Sample Category Title

Yen Continues to Shine as Sentiments Weighed Down by Italy and Trade Tension

Italy political turmoil and trade tensions are weighing on market sentiments on two fronts. Italy will now likely go into a snap election soon. And the eurosceptic parties will frame that as referendum on Euro membership. US President Donald Trump reignites trade spat with China while NAFTA negotiation is going nowhere. More importantly, probably no one knows what's coming next when temporary exemption on US steel tariffs expire on June 1, this Friday.

DOW closed sharply lower by -391.61pts or -1.58% at 24361.45 overnight. And, it's having its sight on 24000 handle next. Asian market follow with Nikkei losing -1.5% at the time of writing. HK HSI is down -1.2%. The bond markets are even more volatile. US 10 year closed the regular session down -0.163 at 2.768. It hit as high as 3.115 just two weeks ago. German 10 year bund yield closed at 0.255 yesterday after hitting as low as 0.187. It's less than half of May's high at 0.651. On the other hand, Italian 10 year yield closed at 3.10 after hitting as high as 3.313, comparing to May's low at 1.736. German-Italian spread broke 300 handle yesterday and could revisit it again today.

One more thing to point out is that markets are fast in paring back Fed rate hike expectations. Fed fund futures are now pricing in less than 80% chance of a June hike to 1.75-2.00%. And it was 100% just a week ago. For another hike to 2.00-2.25% in September, fed fund futures are pricing in only 40% chance. And it was over 80% a week ago.

In the currency markets, Yen remains the strongest one for the week and is trading firmly in Asian session. Another safe haven currency Swiss Franc was uncertain and is mixed for the week. Dollar is the second strongest one for the week, thanks to flight for safety this time. Euro, naturally, trades as the weakest one for the week, followed by Aussie and then Canadian Dollar.

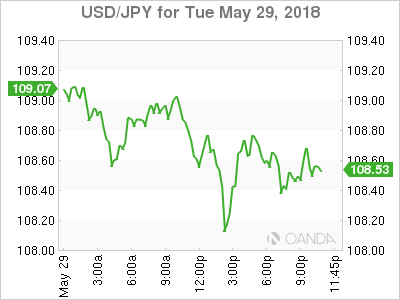

Technically, Yen crosses remains in near term down trend in general. USD/JPY's strong break of 108.82 now opens up the case for deeper fall to 107.20 fibonacci level. USD/CHF recovers after touching near term trend line support and could be heading back up. EUR/CHF broke a key support level at 1.1445 and could be heading to 1.12 handle. The contrasting outlook in USD/CHF and EUR/CHF is worth some attention.

Cottarelli didn't present cabinet to president Mattarella, possibly going to straight to snap election

Italian Prime Minister designate Carlo Cottarelli didn't present his cabinet to President Sergio Mattarella at the meeting yesterday. The president's spokesman Giovanni Grasso said that "the prime minister-designate met with the president and told him about the current situation. The two will meet again tomorrow morning."

It's obvious that the caretaker government won't have enough confidence vote. Whether Cottarelli make up a list of ministers or not, an early election is the most likely outcome. It's possible that Mattarella could dissolve the parliament in the coming days. With that, a snap election could be held as soon as July 29 or in early August. The anti-establishment parties could frame the election as a referendum on staying or leaving Euro.

Trump's White House issued strong statement on China, unexpected yet expected

The White House issued strong worded statement regarding trade relationship with China yesterday.

From a fact sheet titled "President Donald J. Trump is Confronting China's Unfair Trade Policies", it's said that "China has consistently taken advantage of the American economy with practices that undermine fair and reciprocal trade." And it accused that "China has aggressively sought to obtain technology from American companies and undermine American innovation and creativity."

The statement noted that "President Trump has taken long overdue action to finally address the source of the problem, China's unfair trade practices that hurt America's workers and our innovative industries." And, "President Trump has worked to defend America's intellectual property and proprietary technology from theft and other threats."

Simultaneously, there's another statement outlining the Steps to Protect Domestic Technology and Intellectual Property from China's Discriminatory and Burdensome Trade Practices.

The Chinese Ministry of Commerce responded in a statement that the US statements were unexpected yet expected. It said the today's statement contradict the consensus reached in Washington not long ago. And the MOFCOM pledged that "China has confidence, ability, and experience to safeguard the interests of the Chinese people and the country's core interests. China urges the United States to act in accordance with the spirit of the joint statement."

Canada PM Trudeau: No Nafta is better than a bad deal

Canadian Prime Minister Justin Trudeau dismissed the threat of auto tariffs of the US as "negotiating tactic" for NAFTA. And emphasized that won't push Canada to accept a bad deal. He added that "quite frankly that's simply not something we're going to do." Trudeau also reiterated that "no Nafta is better than a bad deal" and "we are not going to move ahead just for the sake of moving ahead."

He also talked down the collapse of NAFTA negotiation and said "the interconnectedness between the Canadian and U.S. economies is not going to change any time soon" and "you can't get around geography". And, "we are their (the Americans') number one customer and there is no question that any disruption of that flow of goods, yes, would be terrible for the Canadian economy but would also be pretty terrible for a lot of U.S. jobs."

Canadian Foreign Minister Chrystia Freeland is in Washington meeting with US Trade Representative Robert Lighthizer. She said there were "very productive discussions" but declined to give any details. Asked about the temporary exemption on steel tariffs that's going to expire this week, Freeland said "our government always is very ready and very prepared to respond appropriately to every action. We are always prepared and ready to defend our workers and our industries."

Trump brought up the issue of border wall again yesterday and said Mexico "do absolutely nothing to stop people from going through Mexico, from Honduras and all these other countries ... They do nothing to help us." And he said "in the end, Mexico is going to pay for the wall." Mexican President Enrique Pena Nieto responded in his tweet saying that "President @realDonaldTrump: NO. Mexico will NEVER pay for a wall. Not now, not ever. Sincerely, Mexico."

To recap, there are a few deadlines for NAFTA negotiations to complete. Firstly, the temporary exemption on US steel and aluminum tariffs will expire on June 1 and it's uncertain what will happen. Mexico Presidential election is upcoming on July 1. Timing is running out, or has already run out, for the current Congress to approve the new NAFTA deal within this year. And less pressing, the US has started national security investigation on automobile imports that could lead to new tariffs.

In the calendar - BoC to stand pat and offer no hint on hike

New Zealand building permits dropped -3.7% mom in April. Australia building approvals dropped -5.0% mom in April. Japan retail sales rose 1.6% yoy in April. UK BRC shop price dropped -1.1% yoy in May.

The calendar is extremely busy today. In European session, German retail sales, import price, unemployment and CPI will be featured. Swiss will release KOF leading indicator. France will release GDP revision. Eurozone will release confidence indications.

BoC is widely expected to keep interest rate unchanged at 1.25% today. Given the uncertainty around NAFTA, steel tariffs and the upcoming auto tariffs, the central is unlikely to give any hint on the timing of the next hike. Governor Stephen Poloz possibly doesn't have a clue himself too. Canada will also release IPPI and RMPI as well as current account.

From US, Q1 GDP revision, trade balance, and ADP employment will be featured. Fed will also release Beige Book economic report.

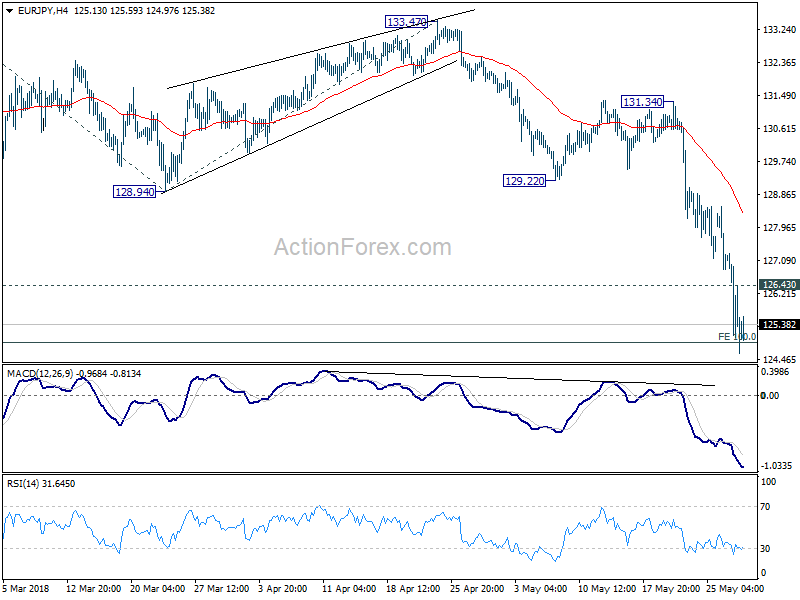

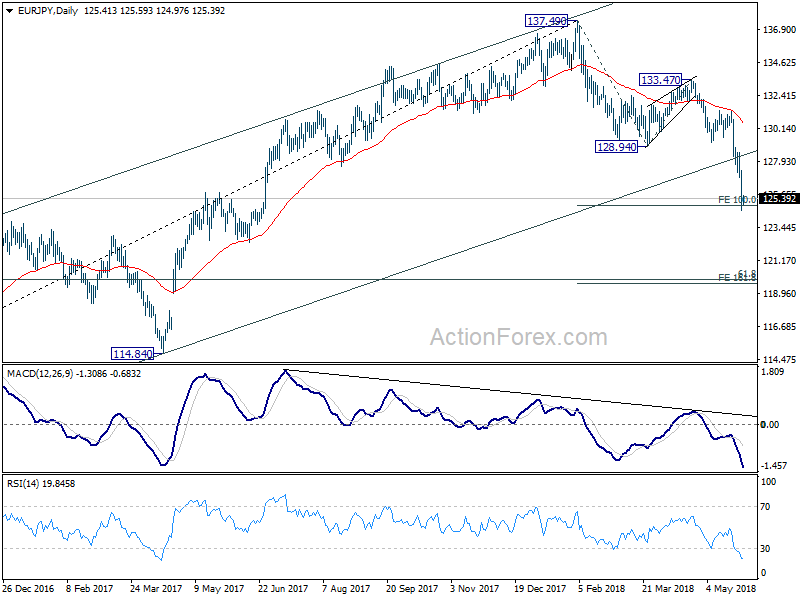

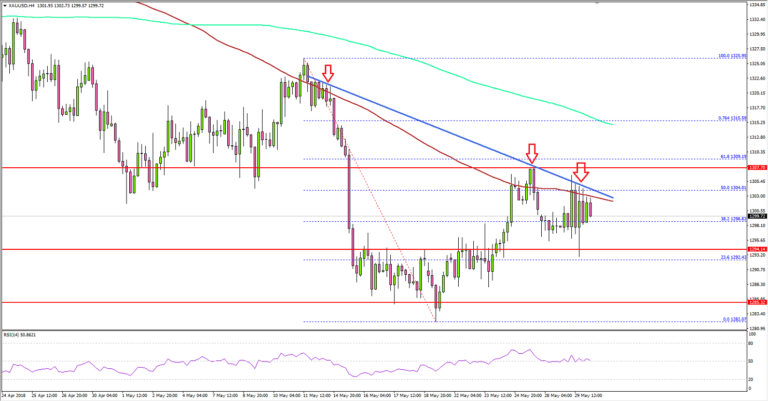

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.30; (P) 125.80; (R1) 126.99; More....

EUR/JPY reached as low as 124.61 so far and breached 100% projection of 137.49 to 128.94 from 133.47 at 124.92. There is no sign of bottoming yet despite oversold condition in both 4 hour and daily RSI. Intraday bias remains on the downside. Sustained trading below 124.92 will pave the way to 161.8% projection at 119.63 next. On the upside, above 126.83 minor resistance will turn intraday bias neutral and bring consolidation first. But near term outlook will remain bearish as long as 128.94 support turned resistance holds.

In the bigger picture, the case of medium term trend reversal continues to build up. That is rise from 109.03 (2016 low) could have completed at 137.49 already. This is supported by bearish divergence in daily MACD current downside acceleration, as well as the break of 38.2% retracement of 109.03 to 137.49 at 126.61. Deeper decline should be seen to 61.8% retracement at 119.90 and below. This will be the preferred case as long as 128.94 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Financial Stability Report | ||||

| 22:45 | NZD | Building Permits M/M Apr | -3.70% | 14.70% | 13.00% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -1.10% | -1.00% | ||

| 23:50 | JPY | Retail Trade Y/Y Apr | 1.60% | 0.90% | 1.00% | |

| 1:30 | AUD | Building Approvals M/M Apr | -5.00% | -3.00% | 2.60% | 3.50% |

| 5:00 | JPY | Consumer Confidence May | 43.9 | 43.6 | ||

| 6:00 | EUR | German Retail Sales M/M Apr | 0.50% | -0.60% | ||

| 6:00 | EUR | German Import Price Index M/M Apr | 0.70% | 0.00% | ||

| 6:45 | EUR | French GDP Q/Q Q1 P | 0.30% | 0.30% | ||

| 7:00 | CHF | KOF Leading Indicator May | 104.7 | 105.3 | ||

| 7:55 | EUR | German Unemployment Change May | -10K | -7K | ||

| 7:55 | EUR | German Unemployment Claims Rate May | 5.30% | 5.30% | ||

| 9:00 | EUR | Eurozone Business Climate Indicator May | 1.3 | 1.35 | ||

| 9:00 | EUR | Eurozone Economic Confidence May | 112 | 112.7 | ||

| 9:00 | EUR | Eurozone Industrial Confidence May | 6.8 | 7.1 | ||

| 9:00 | EUR | Eurozone Services Confidence May | 14.3 | 14.9 | ||

| 9:00 | EUR | Eurozone Consumer Confidence May F | 0.2 | 0.2 | ||

| 12:00 | EUR | German CPI M/M May P | 0.30% | 0.00% | ||

| 12:00 | EUR | German CPI Y/Y May P | 1.90% | 1.60% | ||

| 12:15 | USD | ADP Employment Change May | 190k | 204k | ||

| 12:30 | CAD | Current Account Balance Q1 | -$18.15b | -$16.35b | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.60% | 0.80% | ||

| 12:30 | CAD | Raw Materials Price Index M/M Apr | 2.10% | |||

| 12:30 | USD | Wholesale Inventories M/M Apr P | 0.50% | 0.30% | ||

| 12:30 | USD | GDP Annualized Q/Q Q1 S | 2.30% | 2.30% | ||

| 12:30 | USD | GDP Price Index Q1 S | 2.00% | 2% | ||

| 12:30 | USD | Advance Goods Trade Balance Apr | -71.2B | -68.3B | ||

| 14:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | ||

| 18:00 | USD | Federal Reserve Beige Book |

Fed fund futures now pricing in only 40% chance of two hikes by September

With the global financial market rout continuing, the markets are fast to pare back pricing of Fed hikes. We've pointed that out in out latest weekly report already. And the situation worsen quickly this week.

Fed fund futures are now pricing in less than 80% chance of a June hike to 1.75-2.00%. And it was 100% just a week ago.

For another hike to 2.00-2.25% in September, fed fund futures are pricing in only 40% chance. And it was over 80% a week ago.

Now, it seems a total of four hikes this year is out of the question. And even a total of three is in doubt.

Now, it seems a total of four hikes this year is out of the question. And even a total of three is in doubt.

SNB Jordan: Situation in the currency markets remains fragile

SNB chairman Thomas Jordan said yesterday that "the development in recent days shows the situation in the currency markets remains fragile."

And, "our monetary policy, with negative interest rates and the readiness to intervene in currency markets when necessary, takes this fragility into account."

Canada PM Trudeau: No Nafta is better than a bad deal

Canadian Prime Minister Justin Trudeau dismissed the threat of auto tariffs of the US as "negotiating tactic" for NAFTA. And emphasized that won't push Canada to accept a bad deal. He added that "quite frankly that's simply not something we're going to do." Trudeau also reiterated that "no Nafta is better than a bad deal" and "we are not going to move ahead just for the sake of moving ahead."

He also talked down the collapse of NAFTA negotiation and said "the interconnectedness between the Canadian and U.S. economies is not going to change any time soon" and "you can't get around geography". And, "we are their (the Americans') number one customer and there is no question that any disruption of that flow of goods, yes, would be terrible for the Canadian economy but would also be pretty terrible for a lot of U.S. jobs."

Canadian Foreign Minister Chrystia Freeland is in Washington meeting with US Trade Representative Robert Lighthizer. She said there were "very productive discussions" but declined to give any details. Asked about the temporary exemption on steel tariffs that's going to expire this week, Freeland said "our government always is very ready and very prepared to respond appropriately to every action. We are always prepared and ready to defend our workers and our industries."

Trump brought up the issue of border wall again yesterday and said Mexico "do absolutely nothing to stop people from going through Mexico, from Honduras and all these other countries ... They do nothing to help us." And he said "in the end, Mexico is going to pay for the wall." Mexican President Enrique Pena Nieto responded in his tweet saying that "President @realDonaldTrump: NO. Mexico will NEVER pay for a wall. Not now, not ever. Sincerely, Mexico."

To recap, there are a few deadlines for NAFTA negotiations to complete. Firstly, the temporary exemption on US steel and aluminum tariffs will expire on June 1 and it's uncertain what will happen. Mexico Presidential election is upcoming on July 1. Timing is running out, or has already run out, for the current Congress to approve the new NAFTA deal within this year. And less pressing, the US has started national security investigation on automobile imports that could lead to new tariffs.

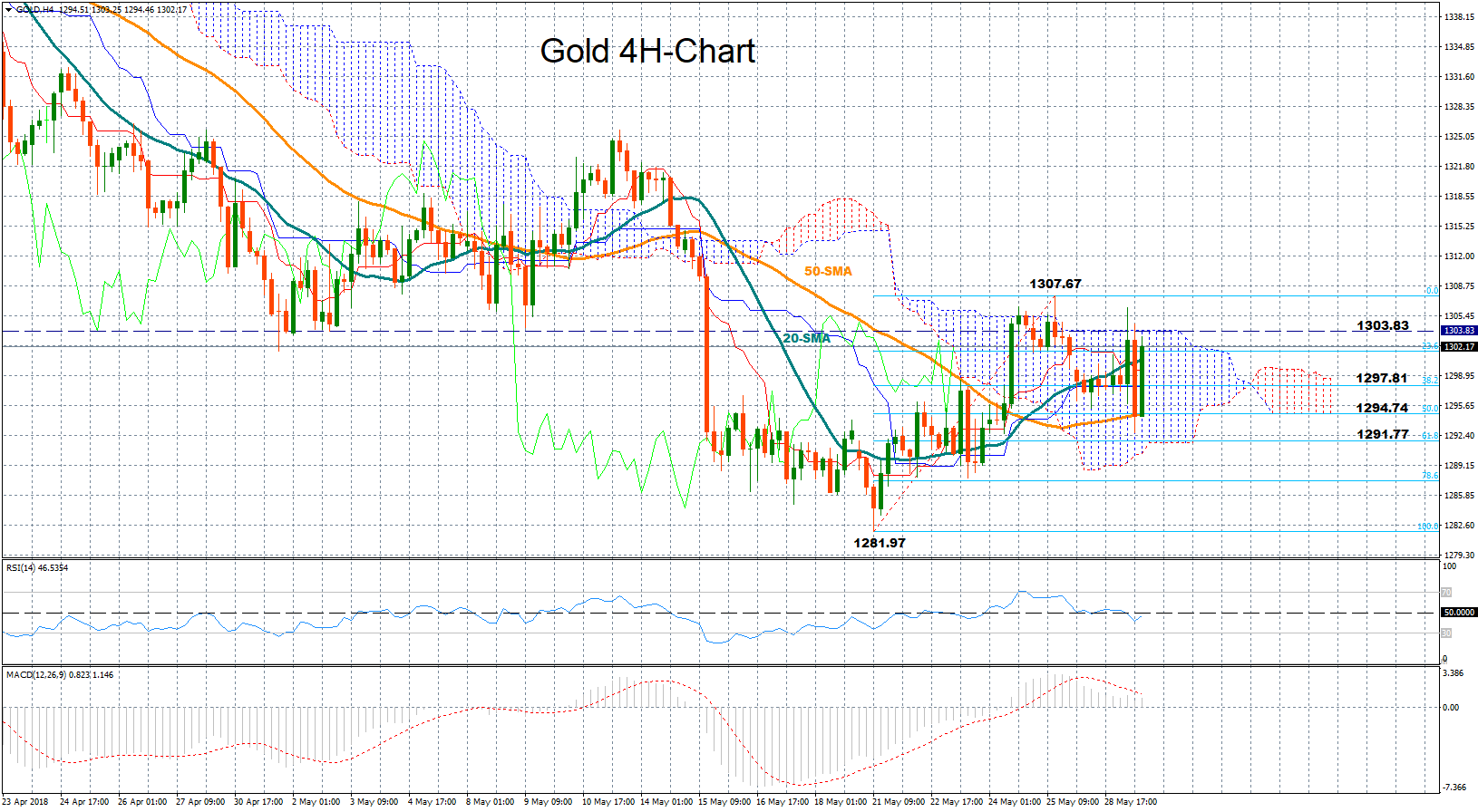

Gold Price Facing Crucial Resistance Ahead Of US GDP

Key Highlights

- Gold price formed a solid support around $1,285 and recovered against the US Dollar.

- There is a major bearish trend line formed with current resistance at $1,306 on the 4-hours chart of XAU/USD.

- The US S&P/Case-Shiller Home Price Indices rose 6.8% in March 2018 (YoY), more than the forecast of +6.4%.

- Today, the US GDP for Q1 2018 (Prelim) will be released, which is forecasted to grow by 2.3%.

Gold Price Technical Analysis

After a major decline, gold price found support above the $1,280-1,281 zone against the US Dollar. The price formed a support base and started an upside move above the $1.290 level.

There was a decent upside move and the price moved above the 23.6% Fib retracement level of the last decline from the $1,325 high to $1,282 low. There was also a break above the $1,300 level, but the price struggled to break the $1,308 resistance and the 100 simple moving average (red, 4-hour).

There is also a major bearish trend line formed with resistance at $1,306 on the 4-hours chart of XAU/USD. Moreover, the 50% Fib retracement level of the last decline from the $1,325 high to $1,282 low is near $1,305.

Therefore, it seems like there is a strong offer zone near the $1,305 and $1,310 levels. As long as the price is below these levels, it could decline back towards $1,285 in the near term.

On the flip side, a successful break above $1,310 and the 100 SMA could open the doors for a move towards $1,325.

Economic Releases to Watch Today

- German Consumer Price Index for May 2018 (Prelim) (YoY) – Forecast +2.0%, versus +1.6% previous.

- German Consumer Price Index for May 2018 (Prelim) (MoM) – Forecast +0.3%, versus 0% previous.

- German Retail Sales for April 2018 (MoM) – Forecast +0.6%, versus -0.6% previous.

- German Retail Sales for April 2018 (YoY) – Forecast 1.2%, versus 1.3% previous.

- Euro Zone Consumer Confidence May 2018 – Forecast 0.2, versus 0.2 previous.

- Euro Zone Services Sentiment May 2018 – Forecast 14.5, versus 14.9 previous.

- US Gross Domestic Product Q1 2018 (Preliminary) – Forecast 2.3% versus previous 2.3%.

- US Personal Consumption Expenditures Prices for Q1 2018 (QoQ) (Prelim) – Forecast +2.7%, versus +2.7% previous.

- BoC Interest Rate Decision – Forecast 1.25%, versus 1.25% previous.

Safety Is The Priority

Seldom do we suddenly fall on demise but rather, advance towards it by slight degrees. However, nothing could be further from the truth when it comes to the Euro's disintegration over the course of the last 24 hours. Forget about juxtaposition with Greece as this potential crisis is monumental in comparison. Italy's economy is ten times the size of Greece, not to mention is burdened with fourth most massive public debt in the world. And given an imminent Italian election may very well amount to a referendum on the Euro, there is a flight to safety from European assets beyond the Italian borders sending and Italian Tsunami warning across global markets. European capital markets are in chaos as it may end up being more than just Rome that is burning.

US equity market losses mounted throughout the day as the latest in a line of top billing European political melodramas greeted traders returning from a three-day weekend. Indeed, not a pretty picture as uncertainly breeds investor anxiety as default fears have the blue-chip Financials buckling, as a crisis of confidence takes hold of financial markets.

And with contagion spreading to international markets, investors are exiting the EURO en masse. In addition to loading up on US Treasuries; investors are seeking shelter under the US dollar and Yen umbrella awaiting the dust to settle in Europe.

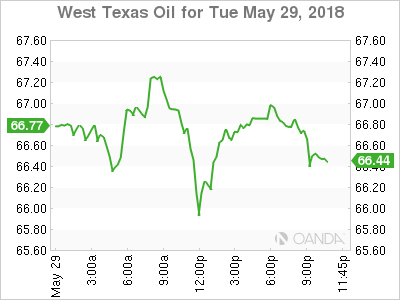

Oil Markets

OPEC supply rebalancing continues to be the primary focus and will continue to be in the lead up to next month's OPEC meeting in Vienna. But finding consensus among the cartel might not be as straightforward as it seems as there appears to be a bit of a trade-off (the US pull out of Iran Nuclear Deal) in the works between Saudi Arabia and the US after President Trump blamed OPEC price manipulation for high US gasoline prices last week.

But also weighing on oil prices to a degree is the political drama in Europe which is hitting the markets at a time when many were already questioning the global growth storyline. So, chalk up another towering hurdle for global growth to overcome.

And while the technical overlays look incredibly bearish below $ 65 per barrel WTI, the market is not naive enough to realise that if there is a collapse in oil prices both Saudi Arabia nor Russia would be less inclined to add supply, given both nations vested interest in higher oil prices.

Finally, while Middle East risk premiums have temporarily deflated, they have not evaporated as Iran remains a very unpredictable wild card in any nuclear deal discussion which should underpin longer-term views on oil prices.

Gold Markets

Conflicting signals abound with Italy contagion fears causing an uproar in the global capital market but offset by the enormous haven demand for US dollar which is creating headwinds for gold prices.

While rising political uncertainty in Italy and growing U.S.-China trade tensions should see gold holding a bid, but with the yellow metals sensitivity to the US dollar is on full display, its unlikely Gold will move significantly higher until we reach the EU ” Crisis Zone” which we are nowhere near at this stage.

Asia Markets

Italian political unrest remains in focus and has risk assets quivering which usually translates into regional losses. Indo, Thai, Malaysia, sing all return to action today after celebrating Vesak day so we should expect some catchup on the downside on the cash market. And while e certainly can't overlook USTR final decision on Section 301 tariffs looming. but the Italian story will most likely be the overriding focus for the day

CNH continues to move higher as the PBoc is putting up few protests and allowing the Yuan to freely adjust to the surging DXY, which should be a significant driver in local FX sentiment. Chinese authorities are showing little concerns t as CNH Spot sliced through the 6.40 barriers like a hot knife through butter. But realistically the Yuan has been sagging since this month weaker than expected retail sales data; it's the unexpected meltdown on the Euro that has marched us above the 6.42 level overnight.

MYR: The Malaysian Ringgit will continue to be in the no-trade zone for foreign investors who were showing little appetite for Malaysia bond and equities prior the Italian meltdown and are even more unlikely to do so with the risk aversion gripping market. And one look at the technical overlay on oil prices should reinforce that view.

Currencies

EUR: EURUSD continues to buckle on haven USD flows given the heightened Italian political risk., While near-term growth dynamics based on the recent run of weak economic data in the EU are also providing tailwinds for the USD. But if this crisis continues, it will bring in to question even the ECB desire to reduce QE.

JPY: Risk aversion coupled The Nikkei dynamics looking fragile continues to weigh on USDJPY sentiment. The question is, are we just seeing the tip of the iceberg which makes the current move all that more dangerous to fade despite history telling us the market has a way of influencing European voter sentiment. I fear that Italian voters are wearing far too many emotions on their sleeve suggesting safety is the priority.

US Private Jobs And Bank Of Canada On The Agenda

The US dollar is mixed as risk aversion has made traditional safe haven currencies (JPY and CHF) advance versus the greenback. The USD is higher against the EUR as the Spanish PM faces a confidence vote with the single currency still reeling from the Italian political crisis that in a worst case scenario could mean the exit of Italy from the European Union. Global stock markets have fallen as fears of contagion rise. The China and US trade stand off continues with the White House set to announce the list of items that are subject to new tariffs in June 15. The Bank of Canada (BoC) will release its rate statement on Wednesday, May 30 at 10:00 am EDT.

- ADP report forecasted to add 186,000 jobs

- US GDP second release for Q1 to remain unchanged at 2.3%

- BoC expected to leave interest rate unchanged at 1.25%

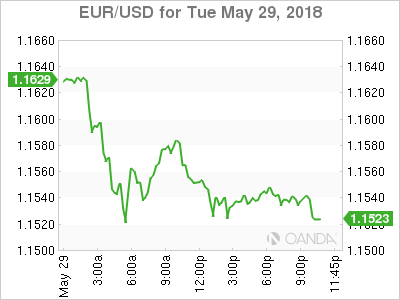

EUR Falls After Political Drama

The EUR/USD lost 0.77 percent on Tuesday. The single pair is trading at 1.1549 after the one-two punch of Spain and Italy. European politics were top of mind as euro sceptic parties rose in relevance across the board. The two largest economies faced their own battle but France and Germany avoided and end of the union scenario earlier. Italy as the third biggest economy is facing economic hardship and in certain aspects not fully recovered from the 2008 crisis. The coalition between the 5-star movement and the League was the last attempt to form a government, but their proposal got rejected as their spending plans could put the EU membership of Italy in jeopardy. If a new vote is called it would be a proxy exit referendum where Italians decide as early as July if they want to remain in the EU.

Spanish Prime Minister Mariano Rajoy will face a no-confidence vote on Friday and the ouster of his party could end up in new elections within months. The market event calendar will mostly focus in the US employment sector. The strongest pillar of the US economic recovery will not bring any headaches to the dollar. In contrast European data will be scarce with flash inflation data on Wednesday the biggest releases.

The biggest economic release in the market will come on Friday, June 1 with the publication of the U.S. non farm payrolls (NFP) report at 8:30 am EDT. The forecast is calling for a gain of 190,000 jobs after a strong 164,000 gain last month. Hourly wages will be in focus with a gain of 0.3 percent expected. The Fed is not worried about the US economy staying above 2 percent for long but it will be a decisive factor in the number of rate hikes in 2018.

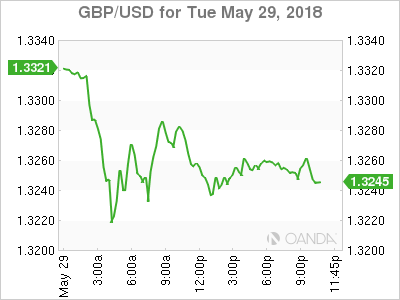

Hard Brexit Outcomes Pressure Pound

The GBP/USD lost 0.49 percent in the last 24 hours. The currency pair is trading at 1.3249 as risk aversion has benefited the USD. The health of the UK economy has taken off the table a short term rate hike from the Bank of England (BoE) and the warming from Governor Carney on a disruptive Brexit. Mr Carney said that if there is a smooth transition the central bank could take a more traditional path, but if there is a disorderly exit the BoE would have to act with a potential rate cut in the cards similar to the post Brexit referendum outcome in 2016.

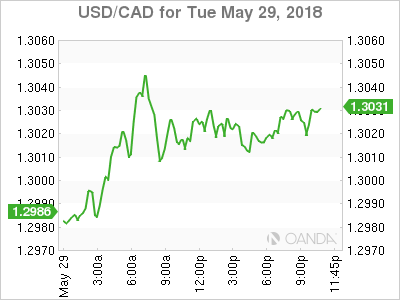

Bank of Canada (BoC) to Hold Citing Uncertainty

The USD/CAD gained 0.23 percent on Tuesday. The currency pair is trading at 1.3019 ahead of the rate statement form the Canadian central bank. The market does not expect a change in the benchmark rate given the surrounding uncertainty about the NAFTA negotiations and less than stellar economic indicators. High levels of household debt will give the BoC food for thought and the bank is not expected to lift rates until after the U.S. Federal Reserve does so again in June.

The price of oil has come off highs after the Organization of the Petroleum Exporting Countries (OPEC) is pondering easing the production cut agreement with other major producers. The deal was able to stabilize prices that were in free fall in 2014. The move worked, but it was only until there was geopolitical friction that prices really had upward momentum. Now with crude at a higher level producers could relax their production quotas and try to reap the benefits of higher prices. The main issue is that demand has not grown enough to justify current levels, and is more of a supply disruptions that have boosted oil prices.

Yen Rises to One Month High on Safe Haven Flows

The USD/JPY lost 1.00 percent in the last 24 hours. The currency pair is trading at 108.32 with a surging yen touching a 30 day high. Safe haven buying of the JPY as trade concerns between the US and China escalate, as well as the political turmoil in continental Europe have put the currency

Market events to watch this week:

Tuesday, May 29

8:00pm JPY BOJ Gov Kuroda Speaks

Wednesday, May 30

8:15am USD ADP Non-Farm Employment Change

8:30am USD Prelim GDP q/q

10:00am CAD BOC Rate Statement

10:45am CHF SNB Chairman Jordan Speaks

9:00pm NZD ANZ Business Confidence

9:30pm AUD Private Capital Expenditure q/q

Thursday, May 31

All Day G7 Meetings

8:30am CAD GDP m/m

11:00am USD Crude Oil Inventories

Friday, June 1

4:30am GBP Manufacturing PMI

All Day G7 Meetings

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate

10:00am USD ISM Manufacturing PMI

Eco Data 5/30/18

[php_everywhere instance="1"]

Gold Back above 1300 But Lacks Direction

Gold managed to bounce back above the 1300 key-level on Tuesday, though, the market continues to lack direction in the four-hour chart according to momentum indicators; the RSI continues to trend around its neutral threshold of 50, while the MACD is moving below its red signal line but above zero.

In case the price corrects to the upside, resistance could run towards the upper bound of the Ichimoku cloud seen around 1303.83. Then a close above this level could drive the market up to the 10-day high of 1307.657 which if successfully broken could bring the upward trend off May’s low of 1281.97 back into play.

However, if the price declines, the 20-period simple moving average (SMA) currently at 1300.71 could provide nearby support ahead of the 38.2% Fibonacci of 1297.81 of the upleg from 1281.97 to 1307.67. Even lower, the 50% Fibonacci of 1294.74, where the 50-period SMA is currently located, could be a stronger barrier to pierce since the area has been frequently approached as resistance over the past three weeks. A break, though, below the 61.8% Fibonacci of 1291.97, could increase the sell-off in the market even further.

Gold Pushes Above $1300 on Italy Tensions

Gold has posted gains in the Tuesday session, erasing the losses seen on Monday. In the North American session, the spot price for one ounce of gold is $1303.85, up 0.44% on the day. On the release front, CB Consumer Confidence dipped to 128.0, missing the estimate of 128.0 points. On Wednesday, there are two key events – ADP nonfarm payrolls and Preliminary GDP.

The markets are focused on geopolitical events this week. The political turmoil in Italy has unnerved investors and boosted gold prices, but the upward movement has been limited, as the much-anticipated summit between the U.S and North Korean leaders may take place. President Trump and North Korean leader Kim Jong-un are scheduled to meet in Singapore on June 12, but curiously, neither side will confirm whether the meeting is on. Last week, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the White House has since sent a team to Singapore and a senior North Korean official is on his way to Washington to meet with Secretary of State Mike Pompeo. If there is confirmation that the meeting is on, traders can expect risk appetite to jump and gold prices to fall.

The drama in Italy is dominating the headlines this week. The political crisis started on the weekend, when President Sergio Mattarella vetoed a ministerial pick of the two parties which were expected to form a coalition, the League Nord and the Five Star Movement. Mattarella rejected the suggestion of Paolo Savona as economic minister, given that Savona is a firm critic of the euro and supports Italy exiting from the eurozone. The reaction from the two parties was fast and furious, with claims that Mattarella was a puppet of Germany and the EU, and there were even demands for his impeachment. The prime minister-elect, Giuseppe Conte, has given up his mandate to form a government, and Mattarella has invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. This could mean that Italy will hold another election in the fall, unless there are more political twists and turns in this crisis.