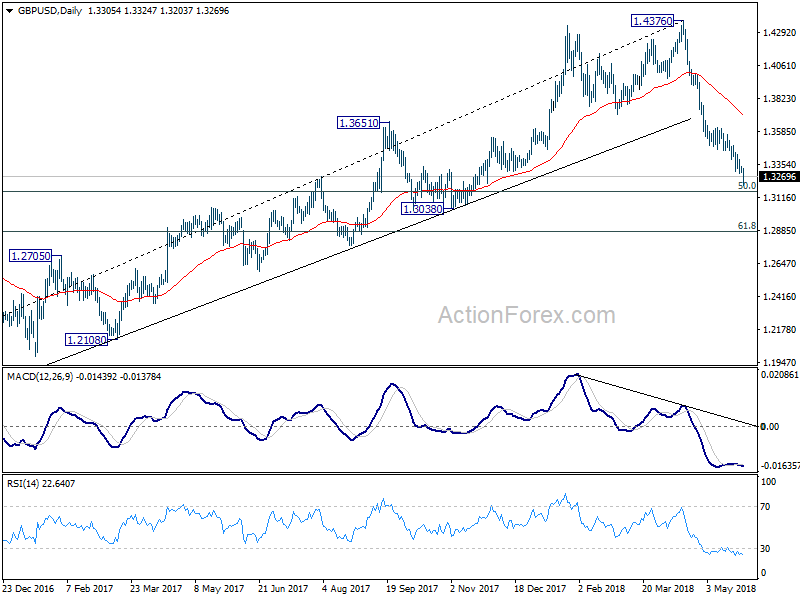

GBP/USD's fall from 1.4376 is still in progress. Intraday bias stays on the downside for next target at 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will larger 61.8% retracement at 1.2875 next. On the upside, above 1.3340 minor resistance will turn intraday bias neutral and bring consolidation. But break of 1.3568 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3730) holds, even in case of strong rebound.

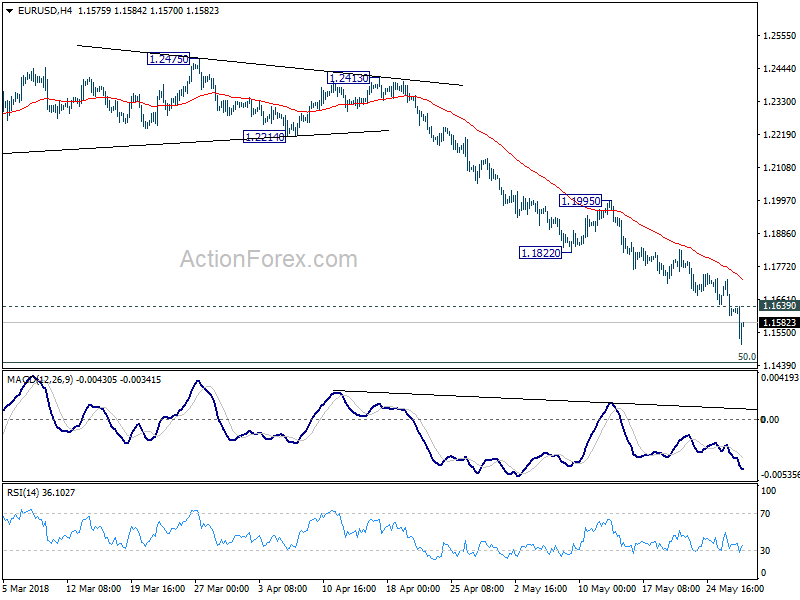

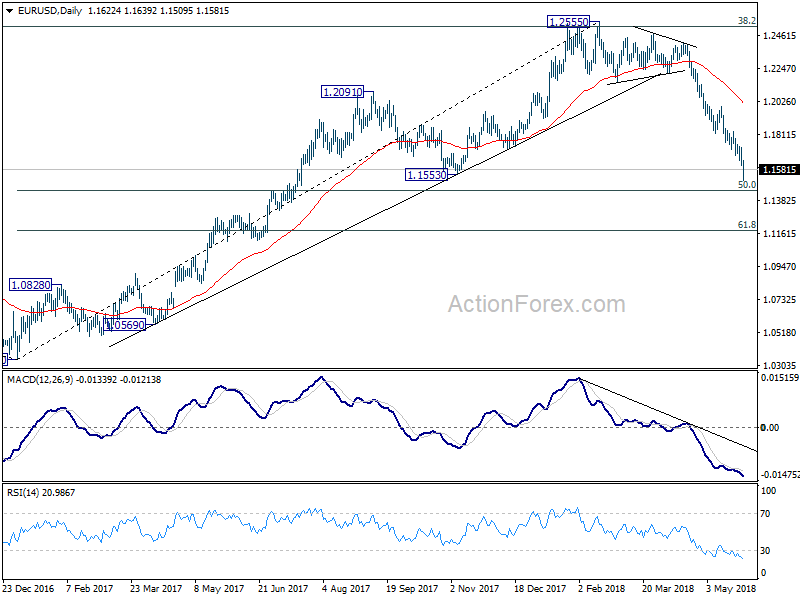

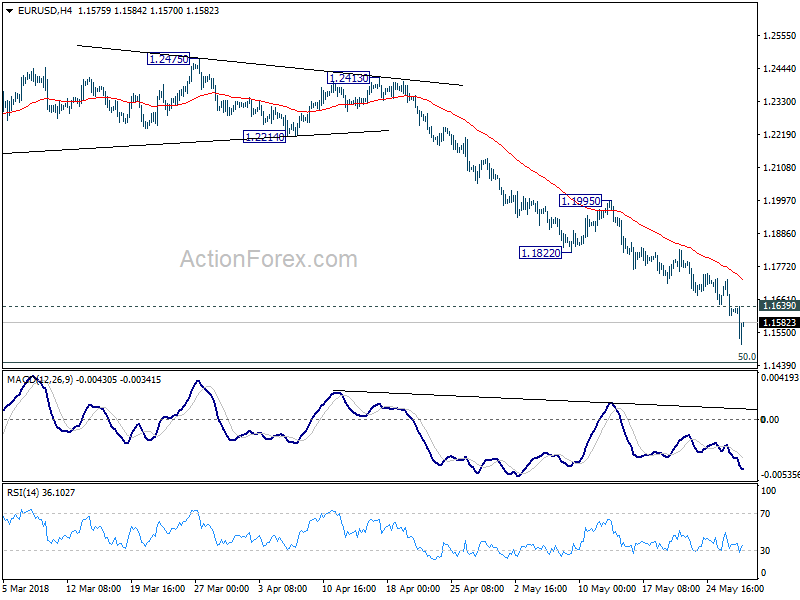

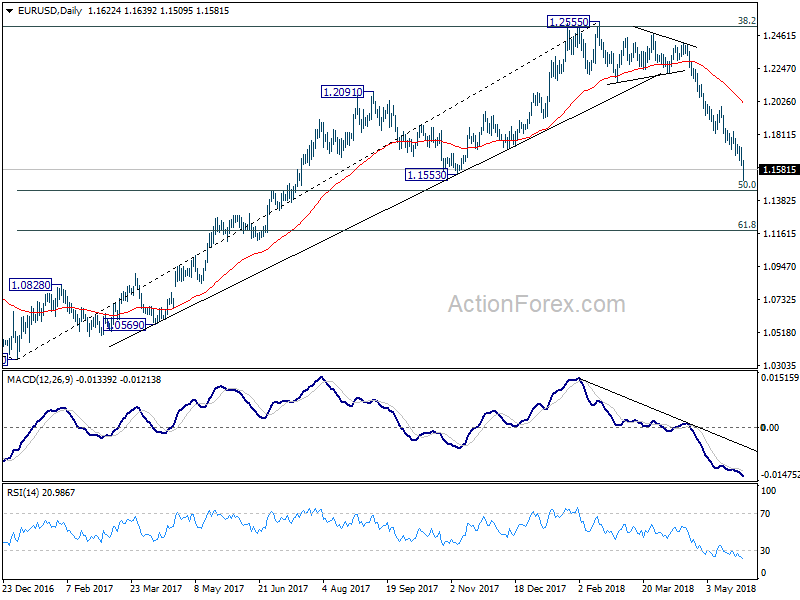

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1578; (P) 1.1653 (R1) 1.1700; More.....

EUR/USD drops to as low as 1.1509 so far today. While it recovers mildly since then, it's kept below 1.1640 minor resistance. Intraday bias remains on the downside for further decline. Current fall from 1.2555 is in progress and should target 50% retracement of 1.0339 to 1.2555 at 1.1447 next. On the upside, above 1.1639 minor resistance will turn intraday bias neutral again. But after all, near term outlook will remain bearish as long as 1.1995 resistance holds, in case of recovery.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Pared Loss after Steep Selloff as 5 Star Di Maio Calmed Markets

While Euro remains the worst performer for today, selling slowed and it recovered much ground as in early US session. Investors seemed to be calmed by Five Star leader Di Maio's facebook comment that he never see leaving the Euro. Also, there are reassessment on how bad the situation could be. 10 year Italian yield reached as high as 3.313 earlier today and is now back at 2.926, but still up 0.257. German 10 year bund yield dropped to as low as 0.187 earlier and is now at 0.331, still down -0.022. German-Italian yield spread is back below 300 bps. US 10 year yield also back at 2.885 after dipping to as low as 2.807.

Overall in the currency market, New Zealand and Australia Dollar follow Euro as the second and third weakest. Yen remains the strongest on risk aversion. But Swiss Franc lags behind Dollar and Canadian Dollar. Technically, EUR/CHF just touched 1.1445 key support level but recovered. Eyes will be on whether it could bottom at around 1.1445 as expected. USD/JPY broke 108.82 cluster support and now revived the bearish case that larger down trend from 118.65 is not completed.

Euro recovers as Five Star leader Di Maio said never sought to leave Euro

Euro and Italian bonds are given a mild lift after Five Star leader Luigi Di Maio said the never sought to leave the Euro via facebook comments. He said that with the "Government of Change" they should be meeting with other EU countries to explain to the the "economic policy that has never foreseen the exit from the euro." Meanwhile, he blamed the over 300 German Italian spread on the lack of prospects of the interim technocrat government.

Separately, Bank of Italy Governor Ignazio Visco warned that Italy is just a few short steps away from "the very serious risk of losing the irreplaceable asset of trust". He defended that Italy is "not constrained by the European rules but by economic logic" and there was no "shortcut" to lower the country's debt.

Money markets quickly retreat ECB 2019 hike pricing

Eurozone money markets are quick to pare back pricing of ECB rate hike in June. Now, the difference between Eonia and forward Eonia rates dated for June 2019 ECB meeting stands at 3 bps. That's half of 6bps last week and 1/3 of 9bps earlier this month. The pricing indicates around 30% chance of a 10 bps hike in the -0.4% deposit rate by June next year. Though, it's still generally expected that ECB would end the asset purchase program this year, as it has done its job already.

While Italy is definitely a concern for ECB policy makers, it should be reminded that they are not totally certain on the reasons for Q1's slow down yet. And how well the economy rebounds in Q2 is a question to be answered. Based on current vulnerable market sentiments, Thursday's Eurozone May CPI flash will be eve more crucial to Euro.

EEF Phipson slams Theresa May's Max Fac brexit border solution as naive, unrealistic and a non-starter

The UK EEF manufacturers' organization slammed Prime Minister Theresa May's "Max Fac" proposal for UK and EU customs as "naive" and "unrealistic". Max fac, or maximum facilitation, is a technological border solution that May push to implement by the time a planned Brexit transition period ends in December 2020.

EEF Chief Executive Stephen Phipson said in a statement that the debate on MaxFac is "misguided". The focus should be on whether it is good enough to "provide a frictionless border" for the "highly complex integrated supply chains with Europe. Also, focus is on whether it "can be implemented quickly enough to be ready for December 2020". Phipson said the answer is "overwhelming no". And, "it may have some long term benefits, but suggesting MaxFac is a solution to our immediate problems is a non-starter".

China said to be considering to increase US coal imports

Bloomberg reported, quoting unnamed source, that China is considering to buy more coal from the US, as part of the plan to reduce trade surplus. In particular, China could boost purchase from West Virginia.

As in 2017, US coal just contributed a tiny portion of China's import. 108.9m tons were from Indonesia, 79.9m ton from Australia, 34.0 tons from Monglolia. Only 3.2m tons were from the US. It's unsure whether China has plan to cut imports from other countries.

PBoC Yi pledges gradual, steady efforts to financial sector reforms

China's PBoC Governor Yi Gang said that the authority will ensure gradual, steady efforts to financial sector reforms.

He acknowledged that "our financial sector still has a lot room to open up relative to the requirements of economic and financial development." And, "the three reforms -- opening up the financial sector to internal and external firms, exchange rate mechanism, and capital account convertibility -- have to be coordinated and pushed ahead together."

Regarding Yuan internationalization, he said that requires "steady progress on capital account convertibility. And, "if many capital account items are restricted, then the financial sector opening is only in name instead of in reality. He added that "only when our capital account is basically convertible and that our financial sector opens up in both ways, will our currency mechanism and the entire financial sector achieve a coordinated development."

St. Louis Fed Bullard urged caution on further rate hike with three reasons

St. Louis Fed President James Bullard urged caution on further rate hike in near term in a presentation at a seminar in Tokyo. And he laid out three reasons for discussions. First, market-based inflation expectations in the U.S. remain somewhat low. Second, the current level of the policy rate appears to be neutral, meaning it is putting neither upward nor downward pressure on inflation. Third, the U.S. nominal yield curve could invert later this year or in 2019, which would be a bearish signal for U.S. macroeconomic prospects,.

Here is the full presentation.

Canada Freeland in Washington again for NAFTA talks

Canadian Foreign Minister Chrystia Freeland is on Washington today to continue NAFTA negotiations. Her spokesman Adam Austen said she will be there on Tuesday and Wednesday. And he added that "we've said all along we are ready to go (to Washington) at any time."

Mexican Economy Minister Ildefonso Guajardo said last week that there is around 40% chance of concluding NAFTA talks before Mexican presidential election on July 1. But Guajardo will not be there at the Tuesday meeting. Instead, he is in Paris for meetings of OECD and WTO.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1578; (P) 1.1653 (R1) 1.1700; More.....

EUR/USD drops to as low as 1.1509 so far today. While it recovers mildly since then, it's kept below 1.1640 minor resistance. Intraday bias remains on the downside for further decline. Current fall from 1.2555 is in progress and should target 50% retracement of 1.0339 to 1.2555 at 1.1447 next. On the upside, above 1.1639 minor resistance will turn intraday bias neutral again. But after all, near term outlook will remain bearish as long as 1.1995 resistance holds, in case of recovery.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Jobless Rate Apr | 2.50% | 2.50% | 2.50% | |

| 06:00 | CHF | Trade Balance (CHF) Apr | 2.29B | 2.23B | 1.77B | 1.69B |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 3.90% | 3.90% | 3.70% | |

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Mar | 6.80% | 6.40% | 6.80% | |

| 14:00 | USD | Consumer Confidence May | 128 | 128.7 |

Canadian Dollar Drops to 2-Month Low, BoC Rate Announcement Next

The Canadian dollar continues to lose ground and has recorded losses for a sixth consecutive day. In Tuesday’s North American session, USD/CAD is trading at 1.3019, up 0.36% on the day. On the release front, there are no Canadian indicators. The US releases CB Consumer Confidence, which is expected to dip to 128.0 points. On Wednesday, there are a host of key indicators. Canada will release Current Account and the Raw Materials Price Index, and the US publishes ADP nonfarm payrolls and Preliminary GDP.

The Canadian dollar remains under pressure this week. The currency has declined 1.4 percent in the month of May and is currently at its lowest level since mid-March. There could be further headwinds for the dollar this week, if, as expected, the Bank of Canada holds interest rates at 1.25 percent. Inflation has moved closer to the BoC target of 2 percent and economic growth has been steady, so the bank may opt for the sidelines when policymakers meet on Wednesday. However, with the Federal Reserve widely expected to raise rates next month, the Canadian dollar will be less attractive to investors. Meanwhile, the growing political crisis in Europe has unnerved investors, which could hurt minor currencies like the Canadian dollar, which tends to lose ground when risk appetite is weak.

Is the summit on or off? The drama and uncertainty continue to swirl around the upcoming summit between President Trump and North Korean leader Kim Jong-un, which may or may not take place on June 12 in Singapore. Just a few days ago, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the White House has since sent a team to Singapore and a senior North Korean official is on his way to Washington to meet with Secretary of State Mike Pompeo. These moves have fueled speculation that the summit will take place, although curiously, neither side has confirmed this.

Money markets quickly retreat ECB 2019 hike pricing

Eurozone money markets are quick to pare back pricing of ECB rate hike in June. Now, the difference between Eonia and forward Eonia rates dated for June 2019 ECB meeting stands at 3 bps. That's half of 6bps last week and 1/3 of 9bps earlier this month. The pricing indicates around 30% chance of a 10 bps hike in the -0.4% deposit rate by June next year. Though, it's still generally expected that ECB would end the asset purchase program this year, as it has done its job already.

While Italy is definitely a concern for ECB policy makers, it should be reminded that they are not totally certain on the reasons for Q1's slow down yet. And how well the economy rebounds in Q2 is a question to be answered. Based on current vulnerable market sentiments, Thursday's Eurozone May CPI flash will be eve more crucial to Euro.