Sample Category Title

5 Star to find someone other than Savona as economy minister

The anti-establishment 5-Star Movement in Italy in is working hard on forming a government to solve the current political turmoil. It's leader Luigi Di Maio met with President Sergio Mattarella today. After that, Di Maio said "let's find someone of the same caliber as Savona, who would still remain in the government in another ministry." And "If the League agrees ... we can still form a government."

Di Maio is now trying to find that "point of compromise" between Mattaralla and eurosceptic League. No name is thrown out yet and it could take some time to negotiate with League. Note that League leade rMatteo Salvini is pushing for another election as the effort to form a coalition government collapsed.

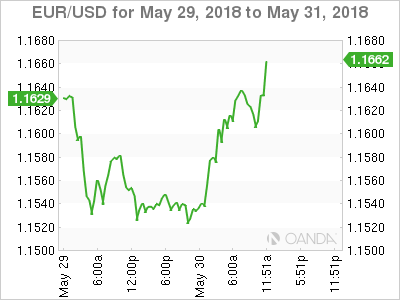

But after all, the development s calmed the markets mildly as Euro also recovered.

British Pound Steady, U.S GDP Meets Expectations

The British pound has posted gains in Wednesday trade, erasing the losses seen on Tuesday. In the North American session, GBP/USD is trading at 1.3287, up 0.26% on the day. On the release front, U.S numbers were mixed. U.S Preliminary GDP came in at 2.2%, just shy of 2.3%. However, ADP nonfarm payrolls dropped sharply to 178 thousand, well off the estimate of 191 thousand. Later in the day, the U.K releases GfK Consumer Confidence, which is expected to come in at -8 points, indicating weak consumer confidence.

After a sluggish first quarter and with the dark cloud of Brexit creeping ever closer, the health of the British economy is raising alarm bells. Economic growth in the first quarter was weaker than expected, and the unseasonably snowy weather in March cannot explain away the economic slowdown. Inflation has dropped to 2.4%, and the Office for National Statistics had a bleak message about the economy, noting that GDP expanded a negligible 0.1% in the first quarter. At its May meeting, the Bank of England reduced its forecast for growth in 2018 to 1.4%, down from the 1.8% forecast in February. With the May government still mired in trying to sort out the endlessly complex divorce with the European Union, the British pound could continue to face headwinds in the second quarter. A rate hike would boost the currency, but the BoE may be reluctant to make a move – the bank had to backtrack from an expected rate increase earlier in May, and there is growing speculation that we will see a repeat (lack of) performance at the BoE’s August meeting, with the odds of an August rate hike at less than 50 percent.

The markets continue to keep a close eye on the “on-again off-again” summit between the U.S and North Korean leaders. President Trump and North Korean leader Kim Jong-un are scheduled to meet in Singapore on June 12, but curiously, neither side will confirm whether the meeting is on. The White House has strongly hinted that the summit will take place, saying that the U.S continues to “actively prepare for President Trump’s expected summit with leader Kim in Singapore.” There is a flurry of activity around the summit – Trump has sent a team to Singapore and a senior North Korean official will meet with senior U.S officials on Wednesday. If Trump tweets out that the summit is on, we could see some positive movement from the US dollar.

Is the European Debt Crisis Rearing Its Ugly Head Again?

Executive Summary

After three years of relative calm, volatility has returned to sovereign bond markets in the euro area due to political uncertainty in Italy and, to a lesser extent, Spain. The Italian government has been able to stabilize its debt-to-GDP ratio in recent years due to sizeable fiscal surpluses, but it is uncertain whether that austerity will continue. Renewed fiscal largesse could lead to a vicious circle of increasing fiscal deficits, higher borrowing costs, slowing economic growth, even larger deficits, etc. The probability of such a vicious circle developing seems to be lower in Spain than in Italy. In our view, it is too early to make confident predictions about how the situation in Italy will ultimately evolve. Much will depend on political decisions that are made in coming months, not only in Italy but in other European countries as well. Readers should be prepared for more volatility in coming months as domestic and foreign actors in the Italian saga make their decisions.

European Bond Markets in Turmoil Again Due to Political Uncertainty

Sovereign debt markets in the euro area, which have been more or less stable since the last Greek government debt crisis in 2015, have encountered turbulence again in the past week or so. The catalyst this time has been political uncertainty in Italy and, to a lesser extent, Spain. The yield on the 10-year government bond in Italy has jumped by more than 100 bps over the past two weeks, while the yield on the comparable bond in Spain is up about 25 bps or so over that period (Figure 1). The euro has also weakened over the U.S. dollar (Figure 2).

In Italy, political uncertainty has been building since the inconclusive general election on March 4 in which no party won enough seats in the Italian parliament to govern solely. But on May 18, the Five Star Movement (5SM), a populist party that tends to have some left-wing views, and the Lega Nord (LN), another populist party that is on the right of the political spectrum, announced that they had reached agreement to form a coalition government. The parties chose Giuseppe Conte, a law professor with little political experience, as their nominee for prime minister, and they named Paolo Savona, an 81-year old economist who previously has called for Italy to exit the Eurozone, as finance minister. This combination proved to be too much for President Mattarella to stomach. He refused to approve the proposed government, which he is constitutionally permitted to do, and it quickly fell apart. It is apparently the intention of President Mattarella to now name a caretaker government, and Italians likely will head back to the polls this autumn for another election.

In Spain, the government of Prime Minister Rajoy, who has governed Spain since 2011, faces a possible no-confidence vote in the Spanish parliament due to corruption allegations. If the government loses the confidence vote, then voters in Spain likely would be heading to the polls as well.

How Much Fiscal Flexibility Does Italy Have?

Although bond yields in Italy and Spain at present are nowhere near the highs that they reached during the first sovereign debt crisis in 2011-2012, it may be a useful exercise to consider how debt dynamics in each country may be affected if borrowing costs remain at current levels or even climb higher. Let's start with Italy first. As we have written in previous reports, a country's debt-to-GDP ratio is affected by its primary budget balance, nominal GDP growth rate and borrowing costs. There obviously are infinite combinations of these three variables, but we focus on four potential scenarios for the Italian debt-to-GDP ratio in Figure 3. For each scenario we use IMF forecasts for nominal GDP growth and the primary budget balance (Table 1), and then consider four different potential borrowing costs.

The debt-to-GDP ratio of the Italian government at the end of 2017 was roughly 134 percent. Before bond yields started their rapid ascent a few weeks ago, the Italian government was issuing longerdated bonds with coupons of approximately 2 percent. If volatility subsides and the Italian government can issue bonds with coupons of roughly 2 percent, then the debt-to-GDP ratio would recede markedly between now and 2030 as long as nominal GDP growth and the primary budget surplus evolve in line with the IMF forecasts. Even if coupons on newly issued Italian government bonds should rise to 5 percent, where they were at the height of the 2011-2012 European sovereign debt crisis, Italy should be able to stabilize its debt-to-GDP ratio.

But this sanguine outcome depends on two optimistic assumptions. First, Italy can maintain a nominal GDP growth rate in excess of 2 percent per annum. Nominal GDP in Italy grew 2.1 percent in 2017, but this solid performance has been rare in recent years. Specifically, nominal GDP in Italy has grown at an annual average growth rate of only 1.1 percent since the end of the global financial crisis in 2010. The second optimistic assumption is that the primary budget surplus will rise from roughly 2 percent this year to 3.6 percent in 2022. Although the Italian government has generally incurred black ink in its primary budget balance since the early 1990s, a budget surplus of this magnitude implies that fiscal policy is quite austere. This latest bout of financial market volatility started when the two potential coalition partners announced that they would aim to enact a flat tax as well as a guaranteed minimum income, stoking concerns that the budget balance would deteriorate sharply. Therefore, it seems that some sensitivity analysis around these favorable debt projections is in order.

Table 2 shows combinations of nominal GDP growth and borrowing costs that would be needed to stabilize Italy's debt-to-GDP ratio at 134 percent for given primary budget balances. For example, if the Italian government wants to run a primary deficit equal to 2.6 percent of GDP (the upper left cell in Table 2), then nominal GDP growth would need to equal 4 percent per annum and borrowing costs would need to be only 2 percent for the debt-to-GDP ratio to remain stable. In our view, it is not likely that Italy would be able to realize this favorable combination of nominal GDP growth rate and borrowing cost anytime soon.

Given its lackluster GDP growth rate, Italy does not appear to have much space to ease fiscal policy significantly. Last year, the government ran a fiscal surplus equivalent to 1.7 percent of GDP. If it wants to ease fiscal policy relative to last year (indicated by the light green boxes in Table 2), then the economy would need to grow markedly faster and/or borrowing costs would need to remain quite low. A move toward significant fiscal easing could lead to a vicious circle of rising bond yields, slower growth, even higher deficits, etc. Indeed, the political uncertainty that now exists in Italy may have jumpstarted such a vicious circle.

Spain: Debt Is Sustainable as Long as the Economy Continues to Grow

As noted above, government bond yields in Spain have risen recently, although not to the same extent as in Italy. Looking forward, the IMF projects that nominal GDP growth in Spain will downshift somewhat over the next few years and that the primary budget balance will swing from a modest deficit of 0.8 percent of GDP in 2017 to small surpluses in coming years (Table 3). Under these assumptions, coupons on newly issued Spanish government bonds could rise to 4 percent - the average coupon on outstanding government bonds is roughly 3 percent at present - without leading to a marked rise in the government's debt-to-GDP ratio (Figure 4).

The Spanish economy has grown roughly 4 percent per annum in nominal terms since 2015 due, at least in part, to labor market reforms that have helped Spain restore price competitiveness vis-àvis other countries. As long as the country can maintain a reasonably solid nominal GDP growth rate, the government should be able to able to stabilize, if not reduce, its debt-to-GDP ratio without an undue amount of fiscal tightening (Table 4). In our view, there is a lower probability of a vicious circle developing in Spain than in Italy.

Is It 'Different' This Time?

Yields on Italian, Portuguese and Spanish government bonds moved significantly higher during the first European sovereign debt crisis in 2011-2012 because there were no financial backstops in place at that time to shore up countries in need of financial assistance. But the European Stability Mechanism (ESM), a €500 billion fund that can be tapped to assist ailing countries, is now capitalized and operational. Furthermore, the European Central Bank has credibly done "whatever it takes to preserve the euro."2 The combined firepower of the ESM and the ECB makes a collapse of the Eurozone less likely today than it was in 2011-2012. But, Italy is among the 10 largest economies in the world, and its government debt outstanding totals €2.3 trillion. A financial fire in Italy, should one start, may be difficult to extinguish.

Conclusion

Sovereign bond markets in Europe generally have been quiet since the last Greek debt crisis in the summer of 2015. However, volatility has returned to "peripheral" bond markets (Italy, Spain, Portugal and Greece) in recent days due to political uncertainty in Italy and, to a lesser extent, Spain. Although volatility could conceivably subside somewhat in coming days, a decline in yields to the levels that existed a few weeks ago in these markets does not seem likely in the near term. Italians probably will be heading back to the polls this autumn, and political uncertainty in Italy likely will remain elevated until the next general election and perhaps beyond. Elevated levels of political uncertainty could spread to Spain, too, if Prime Minister Rajoy does not survive a confidence vote.

Italy has been able to stabilize its government debt-to-GDP ratio over the past few years due to sizeable surpluses in its primary budget balance. However, it will be difficult for the Italian government to bring about a meaningful reduction in its debt-to-GDP ratio in the absence of continued fiscal austerity due to the country's inherently weak economic growth rate. But, it was frustration with the malaise in the economy, which is due in part to chronic austerity that led Italians in the March 4 elections to vote for populist parties that reject austerity.

In our view, it is too early to make confident predictions about how the situation in Italy will ultimately evolve. Much will depend on political decisions that are made in coming months. President Mattarella will probably ask Italian citizens to make political decisions by returning to the polls in a few months for a new round of elections. The outcome of those elections will eventually produce a government that will make its own decisions regarding fiscal policy, and those decisions could help to stabilize the situation or lead to further financial instability. And decisions that are made by political leaders in other European countries and by authorities at the ESM and the ECB will also play a role in the ultimate outcome of the current situation in Italy. To repeat, it is too early to make confident predictions about how the situation in Italy will ultimately evolve, but readers should be prepared for more volatility in the coming months as the actors in the Italian saga make their decisions.

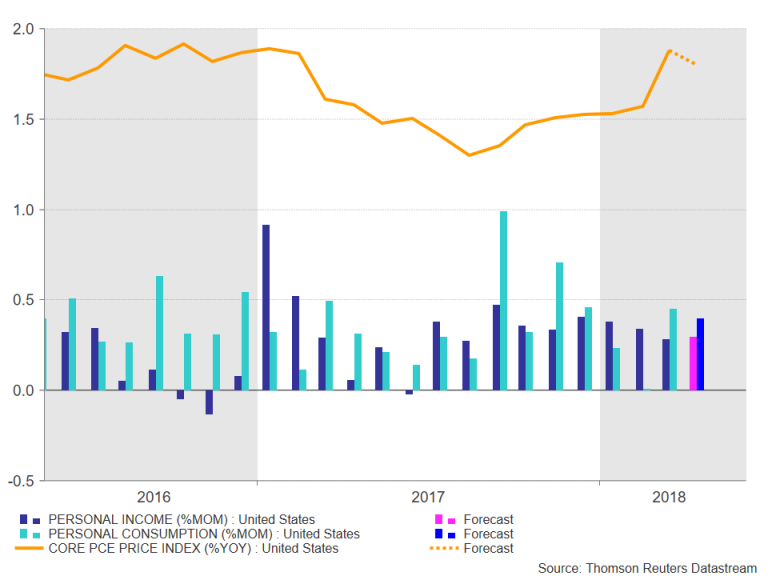

US PCE Inflation Expected to Ease, Underscoring Fed’s Gradual Approach

The US Bureau of Economic Analysis will publish its latest monthly release on personal income and outlays on Thursday at 12:30 GMT. The report will contain closely watched data on personal income and consumption, as well as the PCE measure of inflation. With market fears of a major inflation overshoot having abated recently, Thursday’s figures will likely confirm the continuation of the goldilocks economy, with US personal incomes and spending rising solidly, but price pressures remaining moderate.

Personal income is expected to rise by 0.3% month-on-month in April, the same pace as in March and maintaining positive growth for the 10th straight month. Personal consumption is forecast to grow by 0.4% m/m, also the same rate as in the prior period. If the numbers come in line with expectations, it would point to a descent start to the second quarter. Consumption comprises about 70% of the US economy and given that the personal income and spending data are components of GDP calculations, they are considered to be a strong indicator to GDP growth.

The US economy expanded by an annualized rate of 2.2% in the first quarter of 2018, down from the prior quarter’s 2.9% rate but still among the fastest in advanced economies. A surprisingly weak consumption figure on Thursday would raise doubts about growth rebounding in the second quarter.

The focal point of the report however, will be inflation as measured by personal consumption expenditures (PCE) prices, as the Fed pays closer attention to the PCE price gauge than the alternative consumer price index. In March, the PCE price index hit 2% year-on-year for the first time since February 2017, while the core PCE price index, which excludes food and energy prices and is the Fed’s primary inflation targeting indicator, picked up to 1.9%. Core PCE is forecast to slip back slightly in April to 1.8% y/y.

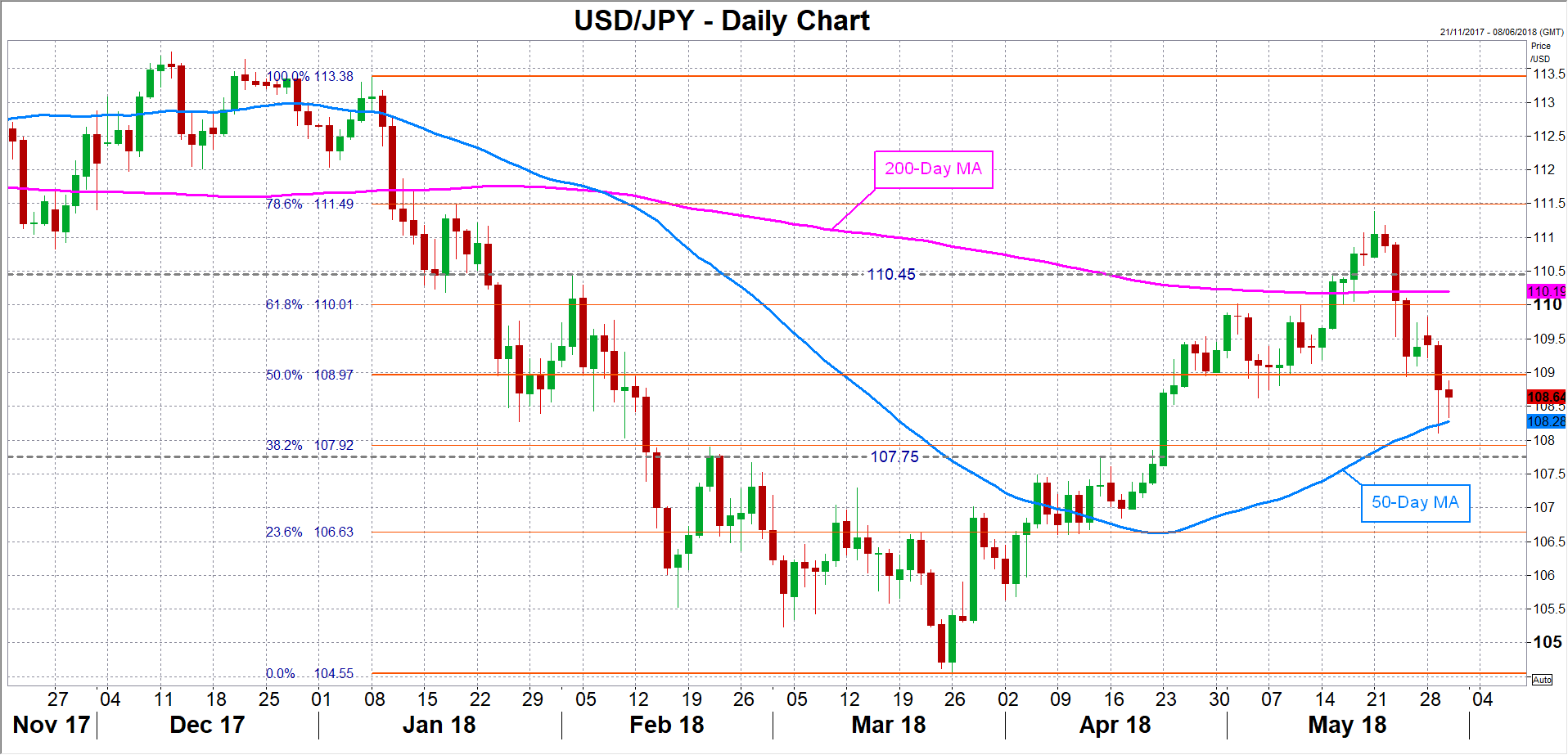

The index has remained below the Fed’s 2% objective since May 2012, but should there be an upside surprise and core PCE reaches the Fed’s target, dollar/yen could get a substantial lift after the sharp sell-off over the past week. The pair could jump above the 110 handle and above its 200-day moving average if the data suggested the Fed may need to raise rates three more times this year. Above the 110 level, there would likely be some resistance from the region around 110.45. A break above this area would clear the way for the 111 level. A bigger-than-expected increase in both personal consumption and core PCE would be the most bullish outcome for the dollar.

Should the data disappoint however, or broadly meet expectations, it would reinforce the view that the Fed will maintain its gradual rate hike path, and market sentiment will continue to be the main driver for dollar/yen in the short term, at least until Friday’s nonfarm payrolls report. The worst-case scenario would be a miss in the core PCE figure and/or a very poor personal spending number, which would exasperate dollar/yen’s recent losses. The pair could breach the tested support at the 50-day moving average, currently around 108.25, and open the way towards a key congestion area around 107.75.

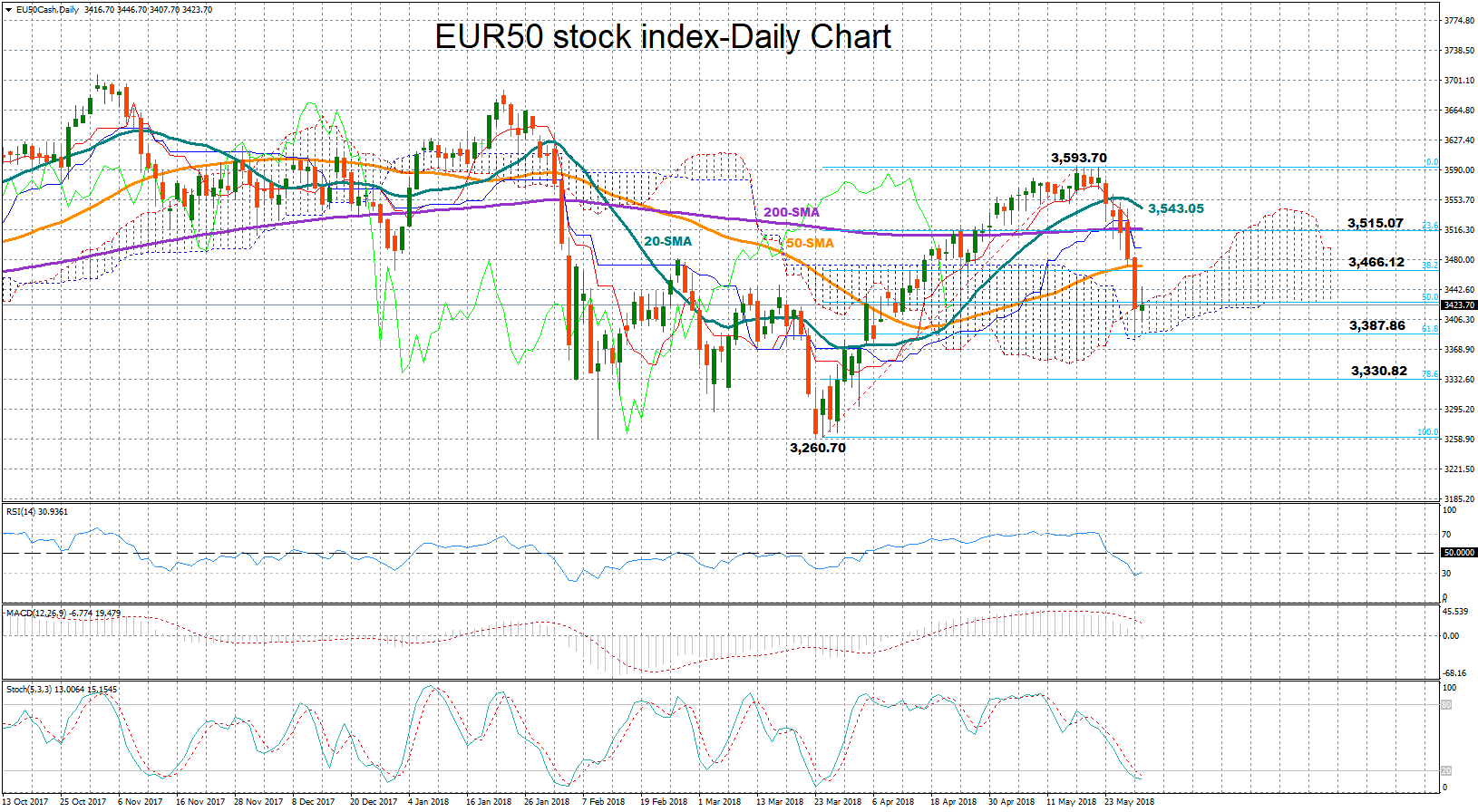

EUR50 Stock Index to Maintain Bearish Structure in Short-Term

The blue-chip Euro 50 stock index has been on the back foot over the past six days after spending a few days testing the 3 ½-month high of 3,593.70, reached first on May 17. At the moment there is not much evidence supporting that the downtrend could be nearing an end since the price is below its moving averages (SMA) which show no sign of reversing to the upside; the 20-day SMA is currently pointing to the downside, suggesting the sell-off could remain in place.

The MACD has deviated further below its red signal line and has just crossed below zero, hinting that negative momentum is likely to persist in the short-term. Yet upside corrections cannot be ruled out yet given that both Stochastics and the RSI are in the oversold zone. The former is ready to post a bullish cross below 20, while the latter is around 30 and set to rebound.

In case of a decline, the price could find support at the 61.8% Fibonacci of 3,387.86 of the upleg from 3,260.70 to 3,593.70, where the bottom of the Ichimoku cloud happens to be. A close below that level could reinforce the bearish case, sending the market lower to the 78.6% Fibonacci of 3,330.82 which has acted as support from February to March. Then, if price breaks even lower, the way could open towards the more-than-a-year low 3,260.70.

Alternatively, a rebound could face resistance at the 38.2% Fibonacci of 3,466.12, meeting the 50-day SMA in the same area, while a leg above from here could increase buying interest, opening the way towards the 23.6% Fibonacci and the 200-day SMA at 3,515.07. A break however above the 20-day SMA at 3,543.05 could increase confidence that the upleg from 3,260.70 could resume soon, turning the medium-term picture from neutral to bullish again.

Bank of Canada Throws “Caution” to the Wind

Highlights:

- The overnight rate has been unchanged at 1.25% since January’s 25 basis point hike.

- The BoC acknowledged Q1 GDP appears to have been firmer than expected, but they still see growth over the first half of the year tracking close to 2%.

- They noted positive signs in exports and business investment but continued weakness in home sales. A solid labour market backdrop is expected to support consumer spending and housing this year.

- The statement reinforced the bank’s data dependence, with particular focus on household sensitivity to rising rates as well as the evolution of excess capacity (the latter is an issue they pledged to look at more closely in their July MPR).

- Deputy Governor Sylvain Leduc will deliver an Economic Progress Report tomorrow that will elaborate on the BoC’s latest thinking.

Our Take:

The Bank of Canada is no fan of forward guidance but there were certainly some hawkish signals in today’s statement that increased our confidence in a July rate hike. While much of the press release was simply a mark-to-market of recent data—with a generally positive tone—changes to the final few sentences were notable. The Governing Council’s mantra has been that they would be “cautious” in future adjustments to monetary policy, but that key word was left out today in favour of a “gradual” approach to tightening. Their bias was also strengthened by noting “higher interest rates will be warranted” without adding “over time” as they have in the past. And surprisingly there was no mention of maintaining “some monetary policy accommodation” over the medium term.

There’s certainly risk of over-interpreting changes between policy statements given the BoC’s ‘blank page’ approach to these communications (a stark contrast with the Fed). So while the odds of the next rate hike coming in July have increased, we’ll also be looking for some of the following to reinforce our expectations:

- Early evidence of growth picking up in Q2—April’s national accounts are out June 29 and along with tomorrow’s March GDP will give a good idea of the economy’s momentum in the current quarter.

- A positive Business Outlook Survey suggesting investment and hiring plans aren’t being put on hold amid uncertainty over US trade policy and slow progress in Nafta talks.

- Some stabilization in home sales and household borrowing that would indicate consumers are taking rising rates and regulatory changes in stride.

- Further evidence of core inflation running around 2% and wages growing at 3%.

USDJPY: Loses Downside Momentum, Recovers

USDJPY: The pair saw price recovery on Wednesday on Tuesday as it looks to weaken further. On the downside, support lies at the 108.50 level where a break if seen will aim at the 108.00 level. A cut through here will turn focus to the 107.50 level and possibly lower towards the 107.00 level. On the upside, resistance resides at the 109.50 level. Further out, we envisage a possible move towards the 110.00 level. Further out, resistance resides at the 110.50 level with a turn above here aiming at the 111.00 level. On the whole, USDJPY faces further downside pressure.

Trade Wars, Geopolitical risks and Inflation Dominate Market Moves

Ongoing political worries about Italy and Spain have triggered big moves in stocks, a drop in the EUR and a massive shift in bond yields in the last week in May. The contagion risks from a potential Italian implosion should concern market participants once again.

The eurozone’s third-largest economy is currently in the midst of an ongoing power struggle, with investors fearful that the looming prospect of “snap” elections could be fought over the country’s role in the E.U and its membership of the single currency. An election would resemble a referendum on E.U membership

Investors have reasons to be worried

The economic fundamentals of Italy are disturbing. It is one of the biggest indebted countries in the world. It’s got an unemployment rate of +11% and its economy is still lower than where it was in 2007, whereas most major economies have recovered.

2017 was a stellar year for economic growth in Europe; we’ve seen a resumption of inflation so those deflationary fears went away. Nevertheless, everybody is now concerned about potential for deflation and even potential for ‘contagion.’

Rain in Spain

Meanwhile in Madrid, parliament is set to vote Friday (June 1) whether to oust Spanish Prime Minister Rajoy and replace his center-right government with one led by the center-left Socialist Party after a Spanish court ruled that Mr. Rajoy’s Popular Party financially benefited from an illegal kickback scheme.

Off again, on again

A senior N. Korean official will be in New York this week to discuss the upcoming summit, proof that the latest indication that an ‘on-again-off-again’ meeting between Trump and Kim Jong-Un may go ahead on June 12 in Singapore.

Trade meetings

President Trump also announced this week that the U.S would proceed with tariffs on +$50B in Chinese imports and introduce new limits on Chinese investment in U.S high-tech industries as part of a broad campaign to crack down on Chinese acquisition of U.S technology. Specifics of the new limits are expected to be announced by June 30 and will take effect shortly thereafter.

Commerce Secretary Wilbur Ross is due to arrive in Beijing June 2 for talks aimed at cooling trade tensions between the two countries.

Regarding Nafta, Canadian Foreign Affairs Minister Chrystia Freeland heads back to Washington (May 29) for a two-day visit as talks to modernize the Tri-lateral agreement hang in the balance.

Time is of the essence for Canada as the latest reprieve from potentially crippling U.S tariffs on imports of steel and aluminum expires June 1, and there are fears they could go into effect without a Nafta deal in place.

BoC: Poloz Holds, But Throws Caution to the Wind

The Bank of Canada held its key monetary policy interest rate at 1.25% this morning, as widely expected. The statement released with the decision had a hawkish tone, suggesting the next rate hike is not far off.

Economic developments since April are seen as in line with the Bank's view, albeit for the first half overall, given an expected Q1 outperformance. Housing activity is expected to improve as the year continues, helped by rising incomes. The Bank sees consumption continuing to play an important role, suggesting that household finances are not (in their estimation) particularly pinched by recent rate hikes.

Beyond our borders, some upside is seen for the U.S., but trade policy uncertainty remains a dampening factor. Emerging market stresses were also highlighted, while recent oil price moves were characterized as driven by geopolitical developments.

On the inflation front, there is little to get excited about. The Bank expects inflation to exceed its earlier forecasts due to gasoline prices, but reminded us that, as usual, they will look through this transitory factor.

All told, the positives seem to outweigh the negatives. Gone was the reference to "caution" that typified the last few statements. Today's statement instead chose the term "gradual" to describe the approach to policy adjustments. Importantly, interest rate sensitivity and the evolution of economic capacity remained areas of particular focus.

Key Implications

No surprise here. With the economy set to outperform the Bank's earlier expectations (Q1 GDP data is released tomorrow morning) and signs of life in all sectors bar housing, economic conditions favour another interest rate hike. While we may need a grammarian to distinguish between "cautious" and "gradual", the message was nevertheless clear: get ready for another rate hike.

Indeed, even more explicit than the adjective change was the dropping of the qualifier "over time" in regards to higher rates, and the only reference to labour markets was expectations for 'solid' income growth – gone are concerns about potential slack. This reinforces our view that as the economy continues to perform well into the middle of the year, the Bank will have the confidence it needs to raise its policy interest rate at its next scheduled decision, this July.

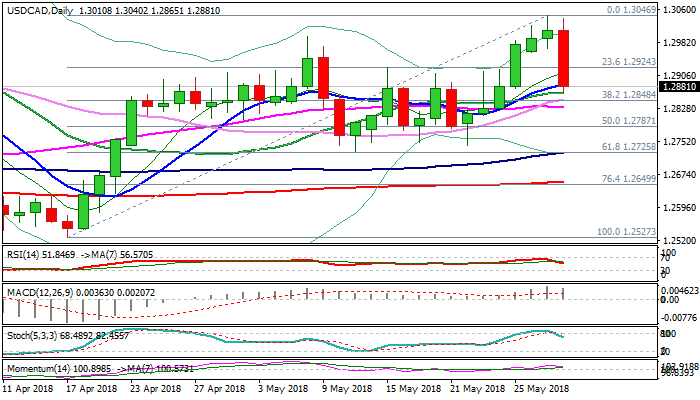

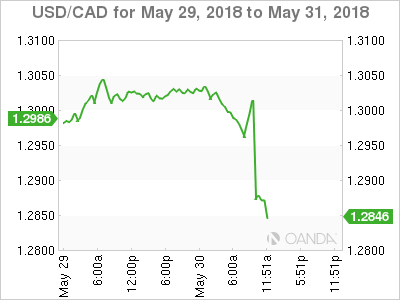

Canadian Dollar Surged on Hawkish BoC

The Canadian dollar surged against its US counterpart after Bank of Canada kept interest rates unchanged at 1.25% as expected, but changed rhetoric about future rate moves, which boosted the loonie. The central bank left rates unchanged but said that higher rates will be warranted to keep inflation near-target, however, gradual approach to policy adjustments will be guided by incoming data.

Hawkish tone from BoC boosted Canadian dollar which managed to recover over 50% of the most recent fall from 1.2742 to 1.3046.

The USD CAD pair dipped to session low at 1.2865, from daily high at 1.3040, which lays just under Monday’s nine-week high at 1.3046. Today’s strong fall signals reversal and failure on probes above psychological 1.30 barrier.

Fresh weakness returned to thick weekly cloud (cloud top lays at 1.2927) and cracked initial support at 1.2886 (rising 10SMA).

Further easing faces a cluster of supports provided by daily MA’s (20/30/55) within 1.2864/32 zone), break of which is needed to confirm reversal, as another pivotal support lays in the zone (Fibo 38.2% of 1.2527/1.3046 recovery rally at 1.2848).

Daily RSI and momentum turned south while slow stochastic reversed from overbought territory, showing a plenty of space downside, and support the notion.

Res: 1.2885; 1.2927; 1.2988; 1.3000

Sup: 1.2865; 1.2848; 1.2832; 1.2787