Sample Category Title

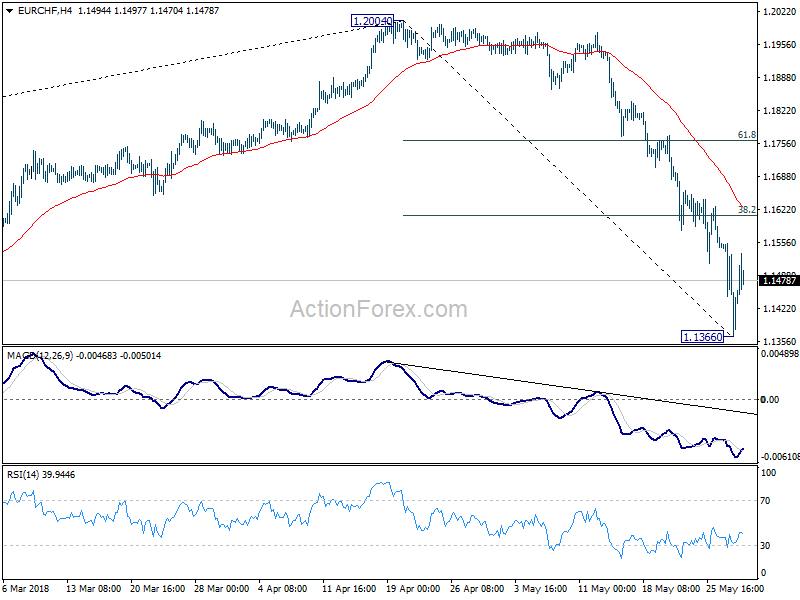

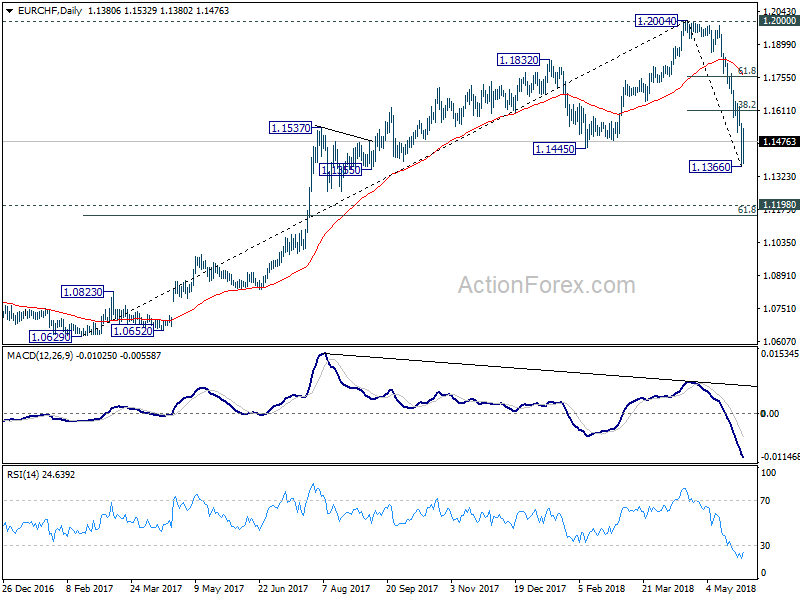

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1352; (P) 1.1454; (R1) 1.1540; More....

EUR/CHF's recovery suggests temporary bottoming at 1.1366 and intraday bias is turned neutral for consolidations. Strong recovery could be seen. but upside should be limited by 38.2% retracement of 1.2004 to 1.1366 at 1.1610 to bring another decline. Below 1.1366 will resume the fall from 1.2004 and target next key support zone between 1.1154 and 1.1198.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. The cross has met 1.1445 already, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern. However, sustained break of 1.1445 will target next key cluster level at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154.

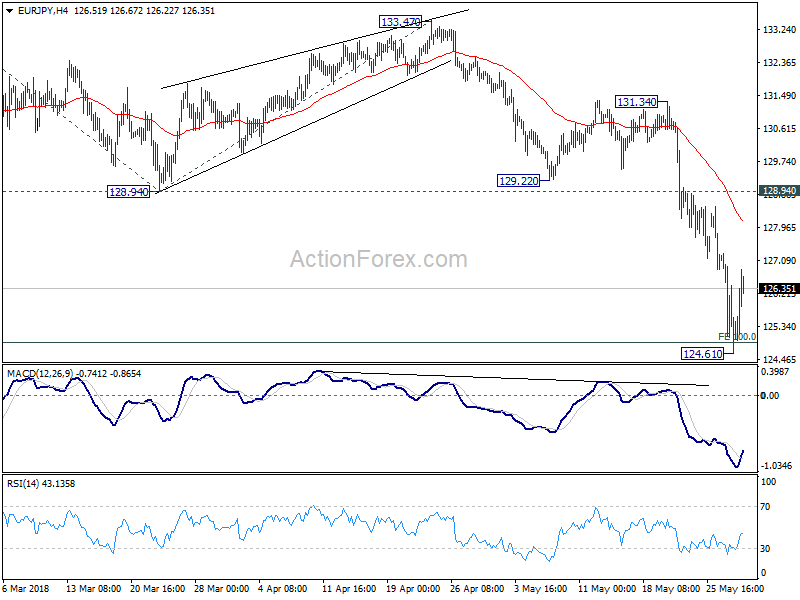

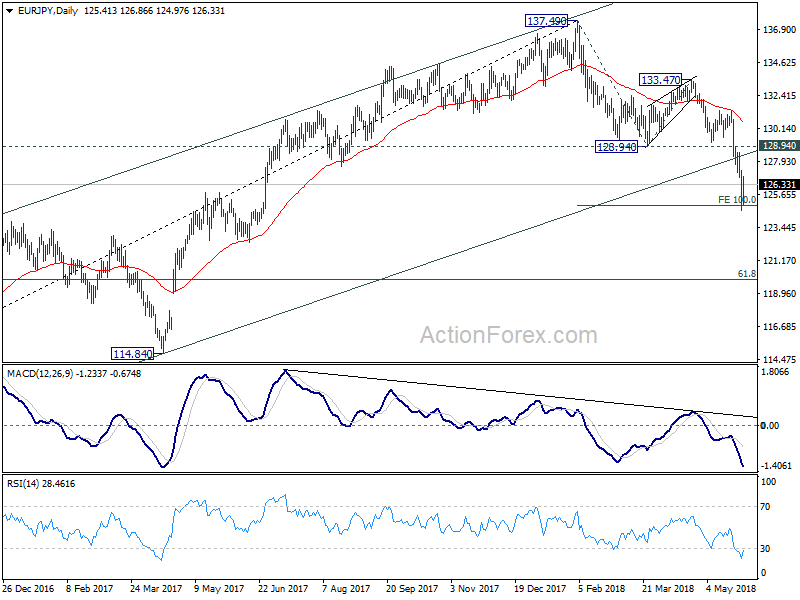

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 124.30; (P) 125.80; (R1) 126.99; More....

EUR/JPY's strong rebound today suggests temporary bottoming at 124.61. That came after meeting 100% projection of 137.49 to 128.94 from 133.47 at 124.92. Intraday bias is turned neutral first and some consolidations could be seen. While further recovery could be seen, near term outlook will remain bearish as long as 128.94 support turned resistance holds. Below 124.71 will resume the fall from 137.49 and target next medium term fibonacci level at 119.90.

In the bigger picture, the case of medium term trend reversal continues to build up. That is rise from 109.03 (2016 low) could have completed at 137.49 already. This is supported by bearish divergence in daily MACD current downside acceleration, as well as the break of 38.2% retracement of 109.03 to 137.49 at 126.61. Deeper decline should be seen to 61.8% retracement at 119.90 and below. This will be the preferred case as long as 128.94 support turned resistance holds.

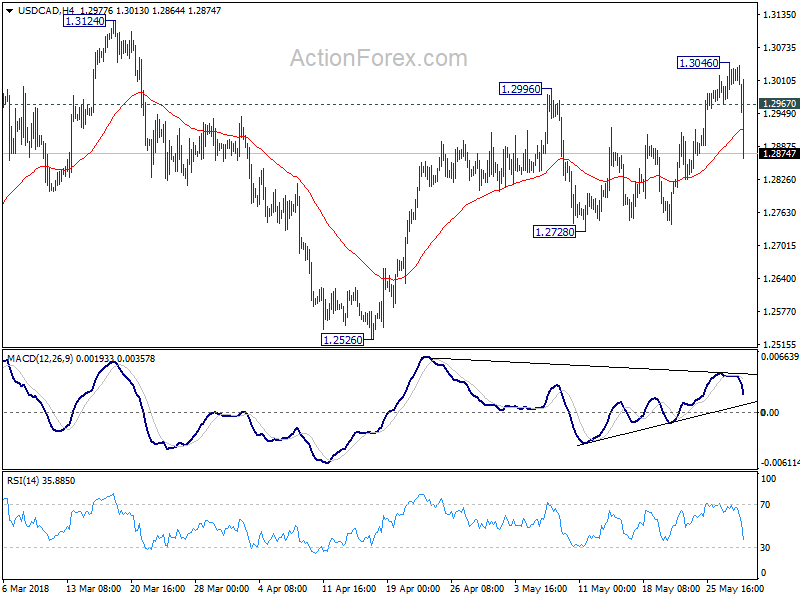

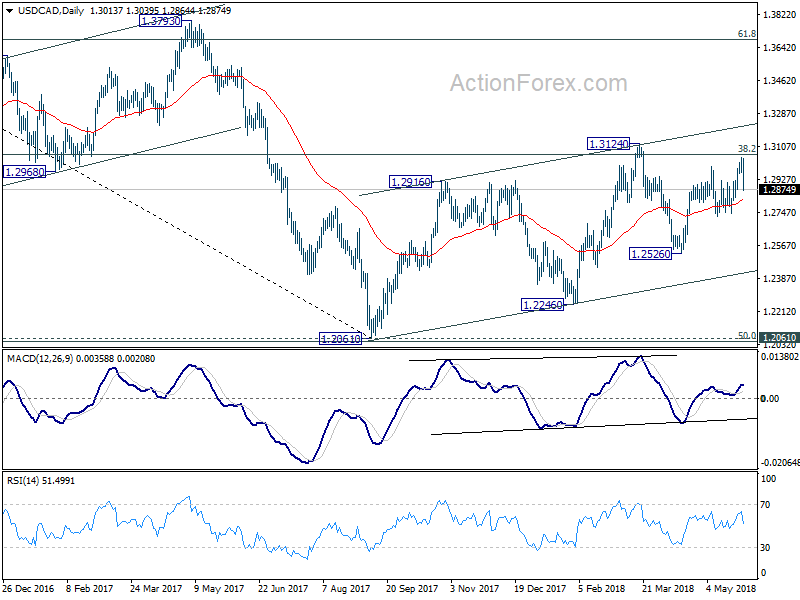

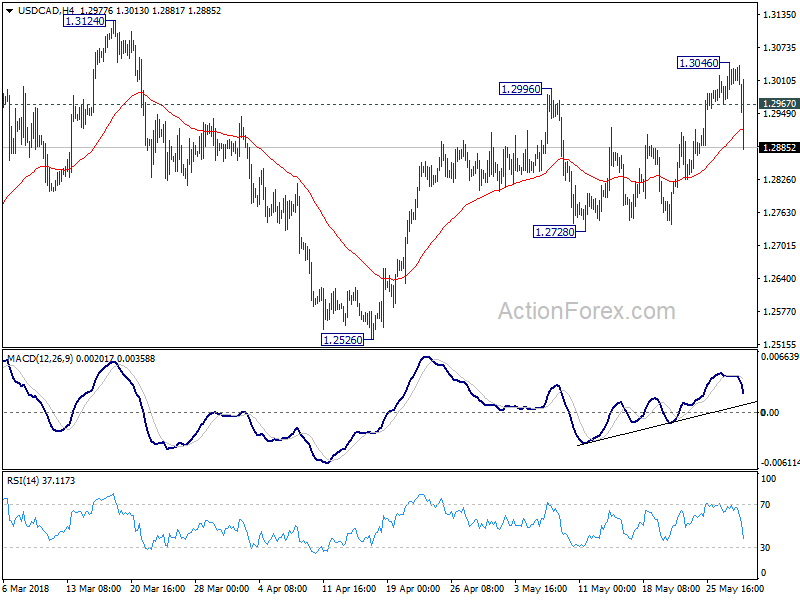

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2977; (P) 1.3013; (R1) 1.3056; More.....

USD/CAD's sharp fall from 1.3046 and strong break of 1.2967 minor support dampened our bullish view. Intraday bias is turned back to the downside for 1.2728 support. Break there will indicate completion of the rebound from 1.2526 at 1.3046. And in that case, deeper fall would be seen back to 1.2526 and below. Nonetheless, strong rebound 1.2728 will put focus back to 1.3046 resistance first.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

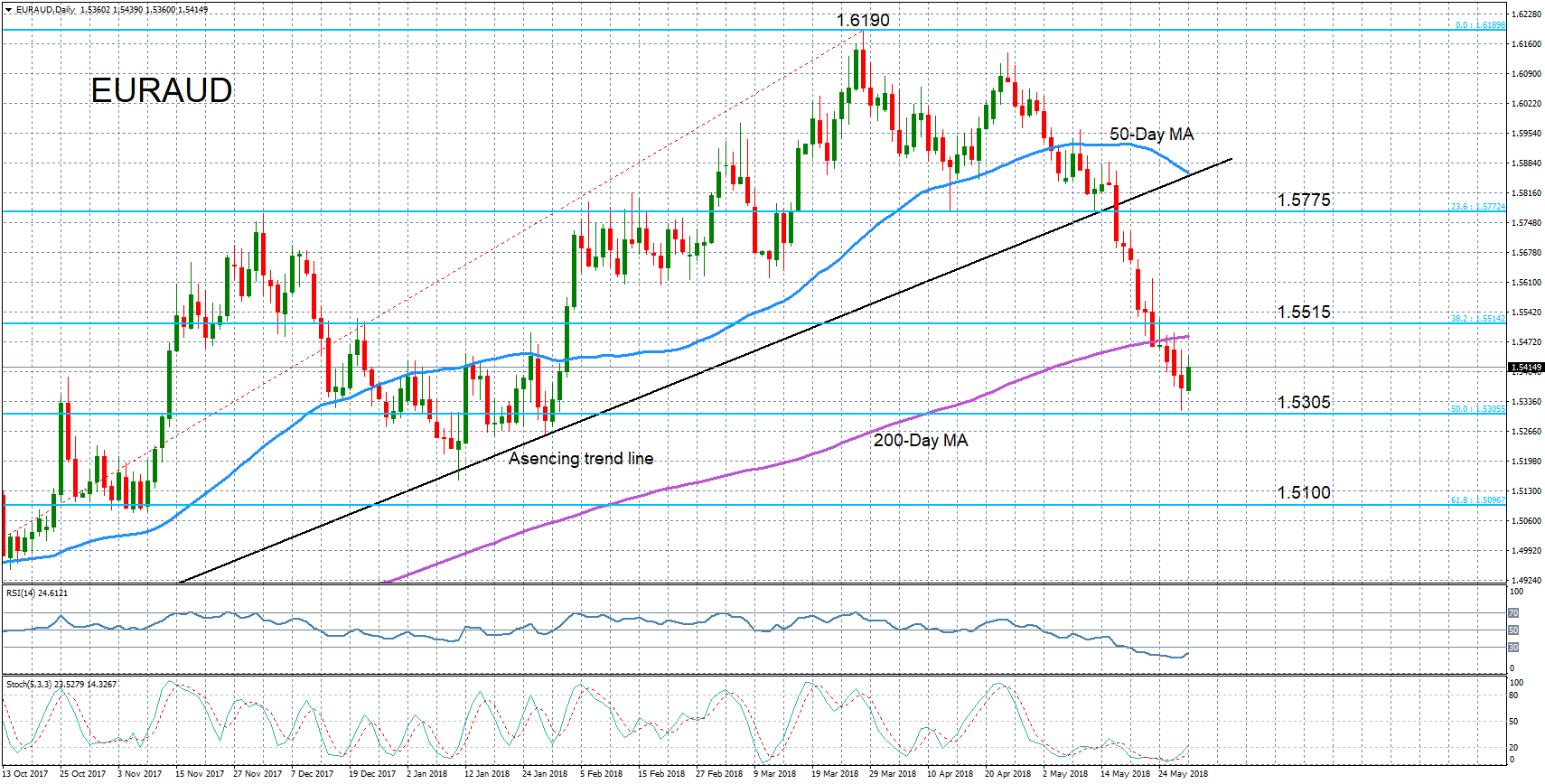

EURAUD Eases from 4-Month Lows; Long-Term Uptrend at Risk

EURAUD fell to a 4-month low of 1.5315 on Tuesday, coming close to touching the 50% Fibonacci retracement of the upleg from 1.4421 to 1.6190 between July 2017 and March 2018. The pair has reversed sharply from the more than two-year high of 1.6190 set on March 28.

However, with momentum indicators having run into oversold territory, an upside correction is currently in progress and prices have jumped higher today. The RSI is pointing up but yet to break out of oversold ground. If it manages to climb above 30 over the next day or two, this would signal a more convincing rebound. The stochastic oscillator is also heading higher, with the %K line just crossing above 20.

If prices maintain the positive momentum, initial resistance could come from the 200-day moving average around 1.5485, followed by the 38.2% Fibonacci at 1.5515. A successful break above the 1.5515 level would strengthen the upside momentum, driving prices towards the 23.6% Fibonacci level at 1.5775. If the pair is able to overcome this hurdle, it could then attempt reclaiming the ascending trend line, which it needs to do in order to keep its longer-term bullish structure intact.

However, if prices were to head lower again, immediate support would come from the 50% Fibonacci at 1.5305. A breach of this level would risk shifting the longer-term outlook to a neutral one, with the next support coming from the 61.8% Fibonacci at the 1.5100 handle.

Sunset Market Commentary

Markets:

Risk sentiment improved today, strengthening our belief that yesterday’s panic selling was a short term exhaustion move. Investors adapted positions to latest Italian political developments and now await new impetus. Lega is steering to new elections, boosted by favorable opinion polls, while 5SM seems to be willing to do a last-ditch effort to form a government. The potential coalition partners seem to be drifting somewhat apart. Strong EMU eco data helped improving risk sentiment together with the short term relief in the BTP markets, supported by a decent (even if it was rather small) BTP auction. National inflation readings beat consensus by a wide margin, suggesting upward risks to tomorrow’s EMU measure (1.6% Y/Y expected from 1.2% Y/Y). EC confidence data, German retail sales and German labour market data surprised on the upside as well. German yields add 7.4 bps (30-yr) to 9.9 bps (5-yr) on a daily basis with the belly of the curve underperforming the wings. US yields increase by 6.1 bps (30-yr) to 8.2 bps (5-yr). 10-yr yield spread changes vs Germany narrow by 30 bps (Greece/Italy) to 16 bps (Portugal/Spain). Semi-core spreads decline by up to 5 bps (France).

Today, global trading entered calmer waters even as visibility on the political situation in Italy remains limited. Investors saw no additional negatives. After yesterday’s ‘exhaustion move’ this triggered a corrective rebound in most assets affected by the Italian risk-off trade, including in the euro. EUR/USD traded in the mid 1.15 area this morning and rebounded about 1 big figure. The EMU eco data, including German inflation (2.2% Y/Y!!!!!) were in theory also euro supportive. US data (ADP, US Q1 growth revision and trade balance) were mixed-to-softer than expected. However, the data had only a secondary impact on global FX trading. The moves in the FX cross rates are mainly a ‘post-Italy’ reaction. EUR/USD trades in the 1.1625 area, a good gain, but off the intraday top. USD/JPY was supported by the rebound in core/US yields. The pair returned close to the 109 area. Question remains whether the situation in Italy has stabilized enough for FX markets to turn their focus again to the economic data (e.g. to the US payrolls on Friday). The jury is still out.

Sterling recently followed the global price moves related to the Italian crisis and this was still the case today. EUR/GBP trended south as the Italian crisis weighed on the euro overall, but the pair didn’t break any technically important levels. Today, EUR/GBP followed the rebound in EUR/USD. The pair trades currently again in the 0.8750 area. Cable rebounded to the 1.33 area. However, the picture in this cross rate remains fragile.

News Headlines:

Germany showered the 19-nation euro area with a flurry of good economic news. Inflation in Europe’s largest economy jumped from 1.4% Y/Y to 2.2% Y/Y in May (vs 1.8% Y/Y consensus), exceeding the rate the ECB aims to achieve for the entire region. Unemployment fell to a record low of 5.2% and economic sentiment improved after three consecutive declines. Retail sales rose by an impressive 2.3% M/M in April, giving a boost to Q2 after a disappointing Q1 GDP. (BB)

The US private sector added fewer jobs than expected this month (178k vs 190k) while the figure from April was revised sharply lower (163k from 204k) as a tight labour market makes it harder for employers to fill positions. (FT)

Italy searched for a last-minute exit from almost three months of political turmoil, with 5SM looking to make a renewed attempt to form a coalition government with the right-wing League. However, League leader Salvini, who is surging in opinion polls, threw cold water on the notion, saying Italy should return to an election as soon as possible. He did, however, appear open to an interim administration to govern for a few months, saying an election at the end of July would be "disruptive" for Italian seasonal workers. (Reuters)

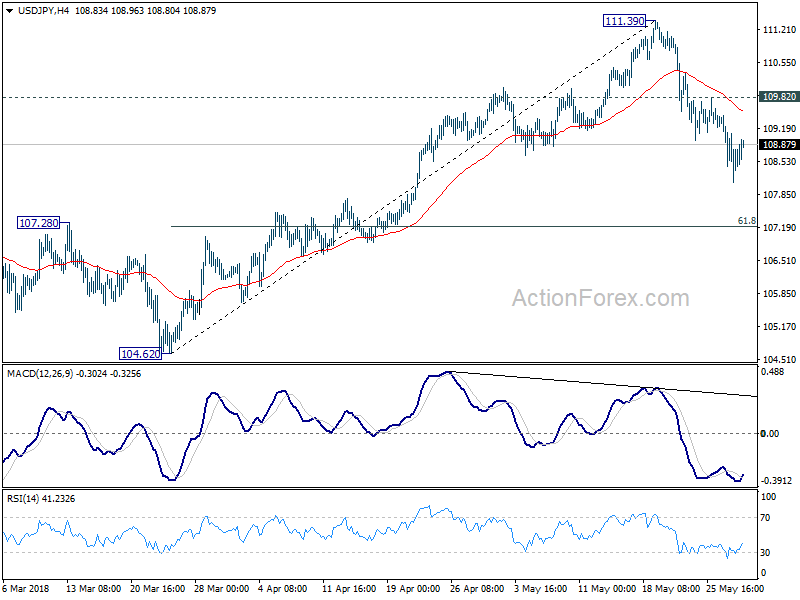

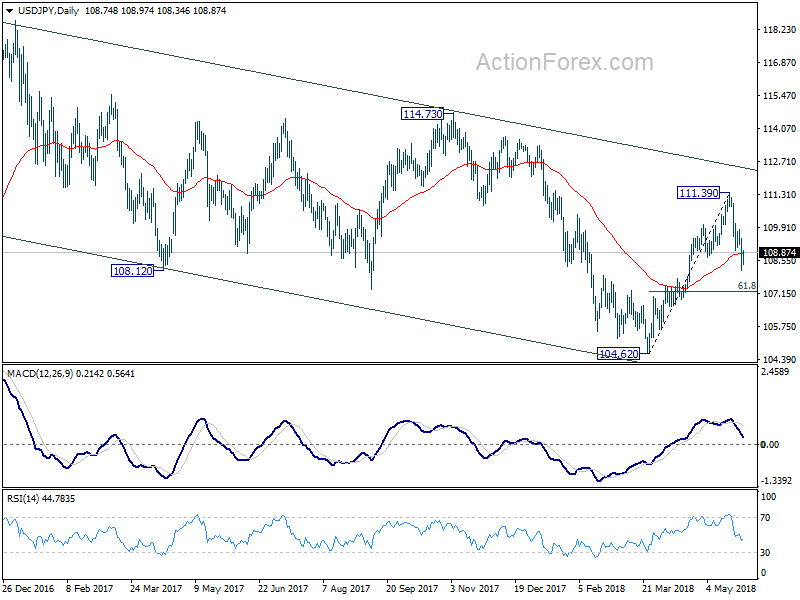

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.10; (P) 108.78; (R1) 109.46; More...

Intraday bias in USD/JPY remains on the downside for the moment. Deeper fall could be seen to 61.8% retracement of 104.62 to 111.39 at 107.20. Break will likely resume larger decline from 118.65 for a new low below 104.62. On the upside, break of 109.82 is needed to confirm completion of the fall from 111.39. Otherwise, near term outlook will be mildly bearish even in case of recovery.

In the bigger picture, USD/JPY remains bounded in medium term falling channel from 118.65 (2016 high). The development. Current deeper than expected fall from 111.39 argues that fall from 118.65 is not finished. Break of 104.62 low would target 98.97 or even below. Though, break of 111.39 will revive the case that fall from 118.65 has completed and turn focus to 114.73 for confirmation.

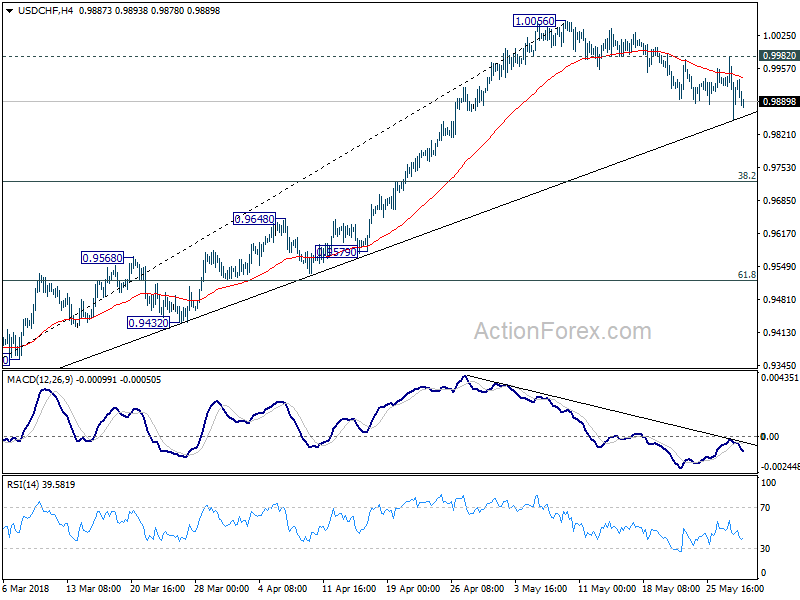

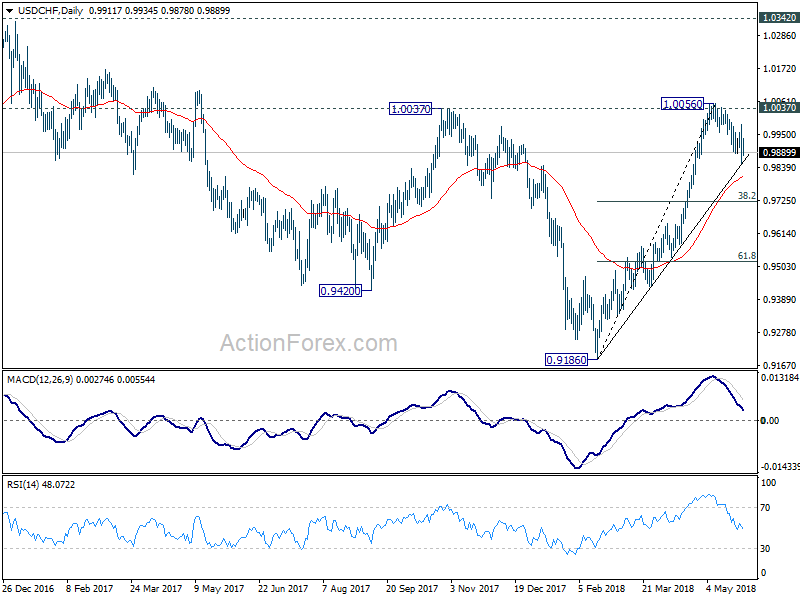

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9850; (P) 0.9916; (R1) 0.9981; More...

Intraday bias in USD/CHF remains neutral at this point. For now, we'd continue to expect strong support from near term trend line (now at 0.9860) to complete the correction from 1.0056 to bring rise resumption. On the upside, above 0.9982 will bring retest of 1.0056 first. However, sustained break of the trend line will argue that it's a larger scale correction and will target 0.9724 fibonacci level.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

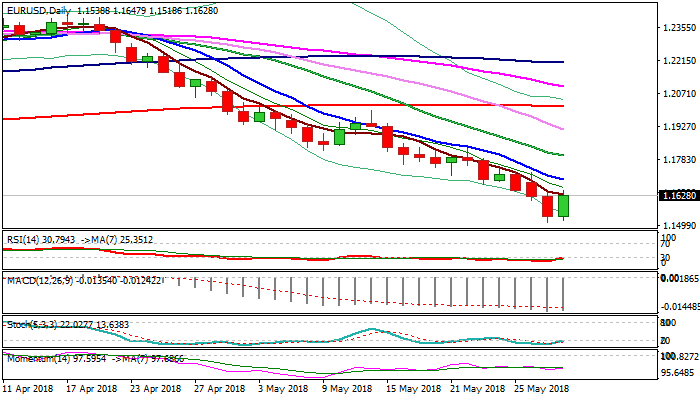

EURUSD Outlook: Extends Recovery on Italian Hopes/Strong EU Data

The Euro extended recovery on hopes that renewed attempts of Italy to form a government and avoid snap elections which could deepen political turmoil. The single currency also benefited from better than expected German inflation data (May m/m 0.5% vs 0.3% f/c) as well as weaker than expected US GDP (Q1 2.2% vs 2.3% f/c). Also, US ADP report which is usually used as an indication for coming US non-farm payrolls report, showed private sector added less than expected jobs in May (178K vs 186K f/c) but previous month's figure was revised lower to 163K (from 204K). Solid European data and weaker than expected US figures, accompanied by easing political tensions in Italy, create positive environment for Euro. Recovery cracked initial barrier at 1.1630 (falling 5SMA) and turned focus towards pivotal 1.1695/97 barriers (Fibo 38.2% of 1.1996/1.1509/falling 10SMA) break of which would generate reversal signal. Broken 1.16 level now acts as initial support while 4-hr 10SMA (1.1577) is expected to keep the downside protected.

Res: 1.1650; 1.1695; 1.1728; 1.1753

Sup: 1.1600; 1.1577; 1.1530; 1.1509

Canadian Dollar surges as hawkish BoC shows much confidence in statement

BoC stands pat and maintains interest rate unchanged at 1.25% as widely expected. The most important part of the statement is that "developments since April further reinforce Governing Council's view that higher interest rates will be warranted to keep inflation near target." This is more hawkish than generally expected and shows that BoC is rather confident to continue with tightening, even though the timing of the next hike is still uncertain.

USD/CAD dives sharply after the release and should be heading back to 1.2728 support.

Here is the full statement:

Bank of Canada maintains overnight rate target at 1¼ per cent

The Bank of Canada today maintained its target for the overnight rate at 1¼ per cent. The Bank Rate is correspondingly 1½ per cent and the deposit rate is 1 per cent.

Global economic activity remains broadly on track with the Bank's April Monetary Policy Report (MPR) forecast. Recent data point to some upside to the outlook for the US economy. At the same time, ongoing uncertainty about trade policies is dampening global business investment and stresses are developing in some emerging market economies. Global oil prices have been higher than assumed in April, in part reflecting geopolitical developments.

Inflation in Canada has been close to the 2 per cent target and will likely be a bit higher in the near term than forecast in April, largely because of recent increases in gasoline prices. Core measures of inflation remain near 2 per cent, consistent with an economy operating close to potential. As usual, the Bank will look through the transitory impact of fluctuations in gasoline prices.

In Canada, economic data since the April MPR have, on balance, supported the Bank's outlook for growth around 2 per cent in the first half of 2018. Activity in the first quarter appears to have been a little stronger than projected. Exports of goods were more robust than forecast, and data on imports of machinery and equipment suggest continued recovery in investment. Housing resale activity has remained soft into the second quarter, as the housing market continues to adjust to new mortgage guidelines and higher borrowing rates. Going forward, solid labour income growth supports the expectation that housing activity will pick up and consumption will continue to contribute importantly to growth in 2018.

Overall, developments since April further reinforce Governing Council's view that higher interest rates will be warranted to keep inflation near target. Governing Council will take a gradual approach to policy adjustments, guided by incoming data. In particular, the Bank will continue to assess the economy's sensitivity to interest rate movements and the evolution of economic capacity.

Information note

The next scheduled date for announcing the overnight rate target is July 11, 2018. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

(BOC) Bank of Canada Maintains Overnight Rate Target at 1¼ Per cent

The Bank of Canada today maintained its target for the overnight rate at 1¼ per cent. The Bank Rate is correspondingly 1½ per cent and the deposit rate is 1 per cent.

Global economic activity remains broadly on track with the Bank's April Monetary Policy Report (MPR) forecast. Recent data point to some upside to the outlook for the US economy. At the same time, ongoing uncertainty about trade policies is dampening global business investment and stresses are developing in some emerging market economies. Global oil prices have been higher than assumed in April, in part reflecting geopolitical developments.

Inflation in Canada has been close to the 2 per cent target and will likely be a bit higher in the near term than forecast in April, largely because of recent increases in gasoline prices. Core measures of inflation remain near 2 per cent, consistent with an economy operating close to potential. As usual, the Bank will look through the transitory impact of fluctuations in gasoline prices.

In Canada, economic data since the April MPR have, on balance, supported the Bank's outlook for growth around 2 per cent in the first half of 2018. Activity in the first quarter appears to have been a little stronger than projected. Exports of goods were more robust than forecast, and data on imports of machinery and equipment suggest continued recovery in investment. Housing resale activity has remained soft into the second quarter, as the housing market continues to adjust to new mortgage guidelines and higher borrowing rates. Going forward, solid labour income growth supports the expectation that housing activity will pick up and consumption will continue to contribute importantly to growth in 2018.

Overall, developments since April further reinforce Governing Council's view that higher interest rates will be warranted to keep inflation near target. Governing Council will take a gradual approach to policy adjustments, guided by incoming data. In particular, the Bank will continue to assess the economy's sensitivity to interest rate movements and the evolution of economic capacity.

Information note

The next scheduled date for announcing the overnight rate target is July 11, 2018. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.